copyright © 2014 pearson education, inc. publishing as prentice hall 15 - 1

TRANSCRIPT

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 1

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 2

Chapter 15

Basic Accounting: Concepts, Techniques,

and Conventions

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 3

Chapter 15 Learning Objectives

1. Read and interpret basic financial statements.

2. Analyze typical business transactions using the balance sheet equation.

3. Distinguish between the accrual basis of accounting and the cash basis of accounting.

4. Make adjustments to the accounts under accrual accounting.

5. Explain the nature of dividends and retained earnings.

6. Select relevant items from a set of data and assemble them into a balance sheet and an income statement.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 4

7. Distinguish between the reporting of corporate owners’ equity and the reporting of owners’ equity for partnerships and sole proprietorships.

8. Explain the role of auditors in financial reporting and how accounting standards are set.

9. Identify how the measurement principles of recognition, matching and cost recovery, and stable monetary unit affect financial reporting.

10. Define continuity, relevance, faithful representation, materiality, conservatism, and cost benefit (Appendix 15A).

11. Use T-accounts, debits, and credits to record transactions (Appendix 15B).

Chapter 15 Learning Objectives

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 5

The Need for Accounting

Accounting information can be used to assess past financial performance of a company and help predict its future performance. All kinds of organizations—government agencies, nonprofit organizations, and others —rely on accounting to gauge their progress.

The accounting process begins with a transaction.A transaction is any event that affects the financial position of an organization and requires recording.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 6

The Need for Accounting

Many concepts, conventions, and rules determine what events a company records as accounting transactions and how accountants measure the financial impact of each transaction.

Financial statements are used to summarize the recorded accounting transactions.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 7

The Need for Accounting

Managers, investors, and other internal groupswant the answers to two important questions:

How well didthe organization

perform? Where doesthe organization

stand?

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 8

The Need for Accounting

Accountants answer these questionswith three major financial statements:

Incomestatement

Balancesheet

Statement ofcash flows

Learning Objective 1

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 9

Balance Sheet

The balance sheet (also called statement of financial position or statement of financial condition) is a snapshot of the financial status of an organization at a point in time.

The balance sheet has two sections(1) assets and (2) liabilities plus owners’ (stockholders’) equity.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 10

Balance Sheet

Assets are economic resources thatare expected to benefit futureactivities of the organization.

Liabilities are the entity’s economicobligations to nonowners.

Owners’ equity is the excessof the assets over the liabilities.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 11

Balance Sheet

Stockholders’ equity

The owners’ equity of a corporationis called stockholders’ equity.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 12

King Hardware TransactionsAn Example

Learning Objective 2

King Hardware Company began business as a corporation—a business organized as a separate legal entity and owned by its stockholders. The company’s first transaction occurred on February 28, 20X1, when its stockholders invested a total of $100,000 cash.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 13

King Hardware Transactions

The following additional transactions occurred during March:

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 14

144,000 144,000

King Hardware Transactions

=Transactions Cash + Accounts + Inventory + Prepaid = Accounts + Paid-in + Retained

Receivable Rent Payable Capital Earnings1 100,000 + + + = + 100,000 +2 (75,000) + + 75,000 + = + +3 + + 35,000 + = 35,000 + +4a 10,000 + 120,000 + + = + + 130,000 Revenue4b + + (100,000) + = + + (100,000) Expense5 15,000 + (15,000) + + = + +6 (20,000) + + + = (20,000) + +7a (3,000) + + + 3,000 = + +7b + + + (1,000) = + + (1,000) Rent Expense

Balance 27,000 + 105,000 + 10,000 + 2,000 = 15,000 + 100,000 + 29,000

Assets Liabilities + Owners' Equity

Analysis of Transactions (in dollars) for March

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 15

Balance Sheet

The balance sheet for King Hardware

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 16

Revenues and Expenses

Revenues are increases in ownershipclaims arising from the delivery

of goods or services.

Recognize revenue by formally recording it in the accounting records during the current period only after it meets two tests:

1.The company must earn the revenues. That is, it must deliver the goods or render the services to customers. 2.The revenue must be realized or realizable.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 17

Revenues and Expenses

Expenses are decreases in ownershipclaims (stockholders’ equity) arising from

delivering goods or services or using up assets.

Income (also called net income, profits, or earnings), is the excess of revenues over expenses. It increases stockholders’ equity.

An income statement summarizes revenues and expenses. It measures an organization’s performance by matching its revenue and its expenses for a span of time, often a month, a quarter, or a year.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 18

Relationship Between Balance Sheet and Income Statement

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 19

Income Statement

The income statement shows that General Mills’ stockholders’ equity (retained earnings) increased by $1,804 million because of profitable operations in the year ended May 29, 2011. This $1,804 million is included in the $6,612 million of stockholders’ equity on the May 29, 2011, balance sheet.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 20

The Analytical Power of theBalance Sheet Equation

The balance sheet equation can highlight the linkbetween the income statement and balance sheet.

Assets (A) = Liabilities (L) + Stockholders’ equity (SE)

A = L + Paid-in capital + Retained income

A = L + Paid-in capital + Revenue – Expenses

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 21

Accrual Basis and Cash Basis

The accrual basis of accountingrecognizes revenues and expenses

when they occur regardless of whencash is received or disbursed.

The cash basis of accounting recognizesrevenue and expense when cash is

received and disbursed.

Learning Objective 3

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 22

Accrual Basis and Cash Basis

The major deficiency of the cash basis of accounting is that it is incomplete.

It fails to match efforts and accomplishmentsin a manner that properly measures economic

performance and financial position.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 23

Nonprofit Organizations

Nonprofit organizations, such as government agencies and charitable organizations, also use balance sheets and income statements.

For years, most nonprofit organizations used cash-basis rather than accrual accounting.

As these organizations face more pressure to develop accurate measures of performance, they are increasingly using accrual accounting.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 24

Nonprofit Organizations

The basic concepts of assets, liabilities, revenues, and expenses apply to all organizations, whatever their goals and wherever they are located. However, organizations that do not seek profits do not measure income. Further, because they have no owners, there is no owners’ equity.

Balance sheets of nonprofit organizations show a category of “net assets” instead of “owners’ equity” To measure the difference between assets and liabilities. Instead of an income statement, nonprofitorganizations have a “statement of activities” that reports changes in net assets.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 25

Adjustments to the Accounts

Under the accrual basis of accounting, record:1.Explicit transactions-day-to-day routine events 2.Implicit transactions - events that day-to-day

recording procedures temporarily ignore, such as expiration of prepaid rent or accrual of interest

due to the passage of time.

Explicit transactions are easy to identify because they are supported by source documents.

Implicit transactions are recorded at the end of each accounting period by using adjusting entries.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 26

Principal Adjustments

Expiration of unexpired costs

Recognition (earning) of unearned revenues

Accrual of unrecorded expenses

Accrual of unrecorded revenues

Four types of principal adjustments:

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 27

Adjustment Type I: Expiration of Unexpired Costs

Assets other than cash and receivables are viewed as economic services awaiting future use—prepaid or stored costs, and they are carried forward to future periods. The values of assets frequently decline (and eventually disappear) because of the passage of time.

When a company uses services represented by a particular cost, the cost expires. An unexpired cost is any asset that managers expect to become an expense in future periods.

Learning Objective 4

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 28

Adjustment Type I: Expiration of Unexpired Costs

Rather than immediately charge these costs as expenses, they are charged as expenses in future periods when the services are used.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 29

Expiration of Unexpired Costs

Assets other than cash and receivables are viewed as economic services

awaiting future use.

Assets frequently expire because of the passage of time.

Unexpired costs are assets that managers expect to become expenses in future

accounting periods.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 30

Depreciation

To account for long-lived assets, assets that will provide services for more than one year:

(2) predict the residual value

(1) predict the length of the asset’s useful life

(3) allocate the cost of the equipment to the years of its useful life in a systematic way.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 31

Adjustment Type II:Unearned Revenue (Deferred Revenue)

Unearned Revenue (deferred revenue) is . . .

Because customers have already paid in advance for merchandise or services . . .

A liability recorded when a company receive collections from customers

before it earns the revenue.

An obligation exists to deliver merchandise or service or refund the customers’ deposits

if the goods or services are not delivered.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 32

Adjustment Type III:Accrual of Unrecorded Expenses

Employee wages

Accrue means to accumulate a receivable or payable during a given

period, even though no explicit transaction occurs.

Interest expense

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 33

Adjustment Type IV:Accrual of Unrecorded Revenues

The recognition of revenues that a company has earned but has not

yet recorded in its accounts is

Interest Revenue

. . . the mirror image of the accrualof unrecorded expenses.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 34

Adjustment Type IV:Accrual of Unrecorded Revenues

Summary of accruals of expenses and revenues (in the columns) and the timing of the accrual compared to the cash flows (in the rows).

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 35

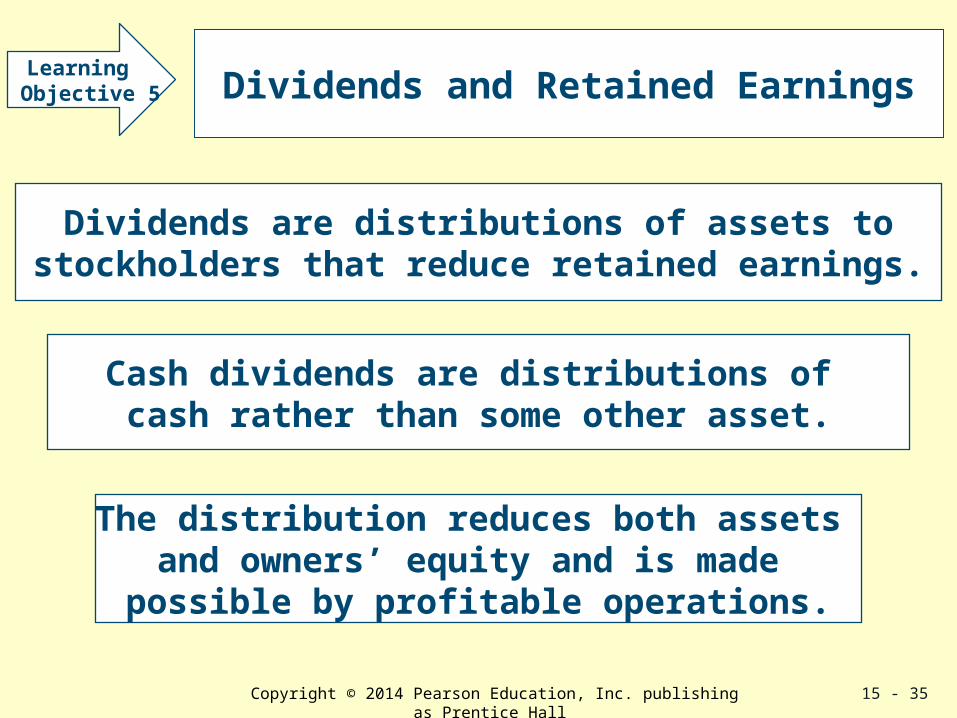

Dividends and Retained Earnings

Dividends are distributions of assets tostockholders that reduce retained earnings.

Cash dividends are distributions of cash rather than some other asset.

The distribution reduces both assets and owners’ equity and is made possible by profitable operations.

Learning Objective 5

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 36

Dividends and Retained Earnings

Dividends reduce retained earnings, But they are not expenses.

Companies do not deduct dividends from revenues when measuring income because they

do not help generate sales or conduct operations.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 37

Retained Earnings

Retained earnings and paid-in capital result from profitable operations. Equity is not a pot of cash awaiting distribution to stockholders.

Stockholders’ equity represents the claims of owners arising out of their initial investment (paid-in capital) and subsequent profitableoperations (retained earnings).

Retained earnings and paid-in capital represent a general claim against, or undivided interest in, total assets, not a specific claim against any asset.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 38

Retained Earnings

Retained earnings and paid-in capital result from profitable operations. Equity is not a pot of cash awaiting distribution to stockholders.

Do not confuse retained earnings and cash. Cash can increase while retained earnings decreases, and vice versa. There is no direct relationship between retained earnings and available cash.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 39

King Hardware Company

Select relevant items from a set of data and assemble them into a balance sheet and an income statement.

Learning Objective 6

The balance sheet uses totals from the asset, liability, and stockholders’ equity columns.

The income statement uses the revenue and expense entries in the retained earnings column.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 40

Balance Sheet

King Hardware CompanyBalance Sheet as of April 30, 20X1

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 41

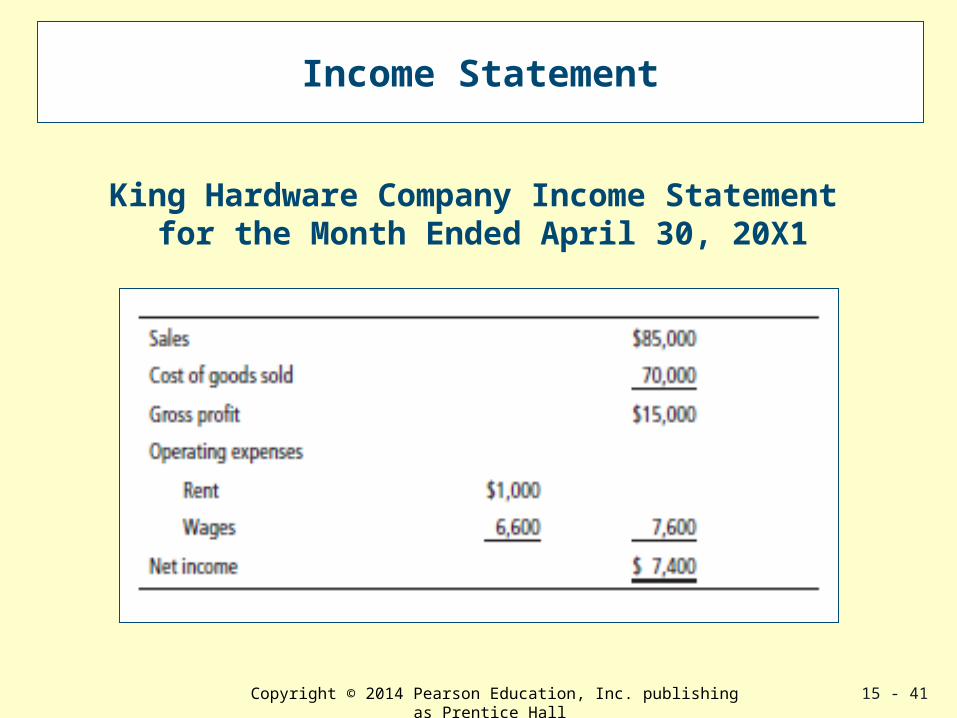

Income Statement

King Hardware Company Income Statement for the Month Ended April 30, 20X1

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 42

Changes in Retained Earnings

King Hardware Company Changes in Retained Earnings for the Month Ended April 30, 20X1

This statement shows the linkage between the balance sheet and income statement. It starts with the beginning balance, adds net income for April, and deducts cash dividends, to arrive at an ending balance.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 43

Sole Proprietorships andPartnerships

A sole proprietorship is a businessentity with a single owner.

A partnership is an organizationthat joins two or more individuals

together as co-owners.

LearningObjective 7

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 44

Comparison of Owners’ Equity Reporting

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 45

Comparison of Owners’ Equity Reporting

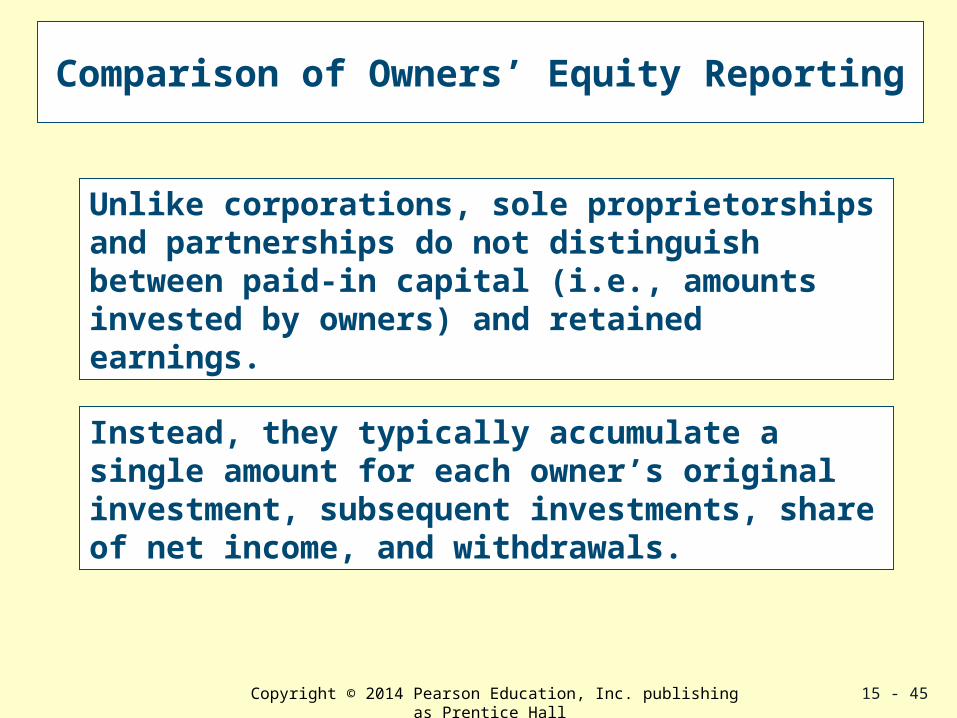

Unlike corporations, sole proprietorships and partnerships do not distinguish between paid-in capital (i.e., amounts invested by owners) and retained earnings.

Instead, they typically accumulate a single amount for each owner’s original investment, subsequent investments, share of net income, and withdrawals.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 46

Generally Accepted Accounting Principles (GAAP)

Accounting is based on a set of principleson which there is general agreement,

not on rules that can be “proved.”

LearningObjective 8

The principles and procedures that together make up accepted accounting practice at any given time are known as generally accepted accounting principles (GAAP).

Accounting is more an art than a science. It is commonly misunderstood as being a precise discipline that produces exact measurements

of a company’s financial position and performance.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 47

Audit

An audit is an “examination” or in-depth inspection of financial statements and companies’

records that is made in accordance withgenerally accepted auditing standards.

Auditing standards are approved by the Public Company Accounting Oversight Board (PCAOB) which is a part of the Securities and Exchange Commission (SEC), a government agency that

regulates the financial markets in the U.S. including financial reporting.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 48

Accounting Standard Setters

The Financial Accounting Standards Board(FASB) is the primary regulatory body over

accounting principles and practices in the U.S.

The FASB consists of seven full-time members plus a staff of nearly 60 members, and it is

an independent creation of the private sector.

The IASB is a similar independent organization whose pronouncements, called International Financial Reporting Standards (IFRS) define

GAAP in more than 100 other countries.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 49

Accounting Standard Setters

In 2008 the SEC started accepting financialstatements based on IFRS for non-U.S.

Companies whose stock is traded in U.S. capital markets.

It defined a “road-map” for eventual adoption of IFRS by U.S. companies as well.

the FASB and IASB are currently workingon converging their separate standards into

one set of world-wide standards.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 50

Accounting Standard Setters

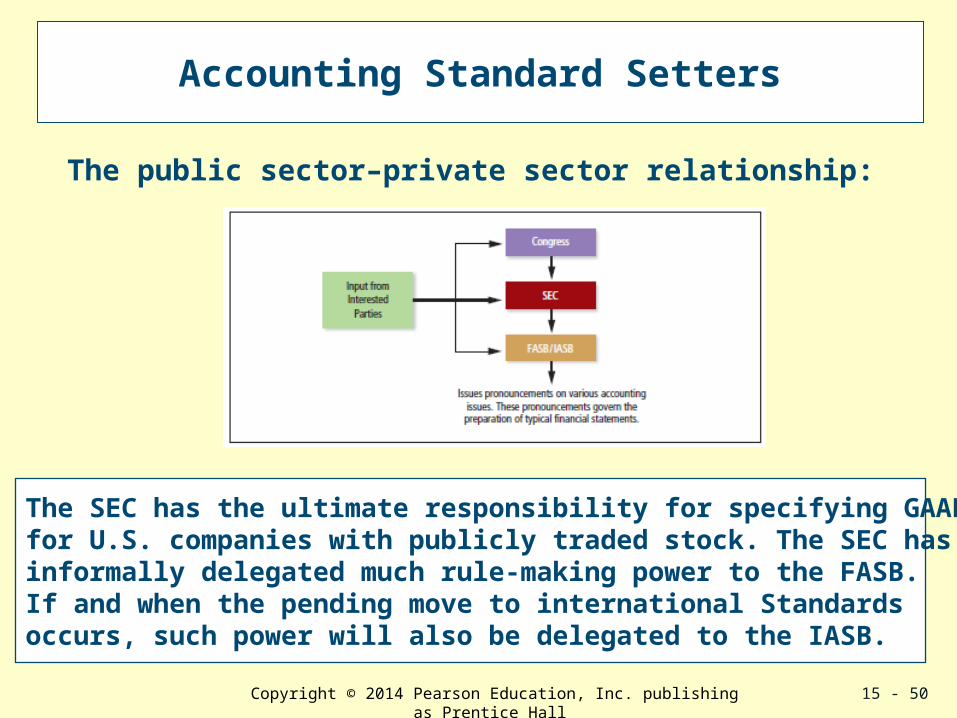

The SEC has the ultimate responsibility for specifying GAAPfor U.S. companies with publicly traded stock. The SEC has informally delegated much rule-making power to the FASB. If and when the pending move to international Standardsoccurs, such power will also be delegated to the IASB.

The public sector–private sector relationship:

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 51

Ethics

A hallmark of the accounting profession has been its ethics and integrity. Most accountants and auditors are highly ethical and truthfully report their financial results in accordance with GAAP.

The public sector–private sector relationship:

Confidence in financial information is important to the smooth functioning of the world’s capital markets, and confidence in financial statements depends on the competence and integrity of accountants and auditors.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 52

Three Measurement Conventions

U. S. GAAP is based on aconceptual framework that contains three broad measurement or valuation conventions (principles) thatunderlie accrual accounting:

Recognition

Matching andcost recovery

Stablemonetary unit

LearningObjective 9

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 53

Recognition Principle

The recognition principle specifies when a company should record revenue in the

accounting records.

Generally, companies recognize revenue when it is both earned and realized or realizable.

In some industries revenue recognition is not so straightforward. These judgment issues require company accountants together with its auditor to decide when earning and realization are sufficiently complete to recognize the revenue.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 54

Matching and Cost Recovery

The timing of revenue recognition is important because it leads to the recording of expenses through the concept of matching—the linking of revenues with expenses incurred to generate them.

Accountants apply matching as follows:1. Identify the revenue recognized during the period.2. Record expenses that relate directly to the recognized revenue.3. Record expenses that are costs of operations duringa specific time period that have no measurable benefit for a future period and must be linked to the current period’s revenues.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 55

Matching and Cost Recovery

The heart of recognizing expense is the cost recovery concept. Companies carry forwardas assets such items as inventories, prepayments, and equipment because they expect to recover the costs of these assets in the form of cash inflows (or reduced cash outflows) in future periods.

At the end of each period, accountants examine evidence to assure themselves that they should not write off these assets—the unexpired costs—as an expense of the current period.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 56

Stable Monetary Unit

The monetary unit (for example, the dollar in the United States, the yen in Japan, or the euro in the European Union) is the principal means for measuring assets, liabilities, and stockholders’ equity.

This measurement assumes that the monetary unit—the dollar, for example—is an unchanging yardstick. Yet, a 2010 dollar does not have the same purchasing power as a 2000 or 1990 dollar. Therefore, users of accounting statements that include dollars from different years must recognize the limitations of the basic measurement unit.

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 57

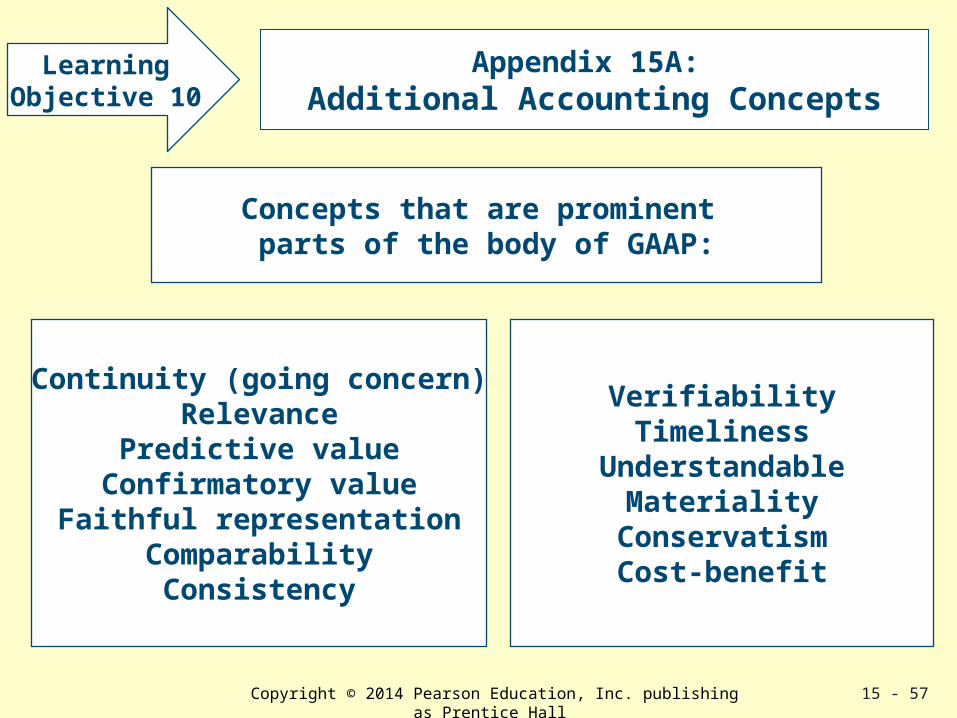

Appendix 15A: Additional Accounting Concepts

Concepts that are prominent parts of the body of GAAP:

Continuity (going concern) Relevance

Predictive valueConfirmatory value

Faithful representationComparabilityConsistency

LearningObjective 10

VerifiabilityTimeliness

UnderstandableMateriality

ConservatismCost-benefit

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 58

Appendix 15B: Using Ledger Accounts

Some techniques that accountants use to record transactions.

T-Accounts Ledger Accounts

Double-Entry SystemDebits and Credits

Learning Objective 11

Copyright © 2014 Pearson Education, Inc. publishing as Prentice Hall

15 - 59

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of the publisher. Printed in the United States of America.