contents - kopykitab · pdf file6 vouching 89 7 verification and ... bills payable secured...

TRANSCRIPT

2

CONTENTS Sr. No. Title Page No.

SECTION - I (AUDITING)

1 Introduction To Auditing 01

2 Introduction To Auditing II 22

3 Audit Planning 33

4 Auditing Techniques And Internal Audit Introduction I 44

5 Internal Control 54

6 Vouching 89

7 Verification And Valuation Of Assets And Liabilities 106

8 Introduction To Company Audit 169

SECTION - II (COST ACCOUNTING)

9 Cost Accounting 173

10 Cost and Cost Classification - Cost Sheet 187

11. Reconcilation of Profit as per Cost and Financial Accounts 204

12. Material, Labour and Overheads 221

13. Method of Costing 237

14. Elementary Principles and Techniques of Marginal

and Standard Costing 267

���

3

SYLLABUS TY.B.COM,

FINANCIAL ACCOUNTING AND AUDITING PAPER - IV (AUDITING AND COST ACCOUNTING)

SECTION - 1 AUDITING

1. Introduction to Auditing

1.1 Basics Financial Statements, Users of Financial Information,

Definition of, Auditing, Objectives of Auditing - Primary &

Secondary , Expression of opinion, Detection of Frauds &

Errors, Inherent limitations of Audit

1.2 Errors and Frauds Definition, Reasons & Circumstances, Types of Errors -

Commission, Omission, Principle & Compensating, Types of Frauds, Risk of fraud & Error Audit, Auditors Duties &

Responsibilities in respect of fraud.

1.3 Principles of Audit Integrity, Objectivity ,& Independence, Confidentiality, skills &

Competence, Work Performed by Others, Documentation, Planning, Audit Evidence, Accounting System & internal

Control, Audit Conclusions & Reporting

1.4 Audit Types Meaning , Advantages & Disadvantages of Balance sheet

Audit, j nterirn Audit, Continuous Audit, Concurrent Audit,

Annual Audit

1.5 Miscellaneous

Advantages of Independent Audit, Qualities of Auditors, Auditing BS Accounting, Aduting Vs Investigation, True and Fair

1.6 Accounting Concepts relevant to auditing Materiality, Going

Concern

2. Audit Planning, procedures and Documentation

2.1 Audit Planning Meaning, Objectives, Factors to be considered, Sources of

obtaining information, Discussions with Client, Overall Audit

Plan

2.2 Audit Programme Meaning, Factors .Advar tages, Disadvantages, Overcoming

Disadvantages, Methods of Work , Instruction before commencing work, Overall Audit Approach

2.3 Audit working Papers Meaning, importance, Factors determining Form & Contents,

Main Functions / Importance, Features,Contents of Permanent Audit File, Temporary Audit File , Ownership, Custody, Access of Othor Parties to Audit Working Papers,

4

Auditors Lien on Working Papers, Auditors Lien on Client’s

Books

2.4 Audit notebook Meaning Structure, Contents, General Information Current Information Importance.

3. Auditing Techniques and Internal Audit introduction

3.1 Test Check Test Checking Vs Routing Checking, test factors to be

considered, when Test Che advantages disadvantages

precautions heck meaning, lectures, ks can be used,

3.2 Audit Sampling Audit Sampling, meaninc , purpose, factors in determining

sample size -Sampling Risk, Tolerobie Error & expected

error, methods of selecting Sample Items Evaluation of Sample Results auditors Liability in conducting

audit based on Sample

3.3 Internal control Meaning & purpose, reviovv of internal control, advantages,

auditors duties, review of internal control. Inherent limitations

of Internal control, internal control samples for sales &

debtors, purchases & eredilors, wages & salaries

3.4 Internal Checks Vs Internal Control ,Internal Checks Vs Test

Checks

3.5 Internal audit Meaning, basic principles of establishing Internal audit, ob

ectives, evaluation of internal Audit by statutory auditor, usefulness of Internal Audit, Internal Audit Vs External Audit, , Internal Checks Vs Internal Audit

4. Auditing Techniques :- vouching

4.1 Vouching

4.2 Audit of Income Cash Sales, Sales on Approval, Consignment Sales, Sales

Returns Recovery of Bad Debts written off, Rental Receipts,

Interest & Dividends Received Royalties Received.

4.3 Audit of Expenditure Purchases, Purchase Returns, Salaries & Wages, Rent, Insurance Premium, Telephone expense

Postage & Courier .Petty Cash Expenses, Traveling

Commission Advertisement, Interest Expense

5. Auditing Techniques:- verification

5.1 Audit of assets Book Debts/Debtors, Stocks-Auditors General Duties,

Patterns, Dies & Loose Tools,Spare Parts,Empties &

Containers Quoted Investments and Unquoted Investment Trade Marks /

Copyrights Patents Know-How Plant & Machinery Land &

Buildings Furniture & Fixtures

5

5.2 Audit of Liabilities

Outstanding Expenses, Bills Payable Secured locns Unsecured Loans Contingent Liabilities

6 Introduction to Company Audit

Qualifications, Disqualifications , appointments, reappointments and removal of auditors

Qualifications, Disqualifications Appointments- First and subsequent auditors Reappointment Removal of auditor

������������

Section II - Cost Accounting

1. Introduction to Cost Accounting (a) Objectives and scope of Cost Accounting (b) Cost centers and Cost units (c) Cost classification for stock valuation, Profit

measurement, Decision making and control (d) Coding systems (e) Elements of Cost (f) Cost behavior pattern, Separating the components of

se.mi- variable costs.

2. Cost Ascertainment

2.1 Material Cost (i) Procurement procedures— Store procedures and

documentation in respect of receipts and issue of stock, Stock verification

(ii) Inventory control —Techniques of fixing of minimum, maximum and reorder levels, Economic Order Quantity, ABC classification; Stocktaking and perpetual inventory

(iii) Inventory accounting

2.2 Labour Cost . (i) Attendance and payroll procedures, Overview of statutory

requirements, Overtime, Idle time and. Incentives (ii) Labour turnover (iii) Utilisation of labour, Direct and indirect labour, Charging

of labour cost, Identifying labour hours with work orders or batches or capital jobs

(iv) Efficiency rating procedures (v) Remuneration systems and incentive schemes

2.3 Overheads Functional analysis — Factory, Administration, Selling,

Distribution, Behavioural analysis — Fixed, Variable, Semi variable cost

Note:- No practical problems on material, labour, overheads

6

3. Cost Book-keeping Reconciliation of cost and financial accounts. Note:- Practical problems based on reconciliation of cost

and financial accounts

4. Costing Systems

4.1 Job and batch costing Job cost cards and databases, Collecting direct costs of each

job, Attributing overhead costs to jobs, Applications of job costing.

4.2 Contract Costing Progress payments, Retention money, Contract accounts,

Accounting for material, Accounting for Tax deducted at source by the contractee, Accounting for plant used in a contract, treatment of profit on incomplete contracts, Contract profit and Balance sheet entries. Excluding Escalation clause

4.3 Process Costing Process loss, Abnormal gains and losses, Joint products and

by products. Excluding Equivalent units, Inter-process profit Note:- Practical problems based on cost sheet, Process Costing and Contract Costing

5. Introduction to Marginal Costing Marginal costing meaning, application, advantages,

limitatations, Contribution, Breakeven analysis and profit volume graph. Note:-Simple Practical problems based on Marginal Costing excluding decision making.

6. Introduction to Standard Costing Various types of standards, Setting of standards, Basic

concepts of material and Labour variance analysis.

Note:-Simple Practical problems based on Material and labour variances excluding sub variar.cas and overhead variances.

������������

9

1 SECTION-1 (AUDITING)

INTRODUCTION TO AUDITING STRUCTURE: 1.1 Objectives 1.2 Introduction -an overview of auditing 1.3 Origin and evolution 1.4 Definition 1.5 Salient features 1.6 Scope of auditing 1.7 Principles of auditing 1.8 Objects of audit 1.9 Detection and prevention of fraud 1.2 1.10 Concept of " true and fair view" 1.11 Advantages of audit 1.12. Limitations of audit 1.13. Let us sum up. 1.14. Keywords. 1.15. Bibliography

1.1 OBJECTIVES After studying this unit you will be able to understand a. the evolution of auditing b. the objects of auditing c. the advantages and disadvantages of auditing d. detection and prevention of frauds and errors e. limitations of auditing

1.2 INTRODUCTION -AN OVERVIEW OF AUDITING:

Economic decisions in every society must be based upon the information available at the time the decision is made. For example, the decision of a bank to make a loan to a business is based upon previous financial relationships with that business, the financial

10

condition of the company as reflected by its financial statements and other factors.

If decisions are to be consistent with the intention of the decision makers, the information used in the decision process must be reliable. Unreliable information can cause inefficient use of resources to the detriment of the society and to the decision makers themselves. In the lending decision example, assume that the barfly makes the loan on the basis of misleading financial statements and the borrower Company is ultimately unable to repay. As a result the bank has lost both the principal and the interest. In addition, another company that could have used the funds effectively was deprived of the money.

As society become more complex, there is an increased likelihood that unreliable information will be provided to decision makers. There are several reasons for this: remoteness of information, voluminous data and the existence of complex exchange transactions.

As a means of overcoming the problem of unreliable information, the decision-maker must develop a method of assuring him that the information is sufficiently reliable for these decisions. In doing this he must weigh the cost of obtaining more reliable information against the expected benefits.

A common way to obtain such reliable information is to have some type of verification (audit) performed by independent persons. The audited information is then used in the decision making process on the assumption that it is reasonably complete, accurate and unbiased.

1.3 ORIGIN AND EVOLUTION

The term audit is derived from the Latin term ‘audire,’ which means to hear. In early days an auditor used to listen to the accounts read over by an accountant in order to check them

Auditing is as old as accounting. It was in use in all ancient countries such as Mesopotamia, Greece, Egypt. Rome, U.K. and India. The Vedas contain reference to accounts and auditing. Arthasashthra by Kautilya detailed rules for accounting and auditing of public finances.

The original objective of auditing was to detect and prevent errors and frauds

Auditing evolved and grew rapidly after the industrial revolution in the 18th century With the growth of the joint stock companies the ownership and management became separate. The

11

shareholders who were the owners needed a report from an independent expert on the accounts of the company managed by the board of directors who were the employees.

The objective of audit shifted and audit was expected to ascertain whether the accounts were true and fair rather than detection of errors and frauds.

In India the companies Act 1913 made audit of company accounts compulsory

With the increase in the size of the companies and the volume of transactions the main objective of audit shifted to ascertaining whether the accounts were true and fair rather than true and correct. Hence the emphasis was not on arithmetical accuracy but on a fair representation of the financial efforts

The companies Act.1913 also prescribed for the first time the qualification of auditors

The International Accounting Standards Committee and the Accounting Standard board of the Institute of Chartered Accountants of India have developed standard accounting and auditing practices to guide the. accountants and auditors in the day to day work

The later developments in auditing pertain to the use of computers in accounting and auditing.

In conclusion it can be said that auditing has come a long way from hearing of accounts to taking the help of computers to examine computerised accounts

1.4 DEFINITION The term auditing has been defined by different authorities. 1. Spicer and Pegler: "Auditing is such an examination of books

of accounts and vouchers of business, as will enable the auditors to satisfy himself that the balance sheet is properly drawn up, so as to give a true and fair view of the state of affairs of the business and that the profit and loss account gives true and fair view of the profit/loss for the financial period, according to the best of information and explanation given to him and as shown by the books; and if not, in what respect he is not satisfied."

2. Prof. L.R.Dicksee. "auditing is an examination of accounting

records undertaken with a view to establish whether they

12

correctly and completely reflect the transactions to which they relate.

3 The book "an introduction to Indian Government accounts

and audit" "issued by the Comptroller and Auditor General of India, defines audit “an instrument of financial control. It acts as a safeguard on behalf of the proprietor (whether an individual or group of persons) against extravagance, carelessness or fraud on the part of the proprietor's agents or servants in the realization and utilisation of the money or other assets and it ensures on the proprietor's behalf that the accounts maintained truly represent facts and that the expenditure has been incurred with due regularity and propriety. The agency employed for this purpose is called an auditor."

1.5 FEATURES OF AUDITING a. Audit is a systematic and scientific examination of the books of

accounts of a business; b. Audit is undertaken by an independent person or body of

persons who are duly qualified for the job. c Audit is a verification of the results shown by the profit and

loss account and the state of affairs as shown by the balance sheet.

d. Audit is a critical review of the system of accounting and

internal control. e. Audit is done with the help of vouchers, documents,

information and explanations received from the authorities. f. The auditor has to satisfy himself with the authenticity of the

financial statements and report that they exhibit a true and fair view of the state of affairs of the concern.

g The auditor has to inspect, compare, check, review, scrutinize

the vouchers supporting the transactions and examine correspondence, minute books of share holders, directors, Memorandum of Association and Articles of association etc., in order to establish correctness of the books of accounts.

1.6 OBJECTIVES OF AUDITING There are two main objectives of auditing. The primary objective and the secondary or incidental objective. a. Primary objective – as per Section 227 of the Companies Act

1956, the primary duty (objective) of the auditor is to report to

13

the owners whether the balance sheet gives a true and fair view of the Company’s state of affairs and the profit and loss A/c gives a correct figure of profit of loss for the financial year.

b. Secondary objective – it is also called the incidental objective

as it is incidental to the satisfaction of the main objective. The incidental objective of auditing are: i. Detection and prevention of Frauds, and ii. Detection and prevention of Errors.

Detection of material frauds and errors as an incidental objective of independent financial auditing flows from the main objective of determining whether or not the financial statements give a true and fair view. As the Statement on auditing Practices issued by the Institute of Chartered Accountants of India states, an auditor should bear in mind the possibility of the existence of frauds or errors in the accounts under audit since they may cause the financial position to be mis-stated. Fraud refers to intentional misrepresentation of financial information with the intention to deceive. Frauds can take place in the form of manipulation of accounts, misappropriation of cash and misappropriation of goods. It is of great importance for the auditor to detect any frauds, and prevent their recurrence. Errors refer to unintentional mistake in the financial information arising on account of ignorance of accounting principles i.e. principle errors, or error arising out of negligence of accounting staff i.e. Clerical errors.

1.7 EXPRESSION OF OPINION When we speak of the objective, we rationalize the thinking process to formulate a set of attainable goals, with reference to the circumstances, feasibility and constraints. In money matters, frauds and errors are common place of occurrence. Apart from this, the statements of account have their own purpose and use of portraying the financial state of affairs. The objective of audit, naturally, should be to see that what the statements of account convey is true and not misleading and that such errors and frauds do not exists as to distort what the accounts should really convey. Till recently, the principal emphasis was on arithmetical accuracy; adequate attention was not paid to appropriate application of accounting principles and disclosure, for ensuring preparation of accounting statement in such a way as to enable the reader of the accounting statement to form a correct view of the slate of affairs. Quite a few managements took advantage of the situation and manipulated profit or loss and assets and liabilities to highlight or conceal affairs according to their own design. This state of affairs came up for consideration in the Royal Mail Steam Packet Company’s Case as a result of which the Companies Acts of England and India were amended in 1948 and 1956 respectively to

14

require the auditor to state inter alia whether the statements of account are true and fair. This is what we can take as the present day audit objective. The implication of the substitution of “true and fair” need to be understood. There has been a shift of emphasis from arithmetical accuracy to the question of reliability to the financial statements. A statement may be reliable even though there are some errors or even frauds, provided they are not so big as to vitiate the picture. The word “correct” was somewhat misplaced as the accounting largely consists of estimates. However, you should not infer that the detection of errors and frauds is no longer an audit objective; it is indeed an audit objective because statements of account drawn up from books containing serious mistakes and fraudulent entries cannot be considered as a true and fair statement. To establish whether the financial statement show a true and fair state of affairs, the auditors must carry out a process of examination and verification and, if errors and frauds exist they would come to his notice in the ordinary course of checking. But detection of errors of frauds is not the primary aim of audit; the primary aim is the establishment of a degree of reliability of the annual statements of account. If there remains a deep laid fraud in the accounts, which in the normal course of examination of accounts may not come to light, it will not be construed as failure of audit, provided the auditor was not negligent in the carrying out his normal work. This principle was established as early as in 1896 in the leading case in Re-Kingston Cotton Mills Co.

1.8 DETECTION OF FRAUD & ERRORS

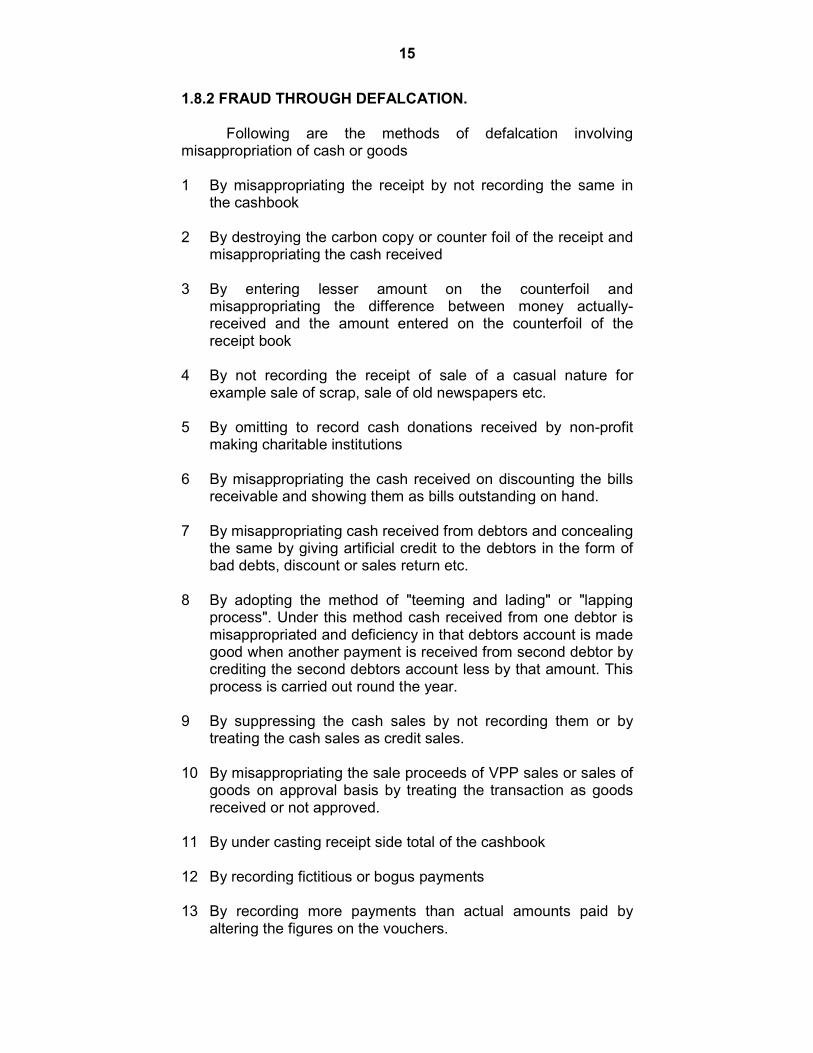

The term fraud means the willful misrepresentation made with an intention of deceiving others. It is a deliberate mistake committed in the accounts with a view to get personal gain. In accounting, fraud means two things. a. Defalcation involving misappropriation of either cash or goods;

and b. Fraudulent manipulation of accounts not involving defalcation. 1.8.1. FRAUD COVERS THE FOLLOWING

15

1.8.2 FRAUD THROUGH DEFALCATION.

Following are the methods of defalcation involving misappropriation of cash or goods 1 By misappropriating the receipt by not recording the same in

the cashbook 2 By destroying the carbon copy or counter foil of the receipt and

misappropriating the cash received 3 By entering lesser amount on the counterfoil and

misappropriating the difference between money actually-received and the amount entered on the counterfoil of the receipt book

4 By not recording the receipt of sale of a casual nature for

example sale of scrap, sale of old newspapers etc. 5 By omitting to record cash donations received by non-profit

making charitable institutions 6 By misappropriating the cash received on discounting the bills

receivable and showing them as bills outstanding on hand. 7 By misappropriating cash received from debtors and concealing

the same by giving artificial credit to the debtors in the form of bad debts, discount or sales return etc.

8 By adopting the method of "teeming and lading" or "lapping

process". Under this method cash received from one debtor is misappropriated and deficiency in that debtors account is made good when another payment is received from second debtor by crediting the second debtors account less by that amount. This process is carried out round the year.

9 By suppressing the cash sales by not recording them or by

treating the cash sales as credit sales. 10 By misappropriating the sale proceeds of VPP sales or sales of

goods on approval basis by treating the transaction as goods received or not approved.

11 By under casting receipt side total of the cashbook 12 By recording fictitious or bogus payments 13 By recording more payments than actual amounts paid by

altering the figures on the vouchers.

16

14 By showing the same payment twice. 15 By showing credit purchases as cash purchases and

misappropriating the amount 16 Recording personal expenses as business expenses 17 By not recording discounts and allowances given by the

creditors and misappropriating the amounts 18 By overcasting the payment side total of the cashbook 19 Recording fictitious and inflated purchases and

misappropriating that amount. 20 By suppressing the credit notes for returns and showing the full

payment to creditors. 21 By including the names of dummy workers or the workers who

have? The job in the wage sheets and misappropriating the amount.

22 By over casting the total of wages sheets and drawing that

amount for misappropriation. 23 By misappropriating the undisbursed wages. 1.8.3 FRAUD THROUGH MANIPULATION OF ACCOUNTS

It implies presentation of accounts more favorably than what they actually are. Window dressing means showing a wrong picture. The fraud through manipulation of accounts is also known as window dressing because accounts are manipulated to show a wrong picture of the profit or loss of the business and its financial state of affairs. Generally this type of fraud is committed by the people at the top management level. This does not involve any misappropriation of cash or goods but it is either over statement of profit or understatement of the same. Such fraud is committed with certain objective and is relatively difficult to detect.

1.8.4 THE AUDITOR CAN SUSPECT FRAUD UNDER THE FOLLOWING CIRCUMSTANCES. 1. When vouchers, invoices, cheques, contracts are missing etc. 2. When control account does not agree with subsidiary books. 3. When the difference in trial balance is difficult to locate. 4. When there are greater fluctuation in G.P. and N.P. ratios.