copyright © 2006 pearson addison-wesley. all rights reserved. lecture 12: joint hypothesis tests...

Post on 18-Dec-2015

216 views

TRANSCRIPT

Copyright © 2006 Pearson Addison-Wesley. All rights reserved.

Lecture 12: Joint Hypothesis Tests

(Chapter 9.1–9.3, 9.5–9.6)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-2

Today’s Agenda

• Review

• Joint Hypotheses (Chapter 9.1)

• F-tests (Chapter 9.2–9.3)

• Applications of F-tests (Chapter 9.5–9.6)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-3

Review

• Perfect multicollinearity occurs when 2 or more of your explanators are jointly perfectly correlated.

• That is, you can write one of your explanators as a linear function of other explanators:

X1 aX2 bX3

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-4

Review (cont.)

• OLS breaks down with perfect multicollinearity (and standard errors blow up with near perfect multicollinearity).

• Multicollinearity most frequently occurs when you want to include:

– Time, age, and birth year effects

– A dummy variable for each category, plus a constant

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-5

Review (cont.)

• Dummy variables (also called binary variables) take on only the values 0 or 1.

• Dummy variables let you estimate separate intercepts and slopes for different groups.

• To avoid multicollinearity while including a constant, you need to omit the dummy variable for one group (e.g. males or non-Hispanic whites). You want to pick one of the larger groups to omit.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-6

0 1 2 1 2 3

0

0 1

0 2

_1 _ 2 _1 _ 2

_1

_ 2

is the intercept for the omitted category.

is the intercept for the category coded by .

is the intercept for the category coded by .

i i i i i i i i iY D D X X D X D

D

D

0 1

1

1 2

1

_1

: 0.

_1

You can test whether group has the same intercept

as the omitted group by testing

is the slope for the omitted category.

is the slope for the category coded by .

D

H

D

3

0 2

_ 2

_1

: 0.

is the slope for the category coded by .

You can test whether group has the same slope

as the omitted group by testing

D

D

H

Review (cont.)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-7

Review (cont.)

• You can multiply 2 variables together to create interaction terms.

• Interaction terms let the slope of each variable depend on the value of the other variable.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-8

Review (cont.)

0 1 1 2 2 3 1 2

1 3 21

i i i i i i

ii

i

Y X X X X

YX

X

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-9

Review (cont.)

• With many of the specifications covered last time, we encountered hypotheses that required us to test multiple conditions simultaneously. For example, to test:

– All categories have the same intercept (with 3 or more categories)

– All categories have the same slope (with 3 or more categories)

– One explanator has no effect on Y, when that explanator has been used in an interaction term

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-10

Review (cont.)

• In economics, many processes are non-linear. Economic theory relies heavily on diminishing marginal returns, decreasing returns to scale, etc.

• We want a specification that lets the 50th unit of X have a different marginal effect than the 1st unit of X.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-11

Review (cont.)

• If we regress not

but rather

then the marginal benefit of a unit of X changes to:

0 1i i iY X

20 1 2i i i iY X X

Y

X

12

2

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-12

Yi

0

1X

i

2X

i2

i

Y

X

12

2

Review (cont.)

• If 2 > 0, then the marginal impact of X is increasing. If 2 = 0, then X has a constant marginal effect. If 2 < 0, then the marginal impact of X is decreasing.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-13

Review (cont.)

• If 2 > 0 and 3 < 0, then this equation traces an inverse parabola.

• Earnings increases quickly in experience at first, but then flattens out.

log(earnings)i

0

1Ed

i

2Exp

i

3Exp

i2

i

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-14

Joint Hypotheses (Chapter 9.1)

log(earnings)i

0

1Ed

i

2Exp

i

3Exp

i2

i

• To test the hypothesis that experience is not an explanator of log(earnings), you need to test

• WARNING: you CANNOT simply look individually at the t-test for 2 = 0 and the t-test for 3 = 0

H0:

20 AND

30

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-15

Joint Hypotheses (cont.)

• You CANNOT test a JOINT hypothesis by combining multiple t-tests.

• Suppose you are testing

• A t-test rejects 1 = 0 if the data would be very surprising to see, given that 1 = 0. A t-test does NOT reject 1 = 0 if the data would only be pretty surprising.

H0:

10 AND

20

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-16

Joint Hypotheses (cont.)

• Each t-test could fail to reject the null if the data would only be “pretty surprising” under each null, taken one at a time.

• However, it might be “very surprising” to see two “pretty surprising” events.

• We do not know the “size” of a joint test conducted by stacking together many t-tests.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-17

Joint Hypotheses (cont.)

• Another problem with t-tests: suppose X1 and X2 are heavily correlated with each other (though not so much as to create perfect multicollinearity). Then each coefficient will have a large standard error.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-18

Joint Hypotheses (cont.)

• Another problem with t-tests: suppose X1 and X2 are heavily correlated with each other.

• If you remove either variable—leaving in the other—then you lose very little explanatory power. The other variable simply picks up the slack (through the omitted variables bias formula).

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-19

Joint Hypotheses (cont.)

• However, to test the null hypotheses that neither variable has explanatory power, we want to consider removing both variables at the same time. The two of them together may share a lot of explanatory power, even if either one could do the job nearly as well as both together.

• We need a new type of test, that lets us consider multiple hypotheses at once.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-20

Joint Hypotheses (cont.)

• Simply including more than one coefficient in the hypothesis does NOT make a joint hypothesis. For example, suppose you believed that X1 and X2 had identical effects. You could test this claim with:

• This test is a single hypotheses, and can be tested using a t-test. The calculation requires you to know the covariance of the two coefficients. See Chapter 7.5.

H0 : 1 2

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-21

Joint Hypothesis (cont.)

• A joint hypothesis tests more than one condition simultaneously. The easiest way to see how many conditions are being tested is to count the number of equal signs.

• E.g. H0 : 1 = 0 AND 2 = 0 has two equal signs, so there are two conditions being tested. This is a joint test.

• This hypothesis is often written 1 2 0

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-22

F-tests (Chapter 9.2–9.3)

• How can we test multiple conditions simultaneously?

• Intuition: run a regression normally, and then also run a regression where you assume the conditions are true. See if imposing the conditions makes a big difference.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-23

F-tests (cont.)

log(earnings)i

0

1Ed

i

2Exp

i

3Exp

i2

i

20 1

0 1

log( ) 0 0i i i i i

i i

earnings Ed Exp Exp

Ed

• To test the hypothesis that experience is not an explanator of log(earnings), you need to test H0 : 2 = 0 AND 3 = 0

• If these conditions are true, then there should be little difference between our “unrestricted” regression and the “restricted” version:

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-24

F-tests (cont.)

• If the conditions we are testing are true, then there should be little difference between our “unrestricted” regression and the “restricted” version.

• What do we mean by “little difference”?

• Does imposing the restrictions we wish to test greatly affect the model’s ability to fit the data?

• We can turn to our measure of fit, R2

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-25

F-tests (cont.)

• To measure the difference in the quality of fit before and after we impose the restrictions we are testing, we can turn to our measure of fit, R2

• Notice that the Total Sum of Squares is the same for both versions of the regression, so we can focus on the Sum of Squares of the Residuals.

20 12

2

ˆ ˆ( )1 1

( )

Y X SSRR

TSSY Y

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-26

F-tests (cont.)

• Does imposing the restrictions from our null hypothesis greatly increase the SSR ? (Remember, we want a low SSR.)

• Run both regressions and calculate the SSR.

• Call the SSR for the unrestricted version the SSRu

• Call the SSR for the restricted version the SSRr

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-27

F-tests (cont.)

• Call the SSR for the unconstrained version the SSRu

• Call the SSR for the constrained version the SSRc

• If the null hypothesis (2 = 3 = 0) is true, then imposing the restrictions will not change the SSR much. We will have a “small” SSRc-SSRu

2 20 1 2 3

ˆ ˆ ˆ ˆ(log( ) )ui i i iSSR earnings Ed Exp Exp

20 1ˆ ˆ(log( ) )c

i iSSR earnings Ed

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-28

F-tests (cont.)

• If the null hypothesis is true, then imposing the restrictions will not change the SSR much. We will have a “small” SSRc-SSRu

• Remember, OLS finds the smallest possible SSR. So SSRc > SSRu

• The more restrictions we impose, the larger SSRc will get, even if the restrictions are true.

• We need to adjust for the number of restrictions (r) we impose.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-29

F-tests (cont.)

• To measure how large an effect our constraints have, look at:

• What constitutes a large difference? We want to compare the difference in SSR to the original SSRu. An increase of 100 units is more worrisome if we start from SSRu = 200 than if SSRu = 20,000.

c uSSR SSR

r

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-30

F-tests (cont.)

• The more data we have, the more we trust our unconstrained regression.

• Also, the more data we have, the more seriously we want to take a deterioration in SSR.

• To capture the effect of more data, we weight by n-k-1.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-31

F-tests (cont.)

( 1)

c u

u

SSR SSRrF

SSRn k

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-32

F-tests (cont.)

• When the i are distributed normally, the F-statistic will be distributed according to the F-distribution with r, n-k-1 degrees of freedom.

• We know how to compute an F-statistic from the data.

• We know the distribution of the F-statistic under the null hypothesis.

• The F-statistic meets all the needs of a test statistic.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-33

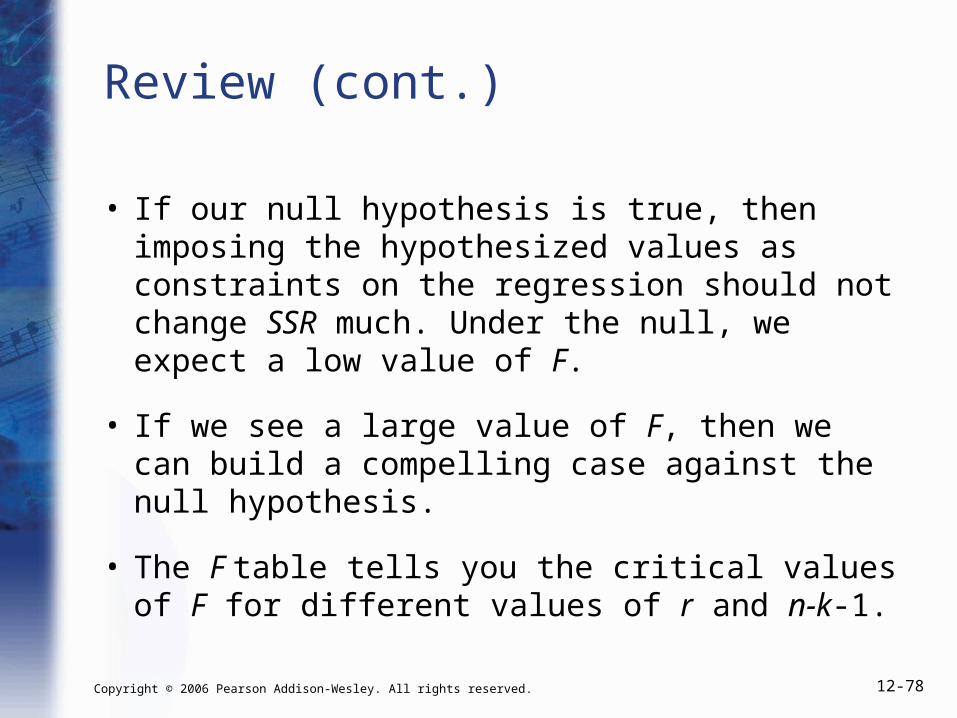

F-tests (cont.)

• If our null hypothesis is true, then imposing the hypothesized values as constraints on the regression should not change SSR much. Under the null, we expect a low value of F.

• If we see a large value of F, then we can build a compelling case against the null hypothesis.

• The F-table tells you the critical values of F for different values of r and n-k-1.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-34

F-tests (cont.)

log(earnings)i

0

1Ed

i

2Exp

i

3Exp

i2

i

• Let’s return to the earnings test example, with the polynomial specification

• To test the hypothesis that experience is not an explanator of log(earnings), you need to test H0

: 20 AND

30

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-35

F-tests (cont.)

H0

: 2

30

r 2; n - k -16540 - 3-16536

Unconstrained Regression:

log(earnings)i

0

1Ed

i

2Exp

i

3Exp

i2

i

SSRu 3844

Constrained Regression:

log(earnings)i

0

1Ed

i v

i

SSRc 3959

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-36

F-tests (cont.)

H0

: 2

30

F

SSRc SSRu

rSSRu

n k 1

3959 3844

23844

6536

97.77

The 5% critical value for F2,6536

is 3. We can reject the

null hypothesis that experience is not an explanator

of log(income).

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-37

F-tests (cont.)

• Note: we must be able to impose the restrictions as part of an OLS estimation. We can impose only linear restrictions.

• For example, we CAN test:

314

1

2

30

14

2 and

3- 3

45

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-38

F-tests (cont.)

• However, we CANNOT test:

1·2 3

1 23

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-39

F-tests (cont.)

• Example:

• There are two equal signs. r = 2.

• How do we impose the restrictions?

• How do we enter this regression into the computer?

Y 0

1X

1

2X

2

3X

3

4X

4

5X

5

H0

: 14

2 and

3- 3

4

5

Y 0 (42 )X1 2 X2 3X3 4 X4 (3 - 34 )X5

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-40

F-tests (cont.)

• To enter a regression into the computer, we need to regroup so that all our explanators receive a single coefficient apiece.

• We need to transform this expression from one with separated explanators and linear combinations of coefficients to one with separated coefficients and linear combinations of explanators.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-41

F-tests (cont.)

• To find the constrained sum of squares, we need to regress Y on a constant, (4X1+X2), (X3+X5), and (X4 -3X5). The SSR from this regression is our SSRc.

Y 0 (42 )X1 2 X2 3X3 4 X4 (3 - 34 )X5 Y 0 2 (4X1 X2 )3(X3 X5 )4 (X4 - 3X5 )

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-42

Y 0 1X1 2 X2

H0 :1 -2

Checking Understanding

• You regress

• You want to test

• What are the constrained and unconstrained regressions? What is r ?

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-43

Checking Understanding (cont.)

Y 0

1X

1

2X

2

H0

: 1-

2

Unconstrained regression:

Y 0

1X

1

2X

2

Constrained regression:

Y 0 (-

2)X

1

2X

2

0

2( X

2- X

1)

r 1

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-44

F-tests

• Note: when r = 1, you have a choice between using a t-test or an F-test.

• When r = 1, F = |t|2. F-tests and t-tests will give the same results.

• When r > 1, you cannot use a t-test.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-45

F-tests (cont.)

• A frequently encountered test is the null hypothesis that all the coefficients (except the constant) are 0. This test asks whether the entire model is useless. Do our explanators do a better job at predicting Y than simply guessing the mean?

• Many econometrics programs automatically calculate this F-statistic when they perform a regression.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-46

log(earnings)i

0

1Ed

i

2Exp

i

3D _ F

i

i

An Application of F-tests (Chapter 9.5)

• Let’s use F-tests to re-examine the differences in earnings equations between black women and black men in the NLSY.

• Regress the following for black workers:

• where Edi = years of education, Expi = years of experience, and D_Fi = 1 if the worker is female

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-47

An Application of F-tests (cont.)

• To test whether black males and black females have the same intercept, we can use a simple t-test with H0 : 3 = 0

• Our estimated coefficient is -0.201 with a standard error of 0.036, yielding a t-statistic of -5.566

• This t-statistic exceeds our critical value of -1.96

• We can reject the null hypothesis at the 5% level

log(earnings)i

0

1Ed

i

2Exp

i

3D _ F

i

i

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-48

TABLE 9.1 Earnings Equation for Black Men and Women (NLSY Data)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-49

An Application of F-tests (cont.)

• We have rejected the null hypothesis that black men and black women have the same intercept.

• Could they also have different slopes for education and experience?

• We can use dummy variable interaction terms.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-50

0 1 2 3

4 5

0 1 2

0

log( ) _

_ _

( _ 0) :

log( )

( _ 1) :

log( ) (

Case: worker is male

Case: worker is female

i i i i

i i i i i

i

i i i i

i

i

earnings Ed Exp D F

Ed D F Exp D F

D F

earnings Ed Exp

D F

earnings

3 1 4 2 5) ( ) ( )i i iEd Exp

0 3 4 5: 0H

An Application of F-tests (cont.)

• To test the null hypothesis that black men and black women have identical earnings equations, we need to test the joint hypothesis:

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-51

An Application of F-tests (cont.)

0 3 4 5

0 1 2 3

4 5

0 1

: 0

log( ) _

_ _

1002.75

log( )

Unconstrained Regression:

Constrained Regression:

i i i i

i i i i i

u

i i

H

earnings Ed Exp D F

Ed D F Exp D F

SSR

earnings Ed

2

1020.378

3, 1 1795

i i

c

Exp v

SSR

r n k

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-52

An Application of F-tests (cont.)

H0

: 3

4

50

F

SSRc SSRu

rSSRu

n k 1

1020.37 1002.75

31002.75

1795

10.51

The critical value at the 5% significance level for F3,1795

is 2.60.

We can reject the null hypothesis at the 5% level.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-53

An Application of F-tests (cont.)

• We can reject the null hypothesis that black men and black women have identical earnings functions.

• Do we really need the interaction terms, or do we get the same explanatory power by simply giving black women a different intercept?

• Let’s test the null hypothesis that the interaction coefficients are both 0.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-54

An Application of F-tests (cont.)

0 4 5

0 1 2 3

4 5

0 1 2

: 0

log( ) _

_ _

1002.75

log( )

Unconstrained Regression:

Constrained Regression:

i i i i

i i i i i

u

i i

H

earnings Ed Exp D F

Ed D F Exp D F

SSR

earnings Ed Ex

3 _

1003.08

2, 1 1795

i i i

c

p D F v

SSR

r n k

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-55

An Application of F-tests (cont.)

H0

: 4

50

F

SSRc SSRu

rSSRu

n k 1

1003.08 1002.75

21002.75

1795

0.30

The critical value at the 5% significance level for F2,1795

is 3.00.

We fail to reject the null hypothesis at the 5% level.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-56

F-tests and Regime Shifts (Chapter 9.6)

• What is the relationship between Federal budget deficits and long-term interest rates?

• We have time-series data from 1960–1994.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-57

F-tests and Regime Shifts (cont.)

• Our dependent variable is long-term interest rates (LongTermt)

• Our explanators are expected inflation (Inflationt), short-term interest rates (ShortTermt), change in real per-capita income (DeltaInct), and the real per-capita budget deficit (Deficitt).

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-58

LongTermt

0

1Inflation

t

2ShortTerm

t

3DeltaInc

t

4Deficit

t

t

F-tests and Regime Shifts (cont.)

• Note that we index observations by t, not i.

• 4 is the change in long-term interest rates from a $1 increase in the Federal deficit (measured in 1996 dollars).

• Financial market de-regulation began in 1982.

• Was the relationship between long-term interest rates and Federal deficits altered by the de-regulation?

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-59

F-tests and Regime Shifts (cont.)

• We can let the co-efficient on Deficitt vary before and after 1982 by interacting with a dummy variable.

• Create the variable D_1982t = 1 if the observation is for year 1983 or later

• To test whether the slope on Deficitt changes after 1982, conduct a t-test of the hypothesis H0

: 6 = 0

0 1 2 3

4 5 6 _1982 _1982t t t t

t t t t t

LongTerm Inflation ShortTerm DeltaInc

Deficit D Deficit D

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-60

F-tests and Regime Shifts (cont.)

• Dependent Variable: LongTermt

• Independent Variables, with standard errors

• Inflationt: 0.765 (0.0372)

• ShortTermt: 0.822 (0.0586)

• DeltaInct: -6.4·10-6 (1.6·10-4)

• Deficitt: 0.002 (0.0004)

• D_1982t: -0.739 (0.6608)

• Deficitt·D_1982t: 0.0005 (0.0007)

• Constant: 1.277 (0.2135)

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-61

F-tests and Regime Shifts (cont.)

• For the period 1960–1982, the slope on Deficitt is 0.0022. A $1 increase in the Federal deficit per capita increases long-term interest rates by 0.0022 points.

• For the period 1983–1994, the slope on Deficitt is 0.0022 + 0.0005 = 0.0027.

• The t-statistic for Deficitt·D_1982t is 0.63. We fail to reject the null hypothesis that the slopes are different.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-62

F-tests and Regime Shifts (cont.)

• For the period 1960–1982, the slope on Deficitt is 0.0022. A $1 increase in the Federal deficit per capita increases long-term interest rates by 0.0022 points.

• Is this change important in magnitude? One quick, crude way to assess magnitudes is to ask, “How many standard deviations does Y change when I change X by 1 standard deviation?”

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-63

F-tests and Regime Shifts (cont.)

• Standard Deviation of Deficitt = 463

• Standard Deviation of LongTermt = 2.65

• A 1-standard-deviation change in Deficitt is predicted to cause a 463·0.0022 = 1.02 percentage point change in LongTermt, or about a third of a standard deviation

• At first glance, the effect of Federal deficits on interest rates is non-negligible, but not massive, either.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-64

F-tests and Regime Shifts (cont.)

• Let’s test a more complicated hypothesis.

• Does the entire financial regime shift after 1982?

• Let’s let every coefficient vary between the two time periods.

0 1 2 3

4 5 6

7 8

9

_1982 _1982

_1982 _1982

_1982

t t t t

t t t t

t t t t

t t t

LongTerm Inflation ShortTerm DeltaInc

Deficit D Inflation D

ShortTerm D DeltaInc D

Deficit D

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-65

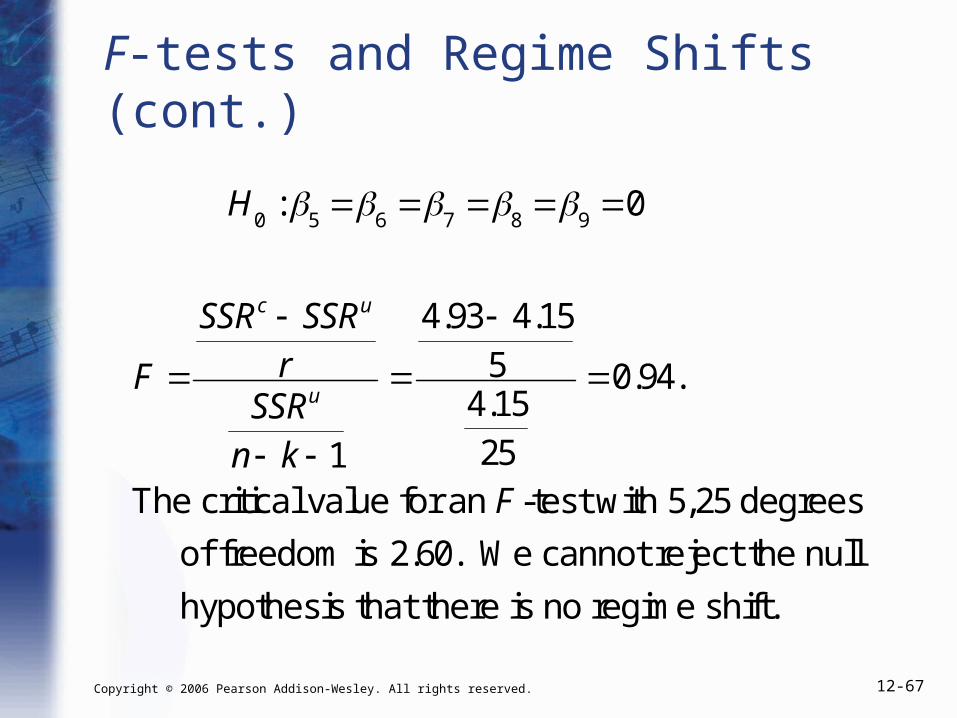

H0 :5 6 7 8 9 0

F-tests and Regime Shifts (cont.)

• Does the entire financial regime shift after 1982?

• Test the joint hypothesis that every interaction term is 0:

• We need an F-test

• There are 5 equal signs, so r = 5

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-66

F-tests and Regime Shifts (cont.)

0 5 6 7 8 9

0 1 2 3

4 5 6

7 8

9

: 0

_1982 _1982

_1982 _1982

Unconstrained regression:

t t t t

t t t t

t t t t

H

LongTerm Inflation ShortTerm DeltaInc

Deficit D Inflation D

ShortTerm D DeltaInc D

Defi

0 1 2 3

4

_1982

Constrained regression:t t t

t t t t

t t

cit D

LongTerm Inflation ShortTerm DeltaInc

Deficit v

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-67

F-tests and Regime Shifts (cont.)

H0

: 5

6

7

8

90

F

SSRc SSRu

rSSRu

n k 1

4.93 4.15

54.15

25

0.94.

The critical value for an F-test with 5,25 degrees

of freedom is 2.60. We cannot reject the null

hypothesis that there is no regime shift.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-68

F-tests and Regime Shifts (cont.)

• Instead of using dummy variables, we could conduct this same test by running the same regression on 3 separate datasets.

• For the constrained regression (there is no regime shift), we use all the data, 1960–1994.

• For the unconstrained regression (there is a regime shift), we run separate regressions for 1960–1982 and 1983–1994.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-69

F-tests and Regime Shifts (cont.)

0 1 2

3 4

t t t

t t t

LongTerm Inflation ShortTerm

DeltaInc Deficit

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-70

1982 1994 19942 2 2

1960 1983 1960t t t

t t t

e e e

F-tests and Regime Shifts (cont.)

• For each regression, we record the SSR

• SSRc is the SSR from the regression for 1960–1994, SSR1960–1994

• SSRu is the sum SSR1960–1982 + SSR1983–1994

• Using these SSR ’s, we can compute F

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-71

F-tests and Regime Shifts (cont.)

SSRu SSR1960 1982 SSR1983 1994

2.17 1.98 4.15

SSRc SSR1960 1994 4.93

r 5

n k 125

F

SSRc SSRu

rSSRu

n k 1

4.93 4.15

54.15

25

0.94

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-72

F-tests and Regime Shifts (cont.)

• See Chapter 9.7 for additional tests for regime shifts.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-73

Review

• How can we test multiple conditions simultaneously?

• Intuition: run a regression normally, and then also run a regression where you constrain the parameters to make the null hypothesis true. See if imposing the conditions makes a big difference.

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-74

Review (cont.)

• Does imposing the restrictions from our null hypothesis greatly increase the SSR ? (Remember, we want a low SSR.)

• Run both regressions and calculate the SSR

• Call the SSR for the unrestricted version the SSRu

• Call the SSR for the restricted version the SSRr

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-75

Review (cont.)

• Run both regressions and calculate the SSR

• Call the SSR for the unrestricted version the SSRu

• Call the SSR for the restricted version the SSRr

• If the null hypothesis is true, then imposing the restrictions will not change the SSR much. We will have a “small” SSRr-SSRu

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-76

Review (cont.)

( 1)

c u

u

SSR SSRrF

SSRn k

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-77

Review (cont.)

• When the i are distributed normally, the F-statistic will be distributed according to the F-distribution with r, n-k-1 degrees of freedom

• We know how to compute an F-statistic from the data

• We know the distribution of the F-statistic under the null hypothesis

• The F-statistic meets all the needs of a test statistic

Copyright © 2006 Pearson Addison-Wesley. All rights reserved. 12-78

Review (cont.)

• If our null hypothesis is true, then imposing the hypothesized values as constraints on the regression should not change SSR much. Under the null, we expect a low value of F.

• If we see a large value of F, then we can build a compelling case against the null hypothesis.

• The F table tells you the critical values of F for different values of r and n-k-1.