corporate report · multiple pillars ensures its stability and a good risk-reward tradeoff. lbs...

TRANSCRIPT

2014Corporate Report

The Franco-German regional bankDie deutsch-französische Regionalbank

Foresight through proximity

CONTENTS

Foreword .......................................................................................................... 6

Group Management Report – Overview ......................................................13

SaarLB consolidated financial statements 2014 ...................................... 68

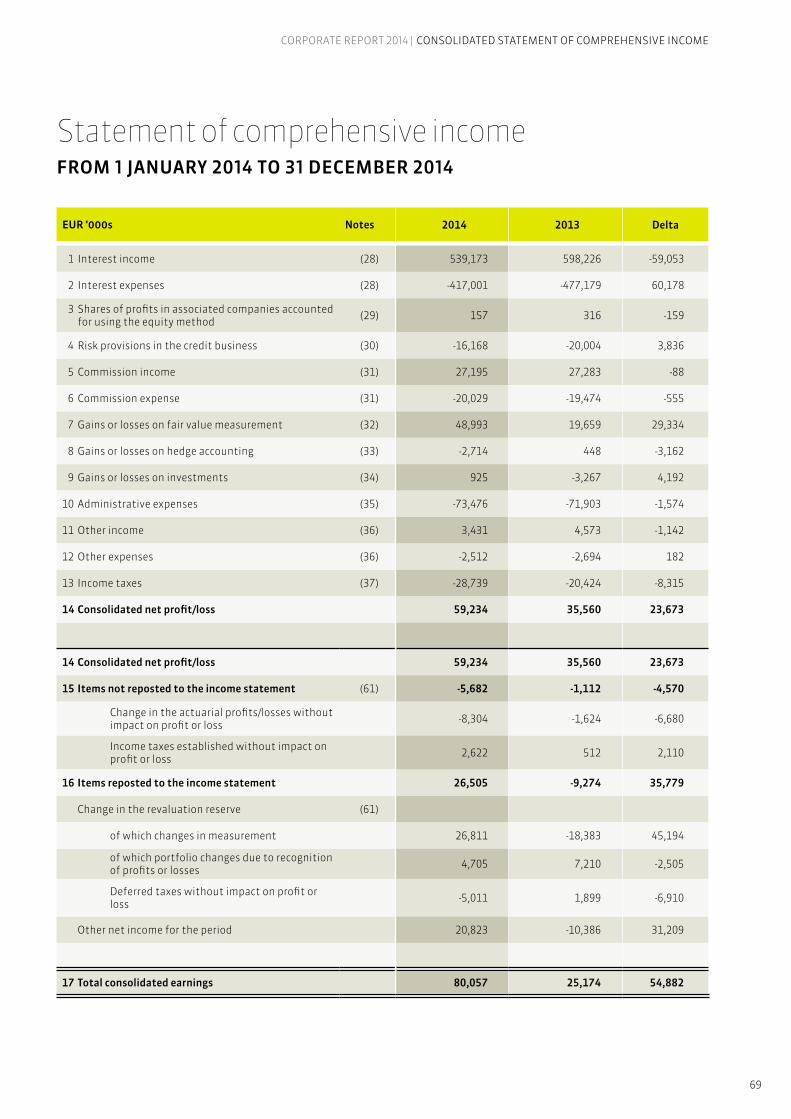

Consolidated statement of comprehensive income ................................ 69

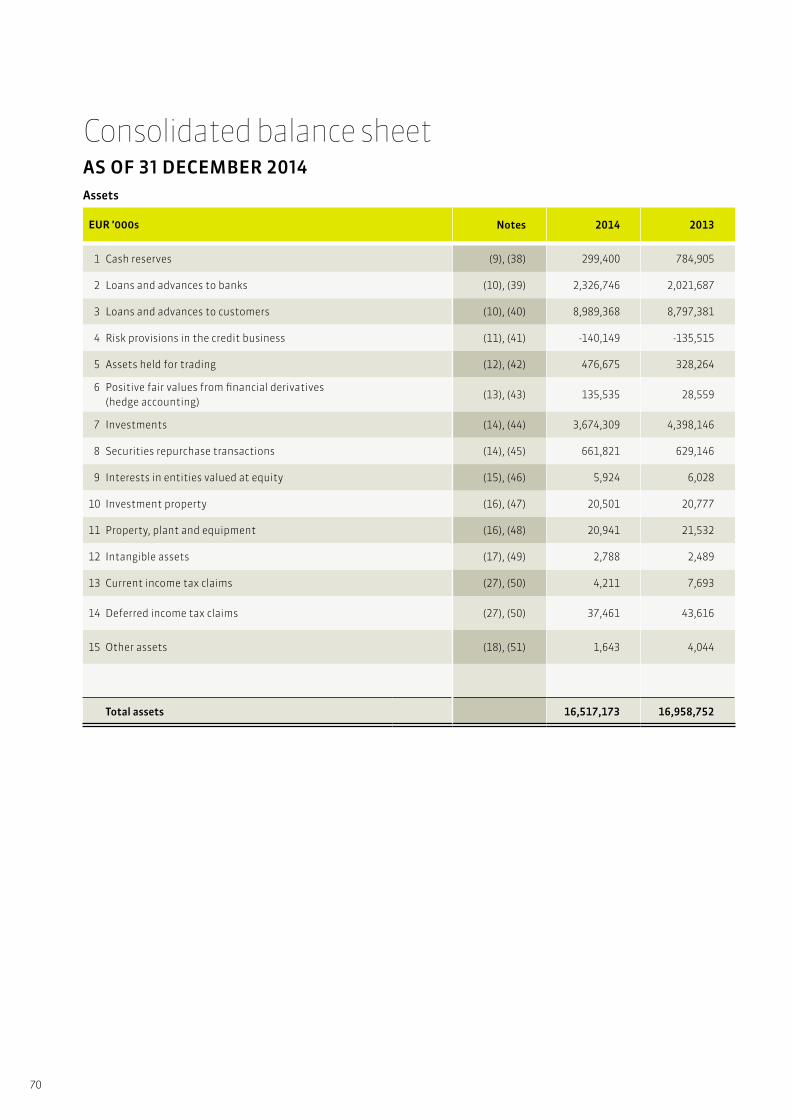

Consolidated balance sheet ........................................................................ 70

Schedule of changes in equity .................................................................... 72

Cash flow statement .................................................................................... 73

Group Notes to the consolidated financial statements 2014 ................. 74

Board of Administration ............................................................................. 159

Board of Management ............................................................................... 160

Independent Auditors’ Report ................................................................... 166

Report of the Board of Administration .................................................... 167

Organisational Chart ................................................................................... 168

Shareholders ................................................................................................ 169

List of abbreviations .................................................................................... 170

3

CORPORATE REPORT 2014 | CONTENTS

We want to be close and take action... As the Franco-German regional bank, we set the agenda. Because we have the courage to try new things and improve existing ones. Because we want to combine economic foresight with human proximity. Because we can act at short notice and think in the long term.

We set the agenda.

People, stories and development

2014

4

1. BALANCE SHEET 31 DEC. 2014EUR MILLION

31 DEC. 2014EUR MILLION CHANGE IN %

Total assets 16,517 16,959 -2.6

Business volumes 17,330 18,026 -3.9

Loans and advances to banks 2,327 2,022 15.1

Loans and advances to customers 8,989 8,797 2.2

Assets held for trading 477 328 45.4

Investments* 4,342 5,033 -13.7

Liabilities to banks 4,880 5,749 -15.1

Liabilities to customers 4,645 4,759 -2.4

Securitised liabilities 5,196 4,940 5.2

Liabilities held for trading 543 433 25.4

Shareholders’ equity 747 585 27.7

Eligible equity in accordance with the CRR 878 876 0.2

2. PROFIT AND LOSS ACCOUNT

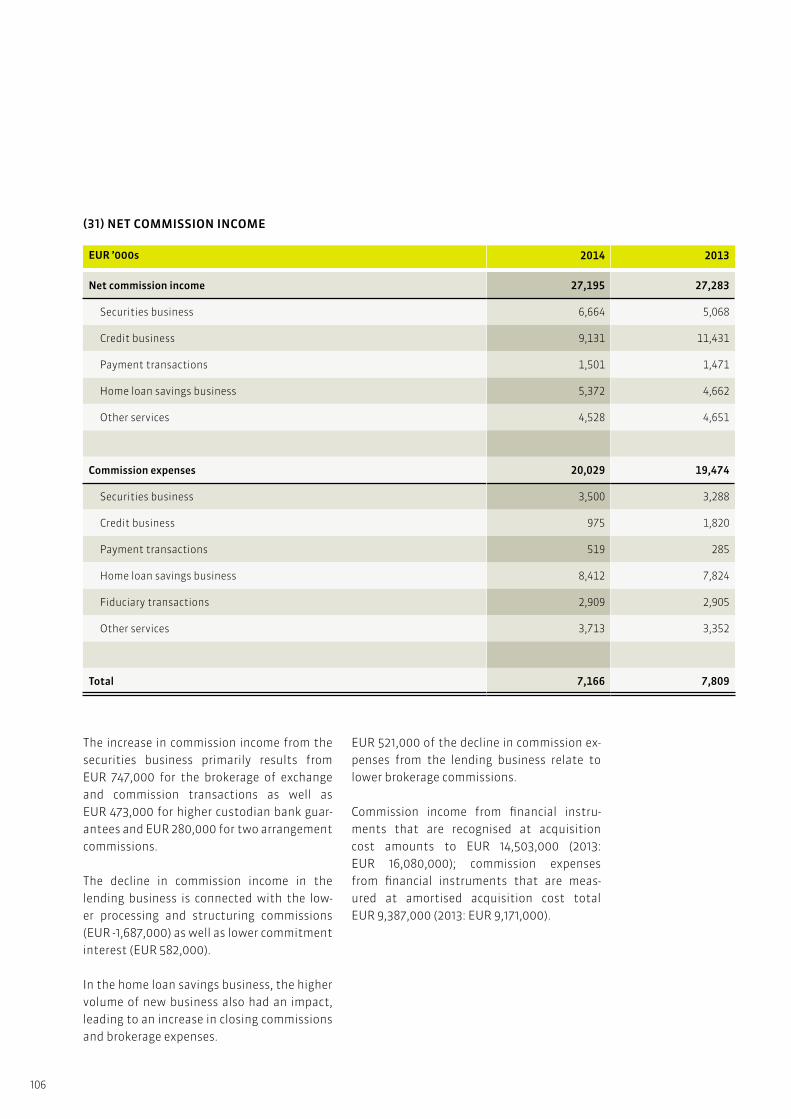

Net interest and commission income** 129.5 129.2 0.2

Gains or losses on fair value measurement 49.0 19.7 > 100.0

Administrative expenses 73.5 71.9 2.2

Earnings before taxes 88.0 56.0 57.1

Consolidated net income/loss for the year 59.2 35.6 66.3

* Including security repurchase transactions and interests in entities valued at equity** Including shares of profits in associated companies accounted for using the equity method

At a glance (IFRS)

5

The Bank’s Franco-German business model again ensured a successful financial year in 2014. There was a significant rise in the IFRS earnings, which was strongly affected by the exceptionally positive fair value gains.

CORPORATE REPORT 2014 | AT A GLANCE (IFRS)

6

(from left to right)

Werner Severin Chairman of the Board of Management

Frank Eloy Member of the Board of Management

Dr. Matthias Böcker Member of the Board of Management

Gunar Feth Chief Representative /

Designated Deputy Chairman of the Board of Management

Ladies and Gentlemen,Business Partners,

7

CORPORATE REPORT 2014 | FOREWORD

What is a sign of success for a company or bank? Growth in business volume? A “solid” profit at the end of the year? Satisfied customers? Motivated employees? All these aspects are certainly important. One point is missing, however: sustainable development. At SaarLB we have attached great importance to this in recent years. It comes with the Bank’s regional orientation – which has been reflected in the pure-ly regional ownership structure of SaarLB since last year. We would like to express our gratitude for the trust and confidence that our owners have in us.

8

The 2014 financial year proves that this path is a successful one. The Bank was able to generate IFRS earnings of EUR 59.2 million after tax-es, greatly exceeding its earnings in 2013. This increase was heavily influenced by the market value changes (over time greatly fluctuat-ing) due to the exceptionally positive fair value gains. A glimpse at the earnings (in terms of the German Commercial Code / HGB) over the last few years shows the stable core returns of the Bank with significantly smaller fluctuations. For 2014, the HGB earnings of EUR 22.2 million after taxes allow for both a reinstatement of the dividend payments to our shareholders and the strengthening of our equity base. Overall, the Bank generated higher income and was exposed to less risk in the last few financial years. The reduction of international capital market activities and the ongoing expansion of the direct customer business were very important. We created this together with our dedicated em-ployees.

Today, the Franco-German business model is established. In its core business, roughly 2/3 of the volume and income come from Germany, 1/3 from France. Our corporate customer business in Germany (new business volumes totalled EUR 305 million) saw an increase in invest-ments in 2014 and strong demand for credit in the region.

In France, our new business with corporate customers expanded de-spite the slow economic performance. In real estate finance, new busi-ness (total of EUR 375 million) was stable in Germany. In France, it de-clined due to margins being under pressure from competitors. Things looked different in the project business (new business volume totalled EUR 359 million): We saw another sharp increase in new business dur-ing 2014 in France. In Germany, by contrast, the “anticipation” effect from 2013 (due to the amendment of the Renewable Energy Act / EEG) lost its impact in 2014.

Together with the savings banks, SaarLB remains an important part-ner for municipalities, not only for municipal loans (EUR 123 million in new business) but, for instance, in the area of interest and currency management to hedge the currently low interest rates. On the deposit side of the balance sheet, the business with high net worth individuals

9

Our balanced business model ensures stability and a good

risk-return tradeoff.

CORPORATE REPORT 2014 | FOREWORD

10

We will continue to finance structurally important

investments in Saarland.

11

was influenced by the ongoing low interest policy in Eu-rope. The basically zero interest rate level we have reached in the meantime has a significant impact not only on pri-vate investors but also the credit economy. Despite the si-multaneously dramatic increase in the requirements from bank regulation, we were able to observe the following for SaarLB: The Bank’s balanced business model based on multiple pillars ensures its stability and a good risk-reward tradeoff. LBS Landesbausparkasse Saar also contributes to this as an integral part of SaarLB. Its new business was again significantly higher in 2014 (at EUR 652 million) than in 2013 (EUR 581 million).

With regard to the future development of SaarLB, we want to remain the first contact for structurally important in-vestments in Saarland.

We view ourselves as an integral part of Saarland’s strategy for France. We want to support SMEs even more strongly abroad, which could benefit from the new cooperation agreements (e.g. with the Bank of China, Frankfurt Branch). For customers, this can be a door-opener to the most im-portant export countries for Saarland. We continue to re-gard the area of renewable energy as a growth segment. In the case of larger financing, we would like to include even stronger partners, such as the savings banks in the region, through syndication.

We look forward to ongoing good collaboration with our customers and partners in 2015. We will introduce four cus-tomers from Germany and France on the following pages: Nanogate AG, VSE AG, EVS Entsorgungsverband Saar and Groupe Soprema.

Werner Severin Frank Eloy Dr. Matthias Böcker Gunar Feth

CORPORATE REPORT 2014 | FOREWORD

12

13

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

OVERVIEW

SAARLBThe SaarLB Group (hereinafter referred to as “SaarLB”) is a corporation established under public law with its headquarters in Saarbrücken.

In April 2014, the state of Saarland completed the acquisition of the shares held by Bayern-LB, as announced in the Management Report appended to the 2013 annual financial state-ments. The owners of SaarLB as of 31 Decem-ber 2014 are: • Saarland: 74.90% • Saar Association of Savings Banks,

Saarbrücken: 25.10%

SaarLB’s strategy is to be the Franco-German regional bank with a focus on corporate cus-tomer business, real estate business, special financing in the area of renewable energies (“RE”) and advisory services for institutional investors, the public sector/municipalities and high net worth individuals (wealth man-agement). SaarLB’s business is managed cen-trally from Saarbrücken. For the French busi-ness, SaarLB also has a branch in Metz as well as sales offices in Strasbourg and Paris.

Landesbausparkasse Saar (LBS), part of SaarLB, finances primarily residential real es-tate through its home loan savings business.

On account of its history and its ownership structure, SaarLB is an integral part of the savings banks finance group (Sparkassen-Fi-nanzgruppe) and attaches great importance to networking, particularly with the Saarland savings banks, while simultaneously concen-trating on core competencies. SaarLB is a central bank for the savings banks and is the principal bank for Saarland.

SaarLB and its shareholders have each made commitments that should ensure the ongo-ing independence of the Bank and its devel-opment into the Franco-German regional

bank. There is also a framework agreement with the Saar Association of Savings Banks on the principles for collaboration between the Saarland savings banks and SaarLB. The binding form is determined by the Bank’s business and risk strategy.

The entire target market includes Saarland, the neighbouring regions in south-west Ger-many, France and Luxembourg. For business in the area of renewable energies, the core market of SaarLB in Germany and France ex-tends across the regions, depending on the geographic conditions that are required for the successful operation of renewable ener-gy plants. The requirements for the business target in real estate and project financing as well as LBS (Landesbausparkasse : subsidiary of savings bank offering collective real estate savings products and providing low-interest residential mortgage loans) are met if the fi-nanced property or project is in Germany or France. In the case of properties (except for LBS), the borrower/investor/asset manager must also be based in the target market; or the financed property must be in the target market. In the area of real estate finance in France, the Île de France region is also one of the major core regions.

On the product side, SaarLB primarily con-centrates on marketable and needs-based products. Complex and highly-specialised products and services are primarily handled by cooperation partners.

In terms of its balance sheet, SaarLB is the largest bank in Saarland and feels a particu-lar connection and obligation to the region. SaarLB has deep roots in the region and ac-tively shapes economic life, making an im-portant contribution to cultural diversity and promoting the sciences in the greater region. This is seen, among others, in the promotion of science and culture through the awarding of the SaarLB science prize and countless permanent loans to the Saarland Museum.

Group Management Report

14

SaarLB’s obligation with respect to its em-ployees is reflected in its human resources work. In 2014, a focal point of SaarLB’s human resources work was on the subject of work-life balance, the overhauling of the management guidelines and the development of a Code of Conduct for all employees as well as the ongo-ing optimisation of the process for standard-ised staff issues.

The subject of work-life balance has been gain-ing importance on account of demographic change, the resulting lack of specialists and the need to strengthen staff loyalty. The fo-cus of the human resources work was on the development and design of instruments that make it possible for staff with dependants, for example, to handle their responsibilities for the Bank and address the needs of their family. Accordingly, a concept for alternating telework was developed and launched. This concept makes it possible to handle some tasks from home. The Bank’s efforts in this regard were acknowledged in October 2014 when it was awarded the seal of a “Fami-ly-friendly company”. The seal is awarded by the state of Saarland.

In various workshops with management and staff, SaarLB developed a collective under-standing of management and a Code of Con-duct that are based on its corporate strategy and brand. The main parts of this are: • Acting as a model generates motivation • Communication opens borders • Innovation shapes the future • Encouragement allows for opportunity

In order to simplify further the standard pro-cesses in the area of human resources, the Bank launched more options for technical support, including areas such as time man-agement.

SaarLB’s group of consolidated companies includes 7 subsidiaries, as in 2014. These in-clude SaarLB Bankenbeteiligungsgesellschaft mbH, Saarbrücken, LBS Immobilien GmbH, Saarbrücken and special funds that are

consolidated in full in accordance with IFRS 10. Companies on which SaarLB can exercise significant influence (associates) are included in the consolidated financial statements in accordance with the “at-equity” method. As in 2013, three associates continue to be valued according to the at-equity method. Materi-ality criteria are used to determine SaarLB’s scope of consolidation. After LBS Immobilien GmbH was consolidated in full for the first time as a material subsidiary in 2013, there are three (31 Dec. 2013: one) subsidiaries and one (31 Dec. 2013: zero) joint venture compa-nies and three associates (31 December 2013: five) neither fully consolidated nor included at equity, since they are insignificant for the net assets, financial position and results of operations of the Group.

SaarLB breaks its business down into a num-ber of segments that are mainly reflected in the structural organisation. The segments are described in the following:

Corporate CustomersThe Corporate Customers segment covers the entire SME business of SaarLB in its target markets. In Germany, this includes Saarland, Rhineland-Palatinate and the adjacent re-gions. In France, SaarLB’s Corporate Customer business is focused on the Grand-Est (Grand East) and here in particular on the neighbour-ing Alsace-Lorraine where the Bank is rep-resented by its branch in Metz and its sales office in Strasbourg. The main product in this segment is traditional lending. Further-more, a full service is provided, primarily by offering investment products, interest rate and currency management products as well as products in the areas of foreign trade and payment transactions in accordance with cus-tomers’ needs and giving business advice on how to finance companies. The broad range of products also includes financing for munic-ipalities and municipally-owned companies.

Real estateThe Real Estate segment at SaarLB is respon-sible for the financing of commercial real

15

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

estate. The business activities are limited to the target markets of SaarLB. Business is transacted on a bilateral basis or in the form of club deals under the leadership of the Bank. Professional and institutional investors who primarily invest in office and retail real es-tate are the focus in this segment. In France, the market is primarily handled by the Cen-tre d’Affaires Paris, which is a part of SaarLB France. In the German target market, SaarLB acts selectively as a financial service provider for developer measures and for public private partnership (PPP) measures for investments in infrastructure, education or other public construction projects. The Real Estate seg-ment’s regional focus on the German side is in the metropolitan area of the Rhine-Main, while in France it is on the urban centre of the Île-de-France. As in the Corporate Customers segment, credit financing is the main product, although SaarLB’s structuring and cross-bor-der legal expertise are also significant for the success of the business segment. Interest hedges with simple derivatives in the portfo-lio and new business are concluded with suc-cess, and increasingly payment transactions and investment products, too.

ProjectsThe Projects segment at SaarLB is responsi-ble for the financing of projects primarily in the renewable energy sector (RE) but also in the area of public private partnership on the French market. In the RE sector, SaarLB acts as a financial service provider for midsized project initiators and manufacturers that invest in wind and/or solar parks at good lo-cations and with sophisticated technology. Many customers in the business segment are supported across borders. The focus of the segment on the German side is regional in Saarland and Rhineland-Palatinate, while on the French side – due to its very good po-sition on the market – it is the entire country of France. The Bank does not finance offshore wind parks. As in the Corporate Customers and Real Estate segments, credit financing is of critical significance for the customer relationships and thus the development of

business. In addition to SaarLB’s particular Franco-German legal expertise, it also has extensive and long-standing know-how de-veloped under constantly changing market conditions in project analysis, the resulting case-specific and cash flow-driven structuring of finance, and SaarLB’s good access to long-term funding, which are viewed as significant key factors for the success of business over the long term.

Savings Banks, Institutionals and High Net Worth IndividualsThe Savings Banks, Institutionals and High Net Worth Individuals segment handles wealth advisory services and management for savings banks, institutionals and high net worth individuals. The focus of the Savings Banks and Institutionals is on increasing ex-isting customer connections and expanding contacts with insurance companies and pen-sion funds in the region and the business re-lationships to savings banks in Rhineland-Pa-latinate. It also deals with the financing of the region’s savings banks and municipalities. In the sub-segment of high net worth private customers, the focus is on complete support and advising for wealthy private customers. Lastly, as a centre of expertise, it actively supports the other segments in customer relationship management, especially in in-vestment, interest rate and currency manage-ment.

Treasury & Portfolio ManagementTreasury is responsible for the management of the interest book, the trading activities of the Bank, the collateral pool and collateral management as well as liquidity control and pricing. Portfolio Management is in charge of managing the liquidity account (Securities Ac-count A, collateral account and LCR portfolio), the management of the Bank’s own invest-ments (direct investments and special funds) and the management of the portfolios that are no longer a part of SaarLB’s core business and are being systematically reduced (reduc-tion portfolios).

16

LBSLandesbausparkasse Saar is a legally depend-ent unit of SaarLB. LBS Saar and its subsidi-aries are a service and excellence centre for “everything related to real estate”, making them an integral part of the Saarland savings banks finance group (Sparkassen-Finanz-gruppe). The main services are home loans and the financing of residential real estate. Another focus of the Bank’s policy is on the financing of energy projects in real estate and investments within the framework of the German Renewable Energy Act (Erneuer-bare-Energien-Gesetz), photovoltaic systems, for example. Additional services range from the management and brokerage of residential and commercial real estate to the preparation of real estate evaluations, energy reports or damage appraisals as well as the brokerage of select network (Verbund) products.

As announced in 2013, equity investments shall no longer be reported as a segment but rather be summarised under “Other items” due to their decreasing significance.

Control system at the BankThe strategic controlling of SaarLB is based on the business strategy for the entire bank and for the segments. It monitors the following IFRS financial performance indicators:

• Return on equity (RoE): Earnings before tax-es in relation to the tied-up economic capi-tal, whereby the economic capital is defined as 8% of the average risk positions in the year under review as calculated in accord-ance with the regulatory requirements, and

• Cost-income ratio (CIR): Administrative ex-penses as a percentage of the total ordinary income (consisting of net interest income, net commission income and other income). The fair value gain/loss is not explicitly tak-en into account in order to avoid market-in-duced dilution effects.

• RWA returns: This key performance indica-tor shows the total from the net interest

income, net commission income and other operating income in relation to the average risk positions.

Non-financial performance indicators are not used for controlling.

Economic environment

Germany began 2014 with a very strong 1st quarter. When adjusted for prices, gross do-mestic product (GDP) rose by 0.8% during this time. This jump benefited from the mild win-ter at the beginning of the year. In particular, construction profited from the seasonable weather. The slowdown in the 2nd quarter dampened the optimism, however. Nonethe-less, the ensuing weakness during this time also continued in the 3rd quarter so that the economy basically stagnated during the sum-mer. In particular, investment activity in Ger-many, which had finally taken off before, col-lapsed quite abruptly again. The 4th quarter has not yet been definitively calculated by the German Federal Statistical Office. The unoffi-cially stated growth of “roughly one quarter” of a percent is an indication, however, that the recovery – supported by cheap oil and a devalued euro – should have started up again.

The first official estimate announced that there was economic growth of 1.5% for the full year of 2014. That is significantly better than the weaker growth rates in 2012 and 2013 (+0.4% and +0.1%) and is even above the potential rate for Germany, which is usually expected to be around a good 1%.

German growth was supported by all the individual components, above all domestic demand. After adjusting for prices, private consumer expenditures rose by 1.1% in 2014. Despite fluctuations over the course of the year, gross capital expenditures increased by a total of 3.1%. The export of goods rose by 3.7% in real terms; imports by 3.3%. As a re-sult, the positive trade balance also made an important contribution to growth in 2014.

17

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

The transition to environmentally-friendly en-ergies continued to move ahead in 2014, with the year turning out to be a record breaker for renewable energies. According to the pre-liminary surveys by the German Energy and Water Industry Association (BDEW) at the end of December, renewable energies as a per-centage of total electricity generated in Ger-many should have increased to 25.8% in the past year (2013: 24.1%). In total, renewable energies covered roughly 27.3% of gross Ger-man electricity consumption in 2014. Wind energy also generated more electricity than ever before, accounting for roughly 8.9 TWh in the last month of the year. Wind energy’s generation of electricity rose by roughly 1.0%, whereas photovoltaics rose much more rap-idly, by roughly 14%. The gross increase in ca-pacity for onshore wind energy was 4,750 MW in 2014 (+58% as compared to 2013) and was thus far above the target corridor of 2,400 to 2,600 MW as set forth in the Renewable Ener-gy Act (EEG) in 2014. The cause of this sharp increase is an anticipatory effect due to the debate over the Renewable Energy Act (EEG).

SaarlandAfter two years of recession-related weak-ness, the Saarland economy recovered during 2014. Above all, the large industrial sectors have returned to their former strength. Gross domestic product (GDP) in Saarland rose by 2.1% in the first half of 2014, when adjusted for prices. On average, the economy in Saar-land outperformed the German economy both in nominal and real terms. For full year 2014, growth of roughly 2.0% is expected in Saarland.

The large industrial sectors in Saarland – the automotive industry, machine building and the steel industry – represent over 70% of the total sales in manufacturing and were able to significantly increase their sales in 2014. In the primary construction industry, incoming orders (+1.2%) rose slightly, while sales again fell substantially (-6.1%). The renovation busi-ness saw a 14.8% jump in sales. After the out-standing performance in 2013, there was no

hope for another improvement in the perfor-mance of construction approvals for residen-tial housing in 2014.

Thanks to the ongoing positive consumer sentiment of private households, retail (not including cars) managed to increase sales by 2.4%. The sale of vehicles, which collapsed by almost 40% in the previous year, continued to remain on a low level, however. This year, the catering and hotel industry should be men-tioned since it gave Saarland tourism a highly welcome lift, above all thanks to the construc-tion of a large recreational park.

Rhineland-PalatinateThe economic position of the economy in Rhineland-Palatinate was stable in 2014. Con-cerns about the ongoing course of domestic sales became the no. 1 risk factor, replacing concerns about high energy and raw material prices over the long term, which had assumed this place for many months. Companies across all industries observed increasingly weak de-mand, both on the part of end consumers as well as commerce and industry.

After a slight recovery in the early summer, investments in Rhineland-Palatinate lost mo-mentum into autumn. Furthermore, the fo-cus of the planned measures continued to be replacement purchases, while investments in the expansion of capacities – at least in indus-try – continued to lose significance.

In 2014, the adjusted production index was in total 0.7% below the level in the previous year. All three of the main industrial groups posted declines of a similar order of magnitude. While the output of intermediate product manufac-turers fell by 0.8%, the throughput in capital goods dropped by 0.6%. Consumer goods pro-duction was also somewhat lower than in the previous year. Of the three largest sectors in the state, only the mechanical engineering sector succeeded in noticeably increase its production output (+7.3%). Car manufactur-ing (-3.2%) and the chemical industry (-8.3%) had to accept declines. Rhineland-Palatinate’s

18

construction industry achieved growth in con-struction sales and in incoming construction orders in 2014. According to the State Statis-tical Office, sales – adjusted for the calendar and season – were 3.8% higher than in 2013. Commercial building construction accounted for a major contribution, rising by roughly 10.2%. Income orders exceeded the level from the previous year by 6.0% and were positively affected in particular by commercial construc-tion and excavation work.

FranceFor France, 2014 was as weak as the two years before, with GDP rising by up to 0.4%. Private consumption expenditures, a traditional driv-er of the French economy, have significantly underperformed since 2011. This reflects the massive uncertainty of French consumers. The consumption climate may have slightly recovered recently, but it is still at a low lev-el. Due to the low inflation rate of 0.8% on account of oil prices, wages in real terms rose slightly. The situation on the labour market stabilised recently.

The French government recognised the need to improve the competitiveness of companies and provide tax relief for them, so it launched a programme called “Crédit d’impôt pour la compétitivité et l’emploi” (CICE). Roughly EUR 40 billion in tax relief was granted over a period of three years. In addition, compa-nies should benefit in two other ways: on the one hand from a change in the threshold val-ues under labour market law and the other requirements that must be met once these thresholds have been reached. On the other, steps have been planned for a liberalisation, above all, of the service sector which is impor-tant for France. These are all steps in the right direction, but the positive effects from them will take time.

The situation on the office market in Paris is by no means as bad as sentiment in the French economy. After multiple quarters with declining rents, the office market should

stabilise gradually. The year 2014 went better than 2013, particularly with regard to the vol-ume and number of conducted transactions. However, the market was characterised by a significant decline in transactions with vol-umes < EUR 100 million (in 2013 their share was 52% vs. 32% in 2014). There were 44 trans-actions with a volume of > EUR 100 million in 2014. The vacancy rate remains relatively sta-ble at an average of 7.8%. Demand for quality properties continues to be very high. Rents are stabilising or starting to rise again.

Wind energy in France is also clearly on the rise. After many weak years in which new con-struction successively declined and the year 2013 when newly installed wind output was at 525 MW, new wind construction gained steam noticeably in 2014. New wind energy plants with a total output of 1,042 MW were connected to the grid in 2014. Among oth-ers, this is also due to the fact that the le-gal dispute over the remuneration waiver (Vergütungserlass) was resolved in May 2014 and various measures for a simplification of the legal framework were introduced for wind energy.

LorraineIndustrial production remained stable in 2014, exceeding the expectations of compa-nies in 2013. Total sales only improved slight-ly in 2014, by roughly 0.2%, but the share of exports in it increased somewhat more mod-erately, by +1.1%. By contrast, employment continued to decrease (-1.5%). The use of tem-porary workers continued to rise during the course of the year, but differs significantly from sector to sector. After a slight recovery in investments in 2013, they declined sharply, by 13.4%, in 2014. This development is mostly due to the significant decline in other indus-trial products, while other sectors (e.g., food production) increased. The performance of other industrial products (-2.2%) was also connected with this, and the chemical indus-try (-13.8%) declined the most in this segment.

19

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

Construction declined by 6.7%, which was significantly higher than forecast in 2013. Income declined across all sectors, with exca-vation accounting for roughly -8.9% and the primary construction industry for -10.2%.

In the service sector, sales decreased by 1.6% overall as compared to a 3.8% decline in 2013, whereby this decline concealed the differences in the individual sectors. While the legal professions, tax and corporate consulting firms as well as engineering and transport had to post declines in growth of between 3-5%, the information and commu-nications sectors saw growth (+6.1%). Sup-ported by government measures, particular-ly with regard to the employment costs, the percentage of employed people fell only very moderately (roughly 0.5%). Investment ac-tivity levelled off across all sectors, primarily in transport.

AlsaceAfter the observed decline in 2013, the situ-ation in industry in Alsace improved slightly in 2014. Total sales rose slightly, by roughly 1.5%, supported in particular by exports (+2.8%), even if the European economy was not especially dynamic. This development had no positive impact on employment, which fell by -0.7% over the course of the year. The food industry was able to increase sales by 4.4%, despite the disappointing re-sults in the sector of meat and drink produc-tion. As predicted, the production of means of transport showed a pleasing improvement of 14.1%, both in the automotive industry (particularly in production) and in other means of transport. The increase in sales is supported in particular by the improvement in exports (+20.9%).

According to a business survey by the Ban-que de France, investments increased by roughly 5.6% in 2014. 85% of businesses have invested in modernisation and in the adjust-ment to applicable standards. Expenses in the food industry, by contrast, fell by 16.1%, after a decline of 6.7% in 2013. In the area

of means of transport and other industrial products (e.g. chemicals, textiles, paper pro-duction) by contrast, investment expendi-tures rose significantly.

In construction, stability was attributable to sales in the secondary construction industry (+3.6%), while the primary construction indus-try (-1.6%) and excavation (-5.9%) confronted a decline in demand and a lack of large projects. The ongoing weakness in incoming orders and the lack of a recovery in demand – above all from the public sector – caused companies to adjust their costs and staff to capacity (-1.1%); use of temporary work was also limited. After the de-cline in the last two years, investment expendi-tures increased overall in 2014 (+4.5%) except in the primary construction industry (-8.2%).

In the service sector, economic growth re-mained 1.3% behind expectations, with de-mand not showing any signs of rising. Trans-port and logistics rose by 2.9%, while the IT industry solely grew by 0.6%. The 1.6% rise in employment was mainly due to hiring in the transport (+1.7%) and IT (+5.9%) industries. In-vestments in the area of the service sector fell by roughly 10.3% in 2014, particularly affected by declines in the transport industry (-10.7%).

Financial sector

The stability of the financial sector in Germa-ny continued to be slightly strained during the reporting period. There is still a series of risks that could disrupt this stability. These include, for example, exposure to countries that are affected by the European sovereign debt crisis or the effect the economic sanctions have on the Russian economy. In addition, the ongoing low-interest environment is also having a no-ticeable impact on the stability of the German financial system.

Furthermore, the financial sector must face the challenges that could result from structur-al changes in the financial system. The signifi-cance of regulatory requirements plays a major role here.

20

The financial market and sovereign debt crisis in recent years caused the adoption and the planning of numerous regulatory measures over the past few years and in 2014. These

measures should affect the regulatory envi-ronment in the financial sector over the long term.

The development on the European and par-ticularly the German stock market is an indi-cator of how the financial crisis continues to abate. The DAX closed the reporting period at roughly 9,800 points, a slight rise of 2.66%. The German benchmark index is currently affected by the significant uncertainty on ac-count of the ongoing conflicts in Ukraine and the Middle East, which is seen in the high de-gree of fluctuation over the course of the year. The 10,000 point benchmark may have been broken twice, but was not held for long.

Contrary to the positive development on the stock market, the euro fell substantially against the US dollar over the course of the year, dropping from 1.38 EUR/USD at the be-ginning of the year to 1.21 EUR/USD at the end of 2014.

The Swiss franc remained stable, above the level of 1.20 CHF/EUR over the course of the year, despite high international demand. This exchange rate was supported by the meas-ures of the Swiss National Bank (SNB), which attempted to avoid an appreciation of the franc. After the SNB stopped the measures on

15 January 2015, the exchange rate fell signif-icantly to roughly 0.86 CHF/EUR. SaarLB and its customers only do business in Swiss francs to an insignificant extent. In this respect, the devaluation did not play an important role for SaarLB.

Due to the slow economic recovery in the eurozone, the ECB lowered its benchmark refinancing rate from 0.15% to 0.05% in Sep-tember. After years of zero interest rates, in-terest rates for the deposit facility at the ECB became negative for the first time at -0.20% in September 2014.

The average 3-month Euribor was below the Bank’s originally expected amount of 0.5% throughout the 2014 reporting year and, after a fairly stable first half of the year, moved sub-stantially downward to an average of 0.3% and thus again fell below the already low level in 2013. The development of long-term inter-est remained on a historically low level over the course of the year and, contrary to our ex-pectations, fell even further as compared to the end of 2013.

3-month Euribor Q1/14 - Q4/14 in %

0.40

0.32

0.24

0.16

0.08

0.00

Q1/14 Q2/14 Q3/14 Q4/14

Source: Deutsche Bundesbank statistics

Swap rates Q1/14 - Q4/14 in %

2.50

2.00

1.50

1.00

0.50

0.00

Q1/14 Q2/14 Q3/14 Q4/14

Source: Bloomberg

10 years 5 years

21

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

The architecture of the European banking un-ion continued to take shape in 2014. The Sin-gle Rule Book, which also includes the Capital Requirements Regulation (CRR) and the Cap-ital Requirements Directive (CRD), standard-ised the European banking supervisory rules. The equity and liquidity requirements of the CRR in force were amended. In accordance with the European Capital Requirements Reg-ulation (CRR), banks have been required to re-port a leverage ratio to the European Banking Authority since 2014. The leverage ratio is a debt ratio independent of risk, consisting of the regulatory capital as a percentage of the Bank’s business volume.

This is now followed by the European Bank-ing Authority (EBA): After a comprehensive review of the 120 largest bank groups in the eurozone, the Single Supervisory Mechanism (SSM) will begin its work. The European Cen-tral Bank (ECB) has been responsible for the supervision of the 120 largest bank groups in the eurozone since November 2014. It works closely with the national supervisory authori-ties. The SSM is a part of the overall project to create a banking union. The next step will be-gin in 2016 and consist of a joint Single Reso-lution Mechanism (SRM) for banks. The main goals of the SSM are the standardisation and the simplification of the banking authority. The ECB completed a Comprehensive Assess-ment in preparation for the assumption of its supervisory function over the 120 bank groups in the eurozone. This included a regulatory risk audit, an asset quality review and a stress test. The stress test was completed in close coordination with the EBA and should deter-mine the resiliency of the banks during times of crisis. SaarLB was not affected by this in 2014.

The harmonisation of the Deposit Guarantee Schemes (DGS), the third component of the banking union, is also moving ahead. All EU countries are obligated to build up bank-fi-nanced deposit guarantee schemes. This will guarantee bank deposits up to EUR 100,000 in cases of loss. The deposit guarantee schemes

in Germany will continue to remain in their ex-isting forms. An EU-wide pooling of the depos-it guarantee schemes is not planned.

In order to implement the European require-ments for the bank union, the German parlia-ment passed a package of laws for the imple-mentation of the European bank processing guidelines (BRRD Implementation Act) and other accompanying laws. The package of laws should facilitate in particular the imple-mentation of the guidelines for a European legal framework for restructuring and un-winding banks, which entered into force on 2 July. The unwinding authority shall receive in particular the right to financially include shareholders and creditors of a bank in the event of an unwinding (so-called “bail-in”). This rule complements the intervention and unwinding instruments that already exist in national law. The most important part is the “Law on the Restructuring and Unwinding of Banks and Financial Groups” (Sanierungs- und Abwicklungsgesetz – SAG).

Besides the far-reaching changes that the fi-nancial sector is facing as a result of the bank-ing union, the current regulatory drafts are already foreshadowing their impact:

the Basel Committee on Banking Supervision has already tightened the existing rules and the regulatory requirements for banks in the principles for the effective aggregation of risk data and the risk reporting (BCBS 239). BCBS 239 consists of eleven principles which are considered relevant for banks in general and are based on overall corporate management and infrastructure, the risk data aggregation capacities and the risk reporting. Starting at the end of 2015, the first banks in Germany will implement the rules.

The Financial Reporting (FINREP) and the Common Reporting (COREP) for regulated bank institutions will also be harmonised and standardised. The FINREP implements the ba-sic understanding of the international finan-cial reporting standards (IFRS). This applies in

22

particular to the classification and the evalu-ation of financial instruments.

The European Banking Authority (EBA) is preparing another regulatory framework by drafting a guideline for the Supervisory Re-view and Evaluation Process (SREP). This is intended for the supervisory authorities of the EU states. In part, these principles have already been included in the guidelines for

the banking supervision by the ECB and are therefore of major significance for future reg-ulatory practice. The institutes are divided into categories according to the concept of proportionality, whereby this categorisation should reflect the institute’s risk for the finan-cial system. The internal governance and con-trols, the significant risks, capital and liquidi-ty stand at the centre of the assessments.

23

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

RESULTS OF OPERATIONSDEVELOPMENT OF EARNINGS IN THE SAARLB GROUP

The consolidated net profit before taxes was EUR 88.0 million, significantly above the good result in the comparative period of 2013 (EUR 56.0 million). However, the slow invest-ment activity and the historically low interest rates had a negative impact on SaarLB’s earn-ings in 2014.

Due to the stable course of business in 2014, the extraordinarily good fair value gains as well as the significantly lower-than-expected

risk provisions, the return on equity (before taxes), in accordance with IFRS, was 16.0% as of 31 December 2014. This is significantly above the amount in the comparative period of 2013 (9.9%) and, on the current reporting date, is better than expected in last year’s forecast. The cost-income ratio in accordance with IFRS is 56.3%, moderately above the com-parative amount of 54.9% in 2013 and in line with our forecast at the end of 2014. The RWA returns remained largely on a constant level.

EUR million 2014 2013 ∆ in million ∆ in %

Net interest income, including profit/loss from companies valued at equity [1] 122.4 121.4 1.0 0.8%

Risk provisions in the credit business [2] -16.2 -20.0 3.8 -19.0%

Net commission income [3] 7.2 7.8 -0.6 -7.7%

Earnings from fair value measurement, including gain/loss on hedge accounting [4] 46.3 20.1 26.2 130.3%

Gain/loss on investments [5] 0.9 -3.3 4.2 -127.3%

Administrative expenses (incl. depreciation) [6] -73.5 -71.9 -1.6 2.2%

Other income [7] 0.9 1.9 -1.0 -52.6%

Consolidated net profit/loss (before taxes) [8] 88.0 56.0 32.0 57.1%

Income taxes [9] -28.7 -20.4 -8.3 40.7%

Consolidated net profit/loss for the year [10] 59.3 35.6 23.7 66.6%

Average risk positions [11] 6,877 7,042 -165.4 -2.3%

CIR ([6] / ([1]+[3]+[7])) [12] 56.3% 54.9% 142 bp

RoE ([8] / ([11]*8%)) [13] 16.0% 9.9% 606 bp

RWA returns (([1]+[3]+[7]) / ([11]) [14] 1.9% 1.9% 4 bp

24

SaarLB’s net interest income (including earn-ings from companies measured at equity) rose by EUR 1.0 million in 2013, from EUR 121.4 mil-lion to EUR 122.4 million in 2014. This remains significantly below the last forecast and cor-responds to a rise of 0.8%.

Net interest income continues to be defined by the very low interest rates and decreasing credit volume, which is largely determined by the systematic reduction of the sub-portfoli-os that are no longer a part of the core busi-ness.

The decline in interest expenses from EUR -477.2 million in 2013 to EUR -417.0 mil-lion in 2014 (-12.6%) was more than fully com-pensated by a moderate decline in interest income from EUR 598.2 million in 2013 to EUR 539.3 million (corresponds to -9.8%) in the current reporting period.

Interest income from credit and money mar-ket transactions fell by EUR 22.9 million and was significantly below the level in the pre-vious year. This is a decline of roughly 7.6%. Interest expenses from liabilities to banks and customers decreased significantly, by EUR 31.2 million, or 17.2%.

Interest expenses for derivatives in hedge accounting and derivatives with economic hedge relationships totalled EUR 196.1 million in the reporting period, which was slightly be-low the amount in 2013 (EUR 220.1 million).

By contrast, interest expenses for sub-ordinate/hybrid capital declined from EUR 18.7 million to EUR 16.6 million (-11.4%) in 2014.

The earnings from companies valued at-equi-ty totalled EUR 0.2 million at the end of 2014, remaining on almost the same level as in 2013 (EUR 0.3 million).

The risk provision in the credit business was EUR -16.2 million, which was EUR 3.8 million below the level of EUR -20.0 million in 2013.

The additions to individual risk provisions (including provisions) were EUR -24.5 million, which was EUR 14.5 million below the amount of EUR -39.0 million in 2013. The releases of individual risk provisions (including provi-sions and the receipt of written-off loans and advances as well as the write-up of loans and advances) totalled EUR 10.7 million, which is roughly EUR 9.1 million below the level of EUR 19.8 million in 2013.

Additions to portfolio risk provisions totalled EUR -2.4 million, which is below the amount in 2013 (EUR -2.9 million). They stand in relation to releases of EUR 0.1 million in 2014 (2013: EUR 2.1 million).

The net commission income amounts to EUR 7.2 million and is thus slightly below the level in 2013 (EUR 7.8 million) and also slightly below the last forecast.

The decline in the net commission income is primarily due to a drop in the commission income from the credit and lending business (EUR -1.5 million as compared to 2013).

Other commission income fell slightly, by EUR 0.5 million, to EUR 0.7 million.

The gains on fair value measurement, incl. the gains on hedge accounting, came to EUR 46.3 million and were significantly above the level of EUR 20.1 million in 2013. The pos-itive valuation effects due to low interest rates accounted for this, including an effect of EUR +7.7 million from securities measured in accordance with the fair value option.

The gains on hedge accounting are EUR -2.7 mil-lion in the year under review, which is below the level of the previous year (2013: EUR +0.4 mil-lion). The gains on hedge accounting show the existing ineffectiveness of the held hedges within the scope of the ranges permitted for hedge accounting. The absolute increase in the gains on hedge accounting is due to the significant increase in the scope of the hedge relationships relative to the end of 2013.

25

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

The gains/losses on investments totalled EUR 0.9 million in the reporting period, which is EUR 4.2 million above the level in 2013 (EUR -3.3 million) and thus confirms the forecast in the previous year. The gains were mainly influenced by the relatively higher capital gains profits (EUR 2.8 million) and higher income from write-ups (EUR 1.6 mil-lion).

Administrative expenses incl. the deprecia-tion of property, plant and equipment and the amortisation of other intangible assets totalled EUR -73.5 million on 31 Decem-ber 2014, which was above the amount in the comparative period of 2013 (EUR -71.9 mil-lion), but significantly better than expected in our original forecast. Personnel expenses rose slightly from 2013, by EUR 1.6 million, to EUR -43.1 million, in accordance with the forecast. Other administrative expens-es also rose slightly, by EUR 0.3 million, to EUR -28.2 million, but that is significantly less than expected in the framework of last year’s forecast. The deviation from the fore-cast is mainly due to the higher than planned capitalisation of IT migration costs at LBS.

The depreciation of property, plant and equip-ment and the amortisation of other intangi-ble assets was EUR -2.2 million and slightly below the level from 2013 (EUR -2.5 million).

Other income amounted to EUR 0.9 million in the reporting period (2013: EUR 1.9 million).

Other income fell year on year from EUR 4.6 million to EUR 3.4 million. It main-ly includes rental income from investment property (EUR 1.3 million; 2013: EUR 1.3 mil-lion) and income from the release of provi-sions (EUR 0.8 million; 2013: EUR 1.5 million). The decline in other income as compared to 31 December 2013 is primarily due to the decline in income from the release of provi-sions (EUR -0.7 million) and the decrease in capital gains from repurchased own issues (EUR -0.4 million).

The sum total of other expenses is EUR -2.5 mil-lion in the reporting period, which is on the level of 2013 (EUR -2.7 million).

In total, the consolidated net profit before taxes in 2014 is EUR 88.0 million as compared to EUR 56.0 million in the comparative period of 2013. The forecast in 2013 was greatly ex-ceeded as a result.

After taking into account the tax expenses of EUR -28.7 million (2013: EUR -20.4 million), there was a consolidated net profit after taxes of EUR 59.3 million (2013: EUR 35.6 mil-lion) of which a dividend in the amount of EUR 3.0 million was distributed to the share-holders. The tax expense consists of an actual tax expense in the amount of EUR -11.6 million (2013: EUR -15.1 million) and an expense for deferred taxes in the amount of EUR -17.2 mil-lion (2013: EUR -5.3 million).

DEVELOPMENT OF BUSINESS AND EARNINGS IN THE SEGMENTS

The contributions made by the core segments to earnings are described in the following:

Corporate Customers (CC)

Corporate Customers services corporate customers in Germany as well as corporate customers, municipalities and municipally owned companies in France. The target mar-kets in Germany are Saarland, Rhineland-Pa-latinate and the surrounding regions. In France, SaarLB concentrates on the Grand-Est (Grand East) and here in particular on the neighbouring Alsace-Lorraine where the Bank is represented by its SaarLB France branch at the offices in Metz and Strasbourg.

26

The Corporate Customers segment achieved net interest income of EUR 25.0 million at the end of 2014 and thus exceeded its earnings in 2013 by EUR 2.1 million. The rise in companies’ business and investment activity, which was noticed in both the French and German target markets in the second half of 2013 also con-tinued in 2014. In the second half of the year, the sectors of metal production and process-ing as well as power plant construction were an exception to this due to the strong compe-tition from the far east and the high level of uncertainty on the market as well as the hes-itancy to make investments in the European energy industry. The high liquidity reserves and good internal financing capabilities place large midsized companies in the position to fund their working capital needs and ongoing investments increasingly from their own re-sources. This increases competitive pressure among banks and keeps the pressure on the margins constantly high. On the German side, SaarLB was able to successfully implement multiple structured financing (promissory notes and syndicated loans) with the involve-ment of Saarland savings banks.

In the business with corporate customers in France, SaarLB benefited in particular from a very dynamic 2nd half of the year. The Bank provided new loans above all to internation-ally active companies and companies with a connection to Germany. New lending business with municipal customers in France remained below expectations in this year. However, it

was possible to draw attention to new points of emphasis through the development of new products and services. The offer of short-term lines of credit based on the reference interest rate and the providing of promissory note loans for German investors should be empha-sised here.

The entire new business volume in the seg-ment totalled roughly EUR 300 million and was distributed almost evenly across Germa-ny and France in 2014. In comparison to the previous year and to the plan, new business could also be improved due to the income components in the current financial year. The portfolio quality as measured in terms of av-erage rating exceeds the budget assumptions but remains slightly below the amount in 2013.

Overall, we slightly exceeded our expecta-tions both in new business and portfolio busi-ness on the basis of the good positioning with our strategic customers and the high number of initiated business relationships, also con-firming our forecast in last year’s financial statements.

The risk provisions in the lending business for EUR -3.4 million were due to new provisions in the Corporate Customers Germany seg-ment. In France, by contrast, the releases of provisions overcompensated for the creation of new provisions. Thanks to the conserva-tive risk provision policy, the actual costs

EUR ’000s 2014 2013 Δ thousand Δ in %

Net interest income 25,034 22,952 2,082 9.1%

Risk provisions in the credit business -3,377 -6,666 3,289 -49.3%

Net commission income 3,526 3,917 -391 -10.0%

Gain/loss on fair value measurement -260 94 -354 -377.0%

Gain/loss on investments 0 115 -115 -100.0%

Administrative expenses -10,905 -15,134 4,229 -27.9%

Earnings before taxes 14,017 5,279 8,739 165.5%

Segment assets 1,906,893 1,778,351 128,543 7.2%

27

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

(individual risk provisions) both in Germany and in France were significantly below the planned risk costs.

Net commission income in the amount of EUR 3.5 million in 2014 consists of almost one half commissions as a result of guarantee business and one half commissions that are largely driven by the credit business.

Administrative expenses totalled EUR -10.9 mil-lion and were roughly EUR 4.2 million below the level in 2013. This is primarily due to a change in the cost system and cost allocations from the previous year. This also applies according-ly to other segments.

The segment assets in the amount of EUR 1,907 million showed slight growth in

comparison to the previous year, rising by EUR 129 million.

Real Estate (RES)

The Real Estate segment is responsible for the financing of commercial real estate in the SaarLB Group. The regional focus is also on the German target market already defined for the Corporate Customers segment and the French Grand East, with a focus on the Île-de-France. The management of French real estate investors is also handled mostly from the offices in Paris. Additionally, the Real Es-tate segment supports public private part-nership measures (PPP) for investments in infrastructure and education as well as other public construction measures in the German regional market.

Net interest income in the Real Estate seg-ment totalled EUR 30.2 million, remaining fairly stable as compared to 2013 (+1.5%) but it did not meet expectations and confirmed the forecast made in the middle of the year. This is due to the lack of new business in the French market, the lacking or very low number of market transactions in the Bank’s target segment as well as the substantially greater competition with new market competitors in the niche business < EUR 20 million. The re-sulting decreases in volumes in France were not compensated by the better development of business in Germany. The large shortfall in the development of new business also led to a corresponding reduction in the net commis-sion income.

The Real Estate segment was revalued and extended for a total of roughly EUR 375 mil-lion in the reporting period. Despite greater competition in both markets, SaarLB was able to achieve its planned margins. The develop-ment of new business remained significantly behind expectations in France in particular.

The risk provisions in the lending business of EUR -6.9 million remained on the level of 2013, deviating by just EUR 0.2 million (2.5%). The release of provisions in Germany and France were not able to compensate for newly cre-ated provisions. The majority of the risk pro-visions are attributable to the Real Estate France segment.

EUR ’000s 2014 2013 Δ thousand Δ in %

Net interest income 30,244 29,787 457 1.5%

Risk provisions in the credit business -6,919 -7,095 176 -2.5%

Net commission income 944 1,544 -600 -38.8%

Gain/loss on fair value measurement -576 0 -576 0.0%

Administrative expenses -8,412 -8,849 437 -4.9%

Earnings before taxes 15,281 15,386 -105 -0.7%

Segment assets 2,637,597 2,713,043 -75,446 -2.8%

28

The change in net commission income primar-ily depends on the new business volume and was – due to the low number of closings – sig-nificantly lower at EUR 0.9 million on 31 De-cember 2014 (-38.8%).

Administrative expenses totalled EUR -8.4 mil-lion in 2014 and are thus slightly below the lev-el of the previous year (EUR -8.8 million).

In total, segment assets amount to roughly EUR 2,638 million and are thus slightly below the level in 2013.

Projects (PF)

The Projects segment is responsible for the financing of projects in the SaarLB Group, es-pecially in the renewable energy sector, but also in the area of public private partnership (PPP) on the French market. The regional fo-cal point of business is in France.

Net interest income in the Projects seg-ment could be significantly increased in 2014, from roughly EUR 20.0 million to EUR 24.7 million (+23.5%). The main reason for this was the continuous expansion of the new lending business in 2014. In total, the Bank awarded credit in the amount of roughly EUR 350 million, which signifi-cantly exceeded the trend described in the 2013 forecast. Of this amount, almost 90% – more than in previous years – was attrib-utable to the French market, which again underscores the strong market position and the structuring and legal expertise of SaarLB as the Franco-German regional bank. In the German target market, new business was in line with expectations, but closures were significantly below the level in 2013 due to the restrictive impact of the Ger-man Renewable Energies Act (EEG). In the sub-segment PPP France, the Bank was able

to maintain its market position as a niche provider for midcap projects, as planned.

The use of the risk provisions was defined by the creation of new provisions in the area of other special finance in the past financial year, and they are also reported in the Pro-jects segment. The portfolio quality in the Renewable Energies segment continues to be linked to the very good level in 2013.

Net commission income of EUR 4.3 million is EUR -0.2 million below the previous year. This is mainly due to a decline in credit com-missions from lending in Germany, which could not be fully compensated by projects in France.

Administrative expenses amount to EUR -6.3 million and are thus below the level in 2013 (EUR -7.4 million).

EUR ’000s 2014 2013 Δ thousand Δ in %

Net interest income 24,675 19,983 4,692 23.5%

Risk provisions in the credit business -5,865 -7 -5,858 ***%

Net commission income 4,305 4,550 -246 -5.4%

Gain/loss on fair value measurement -181 0 -181 ***%

Administrative expenses -6,269 -7,437 1,168 -15.7%

Earnings before taxes 16,664 17,089 -425 -2.5%

Segment assets 2,001,401 1,790,396 211,005 11.8%

29

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

Segment assets in the business segment rose by EUR 211 million to EUR 2,001 million as of 31 December 2014.

Savings Banks, Institutionals and High Net Worth Individuals

Savings Banks, Institutionals and High Net Worth Individuals provides wealth advice and management to savings banks, institutional investors and high net worth individuals. The focus of the Savings Banks and Institutionals segment is on increasing existing customer connections as well as on expanding contacts with insurance companies and pension funds in the region and the business relationships to savings banks in Rhineland-Palatinate. An-other task consists in obtaining liquidity for institutional investors. It also deals with the financing of the region’s savings banks and municipalities.

New business in the area of municipalities ended the year at roughly EUR 122 million, which was significantly above the level in 2013 but below the expectations for the financial year. The forecast at midyear 2014 was con-firmed here. In contrast to this, the achieved

new business margins did meet expectations. For the first time, the business segment for municipal customers acted as the arranger for promissory notes and placed them with insti-tutional investors.

The special fund business thrived, which was seen in particular in a noticeable rise in the depository bank volume. The ongoing low lev-el of interest rates continued to hurt margins in the liabilities business over the course of the year.

In the business with high net worth private customers, the volume of liabilities contin-ued to enjoy a positive development, rising by just under 38% to roughly EUR 330 million at the end of the year. Due to the low interest environment, margins remain on a low level but slightly increased in comparison to the previous year.

The Wealth Management subsegment has been steadily expanded and is improving high net worth individuals’ awareness of SaarLB, particularly those with an entrepreneurial background.

EUR ’000s 2014 2013 Δ thousand Δ in %

Net interest income 6,457 4,430 2,027 45.7%

Risk provisions in the credit business 4 29 -25 -85.6%

Net commission income 4,772 3,775 998 26.4%

Gain/loss on fair value measurement -313 809 -1,122 -138.7%

Administrative expenses -5,939 -7,410 1,472 -19.9%

Earnings before taxes 4,982 1,633 3,349 205.1%

Segment assets 1,596,627 1,817,976 -221,349 -12.2%

Net interest income rose from EUR 4.4 million to EUR 6.5 million. The reasons for this were the increase in volumes, effects from inter-est book management, which had a positive impact on liability margins, and the good success in the placement of the Bank’s own is-sues with institutional investors and savings banks.

A risk provision in the lending business was not required to any significant extent at the time this annual report was prepared, similar to 2013. This reflects the good quality of the portfolio in the segments of Savings Banks, High Net Worth Individuals and Institution-als.

30

Net commission income improved signifi-cantly year on year to EUR 4.8 million (2013: EUR 3.8 million), which is mainly due to a rise in securities and commission income. Besides the classical securities business, the commis-sion business also made a major contribution. The development of the commission business reflects the forecasts made in midyear 2014.

Administrative expenses in the amount of EUR -5.9 million are below the level of the pre-vious year (EUR -7.4 million).

The segment assets, which have been defined by municipal financing and (in the past) the refinancing of savings banks, fell from roughly EUR 1,818 million to around EUR 1,597 million on account of scheduled repayments.

Treasury and Portfolio Management (TP)

The Treasury and Portfolio Management seg-ment is responsible for the classical treasury functions, including management of the in-terest rate risk (asset-liability management) and liquidity, as well as the management of the securities portfolio that is primarily held for liquidity purposes (Securities Account A and LCR Portfolio) and the management of the Bank’s strategic own investments (direct

investments and special funds). In addition, the segment is also responsible for the man-agement of all the portfolios that are no longer included in the Bank’s core business, including investments in international banks and corporate addresses outside of the core of Europe, international commercial real estate finance, securitisations and various smaller subportfolios. Over the medium term, SaarLB would like to sell and run off these re-duction portfolios, 80% of which have invest-ment grade securities.

Thanks to new business of roughly EUR 563 million, which was significantly above the budget, the portfolio volume in Securities Account A will remain at roughly the same level as in the previous year despite the high repayment volumes of EUR 2.3 bil-lion. The LCR portfolio required for Basel III remains on the level of the previous year at roughly EUR 0.3 billion. The development of volumes and income reported here confirms the forecast made in the middle of 2014.

With assets of EUR 1.0 billion at the end of 2014, the reduction portfolio decreased, as planned, by another EUR 0.6 billion since the beginning of 2014.

The reclassification of a subportfolio to Oth-er items/Overhead produced slight shifts in

various items relative to their disclosure in the previous year.

EUR ’000s 2014 2013 Δ thousand Δ in %

Net interest income 27,701 34,632 -6,932 -20.0%

Risk provisions in the credit business 2,182 -8,612 10,794 -125.3%

Net commission income -878 -453 -425 93.9%

Gain/loss on fair value measurement 45,079 1,056 44,023 4,169.3%

Gain/loss on investments 911 -2,947 3,858 -130.9%

Administrative expenses -7,424 -10,485 3,062 -29.2%

Earnings before taxes 67,572 13,191 54,381 412.3%

Segment assets 3,746,522 4,285,141 -538,620 -12.6%

31

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

Net interest income in the amount of EUR 27.7 million was below the level of EUR 34.6 million in 2013. This is due, on the one hand, to the decreasing net interest in-come from the reduction portfolio but also the weaker disposition and maturity-trans-formation results that are hurt by the ongo-ing low interest rates.

Risk provisions in the lending business could be overcompensated by the release of provi-sions during the reporting period and amount-ed to EUR +2.2 million (2013: EUR -8.6 million).

Furthermore, net commission income fell by EUR -0.4 million to EUR -0.9 million, with the commission expenses for the securities and deposit business being the reason.

This stands in relation to the positive fair val-ue gains, which primarily result from interest swaps and amount to EUR 45.1 million. Inter-est derivatives concluded in the Treasury and Portfolio Management segment are primarily used for SaarLB’s interest book management. The significant deviation from the previous year results from the fair value effects distrib-uted across the segments for the first time, in particular the fair value effects from interest derivatives. In the previous year, these com-ponents were still reported in Other items/Overhead.

The gains/losses on investments mainly re-late to securities in the reduction portfolio and totalled EUR 0.9 million, which is signif-icantly above the amount of EUR -2.9 million in the previous year.

Administrative expenses of EUR -7.4 million were significantly below the level of the pre-vious year (EUR -10.5 million).

Segment assets declined as planned – due to the development of the reduction portfolio – and were at a level of EUR 3,747 million, down EUR -538 million in comparison to the dead-line in the previous year.

Landesbausparkasse Saar (LBS)

Privately used real estate was financed in close collaboration with the Saarland savings banks exclusively through the Landesbaus-parkasse Saar, which belongs to SaarLB.

As of 31 December 2014, the credit volume was EUR 0.7 billion higher than the level as of 31 December 2013. The rate of increase in the credit volume is thus around 11.0%.

The new business volume in home loan sav-ings deposits again increased substantially from the record 2013 financial year, by roughly 12.4%, and amounted to EUR 652 million.

EUR ’000s 2014 2013 Δ thousand Δ in %

Net interest income 17,998 17,237 761 4.4%

Risk provisions in the credit business -102 -95 -7 7.0%

Net commission income -3,056 -2,861 -196 6.8%

Administrative expenses -12,016 -10,958 -1,058 9.7%

Other income 379 560 -181 -32.4%

Earnings before taxes 3,203 3,884 -681 -17.5%

Segment assets 830,690 758,462 72,228 9.5%

32

Net interest income rose again from EUR 17.2 million in 2013 to EUR 18.0 million over the course of 2014. This development confirms the forecast made at midyear 2014.

The risk provisions in the home loan savings business showed a sideways trend in 2014, to-talling EUR -0.1 million (2013: EUR -0.1 million).

Commission income was heavily influenced by the brokerage business for savings banks and continued to follow the trend in 2013, reducing the segment’s income by roughly EUR -3.1 million (2013: -2.9 million). This in-crease is due to the very positive new busi-ness in the current financial year. In contrast, sustainable higher net interest income will be generated over the next few years. The

assumed forecast was also confirmed for this item.

Administrative expenses at Landesbaus-parkasse rose from EUR -11.0 million to EUR -12.0 million. The reasons for this were mainly the increase in personnel expenses as well as legal and audit costs relative to 2013.

The income at Landesbausparkasse as of 31 December 2014 was 17.5% below the amount in 2013 and reached EUR 3.2 million.

Segment assets at Landesbausparkasse in-creased by roughly 9.5%, from EUR 758 mil-lion to EUR 831 million.

FINANCIAL POSITIONThe financial position of SaarLB also contin-ued to be good in 2014. The inflow of liquidity due to the current refinancing structures has been secured for the next few years.

The mortgage cover in accordance with Sec-tion 28 PfandBG (German Pfandbrief Act) totalled EUR 704 million, slightly exceeding the amount from 2013 (EUR 698 million) by EUR 6 million. Greater usage of the cover funds for refinancing simultaneously led to a significant increase in the Pfandbriefe (cov-ered bonds) in circulation, so the cover was significantly lower in 2014 at roughly 69% than it was at the end of 2013 (roughly 105%) but still easily in line with the regulatory re-quirements.

The public sector cover funds in accordance with Section 28 PfandBG and the correspond-ing public sector Pfandbriefe in circulation continued to decrease due to maturities and ongoing new business. The total amount

of the cover funds fell moderately from EUR 1,797 million on 31 December 2013 to EUR 1,617 million on 31 December 2014. The cover is roughly 46% as of 31 December 2014, which is slightly below the amount at the end of 2013 (roughly 54%), but substantially above the regulatory requirements.

The situation on the capital market contin-ues to be stable as compared to financial year 2013, from the perspective of SaarLB. With almost EUR 989 million (2013: EUR 778 mil-lion), the placed volumes in 2014 are on a high level and occurred almost entirely as part of private placements with customers and finan-cial partners, as in past years. Roughly half of the funds received were from the network of savings banks and Landesbanks. Investor loy-alty therefore remains of central importance for SaarLB. As a result, SaarLB was largely in-dependent of capital markets in the current financial year 2014, as in 2013. In the process, SaarLB – similar to 2013 – also succeeded in

33

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

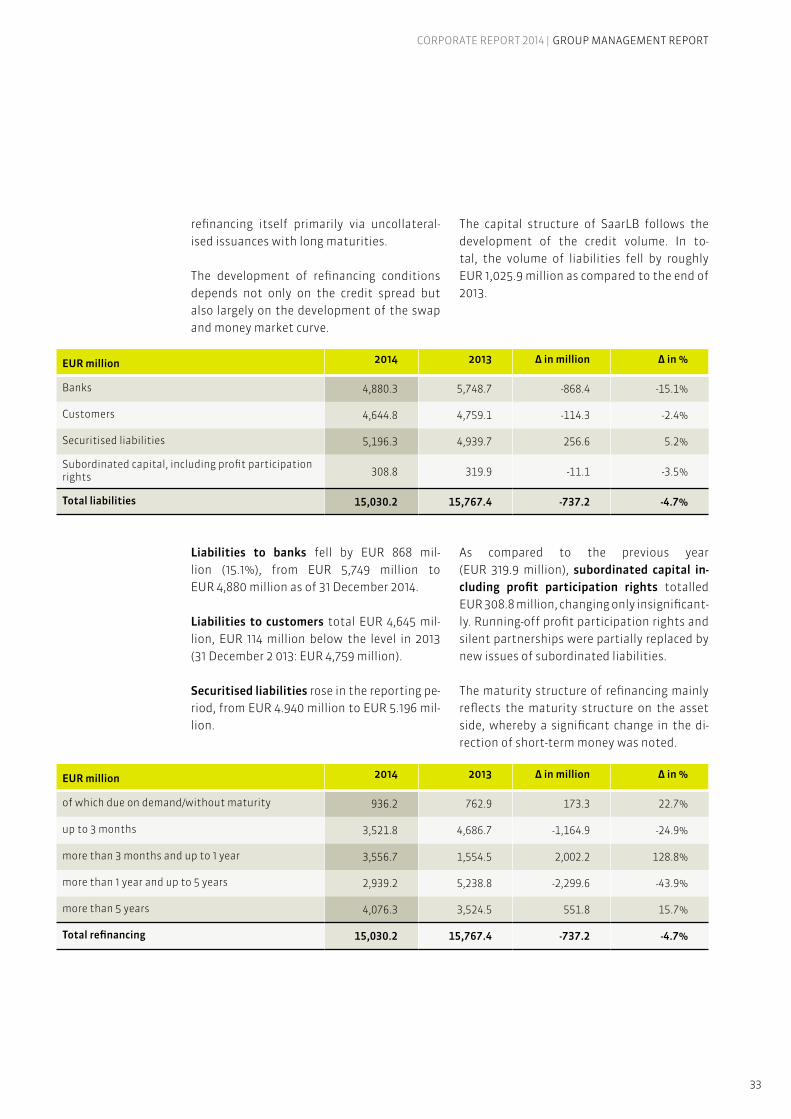

refinancing itself primarily via uncollateral-ised issuances with long maturities.

The development of refinancing conditions depends not only on the credit spread but also largely on the development of the swap and money market curve.

The capital structure of SaarLB follows the development of the credit volume. In to-tal, the volume of liabilities fell by roughly EUR 1,025.9 million as compared to the end of 2013.

Liabilities to banks fell by EUR 868 mil-lion (15.1%), from EUR 5,749 million to EUR 4,880 million as of 31 December 2014.

Liabilities to customers total EUR 4,645 mil-lion, EUR 114 million below the level in 2013 (31 December 2 013: EUR 4,759 million).

Securitised liabilities rose in the reporting pe-riod, from EUR 4.940 million to EUR 5.196 mil-lion.

As compared to the previous year (EUR 319.9 million), subordinated capital in-cluding profit participation rights totalled EUR 308.8 million, changing only insignificant-ly. Running-off profit participation rights and silent partnerships were partially replaced by new issues of subordinated liabilities.

The maturity structure of refinancing mainly reflects the maturity structure on the asset side, whereby a significant change in the di-rection of short-term money was noted.

EUR million 2014 2013 Δ in million Δ in %

Banks 4,880.3 5,748.7 -868.4 -15.1%

Customers 4,644.8 4,759.1 -114.3 -2.4%

Securitised liabilities 5,196.3 4,939.7 256.6 5.2%

Subordinated capital, including profit participation rights 308.8 319.9 -11.1 -3.5%

Total liabilities 15,030.2 15,767.4 -737.2 -4.7%

EUR million 2014 2013 Δ in million Δ in %

of which due on demand/without maturity 936.2 762.9 173.3 22.7%

up to 3 months 3,521.8 4,686.7 -1,164.9 -24.9%

more than 3 months and up to 1 year 3,556.7 1,554.5 2,002.2 128.8%

more than 1 year and up to 5 years 2,939.2 5,238.8 -2,299.6 -43.9%

more than 5 years 4,076.3 3,524.5 551.8 15.7%

Total refinancing 15,030.2 15,767.4 -737.2 -4.7%

34

Reported equity rose by EUR 162.6 million, from EUR 584.9 million at the end of 2013 to EUR 747.5 million. The change is mainly due to the increase in the subscribed capital and the reinvestment of profits from 2013, as well as an increase in new valuation reserves. The retained profit rose from EUR 27.2 million as of 31 December 2013 to EUR 52.7 million at the end of 2014.

Please refer to the “Risk report” section for an explanation of the regulatory capital re-quirements and the resulting regulatory key performance indicators.

Off-balance sheet liabilities of SaarLB are primarily affected by irrevocable credit com-mitments and contingent liabilities. With a total volume of EUR 807.6 million as of 31 De-cember 2014, these liabilities are of only in-significant importance for an assessment of the financial position, as in the previous year (EUR 961.7 million).

In the past financial year, as in 2013, there were not committed credit lines for the ben-efit of SaarLB.

In order to ensure solvency at all times, SaarLB deposited securities amounting to roughly EUR 1,161 million at the Bundesbank, as in 2013 (EUR 1,024 million). Payment obliga-tions could therefore be met independently of other sources of refinancing.

Please refer to the “Risk report” for an expla-nation of the liquidity management.

Due to SaarLB’s business activity focused on Germany and France, the portion of the hedge for net positions in foreign currencies is insig-nificant. Both the new awarding of loans and the corresponding refinancing take place pri-marily in EUR. Still existing foreign currency portfolios are primarily assigned to the reduc-tion portfolio.

The use of derivative financial instruments is overwhelmingly to hedge the Bank’s own in-terest rate risk as part of asset/liability man-agement. The nominal volume rose moderate-ly, by EUR 624 million, to EUR 16,429 million (2013: EUR 15,805 million). Roughly 95% of this relates to interest swaps.

SaarLB’s ability to meet its payment obliga-tions was ensured at all times in the financial year.

SaarLB’s access to money and capital markets is supported by the credit ratings of two in-ternational rating agencies. Fitch lowered the outlook for the long-term rating to negative in April 2014. This step was justified by a forth-coming change in the method for valuing the support rating as a result of the change in the EU rules on “bail-ins”. The viability rating that reflects the internal financial strength of the Bank was confirmed by Fitch at its current lev-el in June 2014.

Rating Moody’s Fitch Ratings

Long-term rating (uncollateralised)

with government liability Aa1 AAA

without government liability A3 A

Outlook Negative Negative

Short-term rating (uncollateralised) P-2 F1

Financial strength/viability rating D bb+

35

CORPORATE REPORT 2014 | GROUP MANAGEMENT REPORT

In summary, the business performance in 2014 was positive overall, but in particular the net interest income was hurt by the on-going low interest phase and remained below the Bank’s expectations. The development of

SaarLB’s loan-driven core business segments and refinancing options was overall in line with the Bank’s expectations, however.