copyright jeremy gold 2010 4(gs): financial economics - simple market ideas applied to public...

TRANSCRIPT

Copyright Jeremy Gold 2010

4(GS): Financial Economics - Simple Market Ideas Applied to Public Pension Plans

Jeremy Gold

Middle Atlantic Actuarial Club

Baltimore, MD

October 7, 2010

Jeremy Gold Pensions

2

• History

• Principles

• Implications

Outline

Jeremy Gold Pensions

3

Something for All to Hate

• Financial economics is the science of financial markets and institutions

• You can’t hate a science but you can hate its implications – and its messenger

• Implications may be negative for

– today’s taxpayers

– today’s elected officials

– employees

Jeremy Gold Pensions

4

Pop Quiz

Jeremy Gold Pensions

5

Pop Quiz

• How much does a $1000 bike cost?

Jeremy Gold Pensions

6

Pop Quiz

$1000

Jeremy Gold Pensions

7

Pop Quiz

• How much does it cost if I pay cash from my latest pay check?

Jeremy Gold Pensions

8

Pop Quiz

$1000

Jeremy Gold Pensions

9

Pop Quiz

• How much does it cost if I take money from my savings account?

Jeremy Gold Pensions

10

Pop Quiz

$1000

Jeremy Gold Pensions

11

Pop Quiz

• What if I charge it on a credit card?

Jeremy Gold Pensions

12

Pop Quiz

$1000

Jeremy Gold Pensions

13

Pop Quiz

• How much if I sell stocks?

Jeremy Gold Pensions

14

Pop Quiz

$1000

Jeremy Gold Pensions

15

The Lesson

• No matter how I finance it, the cost of a $1000 bike is $1000!

Jeremy Gold Pensions

16

Extra Credit

• How much do the following cost?

– $1000 worth of stock

– $1000 worth of bonds

Jeremy Gold Pensions

17

• History

• Principles

• Implications

Outline

Jeremy Gold Pensions

18

Financial EconomicsHistory

– major impact on financial markets in 70’s 80’s and beyond

Financial economics explodes on the financial world

– Academic genius from 1950’s to 1970’s leads to

Jeremy Gold Pensions

19

Financial EconomicsHistory

• Three major branches –

– Asset pricing/portfolio selection

• e.g., the Capital Asset Pricing Model

RiskReturn

Jeremy Gold Pensions

20

Financial EconomicsHistory

• Three major branches –

– Asset pricing

– Financial mathematics• applied to options, futures, swaps

• e.g. Black-Scholes

z

x

dxez2)(

21

)(

Jeremy Gold Pensions

21

Financial EconomicsHistory

• Three major branches –

– Asset pricing

– Financial mathematics

– Modern corporate finance

• ignored by most pension professionals including actuaries

Jeremy Gold Pensions

22

• History

• Principles

– Financial economics

– Modern finance

– Pension finance

• Implications

Outline

Jeremy Gold Pensions

23

Financial EconomicsPrinciples

– Financial economics analyzes financial systems

– All three branches rely on strong assumptions about

• Transparency

• Rationality

• Absence of arbitrage

Jeremy Gold Pensions

24

Financial EconomicsPrinciples

• Transparency– Decision makers have inexpensive

access to all pertinent information– They can see through institutional

structures to the underlying values

Jeremy Gold Pensions

25

Financial EconomicsPrinciples

• Rationality– People behave rationally in their

own interests– Transparency and rationality imply

efficiency – good decisions at low cost

Jeremy Gold Pensions

26

Financial EconomicsPrinciples

• Absence of arbitrage– No free lunches

Jeremy Gold Pensions

27

Financial EconomicsPrinciples

• We also study the limitations of rationality, transparency, arbitrage

Jeremy Gold Pensions

28

• History

• Principles

– Financial economics

– Modern finance

– Pension finance

• Implications

Outline

Jeremy Gold Pensions

29

Modern FinancePrinciples

• Financial institutions are “pass-through” entities

– Their risks and returns pass through to constituents (human beings)• Shareholders/Taxpayers

• Lenders

• Employees

• Suppliers

• Customers

• Risks and rewards are borne by these individuals– Institutions just pass the real economic impacts on to others

Jeremy Gold Pensions

30

Modern FinancePass-Throughs

Humans

Institutions

Contracts & Cash Flows

Jeremy Gold Pensions

31

Modern FinancePass-Throughs

Humans

Institutions

Contracts & Cash Flows

Jeremy Gold Pensions

32

Modern FinancePass-Throughs

Humans

Institutions

Contracts & Cash Flows

Jeremy Gold Pensions

33

Modern FinancePass-Throughs

Humans

Institutions

Contracts & Cash Flows

Jeremy Gold Pensions

34

Modern FinancePass-Throughs

• Shareholders own the corporate assets and owe the liabilities

• Taxpayers own the locality’s assets and owe the liabilities

Jeremy Gold Pensions

35

• History

• Principles

– Financial economics

– Modern finance

– Pension finance

• Implications

Outline

Jeremy Gold Pensions

36

Pension FinanceModern Finance Applied to Pension Plans

• Total employee compensation includes $ today and a contract for $ tomorrow

+

Jeremy Gold Pensions

37

Pension Finance

• Ideally the taxpayers pay for both forms of compensation today – at the same time that the employees are serving the taxpayers

+

Jeremy Gold Pensions

38

Pension Finance

• The contract is really an annuity and it could be bought today from an insurance company

Jeremy Gold Pensions

39

Pension Finance

• Taxpayers would bear little risk and would be indifferent between paying current $ and promising future pensions

Jeremy Gold Pensions

40

Pension Finance

• And if each generation of taxpayers paid for the annuities as they were promised, current and future taxpayers would be in balance too

Jeremy Gold Pensions

41

Pension Finance

• The owners of the insurance company would be taking some mortality risk and some investment risk

• And would expect a profit in return

Jeremy Gold Pensions

42

Pension Finance

• But the insurer would not recognize the profit immediately

• Profits would emerge if and when the risks were gone

Jeremy Gold Pensions

43

Pension Finance

• Remember the $1000 bicycle? How much does a $100,000 annuity cost?

$1000 $100,000

Jeremy Gold Pensions

44

Pension Finance

• Instead of buying the annuity, the taxpayers could run their own insurance company

Jeremy Gold Pensions

45

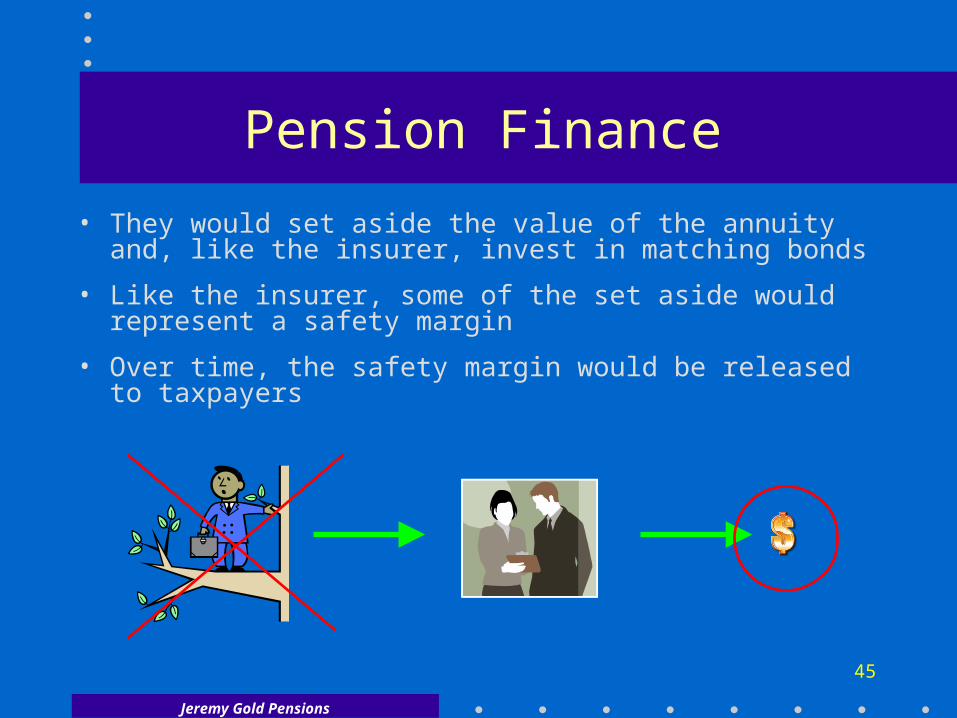

Pension Finance

• They would set aside the value of the annuity and, like the insurer, invest in matching bonds

• Like the insurer, some of the set aside would represent a safety margin

• Over time, the safety margin would be released to taxpayers

Jeremy Gold Pensions

46

Pension Finance

• But the release would go to future taxpayers

• It is the future taxpayers who really bear the risk

• If the investment or mortality experience goes badly, they will have to pay

Jeremy Gold Pensions

47

Pension Finance

• Financial economists would say:

– today’s taxpayers were buying annuities

– tomorrow’s taxpayers were selling annuities

Jeremy Gold Pensions

48

Pension Finance

• Financial economists would say:

– The rewards for taking the risks belong to the future taxpayers

Jeremy Gold Pensions

49

Pension Finance

• Over time the taxpayer’s do-it-yourself insurance company will build up a lot of bond assets that won’t be needed for a long time

Jeremy Gold Pensions

50

Pension Finance

• And someone will say:

– We are long-term investors

– Stocks usually beat bonds over the long term

– Why don’t we put some of our money in stocks?

Jeremy Gold Pensions

51

Pension Finance

• Until that moment

– Taxpayers were running an insurance business with as little risk as possible

– Now they are upping their bets

Jeremy Gold Pensions

52

Pension Finance

• Compared to the insurance company

– They are selling bonds and

– Buying stocks

Jeremy Gold Pensions

53

Pension Finance

• Financial economists say that selling bonds is the same as borrowing

– More money today

– Less money tomorrow

Jeremy Gold Pensions

54

Pension Finance

• So the taxpayer insurance company is borrowing to invest in stocks

– Buying on margin

– We know that buying on margin is risky

– Who is bearing that risk?

– Same as before – future taxpayers

Jeremy Gold Pensions

55

Pension Finance

• Who should get the rewards?

Jeremy Gold Pensions

56

Pension Finance

• When?– After the risks have been taken

Jeremy Gold Pensions

57

• History

• Principles

– Financial economics

– Modern finance

– Pension finance

• Implications

Outline

Jeremy Gold Pensions

58

Implications

• How does the present system work?

– Under today’s rules

• Actuaries and accountants are required to front load the rewards from taking risk

• Before the risks are taken

– $100,000 annuity is marked down to $70,000

Jeremy Gold Pensions

59

Implications

• Future taxpayers should complain

– They take the risk

– Today’s taxpayers take the rewards

• For crying out loud!

Jeremy Gold Pensions

60

Implications

• Who speaks for future taxpayers

– I do

– And so we’ve come full circle

• Now we know why you may all want to hate me

Jeremy Gold Pensions

61

Implications

• Who should hate me first?

– Today’s taxpayers because

• I am saying you should pay more today for the promises you are making

• You cannot take the rewards when your children are taking the risks

Jeremy Gold Pensions

62

Implications

• Who should hate me first?

– Today’s elected officials because

• You will have to give the bad news to your taxpayers

Jeremy Gold Pensions

63

Implications

• Who should hate me first?

– Employees because

• Once taxpayers and elected officials realize how much those annuities really cost

• They will have to promise smaller benefits

Jeremy Gold Pensions

64

Implications

• For today’s taxpayers and elected officials

– Financial economics looks like a bogeyman

• For tomorrow’s taxpayers

– Today’s practice is the bogeyman and

– Financial economics is the benefactor

Jeremy Gold Pensions

65

Implications

For crying out loud!

Jeremy Gold Pensions

66

Restricted Usage

• Copyright Jeremy Gold 2010

• Please note that this document is not publicly available; it is available to attendees at the October 7, 2010 MAAC Conference. It may be shared with others in your organization on an educational basis. It may not be used for commercial purposes or shared outside your firm without permission.

• If you wish to use it for another purpose, please contact Jeremy Gold [email protected].

Copyright Jeremy Gold 2010

4(GS): Financial Economics - Simple Market Ideas Applied to Public Pension Plans

Jeremy Gold

Middle Atlantic Actuarial Club

Baltimore, MD

October 7, 2010