cost term & purpoese

TRANSCRIPT

CHAPTER 2AN INTRODUCTION TO COST TERMS AND PURPOSES

2-1 A cost object is anything for which a separate measurement of costs is desired. Examples include a product, a service, a project, a customer, a brand category, an activity, and a department.

2-2 Cost assignment is a general term that encompasses the assignment of both direct costs and indirect costs to a cost object. Direct costs are traced to a cost object while indirect costs are allocated to a cost object.

• Direct costs of a cost object are related to the particular cost object and can be traced to that cost object in an economically feasible (cost-effective) way.

• Indirect costs of a cost object are related to the particular cost object but cannot be traced to that cost object in an economically feasible (cost-effective) way.

2-3 Managers believe that costs that are traced to a particular cost object are more accurately assigned to that cost object than are allocated costs. When costs are allocated, managers are less certain whether the cost allocation base accurately measures the resources demanded by a cost object. Managers prefer to use more accurate costs in their decisions.

2.4 Factors affecting the classification of a cost as direct or indirect include:• the materiality of the cost in question,• available information-gathering technology,• design of operations, and• contractual arrangements.

2.5 Manufacturing-sector companies purchase materials and components and convert them into various finished goods.

Merchandising-sector companies purchase and then sell tangible products without changing their basic form.Service-sector companies provide services or intangible products to their customers, for example, legal advice or audits.

2.6 A cost driver is a variable, such as the level of activity or volume, that causally affects costs over a given time span. A change in the cost driver results in a change in the level of total costs. For example, number of vehicles assembled is a driver of the costs of steering wheels on a motor-vehicle assembly line.

2.7 A variable cost changes in total in proportion to changes in the related level of total activity or volume. An example is a sales commission that is a percentage of each sales revenue dollar.A fixed cost remains unchanged in total for a given time period, despite wide changes

in the related level of total activity or volume. An example is the leasing cost of a machine that is unchanged for a given time period (such as a year).

2 - 1

2.8 The relevant range is the band of normal activity level or volume in which there is a specific relationship between the level of activity or volume and the cost in question. Costs are described as variable or fixed with respect to a particular relevant range.

2-9 A unit cost is computed by dividing some amount of total costs (the numerator) by the related number of units (the denominator). In many cases, the numerator will include a fixed cost that will not change despite changes in the denominator. It is erroneous in those cases to multiply the unit cost by activity or volume change to predict changes in total costs at different activity or volume levels.

2.10 Manufacturing companies typically have one or more of the following three types of inventory.1. Direct materials inventory. Direct materials in stock and awaiting use in the

manufacturing process.2. Work-in-process inventory. Goods partially worked on but not yet fully

completed. Also called work in progress.3. Finished goods inventory. Goods fully completed but not yet sold.

2.11 Inventoriable costs are all costs of a product that are regarded as assets when they are incurred and then become cost of goods sold when the product is sold. These costs are included in work-in-process and finished goods inventory (they are "inventoried") to build up the costs of creating these assets.

Period costs are all costs in the income statement other than cost of goods sold. These costs are treated as expenses of the period in which they are incurred because they are presumed not to benefit future periods (or because there is not sufficient evidence to conclude that such benefit exists). Expensing these costs immediately best matches expenses to revenues.

2-12 No. Service sector companies have no inventories and, hence, no inventoriable costs.

2-13 Direct materials costs are the acquisition costs of all materials that eventually become part of the cost object (work in process and then finished goods), and that can be traced to the cost object in an economically feasible way.

Direct manufacturing labor costs include the compensation of all manufacturing labor that can be traced to the cost object.(work in process and then finished goods) in an economically feasible way.

Indirect manufacturing costs are all manufacturing costs that are related to the cost object (work in process and then finished goods), but that cannot be traced to that cost object in an economically feasible way.

Prime costs are all direct manufacturing costs (direct materials and direct manufacturing labor).

Conversion costs are all manufacturing costs other than direct material costs.

2-14 Overtime premium is the wage rate paid to workers (for both direct labor and indirect labor) in excess of their straight-time wage rates.

Idle time is a subclassification of indirect labor that typically represents wages paid for unproductive time caused by lack of orders, machine breakdowns, material shortages, poor scheduling, and the like.

2 - 2

2-15 A product cost is the sum of the costs assigned to a product for a specific purpose. Purposes for computing a product cost include:• Pricing and product mix decisions.• Contracting with government agencies.• Preparing financial statements for external reporting under generally accepted accounting

principles.

2-16 (15 min.) Computing and interpreting manufacturing unit costs.

1. (in Millions)Supreme Deluxe Regular

Direct materials costs $ 84.00 $ 54.00 $62.00Direct manuf. labor costs 14.00 28.00 8.00Indirect manuf. costs 42.00 84.00 24.00Total manuf. costs $140.00 $166.00 $94.00

Units produced (millions) 80 120 100Cost per unit (Total manuf.costs ÷ units produced)

$1.7500 $1.3833 $0.9400

2. The unit costs in requirement 1 includes $20 million of indirect manufacturing costs that are fixed irrespective of changes in the volume of output per month, while the remaining variable indirect manufacturing costs change with the production volume. Given the unit volume changes for August 2004, the use of unit costs from the past month at a different unit volume level (both in aggregate and at the individual product level) will yield incorrect estimates of total costs in August 2004.

2-17 (15 min.) Direct and indirect costs, effect of changing the classification of a cost item.

1. Direct costs are costs that are related to the particular paper products (Supreme, Deluxe, or Regular) and can be traced to each one in an economically feasible (cost-effective) way.

Indirect costs are costs that are related to the particular paper products (Supreme, Deluxe, or Regular) but cannot be traced to each one in an economically feasible (cost-effective) way.

2. Energy costs of $90 million can be traced to each individual production line. This tracing will result in a more accurate assignment of costs to products than when the $150 million of indirect manufacturing costs ($20 million of which is fixed) is allocated. Accurate product costing results in assignment of costs to different products in a manner than avoids under costing and over costing of the product lines.

2 - 3

2.17 (Cont’d.)

3. ( in Millions) Supreme Deluxe Regular Direct materials costs $ 84.0 $ 54.0 $62.0Direct manufacturing labor costs 14.0 28.0 8.0Direct energy costs 39.8 40.7 9.5Indirect manufacturing costs 16.8 33.6 9.6Total manufacturing costs $154.6 $156.3 $89.1

Units produced (millions) 80 120 100Cost per unit $1.9325 $ 1.3025 $0.8910

2-18 (15-20 min.) Classification of costs, service sector.

Cost object: Each individual focus groupCost variability: With respect to changes in the number of focus groups

There may be some debate over classifications of individual items. Debate is more likely as regards cost variability.

Cost Item D or I V or FA D VB I F

C I Va

D I FE D VF I FG D V

H I Vb

a Some students will note that phone call costs are variable when each call has a separate charge.

It may be a fixed cost if Consumer Focus has a flat monthly charge for a line, irrespective of the amount of usage.b Gasoline costs are likely to vary with the number of focus groups. However, vehicles likely

serve multiple purposes, and detailed records may be required to examine how costs vary with changes in one of the many purposes served.

2 - 4

2-19 (15-20 min.) Classification of costs, merchandising sector.Cost object: Video section of storeCost variability: With respect to changes in the number of videos sold

There may be some debate over classifications of individual items. Debate is more likely as regards cost variability.

Cost Item D or I V or FA D FB I FC D VD D FE I FF I VG I FH D V

2-20 (15-20 min.) Classification of costs, manufacturing sector.

Cost object: Type of car assembled (Corolla or Geo Prism)Cost variability: With respect to changes in the number of cars assembled

There may be some debate over classifications of individual items. Debate is more likely as regards cost variability.

Cost Item D or I V or FA D VB I FC D FD D FE D VF I VG D VH I F

2-21 (15-20 min.)Variable costs and fixed costs.

1. Variable cost per ton of beach sand mined:

Subcontractor $ 80 per tonGovernment tax 50 per ton Total $130 per ton

Fixed costs per month:

0 to 100 tons of capacity per day = $150,000101 to 200 tons of capacity per day = $300,000201 to 300 tons of capacity per day = $450,000

2 - 5

2.21 (Cont’d.)

2.

Tota

lFix

edC

osts

$450,000

$300,000

$150,000

100 200 300

Tons of Capacity per Day

$975,000

$650,000

$325,000

2,500 5,000 7,500

Tons Mined

Tota

lVar

iabl

eC

osts

The concept of relevant range is potentially relevant for both graphs. However, the question does not place restrictions on the unit variable costs. The relevant range for the total fixed costs is from 0 to 100 tons; 101 to 200 tons; 201 to 300 tons, and so on. Within these ranges, the total fixed costs do not change in total.

3.Tons Mined

per DayTons Mined per Month

Fixed Unit Cost per Ton

Variable Unit Cost per Ton

Total Unit Cost per Ton

(1) (2) = (1) × 25 (3) = FC ÷ (2) (4) (5) = (3) + (4)

(a) 180 4,500 $300,000 ÷ 4,500= $66.67 $130 $196.67

(b) 220 5,500 $450,000 ÷ 5,500=$81.82 $130 $211.82

The unit cost for 220 tons mined per day is $211.82, while for 180 tons it is only $196.67. This difference is caused by the fixed cost increment from 101 to 200 tons being spread over an increment of 80 tons, while the fixed cost increment from 201 to 300 tons is spread over an increment of only 20 tons.

2 - 6

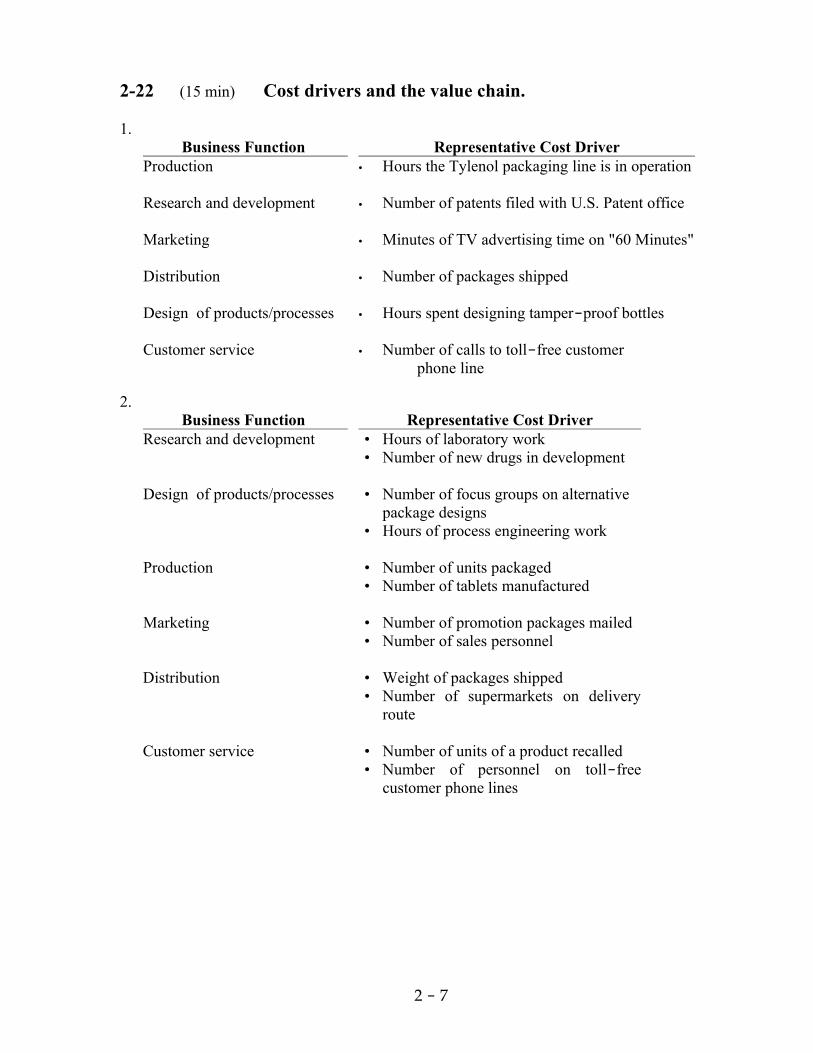

2-22 (15 min) Cost drivers and the value chain.

1.Business Function Representative Cost Driver

Production • Hours the Tylenol packaging line is in operation

Research and development • Number of patents filed with U.S. Patent office

Marketing • Minutes of TV advertising time on "60 Minutes"

Distribution • Number of packages shipped

Design of products/processes • Hours spent designing tamper-proof bottles

Customer service • Number of calls to toll-free customer phone line

2.Business Function Representative Cost Driver

Research and development • Hours of laboratory work• Number of new drugs in development

Design of products/processes • Number of focus groups on alternative package designs

• Hours of process engineering work

Production • Number of units packaged• Number of tablets manufactured

Marketing • Number of promotion packages mailed• Number of sales personnel

Distribution • Weight of packages shipped• Number of supermarkets on delivery

route

Customer service • Number of units of a product recalled• Number of personnel on toll-free

customer phone lines

2 - 7

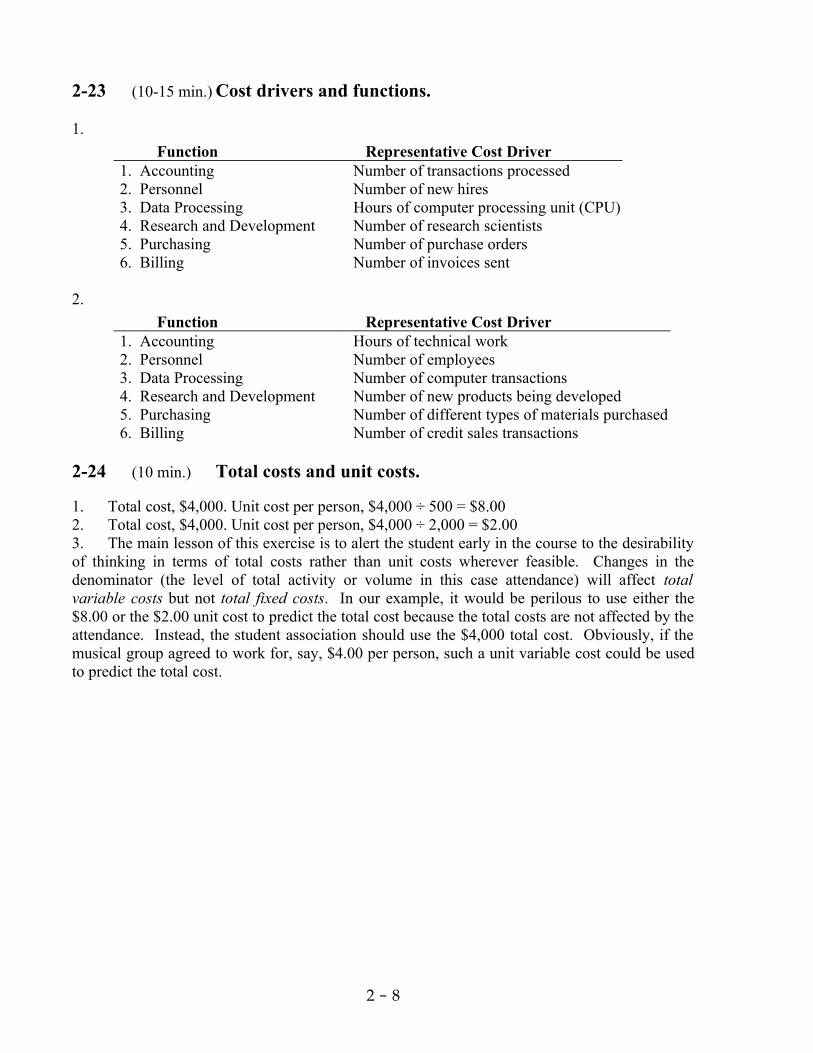

2-23 (10-15 min.) Cost drivers and functions.

1.

Function Representative Cost Driver1. Accounting Number of transactions processed2. Personnel Number of new hires3. Data Processing Hours of computer processing unit (CPU)4. Research and Development Number of research scientists5. Purchasing Number of purchase orders6. Billing Number of invoices sent

2.

Function Representative Cost Driver1. Accounting Hours of technical work2. Personnel Number of employees3. Data Processing Number of computer transactions4. Research and Development Number of new products being developed5. Purchasing Number of different types of materials purchased6. Billing Number of credit sales transactions

2-24 (10 min.) Total costs and unit costs.

1. Total cost, $4,000. Unit cost per person, $4,000 ÷ 500 = $8.002. Total cost, $4,000. Unit cost per person, $4,000 ÷ 2,000 = $2.003. The main lesson of this exercise is to alert the student early in the course to the desirability of thinking in terms of total costs rather than unit costs wherever feasible. Changes in the denominator (the level of total activity or volume in this case attendance) will affect total variable costs but not total fixed costs. In our example, it would be perilous to use either the $8.00 or the $2.00 unit cost to predict the total cost because the total costs are not affected by the attendance. Instead, the student association should use the $4,000 total cost. Obviously, if the musical group agreed to work for, say, $4.00 per person, such a unit variable cost could be used to predict the total cost.

2 - 8

2-25 (15 min.) Total costs and unit costs.

1. (a) $100,000 ÷ 2,000 = $50.00 per packageb (b) $100,000 ÷ 6,000 = $16.67 per packagec (c) $100,000 ÷ 10,000 = $10.00 per package

(d)[$100,000 + (10,000 × $8)] ÷ 20,000=$180,000 ÷ 20,000 = $9.00 per package

The unit cost to ECG decreases on a per-unit base due to the first $100,000 payment being a fixed cost. The $8 amount per package beyond 10,000 units is a variable cost. The cost function is:

2. ECG should not use any of the unit costs in requirement 1 when predicting total costs. Up to 10,000 units, the total cost is a fixed amount. Beyond 10,000 units, the total cost is a combination of a fixed amount plus a per-unit (beyond 10,000 unit) variable amount. The total costs at different volume levels cannot be predicted by using the unit cost at a specific volume level. The total cost should be predicted by combining the total fixed costs and total variable costs rather than multiplying a unit cost amount by the predicted number of packages sold.

2 - 9

Packages Sold

$180,000

$260,000

$100,000

$100,000

$200,000

$300,000

10,000 20,000 30,000

TotalCosts

2-26 (20-30 min.)Inventoriable costs versus period costs.

1. Manufacturing-sector companies purchase materials and components and convert them into different finished goods. Merchandising-sector companies purchase and then sell tangible products without changing their basic form.

Service-sector companies provide services or intangible products to their customers—for example, legal advice or audits.

Only manufacturing and merchandising companies have inventories of goods for sale.

2. Inventoriable costs are all costs of a product that are regarded as an asset when they are incurred and then become cost of goods sold when the product is sold. These costs for a manufacturing company are included in work-in-process and finished goods inventory (they are "inventoried") to build up the costs of creating these assets. Period costs are all costs in the income statement other than cost of goods sold. These costs are treated as expenses of the period in which they are incurred because they are presumed not to benefit future periods (or because there is not sufficient evidence to conclude that such benefit exists). Expensing these costs immediately best matches expenses to revenues.

3. (a) Mineral water purchased for resale by Safeway—inventoriable cost of a merchandising company. It becomes part of cost of goods sold when the mineral water is sold.

(b) Electricity used at GE assembly plant—inventoriable cost of a manufacturing company. It is part of the manufacturing overhead that is included in the manufacturing cost of a refrigerator finished good.

(c) Depreciation on AOL's computer equipment—period cost of a service company. AOL has no inventory of goods for sale and, hence, no inventoriable cost.

(d) Electricity for Safeway's store aisles—period cost of a merchandising company. It is a cost that benefits the current period and is not traceable to goods purchased for resale.

(e) Depreciation on GE's assembly testing equipment—inventoriable cost of a manufacturing company. It is part of the manufacturing overhead that is included in the manufacturing cost of a refrigerator finished good.

(f) Salaries of Safeway's marketing personnel—period cost of a merchandising company. It is a cost that is not traceable to goods purchased for resale. It is presumed not to benefit future periods (or at least not to have sufficiently reliable evidence to estimate such future benefits).

(g) Water consumed by AOL's engineers—period cost of a service company. AOL has no inventory of goods for sale and, hence, no inventoriable cost.

(h) Salaries of AOL's marketing personnel—period cost of a service company. AOL has no inventory of goods for sale and, hence, no inventoriable cost.

2 - 10

2-27 (20 min.) Computing cost of goods purchased and cost of goods sold.

(a) Marvin Department StoreSchedule of Cost of Goods Purchased

For the Year Ended December 31, 2004(in thousands)

Purchases $155,000Add transportation-in 7,000

162,000Deduct:Purchase return and allowances $4,000Purchase discounts 6,000 10,000Cost of goods purchased $152,000

(b) Marvin Department StoreSchedule of Cost of Goods Sold

For the Year Ended December 31, 2004(in thousands)

Beginning merchandise inventory 1/1/2004 $ 27,000Cost of goods purchased (above) 152,000Cost of goods available for sale 179,000Ending merchandise inventory 12/31/2004 34,000Cost of goods sold $145,000

2-28 (30-40 min.) Cost of goods manufactured.

1. Canseco CompanySchedule of Cost of Goods Manufactured for the Year Ended December 31, 2004

(in thousands)

Direct materials costs:Beginning inventory, Jan. 1, 2004 $22,000Purchases of direct materials 75,000Cost of direct materials available for use 97,000Ending inventory, Dec. 31, 2004 26,000

Direct materials used $ 71,000Direct manufacturing labor costs 25,000Indirect manufacturing costs:

Indirect manufacturing labor costs 15,000Plant insurance 9,000Depreciation––plant building and equipment 11,000Repairs and maintenance––plant 4,000 39,000

Manufacturing costs incurred during 2004 135,000Add beginning work-in-process inventory, Jan. 1, 2004 21,000Total manufacturing costs to account for 156,000Deduct ending work-in-process inventory, Dec. 31, 2004 20,000Cost of goods manufactured $136,000

2 - 11

2-28 (Cont’d.)2. Canseco Company

Income Statement for the Year Ended December 31, 2004(in thousands)

Revenues $300,000Cost of goods sold:

Beginning finished goods, Jan. 1, 2004 $ 18,000Cost of goods manufactured (requirement 1) 136,000Cost of goods available for sale 154,000Ending finished goods, Dec. 31, 2004 23,000 131,000

Gross margin 169,000Operating costs:

Marketing, distribution, and customer service 93,000General and administrative 29,000 122,000

Operating income $ 47,000

2-28 Excel ApplicationCanseco Company

Income Statement For the Year Ended December 31, 2004Revenues $300,000 Cost of goods sold: Beginning finished goods $18,000 Cost of goods manufactured 136,000 Cost of goods available for sale 154,000 Ending finished goods 23,000 131,000 Gross margin 169,000 Operating costs: Marketing, distribution, and customer service costs 93,000 General and administrative costs 29,000 122,000 Operating Income $47,000

Canseco CompanySchedule of Cost of Goods Manufactured For the Year Ended 2004

Direct Materials: Beginning direct materials inventory $ 22,000 Purchases of direct materials 75,000 Cost of direct materials available for use 97,000 Ending direct materials inventory 26,000 Direct materials used 71,000 Direct manufacturing labor 25,000Indirect manufacturing costs: Indirect manufacturing labor $15,000 Plant insurance 9,000 Depreciation 11,000 Repairs and Maintenance 4,000 39,000 Manufacturing costs incurred during 2004 135,000 Add beginning work in process 21,000 Total manufacturing costs to account for 156,000Deduct ending work in process 20,000Cost of goods manufactured $136,000

2 - 12

2-29 (25-30 min.) Income statement and schedule of cost of goods manufactured.

Howell CorporationIncome Statement for the Year Ended December 31, 2004

(in millions)

Revenues $950Cost of goods sold:

Beginning finished goods, Jan. 1, 2004 $ 70Cost of goods manufactured (below) 645Cost of goods available for sale 715

Ending finished goods, Dec. 31, 2004 55 660Gross margin 290Marketing, distribution, and customer-service costs 240Operating income $ 50

Howell CorporationSchedule of Cost of Goods Manufacturedfor the Year Ended December 31, 2004

(in millions)

Direct materials costs:Beginning inventory, Jan. 1, 2004 $ 15Purchases of direct materials 325Cost of direct materials available for use 340Ending inventory, Dec. 31, 2004 20

Direct materials used $320Direct manufacturing labor costs 100Indirect manufacturing costs:

Indirect manufacturing labor 60Plant supplies used 10Plant utilities 30Depreciation––plant, building, and equipment 80Plant supervisory salaries 5Miscellaneous plant overhead 35 220

Manufacturing costs incurred during 2004 640Add beginning work-in-process inventory, Jan. 1, 2004 10Total manufacturing costs to account for 650Deduct ending work-in-process, Dec. 31, 2004 5Cost of goods manufactured $645

2 - 13

2-30 (15-20 min.) Interpretation of statements (continuation of 2-29).

1. The schedule in 2-29 can become a Schedule of Cost of Goods Manufactured and Sold simply by including the beginning and ending finished goods inventory figures in the supporting schedule, rather than directly in the body of the income statement. Note that the term cost of goods manufactured refers to the cost of goods brought to completion (finished) during the accounting period, whether they were started before or during the current accounting period. Some of the manufacturing costs incurred are held back as costs of the ending work in process; similarly, the costs of the beginning work in process inventory become a part of the cost of goods manufactured for 2004.

2. The sales manager’s salary would be charged as a marketing cost as incurred by both manufacturing and merchandising companies. It is basically an operating cost that appears below the gross margin line on an income statement. In contrast, an assembler’s wages would be assigned to the products worked on. Thus, the wages cost would be charged to Work in process and would not be expensed until the product is transferred through Finished Goods Inventory to Cost of Goods Sold as the product is sold.

3. The direct-indirect distinction can be resolved only with respect to a particular cost object. For example, in defense contracting, the cost object may be defined as a contract. Then, a plant supervisor working only on that contract will have his or her salary charged directly and wholly to that single contract.

4. Direct materials used = $320,000,000 ÷ 1,000,000 units = $320 per unitDepreciation = $ 80,000,000 ÷ 1,000,000 units = $ 80 per unit

5. Direct materials unit cost would be unchanged at $320. Depreciation cost per unit would be $80,000,000 ÷ 1,200,000 = $66.67 per unit. Total direct materials costs would rise by 20% to $384,000,000 ($320 per unit × 1,200,000 units), whereas total depreciation would be unaffected at $80,000,000.

6. Unit costs are averages, and they must be interpreted with caution. The $320 direct materials unit cost is valid for predicting total costs because direct materials is a variable cost; total direct materials costs indeed change as output levels change. However, fixed costs like depreciation must be interpreted quite differently from variable costs. A common error in cost analysis is to regard all unit costs as one—as if all the total costs to which they are related are variable costs. Changes in output levels (the denominator) will affect total variable costs, but not total fixed costs. Graphs of the two costs may clarify this point; it is safer to think in terms of total costs rather than in terms of unit costs.

2 - 14

2-31 (25-30 min.) Income statement and schedule of cost of goods manufactured.

Chan CorporationIncome Statement

for the Year Ended December 31, 2004(in millions)

Revenues $350Cost of goods sold:

Beginning finished goods, Jan. 1, 2004 $ 40Cost of goods manufactured (below) 204Cost of goods available for sale 244Ending finished goods, Dec. 31, 2004 12 232

Gross margin 118Marketing, distribution, and customer-service costs 90Operating income $ 28

Chan CorporationSchedule of Cost of Goods Manufacturedfor the Year Ended December 31, 2004

(in millions)

Direct material costs:Beginning inventory, Jan. 1, 2004 $ 30Direct materials purchased 80Cost of direct materials available for use 110Ending inventory, Dec. 31, 2004 5

Direct materials used $105Direct manufacturing labor costs 40Indirect manufacturing costs:

Plant supplies used 6Property taxes on plant 1Plant utilities 5Indirect manufacturing labor costs 20Depreciation––plant, building, and equipment 9Miscellaneous manufacturing overhead costs 10 51

Manufacturing costs incurred during 2004 196Add beginning work-in-process inventory, Jan. 1, 2004 10Total manufacturing costs to account for 206Deduct ending work-in-process inventory, Dec. 31, 2004 2Cost of goods manufactured (to income statement) $204

2 - 15

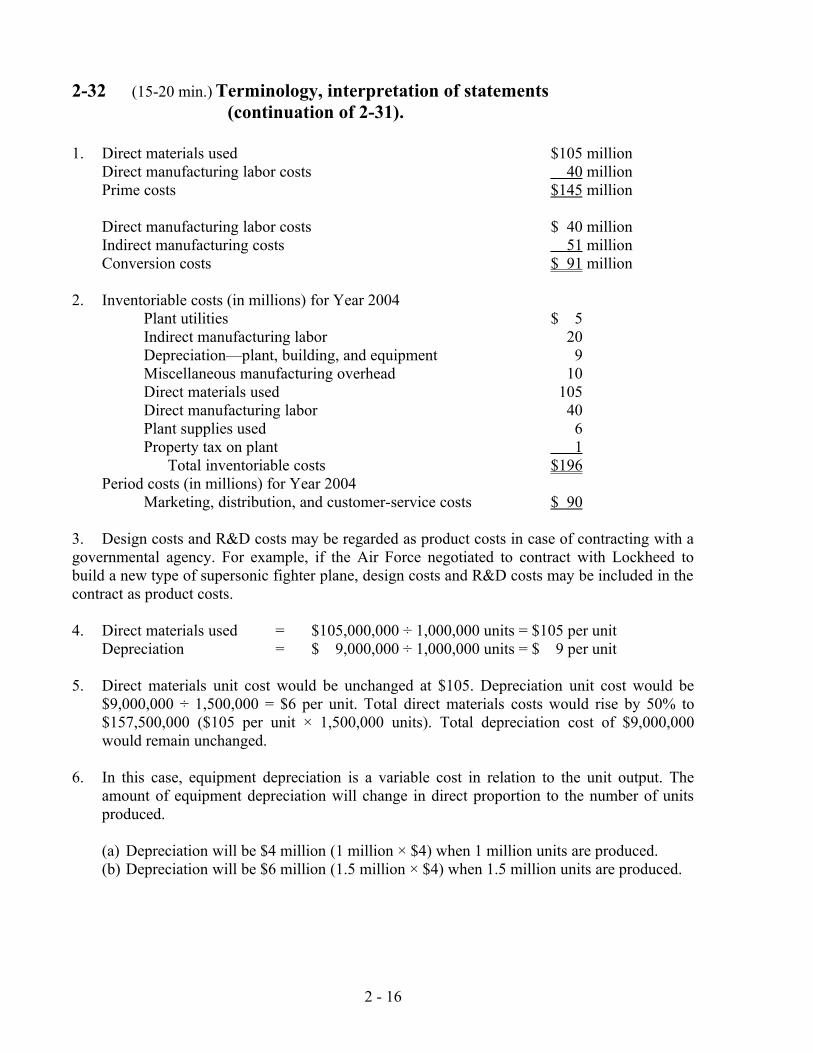

2-32 (15-20 min.) Terminology, interpretation of statements (continuation of 2-31).

1. Direct materials used $105 millionDirect manufacturing labor costs 40 millionPrime costs $145 million

Direct manufacturing labor costs $ 40 millionIndirect manufacturing costs 51 millionConversion costs $ 91 million

2. Inventoriable costs (in millions) for Year 2004Plant utilities $ 5Indirect manufacturing labor 20Depreciation—plant, building, and equipment 9Miscellaneous manufacturing overhead 10Direct materials used 105Direct manufacturing labor 40Plant supplies used 6Property tax on plant 1

Total inventoriable costs $196Period costs (in millions) for Year 2004

Marketing, distribution, and customer-service costs $ 90

3. Design costs and R&D costs may be regarded as product costs in case of contracting with a governmental agency. For example, if the Air Force negotiated to contract with Lockheed to build a new type of supersonic fighter plane, design costs and R&D costs may be included in the contract as product costs.

4. Direct materials used = $105,000,000 ÷ 1,000,000 units = $105 per unitDepreciation = $ 9,000,000 ÷ 1,000,000 units = $ 9 per unit

5. Direct materials unit cost would be unchanged at $105. Depreciation unit cost would be $9,000,000 ÷ 1,500,000 = $6 per unit. Total direct materials costs would rise by 50% to $157,500,000 ($105 per unit × 1,500,000 units). Total depreciation cost of $9,000,000 would remain unchanged.

6. In this case, equipment depreciation is a variable cost in relation to the unit output. The amount of equipment depreciation will change in direct proportion to the number of units produced.

(a) Depreciation will be $4 million (1 million × $4) when 1 million units are produced. (b) Depreciation will be $6 million (1.5 million × $4) when 1.5 million units are produced.

2 - 16

2-33 ( 20-25 min.) Overtime premium.

1.Westec BBC

Revenues $420 $480Direct materials 250 270Direct manuf. labor 40 40Overtime premium - 20Indirect manufacturing 80 80

Total manuf. costs 370 410Gross margin $50 $ 70Gross margin percentage 11.9% 14.6%

2.Westec BBC

Revenues $420 $480Direct materials 250 270Direct manuf. labor 40 40Overtime premium 20 -Indirect manufacturing 80 80

Total manuf. costs 390 390Gross margin $30 $ 90Gross margin percentage 7.1% 18.8%

3.Westec BBC

Revenues $420 $480Direct materials 250 270Direct manuf. labor 40 40Overtime premium 10 10Indirect manufacturing 80 80

Total manuf. costs 380 400Gross margin $40 $ 80Gross margin percentage 9.5% 16.7%

2 - 17

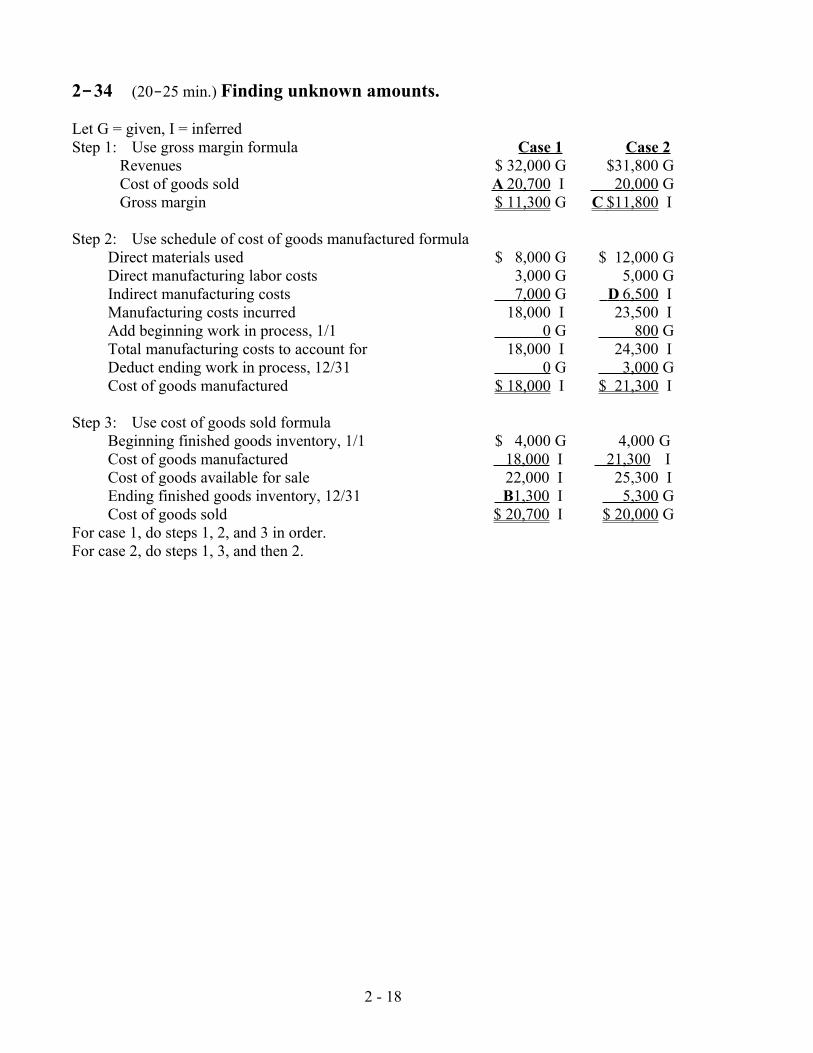

2-34 (20-25 min.) Finding unknown amounts.

Let G = given, I = inferredStep 1: Use gross margin formula Case 1 Case 2

Revenues $ 32,000 G $31,800 GCost of goods sold A 20,700 I 20,000 GGross margin $ 11,300 G C $11,800 I

Step 2: Use schedule of cost of goods manufactured formulaDirect materials used $ 8,000 G $ 12,000 GDirect manufacturing labor costs 3,000 G 5,000 GIndirect manufacturing costs 7,000 G D 6,500 IManufacturing costs incurred 18,000 I 23,500 IAdd beginning work in process, 1/1 0 G 800 GTotal manufacturing costs to account for 18,000 I 24,300 IDeduct ending work in process, 12/31 0 G 3,000 GCost of goods manufactured $ 18,000 I $ 21,300 I

Step 3: Use cost of goods sold formulaBeginning finished goods inventory, 1/1 $ 4,000 G 4,000 GCost of goods manufactured 18,000 I 21,300 ICost of goods available for sale 22,000 I 25,300 IEnding finished goods inventory, 12/31 B 1,300 I 5,300 GCost of goods sold $ 20,700 I $ 20,000 G

For case 1, do steps 1, 2, and 3 in order.For case 2, do steps 1, 3, and then 2.

2 - 18

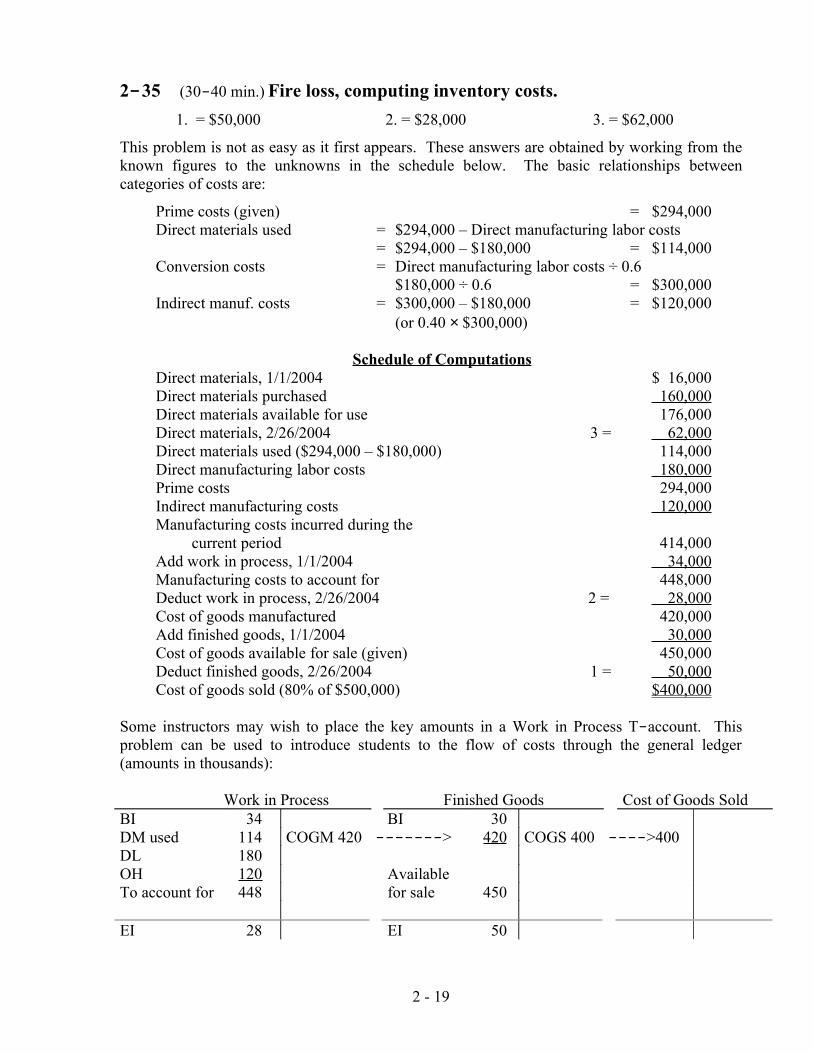

2-35 (30-40 min.) Fire loss, computing inventory costs.

1. = $50,000 2. = $28,000 3. = $62,000

This problem is not as easy as it first appears. These answers are obtained by working from the known figures to the unknowns in the schedule below. The basic relationships between categories of costs are:

Prime costs (given) = $294,000Direct materials used = $294,000 – Direct manufacturing labor costs

= $294,000 – $180,000 = $114,000Conversion costs = Direct manufacturing labor costs ÷ 0.6

$180,000 ÷ 0.6 = $300,000Indirect manuf. costs = $300,000 – $180,000 = $120,000

(or 0.40 × $300,000)

Schedule of ComputationsDirect materials, 1/1/2004 $ 16,000Direct materials purchased 160,000Direct materials available for use 176,000Direct materials, 2/26/2004 3 = 62,000Direct materials used ($294,000 – $180,000) 114,000Direct manufacturing labor costs 180,000Prime costs 294,000Indirect manufacturing costs 120,000Manufacturing costs incurred during the

current period 414,000Add work in process, 1/1/2004 34,000Manufacturing costs to account for 448,000Deduct work in process, 2/26/2004 2 = 28,000Cost of goods manufactured 420,000Add finished goods, 1/1/2004 30,000Cost of goods available for sale (given) 450,000Deduct finished goods, 2/26/2004 1 = 50,000Cost of goods sold (80% of $500,000) $400,000

Some instructors may wish to place the key amounts in a Work in Process T-account. This problem can be used to introduce students to the flow of costs through the general ledger (amounts in thousands):

Work in Process Finished Goods Cost of Goods SoldBI 34 BI 30DM used 114 COGM 420 -------> 420 COGS 400 ---->400DL 180OH 120 AvailableTo account for 448 for sale 450

EI 28 EI 50

2 - 19

2-36 (30 min.) Comprehensive problem on unit costs, product costs.

1. If 2 pounds of direct materials are used to make each unit of finished product, 100,000 units × 2 lbs., or 200,000 lbs. were used at $0.70 per pound of direct materials ($140,000 ÷ 200,000 lbs.). (The direct material costs of $140,000 are direct materials used, not purchased.) Therefore, the ending inventory of direct materials is 2,000 lbs. × $0.70 = $1,400.

2. Manufacturing Costs for 100,000 unitsVariable Fixed Total

Direct materials costs $140,000 $ – $140,000Direct manufacturing labor costs 30,000 – 30,000Plant energy costs 5,000 – 5,000Indirect manufacturing labor costs 10,000 16,000 26,000Other indirect manufacturing costs 8,000 24,000 32,000Cost of goods manufactured $193,000 $40,000 $233,000Average unit manufacturing cost: $233,000 ÷ 100,000 units

= $2.33 per unit

Finished goods inventory in units: =

$20,970 (given)$2.33 per unit

= 9,000 units

3. Units sold in 2004 = Beginning inventory + Production – Ending inventory = 0 + 100,000 – 9,000 = 91,000 units

Selling price per unit in 2004 = $436,800 ÷ 91,000 = $4.80 per unit

4.Revenues (91,000 units sold × $4.80) $436,800Cost of units sold:

Beginning finished goods, Jan. 1, 2004 $ 0Cost of goods manufactured 233,000Cost of goods available for sale 233,000Ending finished goods, Dec. 31, 2004 20,970 212,030

Gross margin 224,770Operating costs:

Marketing, distribution, and customer-service costs 162,850Administrative costs 50,000 212,850

Operating income $ 11,920

Note: Although not required, the full set of unit variable costs is:Direct materials costs $1.40Direct manufacturing labor costs 0.30Plant energy costs 0.05 Per unit manufacturedIndirect manufacturing labor costs 0.10Other indirect manufacturing costs 0.08

Marketing, distribution, and customer-service costs $1.35 Per unit sold

2 - 20

2-37 (25 min.) Product costs, effect of changing the cost classification (continuation of 2-36).

1. Variable manufacturingcosts for 100,000 units

Direct material costs $140,000Direct manufacturing labor costs 30,000Plant energy costs 5,000Indirect manufacturing labor costs 10,000Other indirect manufacturing costs 8,000Variable cost of goods manufactured $193,000

Average unit manufacturing cost $193,000 = $1.93 per unit 100,000 units

Finished goods inventory cost: 9,000 units × $1.93 = $17,370

2. Revenues (91,000 units × $4.80) $436,800Cost of units sold:

Beginning finished goods, 1/1/2004 $ 0Variable cost of goods manufactured 193,000Cost of goods available for sale 193,000Ending finished goods, 12/31/2004 17,370 175,630

Gross margin 261,170Operating costs:

Marketing, distribution, and customer-service costs 162,850Administrative costs 50,000Indirect manufacturing labor costs 16,000Other indirect manufacturing costs 24,000 252,850

Operating income $ 8,320

2-38 (30 min.) Cost analysis, litigation risk, ethics.

1. Reasons for Savage not wanting Nash to include the potential litigation costs include:(a) Genuine belief that the product has no risk of future litigation. Note that she asserts

“she has total confidence in her medical research team.”(b) Concern that the uncertainties about litigation are sufficiently high to make any

numerical estimate “meaningless.”(c) Concern that inclusion of future litigation costs would cause the board of directors to

vote against the project. Savage may be “overly committed” to the project and wants to avoid showing information that prompts questions she prefers not to be raised.

(d) Avoid “smoking gun” memos being included in the project evaluation file. Savage may believe that if subsequent litigation occurs, the plaintiffs will “inappropriately” use a litigation cost line item as “proof” FY “knew the product had health problems” that were known to management at the outset.

2 - 21

2-38 (Cont’d.)

2. Unit costs excluding litigation costs $100Add unit litigation costs 110Total unit costs 210Add 20% markup 42Selling price per unit $252

Since each treatment is planned to cost patients $300, the new selling price of $252 will drop the doctors’ margin to only $48 from the planned margin of $180 based on the planned selling price of $120. This would probably result in the doctors not having much incentive to promote the product. In fact, it may be quite possible that the doctors may not attempt to prescribe the treatment at such low margin because of their own exposure to liability.

3. Nash has already registered his concern to Savage. The difficulty is that Savage asked Nash to not include the possible litigation in his presentation. If there is no record of this presentation, then Nash may have several concerns.

(a) He may be accused at a later stage of not anticipating the costs of litigation. If litigation does occur, some people will try to distance themselves from the problems. It may be to Nash’s advantage to have a record of his early concerns. (Although plaintiffs may make Nash’s life very difficult if they get access to Nash’s files.) Nash may want to keep some record of his presentation to Savage.

(b) He may be portrayed as not being a “team player” if he continues his objections. Savage may have to silence his concerns if he decides to stay at FY.

(c) He may have difficult ethical objections with Savage’s behavior. If he thinks she is acting unethically, his main options are to speak to her first (at least one time), speak to her supervisor (probably chairman of the company), or, as a final resort, resign.

2 - 22

2-39 (30 min.) Missing data. (in millions)

1. Direct materials inventory, 8/1/2004 90Direct materials purchased 360Direct materials available 450Deduct direct materials used 375Direct materials inventory, 8/31/2004 $ 75

2. Total manufacturing overhead costs $ 480Variable manufacturing overhead costs 250Fixed manufacturing overhead costs $ 230

3. Total manufacturing costs $1,600Deduct:

Direct materials used $375Manufacturing overhead 480 855

Direct manufacturing labor costs $ 745

4. Work-in-Process inventory, 8/1/2004 $ 200Total manufacturing costs 1,600

1,800Deduct cost of goods manufactured 1,650Work-in-Process inventory 8/31/2004 $ 150

5. Finished goods inventory 8/1/2004 $ 125Cost of goods manufactured 1,650Goods available for sale $1,775

6. Goods available for sale $1,775Deduct cost of goods sold 1,700Finished goods inventory, 8/31/2004 $ 75

2 - 23

Chapter 2 Internet Exercise

The Internet exercise is available to students only on the Prentice Hall Companion Website www.prenhall.com/horngren. Students can click on Cost Accounting, 11th ed., and access the Internet Exercise for the chapter, which links to the Web site of a company or organization. The Internet Exercise on the Web will be updated periodically so that it is current with the latest information available on the subject organization's Web site. A printout copy of the Internet exercise for this chapter as of early 2002 appears below.

The solution to the Internet exercise, which will also be updated periodically, is available to instructors from the Companion Website's faculty view. To access the solution, click on Cost Accounting, 11th ed., Faculty link, and then register once to obtain your password through the online form. After the initial registration, you will have a personal login ID and password to use to log in. A printout of the solution to the Internet exercise for this chapter as of early 2002 follows. The exercise and solution provide instructors with an idea of the content of the Internet exercise for this chapter.

Internet Exercise

Gibson is a manufacturer of high-quality guitars and accessories. From its Web site, http://www.gibson.com, you can access information on the company, its products, job listings, and artists, and you can take a virtual tour of Gibson's manufacturing process. To take the virtual tour from the Gibson homepage, click on "Products" and then the "Acoustic Guitars" link, or go to: http://montana.gibson.com/tour/tour1a.html.1. Identify direct materials used in manufacturing a guitar.2. Give some examples of indirect materials used in manufacturing a guitar.3. Manufacturing guitars involves a great deal of direct manufacturing labor. Identify tasks

that involve direct manufacturing labor.4. What kind of employees might be considered indirect manufacturing labor?5. Identify some different types of manufacturing overhead in a guitar factory.6. What kinds of accounts would Gibson use to track the flow of costs through the production

process? 7a. What are inventoriable costs? b. Provide some examples of inventoriable costs at Gibson. 8a. What are period costs? b. Provide some examples of period costs at Gibson.9a. What do you think is Gibson's largest fixed cost? b. What do you think is Gibson's largest variable cost?

Solution to Internet Exercise

1. The primary direct material is wood. Maple and mahogany are used for necks, ribs (sides) and backs; spruce for all tops; rosewood for ribs, backs, fingerboards and bridges; ebony for fingerboards and bridges. Other direct materials included strings and tuners.

2. Indirect materials include glue, wood fillers, lacquers, sanding blocks, and small tools.

2 - 24

Internet Exercise (Cont’d.)

3. Tasks for direct manufacturing labor include:• Selecting wood• Building the body: cutting the sound hole, pressing ribs, gluing head blocks,

bracing, and kerfing• Building the neck: installing the fingerboard, in-lays, the head, and tuners• Fitting the neck to the body• Filling, spraying, and applying lacquer• Bridging and set-up

4. Indirect manufacturing labor includes: shop supervisors, material handlers, production managers, and factory supervisors.

5. Different types of manufacturing overhead include: rent or depreciation on the building, depreciation on the equipment, utilities, indirect materials and indirect manufacturing labor.

6. To track the flow of costs through the production process, Gibson would use direct materials inventory, work-in-process inventory, and finished goods inventory.

7a. Inventoriable costs include direct and indirect manufacturing costs.

7b. Inventoriable costs include all of the costs identified in questions 1, 2, 4, and 5.

8a. Period costs are all costs on the income statement excluding cost of goods sold. Period costs are presumed to benefit the current period and not to benefit future periods. Hence, period costs are expensed in the current period to match revenues of the current period.

8b. For Gibson period costs would include all nonmanufacturing costs. Examples include R&D costs, design costs, marketing costs, distribution costs, accounting and administrative costs, interest and taxes.

9a. Gibson's largest fixed cost is most likely depreciation on plant and equipment.

9b. Guitar manufacturing is labor intensive. Gibson's largest variable cost is most likely direct labor (wages).

2 - 25

Chapter 2 Video Case

The video case can be discussed using only the case writeup in the chapter. Alternatively, instructors can have students view the videotape of the company that is the subject of the case. The videotape can be obtained by contacting your Prentice Hall representative. The case questions challenge students to apply the concepts learned in the chapter to a specific business situation.

THREE DOG BAKERY: COST TERMINOLOGY

1. Various cost objects for Three Dog Bakery are:Product: Dog biscuits and treats (125 different kinds)Service: Telephone orders for dogalog salesProject: Investigation of new store locationsCustomer: PetsMart, the national pet store chainActivity: Development and updating of the e-commerce Web siteDepartment: Finance, Marketing, Sales, Production, Shipping, Receiving, and so on.

2. Cost Item D or I F or V a. Salary of the production department manager who

oversees manufacturing D Fb. Salaries of founders Dan Dye and Mark Beckloff I Fc. Cardboard trays used to package sets of twelve specialty D V

biscuitsd. Salary of the graphic designer who prepares the Dogalog Neither*

illustrations and layoute. Annual maintenance service agreement for the

shrink-wrap D Fmachine

f. Wages paid to assembly line workers who mix D VSnickerpoodle ingredients in batches

g. Air conditioning costs for the entire baking commissary D Fh. Cost of flour, eggs, and carob icing for Rollover biscuits D V*Design costs are not related to production and hence are neither direct nor indirect costs of production.

3. Period cost. The costs of preparing and mailing the Dogalog are expensed in the period in which the costs are incurred. This is a reasonable application of the matching principle. These are selling costs. They are not traceable to individual products held in inventory. One could argue that customers hold onto their Dogalogs for ordering products in future periods, thereby yielding some future benefit to Three Dog Bakery, but because most orders come in the weeks following delivery of the print matter, it’s appropriate to classify these costs as period costs.

2 - 26

Video Case (Cont’d.)

4. Three Dog Bakery is a manufacturing company but it is engaged in all three sectors: manufacturing, merchandising, and service. With respect to manufacturing, they produce baked dog biscuits and treats at their central baking commissary. They purchase raw ingredients and convert them into finished goods on their assembly line. They also make special occasions items in each store.

With respect to merchandising, the company operates retail stores. These stores not only sell their baked dog treats, they also sell ready-to-sell merchandise from other manufacturers (dog bowls, hats, leashes, collars, etc.). They also have a mail order business where they sell their products direct to the consumer. They also sell their products to other retailers such as Pets Mart.

With respect to service, Three Dog Bakery hosts an e-commerce Web Site that provides customers a chance to not only order products, but send inquiries to the company and gather information about the company’s operations, locations, and promotions. Some stores host birthday parties and happy hours for socialization.

2 - 27