continuous planning & rolling forecasts - jpk group planning & rolling forecasts utilize...

TRANSCRIPT

JPK

Gro

upBusiness Forecasting and Analytics Forum

September 19-20 • Chicago, IL

Continuous Planning & Rolling Forecasts

Utilize rolling forecasts to adaptto dynamic business challenges and opportunities

September 19, 9:45am

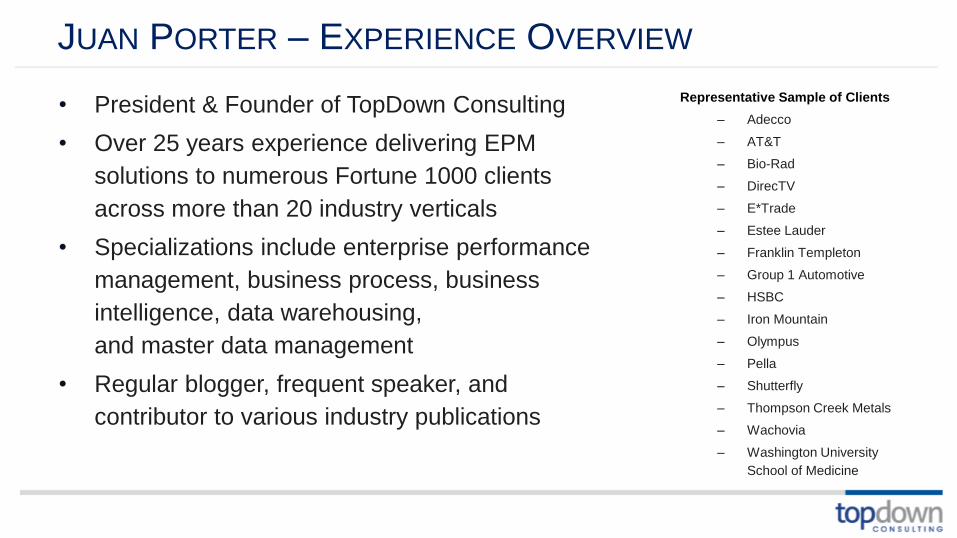

Juan Porter has over 25 years combined client, vendor, and consultant experiencewith Oracle Hyperion. He is a member of the Oracle Hyperion Partner Advisory

Council, he is actively involved in various Hyperion user groups, he has served asthe chair of Hyperion’s National Steering Committee, and he has led many

Hyperion enhancement committees. Juan is the president and founder of a leadingnationwide consulting firm, which serves over 400 of the Global 2000’s largest andbest performing companies. Industry analysts, editors, and authors frequently seekhis expertise on the future direction of EPM, current Hyperion releases, as well as

insight into strategic and practical ways to solve business problems.

View presentation online at:https://jpkgroupsummits.com/attendee5

Juan Porter – TopDown Consulting

CONTINUOUS PLANNING AND ROLLING FORECASTS

Juan Porter

September 19, 2016

JUAN PORTER – EXPERIENCE OVERVIEW

Representative Sample of Clients

– Adecco

– AT&T

– Bio-Rad

– DirecTV

– E*Trade

– Estee Lauder

– Franklin Templeton

– Group 1 Automotive

– HSBC

– Iron Mountain

– Olympus

– Pella

– Shutterfly

– Thompson Creek Metals

– Wachovia

– Washington University

School of Medicine

• President & Founder of TopDown Consulting

• Over 25 years experience delivering EPM

solutions to numerous Fortune 1000 clients

across more than 20 industry verticals

• Specializations include enterprise performance

management, business process, business

intelligence, data warehousing,

and master data management

• Regular blogger, frequent speaker, and

contributor to various industry publications

STEEPED IN TRADITION

TRADITIONAL PLANNING PROCESS

• Annual process

– Out-of-date when finalized

• Time consuming (3-6 months), expensive

• Focus is on detail data preparation and collection

• Heavy use of offline spreadsheets

• Becomes basis for comparison/variance

– Basis for compensation (bonuses)

– Relevant to today

• Authorization to spend – “It’s in my budget”

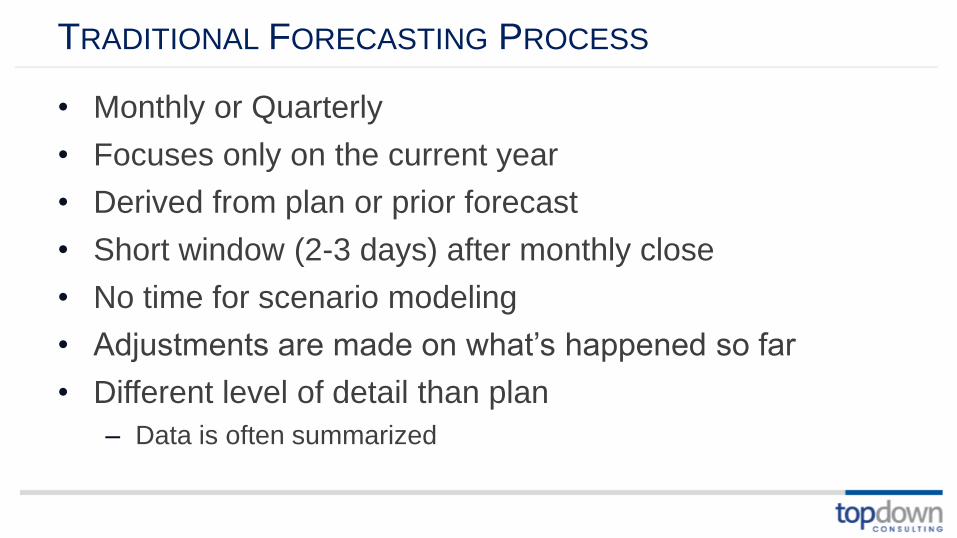

TRADITIONAL FORECASTING PROCESS

• Monthly or Quarterly

• Focuses only on the current year

• Derived from plan or prior forecast

• Short window (2-3 days) after monthly close

• No time for scenario modeling

• Adjustments are made on what’s happened so far

• Different level of detail than plan

– Data is often summarized

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Jan Fcst

Feb Fcst

Mar Fcst

Apr Fcst

May Fcst

Jun Fcst

Jul Fcst

Aug Fcst

Sep Fcst

Oct Fcst

Nov Fcst

Dec Fcst

FY15

Forecast

Actual

FY16

TRADITIONAL FORECASTING PROCESS

SO WHAT’S THE PROBLEM?

LOOKING FORWARD WITH ROLLING FORECASTS

A rolling forecast creates an ongoing cycle of planning, conducting,

evaluating and updating organization-wide operations.

Source: Rolling Forecast Solutions – Five Core Components of a Rolling Forecast, 2011

FIVE CORE COMPONENTS OF A ROLLING FORECAST

• Extends beyond the calendar/fiscal year and covers a

standard number of periods

• Updates on a regular and pre-determined basis

• Emphasizes key business drivers

• Rapid forecast creation

• Blends actual performance along with the updated

forecast

Source: Rolling Forecast Solutions – Five Core Components of a Rolling Forecast, 2011

WHAT IS A ROLLING FORECAST?

• More fluid approach to planning and forecasting

– If you are doing this, may not need to do a typical annual plan

• Emphasizes the forward movement of the business

– Always looking ahead 12, 18, or 24 months

– No cliff event like end-of-year

• Focus on what you manage

– Not what you transact

• Continuous process

– Combines traditional plan and forecast

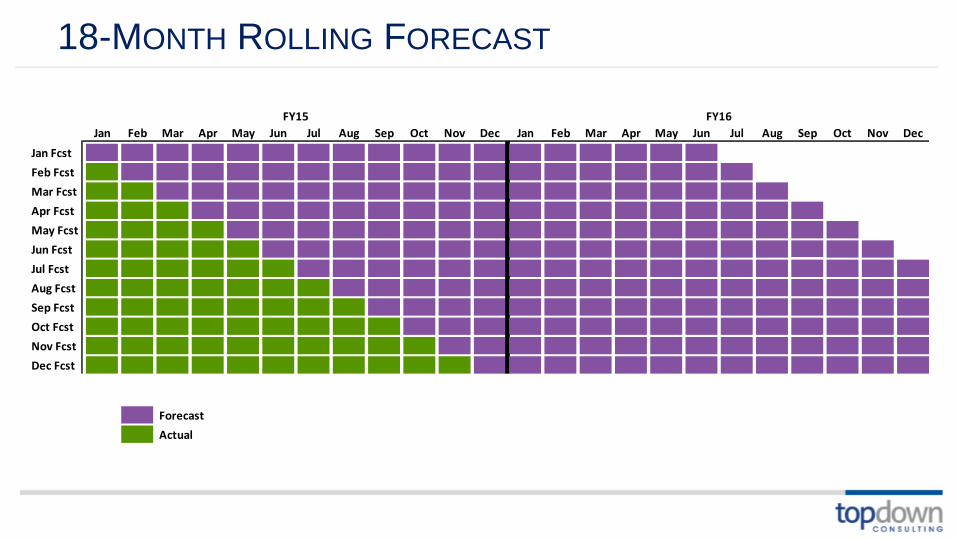

18-MONTH ROLLING FORECAST

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Jan Fcst

Feb Fcst

Mar Fcst

Apr Fcst

May Fcst

Jun Fcst

Jul Fcst

Aug Fcst

Sep Fcst

Oct Fcst

Nov Fcst

Dec Fcst

FY15 FY16

Forecast

Actual

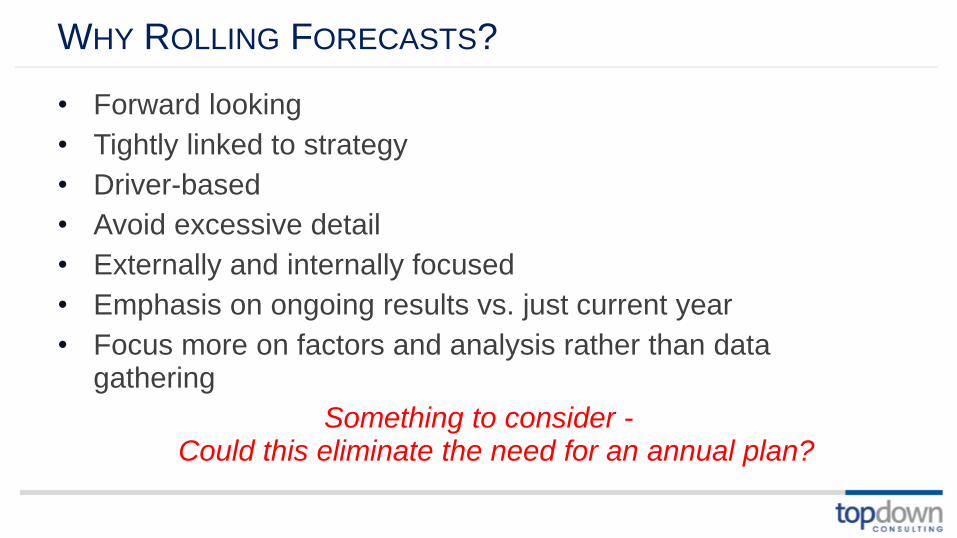

WHY ROLLING FORECASTS?

• Forward looking

• Tightly linked to strategy

• Driver-based

• Avoid excessive detail

• Externally and internally focused

• Emphasis on ongoing results vs. just current year

• Focus more on factors and analysis rather than data gathering

Something to consider -Could this eliminate the need for an annual plan?

18-MONTH ROLLING FORECAST

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Jan Fcst

Feb Fcst

Mar Fcst

Apr Fcst

May Fcst

Jun Fcst

Jul Fcst

Aug Fcst

Sep Fcst

Oct Fcst

Nov Fcst

Dec Fcst

FY15 FY16

Forecast

Actual

HOW IS THIS DIFFERENT?

• More proactive approach to managing the business

– Perpetually forecasting (rolling fashion)

– Improved view beyond current year

• Synchronized with the business

– Process, metrics, etc.

• Less work once implemented

– Reduced cost of doing business

– Less burnout

– Free up time for other activities

– Allows for better analytical decisions

• Operations should be actively involved

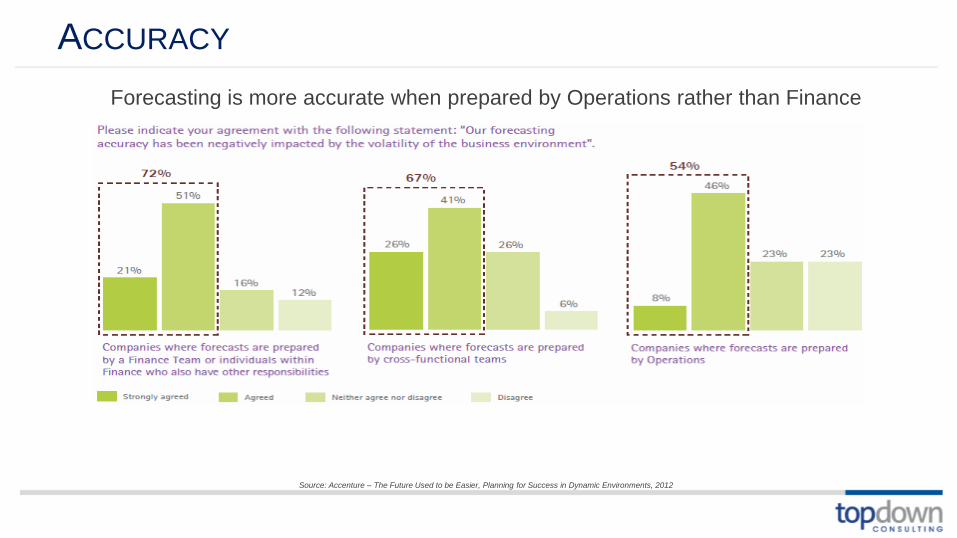

ACCURACY

Forecasting is more accurate when prepared by Operations rather than Finance

Source: Accenture – The Future Used to be Easier, Planning for Success in Dynamic Environments, 2012

PLANNING & FORECASTING LEADING PRACTICES

Leading Practices Benefits

• Align budgeting and forecasting with company strategy –

targets are set by management and cascaded across the

organization for budgeting/forecasting

• Don't burden with excessive detail – "false precision" slows

the process, and reduces the value to be realized through

frequent scenario iteration

• View planning as a continuous, iterative process to guide

business decision-making, not as a once-a-year

administrative exercise – rolling forecasts are one way to do

this

• Utilize "driver-based" logic wherever possible throughout the

planning process – build explicit links between external

forces, operational activities and the resulting financial

performance

• Utilize purpose-built planning tools to support rapid iteration

of complex, multi-dimensional models that are consistent

across business units/groups

• Creates a stronger linkage between the Strategic Plan, the

key targets and the operation of the business

• Provides organization with better ability to react to market

conditions

• Better focus on the review of key drivers of financial results

and influencing those drivers going forward

• Allows for continuous adjustments to planning

assumptions, rather than an annual review

• Improves communication within the business, about the

business, and its tactical and strategic areas of focus

• Increases management accountability for results

• Rolling forecast provides a view into the budget for the next

year

• Less time is spent on developing the detailed budget

• More time can be spent considering the operational

initiatives from the strategic plan

• Allows organization to focus on the analysis efforts not on

process

IMPLEMENTING A ROLLING FORECAST

KEY QUESTIONS TO ASK

• Evaluate how to improve current processes

– How did our current planning and forecasting process evolve over time?

– What do we like/dislike about the current process?

– What frequency – Monthly or Quarterly?

• Understand organizational direction

– Where are we going as a business?

• Determine what information you need to manage, and how you want to measure it

– What’s important to us?

– Does this align with our corporate goals and objectives?

• Do we have the time and resources to prepare plans/forecasts on a more frequent basis?

DECISION AND CRITERIA

• Timing of the implementation

• What resources do you need

– IT support

– Temps for data entry and validation

– New hardware

• Level of detail needed

– Consistency across organization?

– What can you control or influence?

• Choose the right solution

– On-Premise, Hosted, or Cloud

– Spreadsheet-based

WHERE EXCEL FALLS SHORT

• No proper version control

– Are all spreadsheets the correct versions?

• For every 150 lines in your forecasting model there is a 90% chance of a logic error

• Lack of robustness

– Can a CFO be confident in the numbers from an Excel forecast?

• Cannot accommodate changes to assumptions quickly

– how could you cope if the CEO asked “what is the financial impact of stopping production of line x?”

• Designed by staff who are not programmers, nor have been trained in documentation, quality assurance or other vital skills for a core business system

Source: Rolling Forecast Solutions – Five Core Components of a Rolling Forecast, 2011

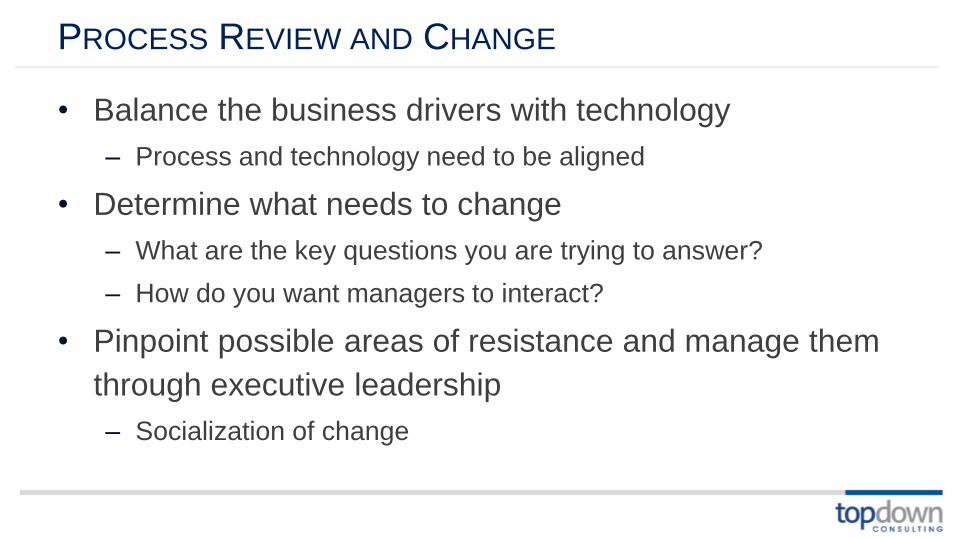

PROCESS REVIEW AND CHANGE

• Balance the business drivers with technology

– Process and technology need to be aligned

• Determine what needs to change

– What are the key questions you are trying to answer?

– How do you want managers to interact?

• Pinpoint possible areas of resistance and manage them

through executive leadership

– Socialization of change

COMMON CHALLENGES

• Initial set up is labor intensive

• Resistance to change

– People are always resistant to change

– Perception that Driver-based not as accurate/detailed

• Costs associated with change

– Software & support

• Existing data

– It’s never as clean as you think

• Training, testing and parallels

KEYS TO SUCCESS

• Executive sponsor must be the “change sponsor”

• Define and socialize the process (who, what, and how)

• Change Management – Change takes time

– Adoption is acceptance and participation

– Identify areas of resistance

• Determine level of detail

– What are you responsible for?

– What can you control?

• Driver-based models

– Focus on key elements (drivers) impacting the business

– Minimizes data entry

– Ability to model different scenarios (Best/Worst case)

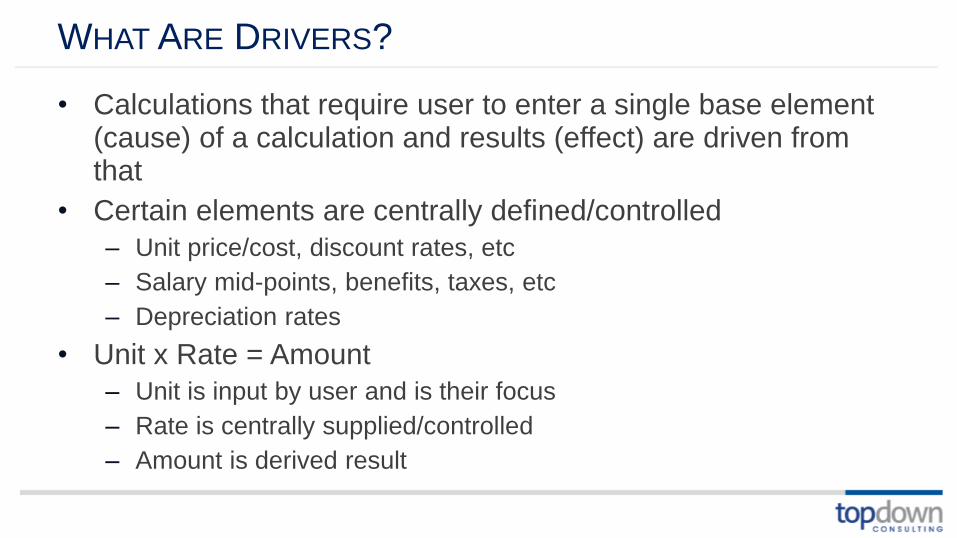

WHAT ARE DRIVERS?

• Calculations that require user to enter a single base element (cause) of a calculation and results (effect) are driven from that

• Certain elements are centrally defined/controlled

– Unit price/cost, discount rates, etc

– Salary mid-points, benefits, taxes, etc

– Depreciation rates

• Unit x Rate = Amount

– Unit is input by user and is their focus

– Rate is centrally supplied/controlled

– Amount is derived result

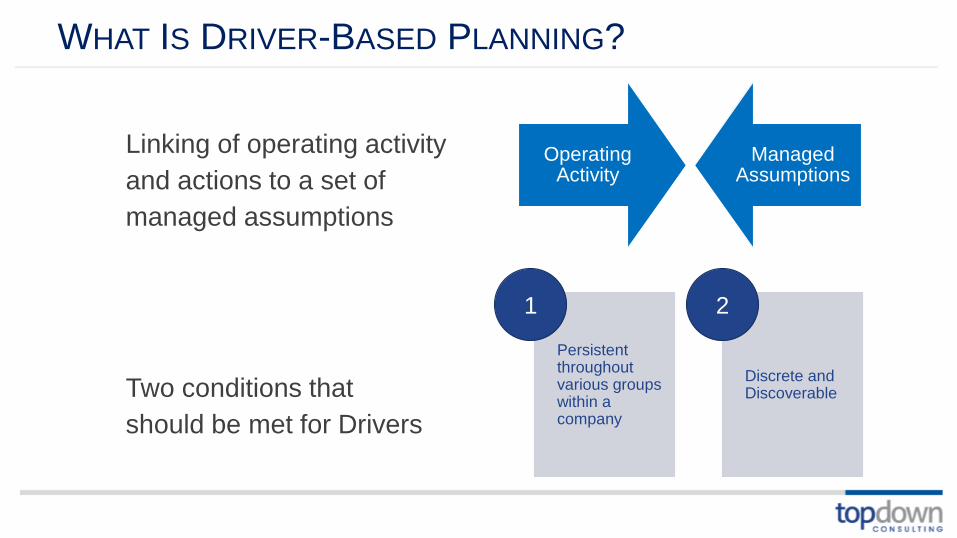

WHAT IS DRIVER-BASED PLANNING?

Linking of operating activity

and actions to a set of

managed assumptions

Two conditions that

should be met for Drivers

Operating Activity

Managed Assumptions

Persistent throughout various groups within a company

Discrete and Discoverable

1 2

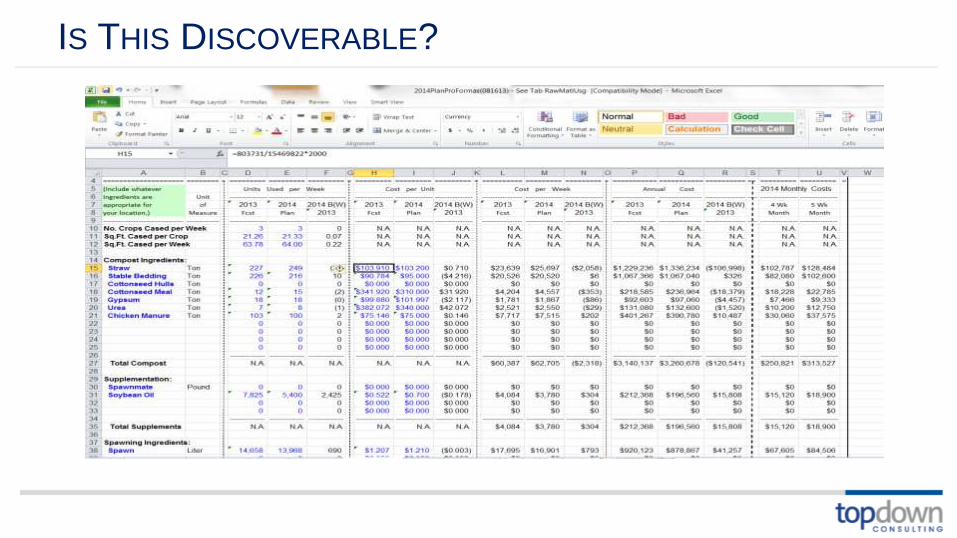

IS THIS DISCOVERABLE?

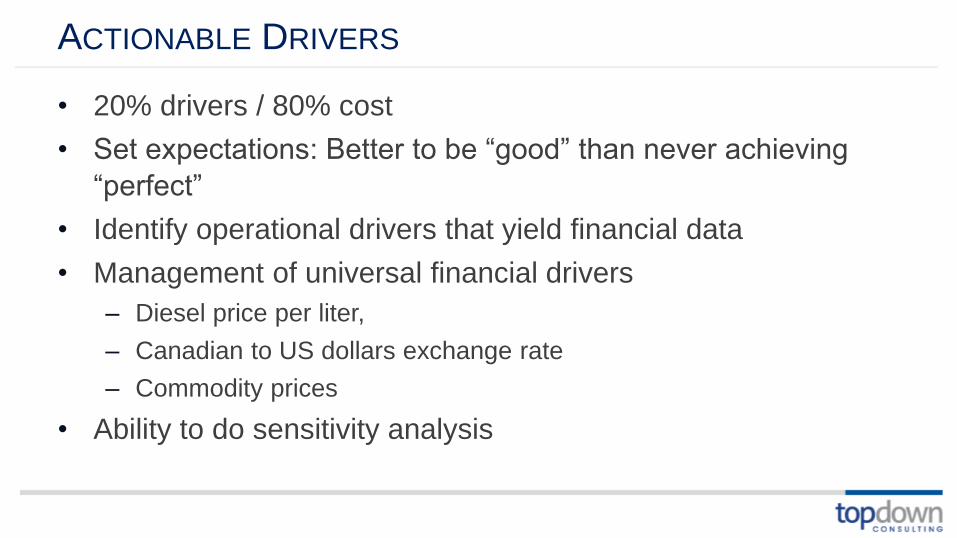

ACTIONABLE DRIVERS

• 20% drivers / 80% cost

• Set expectations: Better to be “good” than never achieving

“perfect”

• Identify operational drivers that yield financial data

• Management of universal financial drivers

– Diesel price per liter,

– Canadian to US dollars exchange rate

– Commodity prices

• Ability to do sensitivity analysis

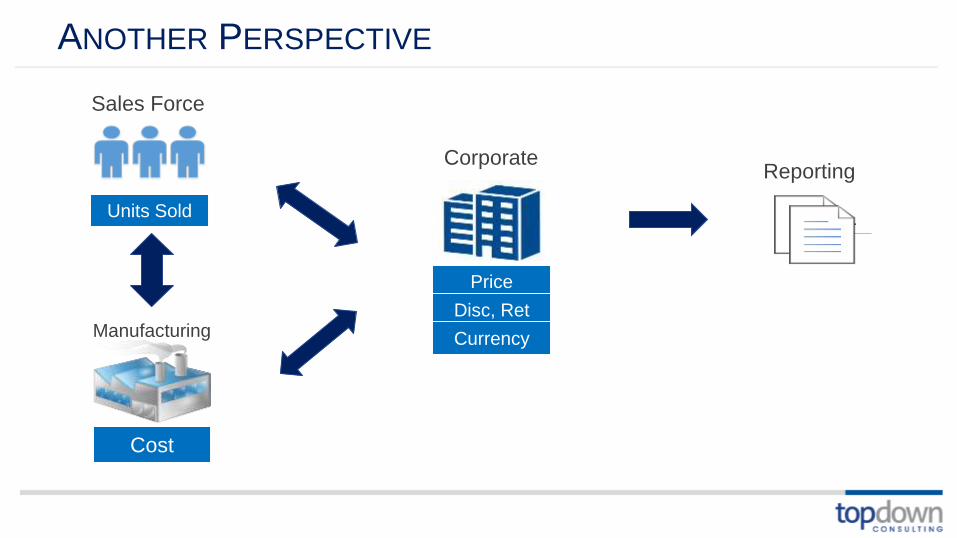

REVENUE/COST BASED DRIVERS

• Drivers set by Corporate or LoB

– Unit Price and Cost

– Discounts, Returns, DiF, etc

– Currency dependencies

• Units sold are input by users

• Strategically link Sales and Manufacturing

– Total units sold has an impact on cost basis

– Improves Finance’s visibility and modeling

Units Sold

Price

Cost

Sales

CoS

Disc, Ret Revenue

ANOTHER PERSPECTIVE

ReportingCorporate

Cost

Units Sold

Sales Force

Manufacturing

Price

Disc, Ret

Currency

EMPLOYEE-BASED DRIVERS

• Drivers set by Corporate or LoB

– Salary levels by grade or position

– Benefits and Payroll Tax rates

– Currency dependencies

• New Hires are input by users

• Focus on type of resource and when to hire

– Improves modeling of different hiring plans

New Hire• Position

• Date

Grade

Mid-point

Benefit

Rate

Salary

Expense

Benefit

Expense

Payroll

Tax Rate

Payroll

Taxes

Grade

Mid-point

Benefit

Rate

Salary

Expense

Benefit

Expense

Payroll Tax

Rate

Payroll

Taxes

Facility

Expense

PC

Purchase

Office

Space

Capital

Expense

Facility

Allocation

Depr

Rate

Depr

Expense

Recruiter

Fee

Recruiting

Expense

EMPLOYEE-BASED – ADVANCED DRIVERS

New Hire• Position

• Date

EXAMPLES OF DRIVERS

• Average Selling Price

• Discounts, Returns

• Average Cost per Unit

• Salary Grade Mid-Point

• Commission rate

• Merit Increase

• Annual Increase

• FICA, FUTA, SUTA

• State Unemployment

• Health Benefit

• Memberships

• 401K Contribution

• Stock Options

• Capital Purchases

• Depreciation

• Square Footage

• Country specific

• LoB specific

MEASURING WHAT YOU NEED TO MANAGE

UNDERSTANDING THE FORECAST

• Basis for variance analysis

– Communicate what is being measured

– Focus should be on what can be controlled, not just raw $’s

• Understand why there is a variance

– Track and store comments / explanations

– Visibility into assumptions and dependencies

• Don’t make currency the issue

– Local currency based

– Constant rate based

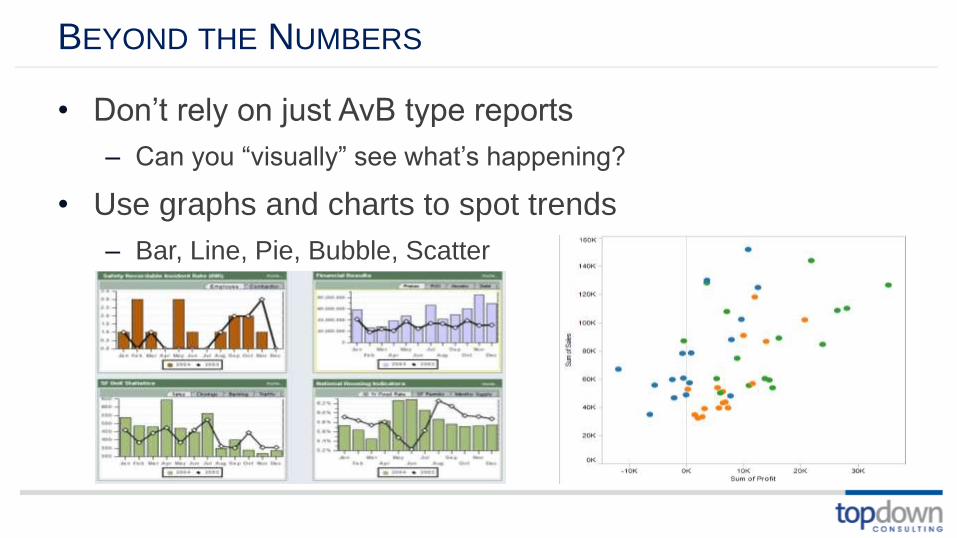

BEYOND THE NUMBERS

• Don’t rely on just AvB type reports

– Can you “visually” see what’s happening?

• Use graphs and charts to spot trends

– Bar, Line, Pie, Bubble, Scatter

– Easier to identify contribution

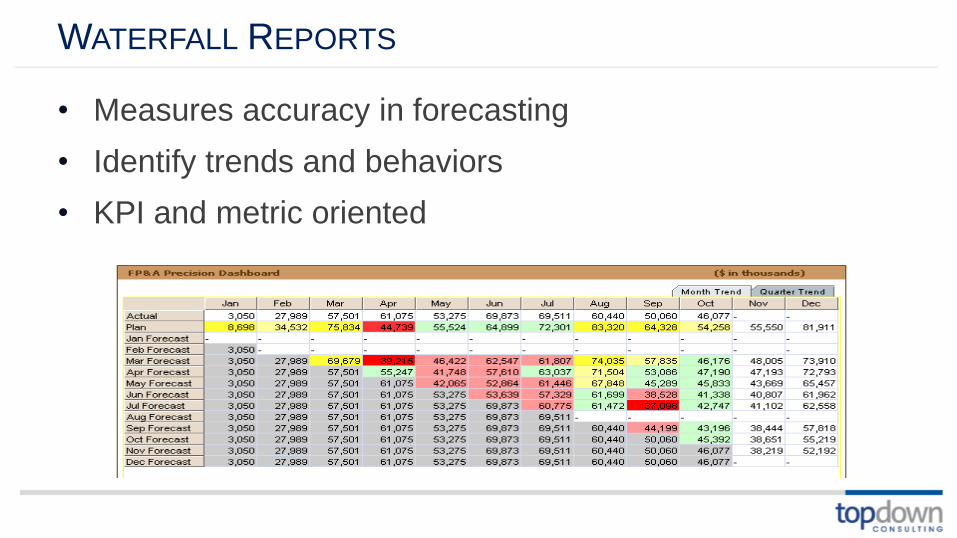

WATERFALL REPORTS

• Measures accuracy in forecasting

• Identify trends and behaviors

• KPI and metric oriented

ADDITIONAL CONSIDERATIONS

ADDITIONAL CONSIDERATIONS

• Change Management

– Users need to understand benefits

• Impact of multiple years on calculations/drivers

• Transition of new hires to employees

• New capital purchases included in depreciation forecast

• Parallel the process

– Balance this with other ongoing initiatives

– Take the time for adoption of the process

• Integration with other processes

– Monthly Close

– Strategic / Long-Range Plan

© Copyright 2016 TopDown Consulting, Incorporated. All Rights Reserved.

Juan Porter

Chief Solutions Officer & Founder

(415) 860-1115