corporate debt restructuring - cdr · pdf filecorporate debt restructuring - cdr strictly...

TRANSCRIPT

Corporate Debt Restructuring - CDR

Strictly Private and Confidential

Mr. Vishal Gupta Vice President-PASF SBI Capital Markets Limited

Corporate Debt Restructuring Strictly Private and Confidential

Corporate Debt Restructuring System

CDR Process

Lender’s Requirements

Relevant IRAC Guidelines

Preparing the Scheme

Other Practical Aspects

Exit & Recompense

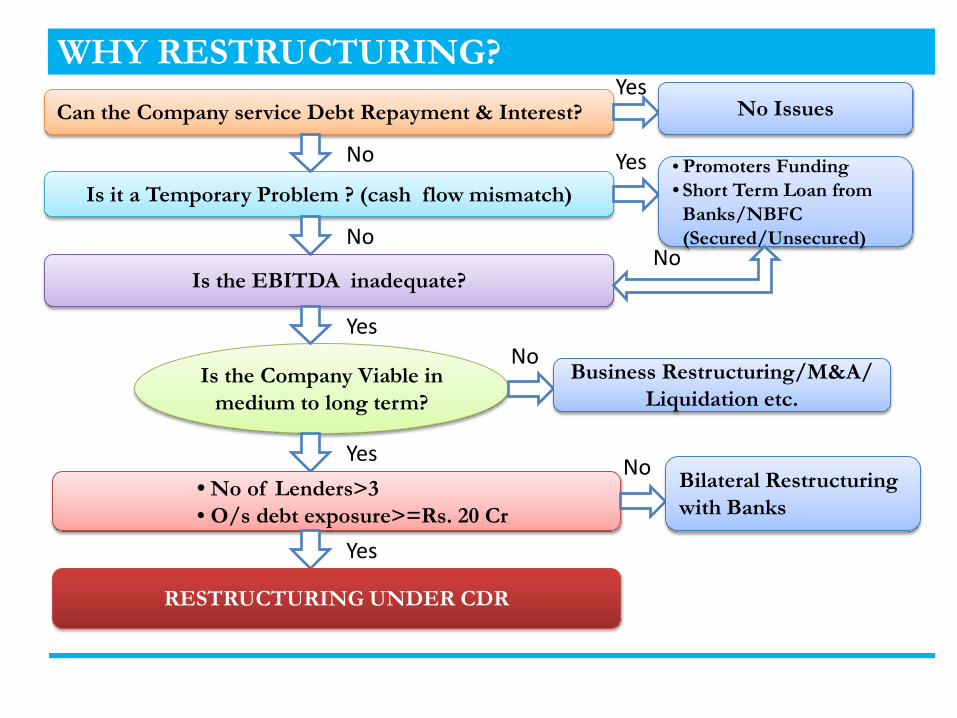

WHY RESTRUCTURING?

Is it a Temporary Problem ? (cash flow mismatch)

Can the Company service Debt Repayment & Interest?

Is the EBITDA inadequate?

Is the Company Viable in medium to long term?

• No of Lenders>3 • O/s debt exposure>=Rs. 20 Cr

RESTRUCTURING UNDER CDR

No Issues Yes

No • Promoters Funding • Short Term Loan from

Banks/NBFC (Secured/Unsecured)

Yes

Yes

No No

No Business Restructuring/M&A/

Liquidation etc.

Yes

Yes

Bilateral Restructuring with Banks

No

CDR Mechanism - Genesis

• Corporate Debt Restructuring (CDR) Mechanism evolved with the guidelines issued by RBI on August 23, 2001

• Need for an institutional mechanism for debt restructuring like felt due to delay in agreement among different lenders, inter creditor issues and also experience from countries like UK, Thailand, Korea, Malaysia etc.

• Basic purpose of CDR exercise is the revival of the corporate and safety of the money lent by Banks and Financial Institutions.

• CDR is voluntary non-statutory system based on Debtor-Creditor Agreement (DCA) and Inter-Creditor Agreement (ICA)

Strictly Private and Confidential

Objectives of CDR

• By way of CDR there is a hope of preservation of viable corporate that are affected by certain internal & external factors

• CDR aims at minimising the losses to creditors & other stakeholders through an

orderly & coordinates restructuring programme • To support continuing economic recovery

Whether a case should be referred for restructuring or not is based upon thorough examination of facts & viability of the case

However, wherever the demand for restructuring is legitimate, and there is a good reason to believe that the corporation may be revived, it must be considered for restructuring.

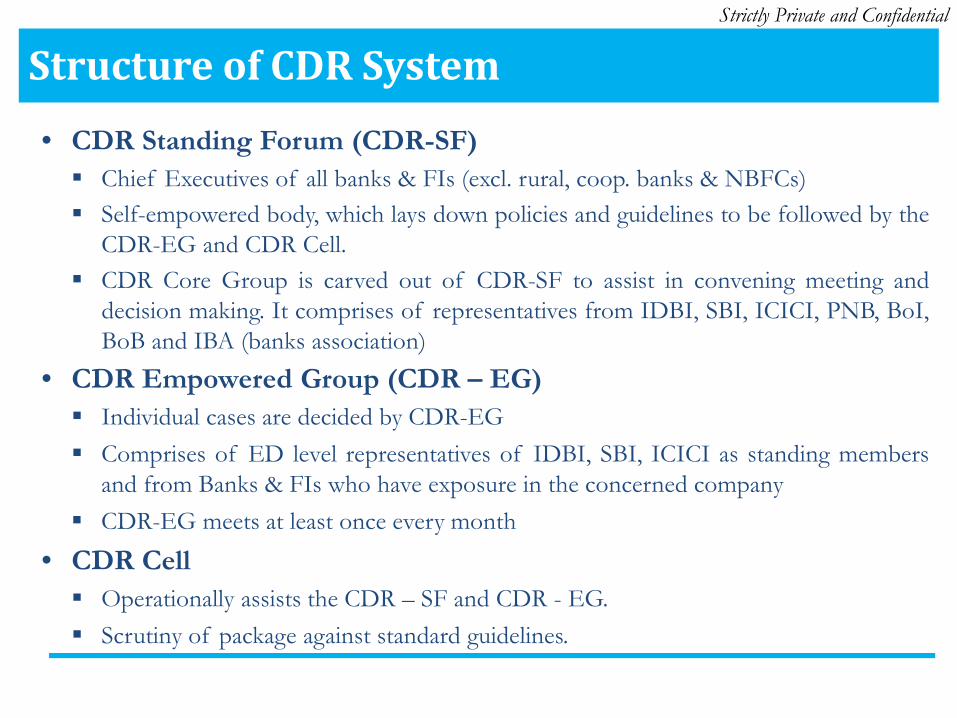

Structure of CDR System

• CDR Standing Forum (CDR-SF) Chief Executives of all banks & FIs (excl. rural, coop. banks & NBFCs) Self-empowered body, which lays down policies and guidelines to be followed by the

CDR-EG and CDR Cell. CDR Core Group is carved out of CDR-SF to assist in convening meeting and

decision making. It comprises of representatives from IDBI, SBI, ICICI, PNB, BoI, BoB and IBA (banks association)

• CDR Empowered Group (CDR – EG) Individual cases are decided by CDR-EG Comprises of ED level representatives of IDBI, SBI, ICICI as standing members

and from Banks & FIs who have exposure in the concerned company CDR-EG meets at least once every month

• CDR Cell Operationally assists the CDR – SF and CDR - EG. Scrutiny of package against standard guidelines.

Strictly Private and Confidential

Legal basis of CDR system Strictly Private and Confidential

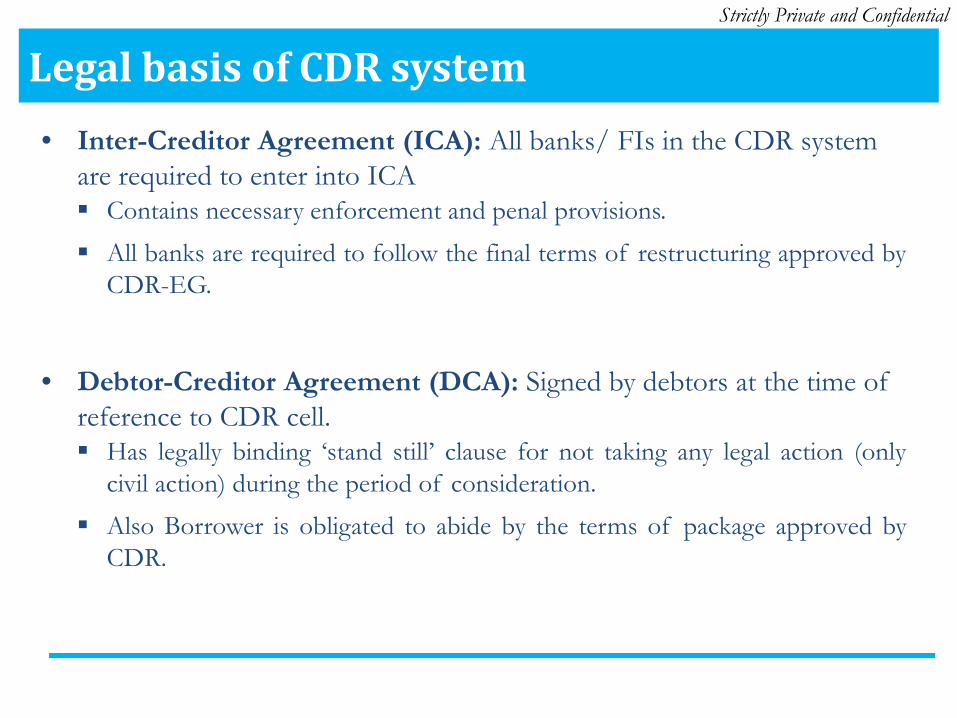

• Inter-Creditor Agreement (ICA): All banks/ FIs in the CDR system are required to enter into ICA Contains necessary enforcement and penal provisions.

All banks are required to follow the final terms of restructuring approved by CDR-EG.

• Debtor-Creditor Agreement (DCA): Signed by debtors at the time of

reference to CDR cell. Has legally binding ‘stand still’ clause for not taking any legal action (only

civil action) during the period of consideration.

Also Borrower is obligated to abide by the terms of package approved by CDR.

Category of Cases under CDR Strictly Private and Confidential

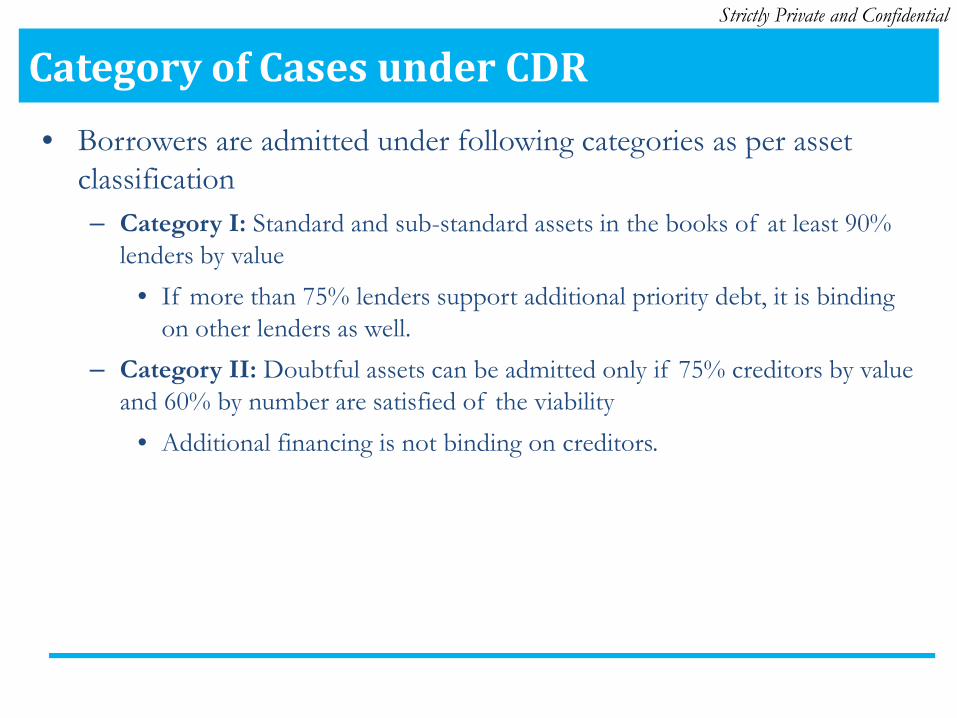

• Borrowers are admitted under following categories as per asset classification – Category I: Standard and sub-standard assets in the books of at least 90%

lenders by value • If more than 75% lenders support additional priority debt, it is binding

on other lenders as well. – Category II: Doubtful assets can be admitted only if 75% creditors by value

and 60% by number are satisfied of the viability • Additional financing is not binding on creditors.

Corporate Debt Restructuring Strictly Private and Confidential

Corporate Debt Restructuring System

CDR Process

Lender’s Requirements

Relevant IRAC Guidelines

Preparing the Scheme

Other Practical Aspects

Exit & Recompense

CDR vs. Restructuring without CDR

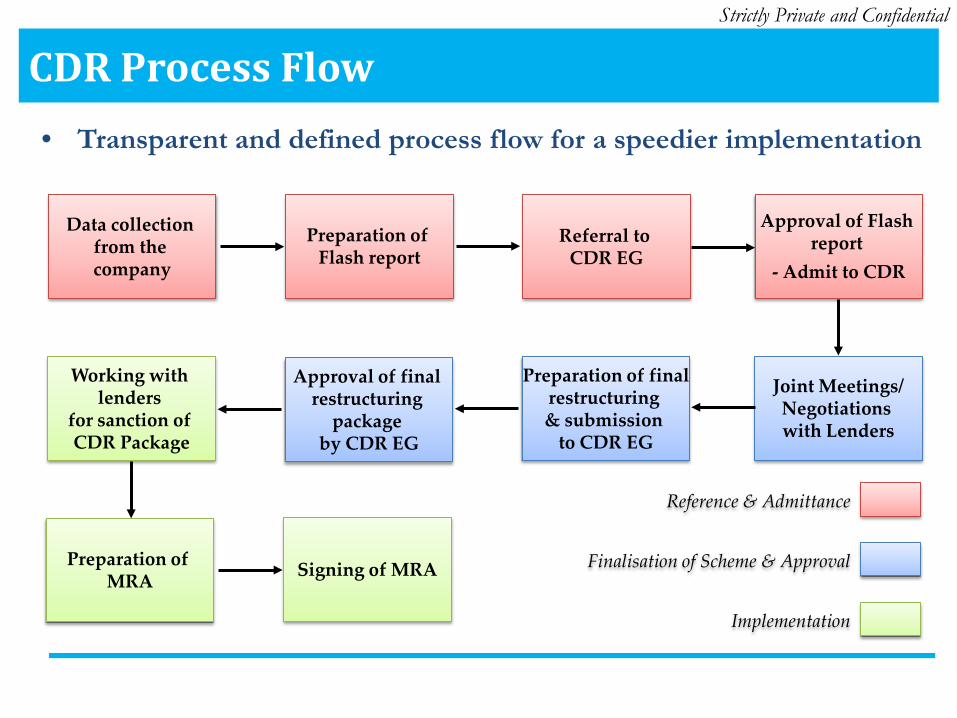

CDR Process Flow Strictly Private and Confidential

• Transparent and defined process flow for a speedier implementation

Data collection from the company

Preparation of Flash report

Referral to CDR EG

Approval of Flash report

- Admit to CDR

Working with lenders

for sanction of CDR Package

Approval of final

restructuring package

by CDR EG

Preparation of final restructuring & submission

to CDR EG

Joint Meetings/ Negotiations with Lenders

Preparation of MRA Signing of MRA

Reference & Admittance

Finalisation of Scheme & Approval

Implementation

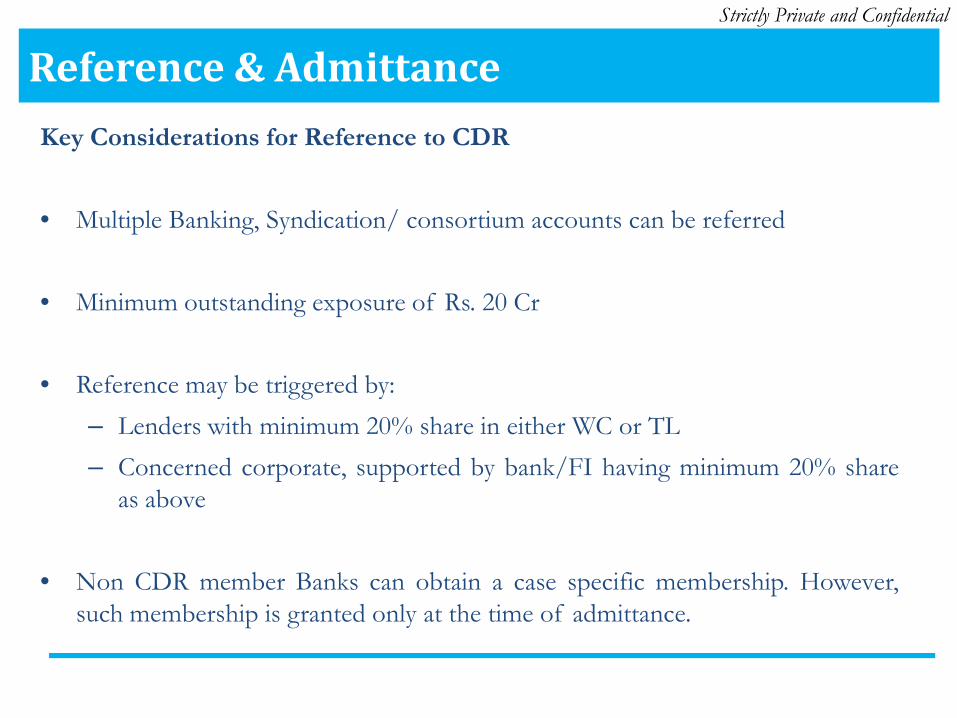

Reference & Admittance Strictly Private and Confidential

Key Considerations for Reference to CDR

• Multiple Banking, Syndication/ consortium accounts can be referred

• Minimum outstanding exposure of Rs. 20 Cr

• Reference may be triggered by: – Lenders with minimum 20% share in either WC or TL – Concerned corporate, supported by bank/FI having minimum 20% share

as above

• Non CDR member Banks can obtain a case specific membership. However, such membership is granted only at the time of admittance.

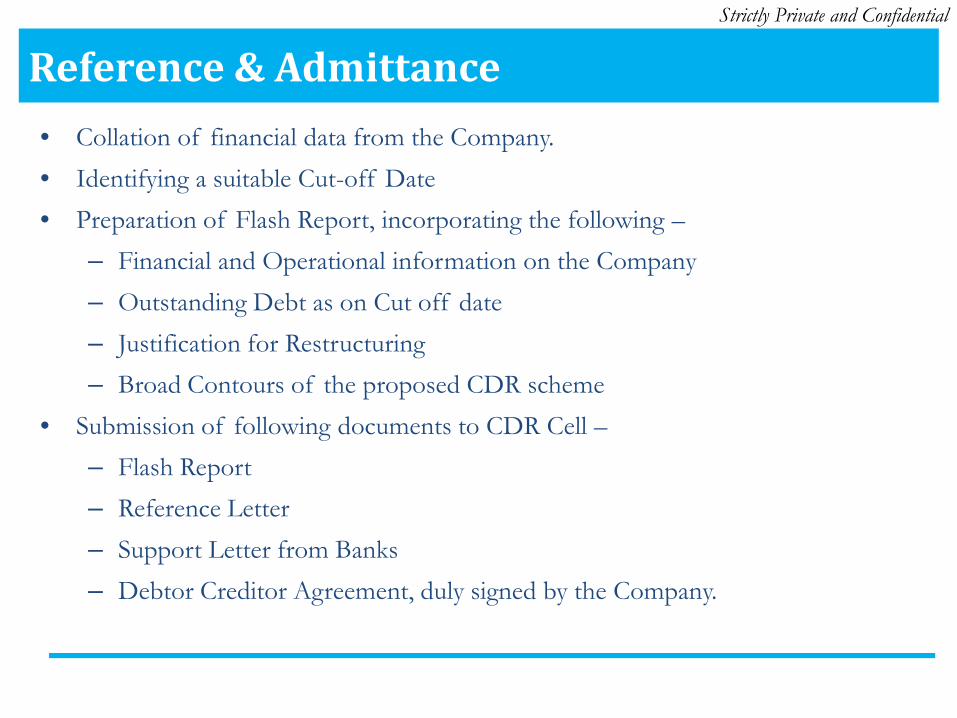

Reference & Admittance Strictly Private and Confidential

• Collation of financial data from the Company. • Identifying a suitable Cut-off Date • Preparation of Flash Report, incorporating the following –

– Financial and Operational information on the Company – Outstanding Debt as on Cut off date – Justification for Restructuring – Broad Contours of the proposed CDR scheme

• Submission of following documents to CDR Cell – – Flash Report – Reference Letter – Support Letter from Banks – Debtor Creditor Agreement, duly signed by the Company.

Reference & Admittance Strictly Private and Confidential

• CDR Cell circulates the Flash Report amongst all the lenders to the Company, which are members of CDR system.

• In the following CDR EG meeting, the lenders vote for/against the admission of the Company into CDR process.

• For admittance Super Majority vote, 60% by number and 75% by outstanding, is required.

• In case few lenders do not have the mandate to vote, they may inform their stand to CDR Cell within 3-4 days or else such lenders are not counted for calculating the Supermajority.

• The CDR cell lenders circulates the Minutes of Meeting, which confirms the admittance of the Company into the CDR Process. Further, the ‘stand still’ comes into effect from the cut-off date upon implementation

Reference & Admittance Strictly Private and Confidential

• Following decisions are taken at the time of Admittance of the Borrower into the CDR process –

– Borrower Classification, which would be one of the following – • Class ‘A’: Corporates affected by external factors pertaining to

economy and industry. • Class ‘B’: Corporates affected by external factors and also have weak

resources, inadequate vision and lack of professional management • Class ‘C’: Over ambitious promoters and corporates which diverted

funds to related/ unrelated fields without lenders permission • Class ‘D’: Financially undisciplined borrower corporates.

– Formation of Monitoring Committee and also the Monitoring Institution.

Finalization of CDR Scheme Strictly Private and Confidential

• Post admittance, detailed discussions take place between borrower, its Advisors and lenders (led/represented by Monitoring Institution) to prepare a scheme acceptable to all.

• The revised scheme is circulated to the Monitoring Committee members for their concurrence and subsequently circulated amongst all the lenders.

• The scheme is then submitted to the CDR Cell for final approval.

• Final approval entails a further Super Majority vote in the CDR EG meet.

• All the lenders and their outstanding are to be considered while calculating Super Majority vote at his stage. These would include the lenders who do not have the mandate to vote on the scheme.

• In case Supermajority is not achieved, the CDR EG can either reject the scheme or, if time permits, may recommend submission of a revised scheme.

Approval of the Scheme Strictly Private and Confidential

• Upon achievement of Super Majority, CDR Cell circulates the confirmed Minutes of Meeting of CDR EG to all the Lenders and the Borrower.

• Further, a Letter of Approval (LoA) is issued by CDR Cell to the Monitoring Institution. A typical LoA shall contain the following –

– Approved Scheme with Lender Wise details – Standard and Additional Conditions stipulated by Lenders and CDR EG to

be adhered to by the Borrower. – Critical Conditions for Implementation of the Scheme. – Instructions to Monitoring Institutions and the Borrower towards

successful implementation of the scheme.

Implementation of the Scheme Strictly Private and Confidential

• The lenders need to obtain approvals from the competent authority on the final restructuring package and for the signing of the Master Restructuring Agreement (MRA).

• Legal Counsel are appointed in consultation with Monitoring Institution for drafting the MRA and other Documents.

• As per the CDR Master Circular, a package is considered implemented if the following conditions are met -

– The package was sanctioned by the lender(s) concerned and effect had been given in the books of account of the lender(s);

– Promoters’ contribution to the extent envisaged in the package had been brought in; and

– MRA was executed binding the lender(s) and the company for compliance of all terms and conditions of the approved package.

• The CDR Cell can also specify additional ‘Critical conditions’ it may deem necessary for the package to be considered implemented.

• Upon successful completion of the above activities, the CDR Scheme is deemed implemented.

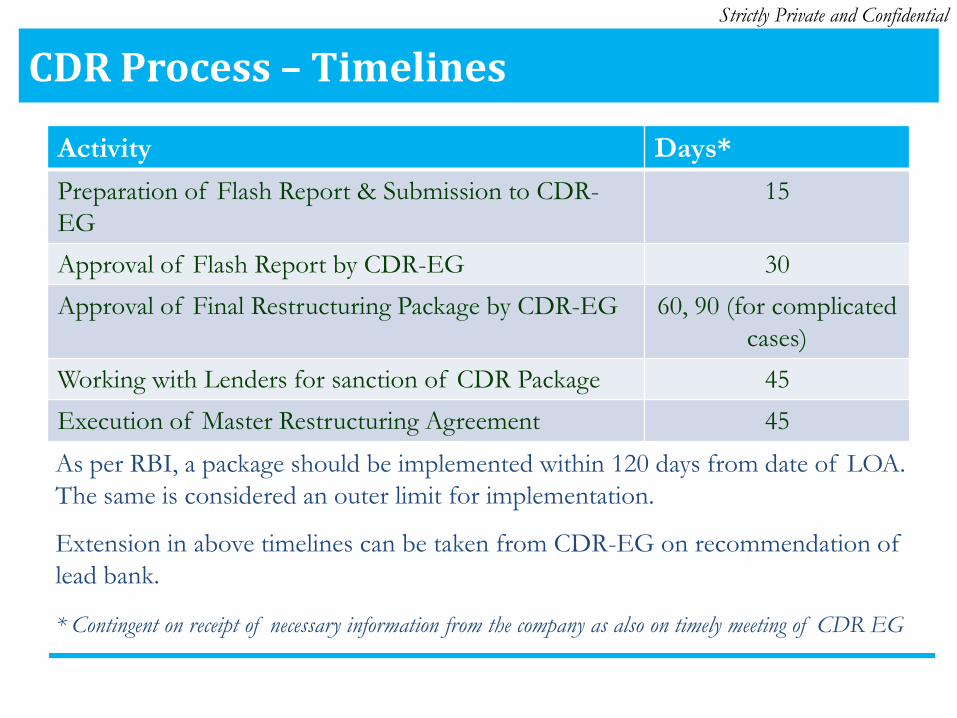

CDR Process – Timelines Strictly Private and Confidential

Activity Days* Preparation of Flash Report & Submission to CDR-EG

15

Approval of Flash Report by CDR-EG 30 Approval of Final Restructuring Package by CDR-EG 60, 90 (for complicated

cases) Working with Lenders for sanction of CDR Package 45 Execution of Master Restructuring Agreement 45

As per RBI, a package should be implemented within 120 days from date of LOA. The same is considered an outer limit for implementation.

Extension in above timelines can be taken from CDR-EG on recommendation of lead bank.

* Contingent on receipt of necessary information from the company as also on timely meeting of CDR EG

Corporate Debt Restructuring Strictly Private and Confidential

Corporate Debt Restructuring System

CDR Process

Lender’s Requirements

Relevant IRAC Guidelines

Preparing the Scheme

Other Practical Aspects

Exit & Recompense

Requirement of lenders- CDR cases

Due diligence Referring institution to ensure viability of unit at time of submission of

flash report.

If required, detailed TEV study from reputed independent agency may be

conducted at time of drafting final CDR package

Possibilities of management change may be explored.

Forensic audit in case MI suspects diversion of funds

Requirement of lenders- CDR cases

Scheme Rate of interest for FITL /WCTL should be minimum base rate

Monetisation of non core assets may be made in time bound manner.

No expansion of unit may be permitted beyond CDR package without

permission of CDR EG.

Funding for expansion to enhance performance may be considered with

funding being borne by promoters.

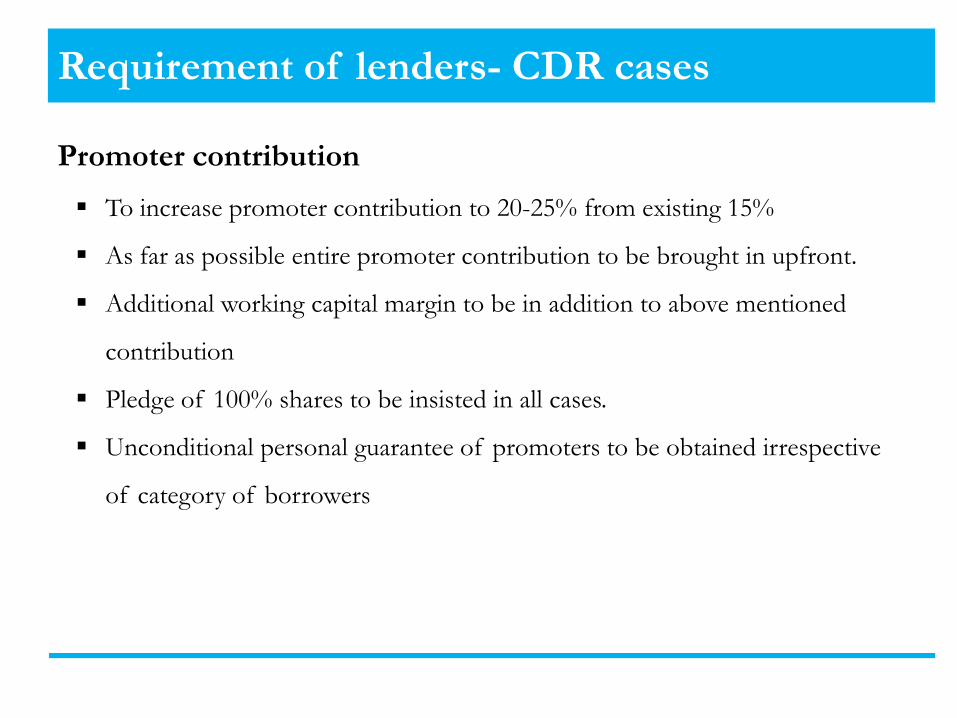

Requirement of lenders- CDR cases

Promoter contribution To increase promoter contribution to 20-25% from existing 15%

As far as possible entire promoter contribution to be brought in upfront.

Additional working capital margin to be in addition to above mentioned

contribution

Pledge of 100% shares to be insisted in all cases.

Unconditional personal guarantee of promoters to be obtained irrespective

of category of borrowers

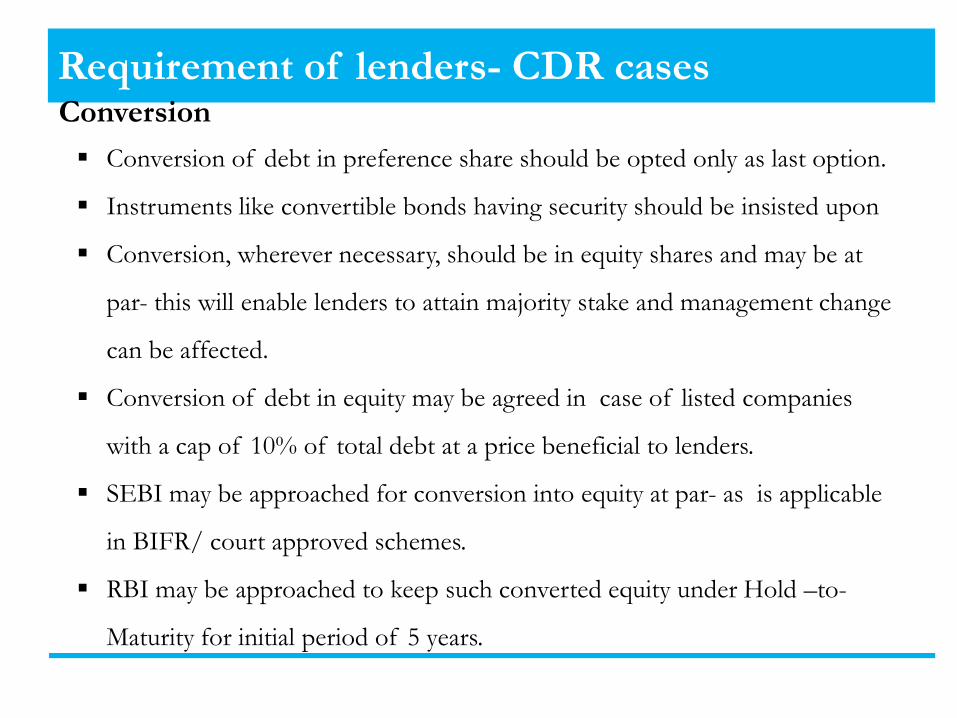

Requirement of lenders- CDR cases Conversion Conversion of debt in preference share should be opted only as last option.

Instruments like convertible bonds having security should be insisted upon

Conversion, wherever necessary, should be in equity shares and may be at

par- this will enable lenders to attain majority stake and management change

can be affected.

Conversion of debt in equity may be agreed in case of listed companies

with a cap of 10% of total debt at a price beneficial to lenders.

SEBI may be approached for conversion into equity at par- as is applicable

in BIFR/ court approved schemes.

RBI may be approached to keep such converted equity under Hold –to-

Maturity for initial period of 5 years.

Requirement of lenders- CDR cases

Monitoring Monitoring mechanism to be strengthened with periodical review

Two lead lenders to be made MI

CDR cell would not be a part of Monitoring committee.

Lead bank to appoint nominee director on board of the Company.

TRA mechanism to be adopted in all cases

Monetisation of non core assets may be made in time bound manner.

No expansion of unit may be permitted beyond CDR package without

permission of CDR EG.

Funding for expansion to enhance performance may be considered with

funding being borne by promoters.

Requirement of lenders- CDR cases

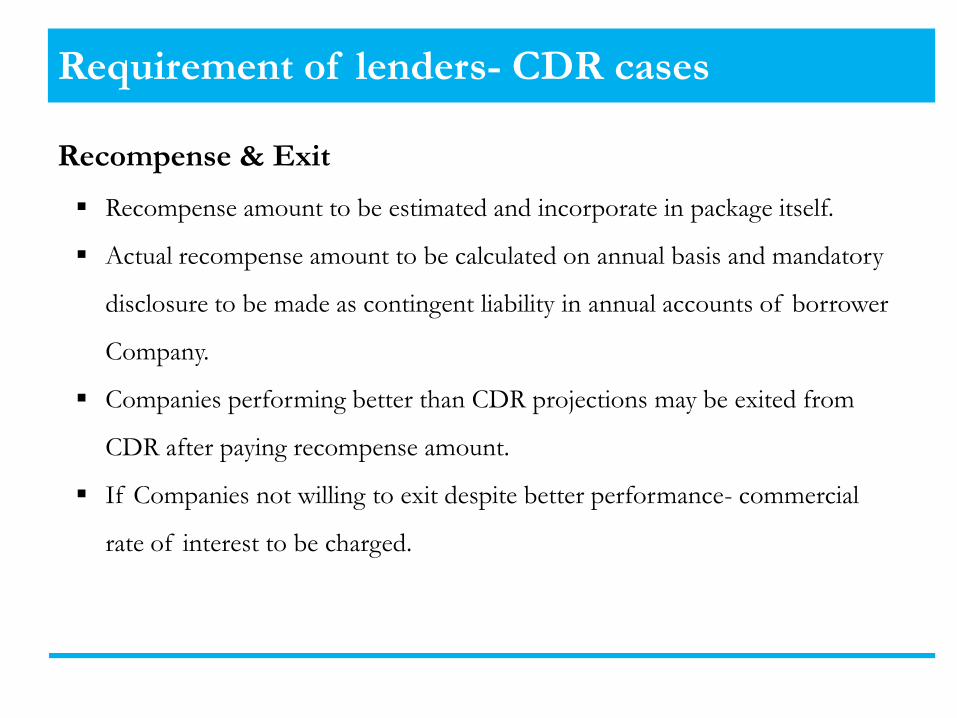

Recompense & Exit Recompense amount to be estimated and incorporate in package itself.

Actual recompense amount to be calculated on annual basis and mandatory

disclosure to be made as contingent liability in annual accounts of borrower

Company.

Companies performing better than CDR projections may be exited from

CDR after paying recompense amount.

If Companies not willing to exit despite better performance- commercial

rate of interest to be charged.

Corporate Debt Restructuring Strictly Private and Confidential

Corporate Debt Restructuring System

CDR Process

Lender’s Requirements

Relevant IRAC Guidelines

Preparing the Scheme

Other Practical Aspects

Exit & Recompense

IRAC Guidelines – Asset Classification

Strictly Private and Confidential

• As per the IRAC Guidelines issued by RBI, the degradation of the asset class upon restructuring can be avoided, provided following conditions are met - – The dues are fully secured

– Unit becomes viable in 10 years (Infrastructure) and 7 Years ( Non – Infrastructure)

– Repayment period, including moratorium, not to exceed 15 years for Infrastructure and 10 years for Non-Infrastructure.

– Promoter’s sacrifice and additional funds brought by them should be at least 15% of the Banks’ sacrifice.

– Personal Guarantee is offered by the promoter except when the unit is affected by external factors pertaining to economy and industry.

– The restructuring under consideration is not a “repeated restructuring”. However, recently RBI has permitted the retention of account classification as standard even while repeated restructuring, if the NPV Loss is covered for.

Strictly Private and Confidential

• As per the IRAC Guidelines issued by RBI (2012) , the promoter contribution should be brought in as follows

– The promoter sacrifice should generally be brought upfront

– However, if the banks are convinced that promoter faces genuine difficulty in bringing in the required amount upfront, following can be allowed

• 50% of the promoter contribution to be brought upfront

• Remaining 50% of the promoter contribution within a period of 1 year

IRAC Guidelines – Promoter Contribution

Strictly Private and Confidential

• As per the IRAC Guidelines issued by RBI (2012) , benefits of asset classification upgradation immediately on restructuring would not be available to the following

– Assets pertaining to the Real Estate, Capital Market Exposure and Consumer and Personal Advances; are immediately downgraded to sub-standard upon restructuring (CDR or otherwise)

– These sub-standard assets would only be eligible for up-gradation to the standard category after observation of satisfactory performance during the 12 months from the first date of payment of principal or interest, as per the restructured package

S IRAC Guidelines – CDR for Real Estate & CME Exposures

Corporate Debt Restructuring Strictly Private and Confidential

Corporate Debt Restructuring System

CDR Process

Lender’s Requirements

Relevant IRAC Guidelines

Preparing the Scheme

Other Practical Aspects

Exit & Recompense

Strictly Private and Confidential

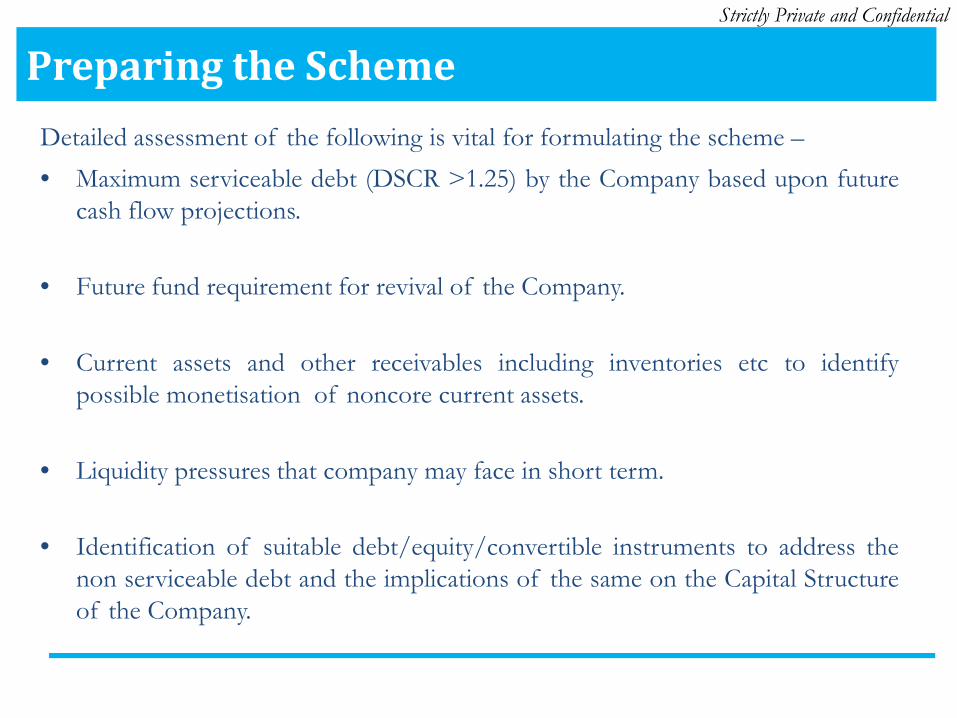

Detailed assessment of the following is vital for formulating the scheme – • Maximum serviceable debt (DSCR >1.25) by the Company based upon future

cash flow projections.

• Future fund requirement for revival of the Company.

• Current assets and other receivables including inventories etc to identify possible monetisation of noncore current assets.

• Liquidity pressures that company may face in short term.

• Identification of suitable debt/equity/convertible instruments to address the non serviceable debt and the implications of the same on the Capital Structure of the Company.

Preparing the Scheme

Strictly Private and Confidential

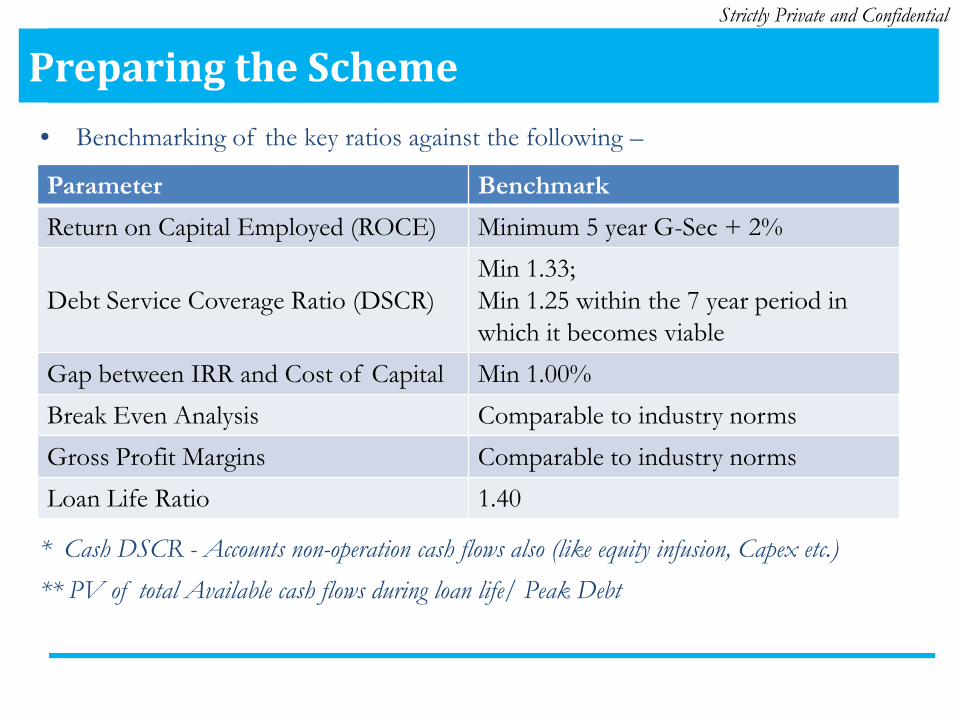

• Benchmarking of the key ratios against the following –

Parameter Benchmark Return on Capital Employed (ROCE) Minimum 5 year G-Sec + 2%

Debt Service Coverage Ratio (DSCR) Min 1.33; Min 1.25 within the 7 year period in which it becomes viable

Gap between IRR and Cost of Capital Min 1.00% Break Even Analysis Comparable to industry norms Gross Profit Margins Comparable to industry norms Loan Life Ratio 1.40

* Cash DSCR - Accounts non-operation cash flows also (like equity infusion, Capex etc.) ** PV of total Available cash flows during loan life/ Peak Debt

Preparing the Scheme

Strictly Private and Confidential

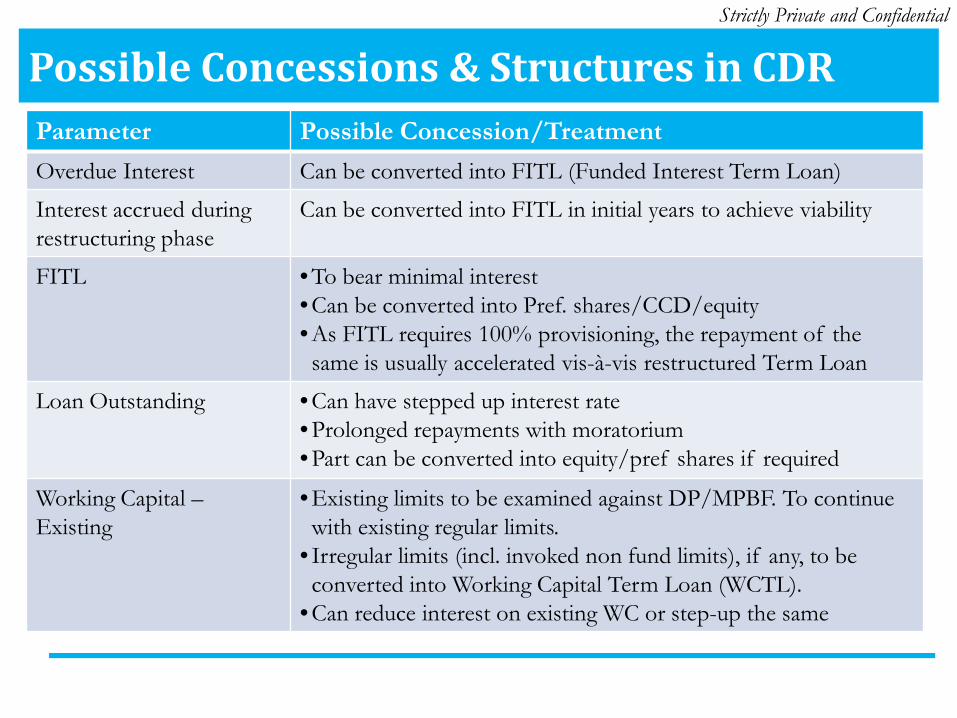

Parameter Possible Concession/Treatment Overdue Interest Can be converted into FITL (Funded Interest Term Loan)

Interest accrued during restructuring phase

Can be converted into FITL in initial years to achieve viability

FITL • To bear minimal interest • Can be converted into Pref. shares/CCD/equity • As FITL requires 100% provisioning, the repayment of the same is usually accelerated vis-à-vis restructured Term Loan

Loan Outstanding • Can have stepped up interest rate • Prolonged repayments with moratorium • Part can be converted into equity/pref shares if required

Working Capital – Existing

• Existing limits to be examined against DP/MPBF. To continue with existing regular limits.

• Irregular limits (incl. invoked non fund limits), if any, to be converted into Working Capital Term Loan (WCTL).

• Can reduce interest on existing WC or step-up the same

Possible Concessions & Structures in CDR

Strictly Private and Confidential

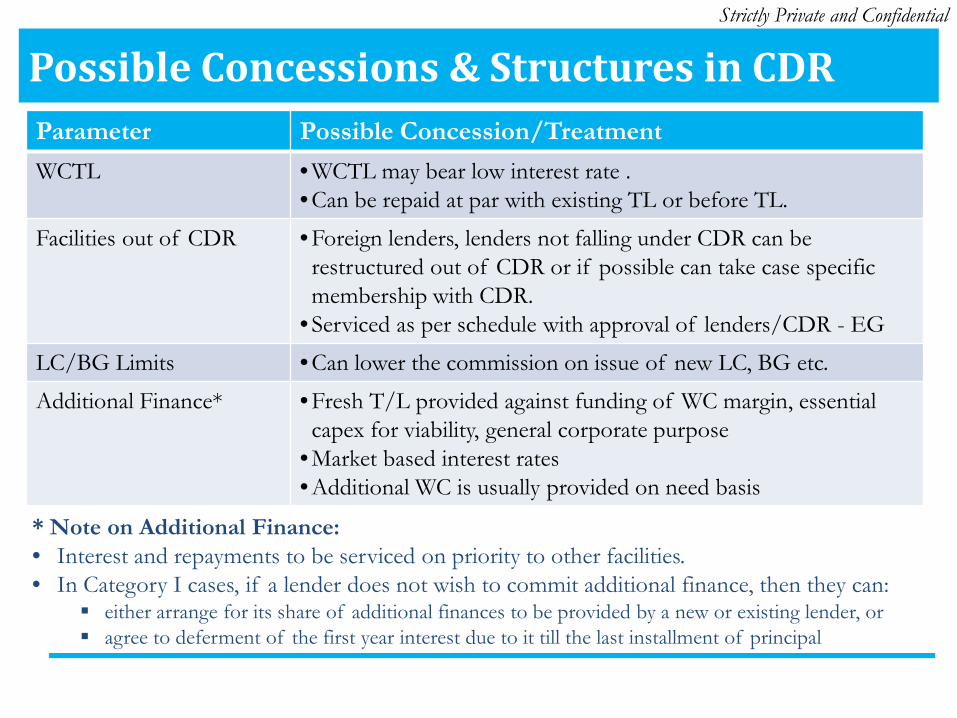

Parameter Possible Concession/Treatment WCTL • WCTL may bear low interest rate .

• Can be repaid at par with existing TL or before TL.

Facilities out of CDR • Foreign lenders, lenders not falling under CDR can be restructured out of CDR or if possible can take case specific membership with CDR.

• Serviced as per schedule with approval of lenders/CDR - EG

LC/BG Limits • Can lower the commission on issue of new LC, BG etc.

Additional Finance* • Fresh T/L provided against funding of WC margin, essential capex for viability, general corporate purpose

• Market based interest rates • Additional WC is usually provided on need basis

* Note on Additional Finance: • Interest and repayments to be serviced on priority to other facilities. • In Category I cases, if a lender does not wish to commit additional finance, then they can:

either arrange for its share of additional finances to be provided by a new or existing lender, or agree to deferment of the first year interest due to it till the last installment of principal

Possible Concessions & Structures in CDR

Strictly Private and Confidential

• All cash flows including operations, infusions, asset sales, repayments etc. shall be routed through the TRA monitored by lead bank and concurrent auditor.

• Concurrent Auditor to review the operations during the package.

• Any additional capex, induction of investors, settlements, dividends issue, asset sale etc. require approval of CDR EG.

• Lenders have right to reset the interest rate of the term loans every 3 years and working capital interest rate every year.

• Promoter to give undertaking for to bring additional funds for meeting any cash shortfall for servicing lender’s interest/repayments

Standard Conditions of CDR

Strictly Private and Confidential

• Lenders have to provide for the loss in fair value of advances (sacrifice amount). Calculation and provisioning methodology provided in following slides.

• Lenders to have right to accelerate repayment in case of better performance and also right to recompense against sacrifice.

• Any settlement with out of CDR creditor will need prior approval of CDR – EG

• Lenders have right to convert up to 20% of the loan outstanding (TL, WCTL, FITL) beyond 7 years into equity

– Such conversion shall be as per SEBI guidelines – For zero-coupon FITL, conversion is applicable on entire outstanding beyond 7

years.

Standard Conditions of CDR contd..

Strictly Private and Confidential

Promoter Contribution: • Should be at least 15% (now 25%) of CDR lender’s sacrifice amount.

– 50% should be brought up-front and balance within 1 year • Reduction in value of equity from the face value of equity owing to de-rating

would be treated as sacrifice. • Dilution of equity shareholding is not be considered as sacrifice.

Promoter’s Share Pledge • Pledge of entire promoter shareholding (or at least 51% of paid-up capital) in

the company is to be pledged in all cases apart from Class ‘A’ borrower. • However, it is normally insisted by lenders for all class of Borrowers.

Personal Guarantee • Personal Guarantee of the borrower is sought for.

Conditions Relating to the Promoter

Corporate Debt Restructuring Strictly Private and Confidential

Corporate Debt Restructuring System

CDR Process

Lender’s Requirements

Relevant IRAC Guidelines

Preparing the Scheme

Other Practical Aspects

Exit & Recompense

Strictly Private and Confidential

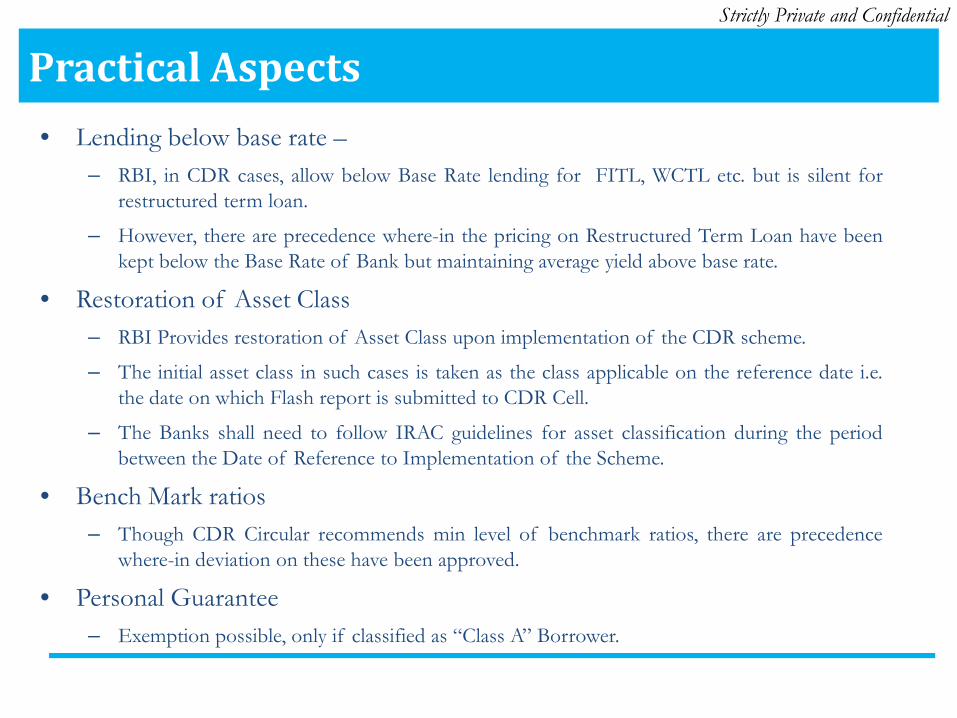

• Lending below base rate – – RBI, in CDR cases, allow below Base Rate lending for FITL, WCTL etc. but is silent for

restructured term loan.

– However, there are precedence where-in the pricing on Restructured Term Loan have been kept below the Base Rate of Bank but maintaining average yield above base rate.

• Restoration of Asset Class – RBI Provides restoration of Asset Class upon implementation of the CDR scheme.

– The initial asset class in such cases is taken as the class applicable on the reference date i.e. the date on which Flash report is submitted to CDR Cell.

– The Banks shall need to follow IRAC guidelines for asset classification during the period between the Date of Reference to Implementation of the Scheme.

• Bench Mark ratios – Though CDR Circular recommends min level of benchmark ratios, there are precedence

where-in deviation on these have been approved.

• Personal Guarantee – Exemption possible, only if classified as “Class A” Borrower.

Practical Aspects

Strictly Private and Confidential

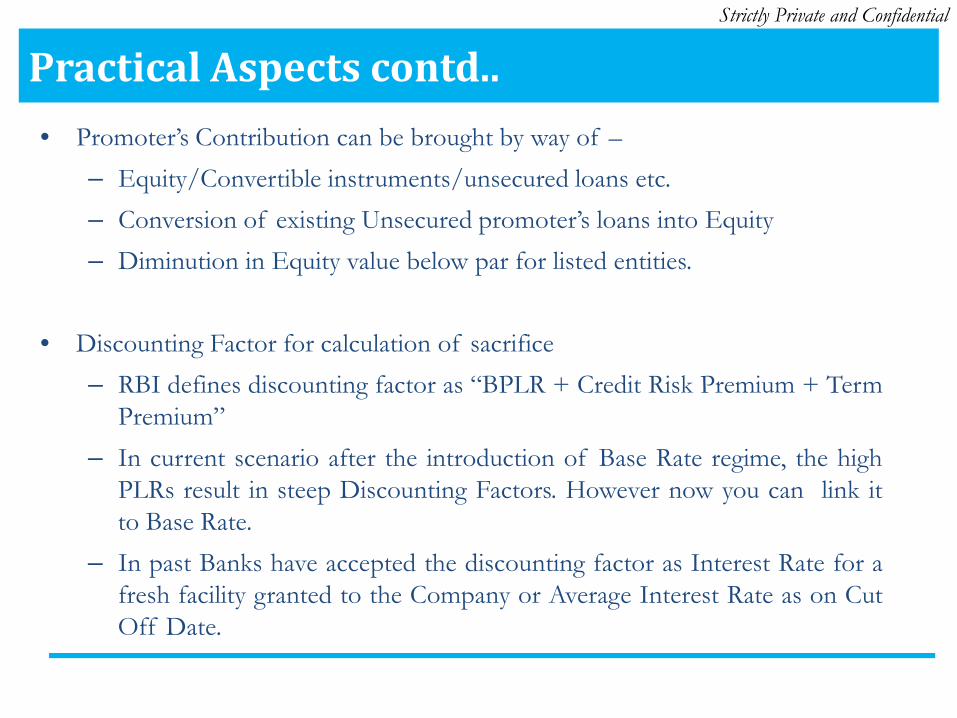

• Promoter’s Contribution can be brought by way of – – Equity/Convertible instruments/unsecured loans etc. – Conversion of existing Unsecured promoter’s loans into Equity – Diminution in Equity value below par for listed entities.

• Discounting Factor for calculation of sacrifice

– RBI defines discounting factor as “BPLR + Credit Risk Premium + Term Premium”

– In current scenario after the introduction of Base Rate regime, the high PLRs result in steep Discounting Factors. However now you can link it to Base Rate.

– In past Banks have accepted the discounting factor as Interest Rate for a fresh facility granted to the Company or Average Interest Rate as on Cut Off Date.

Practical Aspects contd..

Strictly Private and Confidential

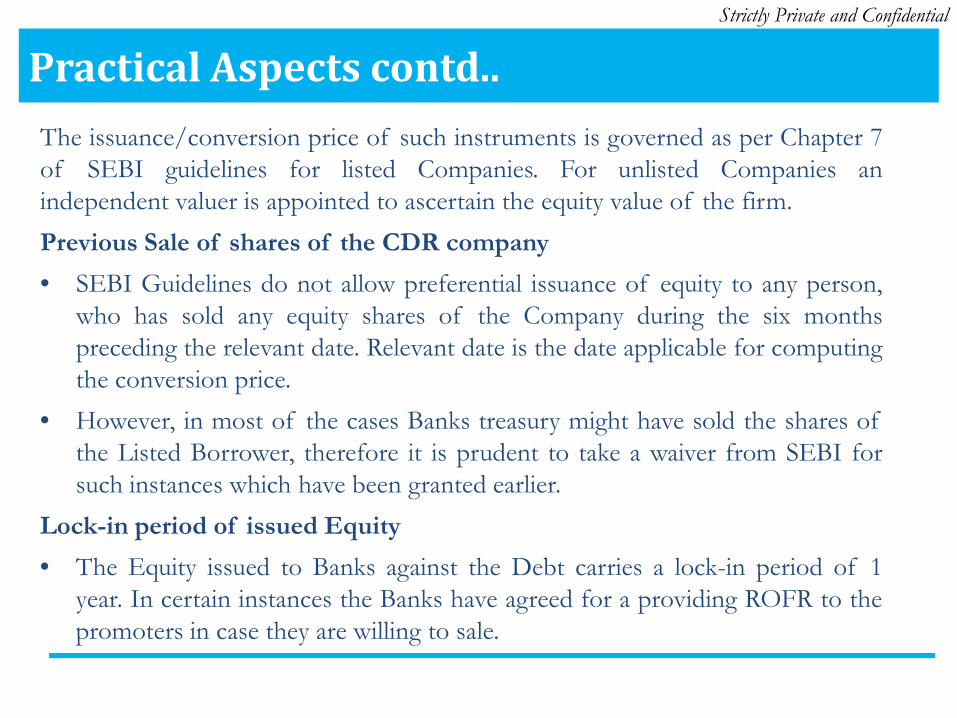

The issuance/conversion price of such instruments is governed as per Chapter 7 of SEBI guidelines for listed Companies. For unlisted Companies an independent valuer is appointed to ascertain the equity value of the firm. Previous Sale of shares of the CDR company • SEBI Guidelines do not allow preferential issuance of equity to any person,

who has sold any equity shares of the Company during the six months preceding the relevant date. Relevant date is the date applicable for computing the conversion price.

• However, in most of the cases Banks treasury might have sold the shares of the Listed Borrower, therefore it is prudent to take a waiver from SEBI for such instances which have been granted earlier.

Lock-in period of issued Equity • The Equity issued to Banks against the Debt carries a lock-in period of 1

year. In certain instances the Banks have agreed for a providing ROFR to the promoters in case they are willing to sale.

Practical Aspects contd..

Corporate Debt Restructuring Strictly Private and Confidential

Corporate Debt Restructuring System

CDR Process

Lender’s Requirements

Relevant IRAC Guidelines

Preparing the Scheme

Other Practical Aspects

Exit & Recompense

CDR vs. Restructuring without CDR

• Only after the entire CDR debt is either refinanced or replaced by the existing / new lenders on fresh terms and the payment of recompense and prepayment premium is made/ settled as per CDR guidelines, the borrowers can exit from CDR.

• Criteria for exit: • The company may exit from CDR system at the end of 5 years after the

performance review. • Regular payment track record and better EBITDA for 2 consecutive years • Lenders/ borrowers may make the reference for exit after minimum 3 years in

line with CDR guidelines • Borrower-corporate seeking exit from CDR has agreed to make payment of

recompense amount as well as prepayment premium

• Above criteria can be waived and part prepayment is also possible for exit from CDR if 100% lenders approve the same.

Strictly Private and Confidential

Exit from CDR Process

Right to Recompense gets triggered on following events:

• Exit of the borrower from the CDR system.

• If average EBITDA of the borrower for 2 consecutive years is in excess of 25% of the average EBITDA of the respective years as per CDR projections

• Declaration of divided in excess of 10% on annualized basis.

• Any Capital expenditure (outside CDR package) other than modernization/ expansion necessary to sustain viability

• Extraordinary income (windfall profit) from asset sale, divestment, etc.

Strictly Private and Confidential

Recompense Clause

CDR lenders have right of recompense on sacrifices made by them.

Eligible elements for calculation of Recompense amount - Sacrifices on account of: • Amount of waiver granted to the repayment of principal/interest dues • Reduction in applicable interest rate • Reduction in commission or other charge/ fee • Reduction in rate of divided or postponement of redemption of Pref Shares. • Conversion of dues into NCDs carrying reduced interest rates/yields • Concessional interest rates for additional finances.

Ineligible elements for calculation of Recompense amount: • One time/ Negotiated settlement • Conversion of debt into equity/convertible instruments • Sacrifices and waivers prior to cut-off date • Reduction in LC/BG commission outside CDR System • Waiver of Penal interest and Liquidated damages

Strictly Private and Confidential

Recompense Clause

Strictly Private and Confidential

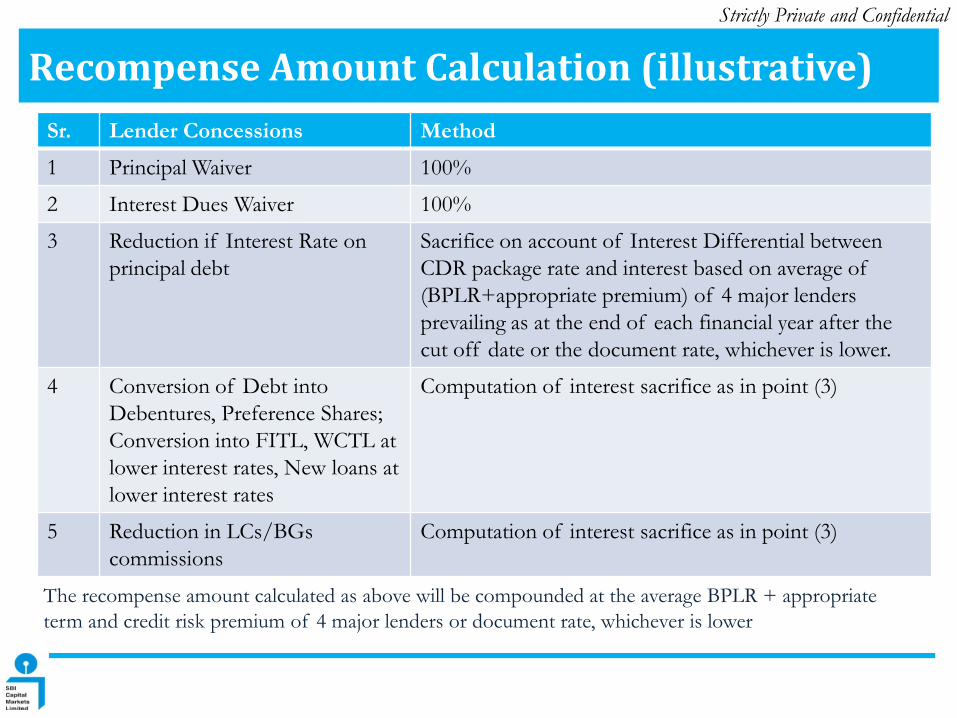

Sr. Lender Concessions Method

1 Principal Waiver 100%

2 Interest Dues Waiver 100%

3 Reduction if Interest Rate on principal debt

Sacrifice on account of Interest Differential between CDR package rate and interest based on average of (BPLR+appropriate premium) of 4 major lenders prevailing as at the end of each financial year after the cut off date or the document rate, whichever is lower.

4 Conversion of Debt into Debentures, Preference Shares; Conversion into FITL, WCTL at lower interest rates, New loans at lower interest rates

Computation of interest sacrifice as in point (3)

5 Reduction in LCs/BGs commissions

Computation of interest sacrifice as in point (3)

The recompense amount calculated as above will be compounded at the average BPLR + appropriate term and credit risk premium of 4 major lenders or document rate, whichever is lower

Recompense Amount Calculation (illustrative)

Thank You