copper and copper alloy scrap use and trade in china … 2013/china, copperalloy...refined copper...

TRANSCRIPT

2013 ISRI Convention

April 12th 2013, Orlando, Florida, USA

Copper and Copper Alloy Scrap Use and Trade

in China and the Rest of the World

Carlos R. Risopatron

Head of Environment and Economics

International Copper Study Group

email: [email protected] www.icsg.org

Copper Scrap Use and Refined Copper Price: Annual Growth 2003-2011

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012:Jan-

Sept

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Secondary Refined Production (Kt-Cu) Cu Content of Direct Melt by Semis Kt-Cu LME Refined Copper Price USD/Tonne

The global use of scrap in smelters and fabricators is driven by refined copper prices.

2012: a 10% fall in refined copper prices with unreported bonded stocks in Shanghai.

The price of refined copper is driven by the global balance of refined copper.

ICSG World Refined Copper Balance and

LME Refined Price Annual Growth 1974-2012

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

-1,000 -800 -600 -400 -200 0 200 400 600 800 1,000

ICSG Refined Copper Balance in Tonnes

2006 miners shortage

2011

2012

World Refined Copper Demand: Million Tonnes of Copper, ICSG.

0 5 10 15 20 25

2002

2012 * Preliminary

World ex-China China

Increasing Chinese demand: the key factor driving

the global shortage of refined copper in the last decade.

1974 2012 Growth

World Refined Demand Kg per Cápita 1.93 2.94 52.3%

Scrap recyclers helped to reduce the impact of the global copper shortage.

… but most of the supply response came at the end from copper miners.

World Mine Capacity Utilization and Refined Copper Price 2002-2012. % Utilization and USD/Tonne.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

80 82 84 86 88 90 92 94

The other key factor of the global refined market shortage

was a sharp contraction in copper mine capacity utilization.

440

183

0

50

100

150

200

250

300

350

400

450

Concentrate SX-EW

Additional World Copper Mine Production Jan-Nov 2012/2011

But in 2012 world copper mine capacity utilization jumped.

Miners increased production before expected new capacity in 2013-2014.

World Copper Mine Capacity 2012 in Kt-Cu

and Plans 2013-2016.

19,81920,388

21,343 21,52322,218 22,550

00

112747

1,978

2,956

00

689

2,214

1000

18,000

20,000

22,000

24,000

26,000

28,000

30,000

2011 2012 2013 2014 2015 2016

Operating Developing Feasibility

2013-2014 copper mine capacity projects pipeline is big as usual. 1.1 Mt-Cu in 2013, ~1 Mt-Cu in 2014, but mine output will grow slower than new capacity.

“Is time to stop building!“ Ivan Glasenberg, CEO Glencore International. (Miami, March 2013)

If copper holds a Ph.D. in economics this is the picture of the world economy.

Industrial use of copper up just in China and a few oil economies.

Country 2007 2012 Oct* Growth SourceMt Mt %

China 6.3 11.31 79.5% ICSG

United States 2.94 2.17 -26.0% ICSG

Germany 1.85 1.52 -17.7% ICSG

Japan 1.75 1.33 -23.9% ICSG

Korean Republic 1.33 1.06 -20.2% ICSG

Italy 1.75 1.03 -41.2% ICSG

Taiwan (China) 0.85 0.71 -16.4% ICSG

Spain 0.34 0.32 -4.7% ICSG

Poland 0.34 0.23 -31.4% ICSG

France 0.54 0.19 -64.5% ICSG

Slovakia 0.02 ICSG

India 0.71 0.64 -9.6% Estimate

Russian Federation 0.80 0.56 -30.2% Estimate

Turkey 0.41 0.27 -34.0% Estimate

Thailand 0.29 0.27 -5.6% Estimate

Brazil 0.37 0.23 -38.4% Estimate

Indonesia 0.20 0.22 8.5% Estimate

United Arab Emirates 0.00 0.21 100% Estimate

Saudi Arabia 0.19 0.21 8.4% Estimate

Iran 0.19 0.20 7.5% Estimate

Sample of Countries 21.1 22.7 7.4%

* 12 months before November 2012

Fabrication of Copper and Copper Alloyed Products: 2012 Versus 2007

million tonnes gross weight, other alloyed metals included

United States of America:

Monthly Semis Output

0

50

100

150

200

250

300

Jan

Feb

Mar Ap

r

May Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar Ap

r

May Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar Ap

r

May Jun

Jul

Aug

Sep

Oct

Nov

2010 2011 2012

Copper Wire Rod (sec>6mm)

Copper Alloys Plates, Sheets & Strips

Copper Tubes

Copper Alloys Bars & Profiles

Copper Plates, Sheets & Strips

Copper Bars & Profiles

Copper Wire - Other

Copper Alloys Tubes (Total)

In the USA and EU-27, copper and copper alloy fabrication continue stagnated

EU-27 Fabricators Reporting Monthly:

Recent Trends, Kt.

0

50

100

150

200

250

300

350

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct

2011 2012

Germany Italy Spain Poland France Slovakia

North East Asia: Copper and Alloys Semifabrication Output

Latest Monthly Data, Kt ICSG

0

200

400

600

800

1,000

1,200

Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2011 2012

China

Japan

Korean Rep.

Taiwan (China)Gross Weight Numbers

Copper Alloys Included

Cu,Zn, Sn,Pb and other metals

Strong growth in China official fabrication statistics in 2012: up >12% to 11.5 Mt !

China Copper Content in Fabrication Output. Source: ICSG Consultants

-

2,000

4,000

6,000

8,000

10,000

2011 2012

Castings Copper Alloy Semis Copper Semis Copper Wire Rod

But copper content in Chinese fabrication ~9.2 Mt-Cu : just 1% growth in 2012 Chinese large semifabricators profits down around 50% in H1-2012!

China Copper Wire Rod Output and Capacity Kt-Cu

0 2,000 4,000 6,000 8,000 10,000 12,000 14,000

2009

2010

2011

2012

2013(f)

2014(f)

2015(f)

Production Capacity

China produced 5.8 Mt-Cu of copper wire rod in 2012. Another 3.3 Mt-Cu used in copper semis, brass mills and castings.

Wire rod capacity utilization around 50% and more plant capacity coming.

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

160.0

180.0

200.0Ja

n

Feb

Mar

Apr

May

Jun Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun Jul

Aug

Sep

Oct

Nov

Dec

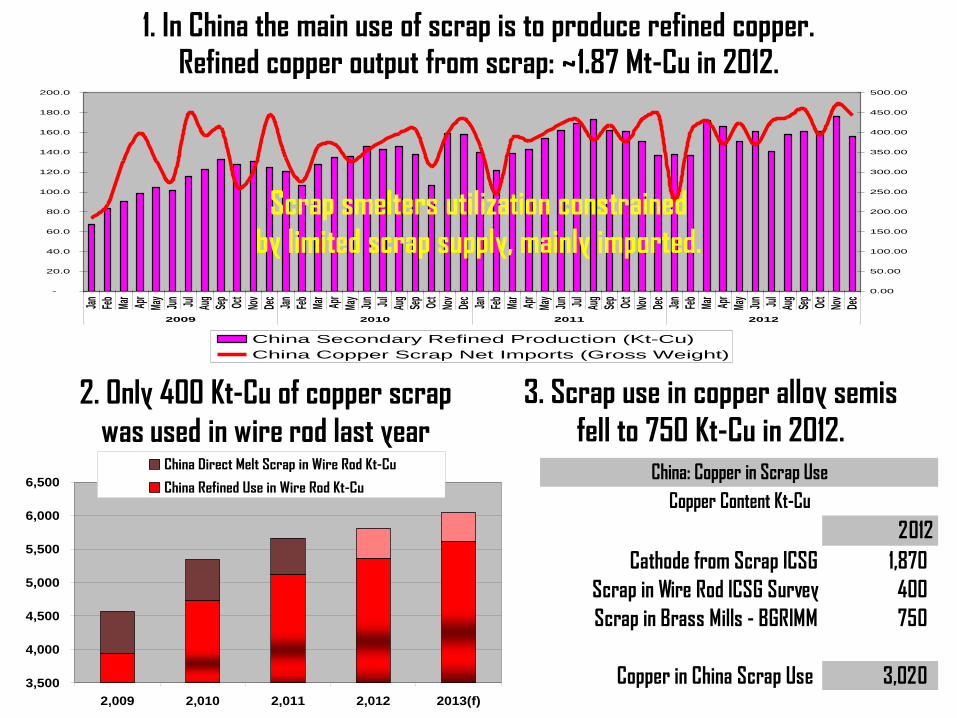

2009 2010 2011 2012

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

450.00

500.00

China Secondary Refined Production (Kt-Cu)

China Copper Scrap Net Imports (Gross Weight)

Scrap smelters utilization constrained

by limited scrap supply, mainly imported.

1. In China the main use of scrap is to produce refined copper. Refined copper output from scrap: ~1.87 Mt-Cu in 2012.

3,500

4,000

4,500

5,000

5,500

6,000

6,500

2,009 2,010 2,011 2,012 2013(f)

China Direct Melt Scrap in Wire Rod Kt-Cu

China Refined Use in Wire Rod Kt-Cu

2. Only 400 Kt-Cu of copper scrap

was used in wire rod last year

3. Scrap use in copper alloy semis

fell to 750 Kt-Cu in 2012.

2012

Cathode from Scrap ICSG 1,870

Scrap in Wire Rod ICSG Survey 400

Scrap in Brass Mills - BGRIMM 750

Copper in China Scrap Use 3,020

China: Copper in Scrap Use

Copper Content Kt-Cu

China 2012: Copper in Scrap Use 3.02 Mt-Cu Copper Content

62%13%

25%

Cathode from Scrap Official ICSG Scrap in Wire Rod ICSG Survey 2012 Scrap in Brass Mills BGRIMM

China Coper Scrap Supply 2011-2013 Kt-Cu

2012-2013 Forecasts

0 500 1,000 1,500 2,000 2,500 3,000 3,500

2011

2012

2013

Copper in Scrap Imports Domestic Old Scrap Domestic New Scrap

Copper in imported scrap

to China ~ 1.8 Mt-Cu in 2011,

+/- the same in 2012 !

Domestic old scrap

recycling growing slowly:

•slow GDP 2011 and 2012,

•lower copper scrap prices,

•low historic stock of copper.

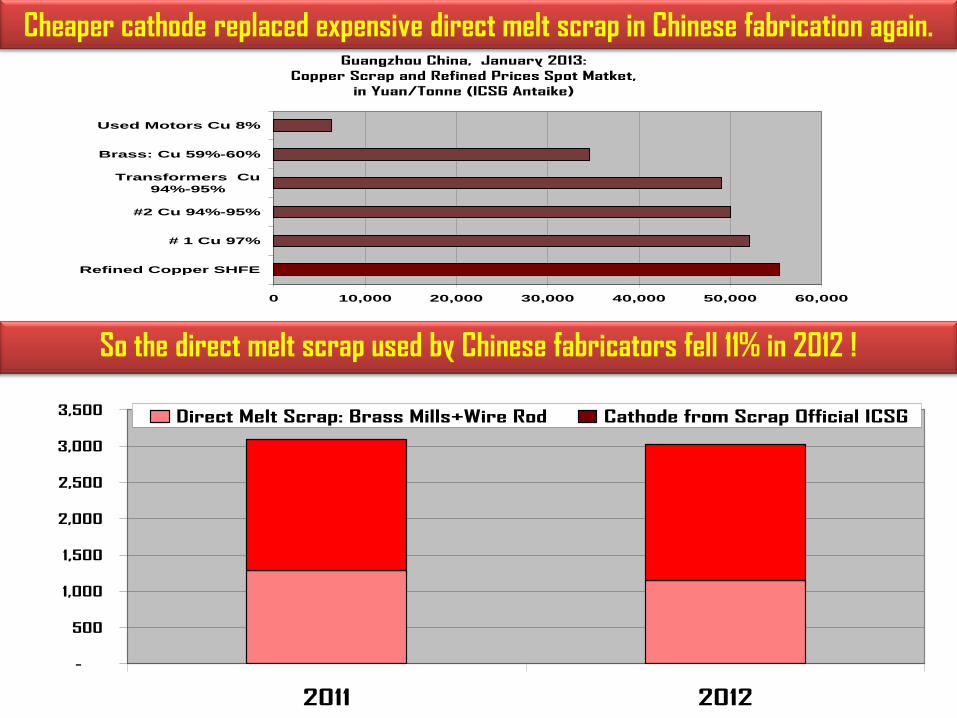

Guangzhou China, January 2013:

Copper Scrap and Refined Prices Spot Matket,

in Yuan/Tonne (ICSG Antaike)

0 10,000 20,000 30,000 40,000 50,000 60,000

Refined Copper SHFE

# 1 Cu 97%

#2 Cu 94%-95%

Transformers Cu

94%-95%

Brass: Cu 59%-60%

Used Motors Cu 8%

Cheaper cathode replaced expensive direct melt scrap in Chinese fabrication again.

So the direct melt scrap used by Chinese fabricators fell 11% in 2012 !

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2011 2012

Direct Melt Scrap: Brass Mills+Wire Rod Cathode from Scrap Official ICSG

China: Annual Growth of Imported Copper

Raw Materials 2012/2011 (%)

(15.0)

(10.0)

(5.0)

0.0

5.0

10.0

15.0

20.0

25.0

Refined Copper Concentrates Scrap

Volume

Value

With lower prices, China imported more refined and concentrate than scrap in 2012 Imported copper scrap values fell in proportion to falling refined copper prices.

0

10000

20000

30000

40000

50000

60000

70000

80000

Jan.

Feb.

Mar

.

Apr

.

May

Jun.

Jul.

Aug

Sep Oct

Nov

Dec Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep Oct

Nov

Dec Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep Oct

Nov

Dec Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep Oct

Nov

Dec

2009 2010 2011 2012

SHFE Cash #1 copper cu 98% min #2 Copper 94%-96%

Lower refined prices increased the chronic

shortage of scrap in China.

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Scrap Smelting

Capacity

2012 Scrap

Smelter Output

2012 Scrap

Refining Capacity

2012 Scrap

Refinery Output

Jiangxi Copper Tongling Group Shandong Dongying FangyuanGuangxi Nonferrous Hebei Jiangchang Copper Shandong JinshengTianyuan Copper Ningbo Jintian JinchuanDaye Non-ferrous Hefeng Copper XiangguangQingyuan Yuntong Qingyuan Smelter of JCC ShengzhouNingbo Jintian_yingtan Lanxi Zili Copper Yunnan CopperShanghai Dachang Jiangxi Jinhui Shanghai XinyeDongying Jinxi Wuhu Hengxin Group Guangzhou Zhujiang CopperDaye Dajiang Copper Tonglu Hengxin Tianjin DatongLuoyang Copper

Smelters Refineries

53.0% 61.4%

Survey: Capacity Utilization 2012

So the increasing copper scrap smelting capacity in China remains under-utilized.

Plant, Location & Technology Capacity kt/a Operating

Jinsheng Copper, Sahndong NGL 100 2013

Shandong Dahai NA 200 2013

Shandong Xinze Smalter & Refinery 200 2013

Tongling Group NGL 120 2014

Jinchian, Fangchenggang, Guangxi AUSMELT 200 2014

Yantai Humon , Shandong NGL 200 2014

Tianjing Datong Ausmelt 200 2015

Total 1,220 3 Years

China Copper Scrap Smelters Pipeline 2013-2015

Scrap smelting capacity 2013-2015:

to grow even more to >1,2 Mt-Cu

Main reason to invest:

EIA approval easier versus mine smelters.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2009 2010 2011 2012 2013(f) 2014(f) 2015(f)

Scrap Recovery/secondary Output China Primary Cathode Production

Refined copper output from scrap may grow faster in China…

but profits at Chinese scrap smelters are squeezed by the small spreads.

Small fabricators and smelters using scrap in China will close in late 2015 (MIIT) Small brass mills to be replaced by large copper alloy plants. Less money to new smelters.

• New Scrap Direct Melt Use Capacity • >= 50kt Allowed.

• <20kt to close by 2015.

• New Scrap Smelters Capacity • > 100 Kt Allowed.

• < 50 Kt to close by 2015.

With lower prices in 2012, global scrap exports down 4%... UK and USA most affected.

2012 Growth in Copper and Alloy Scrap,

Selected Countries, January-November

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

United

King

dom

United

Sta

tes

Belgium

German

y

Nethe

rland

s

Fran

ce Italy

Japa

n

Copper and Alloy Scrap Net Exports: Main Net Exporters

Jan-Nov 2010-2012, Kt Gross Weight

-500

0

500

1,000

1,500

2,000

Jan-Nov 2010 Jan-Nov 2011 Jan-Nov 2012

Belgium Germany Italy Netherlands France United Kingdom United States

European Union Exports to China in 2012

Copper and Alloy Scrap Kt. Gross weight.

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Copper Scrap Alloy ScrapIRELAND LUXEMBOURG MALTA SLOVAKIA LATVIA LITHUANIA

ESTONIA CYPRUS SWEDEN AUSTRIA HUNGARY DENMARK

GREECE BULGARIA SLOVENIA POLAND PORTUGAL ROMANIA

CZECH REPUBLIC (CS->1992) FINLAND FRANCE SPAIN BELGIUM (and LUXBG -> 1998) ITALY

UNITED KINGDOM NETHERLANDS GERMANY (incl DD from 1991)

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

EU-27 copper and alloy scrap

exports to China:

>1 Mt gross weight in 2011

989 Kt gross weight in 2012

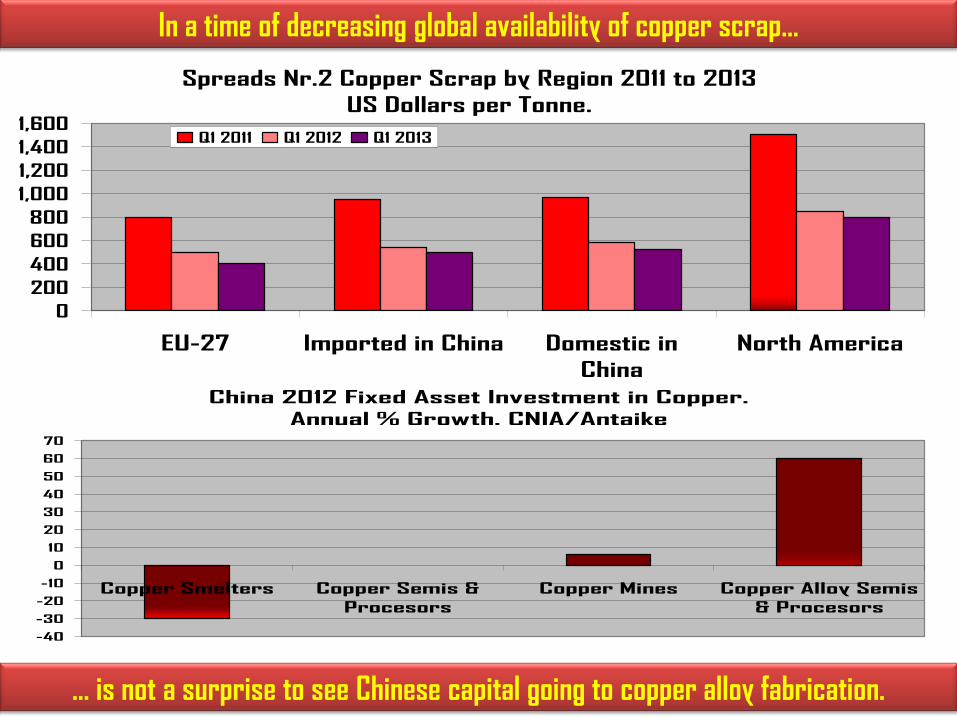

Spreads Nr.2 Copper Scrap by Region 2011 to 2013

US Dollars per Tonne.

0

200

400

600

800

1,000

1,200

1,400

1,600

EU-27 Imported in China Domestic in

China

North America

Q1 2011 Q1 2012 Q1 2013

In a time of decreasing global availability of copper scrap...

China 2012 Fixed Asset Investment in Copper.

Annual % Growth. CNIA/Antaike

-40

-30

-20

-10

0

10

20

30

40

50

60

70

Copper Smelters Copper Semis &

Procesors

Copper Mines Copper Alloy Semis

& Procesors

... is not a surprise to see Chinese capital going to copper alloy fabrication.

21

ICSG Publications Available in 2013: [email protected]

ICSG PUBLICATIONS

•The ICSG Monthly Publication: COPPER BULLETIN - 2012

•ICSG DIRECTORY OF COPPER AND COPPER ALLOY FABRICATORS - 2012

•ICSG DIRECTORY OF COPPER PLANTS AND MINES - 2012

•Access to ICSG ONLINE STATISTICAL DATABASE

The ICSG STATISTICAL YEARBOOK - 2012

•Survey on Non Ferrous Metal Use in Chinese Semifabrication Plants -2012

•Copper Scrap Supply Survey in China -2012

•Copper Scrap Market Recycling in NAFTA -2012

Study of By-products of Copper, Lead, Zinc and Nickel - 2012

ICSG Historic Recyclables Surveys - 2011

•ICSG Global Copper Scrap Research Project Final Report - 2010

•Domestic Copper Scrap Generation in China -2009

China Scrap Usage Survey to Smelters and Semis -2009

•Copper Scrap Market and International Trade in Japan -2009

•The Copper Scrap Market in India -2009

•The Chinese Copper Scrap Market -2009