contemporary engineering economics, 4 th edition, © 2007 process of developing project cash flows...

Post on 21-Dec-2015

227 views

TRANSCRIPT

Process of Developing Project Cash Flows

Lecture No.38Chapter 10Contemporary Engineering EconomicsCopyright © 2006

Chapter Opening Story – New Incentives for Being Green Carrier corporation has

invested $250 million in developing a new energy efficient heat exchangers.

The expected retail price of the system unit is about $4,236.

The initial profit margin is about 7.45%, but there is no way of knowing how long Carrier will be able to sustain their desired profit margin.

Under this circumstance, any project’s justification depends upon the ability to estimate potential cash flows.

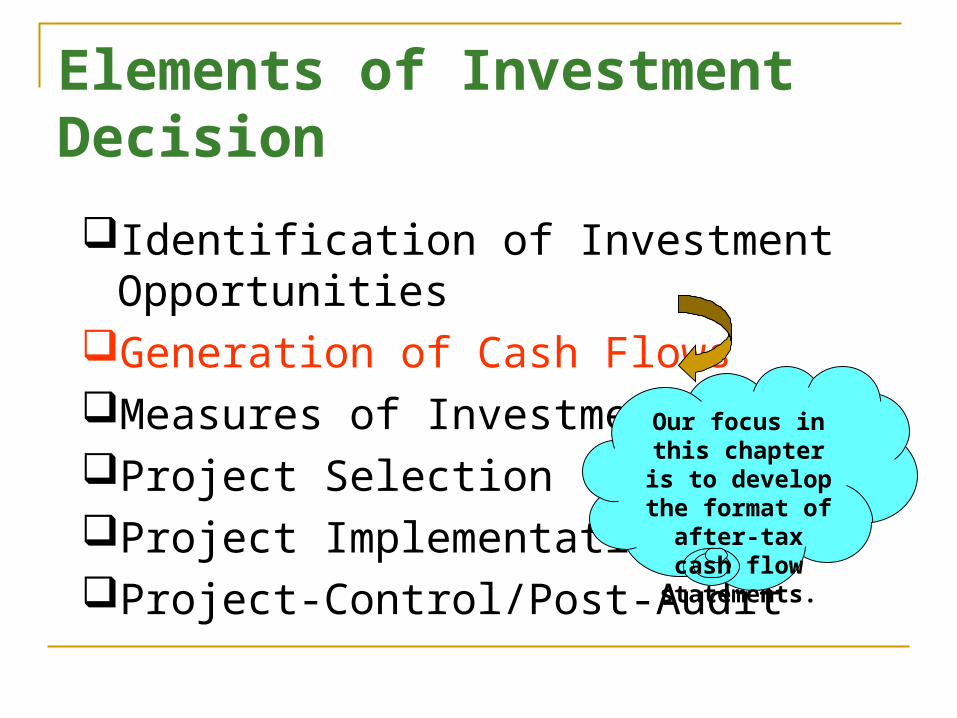

Identification of Investment OpportunitiesGeneration of Cash FlowsMeasures of Investment WorthProject SelectionProject ImplementationProject-Control/Post-Audit

Our focus in this chapter is to

develop the format of after-tax cash flow statements.

Elements of Investment Decision

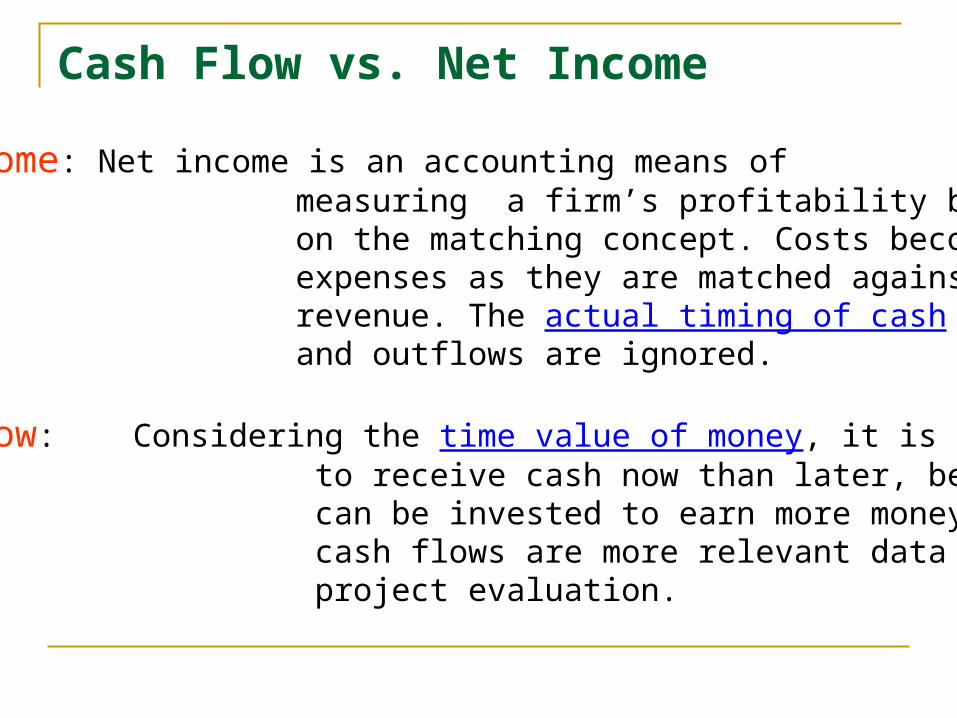

Net income: Net income is an accounting means of measuring a firm’s profitability based on the matching concept. Costs become expenses as they are matched against revenue. The actual timing of cash inflows and outflows are ignored.

Cash flow: Considering the time value of money, it is better to receive cash now than later, because cash can be invested to earn more money. So, cash flows are more relevant data to use in project evaluation.

Cash Flow vs. Net Income

Why Do We Use Cash Flow in Project Evaluation?

Company A Company B

Year 1 Net income

Cash flow

$1,000,000

1,000,000

$1,000,000

0

Year 2 Net income

Cash flow

1,000,000

1,000,000

1,000,000

2,000,000

Both companies (A & B) have the same amount of net income and cash sum over 2 years, but Company A returns $1 million cash yearly, while Company B returns $2 million at the end of 2nd year. Company A can invest $1 million in year1, while Company B has nothing to invest during the same period.

Gross IncomeExpenses Cost of goods sold (revenues) Depreciation Operating expensesTaxable incomeIncome taxesNet income

Item

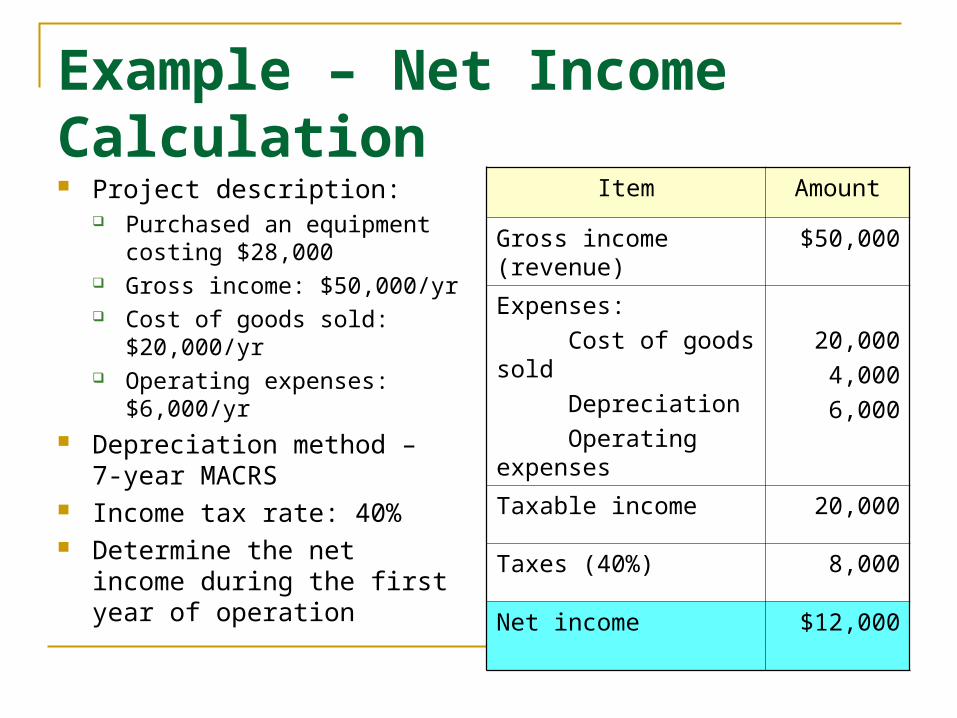

Net Income Calculation – A Starting Point of Cash Flow Estimation

Item Amount

Gross income (revenue) $50,000

Expenses:

Cost of goods sold

Depreciation

Operating expenses

20,000

4,000

6,000

Taxable income 20,000

Taxes (40%) 8,000

Net income $12,000

Example – Net Income Calculation Project description:

Purchased an equipment costing $28,000

Gross income: $50,000/yr Cost of goods sold: $20,000/yr Operating expenses: $6,000/yr

Depreciation method – 7-year MACRS

Income tax rate: 40% Determine the net income

during the first year of operation

01 2 3 4 5 6 7 8

0 87673 41 2

$4,000

$6,850$4,900

$3,500 $2,500 $2,500 $2,500$1,250

$28,000

Capital expenditure(actual cash flow)

Allowed depreciation expenses (not cash flow)

Capital Expenditure versus Depreciation Expenses

Item Income Cash Flow

Gross income (revenue $50,000 $50,000

Expenses

Cost of goods sold

Depreciation

Operating expenses

20,000

4,000

6,000

-20,000

-6,000

Taxable income 20,000

Taxes (40%) 8,000 -8,000

Net income $12,000

Net cash flow $16,000

Cash Flow versus Net Income

$0

$50,000

$40,000

$30,000

$20,000

$10,000

$8,000

$6,000

$20,000

Net income

Depreciation

Income taxes

Operating expenses

Cost of goods sold

Netcash flow

Grossrevenue

$4,000

$12,000

Net cash flows = Net income + non-cash expense (depreciation)

Estimating Net Cash Flow from Net Income

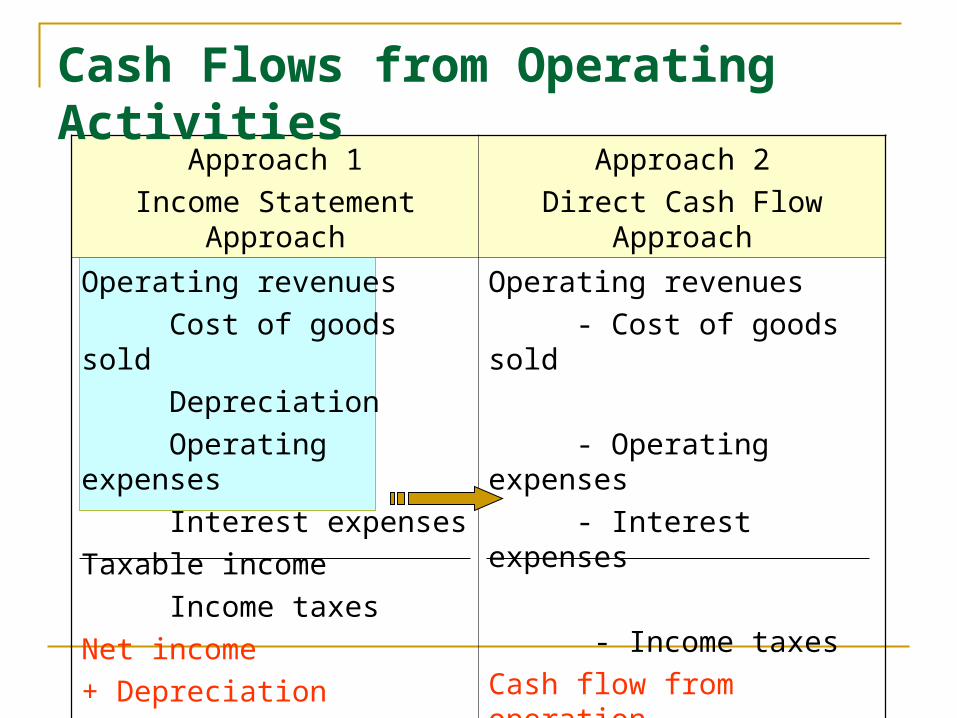

Types of Cash Flow Elements in Project Analysis

Approach 1

Income Statement Approach

Approach 2

Direct Cash Flow Approach

Operating revenues

Cost of goods sold

Depreciation

Operating expenses

Interest expenses

Taxable income

Income taxes

Net income

+ Depreciation

Operating revenues

- Cost of goods sold

- Operating expenses

- Interest expenses

- Income taxes

Cash flow from operation

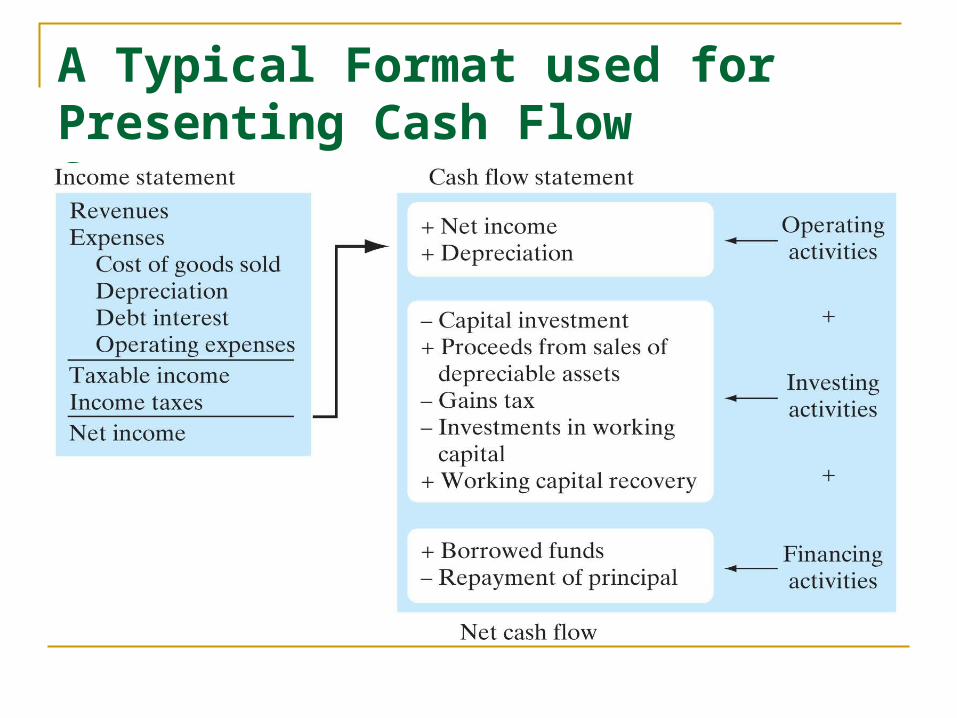

Cash Flows from Operating Activities

A Typical Format used for Presenting Cash Flow Statement