corporate governance index 2015 · 4 it is my pleasure to present the iia sa’s third edition of...

TRANSCRIPT

1

CORPORATE GOVERNANCE INDEX 2015

2

ProgressThrough SharingThe Institute of Internal Auditors South Africa (IIA SA) is part of an international network representing the interests of internal auditors worldwide and is the internationally recognised authority, standard setter, principal educator and acknowledged leader in certification, research and technological guidance for the profession of internal audit. The IIA SA provides internal auditors with the support and opportunities to develop to their fullest potential.

We serve internal auditors by offering

• TechnicalGuidance• ProfessionalTrainingPrograms• CertificationPrograms• ContinuingProfessionalDevelopmentOpportunities• ConferencesandNetworkingOpportunities• ExecutiveLeadershipNetwork

BecomeamemberoftheInstituteandjoinacommunityofdynamicprofessionals

AllrelevantinformationforbecomingamemberoftheIIASAisavailableonWebsite: www.iiasa.org.za. Alternatively you can contact us on: Telephone: 011 450 1040 or E-mail: [email protected] Progress Through Sharing

3

FOREWORD 4

EXECUTIVESUMMARY 5

RESEARCHMETHODOLOGY 6

SURVEYRESULTS 7

OVERALLRESULTS 7

DEMOGRAPHICDATA–I.E.ECONOMICSECTORS(%) 8

RESULTSPERDIMENSION 9-18

MAINFINDINGS 19

THEWAYFORWARD 20

APPENDIX1:SUMMARYOFANSWERSTOSURVEYQUESTIONS(%) 21-22

CONTENTs

The information contained in this report is intended to provide the reader with general information and guidance and may not be applicable in all circumstances.

The information herein should not be regarded as professional or legal advice or the official opinion of the Institute of Internal Auditors of South Africa (IIA SA).

We have taken all reasonable measures to ensure the quality and accuracy of the information. However, no action should be taken on the basis of the information without obtaining professional advice. As such, the IIA SA shall not be held liable for any damage, loss or liability of any nature incurred directly or indirectly by whomever and resulting from any cause in connection with the information contained herein.

4

ItismypleasuretopresenttheIIASA’sthirdeditionoftheCorporateGovernanceIndex–An Internal Audit Perspective.

While Iampleasedtoseethatwherethe Indexdoesnotshowadeclineagainstlastyear’soverallscore,thefactthatwehavenotregainedgroundagainstthe2013resultsisveryconcerning.Idohopethatwewillbeabletorecoverandthatthe2.9scorewillnotbecomethenewyardstick.

Corporate governance, previously considered a mere aspiration, is becomingincreasingly importantwithinalleconomicspheresandtheCAE’s role isprovingto be one of great importance in promoting good governance principles. CAEshave the ability tobe catalysts, as a trusted advisor, for ensuring that corporategovernancewithin their organisations is at the forefrontof the executive team’sstrategic agenda.

ThisreportmeasurestheperceptionofCAEsregardingthestateofcorporategovernanceasitcurrentlystandswithintheirrespectiveorganisations.Theresearchnotonlyprovidesinsightintocurrentperceivedstrengthsandweaknesses,butalsoacomparativeofpreviousresults,thustrackingtheprogressoftheimplementationofbestpractisecorporategovernanceprinciplesaspertheKingCodesofGovernance.

IbelievethatthisIndexhaswideapplication.ItoffersabarometeronthestateofgovernanceinSouthAfricanorganisationsandisalsoagreat toolwhichprovides leaderswith theability tomeasure theirorganisationsagainst theSouthAfricannorm. It isimportantthatleadersdonotbecomecomplacentwhentheyfindthemselvesonparwiththenorm,butratherstrivetoscoreafourineachdimension:Boards,AuditCommittees,Managementand/orExecutivecommitteesandotheroversightbodiesshouldusethevariousdimensionsoftheIndexasdiscussionpointsonhowgovernanceshouldimproveintheirorganisations.

ItisclearfromthereportthattheareawhereorganisationsinSouthAfricastrugglethemostisinthedimensionofexternalrisk.Giventhecontextofa fastchangingworldand increasingcomplexitywhich leadershavetocontendwith, this isasignificantfindingwithnegativeimplicationsfortheSouthAfricaneconomy.Thelessvigilantorganisationalleadersare,themorevulnerabletheSouthAfricaneconomybecomes.Leadersmustthereforeunderstandtheirvigilance/negligenceinthecontextoftheimpactontheirorganisationsandthehealthoftheeconomy.

The researchmethodology underpinning the Corporate Governance Index has been facilitated by our research collaborationwiththeCentrefortheStudyofGovernanceInnovation(GovInn)attheUniversityofPretoria,headedupbyProfessorLorenzoFioramonti.IwouldliketosincerelythankProfessorFioramontiandhisteamfortheireffortsandinsights.MythanksalsoextendtoallCAEswhoparticipatedinthesurvey.Withoutyourwillingnesstoshareyourviews,thisvaluableIndexwouldnothavebeenpossible.

Ihopetohearfromyou,whetheritisintermsofthoughts,suggestionsorideas,yourfeedbackisalwayswelcome.

Dr Claudelle von EckChief Executive OfficerThe Institute of Internal Auditors South Africa August 2015

FOREWORD

5

TheIIASA’sCorporateGovernanceIndexreflectstheviewsofChiefAuditExecutives(CAEs),whoarewellpositionedtoprovidearelativelyimpartialviewofthestateofcorporategovernanceinSouthAfrica.

ThethirdeditionoftheIndexbuildsonthesecondeditionreleasedin2014andisintendedtoprovideacomparativeanalysisoftheperceivedperformanceofSouthAfricanorganisationsincertainkeydimensionsofcorporategovernance.TheIndex,whichwasdevelopedthroughthemethodologicalassistanceoftheCentrefortheStudyofGovernanceInnovation(GovInn)attheUniversityofPretoria,providesabaselineforthemeasurementofperformancefortheentirecountrysinceitsurveysalleconomicsectors1. TheresearchmethodologywhichwascrystallisedinthesecondeditionoftheIndexincludesanincreasednumberofdimensionsmeasuredandhasbeenappliedinthethirdeditionoftheIndex.Thefollowingcriticaldimensionswerecoveredbythesurvey-Ethics,Compliance,Leadership,RiskManagement(OperationalandExternalRisks),PerformanceandInternalAudit.

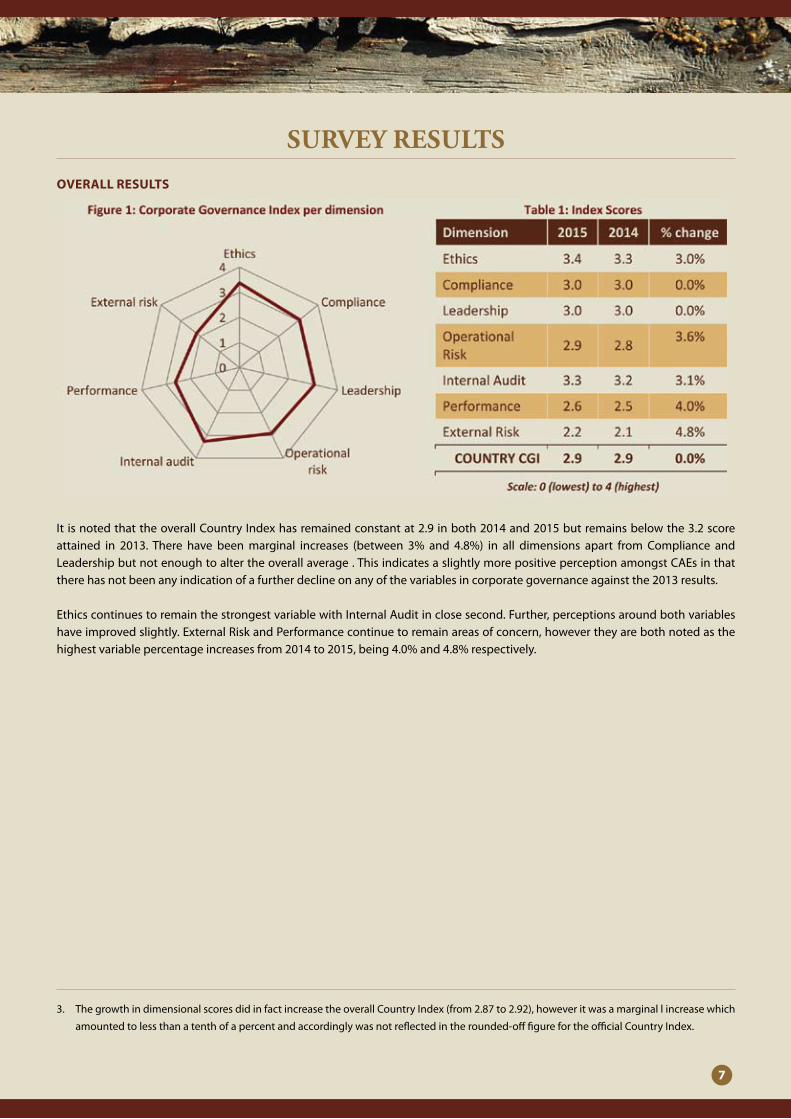

1. TheoverallCountryIndexforCorporateGovernanceinSouthAfricahasremainedconstantat2.9inboth2014and2015(outofamaximumscoreof4).Thisconsistencymaybeviewedintwolights,namely,thatthereisaperceptionofstabilityregardingthecorewell-performingdimensionsandfurtherthatthereisaperceptionthatthedimensionswhichrequirefurtherelevationhaveremainedstagnantoverthelastyear.Inaddition,thescoreremainslowerthanthe2013overallscoreof3.Despitetheoverallscoreremainingconstant,therehavebeenslightincreasesin5ofthe7dimensions,with2remainingconstantandnooverall score decreases noted2.

2. Adherence to ethical principles (3.4) continues to remain the best performing dimension,with Internal Audit (3.3) closelyfollowing.Theimprovementintheethicsdimensionshouldbelookedatinrelationtothedropin2014againstthe2013results.Theoverall3.4scoreisonparwiththe2013score.Thereisaperceptiongapbetweenthetonebeingset(66%)andtheactualculture(60%),amongstthosewhoratedthetwocategoriesintheethicsdimension‘stronglyagree’.Thissuggeststhatleadersshouldalsofocusonwhetherthetonebeingsetdoesactuallyfilterdownthroughoutthewholeorganisation.

3. TheareasofconcernraisedbyrespondentsremainPerformanceandRiskManagement(inparticularwithregardtoExternalRisk).).Afastchangingworldthatbringsincreasedcomplexitiesasaresultoffactorssuchasevolvingsocio-economicandpolitical contexts, shifting economic and political power, changing consumer concerns and buying behaviour, emergingtechnology,cyber-attacks, climatechange, shifting regulations, increasingconvergenceandcompetition,globalisationandemergingenergycrises,necessitatesagreateremphasisonriskmanagement.Thefactthatorganisationsareclearlynotplacingenough emphasis on riskmanagement is very concerning It is however noted that despite the fact that they remain lowperformingdimensions,therehavebeenmarginalincreasesinthescoresofPerformanceandRiskManagement(bothinternalandexternal).ThissuggestssomeimprovementintheperceptionofCAEsaroundthesedimensions.

4. Overall,theperceptionofCAEsregardingallquestionsansweredhaseitherimprovedslightlyorremainedconstant,savefordimensionsrelatingtoExternalRisk,ComplianceandPerformancewhichhaveseenslightdeclinesinstronglyagreeresponsesnotexceeding4%.

5. Inrespectofthequestionsposed,themostfavourableresponsereceivedwasthat70%ofCAEsstronglyagreedthatInternalAuditwasaffordeda“sufficientdegreeofindependence”withintheirorganisation.TheleastfavourableresponsewasinrespectofExternalRisk,withonly13%ofCAEsindicatingastronglyagreeviewregardingthisquestion(a4%declinefrom2014).

EXECUTIVE sUMMARY

1. TheCentrefortheStudyofGovernanceInnovation(GovInn)isdirectedbyProf.LorenzoFioramontiandislocatedattheUniversityofPretoria.

MoreinformationaboutGovInncanbefoundatwww.governanceinnovation.org

2. ThegrowthindimensionalscoresdidinfactincreasetheoverallCountryIndex(from2.87to2.92),howeveritwasamarginalincreasewhich

amountedtolessthanatenthofapercentandaccordinglywasnotreflectedintheroundedofffigurefortheofficialCountryIndex.

6

Thecoredimensionsofcorporategovernancewereidentifiedandappropriatequestionsrelatingtoeachdimensionwerecrafted.Thesurveyconsistedofthreedemographics-relatedquestions,23multiplechoicequestionsandoneopen-endedquestion.The23singleresponsemultiplechoicequestionsweredesignedtocoverthefollowingdimensionsofcorporategovernance:Ethics,Compliance,Leadership,RiskManagement(i.e.OperationalRiskandExternalRisk),PerformanceandInternalAudit.EachofthefollowingpotentialresponseswasassignedavalueasfollowsinordertoaggregatescoresintoanIndexthatwillbetrackedovertime:

0= strongly disagree; 1=slightly disagree; 2=neither agree nor disagree; 3=somewhat agree; 4=strongly agree

ThesurveywasdirectedatSixhundred(600)ChiefAuditExecutives(CAEs)ontheIIASAdatabase,whichtooktheformofaself-administeredweb-basedquestionnaire.CAEsatprofessionalservicesfirmswerespecificallyrequestedtoreportonatypicalclient,ratherthanontheirownfirms.Itwascriticalthatthesurveyelicitedthemosthonestresponsespossible.Consequently,nopersonaldemographicdatawasaskedfor.OveraperiodofeightweeksduringMarch,AprilandMay2015,atotalofTwohundredandseventyone(271)respondentscompletedthesurvey.

REsEARCH METHODOLOGY

ThE InsTITuTE of InTErnal audITors aT a quIck glancE

TheInstituteofInternalAuditorsSouthAfrica(IIASA)isaSection21non-profitorganisation,affiliatedtotheglobalInstituteofInternalAuditorsInc.(IIAInc)asaNationalInstitute.Establishedin1941,theIIAInc.hasmorethan180000membersworldwide. Itservesastheinternalauditprofession’sglobalvoice,recognizedauthority,acknowledgedleader,principaleducator, and chief advocate. The Institute is the creator and custodian of the universal International Standards for the ProfessionalPracticeof InternalAuditing.The IIASAsets thecareerpathstandards for internalauditors inSouthAfrica,promotestheProfessioninthecountryaswellaspromotesadherencetotheIIAstandards.IIASAmembersareaccountable

totheInstituteintermsoftheirconductasprescribedintheIIACodeofEthics.

The IIA SA’sover 8000-strongmembership represents the third largest affiliate in theworld, secondonly to theUSA&Canada,andtheUnitedKingdom.SouthAfricahasrepresentativesonallthemajorIIAIncinternationalcommitteesandin

theprocessmakesasignificantcontributiontothedirectionoftheProfessionglobally.

Aninternalauditor’sfunctionistoevaluatethecontrolsthatanorganisationhasinplacetocounteranyrisksthatmaypreventtheorganisationfromachievingitsobjectives.Toensurethis,theinternalauditortestscontrols,examinesprocesses,andbuildsmodelsofbestpractice.Inrecentyearstheexpectationsplacedoninternalauditorshaveincreaseddramatically.Thisismainlyduetotheincreasedcomplexityandvolatilityinthemarket,whichresultsinincreasedrisks,thatorganisationsarenowcontinuallyfacedwith.Inaddition,KingIIIhasplacedagreateremphasisontheimportanceofinternalaudit.TheInstitute’sprimaryroleistosupportitsmembersinmeetingmarketexpectations.Membershipsupportrevolvesaround

professionaladvice,trainingandmanyotherservices.

MembershipoftheIIASAspeakstothecredibilityoftheinternalauditorastheindividualisrequiredtoworkinaccordancewiththeInternationalStandards(IPPF)andisbeingheldaccountableagainstatheCodeofEthics.Aretheinternalauditors

inyourorganisationmembersoftheIIASA?Toverify,doamembersearchonourwebsitewww.iiasa.org.za.

7

oVErall rEsulTs

It isnotedthattheoverallCountryIndexhasremainedconstantat2.9inboth2014and2015butremainsbelowthe3.2scoreattained in 2013. There have beenmarginal increases (between 3% and 4.8%) in all dimensions apart from Compliance andLeadershipbutnotenoughtoaltertheoverallaverage.ThisindicatesaslightlymorepositiveperceptionamongstCAEsinthattherehasnotbeenanyindicationofafurtherdeclineonanyofthevariablesincorporategovernanceagainstthe2013results.

EthicscontinuestoremainthestrongestvariablewithInternalAuditinclosesecond.Further,perceptionsaroundbothvariableshaveimprovedslightly.ExternalRiskandPerformancecontinuetoremainareasofconcern,howevertheyarebothnotedasthehighestvariablepercentageincreasesfrom2014to2015,being4.0%and4.8%respectively.

sURVEY REsULTs

3. ThegrowthindimensionalscoresdidinfactincreasetheoverallCountryIndex(from2.87to2.92),howeveritwasamarginallincreasewhich

amountedtolessthanatenthofapercentandaccordinglywasnotreflectedintherounded-offfigurefortheofficialCountryIndex.

8

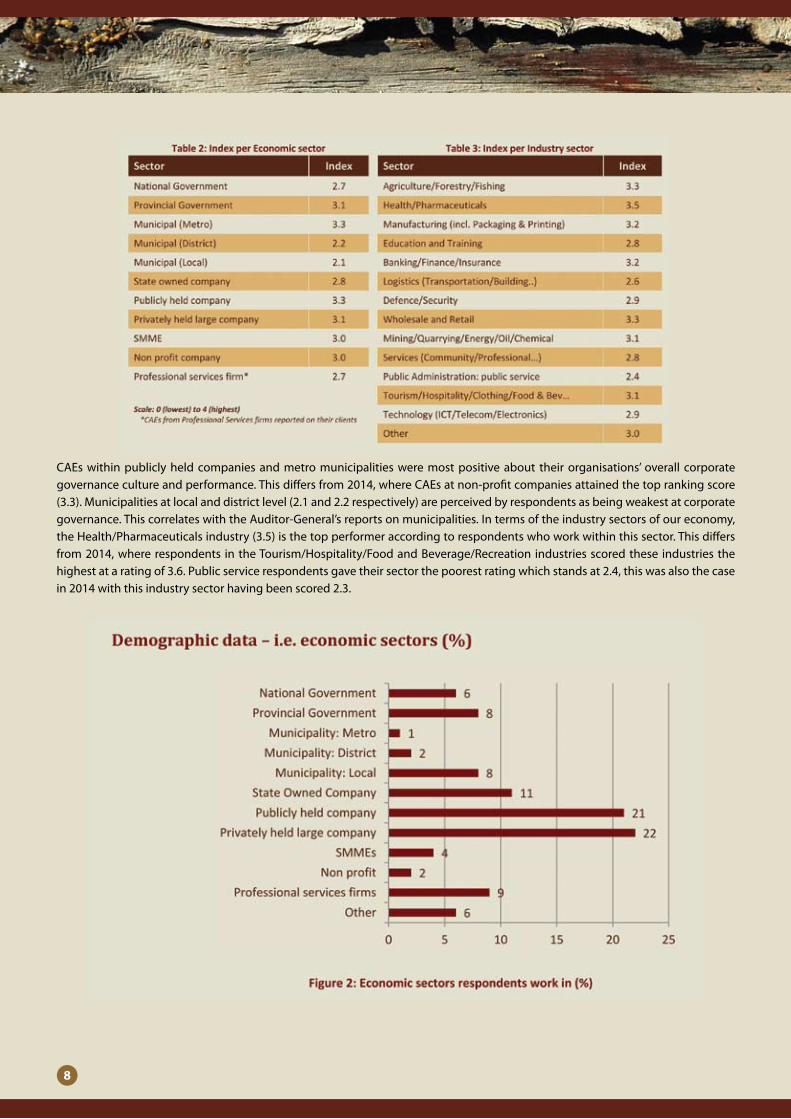

CAEswithinpubliclyheldcompaniesandmetromunicipalitiesweremostpositiveabout theirorganisations’overall corporategovernancecultureandperformance.Thisdiffersfrom2014,whereCAEsatnon-profitcompaniesattainedthetoprankingscore(3.3).Municipalitiesatlocalanddistrictlevel(2.1and2.2respectively)areperceivedbyrespondentsasbeingweakestatcorporategovernance.ThiscorrelateswiththeAuditor-General’sreportsonmunicipalities.Intermsoftheindustrysectorsofoureconomy,theHealth/Pharmaceuticalsindustry(3.5)isthetopperformeraccordingtorespondentswhoworkwithinthissector.Thisdiffersfrom2014,whererespondents intheTourism/Hospitality/FoodandBeverage/Recreation industriesscoredthese industriesthehighestataratingof3.6.Publicservicerespondentsgavetheirsectorthepoorestratingwhichstandsat2.4,thiswasalsothecasein2014withthisindustrysectorhavingbeenscored2.3.

9

(Inthissectionsomeresultsarehighlighted.Thefulllistofquestionsandresponsesareonpages16and17)

EThIcs

Typicalquestion:Ethicsisanimportantpartofyourorganisationalculture

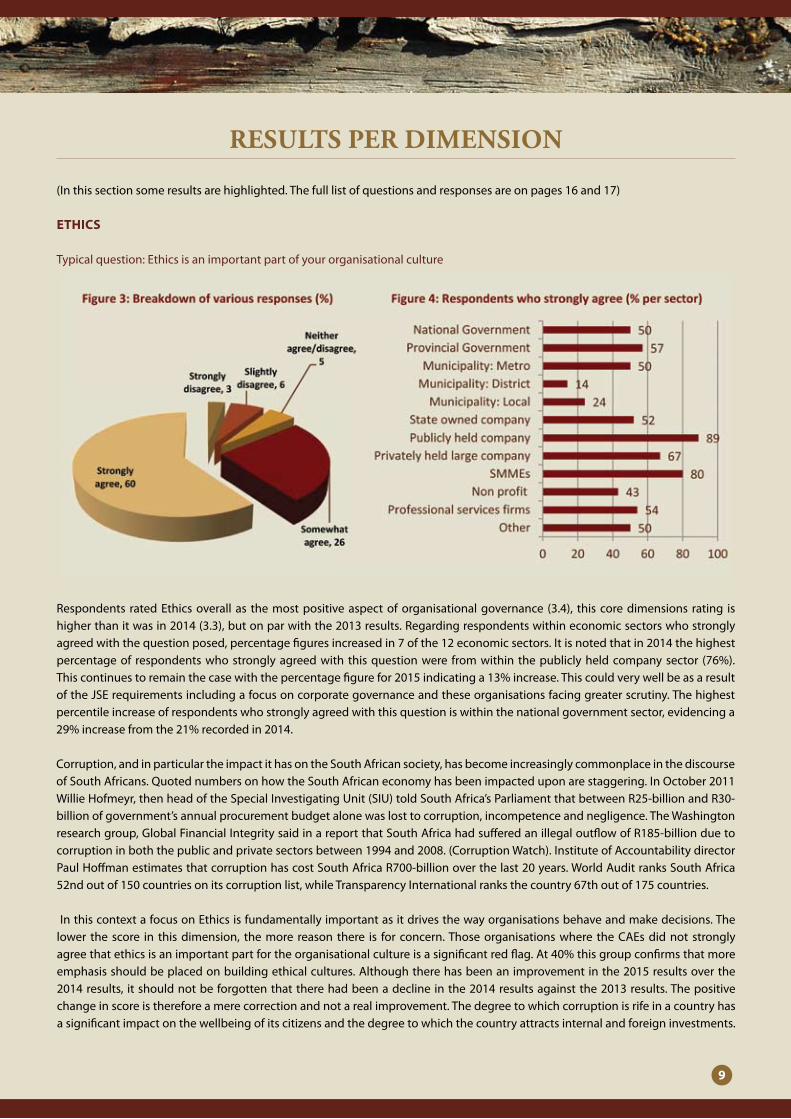

Respondents ratedEthicsoverallas themostpositiveaspectoforganisationalgovernance (3.4), thiscoredimensions rating ishigherthanitwasin2014(3.3),butonparwiththe2013results.Regardingrespondentswithineconomicsectorswhostronglyagreedwiththequestionposed,percentagefiguresincreasedin7ofthe12economicsectors.Itisnotedthatin2014thehighestpercentageof respondentswhostronglyagreedwith thisquestionwere fromwithin thepubliclyheldcompanysector (76%).Thiscontinuestoremainthecasewiththepercentagefigurefor2015indicatinga13%increase.ThiscouldverywellbeasaresultoftheJSErequirementsincludingafocusoncorporategovernanceandtheseorganisationsfacinggreaterscrutiny.Thehighestpercentileincreaseofrespondentswhostronglyagreedwiththisquestioniswithinthenationalgovernmentsector,evidencinga29%increasefromthe21%recordedin2014.

Corruption,andinparticulartheimpactithasontheSouthAfricansociety,hasbecomeincreasinglycommonplaceinthediscourseofSouthAfricans.QuotednumbersonhowtheSouthAfricaneconomyhasbeenimpacteduponarestaggering.InOctober2011WillieHofmeyr,thenheadoftheSpecialInvestigatingUnit(SIU)toldSouthAfrica’sParliamentthatbetweenR25-billionandR30-billionofgovernment’sannualprocurementbudgetalonewaslosttocorruption,incompetenceandnegligence.TheWashingtonresearchgroup,GlobalFinancialIntegritysaidinareportthatSouthAfricahadsufferedanillegaloutflowofR185-billionduetocorruptioninboththepublicandprivatesectorsbetween1994and2008.(CorruptionWatch).InstituteofAccountabilitydirectorPaulHoffmanestimatesthatcorruptionhascostSouthAfricaR700-billionoverthelast20years.WorldAuditranksSouthAfrica52ndoutof150countriesonitscorruptionlist,whileTransparencyInternationalranksthecountry67thoutof175countries.

InthiscontextafocusonEthicsisfundamentallyimportantasitdrivesthewayorganisationsbehaveandmakedecisions.Thelower the score in thisdimension, themore reason there is for concern.Thoseorganisationswhere theCAEsdidnot stronglyagreethatethicsisanimportantpartfortheorganisationalcultureisasignificantredflag.At40%thisgroupconfirmsthatmoreemphasisshouldbeplacedonbuildingethicalcultures.Althoughtherehasbeenanimprovementinthe2015resultsoverthe2014results, itshouldnotbeforgottenthattherehadbeenadecline inthe2014resultsagainstthe2013results.Thepositivechangeinscoreisthereforeamerecorrectionandnotarealimprovement.Thedegreetowhichcorruptionisrifeinacountryhasasignificantimpactonthewellbeingofitscitizensandthedegreetowhichthecountryattractsinternalandforeigninvestments.

REsULTs PER DIMENsION

10

Corruptionincreasesthecostofbusiness,leadstowasteortheinefficientuseofpublicresources,excludespoorpeoplefrompublicservicesandperpetuatespoverty,erodespublictrust,underminestheruleoflawandultimatelydelegitimisesthestate(OECD).Theultimatecostofcorruptionshouldencourageleaderstoproactivelypromoteethicalculturesintheirorganisationsandensurethat the right tone is set at the top.

coMPlIancE

Typicalquestion:Yourorganisationcomplieswithrelevantlegislation,regulationsandstandards

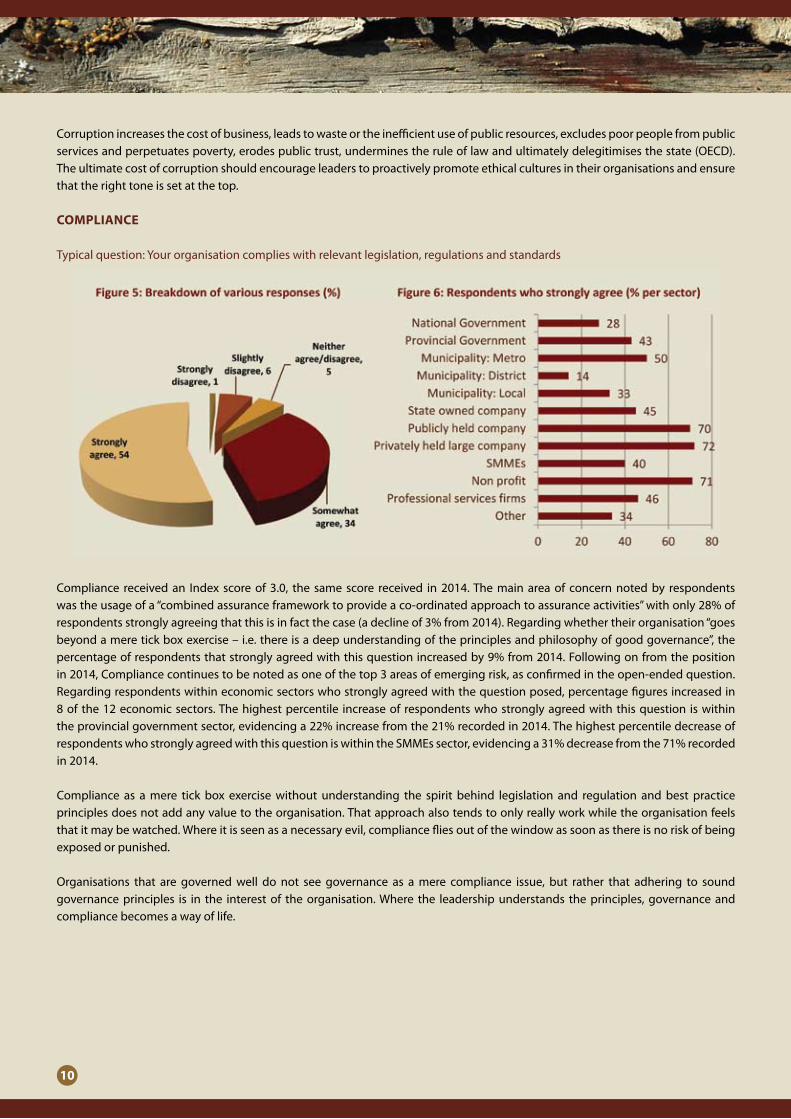

Compliance receivedan Index scoreof3.0, the same score received in2014.Themainareaof concernnotedby respondentswastheusageofa“combinedassuranceframeworktoprovideaco-ordinatedapproachtoassuranceactivities”withonly28%ofrespondentsstronglyagreeingthatthisisinfactthecase(adeclineof3%from2014).Regardingwhethertheirorganisation“goesbeyondameretickboxexercise–i.e.thereisadeepunderstandingoftheprinciplesandphilosophyofgoodgovernance”,thepercentageofrespondentsthatstronglyagreedwiththisquestionincreasedby9%from2014.Followingonfromthepositionin2014,Compliancecontinuestobenotedasoneofthetop3areasofemergingrisk,asconfirmedintheopen-endedquestion.Regardingrespondentswithineconomicsectorswhostronglyagreedwiththequestionposed,percentagefiguresincreasedin8of the12economicsectors.Thehighestpercentile increaseof respondentswhostronglyagreedwiththisquestion iswithintheprovincialgovernmentsector,evidencinga22%increasefromthe21%recordedin2014.ThehighestpercentiledecreaseofrespondentswhostronglyagreedwiththisquestioniswithintheSMMEssector,evidencinga31%decreasefromthe71%recordedin2014.

Compliance as amere tick box exercisewithout understanding the spirit behind legislation and regulation andbest practiceprinciples does not add any value to the organisation. That approach also tends to only really work while the organisation feels thatitmaybewatched.Whereitisseenasanecessaryevil,compliancefliesoutofthewindowassoonasthereisnoriskofbeingexposedorpunished.

Organisations that are governedwell do not see governance as amere compliance issue, but rather that adhering to soundgovernanceprinciples is in the interestof theorganisation.Where the leadershipunderstands theprinciples,governanceandcompliancebecomesawayoflife.

11

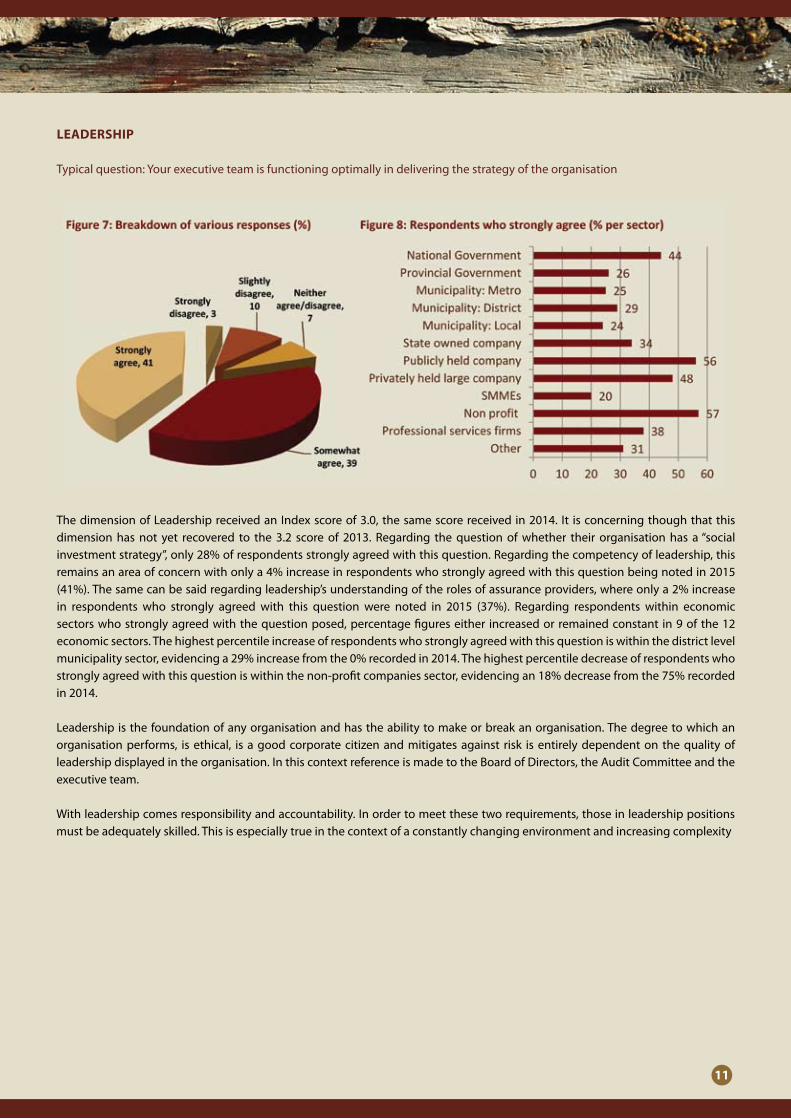

lEadErshIP

Typicalquestion:Yourexecutiveteamisfunctioningoptimallyindeliveringthestrategyoftheorganisation

ThedimensionofLeadershipreceivedanIndexscoreof3.0,thesamescorereceivedin2014. It isconcerningthoughthatthisdimensionhasnot yet recovered to the3.2 scoreof 2013. Regarding thequestionofwhether their organisationhas a“socialinvestmentstrategy”,only28%ofrespondentsstronglyagreedwiththisquestion.Regardingthecompetencyofleadership,thisremainsanareaofconcernwithonlya4%increaseinrespondentswhostronglyagreedwiththisquestionbeingnotedin2015(41%).Thesamecanbesaidregardingleadership’sunderstandingoftherolesofassuranceproviders,whereonlya2%increasein respondents who strongly agreed with this question were noted in 2015 (37%). Regarding respondents within economicsectorswhostronglyagreedwiththequestionposed,percentagefigureseither increasedorremainedconstant in9ofthe12economicsectors.Thehighestpercentileincreaseofrespondentswhostronglyagreedwiththisquestioniswithinthedistrictlevelmunicipalitysector,evidencinga29%increasefromthe0%recordedin2014.Thehighestpercentiledecreaseofrespondentswhostronglyagreedwiththisquestioniswithinthenon-profitcompaniessector,evidencingan18%decreasefromthe75%recordedin2014.

Leadershipisthefoundationofanyorganisationandhastheabilitytomakeorbreakanorganisation.Thedegreetowhichanorganisationperforms, isethical, isagoodcorporatecitizenandmitigatesagainst risk isentirelydependenton thequalityofleadershipdisplayedintheorganisation.InthiscontextreferenceismadetotheBoardofDirectors,theAuditCommitteeandtheexecutiveteam.

Withleadershipcomesresponsibilityandaccountability.Inordertomeetthesetworequirements,thoseinleadershippositionsmustbeadequatelyskilled.Thisisespeciallytrueinthecontextofaconstantlychangingenvironmentandincreasingcomplexity

12

rIsk ManagEMEnT

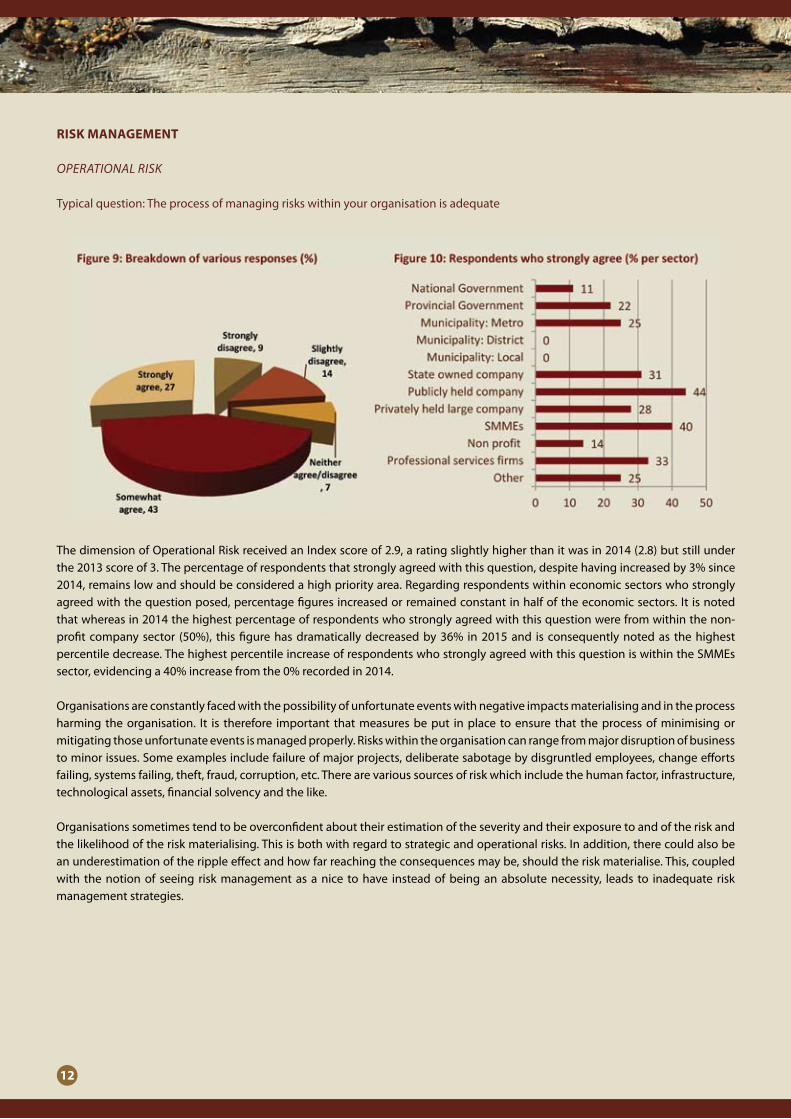

OPERATIONAL RISK

Typicalquestion:Theprocessofmanagingriskswithinyourorganisationisadequate

ThedimensionofOperationalRiskreceivedanIndexscoreof2.9,aratingslightlyhigherthanitwasin2014(2.8)butstillunderthe2013scoreof3.Thepercentageofrespondentsthatstronglyagreedwiththisquestion,despitehavingincreasedby3%since2014,remainslowandshouldbeconsideredahighpriorityarea.Regardingrespondentswithineconomicsectorswhostronglyagreedwiththequestionposed,percentagefiguresincreasedorremainedconstantinhalfoftheeconomicsectors.It isnotedthatwhereasin2014thehighestpercentageofrespondentswhostronglyagreedwiththisquestionwerefromwithinthenon-profitcompanysector (50%), thisfigurehasdramaticallydecreasedby36% in2015and is consequentlynotedas thehighestpercentiledecrease.ThehighestpercentileincreaseofrespondentswhostronglyagreedwiththisquestioniswithintheSMMEssector,evidencinga40%increasefromthe0%recordedin2014.

Organisationsareconstantlyfacedwiththepossibilityofunfortunateeventswithnegativeimpactsmaterialisingandintheprocessharming theorganisation. It is therefore important thatmeasuresbeput inplace toensure that theprocessofminimisingormitigatingthoseunfortunateeventsismanagedproperly.Riskswithintheorganisationcanrangefrommajordisruptionofbusinesstominorissues.Someexamplesincludefailureofmajorprojects,deliberatesabotagebydisgruntledemployees,changeeffortsfailing,systemsfailing,theft,fraud,corruption,etc.Therearevarioussourcesofriskwhichincludethehumanfactor,infrastructure,technological assets, financial solvency and the like.

Organisationssometimestendtobeoverconfidentabouttheirestimationoftheseverityandtheirexposuretoandoftheriskandthelikelihoodoftheriskmaterialising.Thisisbothwithregardtostrategicandoperationalrisks.Inaddition,therecouldalsobeanunderestimationoftherippleeffectandhowfarreachingtheconsequencesmaybe,shouldtheriskmaterialise.This,coupledwith thenotionof seeing riskmanagementasanice tohave insteadofbeinganabsolutenecessity, leads to inadequate riskmanagementstrategies.

13

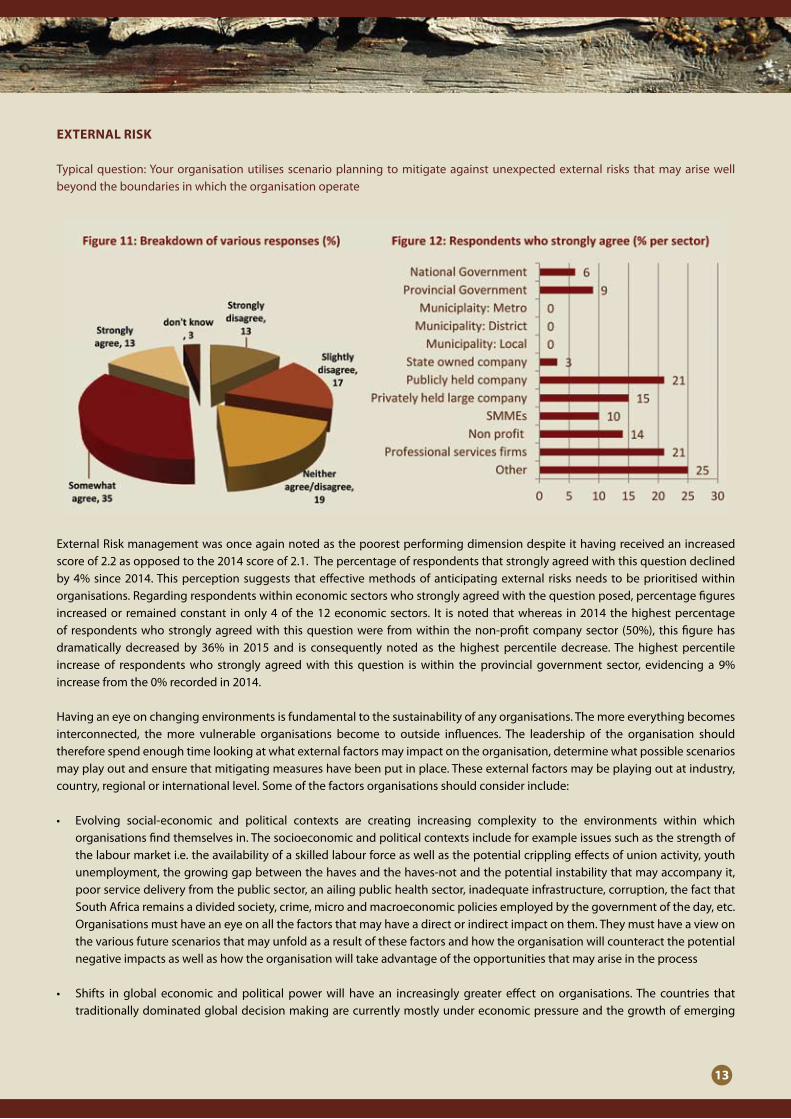

EXTErnal rIsk

Typicalquestion:Yourorganisationutilisesscenarioplanningtomitigateagainstunexpectedexternal risks thatmayarisewellbeyondtheboundariesinwhichtheorganisationoperate

ExternalRiskmanagementwasonceagainnotedasthepoorestperformingdimensiondespiteithavingreceivedanincreasedscoreof2.2asopposedtothe2014scoreof2.1.Thepercentageofrespondentsthatstronglyagreedwiththisquestiondeclinedby4%since2014.Thisperceptionsuggests thateffectivemethodsofanticipatingexternal risksneeds tobeprioritisedwithinorganisations.Regardingrespondentswithineconomicsectorswhostronglyagreedwiththequestionposed,percentagefiguresincreasedor remainedconstant inonly4of the12economicsectors. It isnotedthatwhereas in2014thehighestpercentageof respondentswhostronglyagreedwith thisquestionwere fromwithin thenon-profitcompanysector (50%), thisfigurehasdramatically decreasedby 36% in 2015 and is consequently noted as the highest percentile decrease.The highest percentileincrease of respondentswho strongly agreedwith this question iswithin theprovincial government sector, evidencing a 9%increasefromthe0%recordedin2014.

Havinganeyeonchangingenvironmentsisfundamentaltothesustainabilityofanyorganisations.Themoreeverythingbecomesinterconnected, the more vulnerable organisations become to outside influences. The leadership of the organisation shouldthereforespendenoughtimelookingatwhatexternalfactorsmayimpactontheorganisation,determinewhatpossiblescenariosmayplayoutandensurethatmitigatingmeasureshavebeenputinplace.Theseexternalfactorsmaybeplayingoutatindustry,country,regionalorinternationallevel.Someofthefactorsorganisationsshouldconsiderinclude:

• Evolving social-economic and political contexts are creating increasing complexity to the environments within whichorganisationsfindthemselvesin.Thesocioeconomicandpoliticalcontextsincludeforexampleissuessuchasthestrengthofthelabourmarketi.e.theavailabilityofaskilledlabourforceaswellasthepotentialcripplingeffectsofunionactivity,youthunemployment,thegrowinggapbetweenthehavesandthehaves-notandthepotentialinstabilitythatmayaccompanyit,poorservicedeliveryfromthepublicsector,anailingpublichealthsector,inadequateinfrastructure,corruption,thefactthatSouthAfricaremainsadividedsociety,crime,microandmacroeconomicpoliciesemployedbythegovernmentoftheday,etc.Organisationsmusthaveaneyeonallthefactorsthatmayhaveadirectorindirectimpactonthem.Theymusthaveaviewonthevariousfuturescenariosthatmayunfoldasaresultofthesefactorsandhowtheorganisationwillcounteractthepotentialnegativeimpactsaswellashowtheorganisationwilltakeadvantageoftheopportunitiesthatmayariseintheprocess

• Shifts in global economic andpolitical powerwill have an increasingly greater effect on organisations.The countries thattraditionallydominatedglobaldecisionmakingarecurrentlymostlyundereconomicpressureandthegrowthofemerging

14

economiessuchasChina,IndiaandBrazilhasbeenaccompaniedbyaresultantgradualshiftintheglobalbalanceofpower.GreatertraderelationsbetweenChinaandanumberofAfricanstateshaveaddedtowhatseemstobeagradualshiftofrelianceontheWesttotheEast.Organisationsmustthereforekeepaneyeonhowthegovernmentisrespondingtotheshiftsandhowitispositioningitselfinthenewrealitywhereallthepowernolongerlieswiththetraditionaldecisionmakers.ForexampleanimportantquestioniswhetherAfricanorganisationshavetheabilitytocompetewiththeemergingpowerhousesandtowhatdegreedotheirgovernmentscreateanenablingenvironment

• Changingconsumerconcernsandbuyingbehaviourcanhaveaprofoundimpactontheorganisation.Consumersarebecomingmoreeducated, sophisticated in tasteandaregaininggreateraccess toknowledgeaboutproductsand services.Theyarestartingtounderstandhowmuchpowertheyhaveindetermininghowthoseproductsandservicesareproducedanddelivered.Organisationsthereforefindthemselvesundermorepressurethaneverbeforetomeetprevailingandchangingexpectations.Consumersattitudestowardtheorganisationanditsbrandcoupledwithethicalconsiderationscanhaveaprofoundimpactontheir intentionstopurchase.Someof thenewertrendsdrivingconsumerbehaviour includeexpectationsthatproductsandserviceswillallowformorenewexperiencesinvolvingmoreofthesenses,arequickerandsleeker,personalisedaswellasprovideformoredepthandmeaning.Tocomplicatemattersfurtherthereare increasingsignsthatpersonalreferencingthroughsocialmediaplatformscanoftenbemoreeffectivethanexpensivemarketingcampaigns.Organisationsnotattunedtohowthesechangescouldpotentiallyimpactuponthem,maylosecustomersfasterthantheywhattheycanaffordto.

• Dealingwithemergingtechnologiesandhowtheiradvancement,eitherdirectlyorindirectly,willimpactonorganisationshasprofoundimplications.Newtechnologiesarerevolutionisingthewayorganisationsoperateandevolve.Forexample,howdoestechnologyenablingmeetingsonthewebimpactonthetravelindustry?WheretechnologywaspreviouslyseenasthedomainoftheITgeeks,itisnowanintegralpartofhoworganisationsarerun,particularlyinthedomainofcyberspaceandcomputingpower.Theforeseeablefuturehoweverpromisesmoresignificantshiftsasroboticsaswellasbio-molecular,nanoandquantumtechnologiesemerge.Thesewillinevitablycauseasocialdisruptionandfundamentallychangethewaysocietiesoperateandwillintheprocesshaveaprofoundimpactonhoworganisationsevolveandmorphintoentitiesnotyetseen.Organisationsnotyetreadyforthesoontobenewrealities,mayfindthemselvesirrelevantandlosinggroundatarapidrateinthenewfuture.

• As a result of an increase in activity in cyber space organisations are becoming increasinglymore vulnerable to cyber-attacks.Databreachesarebecomingmorecommonanddevastatingintheirimpacts.MajorcorporationssuchasSonyandeBay,smallerorganisations,NGOsandgovernmentshaveallfeltthepainofcyber-attacks.Allorganisationsarepotentialtargets,whichmeanscyber-attacksisariskareawherenoorganisationscanaffordtoputitsheadinthesand.Informationsecurityshouldthereforebeatthetopofthelistoftheorganisationskeyvigilanceareas.Organisationsshoulddeterminewhichkeyassetsmustbesafeguarded,identifythekeyvulnerabilitiesaroundthoseassetsandminimisetheprobabilityofasuccessfulattack.

• Climatechangeisalreadyhavinganimpactonecosystems,withseasonsshifting,sealevelsrisingandtemperatureschanging.Thisallcouldleadto increasingrisksofdroughts,fires,floods,strongerstormsandincreasedstormdamage,withresultanteconomiclosses.Oneofthebiggestconcernsaroundclimatechangeishowwaterresourceswillbeaffected.Waterresourcesareinturnlinkedtofoodsupply,healthandecosystemintegrity.Foodandwaterscarcityinevitablewouldleadtosocialunrestwhichcouldtearthesocialfabricofcommunities.Suchascenariodoesnotpaintagoodpicturefororganisations.

• Asaresultofsignificantcorporatefailuresandtheglobalfinancialandsovereigndebtcrises,therehasbeenagreateremphasisonregulationasregulatorybodieshaveoftenbeenaccusedofbeingineffective.Shiftingregulationsmakeitmoredifficultfororganisationstooperateandbringtheburdenofhighlevelsofexpectedcompliance.Whereorganisationsdonotembraceandinterweavethespiritbehindregulatoryprinciplesintheorganisation,compliancecancomeatagrudgecost.Someofthepositiveeffectswouldincludestandardisationacrossjurisdictionsandensuringthattheplayingfieldisevenwithallplayersexpectedtoplayafairgame.

• Increasingconvergenceandcompetitionaretwooftheareasthatcouldhaveanimmediateimpactontheorganisationifitisnotvigilant.Havingacompetitiveadvantage,bydefinitionmeansthattheorganisationmusthaveaverygoodunderstandingofitscapabilityinrelationtothatofitscompetitors.Organisationsthatarenotvigilantcouldquiteeasilyfindthemselvesblindsidedbyacompetitorthatisfirsttomarketwithanewproductorfirsttoengagenewtechnologythatsignificantlyreducescosts.Ontheotherhand,thereisalsoanincreasingmovetowardconvergenceofdifferentsegmentsacrossanindustry,particularly

15

whereinvestmentefficiencyandprofitabilityarethedrivers.Thusanorganisation’scompetitormayverywellchangethegamebyengaginginconvergingstrategieswithplayersthattraditionallywerenotseenaspartofthecompetitionequation.

• Globalisationhasbothpositiveandnegativeimplicationsfororganisations.Somenegativeconsequencesincludeinternationalcompanies becoming increasingly more powerful with a profit motivation that can be harmful to developing countries,protectionistpoliciesinindustrialisedcountriesharmingdevelopingcountries,volatilityincapitalflowscreatingcurrencycrisesandinternationaltradeworseninginequalities.Somepositiveconsequencesincludethebroadeningofdistributionpatternswithorganisationsbeingabletotapintomuchlargermarketsandincreasedaccesstocapitalflowsandgoodsandservices.Furthermoretheimpactoflabourmigrationcouldhavepositiveornegativeconsequences.Ontheonehandacountrymaygainscarceskillsasaresultofmigration;ontheotherhanditcouldcausesocialinstability.AgoodexampleisthecurrentinfluxintoanillpreparedEuropefromNorthAfrica,Syriaandotherwartorncountries.

• Theemergingenergycrisisisbecomingoneofthemostsignificantexternalrisksorganisationsface.Astheworldismovingintoaknowledgebasedeconomy,thedemandforenergyseemstobeincreasing.Therehasbeenmuchtalkaboutpeakoilandtheendoftheearth’sabilitytoservetheworld’sneedforoil.Thesamegoesforthesupplyofcoalinrelationtoelectricitythatisinadditiontothelocalelectricityutility’sinabilitytosupplyenoughelectricitytosustaintheeconomy.Unlessalternativesourcesofenergyareaggressivelypursued,theenergycrisisissettogrowevenbiggerwithalarmingconsequences.Organisationsthathavenotyetlookedatthepotentialimpactminimisedtheirneedforenergyandsoughtalternativesourcesofenergymaysoonfindthemselvesonthebackfoot.

Inafastchangingworldwithmultipleexternalfactorsplayinghavocwithorganisations’sustainabilityefforts,beinginastateofreadinessiseasiersaidthandone.Thisisfurtheraggravatedbythefactthatitisevenmoredifficulttoanticipateblackswanevents.However,aheadinthesandapproachwillonlydomoreharmthangood.Leadershipofanorganisationmustputmeasuresinplacewhichwillensureadequatefocusontheexternalriskstheorganisationmayface.

16

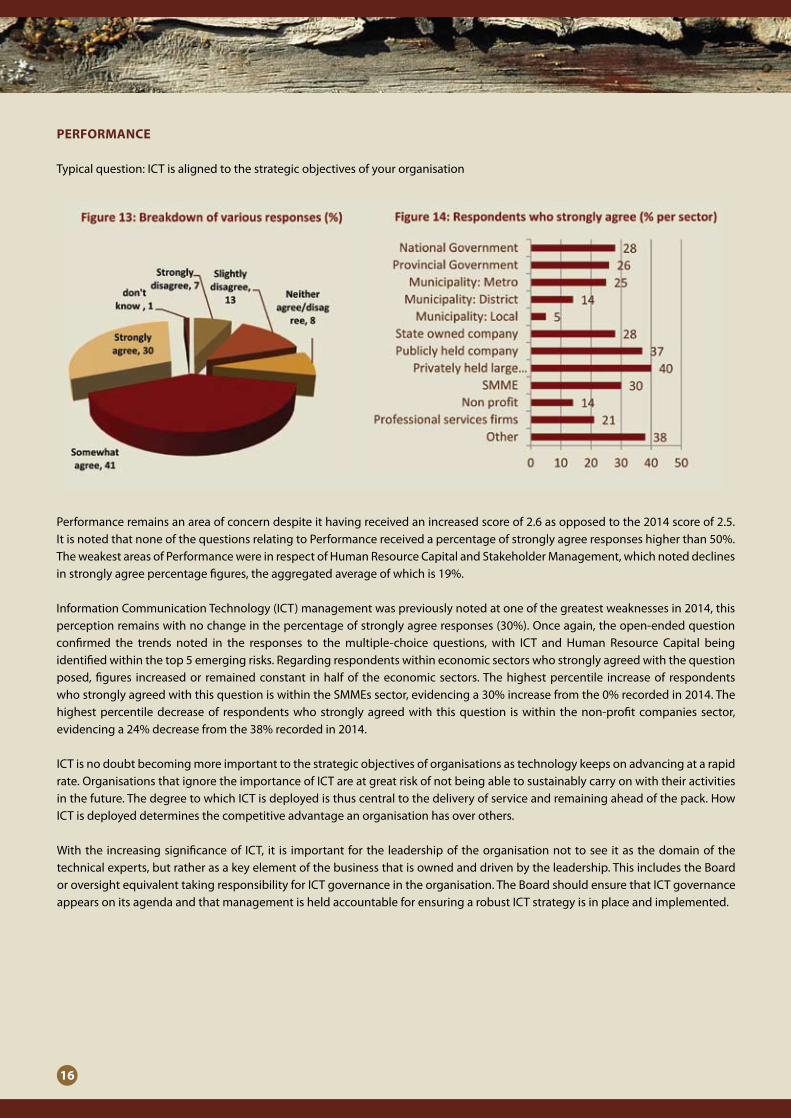

PErforMancE

Typicalquestion:ICTisalignedtothestrategicobjectivesofyourorganisation

Performanceremainsanareaofconcerndespiteithavingreceivedanincreasedscoreof2.6asopposedtothe2014scoreof2.5.ItisnotedthatnoneofthequestionsrelatingtoPerformancereceivedapercentageofstronglyagreeresponseshigherthan50%.TheweakestareasofPerformancewereinrespectofHumanResourceCapitalandStakeholderManagement,whichnoteddeclinesinstronglyagreepercentagefigures,theaggregatedaverageofwhichis19%.

InformationCommunicationTechnology(ICT)managementwaspreviouslynotedatoneofthegreatestweaknessesin2014,thisperceptionremainswithnochangeinthepercentageofstronglyagreeresponses(30%).Onceagain,theopen-endedquestionconfirmed the trends noted in the responses to themultiple-choice questions, with ICT and Human Resource Capital beingidentifiedwithinthetop5emergingrisks.Regardingrespondentswithineconomicsectorswhostronglyagreedwiththequestionposed,figures increasedor remainedconstant inhalfof theeconomicsectors.Thehighestpercentile increaseof respondentswhostronglyagreedwiththisquestioniswithintheSMMEssector,evidencinga30%increasefromthe0%recordedin2014.Thehighestpercentiledecreaseof respondentswhostronglyagreedwith thisquestion iswithin thenon-profitcompanies sector,evidencinga24%decreasefromthe38%recordedin2014.

ICTisnodoubtbecomingmoreimportanttothestrategicobjectivesoforganisationsastechnologykeepsonadvancingatarapidrate.OrganisationsthatignoretheimportanceofICTareatgreatriskofnotbeingabletosustainablycarryonwiththeiractivitiesinthefuture.ThedegreetowhichICTisdeployedisthuscentraltothedeliveryofserviceandremainingaheadofthepack.HowICTisdeployeddeterminesthecompetitiveadvantageanorganisationhasoverothers.

Withthe increasingsignificanceof ICT, it is important for the leadershipof theorganisationnottosee itas thedomainof thetechnicalexperts,butratherasakeyelementofthebusinessthatisownedanddrivenbytheleadership.ThisincludestheBoardoroversightequivalenttakingresponsibilityforICTgovernanceintheorganisation.TheBoardshouldensurethatICTgovernanceappearsonitsagendaandthatmanagementisheldaccountableforensuringarobustICTstrategyisinplaceandimplemented.

17

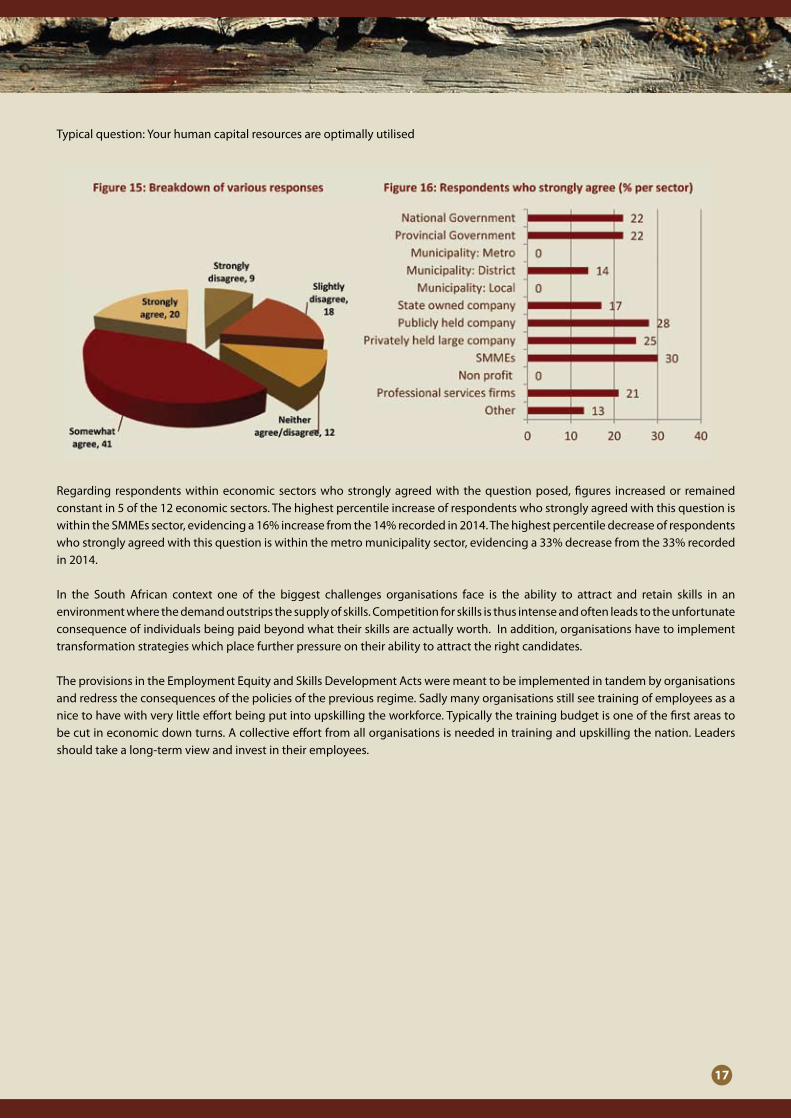

Typicalquestion:Yourhumancapitalresourcesareoptimallyutilised

Regarding respondentswithineconomic sectorswhostronglyagreedwith thequestionposed,figures increasedor remainedconstantin5ofthe12economicsectors.ThehighestpercentileincreaseofrespondentswhostronglyagreedwiththisquestioniswithintheSMMEssector,evidencinga16%increasefromthe14%recordedin2014.Thehighestpercentiledecreaseofrespondentswhostronglyagreedwiththisquestioniswithinthemetromunicipalitysector,evidencinga33%decreasefromthe33%recordedin2014.

In the South African context one of the biggest challenges organisations face is the ability to attract and retain skills in anenvironmentwherethedemandoutstripsthesupplyofskills.Competitionforskillsisthusintenseandoftenleadstotheunfortunateconsequenceofindividualsbeingpaidbeyondwhattheirskillsareactuallyworth.Inaddition,organisationshavetoimplementtransformationstrategieswhichplacefurtherpressureontheirabilitytoattracttherightcandidates.

TheprovisionsintheEmploymentEquityandSkillsDevelopmentActsweremeanttobeimplementedintandembyorganisationsandredresstheconsequencesofthepoliciesofthepreviousregime.Sadlymanyorganisationsstillseetrainingofemployeesasanicetohavewithverylittleeffortbeingputintoupskillingtheworkforce.Typicallythetrainingbudgetisoneofthefirstareastobecutineconomicdownturns.Acollectiveeffortfromallorganisationsisneededintrainingandupskillingthenation.Leadersshouldtakealong-termviewandinvestintheiremployees.

18

InTErnal audIT

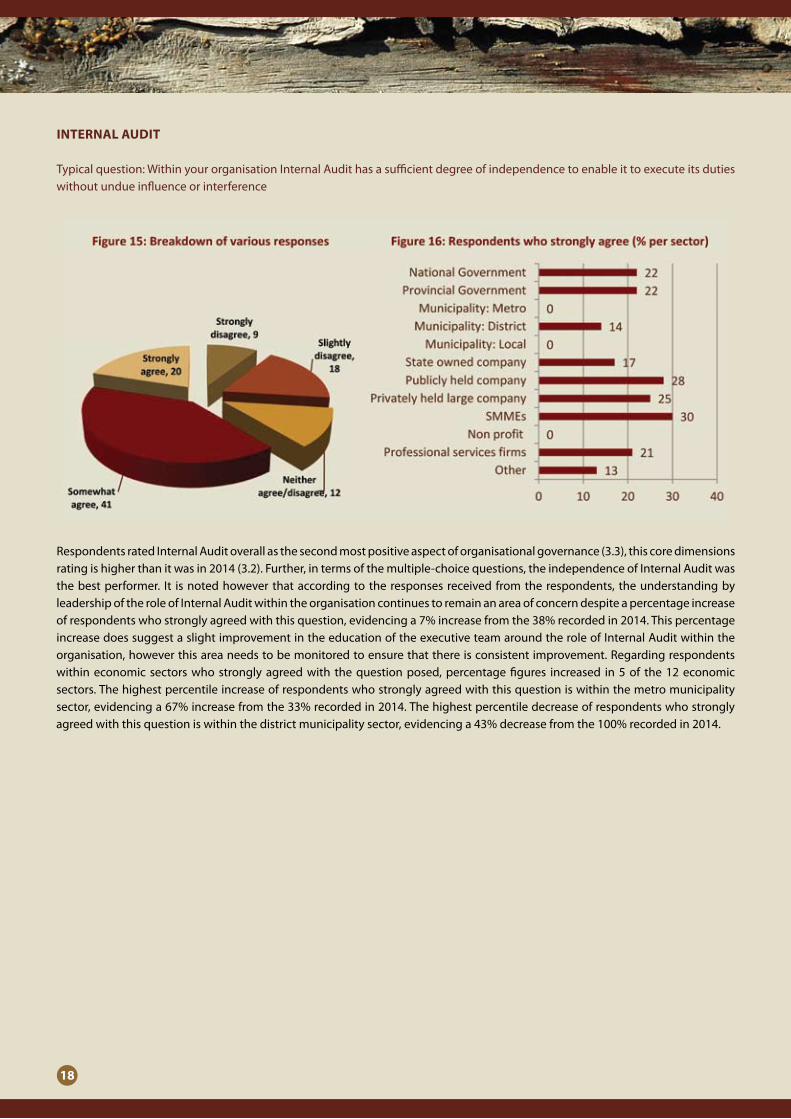

Typicalquestion:WithinyourorganisationInternalAudithasasufficientdegreeofindependencetoenableittoexecuteitsdutieswithoutundueinfluenceorinterference

RespondentsratedInternalAuditoverallasthesecondmostpositiveaspectoforganisationalgovernance(3.3),thiscoredimensionsratingishigherthanitwasin2014(3.2).Further,intermsofthemultiple-choicequestions,theindependenceofInternalAuditwasthebestperformer. It isnotedhowever thataccordingtotheresponses receivedfromtherespondents, theunderstandingbyleadershipoftheroleofInternalAuditwithintheorganisationcontinuestoremainanareaofconcerndespiteapercentageincreaseofrespondentswhostronglyagreedwiththisquestion,evidencinga7%increasefromthe38%recordedin2014.ThispercentageincreasedoessuggestaslightimprovementintheeducationoftheexecutiveteamaroundtheroleofInternalAuditwithintheorganisation,howeverthisareaneedstobemonitoredtoensurethatthereisconsistentimprovement.Regardingrespondentswithineconomic sectorswhostronglyagreedwith thequestionposed,percentagefigures increased in5of the12economicsectors.Thehighestpercentileincreaseofrespondentswhostronglyagreedwiththisquestioniswithinthemetromunicipalitysector,evidencinga67%increasefromthe33%recordedin2014.Thehighestpercentiledecreaseofrespondentswhostronglyagreedwiththisquestioniswithinthedistrictmunicipalitysector,evidencinga43%decreasefromthe100%recordedin2014.

19

Belowisalistofthemostsignificantresearchfindings:

1. ThestabilityoftheCountryIndexat2.9mayindicateaperceptionthatchangeinorganisationsregardingtheimplementationofcorporategovernanceisslow.Nonetheless,the incremental increases in5ofthe7dimensionswithnooveralldecreasesbeingnotedreflectsapositivefutureoutlook.

2. Ethicshasretainedthepositionoftopachievingdimension(3.4),whichisnotedasanextremelypositivefindingowingtothefactthatitissointegraltotheInternalAuditprofession.Further,themultiple-choicequestionrelatingtotheindependenceofInternalAuditwithinorganisationshasreceivedthemostfavourableresponsefromrespondents,anotherkeyprincipleforensuringobjectivitywithintheInternalAuditprofession.

3. DespiteithavingretaineditsIndexscoreof3.0,Compliancewasnotedasanareaofconcernbyrespondents,particularlyasasignificantemergingriskwithinorganisations.ThisisduetotheperceptionofrespondentssurroundingamendmentstothelegislativeandregulatoryframeworkwithinSouthAfricaandabroad.Emphasisistobeplacedonefficientandconsistentusageofacombinedassuranceframeworkwithinorganisations.

4. RegardingLeadership,thereappearstobealackofemphasisplacedondevelopmentofasocialinvestmentstrategywithinorganisations. Further, the competencyof leadershipand leadership’sunderstandingof the roleof InternalAuditwith theorganisationremainanareaofconcernforCAEs.Thiswasalsoexpressedasanemergingrisk intheopen-endedquestion.Adequatemonitoringoftheseareasisrequiredinordertoensureconsistentimprovement.

5. OperationalRiskfaredbetterthanExternalRisk,receivinganIndexscoreof2.9,howevertheadequacyofriskmanagement

withinorganisationscontinuestoreceivelowpercentagescoresfromrespondents.Thisshouldbeconsideredahighpriorityarea.

6. ExternalRiskwasthelowestperformingdimension,despiteithavingreceivedanIndexscoreof2.2asopposedto2.1in2014.Effectivemethodsofanticipatingexternalrisksneedtobeprioritisedwithinorganisations.Thisassertionisfurtherbolsteredbythefactthatvariousexternalriskfactorssuchasinfrastructurecollapse,stabilityofessentialservicesandawaningeconomicclimatewereidentifiedassignificantemergingrisksintheopen-endedquestion.

7. The IndexscoreofPerformancewas2.6asopposed to2.5 in2014.However,despite this increase, thisdimension remainsonewhich contains complex issues to be resolved, includingHuman Resource Capital, StakeholderManagement and ICTmanagement.Further,theseareaswerenotedinthetop5emergingrisksintheopen-endedquestion.

8. Thetop5areasoffocusoverthenextfewyearsare,inorderofpriority:HumanResources,Compliance,Macro-EnvironmentalEconomicRisks,ICTaswellasinfrastructurecollapseandstabilityofessentialservices.

MAIN FINDINGs

20

The annual Corporate Governance Index is intended to present management, boards and audit committees with a credibleperspectiveonemergingcorporategovernancetrendsinSouthAfrica.

Theoverall findings suggest thatorganisations arebecomingmore awareof thenecessityof corporategovernance,howeverprogressinachievingthebestpractisestandardsaspertheKingCodesofGovernanceisslow.Itishowevernotedthatprogress,regardlessofitspace,isapositivefindingandinstillingthesepractiseswithinallbranchesoftheorganisationisatimeousandchallengingprocess.Nonetheless,forlastingfoundationstobebuiltandstandthetestoftime,muchhardworkandperseveranceisrequired.

ItisimportanttonotethatthecurrentemergingriskswhichhavecometotheforearenotonlyriskswhichfacetheInternalAuditprofession,buttheSouthAfricaneconomyat large. It ishoweverthemandateofCAEstosharetheirconcernswithleadershipandfacilitateconversationsaroundtheInternalAuditteam’srolewithintheorganisation.Whetheritbethefastmovingpaceoftechnologicaldevelopmentsortheinstabilityofinfrastructureandtheeconomy,thefarreachingimplicationsofsuchissuescanbemanagedwherethere isacollaborativeeffortwithinorganisations.An increasedefforttowards improvingtheexternal riskmanagementtoolswithintheorganisationmustberecognised.

Furthermore, theperception thatcertain risksarebeyond thecontroloforganisations isa realone,however throughpositivediscourseandcounteractivemeasures,theprobabilityofavoidanceorattheveryleastmanagementofsuchpotentialpitfallswillbefavourable.

Youareencouragedtotakenoteofthefindingsascontainedinthisreportandinternalisesame,whilstbeingmindfulthateachdimensioncannotbeviewedininsolation.Bytakingcognisanceofthefindingsintheirentirety,organisationswillbenefitfromtheknockoneffectoftheimprovementofonedimensiononanother.Indoingso,thiswillelevatethestateofcorporategovernancewithintheorganisationtoabenefitlevelwhichtranscendsthroughouttheorganisationandbeyond.

The IIA SA takes the survey results seriously andwill address relevant findings through training programs and discussions atitsvariousconferences.As the Indexbecomesmorewidelydistributed,weexpectother relatedprofessions tostart theirownprocessesofinternaldialogueanddebatewithaviewtoaddressingthegapsthathavebeenidentified.Afterall,thefindingsreflectourcollectiveabilitytodelivervaluetoourshareholdersandstakeholders.Therealpowerofthisreportthereforeliesinourabilityto translate knowledge into action.

THE WAY FORWARD

21

Percentages (%)

dimension question stronglydisagree

slightly disagree

neither agree/

disagree

somewhat agree

strongly agree

Ethics

TheOversightbody(suchastheBoardorCouncil),setsacleartoneofzerotolerancetowardunethicalbehaviour,including fraud and corruption in your organisation.

5 4 6 19 66

Ethicsisanimportantpartofyourorganisational culture. 3 6 5 26 60

compliance

Yourorganisationiscommittedtoimplementingrelevantgoodcorporategovernance principles (as outlined inKingIIIortheNationalTreasurygovernanceframeworks).

3 6 6 28 57

Whenitcomestocorporategovernance,yourorganisationgoesbeyondameretickboxexercise-i.e.thereisadeepunderstanding of the principles and philosophy of good governance.

4 12 8 38 38

Yourorganisationusesacombinedassuranceframeworktoprovideaco-ordinatedapproachtoassuranceactivities. *Note:1%ofrespondentsanswered“don’tknow”tothisquestion.

8 13 11 39 28

Yourorganisationcomplieswithrelevantlegislation, regulations and standards. 1 6 5 34 54

leadership

YourOversightbody(suchastheBoardorCouncil)providesclearstrategicdirectiontoachievetheobjectivesofyour organisation.

4 5 7 30 54

The leadership of your organisation (i.e.seniorandexecutivemanagementas well as the Board) displays a good understanding of the varying roles of assurance providers (such as internal audit,externalaudit,riskmanagementetc.)

4 9 10 40 37

TheAuditCommitteeiseffectiveinitsoversightrole.*Note:1%ofrespondentsanswered“don’tknow”tothisquestion.

3 7 8 28 53

APPENDIX 1: sUMMARY OF ANsWERs TO sURVEY QUEsTIONs

22

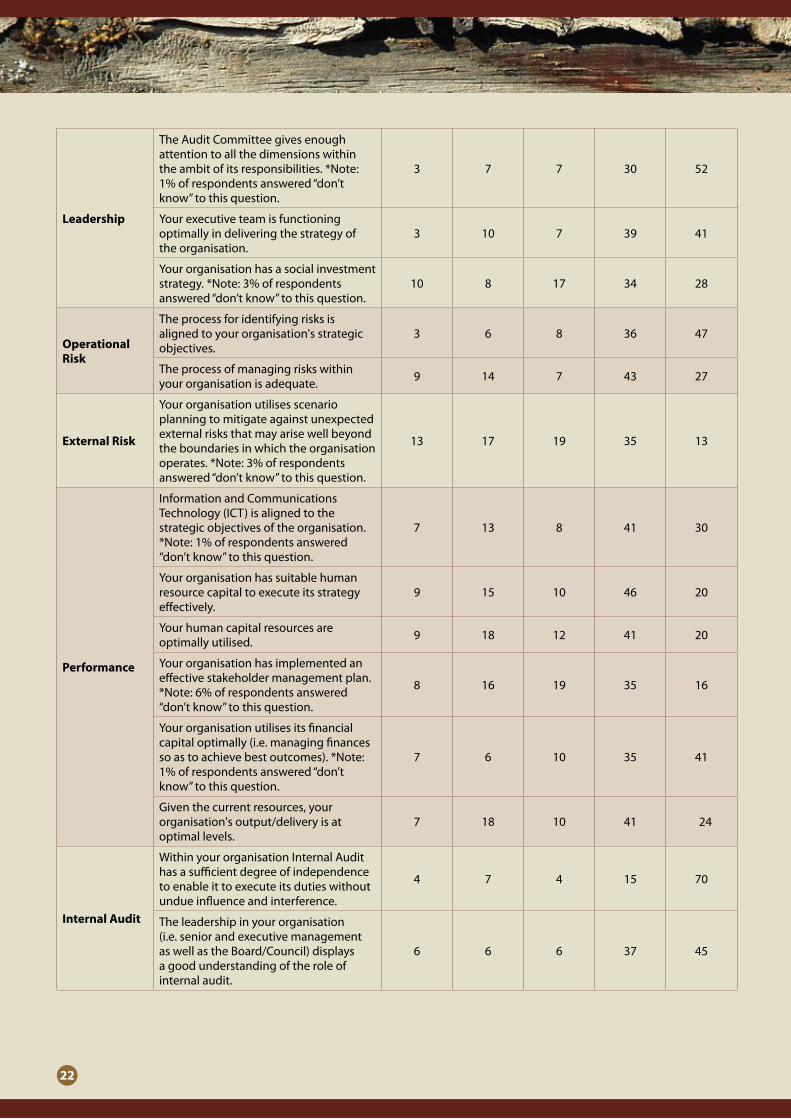

leadership

TheAuditCommitteegivesenoughattentiontoallthedimensionswithintheambitofitsresponsibilities.*Note:1%ofrespondentsanswered“don’tknow”tothisquestion.

3 7 7 30 52

Yourexecutiveteamisfunctioningoptimallyindeliveringthestrategyofthe organisation.

3 10 7 39 41

Yourorganisationhasasocialinvestmentstrategy.*Note:3%ofrespondentsanswered“don’tknow”tothisquestion.

10 8 17 34 28

operational risk

The process for identifying risks is aligned to your organisation's strategic objectives.

3 6 8 36 47

Theprocessofmanagingriskswithinyourorganisationisadequate. 9 14 7 43 27

External risk

Yourorganisationutilisesscenarioplanningtomitigateagainstunexpectedexternalrisksthatmayarisewellbeyondtheboundariesinwhichtheorganisationoperates.*Note:3%ofrespondentsanswered“don’tknow”tothisquestion.

13 17 19 35 13

Performance

InformationandCommunicationsTechnology(ICT)isalignedtothestrategicobjectivesoftheorganisation.*Note:1%ofrespondentsanswered“don’tknow”tothisquestion.

7 13 8 41 30

Yourorganisationhassuitablehumanresourcecapitaltoexecuteitsstrategyeffectively.

9 15 10 46 20

Yourhumancapitalresourcesareoptimallyutilised. 9 18 12 41 20

Yourorganisationhasimplementedaneffectivestakeholdermanagementplan.*Note:6%ofrespondentsanswered“don’tknow”tothisquestion.

8 16 19 35 16

Yourorganisationutilisesitsfinancialcapitaloptimally(i.e.managingfinancessoastoachievebestoutcomes).*Note:1%ofrespondentsanswered“don’tknow”tothisquestion.

7 6 10 35 41

Giventhecurrentresources,yourorganisation'soutput/deliveryisatoptimallevels.

7 18 10 41 24

Internal audit

WithinyourorganisationInternalAudithasasufficientdegreeofindependencetoenableittoexecuteitsdutieswithoutundueinfluenceandinterference.

4 7 4 15 70

The leadership in your organisation (i.e.seniorandexecutivemanagementaswellastheBoard/Council)displaysa good understanding of the role of internal audit.

6 6 6 37 45

TheInstituteofInternalAuditorsSouthAfricahaslaunchedtheExecutiveLeadershipNetwork(ELN).TheELNhasbeendeveloped

toassistChiefAuditExecutives(CAEs)toachievetheirgoals,meetandexceedthedemandsplaceduponthemandsupporttheir

effortsintheircapacityaspioneersintheirorganisations.Inanincreasinglycompetitiveandcomplexbusinessenvironment,

CAEsneedtoensuretheykeepinformedofimportantissuesandstayconnectedwithpeerswhounderstandandfacethesame

challenges.

TheELNisanexclusiveplatformforCAEswheretools,resources,informationandtopicdiscussionsareattheirfingertips

tokeepthematthecuttingedgeofinternalaudit.AsleadersoftheInternalAuditprofession,CAEsareprovidedwithan

exclusiveserviceto“remainontopofthegame.”

Withtherapidchangesinfluencingtheperformanceofbusinessestoday,theELNwasdevelopedtosupportCAEsinaddressingthe

demandsplacedonthembysuchchanges.

Why become a subscriber of the Executive Leadership Network?

Being a subscriber to the Eln means:

•Yousavevaluabletimesearchingforinformationandcompilingauditworkingdocuments.

•YoucanconvenientlyandeconomicallynetworkwithotherCAEs.

•YoucanshareconcernswithotherCAEstoderiveatfeasiblesolutions

•Youareawareofchangesintheprofessionandarefullyequippedtodealwithdemandsplacedonyoucausedbychangesinthemarket.

•YouhavethenecessarysupporttostrategicallypositiontheInternalAuditdepartmentasavalue-addorganisationalresource.

ExecutiveLeadership NetworkResourceCenterforChiefAuditExecutives

Executive Leadership NetworkResourceCenterforChiefAuditExecutives

for more information contactIschtelle hechter,

DepartmentHead:ExecutiveLeadershipNetworkTel:+27114501040•fax: +27114501070

Email:[email protected]•Web: www.iiasa.org.za

©2015byTheInstituteofInternalAuditorsSouthAfrica,POBox2290,Bedfordview,2008

ThisworkisCopyrightundertheBerneConvention.IntermsoftheCopyrightAct,No.98of1978(asamended)nopartofthisworkmaybereproducedortransmittedinanyformorbyanymeans-electronic,mechanical,includingphotocopying,recording

orbyanyinformationstorageandretrievalsystem-withoutpermissioninwritingfromtheauthor.

Althoughcareistakentoensuretheaccuracyofthispublication,supplements,updatesandreplacementmaterialstheauthors,editors,publishersandprintersdonotacceptresponsibilityforanyact,omission,loss,damageortheconsequencethereof

occasionedbyareliancebyanypersonuponthecontenthereof.