corporate officers & directors liability - dla piper

TRANSCRIPT

CORPORATE OFFICERS & DIRECTORS LIABILITY

Westlaw Journal Formerly Andrews Litigation Reporter

40856729

WHAT’S INSIDE

Litigation News and Analysis • Legislation • Regulation • Expert Commentary VOLUME 26, ISSUE 4 / AUGUST 16, 2010

SUBPRIME

10 New York pension funds sue Merrill Lynch for subprime fraud

DiNapoliv.MerrillLynch&Co. (S.D.N.Y.)

11 Goldman VP seeks dismissal after firm settles SEC suit

SECv.GoldmanSachs&Co. (S.D.N.Y.)

SETTLEMENTS/SUBPRIME

13 Judge gives nod to $624 million Countrywide fraud settlement

InreCountrywideFin.Corp.Sec.Litig. (C.D. Cal.)

14 $125 million settlement reached in New Century subprime case

InreNewCenturyFin.Corp. (C.D. Cal.)

15 Citigroup to pay $75 million to settle SEC suit

SECv.Citigroup (D.D.C.)

15 Mortgage insurer PMI settles subprime suit for $31 million

InrePMIGroupSec.Litig. (N.D. Cal.)

POISON PILLS

16 Both parties appeal parts of ruing on potent poison pill

VersataEnters.v.SelecticaInc. (Del.)

BOOKS & RECORDS

17 Records action not an end run around discovery rules, plaintiff’s appeal says

Kingv.VeriFoneHoldings (Del.)

SEE PAGE 9

CONTINUED ON PAGE 12

COMMENTARY

The Foreign Corrupt Practices Act: A midyear reviewKiera S. Gans and Robert A. Johnston Jr. of DLA Piper present a comprehensive update on enforcement trends under the Foreign Corrupt Practices Act, and they advise cor-porate counsel to prepare for an ever more rigorous and hostile regulatory environment in the near future.

SEE PAGE 3

COMMENTARY

Dodd-Frank law expands whistle-blower provisions of Sarbanes-Oxley ActAttorney Steven Pearlman of Seyfarth Shaw LLP discusses the new whistle-blower provi-sions of the Dodd-Frank Wall Street Reform and Consumer Protection Act and their impact on financial services companies.

SUBPRIME/SECURITIES FRAUD

N.Y. pensioners file new challenge to BofA–Merrill mergerBank of America’s top officers duped investors into backing its $50 billion rescue buy-out of Merrill Lynch by hiding Merrill’s massive exposure to risky subprime mortgages, a New York public employee pension fund has charged in Manhattan federal court.

REUTERS/Dylan MartinezREUTERS/Brendan McDermid

© 2010 Thomson Reuters2 | WESTLAW JOURNAL n CORPORATE OFFICERS & DIRECTORS LIABILITY

TABLE OF CONTENTSWestlaw Journal Corporate Officers & Directors LiabilityPublished since November 1985

Publisher: Mary Ellen Fox

Executive Editor: Jodine Mayberry

Production Coordinator: Tricia Gorman

Managing Editor: Donna M. Higgins

Editor: Frank [email protected]

Westlaw Journal Corporate Officers & Directors Liability (ISSN 2155-5885) is published biweekly by Andrews Publications, a Thomson Reuters/West business.

Andrews Publications175 Strafford AvenueBuilding 4, Suite 140Wayne, PA 19087877-595-0449Fax: 800-220-1640www.andrewsonline.comCustomer service: 800-328-4880

For more information, or to subscribe,please call 800-328-9352 or visitwest.thomsom.com.

Reproduction AuthorizationAuthorization to photocopy items for internal or personal use, or the internal or personal use by specific clients, is granted by Andrews Publications for libraries or other users reg-istered with the Copyright Clearance Center (CCC) for a fee to be paid directly to the Copyright Clearance Center, 222 Rosewood Drive, Danvers, MA 01923; 978-750-8400; www.copyright.com.

How to Find Documents on WestlawThe Westlaw number of any opinion or trial filing is listed at the bottom of each article available. The numbers are configured like this: 2009 WL 000000. Sign in to Westlaw and on the “Welcome to Westlaw” page, type the Westlaw number into the box at the top left that says “Find this document by citation” and click on “Go.”

Subprime/Securities Fraud: DiNapoli v. Bank of Am. Corp.N.Y. pensioners file new challenge to BofA–Merrill merger (S.D.N.Y.) ..............................................................1

Commentary: By Kiera S. Gans, Esq., and Robert A. Johnston Jr., Esq.The Foreign Corrupt Practices Act: A midyear review ....................................................................................... 3

Commentary: By Steven Pearlman, Esq.Dodd-Frank law expands whistle-blower provisions of Sarbanes-Oxley Act .................................................9

Subprime/Mortgage-Backed Securities: DiNapoli v. Merrill Lynch & Co.New York pension funds sue Merrill Lynch for subprime fraud (S.D.N.Y.)...................................................... 10

Subprime: SEC v. Goldman Sachs & Co.Goldman VP seeks dismissal after firm settles SEC suit (S.D.N.Y.) ..................................................................11

Settlements/Subprime: In re Countrywide Fin. Corp. Sec. Litig.Judge gives nod to $624 million Countrywide fraud settlement (C.D. Cal.) ..................................................13

Settlements/Subprime: In re New Century Fin. Corp.$125 million settlement reached in New Century subprime case (C.D. Cal.) .................................................14

Settlements/Subprime: SEC v. CitigroupCitigroup to pay $75 million to settle SEC suit (D.D.C.) ..................................................................................15

Settlements/Subprime: In re PMI Group Sec. Litig.Mortgage insurer PMI settles subprime suit for $31 million (N.D. Cal.) ..........................................................15

Poison Pills: Versata Enters. v. Selectica Inc.Both parties appeal parts of ruing on potent poison pill (Del.) ......................................................................16

Books & Records: King v. VeriFone HoldingsRecords action not an end run around discovery rules, plaintiff’s appeal says (Del.) ................................... 17

Stock Option Backdating/Settlements: In re Staples Inc. S’holder Deriv. Litig.Judge OKs $7.2 million settlement of Staples options backdating suits (Del. Ch.) .......................................18

Advancement: Crawford v. Spectrum Group Int’lEx-officer says company delays, discounts and denies legal bills (Del. Ch.) .................................................19

Chancery Court Shorts ....................................................................................................................................20

Case and Document Index ...............................................................................................................................21

HOW TO SUBMIT A COMMENTARY OR BYLINED ARTICLEWest Publishing, a Thomson Reuters business, encourages its readers to submit commentaries or expert analysis on a variety of topics. Our focus includes trends affecting the legal community, as well as issues arising from court rulings or legislative initiatives. Articles between 2,000 and 2,500 words are preferred but other lengths will be considered. Please contact the editor of this publication, or contact Phyllis Skupien, Managing Editor, at [email protected] for more information.

ABOUT ANDREWSAndrews Publications is a specialized information publisher focusing on litigation developments. A division of Thomson Reuters, Andrews produces newsletters and Westlaw databases tightly focused on more than 45 individual practice areas. Andrews’ softbound books and online contin-uing legal education courses draw on the expertise of legal practitioners and experts across the country to create a knowledge-sharing community. Andrews’ customers are lawyers, insurers, corporate counsel, medical groups, academics, government agencies and other professionals whose work requires up-to-date litigation information.

AUGUST 16, 2010 n VOLUME 26 n ISSUE 4 | 3© 2010 Thomson Reuters

COMMENTARY

The Foreign Corrupt Practices Act: A midyear reviewBy Kiera S. Gans, Esq., and Robert A. Johnston Jr., Esq.

Halfway through 2010, it is apparent that the stringent anti-corruption environment that has been developing over the last several years has only continued to tighten. U.S. authorities are dedicating more resources to enforcement of the Foreign Corrupt Practices Act. In late 2009, the Department of Justice and the Securities and Exchange Commission created specialized units with dedicated chiefs and staff; these units were designed to centralize experience and knowledge in FCPA enforcement. In addition, the DOJ is adding experienced prosecutors to its ranks and partnering with U.S. attorneys’ offices and other government agencies throughout the country, including the FBI, to maximize resources.

Prosecutors continue to develop novel prosecutorial approaches, and with new anti-bribery legislation coming out of the United Kingdom and a new U.S. law that would reward whistle-blowers who assist in the prosecution of FCPA violations, the regulatory regime has become increasingly thorny. Indeed, companies that faced a harsh regime in 2009 continue to face many of the same — and some new — enforcement trends or risks this year.

This article provides a midyear review of the FCPA and anti-corruption landscape and also:

• Provides a brief overview of the FCPA.

• Addresses recent trends in FCPA enforcement, including the increased prosecution of individuals, changes in the scope of remedies sought by authorities and other new prosecutorial approaches.

• Highlights the opinion procedure release obtained in 2010.

• Discusses recent developments regarding the international approach to corruption.

THE FCPA

The FCPA’s anti-bribery provisions make it unlawful for any corporation or any corporate officer, director, employee, agent

or stockholder acting on behalf of the corporation to make (or promise to make) payments to foreign officials, political parties or other persons for the purposes of influencing or inducing the foreign official to act in a particular manner or to secure a business advantage.1

The accounting provisions require that books, records and accounts accurately reflect the company’s transactions and that the company devises and maintains a system of internal accounting controls sufficient to provide reasonable assurances that financial

statements and other public disclosures are accurate.2 These provisions impose criminal liability on individuals who knowingly circumvent or fail to implement a system of internal controls or knowingly falsify any books, records or accounts.3

TRENDS IN FCPA ENFORCEMENT

The FCPA provides for severe criminal and civil penalties against corporations and individuals.4

Increased focus on individuals

Since as early as November 2009, the prosecution of individuals has been a “cornerstone” of FCPA enforcement.5 Regulators have sought to prosecute third-party intermediaries as well as corporate executives such as country managers, salespeople and C-level executives. This approach has been favored by regulators who view the prosecution of individual wrongdoers as a powerful incentive for compliance while not taxing innocent shareholders.

Parallel proceedings

A trend from 2009 that has continued into the first half of 2010 is parallel enforcement proceedings against employees and companies. As a corollary, the requirement

to continue to cooperate in the prosecution of corporate employees has increasingly become a routine part of companies’ negotiated resolution with regulatory authorities.

In the case against Control Components Inc., the DOJ prosecuted the California-based valve company and eight of its corporate officers in their individual capacities. The company’s former director of worldwide factory sales pleaded guilty Jan. 8, 2009, to conspiring to violate the FCPA. He further admitted that he provided

false and misleading responses to internal investigators during a 2004 internal audit and destroyed e-mails to obstruct the internal audit. The company’s former finance director pleaded guilty Feb. 3, 2009, to one count of conspiracy to violate the FCPA. These two corporate officers await sentencing.

Subsequently, on April 8, 2009, six other former executives, including the former CEO, were charged in a 16-count indictment with violations of the FCPA, the Travel Act and other statutes. The trial was originally set for Dec. 8, 2009, but it has since been moved to Nov. 2.

Control Components entered guilty pleas to violations of the FCPA and the Travel Act July 31. Pursuant to the plea agreement, the company will pay a criminal fine of $18.2 million, create and maintain an anti-corruption compliance program, retain an independent monitor, and continue to cooperate with the DOJ in the ongoing investigation.

Last March Innospec Inc., a U.S.-based chemical company, pleaded guilty and paid a $40 million global settlement to resolve criminal charges brought in the United States and the United Kingdom that it committed violations of the FCPA and other

Indeed, companies that faced a harsh regime in 2009 continue to face many of the same — and

some new — enforcement trends or risks this year.

4 | WESTLAW JOURNAL n CORPORATE OFFICERS & DIRECTORS LIABILITY © 2010 Thomson Reuters

laws. The SEC’s complaint against Innospec referenced an e-mail from company agent Ousama Naaman to the company’s management that stated that Iraqi officials were demanding a 2 percent kickback on sales. In a reply e-mail, Innospec’s business director authorized more than $195,000 in bribes. U.S. authorities pursued Naaman, a dual citizen of Canada and Lebanon, for arranging bribes on behalf of a U.S. entity.

An indictment against Naaman was returned in August 2008, and he was arrested in and extradited from Germany in the summer of 2009. Naaman pleaded guilty June 25 to participation in a conspiracy to violate the FCPA and to a violation of the FCPA. Specifically, he admitted paying or promising to pay more than $3 million to Iraqi officials to win business for Innospec.

On April 28 the SEC announced a settlement with four former Alliance One employees in connection with an ongoing investigation of the North Carolina-based tobacco company. The SEC alleged that between 1996 and 2004, Alliance One’s Kyrgyz subsidiary paid bribes to officials in Kyrgyzstan. According to the SEC’s complaint, Alliance One’s subsidiary had been the subject of incessant audits by Kyrgyz tax officials, who threatened to impose fines, seize bank accounts and confiscate tobacco inventory. The tax inspectors subsequently offered to reduce the penalties in exchange for cash payments.

The SEC’s complaint further alleged that the individual defendants authorized more than $500,000 in cash and travel benefits to officials of the Thailand Tobacco Monopoly in exchange for $9.4 million in contracts. All four individual defendants have consented to civil injunctions, and two of the defendants have each agreed to pay $40,000 in civil penalties.

Increased number of trials

In the past, FCPA trials were rare, with most companies seeking to voluntarily settle cases made against them rather than risk having their corporate reputation destroyed and their employees distracted by the uncertainties

associated with an outstanding claim. The trend toward prosecuting individuals — and the personal nature of the consequences for individuals rather than corporate defendants — has meant an increase in the number of persons who are willing to challenge allegations in court rather than accept a plea.

There were three trials in 2009, all of which resulted in a guilty verdict, notwithstanding factors that played on jurors’ sympathies. Jurors convicted a well-known philanthropist with no actual knowledge of the bribery scheme (Frederic Bourke), a popular public servant (former congressman William Jefferson), and an elderly man in poor health (Gerald Green) and his wife.

At this point in the year, all evidence suggests that this trend of increased trials will continue well into 2010. As of July, there were at least

14 individuals in addition to the 22 so-called “SHOT Show” defendants (not all of whom are likely to take their cases to court) who are scheduled for trial over the next year or so. This case is described later.

On Sept. 14, 2009, Gerald and Patricia Green were convicted of nine counts of violating the FCPA, one count of conspiring to violate the FCPA, seven counts of money laundering and one count of conspiring to commit money laundering. Patricia also was found guilty of two counts of falsely subscribing to a U.S. income tax return. The Greens were accused of bribing a Thai official in exchange for contracts to manage and operate a film festival.

Despite several factors playing on the jury’s sympathies, including the elderly Gerald’s poor health (he wore a breathing tube attached to an oxygen tank) and advanced age, the Greens were found guilty. They were scheduled to be sentenced Dec. 17, 2009. In a Dec. 14 court filing, prosecutors argued that notwithstanding the pre-sentence report’s recommendation for a downward departure from the federal sentencing guidelines, Gerald’s sentence should be enhanced because he orchestrated the bribery plot and perjured himself. Sentencing has been postponed.

A federal indictment was unsealed in Los Angeles Jan. 19 charging Juthamas Siriwan, the ex-governor of the Tourism Authority of Thailand, and her daughter Jittisopa Siriwan with accepting and soliciting bribes from the Greens. The two were not charged with a substantive FCPA violation because the law contains no provision targeting the recipients of bribes. Nevertheless, the case itself is noteworthy in that it indicates a willingness of regulators to use other statutes in order to target foreign officials on the demand side of bribery. No trial date has been set.

On Jan. 19, 2010, U.S. authorities arrested 22 people in an industry-wide sting in the military equipment industry. The so-called SHOT Show cases involve shooting, hunting and outdoor trades. These cases constitute the first large-scale FCPA sting operation executed by U.S. authorities. In connection with the mass arrests, U.S. authorities engaged 150 FBI agents who exercised 14 search warrants across the country.

The unsealed indictments allege the SHOT Show defendants intended to bribe the minister of defense of an unidentified African country to win a $15 million contract to outfit that country’s presidential guard. The defendants allegedly agreed to pay a 20 percent commission to the “sales agent” brokering in the deal. Although it is expected that many of the SHOT Show defendants will face trial, it is unclear at this point whether they will be tried individually or jointly.

Shortly after the mass arrests, the federal judge presiding over the cases said he did not see a “grand conspiracy.” Recently, prosecutors have proposed trying the 22 defendants in four separate groups.

Extraditions

Another trend that has coincided with the increased prosecution of individuals is more forceful efforts by U.S. authorities to reach individual wrongdoers by use of extradition. Last March and April, London courts ordered the extradition of two British citizens for their roles as intermediaries who arranged hundreds of millions of bribes to Nigerian officials to secure contracts for their clients.

Similarly, as discussed above, Ousama Naaman, a citizen of Canada and Lebanon, was extradited from Germany to the United States for his role in the Innospec case. In July U.S. authorities successfully extradited Flavio Ricotti, an Italian citizen, from Germany after

A trend from 2009 that has continued into the first half of this year is parallel enforcement

proceedings against employees and companies.

AUGUST 16, 2010 n VOLUME 26 n ISSUE 4 | 5© 2010 Thomson Reuters

an indictment was returned against him for violations of the FCPA and the Travel Act. Ricotti was the former vice-president of Control Components and head of sales for Europe, Africa and the Middle East.

Changes in the scope of remedies sought by authorities

Increased fines, disgorgement and forfeiture: Since 2005, FCPA fines have steadily increased, with that pattern unchanged in 2010. Indeed, the six largest FCPA settlements ever all occurred in the past 20 months. Recently, authorities have increasingly sought disgorgement and forfeiture as well. In February, Pride International, a Houston-based oil rig operator, announced that it was setting aside $56.2 million for an expected settlement with the DOJ and SEC.

BAE Systems PLC pleaded guilty March 1 to one count of conspiracy to defraud the United States by impairing and impeding its lawful functions, to make false statements about its FCPA compliance and to violate the Arms Export Control Act and International Traffic in Arms Regulations. BAE agreed to pay a $400 million fine.

Also in March 2010, as part of Innospec’s global settlement with U.S. and U.K. officials, the specialty chemical maker agreed to pay $29 million in fines and disgorge $11.2 million in profits. In April German car manufacturer Daimler AG, agreed to pay a $93.6 million fine and disgorge $91.4 million in profits to resolve DOJ and SEC inquiries into potential FCPA violations by the company and its subsidiaries in Bosnia, China, Croatia, Hungary, Latvia, Nigeria, Russia and Vietnam.

Decreased use of independent monitors: At least one trend that emerged over the previous years seems to have diminished slightly in the past several months. Although in the past virtually every case resulted in the imposition of a monitor, this may no longer be the case. The imposition of a monitor may be less likely, for example, in instances in which the corrupt conduct results from an isolated event rather than a pervasive pattern and/or companies are able to successfully convince regulators about their ability to self-police.6

The DOJ declined to impose a monitor as part of the eLandia/Latinode plea agreement. After acquiring Latinode, eLandia discovered that Latinode had made corrupt payments totaling approximately $2.2 million to

third-party consultants with knowledge that some of that money would be passed to Honduran and Yemeni government officials in exchange for business advantages. Upon learning these facts during post-closing discovery, eLandia, the new corporate parent, undertook an internal investigation, disclosed its findings to the DOJ and took remedial measures. Likewise, no monitor was appointed in the Helmerich & Payne Inc. case or UTStarCom cases, and instead the companies — both of which had self-disclosed — appear to have successfully convinced regulators of their ability to self-monitor.

In spite of the above, it should not be assumed that the risk of a compliance monitor has been eradicated completely. For example, in March Daimler announced that it would retain a compliance monitor as part of its settlement. Further, as recently as May, BAE filed a motion to extend its deadline to appoint a compliance monitor because it could not agree with the DOJ regarding an acceptable candidate to serve as a monitor.

Debarment: Although an infrequently used remedy, it is well known that a violation of the FCPA (in addition to certain foreign anti-corruption laws) can result in an entity being prohibited from participating in U.S. government–sponsored projects. In March, the U.S. State Department threatened to debar BAE Systems by announcing that it was putting a temporary administrative hold on weapons export licenses by the company, or companies using BAE’s products. The hold applies to BAE Systems Inc. (the U.S. subsidiary), as well as BAE Systems PLC (the U.K. parent) while the department studies the guilty plea and determines whether to take additional action against the company.

Unlike the U.S. government, the World Bank frequently uses debarment to punish and deter corruption in World Bank projects.7 The debarments prevent a sanctioned party from bidding on a future World Bank-financed contract either permanently or for a proscribed period of time.8

For example, the World Bank, in one of its most important and far-reaching cases to date, announced Jan. 14, 2009, that it was debarring eight entities (two permanently) for their roles in bid-rigging in a World Bank-financed road project in the Philippines. The investigation began after the project team reported suspicions of collusion in the bidding process. There is now a worldwide review of the World Bank’s activity in the roads sector.9

The World Bank also announced April 30 that it had debarred a British subsidiary of Macmillan Publishers for six years after a disclosure of a corrupt scheme involving public officials in Sudan. Although the original debarment period was set at eight years, it was reduced to six years because of an early acknowledgement of misconduct by the company. The time period can be further reduced if the company implements a compliance program and cooperates with the World Bank’s anti-corruption efforts.

Increased periods of incarceration: At the end of 2009, Frederic Bourke received a

much-publicized 366-day jail sentence for violations of the FCPA. At the beginning of 2010, Jim Brown and Jason Steph, former managers at Willbros Group, received similar sentences for their roles in providing bribes to officials in Nigeria and Ecuador.

A few months later, there has been a seeming upward tick in the average amount of incarceration time. Specifically, a judge sentenced Charles Jumet to 87 months (about seven years) in prison April 19. Regulators and FCPA observers widely touted the sentence as the longest prison sentence ever imposed in an FCPA case. The significance of this landmark decision — including whether it will set the bar for future prosecutions — is not yet known.

Indeed, in June Jumet’s co-conspirator, John Webster Warwick, was sentenced to 37 months in prison followed by two years of supervised release. The DOJ did not comment on the 50-month difference in the prison sentences imposed on Warwick and

The trend toward prosecuting individuals has meant an increase in the number of

those who are willing to challenge allegations in court rather than accept a plea.

6 | WESTLAW JOURNAL n CORPORATE OFFICERS & DIRECTORS LIABILITY © 2010 Thomson Reuters

Jumet. One possible key distinction between the conspirators is that Jumet also was charged with lying to investigators.

New prosecutorial approaches

Last year saw the development and expan-sion of various novel prosecutorial approaches to FCPA enforcement. In 2009 the SEC pushed to expand the reach of the FCPA by asserting, for the first time, a theory of “control person liability”10 against two senior executives11 and sought to expand the reach of the doctrine of constructive knowledge.12

In 2010, U.S. authorities continue to expand the reach of FCPA liability and culpable conduct. For example, thus far, 2010 has witnessed the assertion of jurisdiction on the basis of correspondent bank accounts, the use of traditional law enforcement techniques such as sting operations to ensnare FCPA violators and attempts to freeze a defendant’s assets before trial.

Jurisdiction over foreigners based on correspondent accounts: The government has sought to assert jurisdiction over foreign defendants through the use of correspondent bank accounts in the United States. Typically, dollar-denominated transactions clear through correspondent bank accounts at U.S. banks. However, the use of correspondent accounts or transactions as a basis to assert jurisdiction is a fairly new prosecutorial development.

In a few prior instances, the DOJ and the SEC asserted jurisdiction based on the use of correspondent accounts. However, in those cases, the agencies also relied on more traditional theories of jurisdiction, such as direct transfers from U.S. bank accounts, thus leaving open questions as to whether correspondent accounts alone would establish jurisdiction.

For the first time, in the prosecutions of two British nationals, the government is predicating jurisdiction solely based on the use of correspondent accounts. The British men are accused of wiring dollar-denominated payments to Nigerian officials through a Gibraltar company, a Japanese trading company and Monégasque and Swiss banks. Because the transactions were dollar-denominated, U.S. authorities have asserted that these wire transfers must have cleared through a correspondent account at a U.S. bank.

Undercover sting operations: In the past 18 months, U.S. authorities have carried out two high-profile FCPA undercover sting operations, perhaps signaling a reemergence of traditional law enforcement techniques. The first was the William Jefferson case, which began after the former congressman was videotaped by the FBI receiving $100,000 in a briefcase and telling the investor, who was wearing a wire, that he would need to give the vice president of Nigeria $500,000 to ensure that their company won contracts in Nigeria.

The second instance was the SHOT Show case discussed above. During the sting operation, FBI agents taped 5,287 phone calls, collected more than 800 hours of video and audio recordings, and made 231 recordings of meetings between the undercover agents and defendants. The SHOT Show indictments, announced Jan. 19, charge 22 executives with engaging in a scheme to bribe the minister of defense of an unspecified African country in exchange for a portion of a $15 million contract to outfit the country’s presidential guard. This FCPA enforcement action constitutes a watershed case involving the “large-scale use of undercover law enforcement techniques” in connection with FCPA cases.

Following the large-scale SHOT Show sting, it is expected that U.S. authorities will continue to use sting operations in order to deter corruption. Indeed, as stated by Assistant Attorney General Lanny A. Breuer, “[f]rom now on, would-be FCPA violators should stop and ponder whether the person they are trying to bribe might really be a federal agent.”

Freezing the proceeds of bribery before trial: Another significant trend in FCPA prosecutions is the freezing of the proceeds of bribery before trial. Before the trial of the Greens, the government filed a superseding indictment that included criminal forfeiture allegations and made claims on the defendants’ home and pension fund. Similarly, in the matter of Victor Kozeny (the alleged promoter of the bribery scheme in Azerbaijan which ensnared Frederic Bourke), the DOJ sought and obtained a court order freezing the $23 million proceeds from the sale of Kozeny’s home in Aspen, Colo. Kozeny is currently a fugitive residing in the Bahamas.

OPINION PROCEDURE RELEASES

Opinion procedure releases are meant to assist companies in determining whether certain actions would violate the FCPA. The opinions are issued in response to requests by private parties. They can be relied upon only to the extent that the disclosure of facts and circumstances in a request is accurate and complete. An opinion procedure release has no binding application on any party that did not join in the request.

In 2009 companies made limited use of this mechanism to seek guidance from regulators, with only one opinion released, on Aug. 3, 2009. The opinion sought advice on a narrow issue regarding the donation of medical devices to private citizens. The limited use of the release process for the opinion procedure continues into 2010, with only one opinion having been released during the first half of the year.

The April 19 opinion involved the employment of a foreign official. Although the individual being compensated is a “foreign official” under the FCPA and will be compensated by the requesting company through a subcontractor, the individual at issue is being hired pursuant to an agreement with a U.S. governmental agency and the foreign country. Furthermore, the requesting company played no role in selecting the individual at issue for the position, and the individual at issue will not be in a position to influence any act or decision by the foreign country. As such, the requesting company has been informed that employment of this individual will not result in action by authorities.

A July 23 opinion involved a nonprofit microfinance institution. The institution is in the process of converting its local subsidiaries into licensed financial institutions. As a condition precedent to the approval of the transformation of its subsidiary in a “Eurasian country,” the Eurasian country’s regulatory body has demanded that the Eurasian subsidiary make a grant to one or more of six entities in the country.

Three rounds of due diligence were conducted, which eliminated five of the six entities, and it was discovered that a board member of the sixth entity was a governmental official. However, the governmental official does not work in an area related to the microfinance industry, and local law prohibits paying such a governmental official for board service.

AUGUST 16, 2010 n VOLUME 26 n ISSUE 4 | 7© 2010 Thomson Reuters

Furthermore, the institution proposed controls over the grant fund such as staggering payments, ongoing monitoring and auditing, earmarking funds for specific tasks, prohibiting the compensation of board members with monies from the grant and including anti-corruption compliance provisions. Based on the above circumstances, the DOJ has permitted the company to proceed without risking prosecution.

WHISTLE-BLOWER ‘BOUNTY’ PROGRAM

Recent legislation has established a new program that could provide the SEC with yet more resources in its efforts to investigate securities violations. On July 21 President Obama signed into law the Restoring American Financial Stability Act of 2010, which contains provisions that would allow whistle-blowers who report securities violations to recover a percentage of any settlement or sanction.

Under the law, a whistle-blower who provides original information leading to civil enforcement or criminal prosecution would be guaranteed to receive at least 10 percent of a sanction and could stand to receive up to 30 percent, so long as the sanction collected exceeds $1 million. The SEC would determine the amount of the reward based on various criteria, including the significance of the information and the level of cooperation provided by the individual.

The proposed provisions also extend the reward to actions taken by other prosecuting agencies, including the DOJ or foreign regulators, based on the reported information. The SEC has 270 days, until April 17, 2011, to prescribe rules to implement the new whistle-blower protections and award program.

It remains to be seen just how strong of an incentive this program could provide for employees who have information concerning potential violations of the FCPA or the impact on companies. On the one hand, the ability of regulators to affirmatively detect violations has increased by virtue of having “deputized” a whole cadre of potential whistle-blowers so as to add to their investigative ranks. On the other hand, it is equally likely that regulators may see an increase in the number of cases that are voluntarily disclosed. Indeed, for companies contemplating voluntary

disclosure, this type of incentive program introduces new variables to the calculus regarding whether alleged wrongdoing is otherwise likely to come to the attention of regulators.

INCREASED INTERNATIONAL COOPERATION

U.S. and foreign authorities are increasingly cooperating in the prosecution of bribery cases through the sharing of resources and evidence as well as the apprehension of suspected wrongdoers.

U.K. Bribery Act

Perhaps the most important anti-corruption development outside of the United States so far in 2010 was the April enactment of the Bribery Act in the United Kingdom. The Bribery Act will have far-reaching implications for every company doing business in the United Kingdom, since simply having a U.K. presence (subsidiary, office or operations) will create jurisdiction. It applies to both U.K. companies and foreign companies with operations in the United Kingdom, even if the offense takes place in a third country and is unrelated to the U.K. operations.

In many ways, the Bribery Act creates a platform for what could be the toughest enforcement regime in any country. There are some significant differences from the FCPA, since the Bribery Act criminalizes the giving and receiving of a bribe as well as the bribing of private companies or individuals.

In addition, unlike the FCPA, there is no need to prove corrupt intent under the Bribery Act, there is no exception for facilitating payments, there is strict liability for corporations that fail to prevent bribery and the extraterritorial reach has a broader impact for companies and individuals.

Like the FCPA, penalties under the Bribery Act can be severe. The only defense available to commercial organizations charged with violating the Bribery Act will be for the organization to show that it had in place “adequate procedures” to prevent an act of bribery being committed in connection with its business. The phrase “adequate procedures” is not defined in the Bribery Act, but it is widely acknowledged that compliance procedures will be subject to intense scrutiny.

The Ministry of Justice announced July 20 that the implementation of the Bribery Act

will be delayed until April 2011 (it had been expected to come into force in October) so that guidance on “adequate procedures” can be provided before the law goes into effect.

Increased recognition of the pitfalls of corruption

In May the Obama administration announced that as part of its National Security Strategy, the United States will “work within the broader international system, including the U.N. [United Nations], G-20 [Group of 20], Organization for Economic Cooperation and Development (OECD) and the international financial institutions, to promote the recognition that pervasive corruption is a violation of basic human rights and a severe impediment to development and global security.”

Echoing the same sentiments as the Obama administration, the G-20 leaders issued strong anti-corruption statements June 27. The statements evidenced a clear recognition that corruption threatens the integrity of markets, destroys public trust and undermines the rule of law.

Although it is not yet clear to what degree these strong words will be accompanied by tangible action, the G-20 did create a working group to provide recommendations regarding practical international efforts to combat corruption. The working group will focus on the adoption and enforcement of anti-bribery rules, barring corrupt persons from global financial systems, protecting whistle-blowers and promoting international cooperation in visa denial, extradition and recovery of the assets of corrupt persons. The findings and recommendations of the anti-corruption working group are to be presented at the November G-20 summit in Seoul, South Korea.

Cross-border enforcement

Cross-border regulatory cooperation increases the likelihood that individuals and companies will be subject to enforcement actions in multiple jurisdictions. In addition to cross-border coordination in evidence gathering, international cooperation is increasingly resulting in multi-jurisdictional enforcement proceedings.

On Feb. 5 BAE Systems PLC settled charges with both U.S. authorities and the U.K.’s Serious Fraud Office. Under its agreement with the SFO, BAE will plead guilty to one count of breach of duty to keep accounting

8 | WESTLAW JOURNAL n CORPORATE OFFICERS & DIRECTORS LIABILITY © 2010 Thomson Reuters

records in relation to payments made to a former marketing advisor in Tanzania and will pay a penalty of £30 million (about $47 million). This penalty assessed against BAE by the SFO is to cover a judicially assessed penalty, with any remaining balance to be paid as a charitable donation for the benefit of Tanzania.

Similarly, as previously discussed, pursuant to its global settlement in March, Innospec will pay $40.2 million ($27.5 million in fines and disgorgement to U.S. authorities and a $12.7 million criminal fine to the SFO). The DOJ and the SFO have credited each other with assisting in the investigations. The Innospec case has been described as the first instance of a cross-border global settlement of corruption charges, but it may be the last.

Although the agreement was ultimately approved, two different U.K. judges criticized the global settlement as insufficient in light of the wrongdoing, over-reaching by the SFO and an improper restriction on judicial authority. Therefore, it remains unclear whether or not global settlements will continue to be available to companies facing corruption charges in both the United Kingdom and the United States.

KEY LESSONS AND EXPECTATIONS FOR THE FUTURE

It is expected that increased FCPA enforcement will continue in the second half of 2010 and beyond. The trends in FCPA enforcement that have emerged in the recent past are likely to continue into the future, including:

• More focused prosecution of individual wrongdoers.

• Increased civil and criminal penalties.

• Broadening definition of culpable intent.

• Continued push to expand jurisdictional reach.

• More sector-wide investigations.

• Increased use of traditional law enforcement techniques such as sting operations.

• Enhanced international cooperation in the prosecution of corruption.

Indeed, going forward, corporations and individuals can expect to face an ever more rigorous and hostile regulatory environment. Therefore, it is critical for companies and corporate officers to be aware of areas of potential risk and take a proactive approach, with particular attention paid to third-party agents, corporate combinations, entertainment expenses and infrastructure projects.

In the event that a company learns of a potential FCPA violation, it must act promptly and efficiently to minimize the impact on its business, to prevent further infractions and to uncover the scope of the problem. WJ

NOTES1 15U.S.C.§§ 78dd-1(a).

2 15U.S.C.§§ 78m(b)(2).

3 15U.S.C.§§ 78m(b)(5).

4 15U.S.C.§§ 78dd-2(g).

5 SeeCommentsofAssistantAttorneyGeneralLannyA.Breuerbeforethe22ndNationalForumontheFCPA,Nov.17,2009,http://www.docstoc.com/docs/39515039/Lanny-A-Breuer-Assistant-Attorney-General-Criminal-Division.

6 Inarelatedissue,aproposedamendmenttothesentencingguidelines(Section8B2.1,subsection(b)(7))wouldrecognizeretaininganoutsideprofessionalcomplianceadviserasapartofaneffectivecomplianceprogramthatcanassistinthedetectionofFCPAviolationsandthereforeavoidthemoststringentsanctions.Althoughanadviserisnotthesameasamonitor,thereisapossibilitythattheretentionoftheformermaystaveofftheimpositionofthelatter.

7 Therearecurrently157debarredfirmsorindividuals.Seehttp://web.worldbank.org/external/default/main?theSitePK=84266&contentMDK=64069844&menuPK=116730&pagePK=64148989&piPK=64148984.

8 Seehttp://web.worldbank.org/WBSITE/EXTERNAL/NEWS/0,,contentMDK:22034560~pagePK:34370~piPK:34424~theSitePK:4607,00.html.

9 Seehttp://web.worldbank.org/WBSITE/EXTERNAL/NEWS/0,,contentMDK:22034560~pagePK:34370~piPK:34424~theSitePK:4607,00.html.

10 Section20(a)oftheSecurityExchangeActprovidesthatanyone“whodirectly,orindirectly,controlsanypersonliable”isalsoliabletotheextentthatheorshecontrolledsuchacontrolledperson.

11 IntheNature’sSunshinecase,theSECchargedtwoexecutiveswithFCPAviolationsarisingfromtheactsoftheirsubordinateswithoutallegingthattheexecutiveswerecomplicitin,orevenawareof,themisconduct.Becausethepartiessettled,itisunclearhowsuccessfulthetheoryof“controlperson”liabilityinaFCPAactionwouldbebeforeajuryoracourt.

12 IntheUnitedIndustrialCorp.case,theSECassertedthataparentcorporationwasliablefortheFCPAviolationsofitswhollyownedsubsidiary.TheSECneverallegedthattheUIChadanydirectknowledgethatitwasviolatingtheFCPA.Instead,theSECseemstohaveconcludedthatoneexecutive’sinvolvementwassufficienttoimposeconstructiveknowledgeofwrongdoingtotheparentcompany,therebytriggeringviolationoftheFCPA.Again,thefactthatthistheoryofliabilitywasnottestedincourtleavesopensomequestionsregardingtheviabilityofthistheoryinthefuture.

Kiera S. Gans is an associate in the litigation practice group of DLA Piper in New York. She has extensive experience in conducting multi-jurisdictional investigations for clients in the defense, financial services, aerospace and telecommunications industries in Latin America, Europe, the Middle East and Asia. Robert A. Johnston Jr., also an associate in the litigation practice group, has represented public and nonpublic companies in commercial disputes, regulatory enforcement defense, internal investigations, employment litigation and contract renegotiations and has advised both domestic and foreign companies in their efforts to comply with anti-bribery laws.

AUGUST 16, 2010 n VOLUME 26 n ISSUE 4 | 9© 2010 Thomson Reuters

COMMENTARY

Dodd-Frank law expands whistle-blower provisions of Sarbanes-Oxley ActBy Steven Pearlman, Esq.

On July 21, President Obama signed the Dodd-Frank Wall Street Reform and Consumer Protection Act (H.R. 4173) into law. This act eliminates a number of defenses upon which employers have relied in defeating whistle-blower claims under the Sarbanes-Oxley Act of 2002, offers bounties designed to encourage employees to “blow the whistle” on fraud and creates new private rights of action.

EXPANSION OF PROVISIONS FOR WHISTLE-BLOWER PROTECTION

Sections 922 and 929A significantly expand the provisions for whistle-blower protection in Section 806 of Sarbanes-Oxley by:

• Covering private subsidiaries or affiliates of publicly traded companies whose financial information is included in the consolidated financial statements of such companies and covering nationally recognized statistical rating organizations.

• Increasing the current 90-day statute of limitations to 180 days.

• Providing a right to a jury trial in Sarbanes-Oxley actions removed to federal district courts.

• Prohibiting pre-dispute arbitration agreements and any other “agreement, policy, form, or condition of employment” that requires a waiver of rights under Sarbanes-Oxley.

REWARDS FOR BLOWING THE WHISTLE

Section 922 amends the Securities Exchange Act of 1934 by including a provision requiring the Securities and Exchange Commission to provide a monetary award to individuals who provide “original information” to the SEC that results in sanctions exceeding $1 million. The SEC has discretion to award between 10 percent and 30 percent of the total amount of the sanctions.

Such bounties are not available to individuals who are convicted of criminal violations

related to the action for which the whistle-blower provided information or to individuals who obtain the information through audits of financial statements required by securities laws and for whom submission would be contrary to the requirements of Section 10A of the Exchange Act.

Likewise, employees of an appropriate regulatory agency, the Department of Justice, a self-regulatory agency, the Public Company Accounting Oversight Board or a law enforcement organization are ineligible for such awards.

Also, Section 922 affords whistle-blowers a private right of action that they may pursue directly in federal court. This right presents a stark contrast to Sarbanes-Oxley actions, which require an employee to exhaust administrative remedies by first filing a claim with the Occupational Safety and Health Administration.

Successful employees may obtain substantial remedies, including reinstatement without loss of seniority, double back pay, reasonable attorney fees, costs and expert-witness fees.

Further, the lengthy statute of limitations under Section 922 is particularly noteworthy. It affords an employee up to six years after the violation occurred, or three years after he or she knew or reasonably should have known of facts material to the violation, so long as the complaint is filed within 10 years after the violation.

In addition, Section 748 amends the Commodity Exchange Act to provide incentives to whistle-blowers in a manner that is substantially similar to the amendments that Section 922 makes to the Exchange Act. However, this section contains a two-year statute of limitations.

Awards under Section 748 are not available to any employee of an appropriate regulatory agency, the Justice Department, a registered entity, a registered futures association or a self-regulatory organization (as defined in Section 3[a] of the Exchange Act).

WHISTLE-BLOWER PROTECTION FOR EMPLOYEES OF FINANCIAL SERVICES ORGANIZATIONS

Section 1057 creates a cause of action for employees who perform tasks related to the offering or provision of a consumer financial product or service. This section protects employees who engage in the following conduct:

• Providing information to an employer, the Bureau of Consumer Financial Protection or any state, local or federal government authority or law enforcement agency relating to the violation of consumer financial protection laws at issue in this statute or that are subject to the bureau’s jurisdiction.

• Testifying in a proceeding against an employer resulting from the enforcement of consumer protection laws at issue in this statute or law that are subject to the bureau’s jurisdiction; or

• Helping to initiate any proceeding of consumer financial protection laws at issue in this statute and objecting or refusing to participate in any activity that the employee reasonably believes to violate any law subject to the bureau’s jurisdiction.

A claim under this section must be filed with the Department of Labor (specifically, with OSHA) within 180 days. A complainant has the option of proceeding through the DOL (i.e., appealing to an administrative law judge and then to the administrative review board) or removing the claim to a federal district court within 210 days after the filing of the complaint if the DOL has not issued a final order within that timeframe.

The new law offers bounties to encourage

employees to “blow the whistle” on fraud.

10 | WESTLAW JOURNAL n CORPORATE OFFICERS & DIRECTORS LIABILITY © 2010 Thomson Reuters

Claims under this section may not be waived by any agreement, policy, form or condition of employment, including by any pre-dispute arbitration agreement.

WHAT SHOULD EMPLOYERS DO?

The bounty provisions, expansion of Sarbanes-Oxley coverage and statute of limitations, and the new private rights of action created under the Dodd-Frank Act require employers to take calculated steps to minimize the risk of whistle-blower claims.

Indeed, employers need to ensure that, where practicable, whistle-blower claims are resolved internally, since employees

now have a unique incentive (in the form of a bounty) to report perceived misconduct to third parties such as the SEC, even before an employer may adequately address their concerns.

Thus, employers are compelled to implement sophisticated complaint hot lines and provide multiple avenues through which employees can report perceived misconduct without fear of retaliation.

Likewise, employers, including both publicly traded companies and their private subsidiaries and affiliates, need to promulgate appropriate codes of ethics and anti-retaliation policies and train managers to be receptive and responsive to employee complaints.

Further, on a broader scale, management should adopt leadership models that foster a culture of integrity and accountability throughout the organization. Management should do so with an eye toward encouraging employees to raise complaints internally rather than to third parties. WJ

Steven Pearlman, a partner in the labor and employment area of Seyfarth Shaw LLP in Chicago, regularly defends companies against Sarbanes-Oxley whistle-blower claims before federal courts in addition to the Department of Labor. He can be reached at [email protected].

Employers should encourage employees to settle complaints

internally rather than involve third parties.

SUBPRIME/MORTGAGE-BACKED SECURITIES

New York pension funds sue Merrill Lynch for subprime fraudA New York public employee pension fund has sued investment bank Merrill Lynch for allegedly hiding its exposure to risky subprime mortgages while selling overpriced shares during a two-year period ending in 2008.

DiNapoli v. Merrill Lynch & Co. et al., No. 10-CV-5562, complaint filed (S.D.N.Y. July 22, 2010).

The suit, filed by New York Comptroller Thomas P. DiNapoli on behalf of the fund, alleges Merrill Lynch, ex-CEO E. Stanley O’Neal and former CFO Jeffrey N. Edwards violated the Securities Exchange Act of 1934, 15 U.S.C. §§ 78j(b) and 78t(a).

The defendants “brashly ignored” known risks while “recklessly and exponentially intensifying Merrill’s subprime lending,” according to the complaint filed in the U.S. District Court for the Southern District of New York.

As the firm gradually revealed the truth about its financial predicament, its share price declined from about $76 to $11 between October 2007 and December 2008, the suit says.

The fund bought nearly 5 million shares during that time, it says.

The suit details Merrill’s “reckless” foray into subprime investments, from direct mortgage lending to “toxic” financial derivatives, including collateralized debt obligations, so-called “synthetic” CDOs and credit default swaps.

Merrill eventually wrote down $31.8 billion in subprime investments, the suit says.

“Investors, like the fund, can tolerate risk — it’s what we do — but we cannot tolerate this kind of corporate irresponsibility,” DiNapoli said in a statement.

In a deal allegedly brokered by federal officials, Merrill avoided collapse by merging with Bank of America in January 2009.

DiNapoli separately sued Bank of America, alleging fraud in connection with the merger. DiNapoli v. Bank of Am., No. 10-CV-5563, complaintfiled (S.D.N.Y. July 22, 2010).

“These companies thought they could get away with profiting at the expense of New York’s pensioners and taxpayers through fraudulent activities and misleading public disclosures, and they were mistaken,” DiNapoli said.

Attorneys:Plaintiff:AndrewJ.Entwistle,JohnstondeF.WhitmanJr.,JonathanH.Beemer,JoshuaK.PorterandJordanA.Cortez,Entwistle&Cappucci,NewYork

Related Court Documents: Complaint:2010WL2967301

AUGUST 16, 2010 n VOLUME 26 n ISSUE 4 | 11© 2010 Thomson Reuters

SUBPRIME

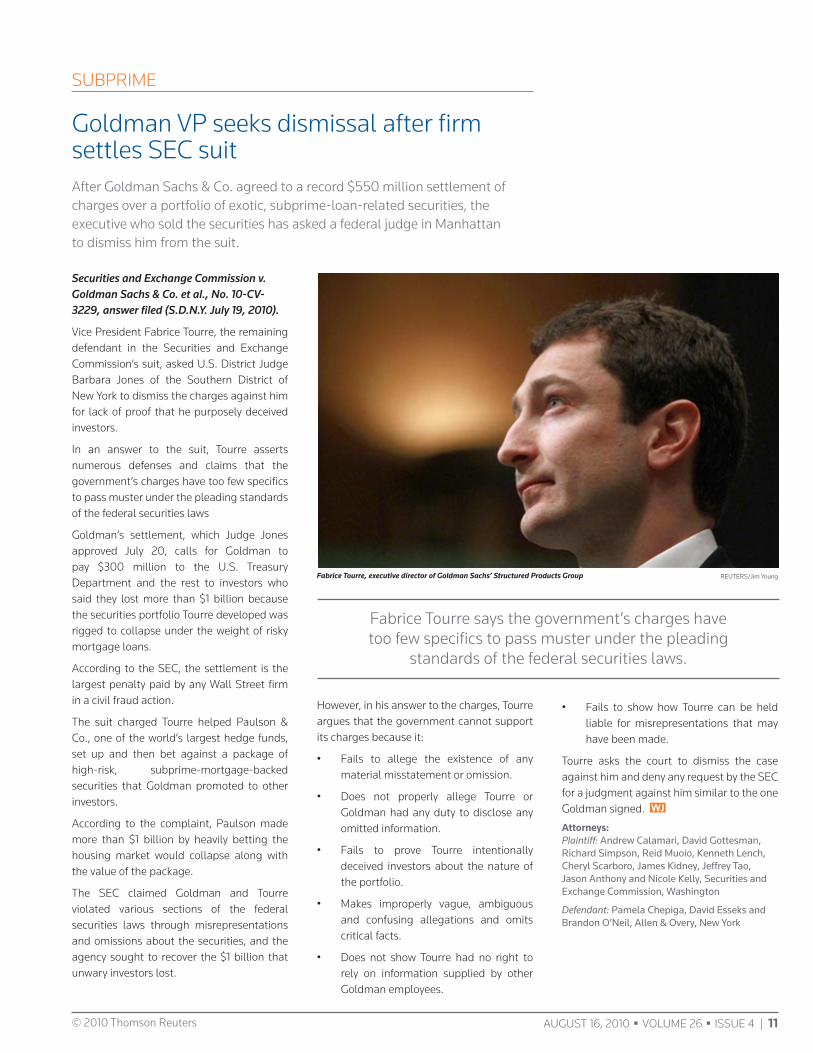

Goldman VP seeks dismissal after firm settles SEC suit After Goldman Sachs & Co. agreed to a record $550 million settlement of charges over a portfolio of exotic, subprime-loan-related securities, the executive who sold the securities has asked a federal judge in Manhattan to dismiss him from the suit.

Securities and Exchange Commission v. Goldman Sachs & Co. et al., No. 10-CV-3229, answer filed (S.D.N.Y. July 19, 2010).

Vice President Fabrice Tourre, the remaining defendant in the Securities and Exchange Commission’s suit, asked U.S. District Judge Barbara Jones of the Southern District of New York to dismiss the charges against him for lack of proof that he purposely deceived investors.

In an answer to the suit, Tourre asserts numerous defenses and claims that the government’s charges have too few specifics to pass muster under the pleading standards of the federal securities laws

Goldman’s settlement, which Judge Jones approved July 20, calls for Goldman to pay $300 million to the U.S. Treasury Department and the rest to investors who said they lost more than $1 billion because the securities portfolio Tourre developed was rigged to collapse under the weight of risky mortgage loans.

According to the SEC, the settlement is the largest penalty paid by any Wall Street firm in a civil fraud action.

The suit charged Tourre helped Paulson & Co., one of the world’s largest hedge funds, set up and then bet against a package of high-risk, subprime-mortgage-backed securities that Goldman promoted to other investors.

According to the complaint, Paulson made more than $1 billion by heavily betting the housing market would collapse along with the value of the package.

The SEC claimed Goldman and Tourre violated various sections of the federal securities laws through misrepresentations and omissions about the securities, and the agency sought to recover the $1 billion that unwary investors lost.

However, in his answer to the charges, Tourre argues that the government cannot support its charges because it:

• Fails to allege the existence of any material misstatement or omission.

• Does not properly allege Tourre or Goldman had any duty to disclose any omitted information.

• Fails to prove Tourre intentionally deceived investors about the nature of the portfolio.

• Makes improperly vague, ambiguous and confusing allegations and omits critical facts.

• Does not show Tourre had no right to rely on information supplied by other Goldman employees.

• Fails to show how Tourre can be held liable for misrepresentations that may have been made.

Tourre asks the court to dismiss the case against him and deny any request by the SEC for a judgment against him similar to the one Goldman signed. WJ

Attorneys: Plaintiff: AndrewCalamari,DavidGottesman,RichardSimpson,ReidMuoio,KennethLench,CherylScarboro,JamesKidney,JeffreyTao,JasonAnthonyandNicoleKelly,SecuritiesandExchangeCommission,Washington

Defendant: PamelaChepiga,DavidEsseksandBrandonO’Neil,Allen&Overy,NewYork

REUTERS/Jim Young

Fabrice Tourre says the government’s charges have too few specifics to pass muster under the pleading

standards of the federal securities laws.

Fabrice Tourre, executive director of Goldman Sachs’ Structured Products Group

12 | WESTLAW JOURNAL n CORPORATE OFFICERS & DIRECTORS LIABILITY © 2010 Thomson Reuters

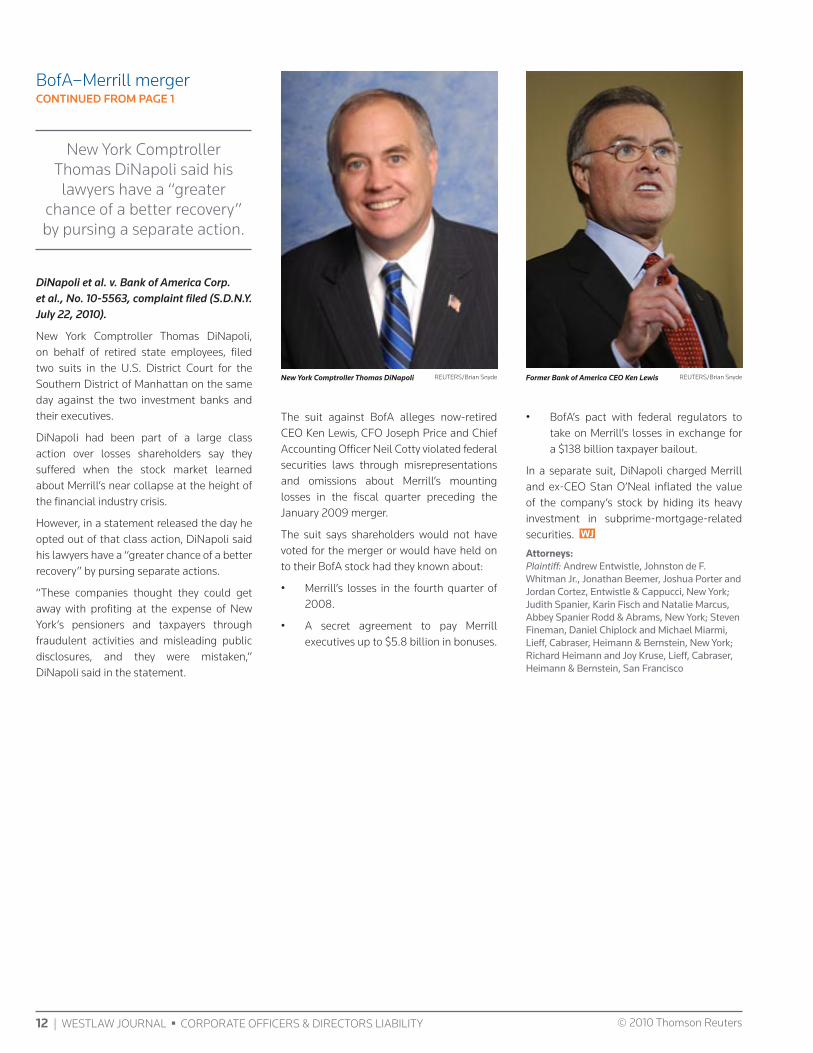

DiNapoli et al. v. Bank of America Corp. et al., No. 10-5563, complaint filed (S.D.N.Y. July 22, 2010).

New York Comptroller Thomas DiNapoli, on behalf of retired state employees, filed two suits in the U.S. District Court for the Southern District of Manhattan on the same day against the two investment banks and their executives.

DiNapoli had been part of a large class action over losses shareholders say they suffered when the stock market learned about Merrill’s near collapse at the height of the financial industry crisis.

However, in a statement released the day he opted out of that class action, DiNapoli said his lawyers have a “greater chance of a better recovery” by pursing separate actions.

“These companies thought they could get away with profiting at the expense of New York’s pensioners and taxpayers through fraudulent activities and misleading public disclosures, and they were mistaken,” DiNapoli said in the statement.

BofA–Merrill mergerCONTINUED FROM PAGE 1

The suit against BofA alleges now-retired CEO Ken Lewis, CFO Joseph Price and Chief Accounting Officer Neil Cotty violated federal securities laws through misrepresentations and omissions about Merrill’s mounting losses in the fiscal quarter preceding the January 2009 merger.

The suit says shareholders would not have voted for the merger or would have held on to their BofA stock had they known about:

• Merrill’s losses in the fourth quarter of 2008.

• A secret agreement to pay Merrill executives up to $5.8 billion in bonuses.

• BofA’s pact with federal regulators to take on Merrill’s losses in exchange for a $138 billion taxpayer bailout.

In a separate suit, DiNapoli charged Merrill and ex-CEO Stan O’Neal inflated the value of the company’s stock by hiding its heavy investment in subprime-mortgage-related securities. WJ

Attorneys: Plaintiff: AndrewEntwistle,JohnstondeF.WhitmanJr.,JonathanBeemer,JoshuaPorterandJordanCortez,Entwistle&Cappucci,NewYork;JudithSpanier,KarinFischandNatalieMarcus,AbbeySpanierRodd&Abrams,NewYork;StevenFineman,DanielChiplockandMichaelMiarmi,Lieff,Cabraser,Heimann&Bernstein,NewYork;RichardHeimannandJoyKruse,Lieff,Cabraser,Heimann&Bernstein,SanFrancisco

REUTERS/Brian SnydeREUTERS/Brian SnydeNew York Comptroller Thomas DiNapoli Former Bank of America CEO Ken Lewis

New York Comptroller Thomas DiNapoli said his lawyers have a “greater

chance of a better recovery” by pursing a separate action.

AUGUST 16, 2010 n VOLUME 26 n ISSUE 4 | 13© 2010 Thomson Reuters

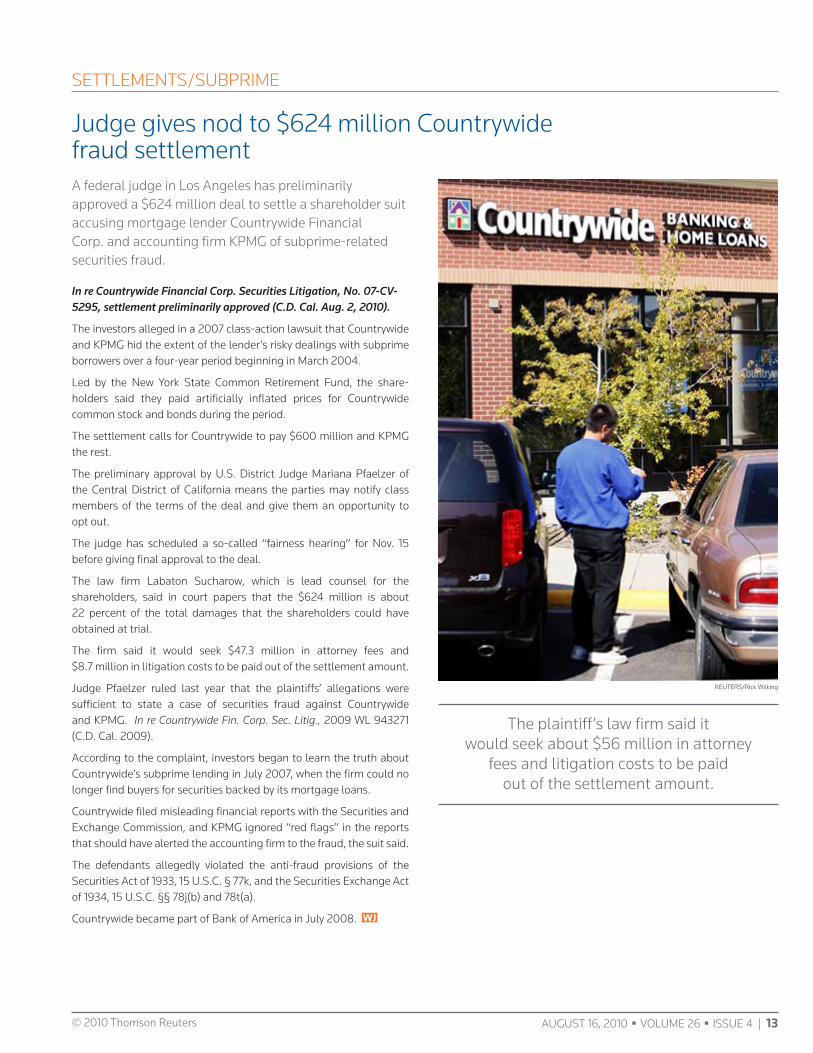

SETTLEMENTS/SUBPRIME

Judge gives nod to $624 million Countrywide fraud settlementA federal judge in Los Angeles has preliminarily approved a $624 million deal to settle a shareholder suit accusing mortgage lender Countrywide Financial Corp. and accounting firm KPMG of subprime-related securities fraud.

In re Countrywide Financial Corp. Securities Litigation, No. 07-CV-5295, settlement preliminarily approved (C.D. Cal. Aug. 2, 2010).

The investors alleged in a 2007 class-action lawsuit that Countrywide and KPMG hid the extent of the lender’s risky dealings with subprime borrowers over a four-year period beginning in March 2004.

Led by the New York State Common Retirement Fund, the share-holders said they paid artificially inflated prices for Countrywide common stock and bonds during the period.

The settlement calls for Countrywide to pay $600 million and KPMG the rest.

The preliminary approval by U.S. District Judge Mariana Pfaelzer of the Central District of California means the parties may notify class members of the terms of the deal and give them an opportunity to opt out.

The judge has scheduled a so-called “fairness hearing” for Nov. 15 before giving final approval to the deal.

The law firm Labaton Sucharow, which is lead counsel for the shareholders, said in court papers that the $624 million is about 22 percent of the total damages that the shareholders could have obtained at trial.

The firm said it would seek $47.3 million in attorney fees and $8.7 million in litigation costs to be paid out of the settlement amount.

Judge Pfaelzer ruled last year that the plaintiffs’ allegations were sufficient to state a case of securities fraud against Countrywide and KPMG. InreCountrywideFin.Corp.Sec.Litig., 2009 WL 943271(C.D. Cal. 2009).

According to the complaint, investors began to learn the truth about Countrywide’s subprime lending in July 2007, when the firm could no longer find buyers for securities backed by its mortgage loans.

Countrywide filed misleading financial reports with the Securities and Exchange Commission, and KPMG ignored “red flags” in the reports that should have alerted the accounting firm to the fraud, the suit said.

The defendants allegedly violated the anti-fraud provisions of the Securities Act of 1933, 15 U.S.C. § 77k, and the Securities Exchange Act of 1934, 15 U.S.C. §§ 78j(b) and 78t(a).

Countrywide became part of Bank of America in July 2008. WJ

REUTERS/Rick Wilking

The plaintiff’s law firm said it would seek about $56 million in attorney

fees and litigation costs to be paid out of the settlement amount.

14 | WESTLAW JOURNAL n CORPORATE OFFICERS & DIRECTORS LIABILITY © 2010 Thomson Reuters

SETTLEMENTS/SUBPRIME

$125 million settlement reached in New Century subprime caseNew Century shareholders have asked a federal judge in Los Angeles to approve a $125 million settlement of a securities fraud suit against former executives, underwriters and auditor of the now-bankrupt mortgage lender.

Judge Pregerson dismissed the investors’ original complaint in January 2008. Goldv.Morrice, 2008 WL 467619 (C.D. Cal. 2008).

They filed a 372-page amended complaint that relied in part on a bankruptcy examiner’s lengthy report detailing events leading to New Century’s 2007 collapse.

The judge ruled in December 2008 that the amended suit met federal pleading standards for securities fraud. In re NewCenturyFin.Corp.(Goldv.Morrice), 2008 WL 5147991 (C.D. Cal. 2008).

The suit said the defendants violated the anti-fraud provisions of the Securities Exchange Act of 1934, 15 U.S.C. § 78j(b), and Sections 11 and 12 of the Securities Act of 1933, 15 U.S.C. § 77(k). WJ

Attorneys: Plaintiffs: BlairA.Nicholas,ElizabethLin,NikiL.Mendoza,BenjaminGaldstonandTakeoA.Kellar,BernsteinLitowitzBerger&Grossmann,SanDiego;SalvatoreJ.GrazianoandLaurenA.McMillen,BernsteinLitowitzBerger&Grossmann,NewYork

Related Court Documents: Memoinsupportofsettlement:2010WL3054214

REUTERS/Fred Prouser

In re New Century Financial Corp. (Gold v. Morrice), No. 07-CV-931, memo supporting settlement filed (C.D. Cal. July 30, 2010).

The 2007 class-action suit alleged that former CEO Brad Morrice and ex-CFOs Patti Dodge and Edward Gotschall hid the company’s subprime loan losses while selling overpriced shares.

Numerous New Century directors, loan underwriters and auditor KPMG also were defendants in the suit, filed in the U.S. District Court for the Central District of California.

Irvine, Calif.-based New Century was not named because it has been under bankruptcy protection since April 2007.

The lead plaintiff, the New York State Teachers Retirement System, was seeking compensation on behalf of all investors who bought New Century common and preferred stock between May 2005 and March 2007.

In a recent memo NYSTRS asked U.S. District Judge Dean Pregerson to approve a settlement calling for the officers and directors to pay $65 million, KPMG about $45 million, and the underwriters $15 million.

“The proposed settlements represent an outstanding result for plaintiffs and the class, particularly in light of New Century’s bankruptcy and the risks to the class if the action continued, including … the risks that there would be significantly less funds available to satisfy any judgment or post-trial settlement,” the memo says.

The lead plaintiff is seeking compensation for all investors who bought

New Century stock between May 2005 and March 2007.

AUGUST 16, 2010 n VOLUME 26 n ISSUE 4 | 15© 2010 Thomson Reuters

SETTLEMENTS/SUBPRIME

Robert Khuzami said in a statement.

Citigroup allegedly violated Section 17(a)(2) of the Securities Act of 1933, 15 U.S.C. § 77q(a)(2); Section 13(a) of the Securities Exchange Act of 1934, 15 U.S.C. § 78m(a); and Exchange Act Rules 12b-20 and 13a-11m, 17 C.F.R. §§ 240.12b-20 and 240.13a-11.

In related administrative charges, the SEC alleged that one current and one former executive caused Citigroup to make the misleading statements in an agency filing.

Cross-marketing chief Arthur Tildesley Jr. and former CFO Gary Crittenden agreed to pay $80,000 and $100,000, respectively, to settle the charges, the SEC said in a statement.

They allegedly caused Citigroup to violate Section 13(a) of the Exchange Act and Exchange Act Rules 12b-20 and 13a-11m.

In settling they neither admitted nor the denied the allegations. WJ

Related Court Documents: Complaint:2010WL3017640

REUTERS/Jim YoungSEC Enforcement Division Director Robert Khuzami

Securities and Exchange Commission v. Citigroup Inc., No. 10-CV-1277, complaint filed (D.D.C. July 29, 2010).

In a complaint filed in the U.S. District Court for the District of Columbia, the SEC said Citigroup repeatedly made misleading statements between July 20, 2007, and Nov. 4, 2007, about the extent of its holdings of assets backed by subprime mortgages.

The agency simultaneously filed an agreement in which Citigroup, without admitting or denying the allegations, consented to pay the fine.

The settlement is subject to the approval of U.S. District Judge Ellen S. Huvelle.

According the complaint, Citigroup said in public filings and conference calls with market analysts that the subprime exposure in its investment banking unit, Citi Markets & Banking, was $13 billion or less. In fact, the exposure was nearly $55 billion, the complaint said.

The $13 billion figure allegedly was misleading because it omitted Citigroup’s exposure to mortgage-backed debt by way of “liquidity puts.” The puts functioned as a guarantee by the bank that investors would be paid even if the mortgage market declined, the suit said.

Citigroup made the alleged misleading disclosures at a time of heightened investor and analyst interest in public-company exposure to subprime mortgages, the suit said.

“The rules of financial disclosure are simple — if you choose to speak, speak in full and not in half-truths,” SEC Enforcement Director

Citigroup allegedly concealed “liquidity puts” that exposed

it to about $40 billion in mortgage-backed debt.

Mortgage insurer PMI settles subprime suit for $31 millionPMI Group and top executives have agreed to pay $31 million to settle a subprime-related fraud suit alleging they misled shareholders about the mortgage insurer’s subprime risks.

In re PMI Group Inc. Securities Litigation, No. 08-CV-1405, settlement announced (N.D. Cal. July 19, 2010).

The 2008 suit accused the Walnut Creek, Calif.-based company of hiding its underwriting of risky subprime loans while selling overpriced common stock. Investors allegedly lost millions of dollars as PMI’s share price collapsed when the truth came out.

The executives named in the suit are CEO L. Stephen Smith, CFO Donald P. Lofe Jr., COO David H. Katkov and President Bradley M. Shuster.

The plaintiffs announced the settlement July 19 in papers asking U.S. District Judge Susan Illston of the Northern District of California to cancel a pending case-management conference.

In an Aug. 3 filing with the Securities and Exchange Commission, PMI disclosed the settlement amount and indicated that its insurers will pay it.

“The proposed settlement does not involve any admission of wrongdoing or liability, and PMI Group and the individual defendants will receive a full and complete release of all claims asserted against them in the litigation,” the filing said.

“Defendants will have the option to terminate the settlement if 4 percent or more of the class members or shares opt out of the settlement class,” it said.

Citigroup to pay $75 million to settle SEC suitCitigroup has agreed to pay a $75 million fine to settle the Securities and Exchange Commission’s charges that the bank misled investors in 2007 about its exposure to subprime-mortgage-related assets.

PMI shares allegedly fell from about $50 to $6 each

during the class period.

16 | WESTLAW JOURNAL n CORPORATE OFFICERS & DIRECTORS LIABILITY © 2010 Thomson Reuters

Judge Illston tossed the original complaint, saying the allegations failed to show that the executives intended to deceive the shareholders. In re PMI Group Sec. Litig., 2009 WL 1916934 (N.D. Cal. 2009).

But last November she ruled that an amended complaint met federal pleading standards for securities fraud. In re PMI

Group Sec. Litig., 2009 WL 3681669 (N.D. Cal. 2009).

The suit accused the defendants of violating the anti-fraud provisions of the Securities Exchange Act of 1934, 15 U.S.C. §§ 78j(b) and 78t(a).

The plaintiffs sought compensation on behalf of a class of investors who bought

PMI’s shares between November 2006 and March 2008, when the company revealed the full extent of its losses for 2007, about $1.1 billion.

PMI shares fell from about $50 to $6 each during the class period, according to the suit. WJ

POISON PILLS

Both parties appeal parts of ruing on potent poison pill The Delaware Supreme Court heard argument July 7 on multiple issues in an appeal over Selectica Inc.’s use of a novel poison pill against rival software developer Trilogy Inc.’s proxy contest to unseat Selectica’s directors.

Versata Enterprises Inc. et al. v. Selectica Inc. et al., No. 193-2010, oral argument held (Del. July 7, 2010).

The main issue in the appeal is whether the Chancery Court wrongly allowed Selectica’s directors to use a hair-trigger poison pill along with a “staggered board” defense to make it realistically impossible for investors to unseat them in a proxy contest.

A staggered-board defense ensures that a majority of the company’s directors are never up for re-election at one time. This prevents a hostile suitor or dissident shareholder from quickly gaining control of the board through a proxy contest.

AN UNUSUAL PILL

Trilogy subsidiary Versata Enterprises Inc. is appealing a poison-pill ruling it calls precedent-setting because it purportedly allowed Selectica to use an unusually potent version of that takeover defense not justified by the threat Trilogy’s stock purchase posed.

Meanwhile, Selectica is appealing Vice Chancellor John Noble’s denial of its request to force Trilogy to pay for part of the litigation it allegedly caused by threatening to intentionally trigger a poison-pill provision that could have cost Selectica “tens of millions of dollars.”

A poison pill, also known as a shareholder rights plan, deters unwelcome suitors from acquiring more than a set percentage of the target firm by threatening to explode into thousands of new, discount-priced shares of stock for all investors except the suitor, thus making control too costly.

Shareholders can ask the court to strike down the plan if they can show it is an unnecessarily restrictive defensive tactic in proportion to the threat posed by the proposed transaction.

Vice Chancellor Noble’s opinion in this case was the first to address the use of a pill to protect net operating losses, accumulated tax credits awarded to companies that have lost money in past years. In addition the pill had an unusually low trigger point.

Since Selectica had been losing money for years, it had accumulated $160 million in NOL credits that a profitable acquirer like Versata could use to offset its taxes.

But the Selectica directors were not interested in Versata’s merger offer and lowered the pill’s trigger point from 15 percent to 4.99 percent of Selectica’s stock to keep it at arm’s length.

Versata claimed the unusually low trigger for the pill meant it would explode long before any suitor acquired enough stock to become a takeover threat.

Selectica then sought a Chancery Court ruling that its action was valid.

Vice Chancellor Noble said the combination of the pill and other defenses was formidable but did not make a shareholder vote to change the directors impossible, so he refused to invalidate them.

IMPREGNABLE DEFENSE?

The issue in Versata’s appeal is whether the combination of the poison pill and a staggered-board defense left dissident shareholders like itself with no chance of changing company policy by replacing the incumbent directors.

Selectica’s cross-appeal claims that it was forced to bring this action, seeking a declaration that its pill was valid, because Versata used its proxy contest to threaten the value of the NOLs by intentionally triggering the pill.

“[Versata parent] Trilogy sought to employ the shareholder franchise intentionally to impair Selectica’s corporate assets or else to coerce the company into meeting certain business demands,” Selectica argued in its reply brief in support of its cross-appeal.

The high court normally rules on appeals within 90 days. WJ

Attorneys: Plaintiffs: GregoryVarallo,LisaSchmidt,JohnHendershot,EthanShaner,ScottPerkinsandJillianRemming,RichardsLayton&Finger,Wilmington,Del.

Defendants: MeganCascio,LesliePolizotiandRyanStottmann,Morris,Nichols,Arsht&Tunnell,Wilmington;NicholasEvenandDanielGold,Haynes&Boone,Dallas

Related Court Documents: Replybrief:2010WL2751682

AUGUST 16, 2010 n VOLUME 26 n ISSUE 4 | 17© 2010 Thomson Reuters

BOOKS & RECORDS

Records action not an end run around discovery rules, plaintiff’s appeal saysA VeriFone Holdings shareholder wants Delaware’s high court to reverse a ruling that bars an investor from filing a records-inspection action in the Chancery Court if he has already sued the company’s directors for breach of duty in another court.

King v. VeriFone Holdings Inc., No. 330-2010, opening brief filed (Del. July 19, 2010).

The Chancery Court dismissed Charles King’s suit to get information about VeriFone’s disastrous 2006 acquisition of Lipman Electronic Engineering Ltd.

The court said King should have filed his Delaware records action before he filed one of the many derivative and securities fraud suits investors lodged in a California federal court over the merger. Kingv.VeriFoneHoldings, No. 5047, 2010 WL 190497 (Del. Ch. May 12, 2010).

In his opening brief in support of an appeal of that ruling, King argues that his California derivative suit had been dismissed with leave to replead at the time he filed the records-inspection action in Delaware.

COLLATERAL DAMAGE

King contends that the ruling appears to bar not just him, but any shareholder from filing a books-and-records action if any other shareholder has elected to forgo that step in a “race to the courthouse” to win the lead plaintiff role.

He says he was doing exactly what the California federal judge in his derivative action advised: Use a books-and-records

action to get ammunition for an amended complaint.

The question for the Delaware Supreme Court is whether Vice Chancellor Leo Strine went too far by ruling that when a plaintiff who wins the race to the courthouse is dismissed because his suit lacks specifics, he cannot go back and file a records-inspection action, King says.

Since VeriFone, an online bill-paying vendor, is incorporated in Delaware, even though its headquarters are in California, its shareholders have the right to inspect the corporate records if the investor has a proper purpose, such as confirming suspicions of management wrongdoing.

The value of VeriFone stock dropped dramatically after it announced Dec. 3, 2007, that it would restate the results of the first three fiscal quarters of the year because of accounting errors arising from the integration of its inventory system with Lipman’s.

THE RACE TO THE COURTHOUSE

A civil complaint by the Securities and Exchange Commission and numerous shareholder suits charging breach of duty and securities fraud soon followed in federal court

in San Francisco. InreVeriFoneHoldingsSec.Litig., No. 07-06140 (N.D. Cal.); InreVeriFoneHoldingsS’holderDeriv.Litig., No. C07-06347, 2009 WL 1458233 (N.D. Cal. May 26, 2009).