copyright 2002 by harcourt, inc. all rights reserved. chapter 14: meeting retirement goals clip art...

TRANSCRIPT

Copyright 2002 by Harcourt, Inc. All rights reserved.

CHAPTER 14:

MEETING RETIREMENT GOALS

Clip Art 2001 Microsoft Corporation. All rights reserved.

14-2

Copyright 2002 by Harcourt, Inc. All rights reserved.

Pitfalls in Retirement Planning

Starting too late.

Putting away too little.

Investing too conservatively (especially when you are younger).

14-3

Copyright 2002 by Harcourt, Inc. All rights reserved.

Steps in Retirement Planning

At what age do you want to retire?

Start early in your career devoting money toward your retirement goals.

Clip Art 2001 Microsoft Corporation. All rights reserved.

1. Set Your Goals:

14-4

Copyright 2002 by Harcourt, Inc. All rights reserved.

2. Estimate Your Needs:

Determine household expenditures.

Estimate income.

Consider the effects of inflation.

Decide how you will provide for the difference between income and needs.

14-5

Copyright 2002 by Harcourt, Inc. All rights reserved.

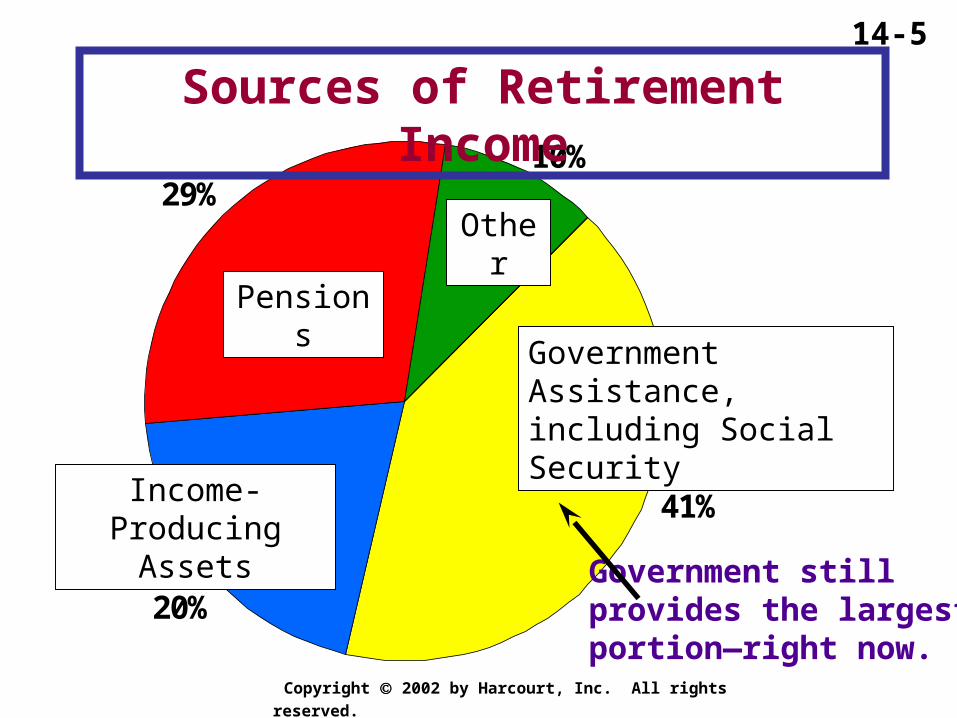

10%29%

20%

41%

Government stillprovides the largestportion—right now.

Government Assistance, including Social Security

Income-Producing Assets

Pensions

Other

Sources of Retirement Income

14-6

Copyright 2002 by Harcourt, Inc. All rights reserved.

Social Security

Benefits are provided by taxes you and your employer pay (you pay both halves if you are self-employed).

Amount of benefits may be insufficient by the time you retire.

Think of it as an insurance system rather than a retirement plan.

14-7

Copyright 2002 by Harcourt, Inc. All rights reserved.

Why SS may be in trouble:

The number of people retiring is increasing.

The number of people who work and pay the taxes for retirement benefits is decreasing.

Eventually more money may be flowing out of the system than is flowing in.

14-8

Copyright 2002 by Harcourt, Inc. All rights reserved.

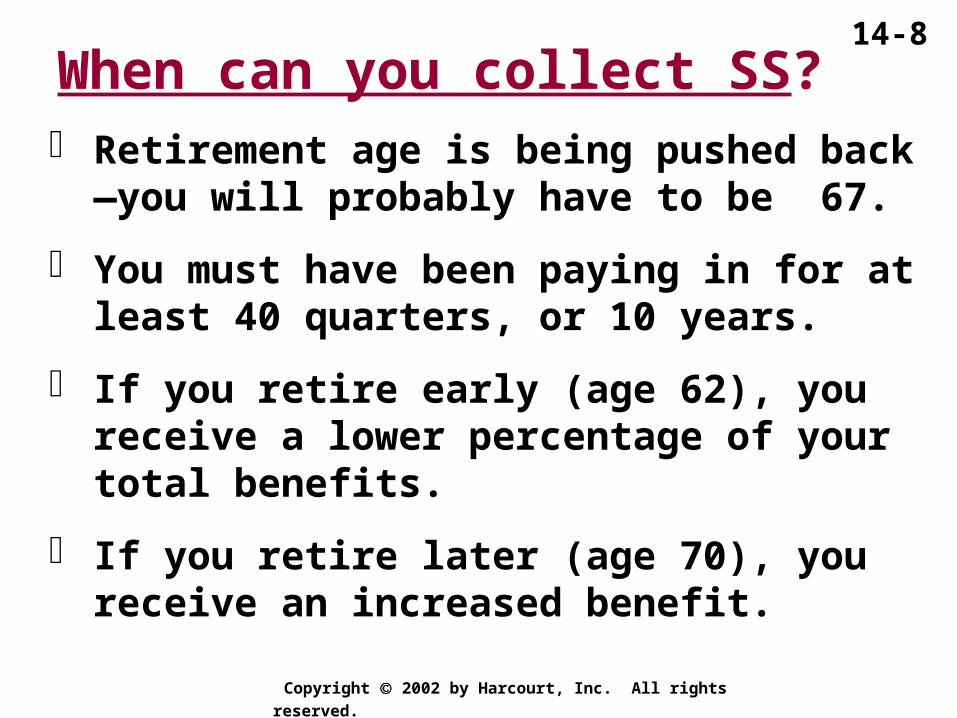

When can you collect SS? Retirement age is being pushed back—

you will probably have to be 67.

You must have been paying in for at least 40 quarters, or 10 years.

If you retire early (age 62), you receive a lower percentage of your total benefits.

If you retire later (age 70), you receive an increased benefit.

14-9

Copyright 2002 by Harcourt, Inc. All rights reserved.

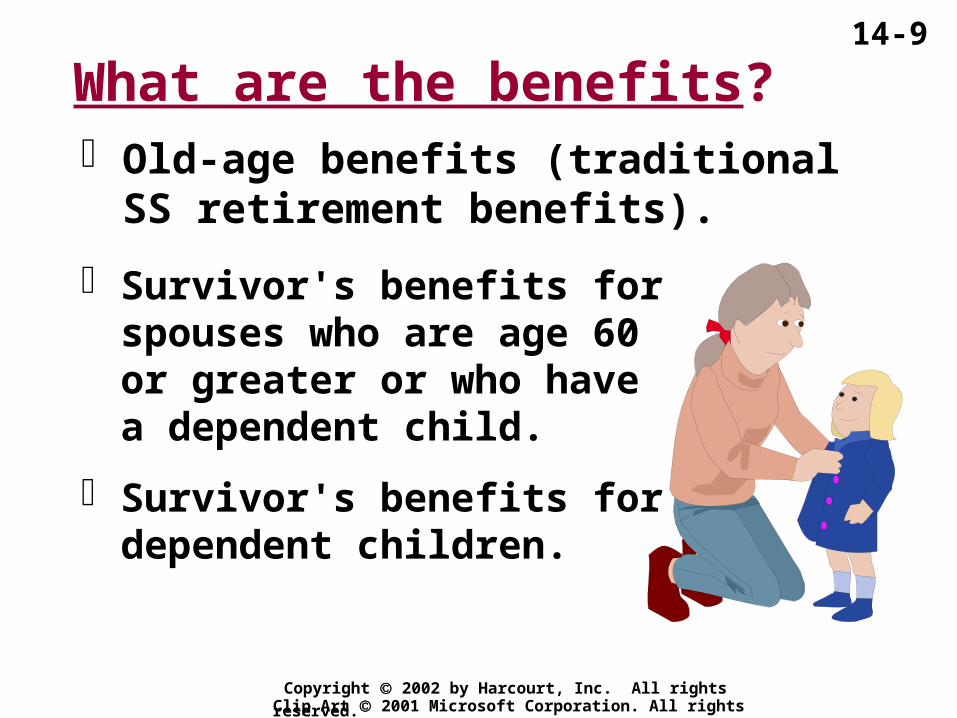

What are the benefits?

Survivor's benefits for spouses who are age 60 or greater or who have a dependent child.

Survivor's benefits for dependent children.

Old-age benefits (traditional SS retirement benefits).

Clip Art 2001 Microsoft Corporation. All rights reserved.

14-10

Copyright 2002 by Harcourt, Inc. All rights reserved.

SS benefits benefits are reduced $1 for every $2 of earnings over the $10,680 (in 2001) annual threshold.

If you are age 62–65 and have elected to receive SS benefits but continue to work—

$

Clip Art 2001 Microsoft Corporation. All rights reserved.

Reductions in SS benefits:

14-11

Copyright 2002 by Harcourt, Inc. All rights reserved.

“Unearned income” does not affect SS benefits. (Ex: investment income)

SS benefits are income taxable if your annual income exceeds $25,000 if single ($32,000 for married filing jointly).

For those age 65 or older who work, SS benefits are no longer reduced!

14-12

Copyright 2002 by Harcourt, Inc. All rights reserved.

Pension Plansand

Retirement Programs

Employer-sponsored retirement programs

Self-directed retirement programs

Clip Art 2001 Microsoft Corporation. All rights reserved.

14-13

Copyright 2002 by Harcourt, Inc. All rights reserved.

Participation requirements — are you eligible to participate in the program?

Contributions — am I required to contribute to my own plan or not?

Vesting — how long before I can take the money with me if I leave?

Retirement age — when can I retire?

Qualifying — does it qualify for tax deductibility?

Employer-Sponsored Programs:

14-14

Copyright 2002 by Harcourt, Inc. All rights reserved.

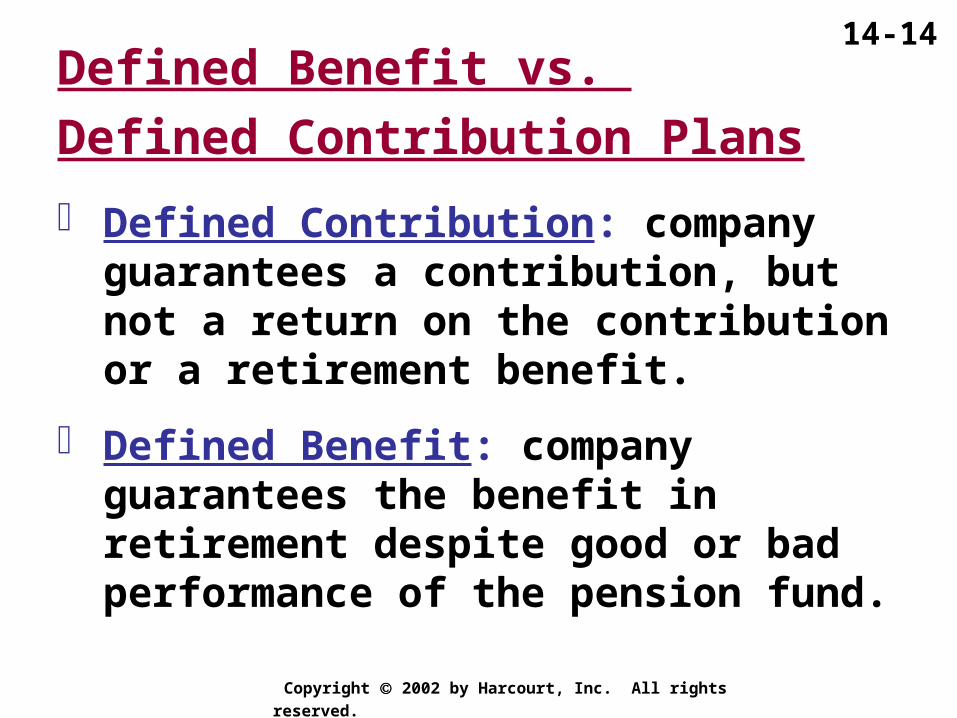

Defined Contribution: company guarantees a contribution, but not a return on the contribution or a retirement benefit.

Defined Benefit: company guarantees the benefit in retirement despite good or bad performance of the pension fund.

Defined Benefit vs.

Defined Contribution Plans

14-15

Copyright 2002 by Harcourt, Inc. All rights reserved.

Profit-sharing plans — employees benefit from company's earnings.

Thrift and savings plans — employer contributes to employee's fund. Employee contributions NOT deductible.

Salary reduction plans — employee contributes part of salary; contributions tax deductible; employer may also contribute as in a 401(k), 457, or 403(b).

Supplemental Plans:Allow employees to increase retirement funds. These plans are often voluntary, and contributions may be tax deductible.

14-16

Copyright 2002 by Harcourt, Inc. All rights reserved.

Keogh Plans — for professionals or small business owners and employees.

SEP Plans — for professionals or small business owners with few or no employees; simple to administer.

IRAs — anyone can open one; other self-directed plans may allow greater contributions.

Self-Directed Retirement Programs:Allow individuals and the self-employed to set up tax-deferred retirement plans for themselves and their employees.

14-17

Copyright 2002 by Harcourt, Inc. All rights reserved.

Traditional Tax-Deductible IRA — for those with no employer-sponsored plan or with incomes below a certain level.

Traditional Non-Deductible IRA — for those with an employer-sponsored plan and incomes over a certain level.

Roth IRA — contributions not deductible; for those with incomes below a much higher level, regardless of employer-sponsored plans.

Types of IRAs:Each year, you must EARN at least as much as you contribute to an IRA.

14-18

Copyright 2002 by Harcourt, Inc. All rights reserved.

More on IRAs: Maximum total yearly contribution to all IRAs

combined is $3000 (as of 2002) or your earned income (whichever is less).

Non-working spouse can also contribute up to $3000 (as of 2002).

An IRA is not an investment; it is the container and can hold a variety of types of investments.

Education IRAs are for future education costs of child or grandchild. Currently, $2000 (as of 2002) is max for yearly contributions, which are NOT deductible.

14-19

Copyright 2002 by Harcourt, Inc. All rights reserved.

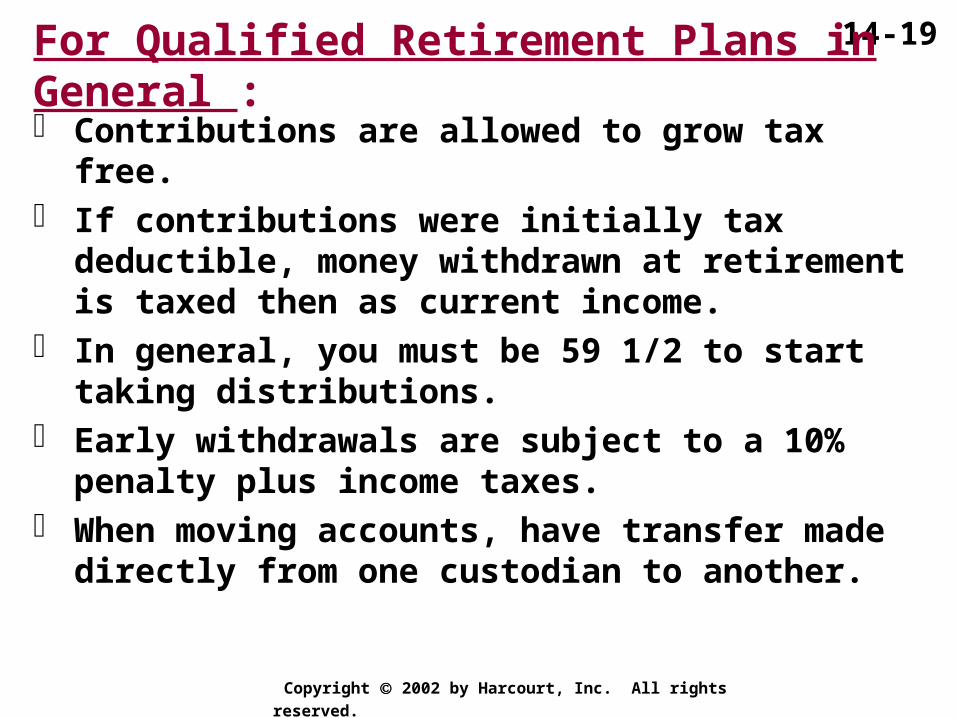

For Qualified Retirement Plans in General :

Contributions are allowed to grow tax free. If contributions were initially tax deductible,

money withdrawn at retirement is taxed then as current income.

In general, you must be 59 1/2 to start taking distributions.

Early withdrawals are subject to a 10% penalty plus income taxes.

When moving accounts, have transfer made directly from one custodian to another.

14-20

Copyright 2002 by Harcourt, Inc. All rights reserved.

Annuities Tax-sheltered investment vehicles

administered by life insurance companies.

An agreement to make contributions now in return for a series of payments later.

Contributions NOT tax deductible.

14-21

Copyright 2002 by Harcourt, Inc. All rights reserved.

Before Retirement: Accumulation Period — annuitant

purchases annuity by paying premiums into the account.

During Retirement:

Distribution Period — insurance company makes payments to annuitant. Portion not returned to annuitant prior to death goes to beneficiaries.

14-22

Copyright 2002 by Harcourt, Inc. All rights reserved.

Single Premium vs. Installments — one large lump-sum payment or a series of payments to purchase the annuity.

Immediate vs. Deferred — begin receiving payments immediately or wait to receive payments after purchasing annuity.

Fixed vs. Variable — investment grows at a low guaranteed fixed rate or at a presumably higher variable market-based rate with no guarantee of return.

Classification of Annuities:

14-23

Copyright 2002 by Harcourt, Inc. All rights reserved.

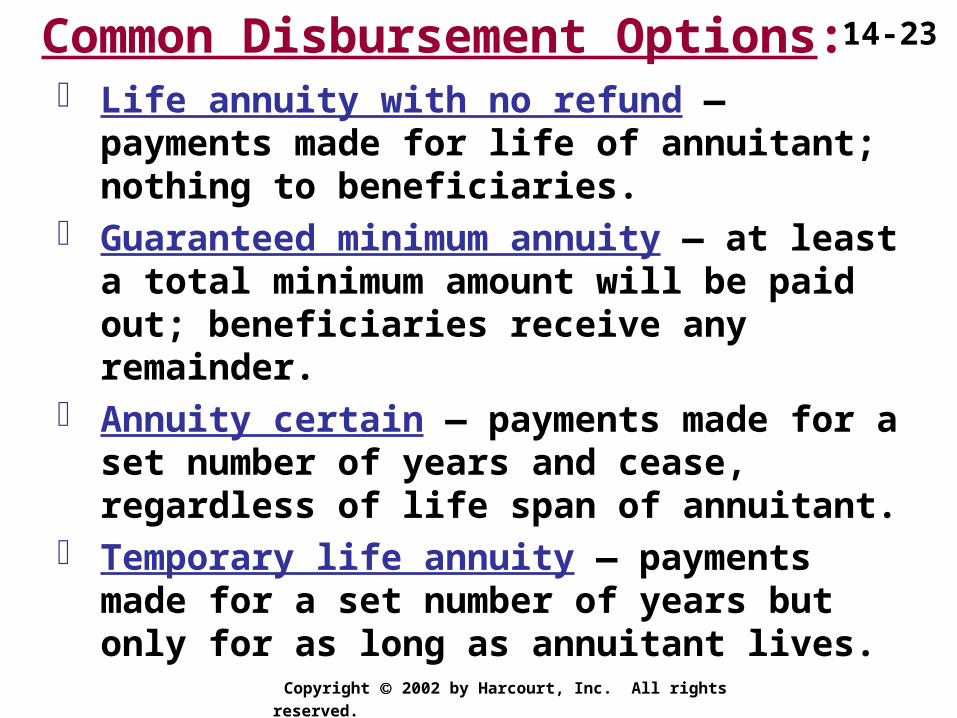

Life annuity with no refund — payments made for life of annuitant; nothing to beneficiaries.

Guaranteed minimum annuity — at least a total minimum amount will be paid out; beneficiaries receive any remainder.

Annuity certain — payments made for a set number of years and cease, regardless of life span of annuitant.

Temporary life annuity — payments made for a set number of years but only for as long as annuitant lives.

Common Disbursement Options:

14-24

Copyright 2002 by Harcourt, Inc. All rights reserved.

Remember: Annuities are life insurance products,

which usually mean higher yearly fees plus surrender charges.

Annuities are only as good as the financial strength of the companies which issue them.

Retirement accounts are already tax sheltered.

Withdrawals made before age 59 1/2 are subject to 10% penalty and income taxes.

14-25

Copyright 2002 by Harcourt, Inc. All rights reserved.

Annuities may be an attractive means for higher income individuals who have fully funded their retirement accounts to tax shelter even more money.

Clip Art 2001 Microsoft Corporation. All rights reserved.

Copyright 2002 by Harcourt, Inc. All rights reserved.

THE END!