contract support costs contract support costs april 17, 2009

TRANSCRIPT

Contract Support CostsContract Support Costs

April 17, 2009April 17, 2009

Contract Support CostsContract Support Costs

Consists of Indirect Costs, Direct Contract Support Costs, and Start UpConsists of Indirect Costs, Direct Contract Support Costs, and Start Up

Section 106(a)(2):Section 106(a)(2):

““There shall be added to the amount required by paragraph (1) There shall be added to the amount required by paragraph (1) contract support costs which shall consist of an amount for the reasonable costs for contract support costs which shall consist of an amount for the reasonable costs for activities which must be carried on by a tribal organization as a contractor to ensure compliance with the terms of the contract and prudent managementactivities which must be carried on by a tribal organization as a contractor to ensure compliance with the terms of the contract and prudent management, , but which – but which –

(A) normally are not carried on by the respective Secretary in his direct operation of the program; or (A) normally are not carried on by the respective Secretary in his direct operation of the program; or

(B) (B) are provided by the Secretary in support of the contracted amount from resources other than those under contract”.are provided by the Secretary in support of the contracted amount from resources other than those under contract”.

Section 106(a)(3)(A):Section 106(a)(3)(A):

““The contract support costsThe contract support costs that are eligible costs for the purposes of receiving funding under this Act that are eligible costs for the purposes of receiving funding under this Act shall include the costs ofshall include the costs of reimbursing each tribal reimbursing each tribal contractor for reasonable and allowable costs of – contractor for reasonable and allowable costs of –

(i) direct program expenses for the operation of the Federal program that is the subject of the contract, and(i) direct program expenses for the operation of the Federal program that is the subject of the contract, and

(ii) any additional administrative or other expenses related to the overhead incurred by the tribal contractor(ii) any additional administrative or other expenses related to the overhead incurred by the tribal contractor in connection with the in connection with the operation of the Federal program, function, service, or activity pursuant to the contract, except that such funding shall not duplicate any funding provided operation of the Federal program, function, service, or activity pursuant to the contract, except that such funding shall not duplicate any funding provided under section 106(a)(3)(A)”.under section 106(a)(3)(A)”.

Section 106(a)(5):Section 106(a)(5):

““Subject to paragraph (6), during the initial year that a self-determination contract is in effect, the amount required to be paid under paragraph (2) Subject to paragraph (6), during the initial year that a self-determination contract is in effect, the amount required to be paid under paragraph (2) shall shall include startup costs consisting of the reasonable costs that have been incurred or will be incurred on a one-time basisinclude startup costs consisting of the reasonable costs that have been incurred or will be incurred on a one-time basis pursuant to the contract necessary pursuant to the contract necessary – –

(A) (A) to plan, prepare for, and assume operationto plan, prepare for, and assume operation of the program, function, service, or activity that is the subject of the contract; and of the program, function, service, or activity that is the subject of the contract; and

(B) to ensure compliance with the terms of the contract and prudent management”.(B) to ensure compliance with the terms of the contract and prudent management”.

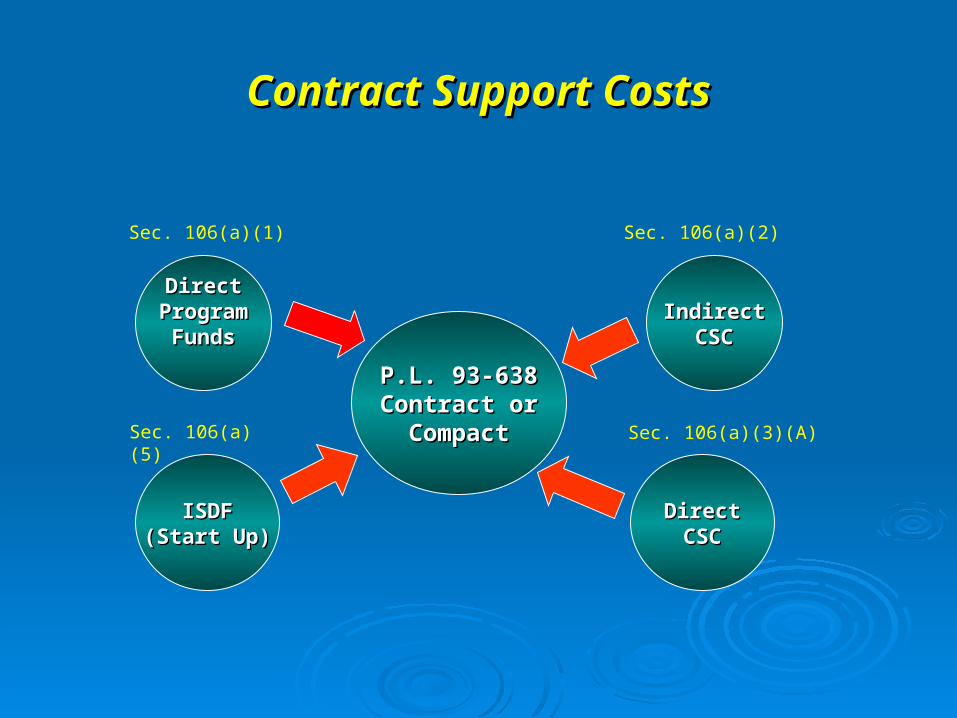

Contract Support CostsContract Support Costs

P.L. 93-638P.L. 93-638Contract orContract or

CompactCompact

IndirectIndirectCSCCSC

DirectDirectProgramProgram

FundsFunds

ISDFISDF(Start Up)(Start Up)

DirectDirectCSCCSC

Sec. 106(a)(1) Sec. 106(a)(2)

Sec. 106(a)(5) Sec. 106(a)(3)(A)

Start-Up CostsStart-Up Costs

One time costs incurred either prior to or after an One time costs incurred either prior to or after an award to plan, prepare for, and assume the award to plan, prepare for, and assume the operation of a Program, Function, Service, or operation of a Program, Function, Service, or Activity (PFSA).Activity (PFSA).

Must be reasonable and necessary and pay for Must be reasonable and necessary and pay for activities that are not provided in the amount activities that are not provided in the amount computed pursuant to Section 106(a)(1) or in the computed pursuant to Section 106(a)(1) or in the Awardee’s recurring direct or indirect contract Awardee’s recurring direct or indirect contract support costs.support costs.

Indirect CostsIndirect Costs Indirect costs are those: (a) incurred for a common or Indirect costs are those: (a) incurred for a common or

joint purpose benefiting more than one cost objective, joint purpose benefiting more than one cost objective, and (b) not readily assignable to the cost objectives and (b) not readily assignable to the cost objectives specifically benefited, without effort disproportionate to specifically benefited, without effort disproportionate to the results achieved. Generally negotiated with the DOI the results achieved. Generally negotiated with the DOI National Business Center. Ex. accounting, purchasing, National Business Center. Ex. accounting, purchasing, HR HR

Awardees Without Negotiated IDC Rates. A lump sum Awardees Without Negotiated IDC Rates. A lump sum amount (lump sum agreement) for “indirect types of amount (lump sum agreement) for “indirect types of costs” may be computed for an awardee that does not costs” may be computed for an awardee that does not have a formally negotiated IDC agreement. have a formally negotiated IDC agreement.

Direct CSCDirect CSC

Direct Contract Support Costs (DCSC) pay for activities that are not Direct Contract Support Costs (DCSC) pay for activities that are not contained in either the IDC pool (or indirect type cost budget) or the contained in either the IDC pool (or indirect type cost budget) or the amount computed pursuant to Section 106(a)(1). DCSC amounts amount computed pursuant to Section 106(a)(1). DCSC amounts are awarded on a recurring basis and need not be justified each are awarded on a recurring basis and need not be justified each year. They are more like direct program dollars than an indirect year. They are more like direct program dollars than an indirect dollars.dollars.

Examples:Examples: Unemployment taxes on direct program salariesUnemployment taxes on direct program salaries Workers compensation insurance on direct program Workers compensation insurance on direct program

salariessalaries Cost of retirement for converted Civil Service salariesCost of retirement for converted Civil Service salaries Facilities support costsFacilities support costs Training required to maintain certification requirementsTraining required to maintain certification requirements

CSC PolicyCSC PolicyIHS and BIAIHS and BIA

Since FY 2006, both BIA and IHS have Since FY 2006, both BIA and IHS have very similar CSC policies. very similar CSC policies.

The policies both allow the payment of The policies both allow the payment of Direct Contract Support Costs (DCSC) in Direct Contract Support Costs (DCSC) in addition to the payment of Indirect addition to the payment of Indirect Contract Support Costs (IDC) and Start Up Contract Support Costs (IDC) and Start Up Funds.Funds.

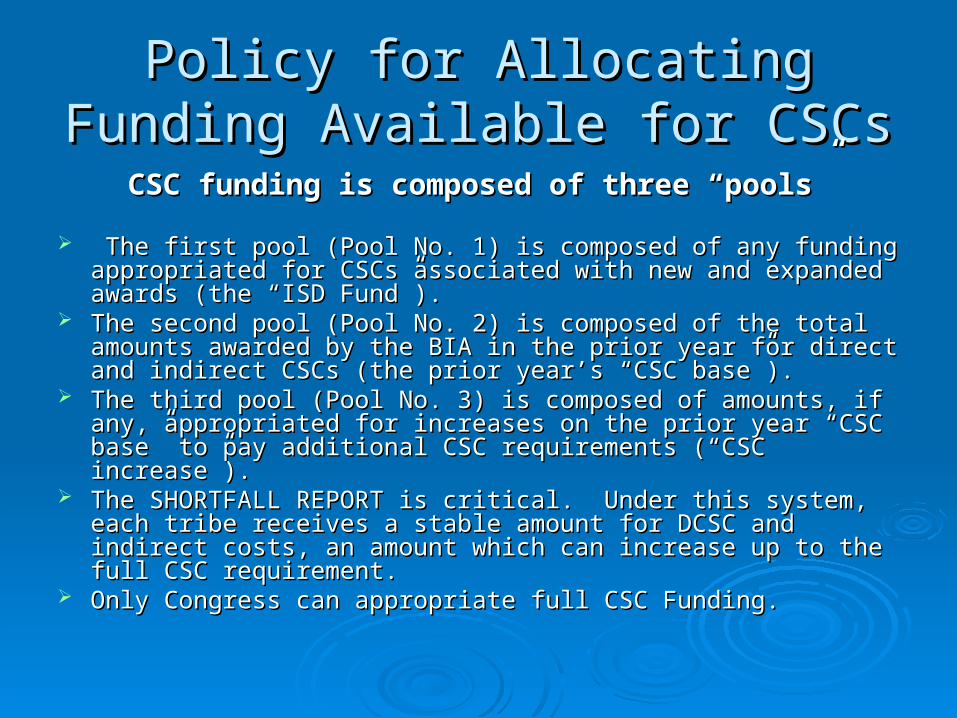

Policy for Allocating Funding Policy for Allocating Funding Available for CSCsAvailable for CSCs

CSC funding is composed of three “pools”CSC funding is composed of three “pools”

The first pool (Pool No. 1) is composed of any funding appropriated The first pool (Pool No. 1) is composed of any funding appropriated for CSCs associated with new and expanded awards (the “ISD for CSCs associated with new and expanded awards (the “ISD Fund”). Fund”).

The second pool (Pool No. 2) is composed of the total amounts The second pool (Pool No. 2) is composed of the total amounts awarded by the BIA in the prior year for direct and indirect CSCs awarded by the BIA in the prior year for direct and indirect CSCs (the prior year’s “CSC base”). (the prior year’s “CSC base”).

The third pool (Pool No. 3) is composed of amounts, if any, The third pool (Pool No. 3) is composed of amounts, if any, appropriated for increases on the prior year “CSC base” to pay appropriated for increases on the prior year “CSC base” to pay additional CSC requirements (“CSC increase”). additional CSC requirements (“CSC increase”).

The SHORTFALL REPORT is critical. Under this system, each tribe The SHORTFALL REPORT is critical. Under this system, each tribe receives a stable amount for DCSC and indirect costs, an amount receives a stable amount for DCSC and indirect costs, an amount which can increase up to the full CSC requirement.which can increase up to the full CSC requirement.

Only Congress can appropriate full CSC Funding. Only Congress can appropriate full CSC Funding.

Contract Support Cost FundingContract Support Cost Funding

IHS– Shortfall for 2009 estimated to be of IHS– Shortfall for 2009 estimated to be of just under $160 million. Currently, Tribes just under $160 million. Currently, Tribes are funded at an estimated 68% of need.are funded at an estimated 68% of need.

BIA—Shortfall for 2008 (2009 estimates BIA—Shortfall for 2008 (2009 estimates are not yet complete) are estimated at just are not yet complete) are estimated at just under $54 million. The level of need under $54 million. The level of need funded is approximately 71.8% funded is approximately 71.8%

Frequently Asked QuestionsFrequently Asked Questions

Question # 3 and Question # 5: Why do Question # 3 and Question # 5: Why do Tribes require CSCs? Tribes require CSCs?

Answer: An ISDA Contract does not Answer: An ISDA Contract does not include all of the support services an include all of the support services an Agency has at its disposal such as Agency has at its disposal such as financial management, human resources, financial management, human resources, or OGC. Additionally, Tribes incur costs or OGC. Additionally, Tribes incur costs that Agencies do not have such as that Agencies do not have such as insurance and annual audits.insurance and annual audits.

Frequently Asked QuestionsFrequently Asked Questions

Question # 8: What happens when a Tribe is Question # 8: What happens when a Tribe is not paid its Contract Support Costs?not paid its Contract Support Costs?

Answer: Since CSCs are fixed costs that a Tribe Answer: Since CSCs are fixed costs that a Tribe must incur, they typically either: 1) reduce funds must incur, they typically either: 1) reduce funds budgeted for direct services in order to cover the budgeted for direct services in order to cover the shortfall; 2) Divert Tribal funds to subsidize the shortfall; 2) Divert Tribal funds to subsidize the federal contract; or 3) a combination of these federal contract; or 3) a combination of these two approaches. two approaches.

Frequently Asked Questions Frequently Asked Questions Question 40: Why has the ISDA initiative slowed down Question 40: Why has the ISDA initiative slowed down

so severely?so severely? Answer: Contracting activities have slowed down Answer: Contracting activities have slowed down

primarily because of the enormous backlog in contract primarily because of the enormous backlog in contract support costs. For a while, IHS demanded that Tribes support costs. For a while, IHS demanded that Tribes waive their statutory rights to CSC as a condition to waive their statutory rights to CSC as a condition to taking on any new programs. taking on any new programs.

UPDATE: Currently, the biggest impediment on both the UPDATE: Currently, the biggest impediment on both the IHS and BIA side is a lack of full funding. Start-up IHS and BIA side is a lack of full funding. Start-up funding is a problem for new IHS and BIA contractors for funding is a problem for new IHS and BIA contractors for different reasons. IHS has administratively elected not different reasons. IHS has administratively elected not to allocate CSC funds to Start-up while BIA does not to allocate CSC funds to Start-up while BIA does not have budget authority for recurring start-up CSC funds. have budget authority for recurring start-up CSC funds.