corporate finance lecture note packet 2...

TRANSCRIPT

CORPORATEFINANCELECTURENOTEPACKET2CAPITALSTRUCTURE,DIVIDENDPOLICYANDVALUATION

AswathDamodaran Spring2016

Aswath Damodaran 1

CAPITALSTRUCTURE:THECHOICESANDTHETRADEOFF“Neitheraborrowernoralenderbe”Someonewhoobviouslyhatedthispartofcorporate finance

Aswath Damodaran 2

3

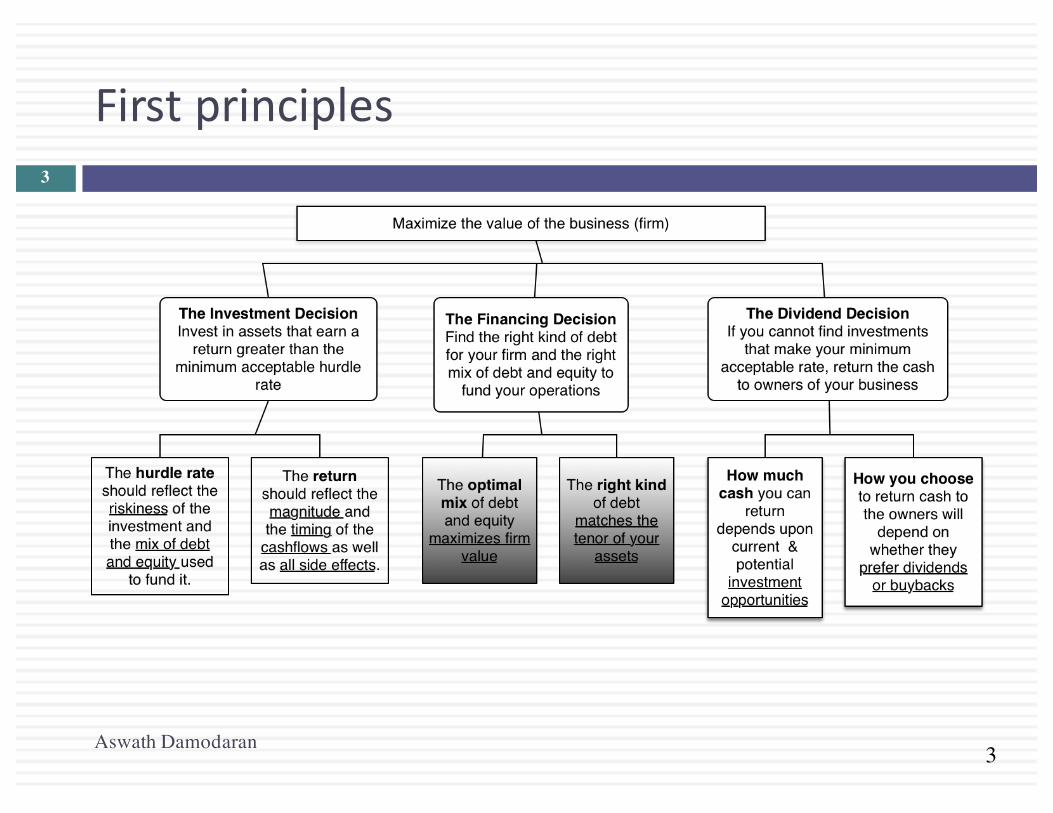

Firstprinciples

Aswath Damodaran

3

4

TheChoicesinFinancing

Aswath Damodaran

4

¨ Thereareonlytwowaysinwhichabusiness canraisemoney.¤ Thefirstisdebt.Theessence ofdebt isthatyoupromise tomakefixed

paymentsinthefuture (interestpaymentsandrepayingprincipal). Ifyoufailtomakethosepayments,youlosecontrolofyourbusiness.

¤ Theother isequity.Withequity,youdogetwhatever cashflowsareleftoverafteryouhavemadedebtpayments.

5

GlobalPatternsinFinancing…

Aswath Damodaran

5

6

AndamuchgreaterdependenceonbankloansoutsidetheUS…

Aswath Damodaran

6

7

Assessingtheexistingfinancingchoices:Disney,Vale,TataMotors,Baidu &Bookscape

Aswath Damodaran

7

8

9

TheTransitionalPhases..

Aswath Damodaran

9

¨ Thetransitionsthatweseeatfirms– fromfullyownedprivatebusinessestoventurecapital,fromprivatetopublicandsubsequentseasonedofferingsareallmotivatedprimarilybytheneedforcapital.

¨ Ineachtransition,though,therearecostsincurredbytheexistingowners:¤ Whenventurecapitalistsenter thefirm,theywilldemandtheir fair

shareandmoreoftheownershipofthefirmtoprovideequity.¤ Whenafirmdecides togopublic,ithastotradeoffthegreateraccess

tocapitalmarketsagainsttheincreased disclosure requirements (thatemanate frombeingpubliclylists),lossofcontrolandthetransactionscostsofgoingpublic.

¤ Whenmakingseasoned offerings, firmshavetoconsider issuancecostswhilemanagingtheirrelationswithequityresearch analystsandrat

10

Measuringafirm’sfinancingmix…

Aswath Damodaran

10

¨ Thesimplestmeasureofhowmuchdebtandequityafirmisusingcurrentlyistolookattheproportionofdebtinthetotalfinancing.Thisratioiscalledthedebttocapitalratio:DebttoCapitalRatio=Debt/(Debt+Equity)

¨ Debtincludesallinterestbearingliabilities,shorttermaswellaslongterm.Itshouldalsoincludeothercommitmentsthatmeetthecriteriafordebt:contractuallypre-setpaymentsthathavetobemade,nomatterwhatthefirm’sfinancialstanding.

¨ Equitycanbedefinedeitherinaccountingterms(asbookvalueofequity)orinmarketvalueterms(baseduponthecurrentprice).Theresultingdebtratioscanbeverydifferent.

11

TheFinancingMixQuestion

Aswath Damodaran

11

¨ Indecidingtoraisefinancingforabusiness,isthereanoptimalmixofdebtandequity?¤ Ifyes,whatisthetradeoffthatletsusdeterminethisoptimalmix?

n Whatarethebenefits ofusingdebtinsteadofequity?n Whatarethecostsofusingdebtinsteadofequity?

¤ Ifnot,whynot?

12

TheIllusoryBenefitsofDebt

¨ Atfirstsight,thebenefitofdebtseemsobvious.Thecostofdebtislowerthanthecostofequity.

¨ Thatbenefitisanillusion,though,becausedebtischeaperthanequityforasimplereason.Thelendergetsbothfirstclaimonthecashflowsandacontractuallypre-setcashflow.Theequityinvestorislastinlineandhastodemandahigherrateofreturnthanthelenderdoes.

¨ Byborrowingmoneyatalowerrate,youarenotmakingabusinessmorevaluable,butjustmovingtheriskaround.

Aswath Damodaran

12

13

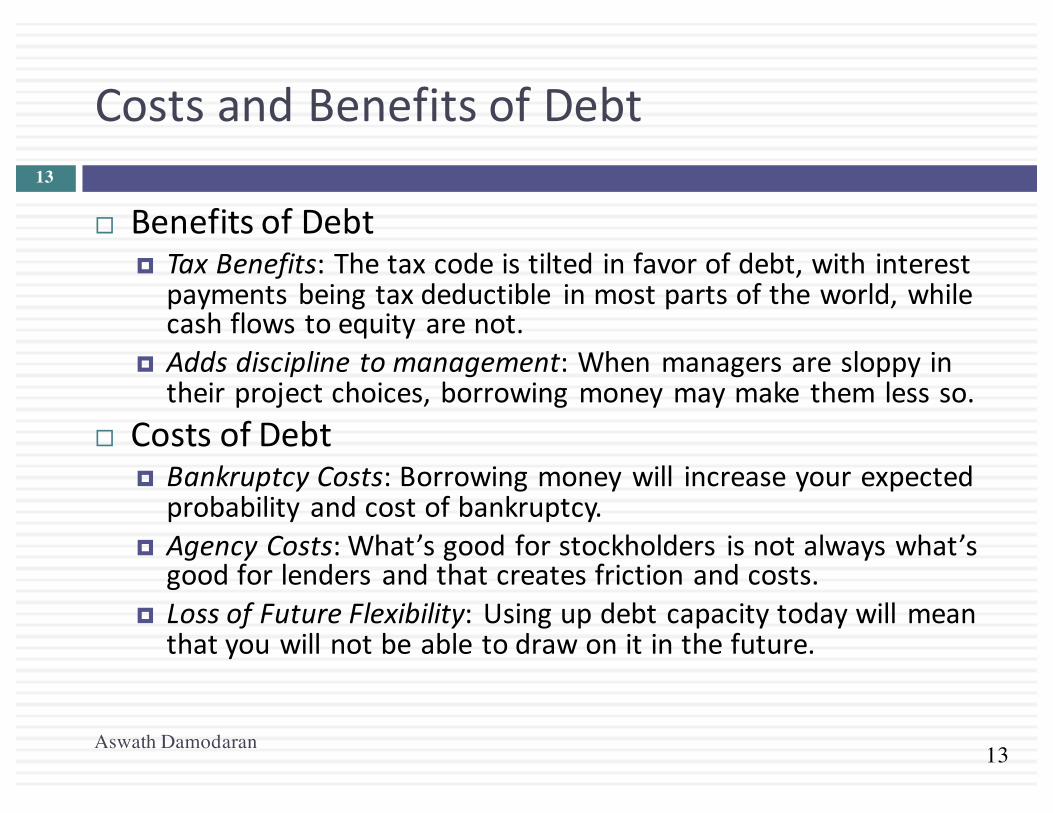

CostsandBenefitsofDebt

Aswath Damodaran

13

¨ BenefitsofDebt¤ TaxBenefits:Thetaxcodeistiltedinfavorofdebt,withinterestpaymentsbeingtaxdeductible inmostpartsoftheworld,whilecashflowstoequity arenot.

¤ Addsdisciplinetomanagement:Whenmanagersaresloppyintheirprojectchoices,borrowingmoneymaymake themlessso.

¨ CostsofDebt¤ BankruptcyCosts:Borrowingmoneywill increaseyourexpectedprobability andcostofbankruptcy.

¤ AgencyCosts:What’sgoodforstockholders isnotalwayswhat’sgoodforlenders andthatcreatesfrictionandcosts.

¤ LossofFutureFlexibility:Usingupdebtcapacitytodaywillmeanthatyouwillnotbeabletodrawonitinthefuture.

14

TaxBenefitsofDebt

Aswath Damodaran

14

¨ Whenyouborrowmoney,youareallowedtodeductinterestexpensesfromyourincometoarriveattaxableincome.Thisreducesyourtaxes.Whenyouuseequity,youarenotallowedtodeductpaymentstoequity(suchasdividends)toarriveattaxableincome.

¨ Thedollartaxbenefitfromtheinterestpaymentinanyyearisafunctionofyourtaxrateandtheinterestpayment:¤ Taxbenefiteachyear=TaxRate*InterestPaymentThecaveatisthatyouneedtohave theincometocoverinterestpaymentstogetthistaxbenefit.

¨ Proposition1:Otherthingsbeingequal,thehigherthemarginaltaxrateofabusiness,themoredebtitwillhaveinitscapitalstructure.

15

TheEffectsofTaxes

Aswath Damodaran

15

¨ Youarecomparingthedebtratiosofrealestatecorporations,whichpaythecorporatetaxrate,andrealestateinvestmenttrusts,whicharenottaxed,butarerequiredtopay95%oftheirearningsasdividendstotheirstockholders.Whichofthesetwogroupswouldyouexpecttohavethehigherdebtratios?

a. Therealestatecorporationsb. Therealestateinvestmenttrustsc. Cannottell,withoutmoreinformation

16

Debtaddsdisciplinetomanagement

Aswath Damodaran

16

¨ Ifyouaremanagersofafirmwithnodebt,andyougeneratehighincomeandcashflowseachyear,youtendtobecomecomplacent.Thecomplacencycanleadtoinefficiencyandinvestinginpoorprojects.Thereislittleornocostbornebythemanagers

¨ Forcingsuchafirmtoborrowmoneycanbeanantidotetothecomplacency.Themanagersnowhavetoensurethattheinvestmentstheymakewillearnatleastenoughreturntocovertheinterestexpenses.Thecostofnotdoingsoisbankruptcyandthelossofsuchajob.

17

DebtandDiscipline

Aswath Damodaran

17

¨ Assumethatyoubuyintothisargumentthatdebtaddsdisciplinetomanagement.Whichofthefollowingtypesofcompanieswillmostbenefitfromdebtaddingthisdiscipline?

a. Conservativelyfinanced(verylittledebt),privatelyownedbusinesses

b. Conservativelyfinanced,publiclytradedcompanies,withstocksheldbymillionsofinvestors,noneofwhomholdalargepercentofthestock.

c. Conservativelyfinanced,publiclytradedcompanies,withanactivistandprimarilyinstitutionalholding.

18

BankruptcyCost

Aswath Damodaran

18

¨ Theexpectedbankruptcycostisafunctionoftwovariables--¤ theprobabilityofbankruptcy,whichwilldependuponhowuncertain

youareaboutfuturecashflows¤ thecostofgoingbankrupt

n directcosts:LegalandotherDeadweightCostsn indirectcosts:Costsarisingbecause peopleperceive youtobeinfinancialtrouble

¨ Proposition2:Firmswithmorevolatileearningsandcashflowswillhavehigherprobabilitiesofbankruptcyatanygivenlevelofdebtandforanygivenlevelofearnings.

¨ Proposition3:Otherthingsbeingequal,thegreatertheindirectbankruptcycost,thelessdebtthefirmcanaffordtouseforanygivenlevelofdebt.

19

Debt&BankruptcyCost

Aswath Damodaran

19

¨ Rankthefollowingcompaniesonthemagnitudeofbankruptcycostsfrommosttoleast,takingintoaccountbothexplicitandimplicitcosts:

a. AGroceryStoreb. AnAirplaneManufacturerc. HighTechnologycompany

20

AgencyCost

Aswath Damodaran

20

¨ Anagencycostarises whenever youhiresomeone elsetodosomethingforyou.Itarisesbecauseyourinterests(as theprincipal)maydeviate fromthoseofthepersonyouhired(astheagent).

¨ Whenyoulendmoneytoabusiness, youareallowingthestockholders tousethatmoneyinthecourseofrunningthatbusiness. Stockholdersinterestsaredifferent fromyourinterests, because¤ You(aslender)areinterested ingettingyourmoneyback¤ Stockholders areinterestedinmaximizing theirwealth

¨ Insomecases, theclashofinterestscanleadtostockholders¤ Investinginriskierprojects thanyouwouldwantthemto¤ Payingthemselves largedividends whenyouwouldratherhavethemkeepthecash

inthebusiness.¨ Proposition4:Otherthingsbeingequal,thegreatertheagencyproblems

associatedwithlendingtoafirm,thelessdebtthefirmcanaffordtouse.

21

DebtandAgencyCosts

Aswath Damodaran

21

¨ Assumethatyouareabank.Whichofthefollowingbusinesseswouldyouperceivethegreatestagencycosts?

a. ATechnologyfirmb. ALargeRegulatedElectricUtilityc. ARealEstateCorporation¨ Why?

22

Lossoffuturefinancingflexibility

Aswath Damodaran

22

¨ Whenafirmborrowsuptoitscapacity,itlosestheflexibilityoffinancingfutureprojectswithdebt.

¨ Thus,ifthefirmisfacedwithanunexpectedinvestmentopportunityorabusinessshortfall,itwillnotbeabletodrawondebtcapacity,ifithasalreaduseditup.

¨ Proposition5:Otherthingsremainingequal,themoreuncertainafirmisaboutitsfuturefinancingrequirementsandprojects,thelessdebtthefirmwilluseforfinancingcurrentprojects.

23

Whatmanagersconsiderimportantindecidingonhowmuchdebttocarry...

Aswath Damodaran

23

¨ AsurveyofChiefFinancialOfficersoflargeU.S.companiesprovidedthefollowingranking(frommostimportanttoleastimportant)forthefactorsthattheyconsideredimportantinthefinancingdecisionsFactor Ranking (0-5)1.Maintainfinancialflexibility 4.552.Ensurelong-term survival 4.553.MaintainPredictable SourceofFunds 4.054.Maximize StockPrice 3.995.Maintainfinancial independence 3.886.Maintainhighdebtrating 3.567.Maintaincomparabilitywithpeergroup 2.47

24

Debt:Summarizingthetradeoff

Aswath Damodaran

24

25

TheTradeoffforDisney,Vale,TataMotorsandBaidu

Aswath Damodaran

25

Debt trade off Discussion of relative benefits/costs Tax benefits Marginal tax rates of 40% in US (Disney & Bookscape), 32.5% in India (Tata

Motors), 25% in China (Baidu) and 34% in Brazil (Vale), but there is an offsetting tax benefit for equity in Brazil (interest on equity capital is deductible).

Added Discipline

The benefits should be highest at Disney, where there is a clear separation of ownership and management and smaller at the remaining firms.

Expected Bankruptcy Costs

Volatility in earnings: Higher at Baidu (young firm in technology), Tata Motors (cyclicality) and Vale (commodity prices) and lower at Disney (diversified across entertainment companies). Indirect bankruptcy costs likely to be highest at Tata Motors, since it’s products (automobiles) have long lives and require service and lower at Disney and Baidu.

Agency Costs Highest at Baidu, largely because it’s assets are intangible and it sells services and lowest at Vale (where investments are in mines, highly visible and easily monitored) and Tata Motors (tangible assets, family group backing). At Disney, the agency costs will vary across its business, higher in the movie and broadcasting businesses and lower at theme parks.

Flexibility needs

Baidu will value flexibility more than the other firms, because technology is a shifting and unpredictable business, where future investment needs are difficult to forecast. The flexibility needs should be lower at Disney and Tata Motors, since they are mature companies with well-established investment needs. At Vale, the need for investment funds may vary with commodity prices, since the firm grows by acquiring both reserves and smaller companies. At Bookscape, the difficulty of accessing external capital will make flexibility more necessary.

26

6 ApplicationTest:Wouldyouexpectyourfirmtogainorlosefromusingalotofdebt?

Aswath Damodaran

26

¨ Considering,foryourfirm,¤ Thepotentialtaxbenefitsofborrowing¤ Thebenefitsofusingdebtasadisciplinarymechanism¤ Thepotentialforexpectedbankruptcycosts¤ Thepotentialforagencycosts¤ Theneedforfinancialflexibility

¨ Wouldyouexpectyourfirmtohaveahighdebtratiooralowdebtratio?

¨ Doesthefirm’scurrentdebtratiomeetyourexpectations?