corporate taxation and fdi within the eu25 amina lahrèche-révil cepii 2nd euroframe conference on...

TRANSCRIPT

Corporate taxation and FDI within the EU25

Amina Lahrèche-RévilCEPII

2nd EUROFRAME Conference on Economic Policy Issues in the European Union

Vienna, Friday 3 June 2005

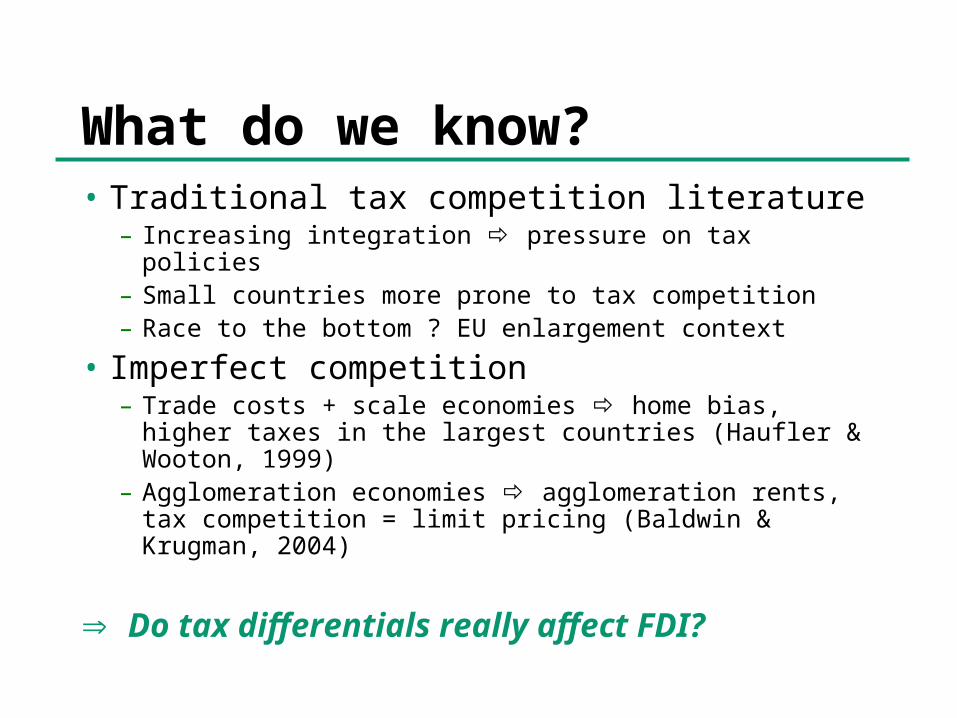

What do we know?• Traditional tax competition literature

– Increasing integration pressure on tax policies– Small countries more prone to tax competition– Race to the bottom ? EU enlargement context

• Imperfect competition– Trade costs + scale economies home bias, higher

taxes in the largest countries (Haufler & Wooton, 1999)

– Agglomeration economies agglomeration rents, tax competition = limit pricing (Baldwin & Krugman, 2004)

Do tax differentials really affect FDI?

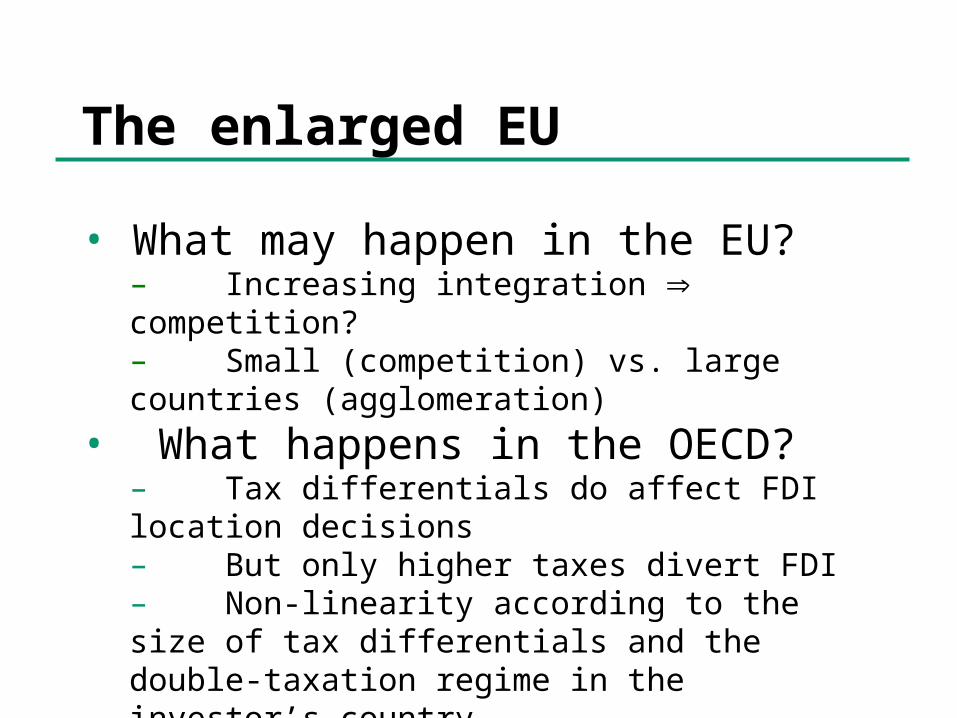

The enlarged EU

• What may happen in the EU?– Increasing integration competition?– Small (competition) vs. large countries (agglomeration)

• What happens in the OECD?– Tax differentials do affect FDI location decisions– But only higher taxes divert FDI– Non-linearity according to the size of tax differentials and the double-taxation regime in the investor’s country.– Competition from third countries

Outline

Stylized factsEconometric methodologyResultsConclusion

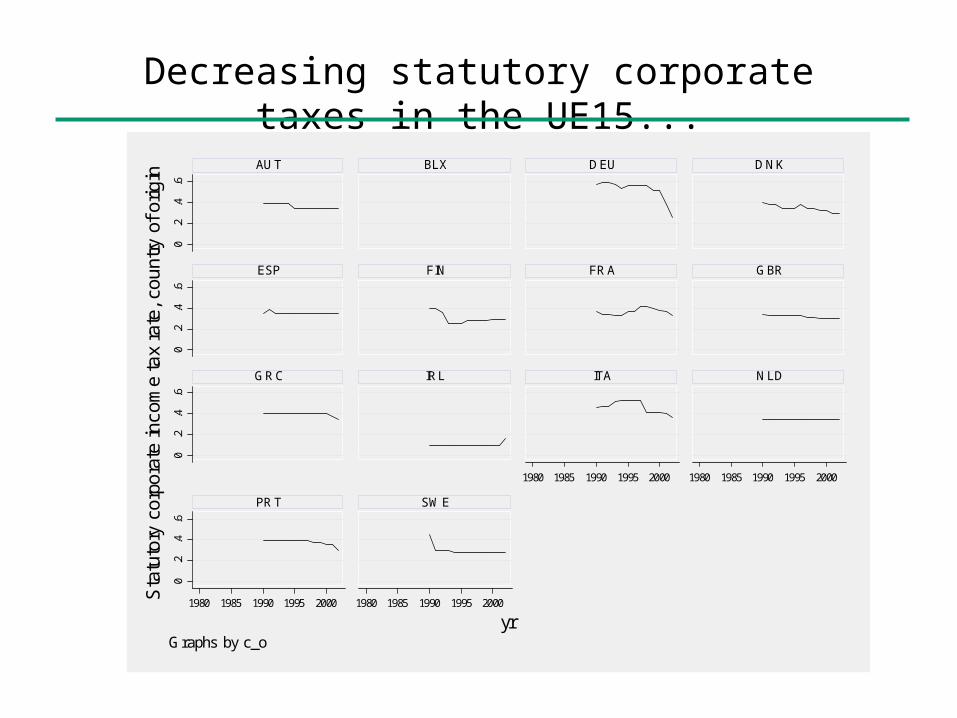

Decreasing statutory corporate taxes in the UE15...

0.2

.4.6

0.2

.4.6

0.2

.4.6

0.2

.4.6

1980 1985 1990 1995 2000 1980 1985 1990 1995 2000

1980 1985 1990 1995 2000 1980 1985 1990 1995 2000

AUT BLX DEU DNK

ESP FIN FRA GBR

GRC IRL ITA NLD

PRT SWE

Sta

tuto

ry c

orpo

rate

inco

me

tax

rate

, cou

ntry

of o

rigin

yrGraphs by c_o

… and in the NEM

.2.3

.4.5

.2.3

.4.5

.2.3

.4.5

1980 1985 1990 1995 2000

1980 1985 1990 1995 2000 1980 1985 1990 1995 2000

CZE EST HUN

LTU LVA POL

SVK SVN

Sta

tuto

ry c

orpo

rate

inco

me

tax

rate

, cou

ntry

of o

rigin

yrGraphs by c_o

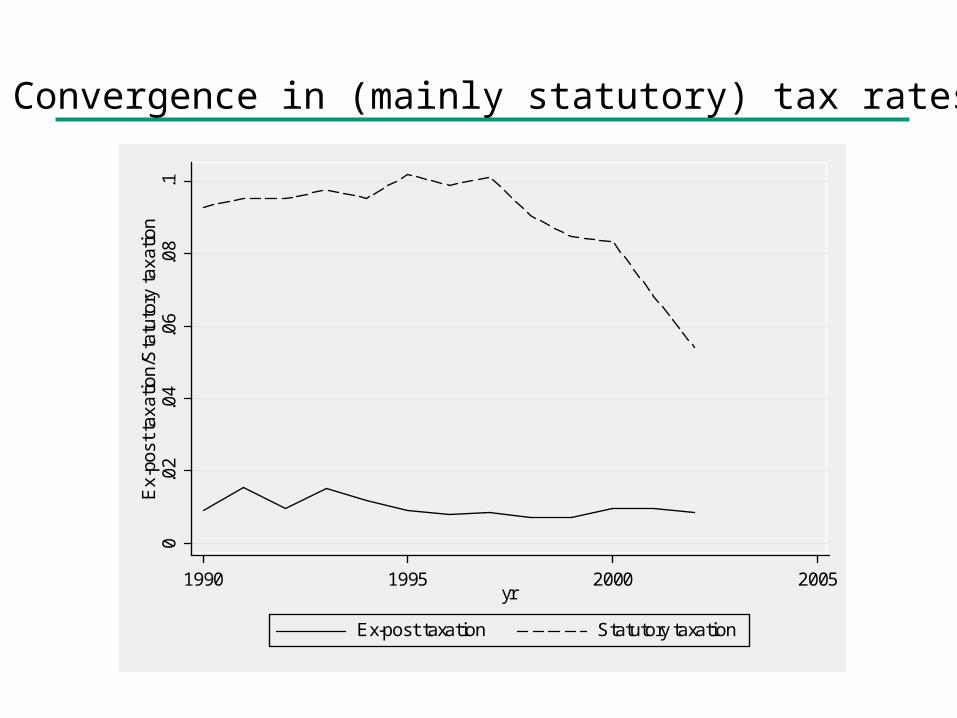

Convergence in (mainly statutory) tax rates

0.0

2.0

4.0

6.0

8.1

Ex-

post

taxa

tion/

Sta

tuto

ry ta

xatio

n

1990 1995 2000 2005yr

Ex-post taxation Statutory taxation

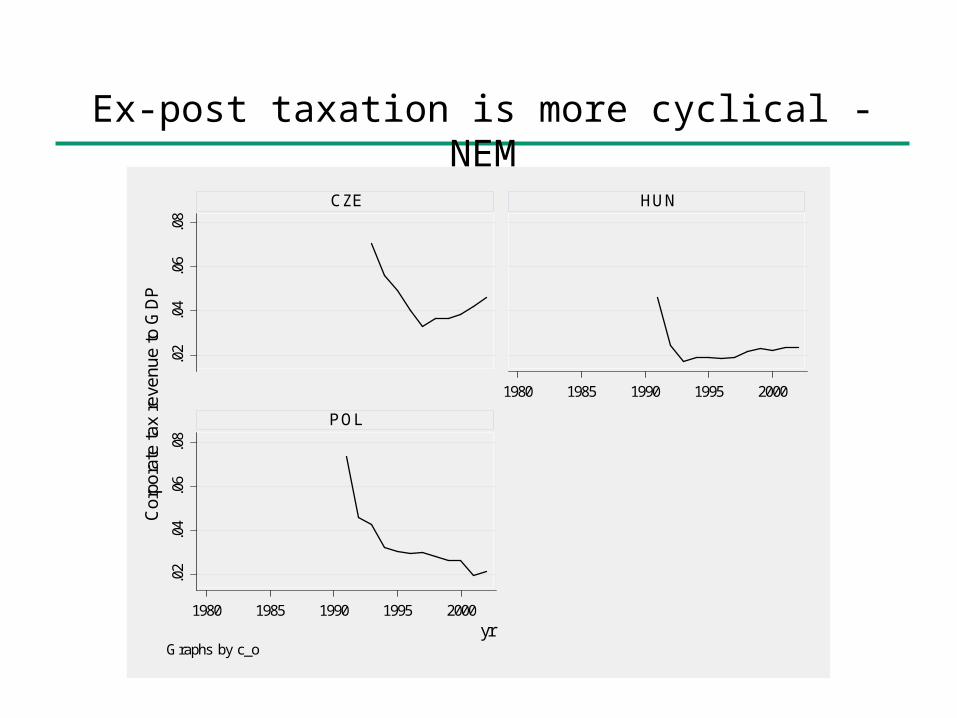

Ex-post taxation is more cyclical - NEM

.02

.04

.06

.08

.02

.04

.06

.08

1980 1985 1990 1995 2000

1980 1985 1990 1995 2000

CZE HUN

POL

Co

rpor

ate

tax

rev

enu

e to

GD

P

yrGraphs by c_o

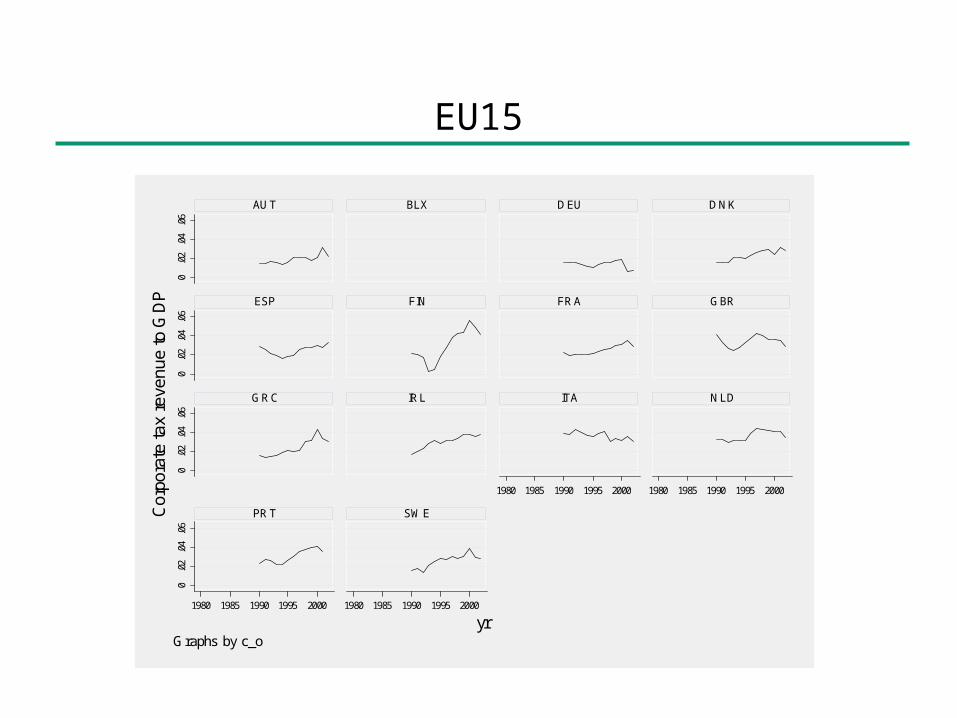

EU15

0.0

2.0

4.0

60

.02

.04

.06

0.0

2.0

4.0

60

.02

.04

.06

1980 1985 1990 1995 2000 1980 1985 1990 1995 2000

1980 1985 1990 1995 2000 1980 1985 1990 1995 2000

AUT BLX DEU DNK

ESP FIN FRA GBR

GRC IRL ITA NLD

PRT SWECor

pora

te ta

x re

venu

e to

GD

P

yrGraphs by c_o

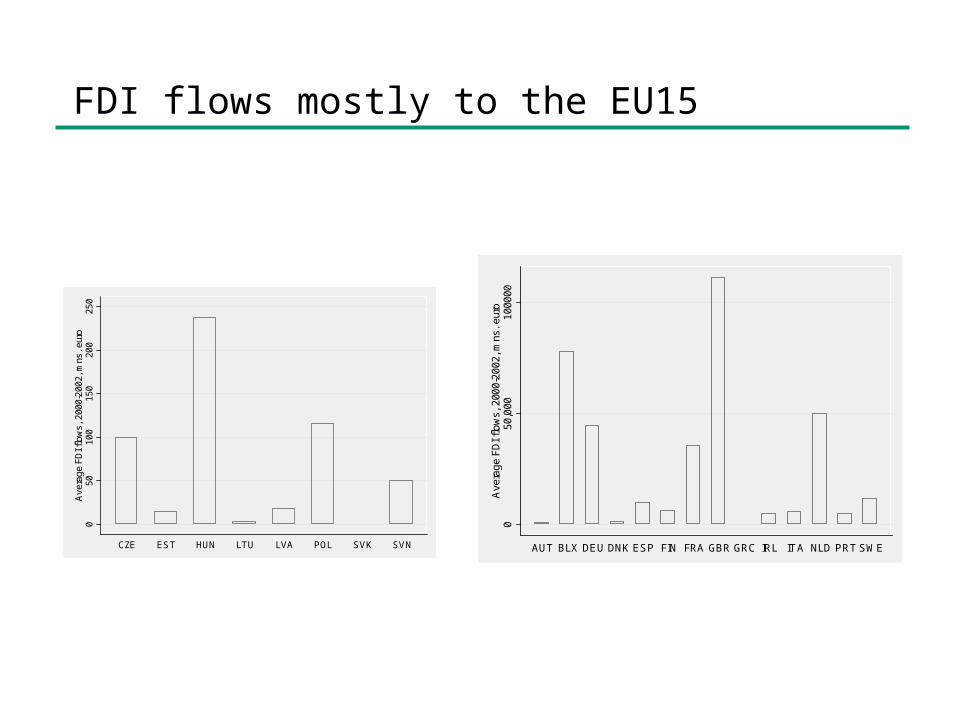

FDI flows mostly to the EU150

5010

015

020

025

0A

vera

ge F

DI f

low

s, 2

000-

2002

, mns

. eur

o

CZE EST HUN LTU LVA POL SVK SVN

05

0,00

01

0000

0A

ver

age

FD

I fl

ow

s,

200

0-2

002

, mns

. eur

o

AUT BLX DEU DNK ESP FIN FRA GBR GRC IRL ITA NLD PRT SWE

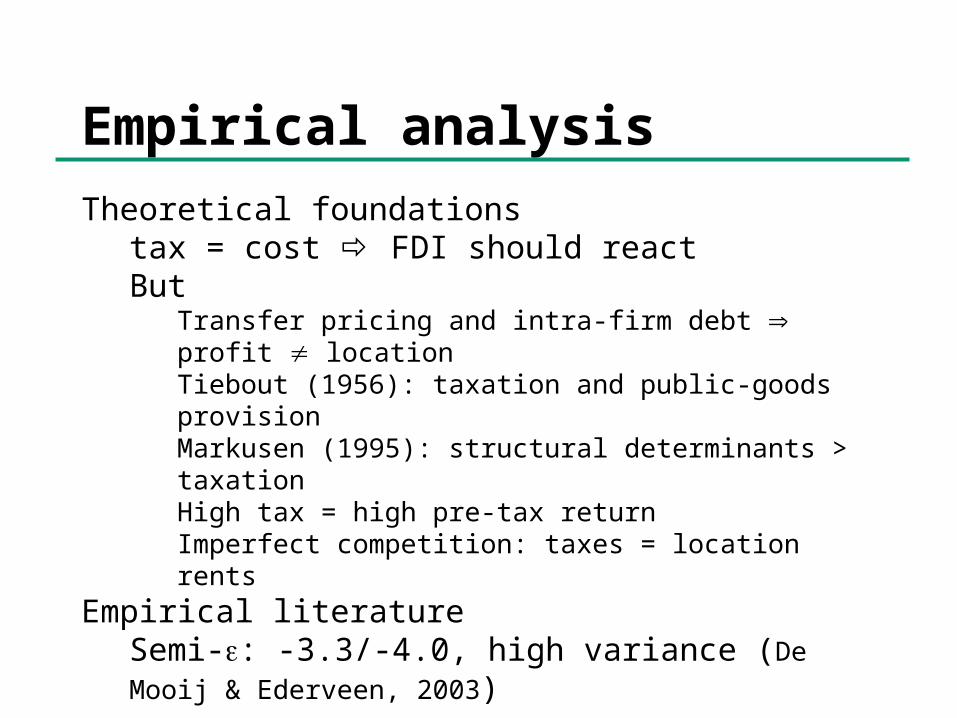

Empirical analysisTheoretical foundations

tax = cost FDI should reactBut

Transfer pricing and intra-firm debt profit locationTiebout (1956): taxation and public-goods provisionMarkusen (1995): structural determinants > taxationHigh tax = high pre-tax returnImperfect competition: taxes = location rents

Empirical literatureSemi-: -3.3/-4.0, high variance (De Mooij & Ederveen, 2003)

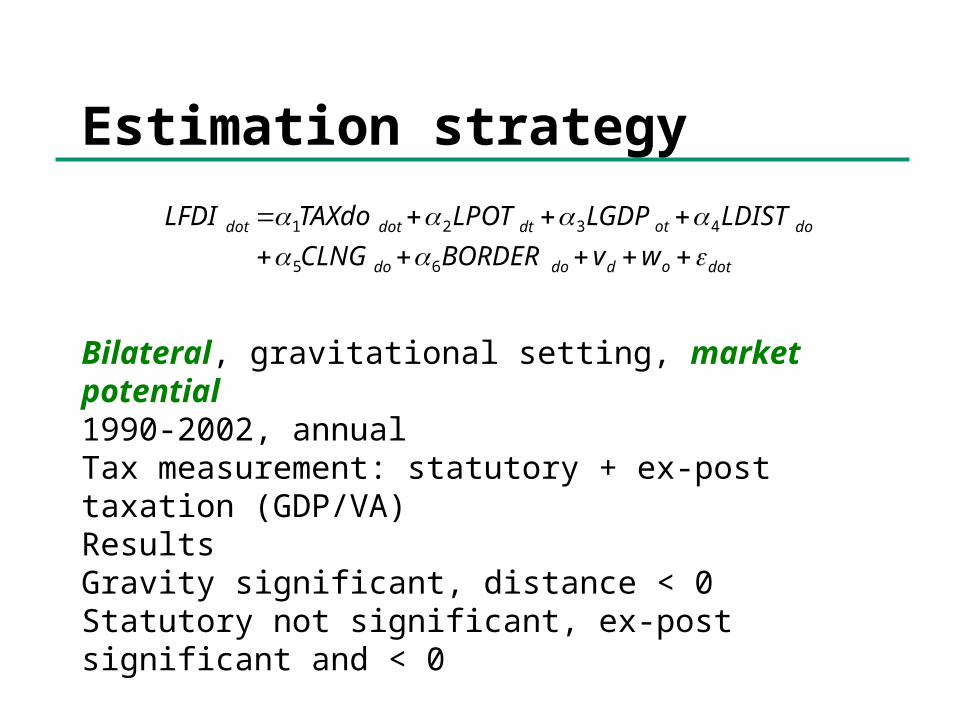

Estimation strategy

Bilateral, gravitational setting, market potential1990-2002, annualTax measurement: statutory + ex-post taxation (GDP/VA)ResultsGravity significant, distance < 0Statutory not significant, ex-post significant and < 0

dotoddodo

dootdtdotdot

wvBORDERCLNG

LDISTLGDPLPOTTAXdoLFDI

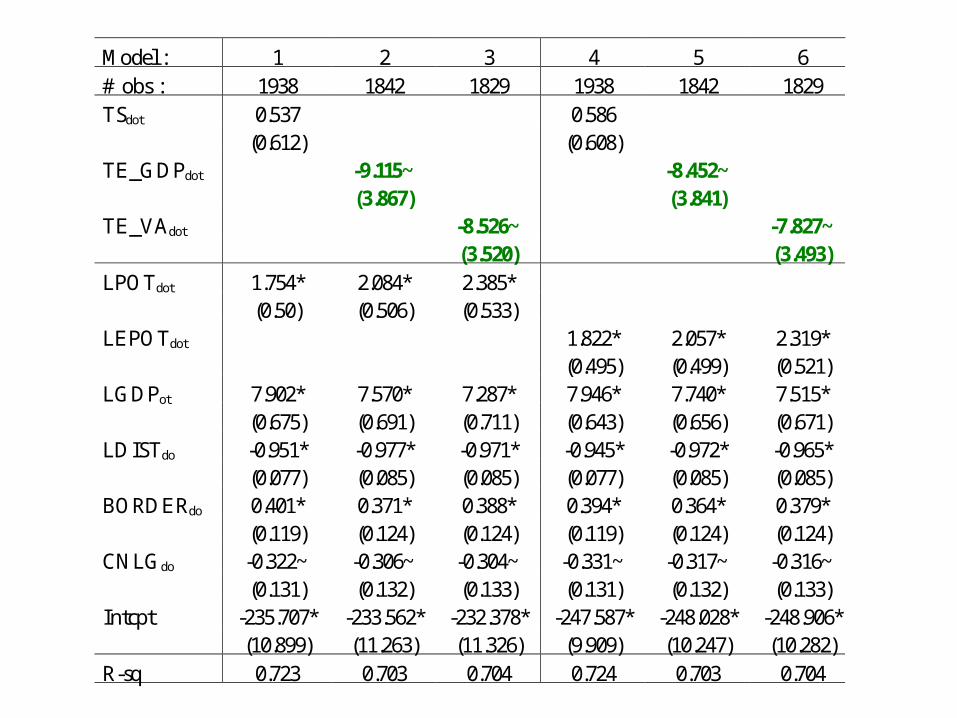

65

4321

Model : 1 2 3 4 5 6# obs : 1938 1842 1829 1938 1842 1829TSdot 0.537 0.586

(0.612) (0.608)TE_GDPdot -9.115~ -8.452~

(3.867) (3.841)TE_VAdot -8.526~ -7.827~

(3.520) (3.493)LPOTdot 1.754* 2.084* 2.385*

(0.50) (0.506) (0.533)LEPOTdot 1.822* 2.057* 2.319*

(0.495) (0.499) (0.521)LGDPot 7.902* 7.570* 7.287* 7.946* 7.740* 7.515*

(0.675) (0.691) (0.711) (0.643) (0.656) (0.671)LDISTdo -0.951* -0.977* -0.971* -0.945* -0.972* -0.965*

(0.077) (0.085) (0.085) (0.077) (0.085) (0.085)BORDERdo 0.401* 0.371* 0.388* 0.394* 0.364* 0.379*

(0.119) (0.124) (0.124) (0.119) (0.124) (0.124)CNLGdo -0.322~ -0.306~ -0.304~ -0.331~ -0.317~ -0.316~

(0.131) (0.132) (0.133) (0.131) (0.132) (0.133)Intcpt -235.707* -233.562* -232.378* -247.587* -248.028* -248.906*

(10.899) (11.263) (11.326) (9.909) (10.247) (10.282)R-sq 0.723 0.703 0.704 0.724 0.703 0.704

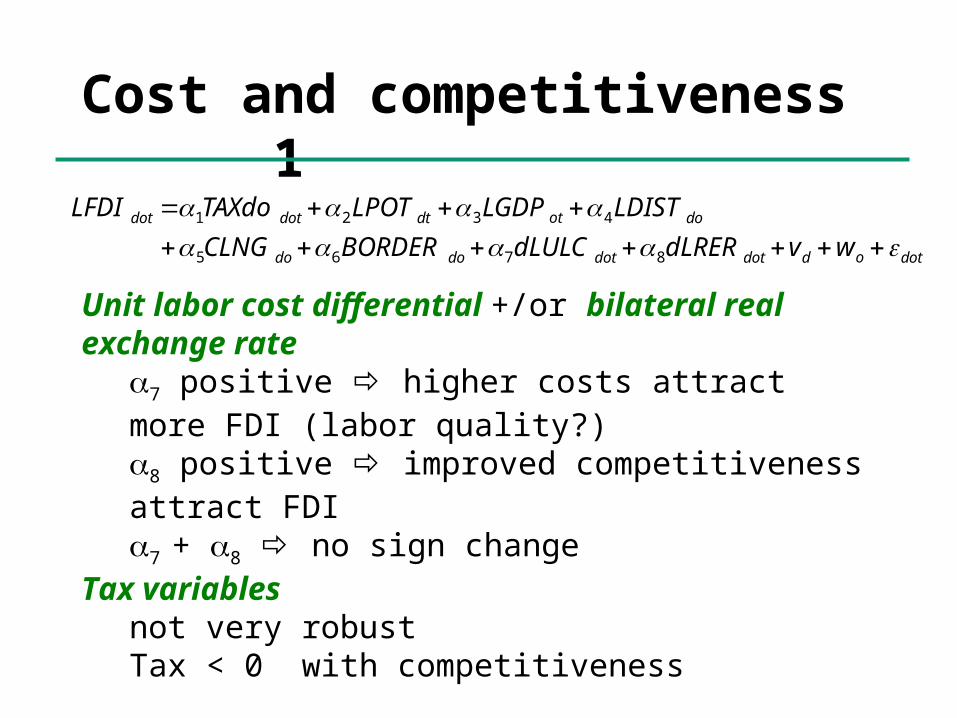

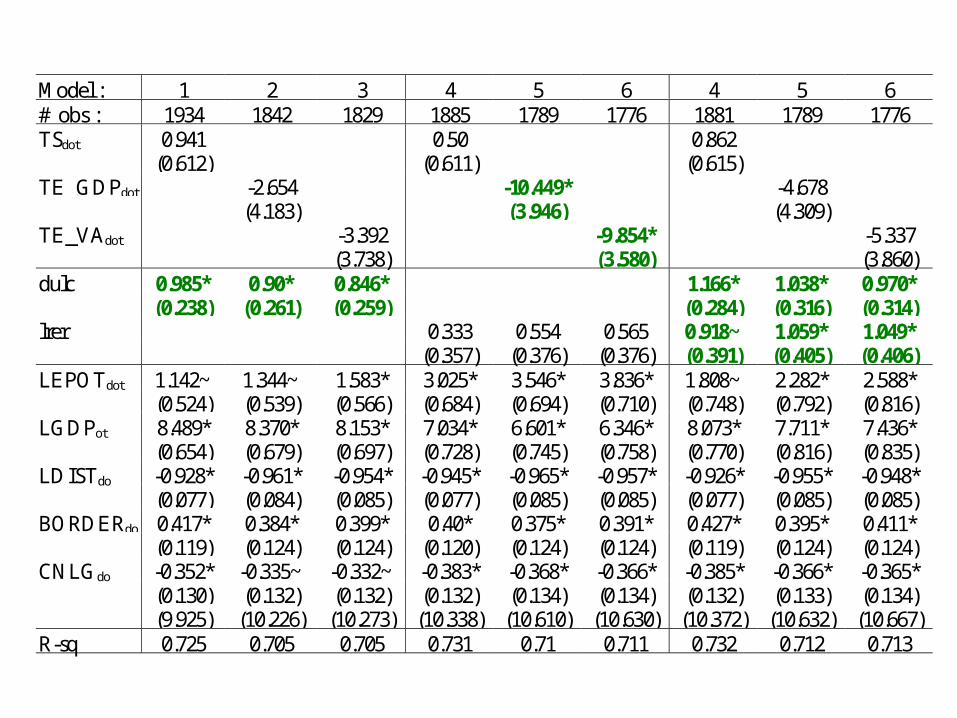

Cost and competitiveness1

Unit labor cost differential +/or bilateral real exchange rate

7 positive higher costs attract more FDI (labor quality?)8 positive improved competitiveness attract FDI7 + 8 no sign change

Tax variablesnot very robustTax < 0 with competitiveness

dotoddotdotdodo

dootdtdotdot

wvdLRERdLULCBORDERCLNG

LDISTLGDPLPOTTAXdoLFDI

8765

4321

Model : 1 2 3 4 5 6 4 5 6# obs : 1934 1842 1829 1885 1789 1776 1881 1789 1776TSdot 0.941 0.50 0.862

(0.612) (0.611) (0.615)TE_GDPdot -2.654 -10.449* -4.678

(4.183) (3.946) (4.309)TE_VAdot -3.392 -9.854* -5.337

(3.738) (3.580) (3.860)dulc 0.985* 0.90* 0.846* 1.166* 1.038* 0.970*

(0.238) (0.261) (0.259) (0.284) (0.316) (0.314)lrer 0.333 0.554 0.565 0.918~ 1.059* 1.049*

(0.357) (0.376) (0.376) (0.391) (0.405) (0.406)LEPOTdot 1.142~ 1.344~ 1.583* 3.025* 3.546* 3.836* 1.808~ 2.282* 2.588*

(0.524) (0.539) (0.566) (0.684) (0.694) (0.710) (0.748) (0.792) (0.816)LGDPot 8.489* 8.370* 8.153* 7.034* 6.601* 6.346* 8.073* 7.711* 7.436*

(0.654) (0.679) (0.697) (0.728) (0.745) (0.758) (0.770) (0.816) (0.835)LDISTdo -0.928* -0.961* -0.954* -0.945* -0.965* -0.957* -0.926* -0.955* -0.948*

(0.077) (0.084) (0.085) (0.077) (0.085) (0.085) (0.077) (0.085) (0.085)BORDERdo 0.417* 0.384* 0.399* 0.40* 0.375* 0.391* 0.427* 0.395* 0.411*

(0.119) (0.124) (0.124) (0.120) (0.124) (0.124) (0.119) (0.124) (0.124)CNLGdo -0.352* -0.335~ -0.332~ -0.383* -0.368* -0.366* -0.385* -0.366* -0.365*

(0.130) (0.132) (0.132) (0.132) (0.134) (0.134) (0.132) (0.133) (0.134)(9.925) (10.226) (10.273) (10.338) (10.610) (10.630) (10.372) (10.632) (10.667)

R-sq 0.725 0.705 0.705 0.731 0.71 0.711 0.732 0.712 0.713

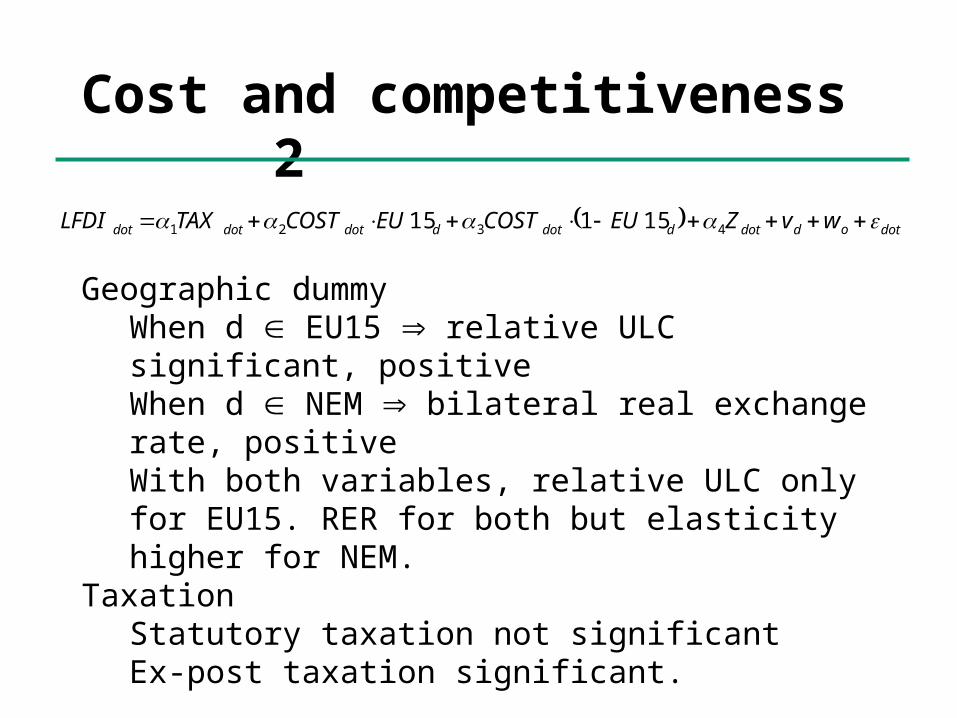

Cost and competitiveness2

Geographic dummyWhen d EU15 relative ULC significant, positiveWhen d NEM bilateral real exchange rate, positiveWith both variables, relative ULC only for EU15. RER for both but elasticity higher for NEM.

TaxationStatutory taxation not significantEx-post taxation significant.

dotoddotddotddotdotdot wvZEUCOSTEUCOSTTAXLFDI 4321 15115

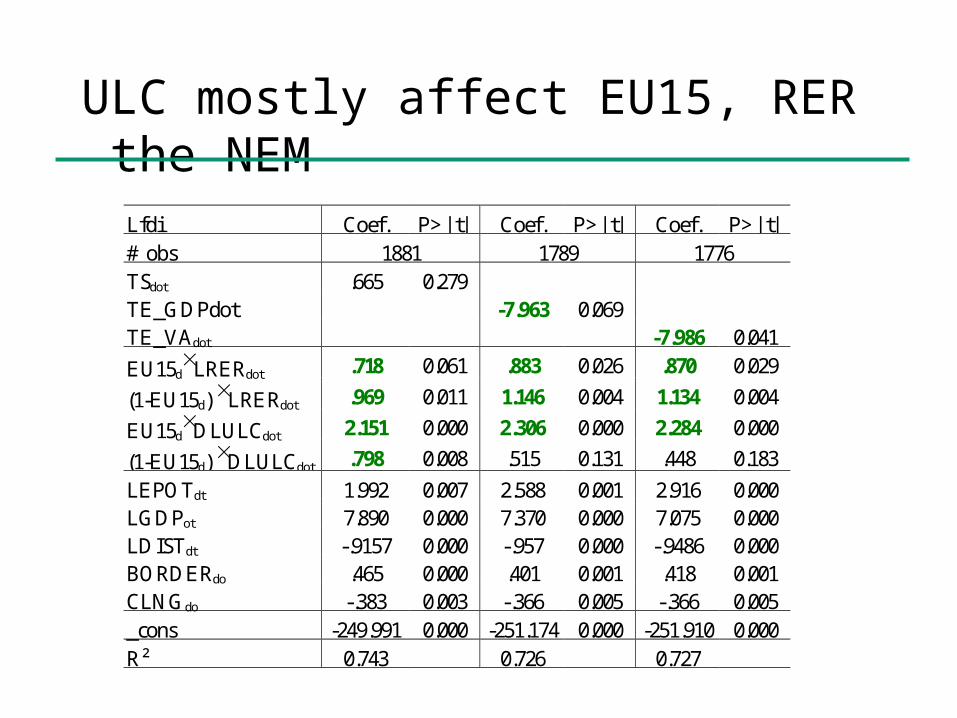

Lfdi Coef. P>| t| Coef. P>| t| Coef. P>| t|# obs 1881 1789 1776TSdot .665 0.279TE_GDPdot -7.963 0.069TE_VAdot -7.986 0.041

EU15dLRERdot .718 0.061 .883 0.026 .870 0.029

(1-EU15d) LRERdot .969 0.011 1.146 0.004 1.134 0.004

EU15dDLULCdot 2.151 0.000 2.306 0.000 2.284 0.000

(1-EU15d) DLULCdot .798 0.008 .515 0.131 .448 0.183

LEPOTdt 1.992 0.007 2.588 0.001 2.916 0.000LGDPot 7.890 0.000 7.370 0.000 7.075 0.000LDISTdt -.9157 0.000 -.957 0.000 -.9486 0.000BORDERdo .465 0.000 .401 0.001 .418 0.001CLNGdo -.383 0.003 -.366 0.005 -.366 0.005_cons -249.991 0.000 -251.174 0.000 -251.910 0.000R² 0.743 0.726 0.727

ULC mostly affect EU15, RER the NEM

Taxation only impacts FDI in the EU15...

lfdi Coef. P>| t| Coef, P>| t| Coef, P>| t|# obs. 1881 1789 1776EU15d

TSdot 0,96 0,143(1-EU15d) TSdot -0,01 0,987EU15d

TE_GDPdot -8,75 0,083(1-EU15d) TE_GDPdot -6,67 0,267EU15d

TE_VAdot -8,56 0,058(1-EU15d) TE_VAdot -7,07 0,182EU15d LRERdot 0,69 0,075 0,88 0,027 0,87 0,029(1- EU15d)LRERdot 0,94 0,014 1,14 0,004 1,13 0,005EU15d LULCdot 2,05 0,000 2,32 0,000 2,29 0,000(1- EU15d)LULCdot 0,76 0,012 0,55 0,127 0,48 0,179LEPOTdt 2,00 0,006 2,57 0,001 2,90 0,000LGDPot 7,89 0,000 7,38 0,000 7,08 0,000LDISTdt -0,93 0,000 -0,96 0,000 -0,95 0,000BORDERdo 0,46 0,000 0,40 0,001 0,42 0,001CLNGdo -0,39 0,003 -0,36 0,005 -0,36 0,005_cons -250,27 0,000 -250,78 0,000 -251,59 0,000R² 0.744 0.726 0.727

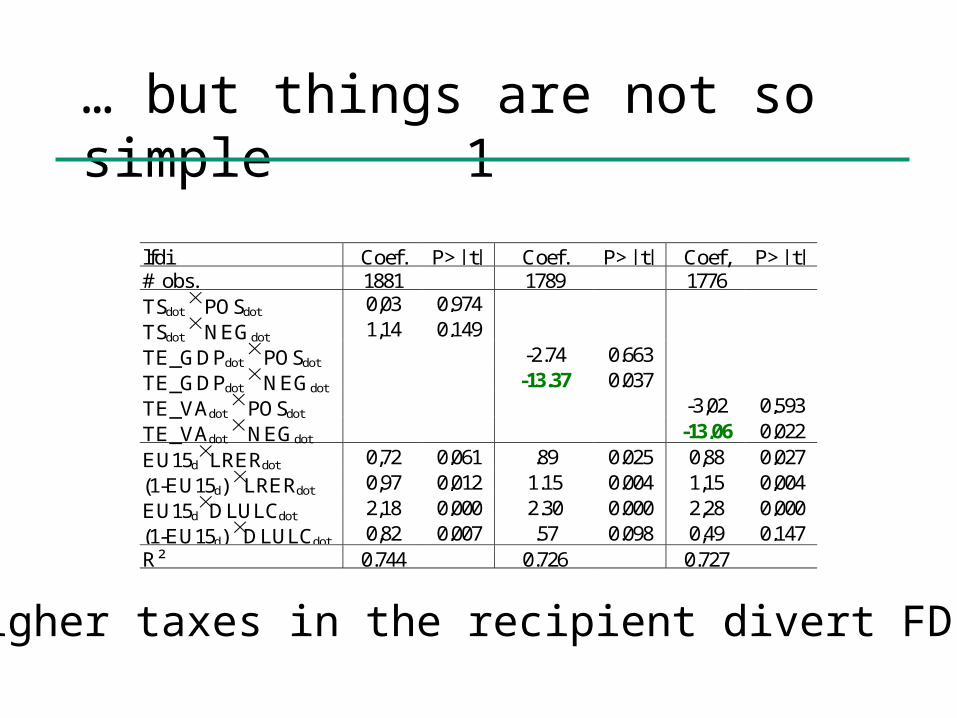

… but things are not so simple 1

lfdi Coef. P>| t| Coef. P>| t| Coef, P>| t|# obs. 1881 1789 1776TSdot POSdot 0,03 0,974TSdot NEGdot 1,14 0,149TE_GDPdot POSdot -2.74 0.663TE_GDPdot NEGdot -13.37 0.037TE_VAdot POSdot -3,02 0,593TE_VAdot NEGdot -13,06 0,022EU15d

LRERdot 0,72 0,061 .89 0.025 0,88 0,027(1-EU15d) LRERdot 0,97 0,012 1.15 0.004 1,15 0,004EU15d

DLULCdot 2,18 0,000 2.30 0.000 2,28 0,000(1-EU15d) DLULCdot 0,82 0,007 .57 0.098 0,49 0,147R² 0.744 0.726 0.727

Higher taxes in the recipient divert FDI

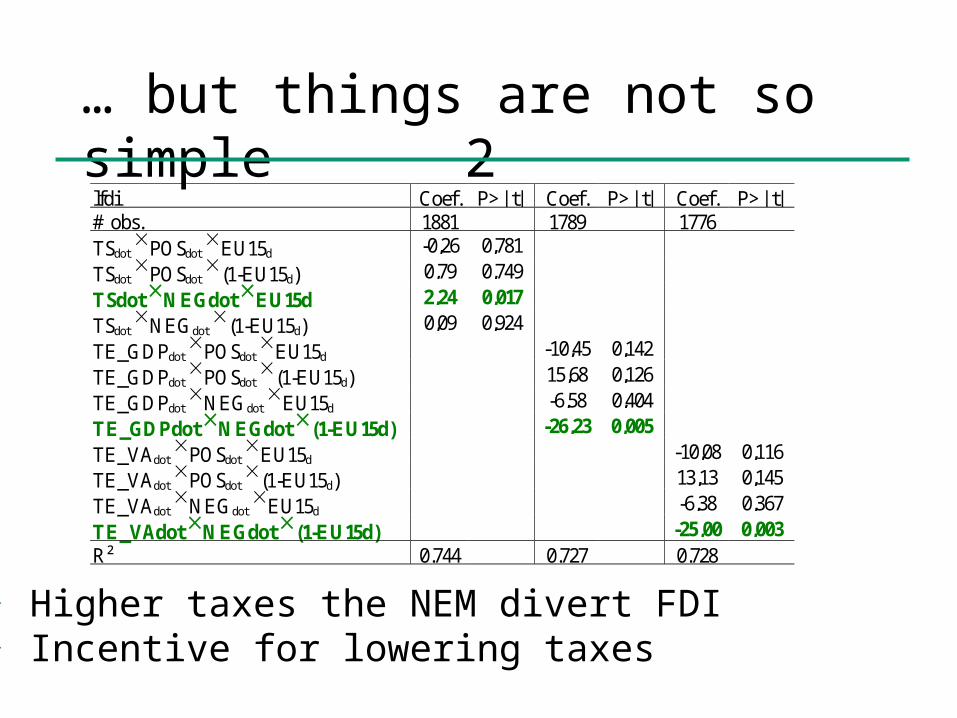

… but things are not so simple 2lfdi Coef. P>| t| Coef. P>| t| Coef. P>| t|# obs. 1881 1789 1776TSdot POSdot EU15d -0,26 0,781TSdot POSdot (1-EU15d) 0,79 0,749TSdot NEGdot EU15d 2,24 0,017TSdot NEGdot (1-EU15d) 0,09 0,924TE_GDPdot POSdot EU15d -10,45 0,142TE_GDPdot POSdot (1-EU15d) 15,68 0,126TE_GDPdot NEGdot EU15d -6,58 0,404TE_GDPdot NEGdot (1-EU15d) -26,23 0,005TE_VAdot POSdot EU15d -10,08 0,116TE_VAdot POSdot (1-EU15d) 13,13 0,145TE_VAdot NEGdot EU15d -6,38 0,367TE_VAdot NEGdot (1-EU15d) -25,00 0,003R² 0.744 0.727 0.728

Higher taxes the NEM divert FDI Incentive for lowering taxes

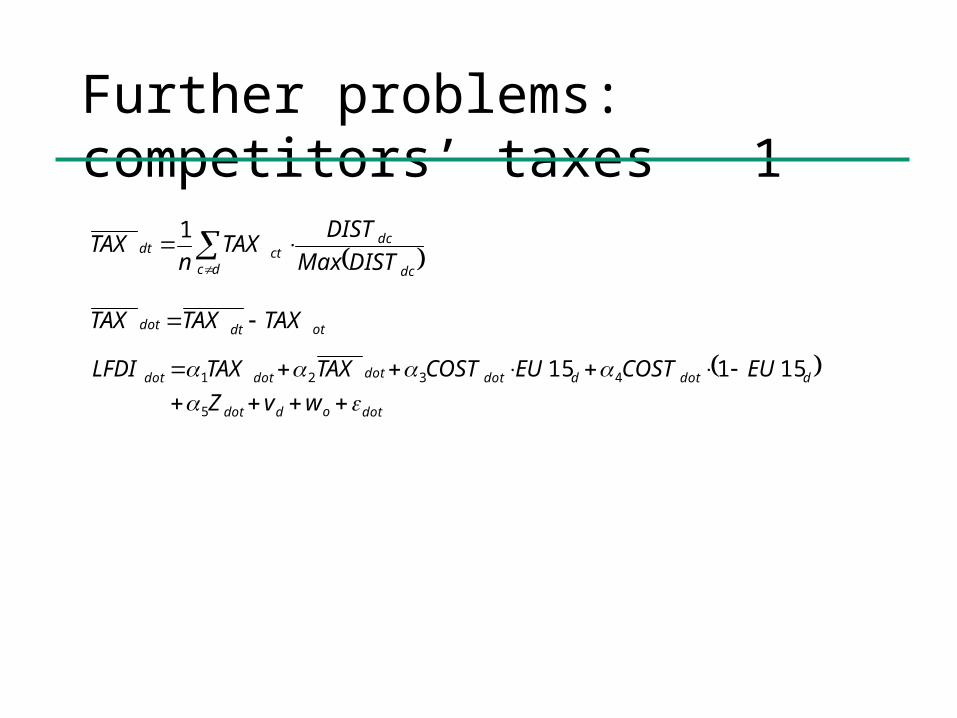

Further problems: competitors’ taxes 1

dc dc

dcctdt

DISTMaxDIST

TAXn

TAX1

otdtdot TAXTAXTAX

dotoddot

ddotddotdotdotdot

wvZ

EUCOSTEUCOSTTAXTAXLFDI

5

4321 15115

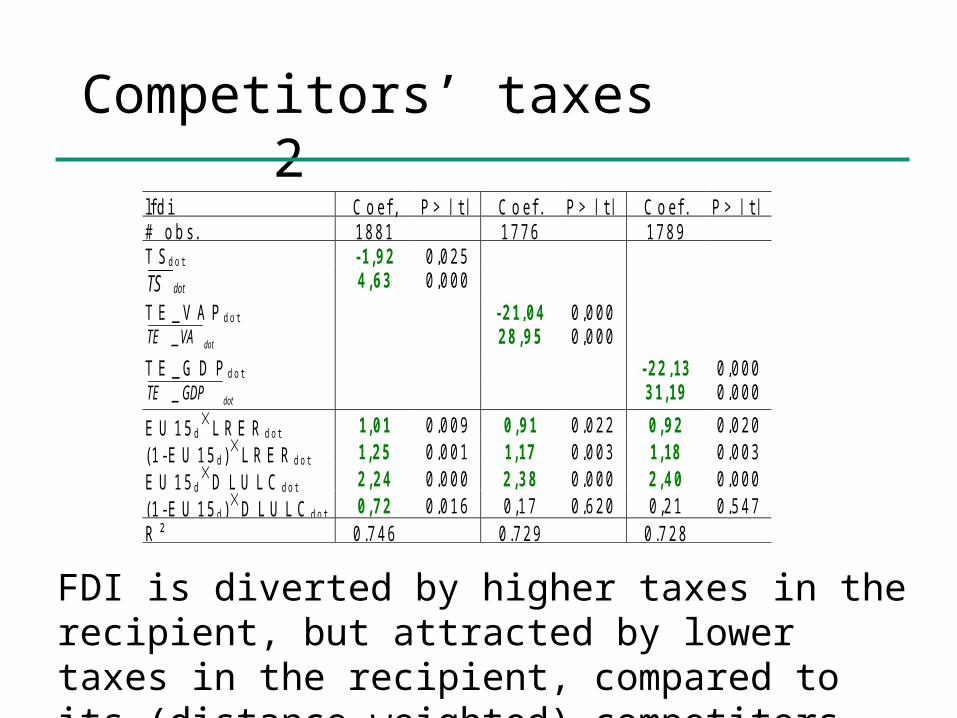

Competitors’ taxes2

lf d i C o ef , P > | t| C o ef . P > | t| C o ef . P > | t|# o b s. 18 81 17 76 17 89T S d o t -1,92 0 ,0 25

dotTS 4,63 0 ,0 00

T E _ V A P d o t -21,04 0 ,0 00

dotVATE _ 28,95 0 ,0 00

T E _ G D P d o t -22,13 0 ,0 00

dotGDPTE _ 31,19 0 ,0 00

E U 1 5 dL R E R d o t 1,01 0 ,0 09 0,91 0 ,0 22 0,92 0 ,0 20

(1 - E U 15 d )L R E R d o t 1,25 0 ,0 01 1,17 0 ,0 03 1,18 0 ,0 03E U 1 5 d

D L U L C d o t 2,24 0 ,0 00 2,38 0 ,0 00 2,40 0 ,0 00(1 - E U 15 d )D L U L C d o t 0,72 0 ,0 16 0 ,1 7 0 ,6 20 0 ,2 1 0 ,5 47R ² 0 .7 46 0 .7 29 0 .7 28

FDI is diverted by higher taxes in the recipient, but attracted by lower taxes in the recipient, compared to its (distance-weighted) competitors

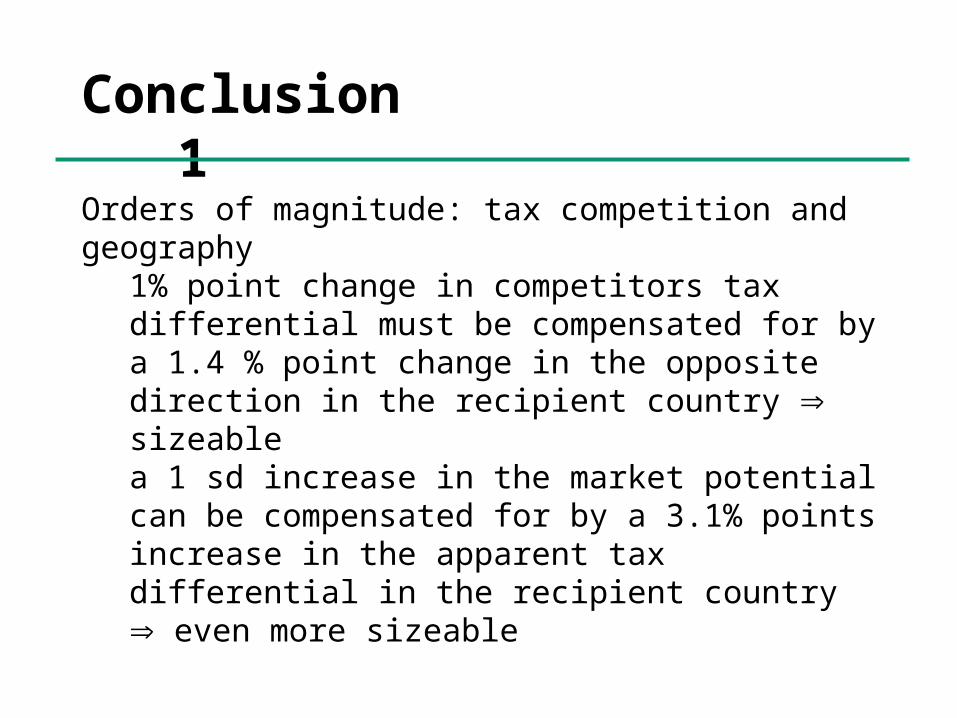

Conclusion1

Orders of magnitude: tax competition and geography

1% point change in competitors tax differential must be compensated for by a 1.4 % point change in the opposite direction in the recipient country sizeablea 1 sd increase in the market potential can be compensated for by a 3.1% points increase in the apparent tax differential in the recipient country even more sizeable