container port capacity study - savethecape.orgsavethecape.org/stcwp1/wp-content/uploads/pdfs/port...

TRANSCRIPT

The Tioga Group, Inc. 288 Rheem Blvd. Moraga, CA 94556 Phone 925.631.0742 Fax 925.631.7936

CONTAINER PORT CAPACITY STUDY

The Tioga Group, Inc.

Prepared for:

CDM/IWR

December 2, 2010

Page i

Tioga

Contents

I. SUMMARY 1

II. BACKGROUND AND APPROACH 8

III. NORTH ATLANTIC PORTS 24

IV. SOUTH ATLANTIC PORTS 65

V. GULF PORTS 104

VI. APPENDIX: SECONDARY CONTAINER PORTS 125

Page ii

Tioga

Exhibits

Exhibit 1: Major Ports Analyzed .................................................................................................................... 1

Exhibit 2: 2008 Port Utilization Summary ...................................................................................................... 2

Exhibit 3: Reserve Container Port Capacity by Coast .................................................................................. 3

Exhibit 4: Terminal Space and CY Utilization ............................................................................................... 3

Exhibit 5: 2008 TEU and CY TEU Capacity .................................................................................................. 4

Exhibit 6: Average TEU Slots per CY Acre ................................................................................................... 5

Exhibit 7: Container Cranes and Utilization .................................................................................................. 5

Exhibit 8: Berth and Vessel Capacity and Utilization .................................................................................... 6

Exhibit 9: Major Ports Analyzed .................................................................................................................. 10

Exhibit 10: Five "Dimensions" of Container Terminal Capacity .................................................................. 11

Exhibit 11: Container Vessel DWT vs. TEU Capacity ................................................................................. 13

Exhibit 12: Reported vs. Estimated Container Vessel TEU ........................................................................ 14

Exhibit 13: DWT vs. Draft ............................................................................................................................ 14

Exhibit 14: USACE Guidance on Cargo Capacity as a Percentage of DWT .............................................. 15

Exhibit 15: Maximum vs. Average Vessel Capacity - TEU ......................................................................... 15

Exhibit 16: Vessel Size and Load Comparison ........................................................................................... 16

Exhibit 17: Berth Capacity - Maximum Vessel Basis Example ................................................................... 17

Exhibit 18: Berth Capacity Estimate- Vessel Call Basis Example .............................................................. 17

Exhibit 19: Container Yard Handling Equipment Types .............................................................................. 18

Exhibit 20: Progression of Terminal Handling Methods .............................................................................. 18

Exhibit 21: Wheeled Containers on RTG Layout ........................................................................................ 19

Exhibit 22: Typical CY Storage Densities ................................................................................................... 20

Exhibit 23: CY Acreage Example: Port of New Orleans ............................................................................. 20

Exhibit 24: CY Capacity Example: Port of New Orleans ............................................................................. 21

Exhibit 25: Typical Two-Berth/Four-Crane Terminal ................................................................................... 23

Exhibit 26: Container Cranes and Utilization .............................................................................................. 23

Exhibit 27: North Atlantic Capacity and Utilization Summary ..................................................................... 24

Exhibit 28: North Atlantic Drafts and Vessel Data ...................................................................................... 25

Exhibit 29: Port of Boston Conley Container Terminal ............................................................................... 25

Exhibit 30: Conley Container Terminal Profile ............................................................................................ 26

Exhibit 31: Conley Terminal Land Use ........................................................................................................ 27

Page iii

Tioga

Exhibit 32: Conley Terminal Near Term CY Capacity ................................................................................. 27

Exhibit 33: Conley Terminal Near Term Crane Capacity ............................................................................ 28

Exhibit 34: Boston Near Term Berth Capacity Maximum Vessel Basis ...................................................... 29

Exhibit 35: Conley 2007 Berth Capacity Vessel Call Basis ........................................................................ 29

Exhibit 36: Conley Terminal Near Term Capacity and Productivity Summary ........................................... 30

Exhibit 37: Port of New York and New Jersey ............................................................................................ 31

Exhibit 38: Red Hook Marine Terminal ....................................................................................................... 32

Exhibit 39: Global Marine Terminal ............................................................................................................. 33

Exhibit 40: Port Newark Container Terminal (PNCT) ................................................................................. 34

Exhibit 41: Maher Terminal ......................................................................................................................... 35

Exhibit 42: APM Elizabeth Marine Terminal ................................................................................................ 36

Exhibit 43: New York Container Terminal ................................................................................................... 37

Exhibit 44: Port of New York and New Jersey Land Use ............................................................................ 38

Exhibit 45: Port of New York and New Jersey Near Term CY Storage Capacity ....................................... 38

Exhibit 46: Port of New York and New Jersey Near-term Crane Capacity ................................................. 39

Exhibit 47: Port of New York and New Jersey Near Term Berth Capacity Maximum Vessel Basis ........... 39

Exhibit 48: Port of New York and New Jersey Berth Capacity Vessel Call Basis ...................................... 40

Exhibit 49: Port of New York and New Jersey Near Term Capacity and Productivity Summary ............... 41

Exhibit 50: Packer Marine Terminal ............................................................................................................ 42

Exhibit 51: Packer Marine Terminal, Philadelphia ...................................................................................... 43

Exhibit 52 Wilmington Marine Terminal ...................................................................................................... 44

Exhibit 53: Wilmington Marine Terminal, Wilmington, DE .......................................................................... 45

Exhibit 54: Delaware River Ports Land Use ................................................................................................ 45

Exhibit 55: Delaware River Ports Near Term CY Storage Capacity ........................................................... 46

Exhibit 56: Delaware River Ports Near-term Crane Capacity ..................................................................... 46

Exhibit 57: Delaware River Ports Near Term Berth Capacity Maximum Vessel Basis ............................... 47

Exhibit 58: Delaware River Ports Berth Capacity Vessel Call Basis........................................................... 47

Exhibit 59: Delaware River Ports Near Term Capacity and Productivity Summary .................................... 48

Exhibit 60: Port of Baltimore........................................................................................................................ 49

Exhibit 61: Dundalk Marine Terminal .......................................................................................................... 50

Exhibit 62: Seagirt Marine Terminal ............................................................................................................ 51

Exhibit 63: Port of Baltimore Land Use ....................................................................................................... 52

Page iv

Tioga

Exhibit 64: Port of Baltimore Near Term CY Storage Capacity .................................................................. 52

Exhibit 65: Port of Baltimore Near-term Crane Capacity ............................................................................ 53

Exhibit 66: Port of Baltimore Near Term Berth Capacity Maximum Vessel Basis ...................................... 54

Exhibit 67: Port of Baltimore Berth Capacity Vessel Call Basis .................................................................. 54

Exhibit 68: Port of Baltimore Near Term Capacity and Productivity Summary ........................................... 55

Exhibit 69: Port of Hampton Roads ............................................................................................................. 56

Exhibit 70: Norfolk International Terminal ................................................................................................... 57

Exhibit 71: Portsmouth Marine Terminal ..................................................................................................... 58

Exhibit 72: Newport News Marine Terminal (NNMT) .................................................................................. 59

Exhibit 73: APM Terminals Virginia ............................................................................................................. 60

Exhibit 74: Port of Virginia Land Use .......................................................................................................... 61

Exhibit 75: Port of Virginia Near Term CY Storage Capacity ...................................................................... 61

Exhibit 76: Port of Virginia Near-term Crane Capacity ............................................................................... 62

Exhibit 77: Port of Virginia Near Term Berth Capacity Maximum Vessel Basis ......................................... 62

Exhibit 78: Port of Virginia Berth Capacity Vessel Call Basis ..................................................................... 63

Exhibit 79: Port of Hampton Roads Near Term Capacity and Productivity Summary ................................ 64

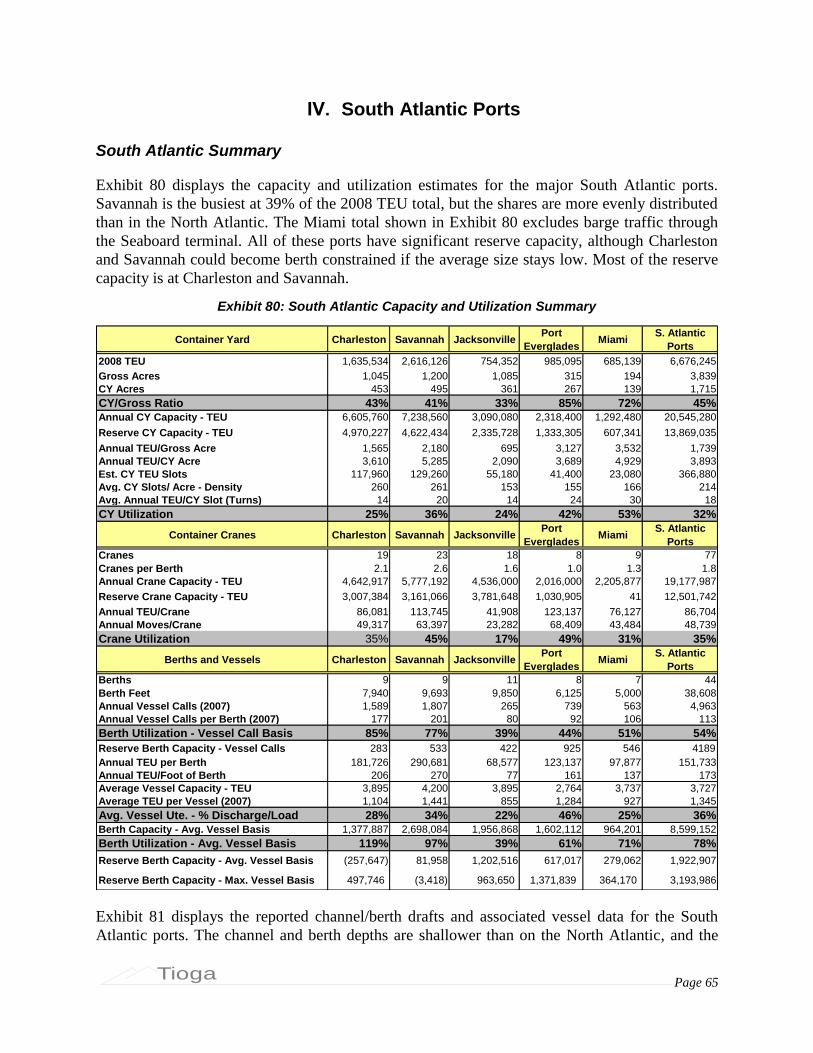

Exhibit 80: South Atlantic Capacity and Utilization Summary ..................................................................... 65

Exhibit 81: South Atlantic Drafts and Vessels ............................................................................................. 66

Exhibit 82: Port of Charleston ..................................................................................................................... 67

Exhibit 83: Wando Welch Terminal ............................................................................................................. 68

Exhibit 84: North Charleston Terminal Profile ............................................................................................. 69

Exhibit 85: North Charleston Terminal Drawing .......................................................................................... 70

Exhibit 86: Columbus Street Terminal ........................................................................................................ 70

Exhibit 87: Columbus Street Terminal Profile ............................................................................................. 71

Exhibit 88: Port of Charleston Land Use ..................................................................................................... 71

Exhibit 89: Port of Charleston Near Term CY Storage Capacity ................................................................ 72

Exhibit 90: Port of Charleston Near Term Crane Capacity ......................................................................... 72

Exhibit 91: Port of Charleston Near Term Berth Capacity Maximum Vessel Basis .................................... 73

Exhibit 92: Charleston 2007 Berth Capacity Vessel Call Basis .................................................................. 73

Exhibit 93: Port of Charleston Near Term Capacity and Productivity Summary ......................................... 75

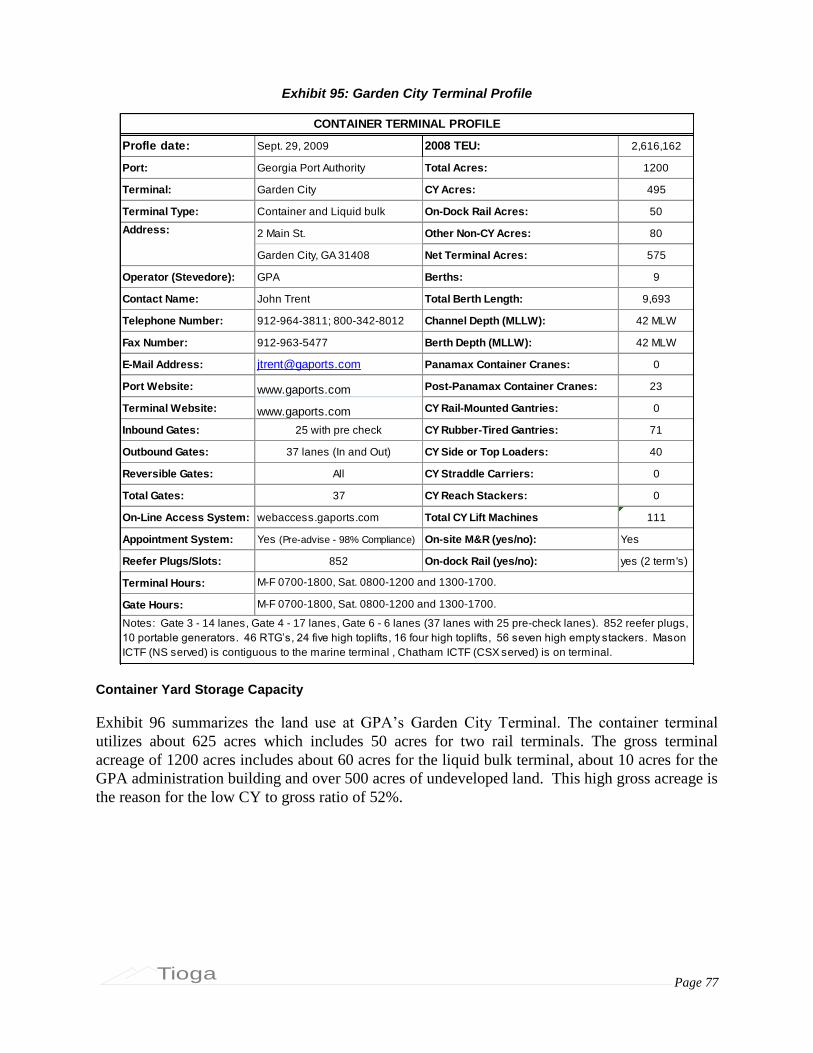

Exhibit 94: Garden City Container Terminal ............................................................................................... 76

Exhibit 95: Garden City Terminal Profile ..................................................................................................... 77

Page v

Tioga

Exhibit 96: Garden City Land Use ............................................................................................................... 78

Exhibit 97: Garden City Near Term CY Storage Capacity .......................................................................... 78

Exhibit 98: Garden City Terminal Near Term Crane Capacity .................................................................... 79

Exhibit 99: Garden City Terminal Near Term Berth Capacity Max Vessel Basis ....................................... 79

Exhibit 100: Garden City 2007 Berth Capacity Vessel Call Basis .............................................................. 80

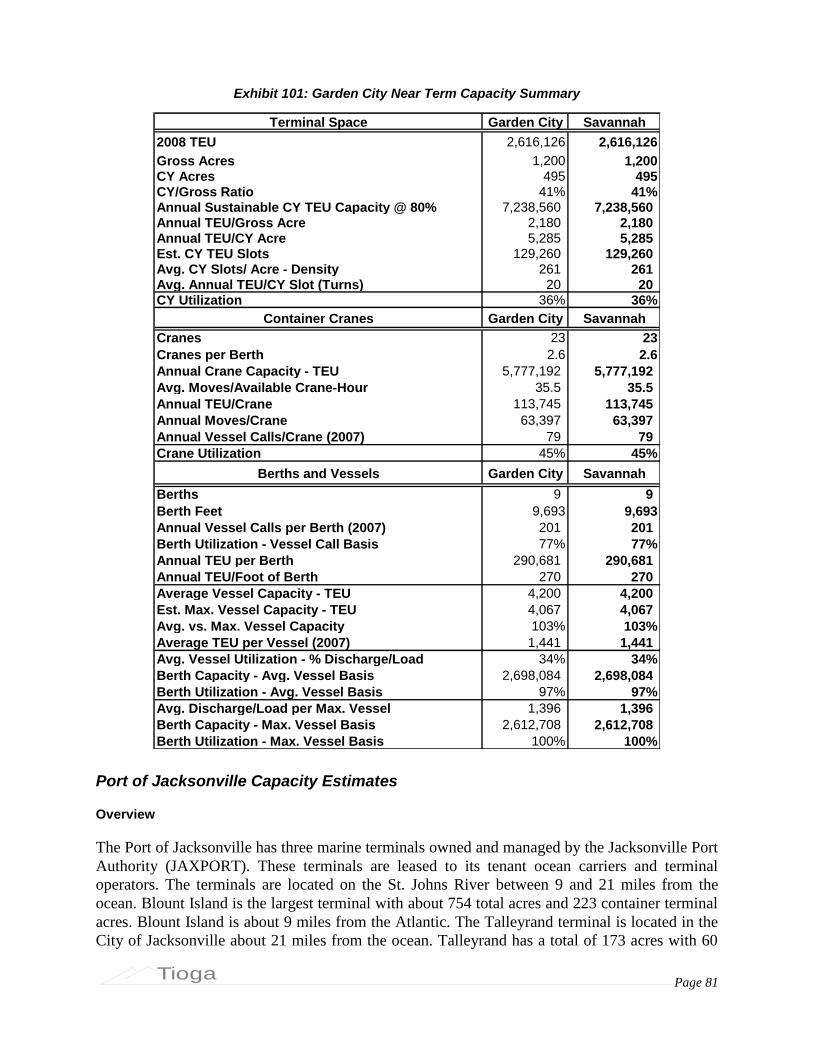

Exhibit 101: Garden City Near Term Capacity Summary ........................................................................... 81

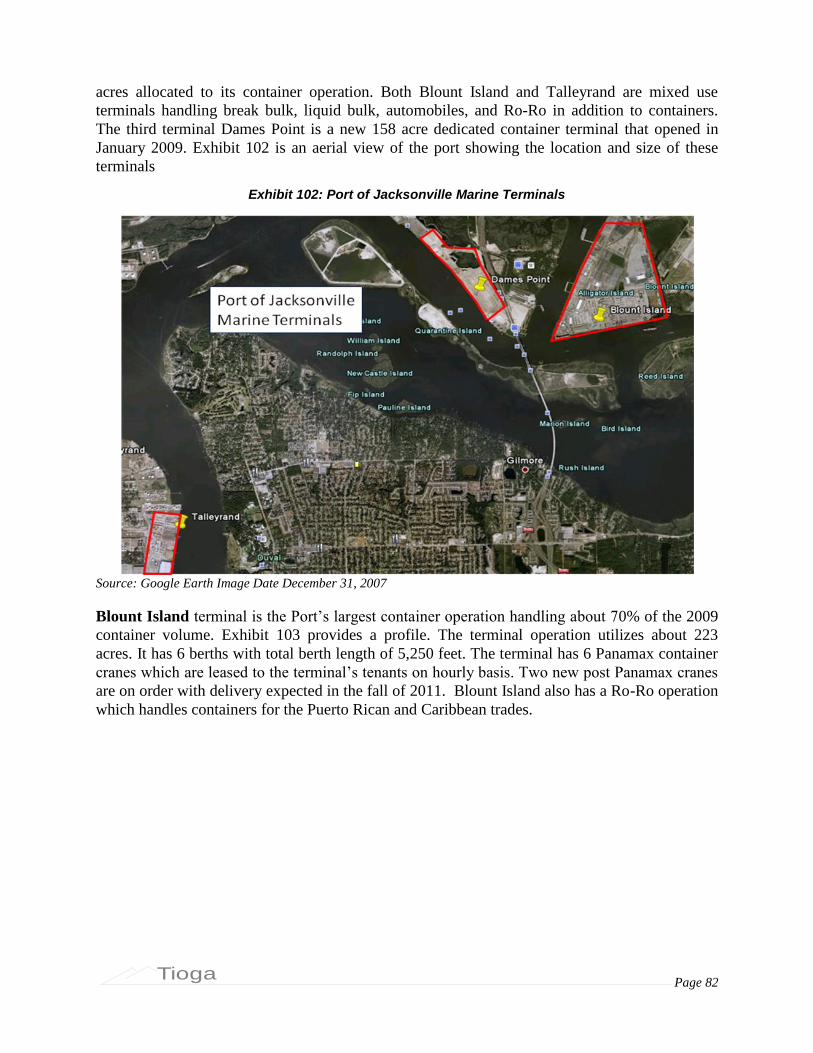

Exhibit 102: Port of Jacksonville Marine Terminals .................................................................................... 82

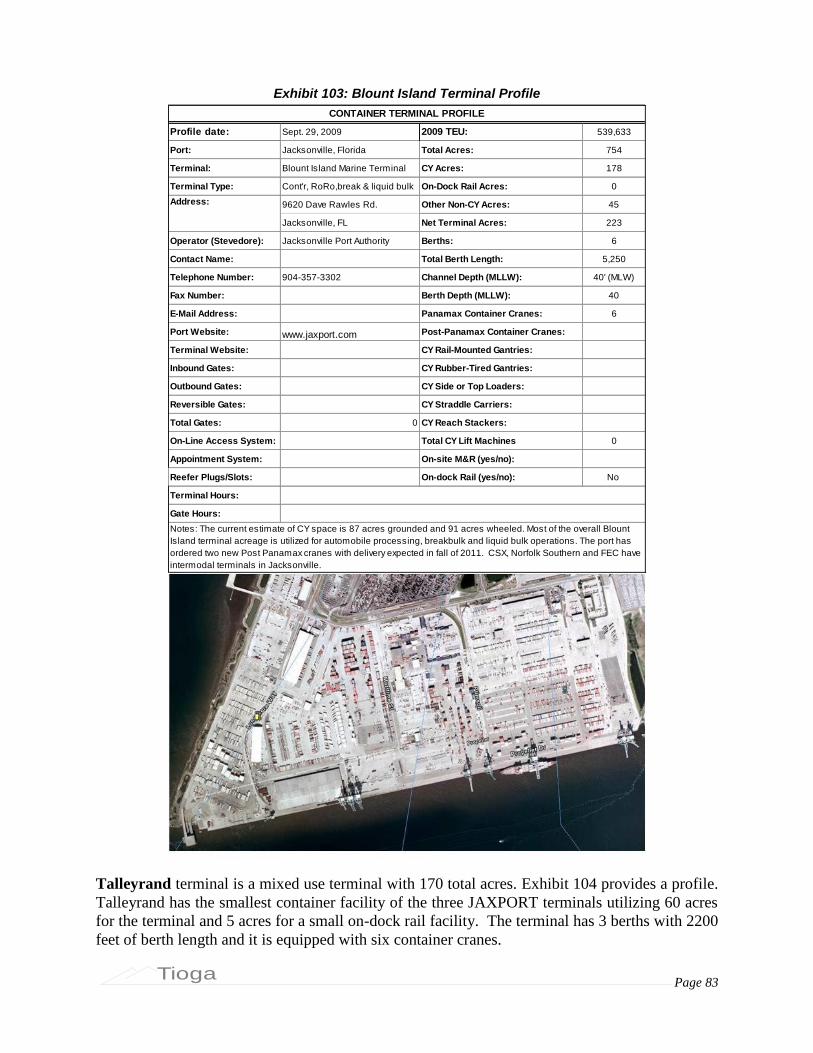

Exhibit 103: Blount Island Terminal Profile ................................................................................................. 83

Exhibit 104: Talleyrand Marine Terminal .................................................................................................... 84

Exhibit 105: Dames Point Container Terminal ............................................................................................ 85

Exhibit 106: Port of Jacksonville Land Use ................................................................................................. 86

Exhibit 107: Port of Jacksonville CY Storage Capacity .............................................................................. 86

Exhibit 108: Port of Jacksonville Near Term Crane Capacity ..................................................................... 87

Exhibit 109: Port of Jacksonville Near Term Berth Capacity Max Vessel Basis ......................................... 88

Exhibit 110: Port of Jacksonville 2009 Berth Capacity Vessel Call Basis .................................................. 88

Exhibit 111: Port of Jacksonville Near Term Capacity and Productivity Summary..................................... 89

Exhibit 112: Port Everglades Container Terminals ..................................................................................... 90

Exhibit 113: Port Everglades Container Terminal Profile ............................................................................ 91

Exhibit 114: Midport Terminal Area ............................................................................................................. 92

Exhibit 115: Port Everglades Land Use ...................................................................................................... 92

Exhibit 116: Port Everglades Near Term CY Capacity ............................................................................... 93

Exhibit 117: Port Everglades Near Term Crane Capacity .......................................................................... 93

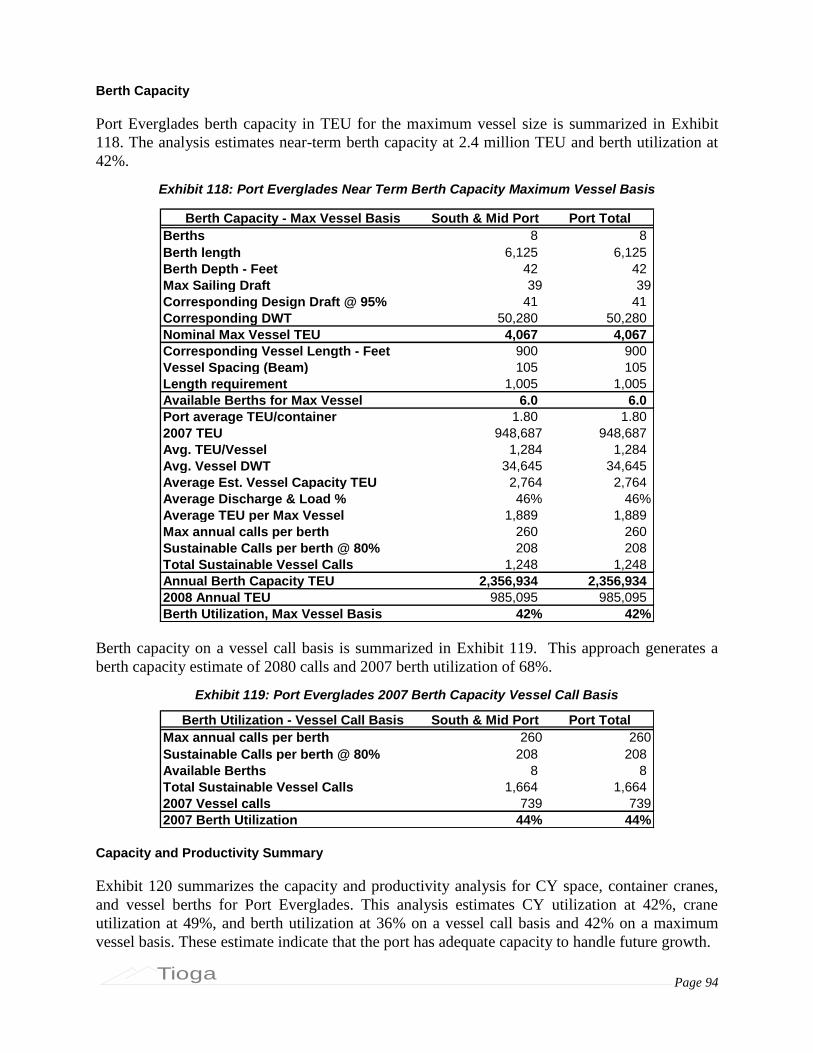

Exhibit 118: Port Everglades Near Term Berth Capacity Maximum Vessel Basis ..................................... 94

Exhibit 119: Port Everglades 2007 Berth Capacity Vessel Call Basis ........................................................ 94

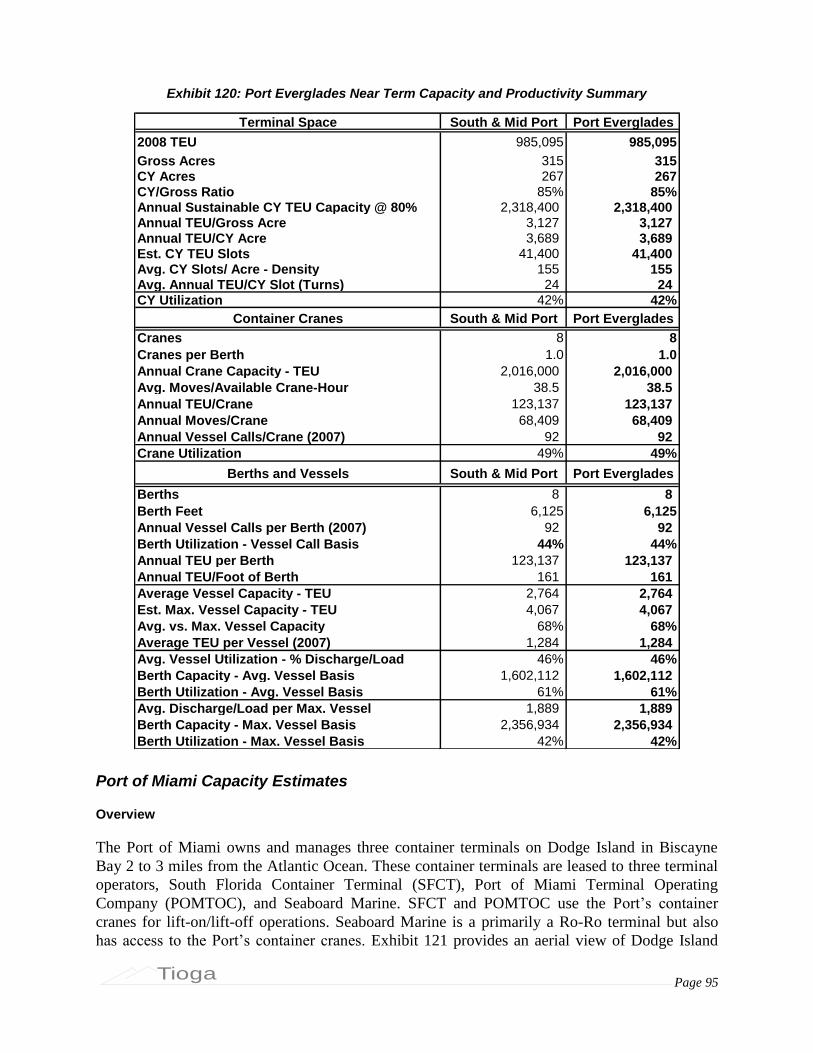

Exhibit 120: Port Everglades Near Term Capacity and Productivity Summary .......................................... 95

Exhibit 121: Port of Miami Container Terminals.......................................................................................... 96

Exhibit 122: Miami Tunnel Project .............................................................................................................. 96

Exhibit 123: South Florida Container Terminal Profile ................................................................................ 97

Exhibit 124: Port of Miami Terminal Operating Company Terminal (POMTOC) ........................................ 98

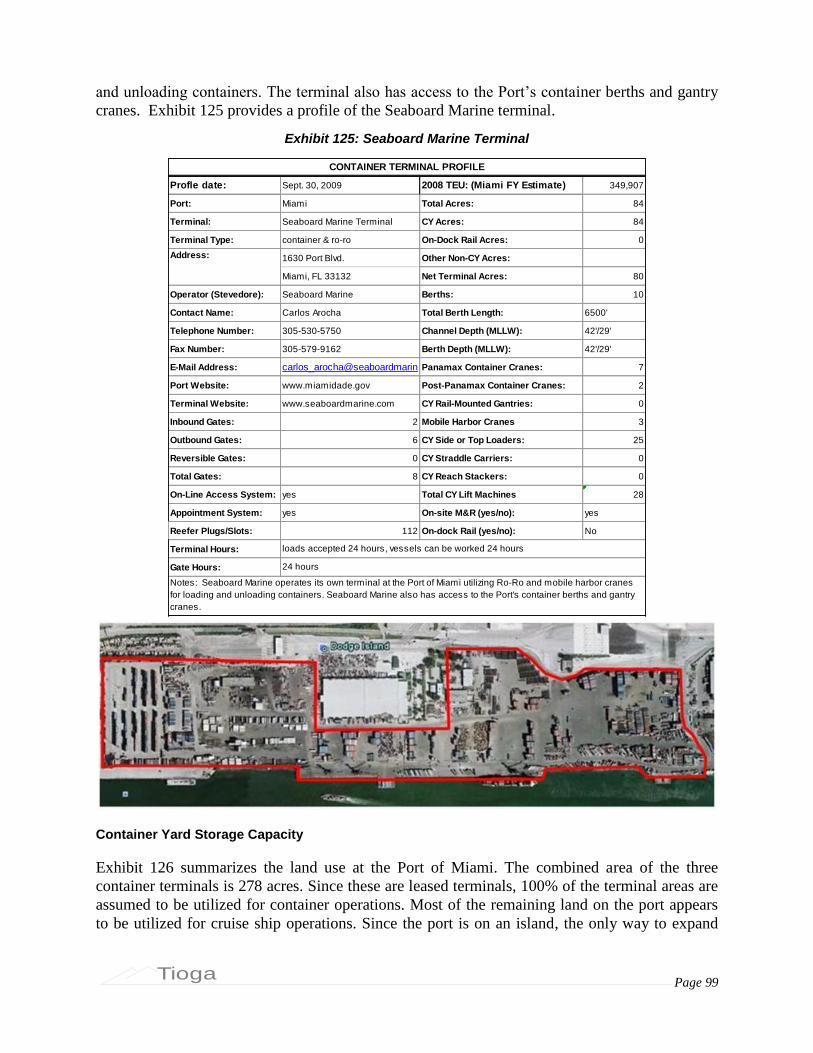

Exhibit 125: Seaboard Marine Terminal ...................................................................................................... 99

Exhibit 126: Port of Miami Land Use ......................................................................................................... 100

Exhibit 127: Port of Miami CY Storage Capacity ...................................................................................... 100

Page vi

Tioga

Exhibit 128: Port of Miami Near Term Crane Capacity ............................................................................. 101

Exhibit 129: Port of Miami Near Term Berth Capacity Maximum Vessel Basis ........................................ 101

Exhibit 130: Port of Miami 2007 Berth Capacity Vessel Call Basis .......................................................... 102

Exhibit 131: Port of Miami Near Term Capacity and Productivity Summary ............................................ 103

Exhibit 132: Gulf Coast Capacity and Utilization Summary ...................................................................... 105

Exhibit 133: Gulf Coast Draft and Vessel Data ......................................................................................... 106

Exhibit 134: Mobile Container Terminal (MCT) ......................................................................................... 106

Exhibit 135: Mobile Pier Two - Container and General Cargo Terminal ................................................... 107

Exhibit 136: Mobile Container Terminal Profile ......................................................................................... 107

Exhibit 137: Pier Two Terminal Profile ...................................................................................................... 108

Exhibit 138: Port of Mobile Land Use ........................................................................................................ 109

Exhibit 139: Port of Mobile Near Term CY Storage Capacity ................................................................... 109

Exhibit 140: Port of Mobile Near Term Crane Capacity ............................................................................ 110

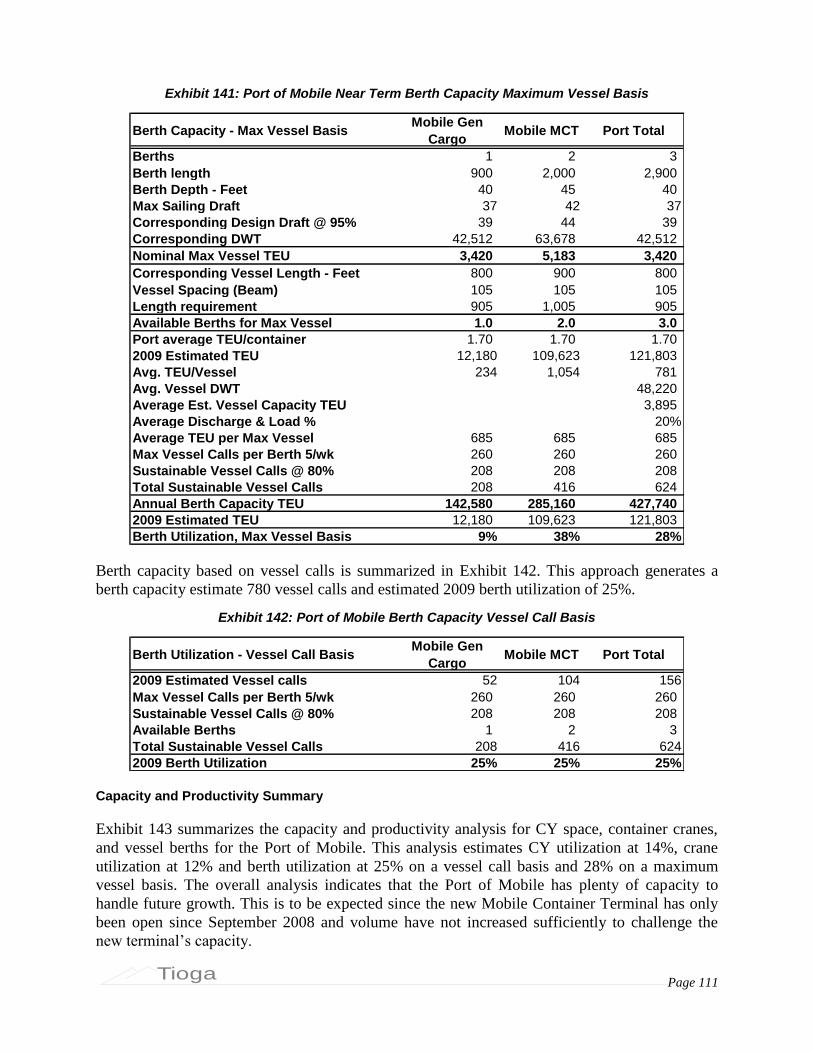

Exhibit 141: Port of Mobile Near Term Berth Capacity Maximum Vessel Basis ....................................... 111

Exhibit 142: Port of Mobile Berth Capacity Vessel Call Basis .................................................................. 111

Exhibit 143: Port of Mobile Near Term Capacity and Productivity Summary ........................................... 112

Exhibit 144: Port of New Orleans Napoleon Avenue Terminal ................................................................. 113

Exhibit 145: Napoleon Avenue Terminal Profile ....................................................................................... 114

Exhibit 146: Port of New Orleans Land Use ............................................................................................. 114

Exhibit 147: Port of New Orleans Near Term Storage Capacity ............................................................... 115

Exhibit 148: Port of New Orleans Near Term Crane Capacity .................................................................. 115

Exhibit 149: Port of New Orleans Near Term Berth Capacity Maximum Vessel Basis ............................ 116

Exhibit 150: Port of New Orleans 2007 Berth Capacity Vessel Call Basis ............................................... 116

Exhibit 151: Port of New Orleans Near Term Capacity and Productivity Summary ................................. 117

Exhibit 152: Port of Houston Terminals .................................................................................................... 118

Exhibit 153: Barbours Cut Terminal .......................................................................................................... 119

Exhibit 154: Bayport Terminal ................................................................................................................... 120

Exhibit 155: Port of Houston Land Use ..................................................................................................... 121

Exhibit 156: Port of Houston Near Term CY Storage Capacity ................................................................ 121

Exhibit 157: Port of Houston Near Term Crane Capacity ......................................................................... 122

Exhibit 158: Port of Houston Near Term Berth Capacity Maximum Vessel Basis .................................... 122

Exhibit 159: Port of Houston 2007 Berth Capacity Vessel Call Basis....................................................... 123

Page vii

Tioga

Exhibit 160: Port of Houston Near Term Capacity and Productivity Summary ......................................... 124

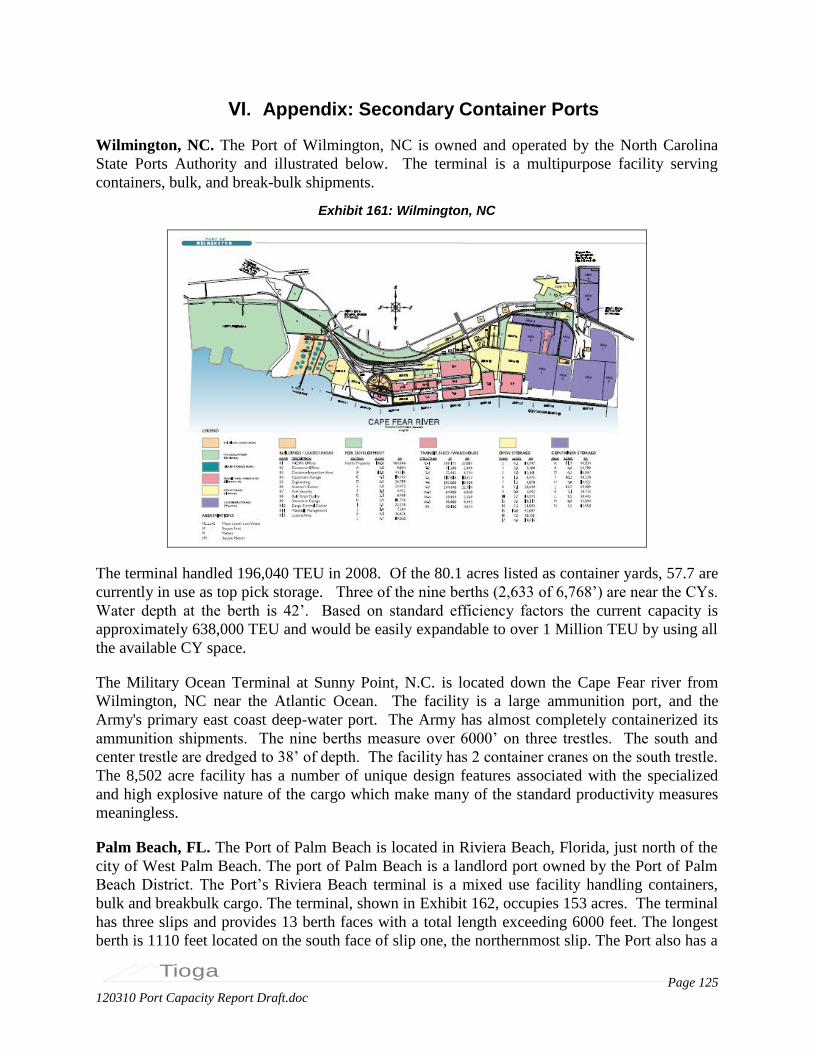

Exhibit 161: Wilmington, NC ..................................................................................................................... 125

Exhibit 162: Port of Palm Beach - Riviera Beach Terminal ...................................................................... 126

Exhibit 163: Port of Tampa........................................................................................................................ 127

Exhibit 164: Port of Gulfport ...................................................................................................................... 128

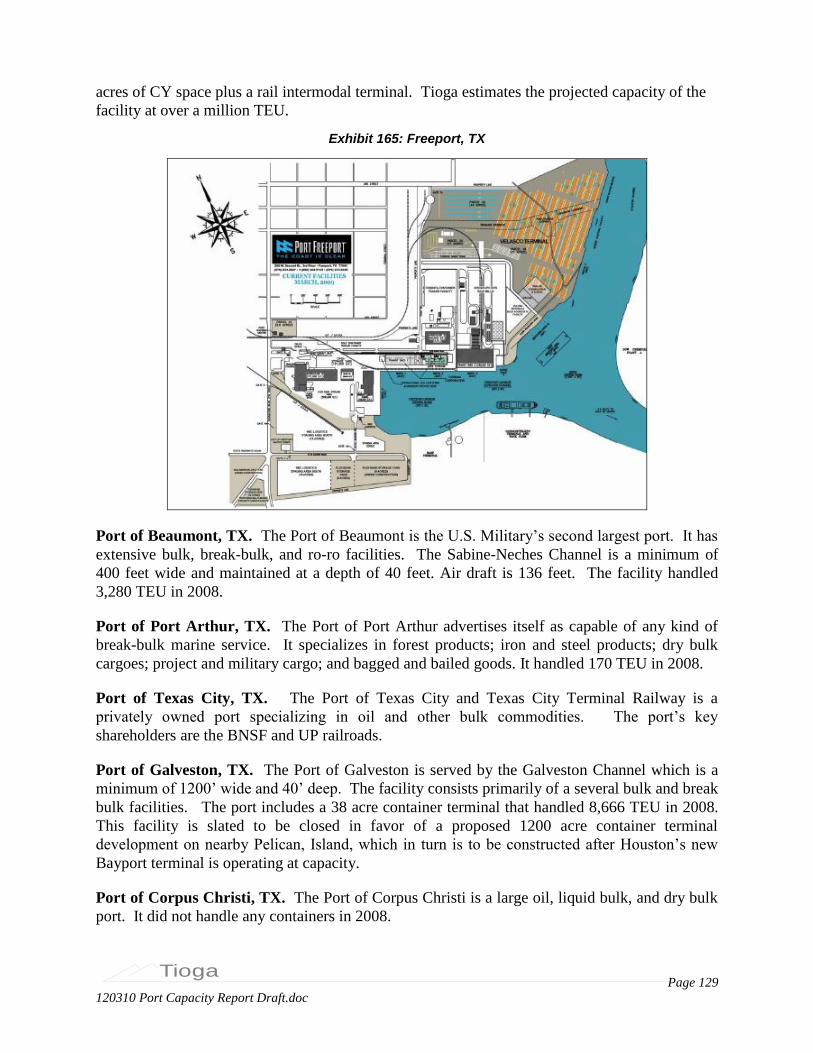

Exhibit 165: Freeport, TX .......................................................................................................................... 129

Exhibit 166: Additional Texas Ports .......................................................................................................... 130

Page 1

Tioga

I. Summary

U.S. container port capacity is the single most critical factor in the nation’s ability to participate

in containerized trade. Within this port network the Corps of Engineers’ primary focus is on

navigation improvements – developing and maintaining the channels, berths, and other aids that

give container ships access to port terminals. The facilities, equipment, systems, and manpower

needed for container terminals are all costly. There is an inherent tension between having

enough capacity for trade peaks and expected growth and creating excess capacity that ties up

valuable resources.

This study was initiated to obtain a broad overview of East Coast and Gulf Coast container port

capacity as an input to the Corps’ planning and as a supplement to the many documents and

studies produced in the course of project feasibility studies. The study team attempted to address

the following questions.

What are the near-term and long-term capacities of the major East Coast and Gulf

Coast container ports?

What factors constrain the capacities of those ports?

How well is capacity currently utilized?

How well are the major ports prepared to handle larger vessels?

How do the smaller container ports or terminals fit into the picture?

There is a particular concern over capacity at East Coast (North Atlantic and South Atlantic) and

Gulf Coast ports. Before the recession, emergence of multi-coast import strategies shifted

market share and volume from the West Coast to the East and Gulf Coasts. The planned opening

of the new, higher-capacity Panama Canal locks in 2014 will permit carriers to deploy larger,

more economical vessels in Asia-East Coast and Asia-Gulf services.

The study team analyzed the following major container ports (Exhibit 9).

Exhibit 1: Major Ports Analyzed

North Atlantic South Atlantic Gulf

Boston Charleston Mobile

New York/New Jersey Savannah New Orleans

Philadelphia Jacksonville Houston

Wilmington Port Everglades

Baltimore Miami

Virginia

Exhibit 2 display five measures of estimated 2008 utilization for these major North Atlantic,

South Atlantic, and Gulf ports, and for the East Coast and Gulf total. With the exception of high

estimated berth utilization at some South Atlantic ports, the data in Exhibit 1 indicate substantial

reserve capacity. North Atlantic ports, notable the Port Authority of New York and New Jersey

Page 2

Tioga

(PANYNJ) are relatively tight on container yard (CY) capacity. Gulf ports have higher vessel

utilization (e.g. are discharging and loading a higher percentage of vessel capacity), largely due

to draft restrictions at Houston that hold down maximum vessel size.

Exhibit 2: 2008 Port Utilization Summary

55%

34%

46%

42%

30%

37%

34% 33%

42%39%

57%

42%

39%

54%

42%

49%

42%

83%

44%

53%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

N. Atlantic Ports* S. Atlantic Ports Gulf Ports East & Gulf Coast Ports

CY Utilization

Crane Utilization

Avg. Vessel Ute. - % Discharge/Load

Berth Utilization - Vessel Call Basis

Berth Utilization - Avg. Vessel Basis

Utilization estimates for the combined East Coast and Gulf ports are near or below 50%. On

average, these ports are using:

42% of their CY storage capacity given existing land uses;

33% of the two-shift capacity of their container cranes;

49% of the berth capacity for vessel calls;

42% of the vessel capacity for cargo discharge and load; and

53% of the berth TEU throughput capability using the maximum vessel sizes.

Many ports have annual volume peaks that can strain capacity for a short period. The figures in

Exhibit 2 and throughput the report are based on an annual capability of 80% of the theoretical

maximum to allow for peaking and sustainable service quality.

Volume figures used throughout this report are compared to 2008 volumes reported to the

American Association of Port Authorities (AAPA). As has been widely reported, 2009 cargo

volumes were down 10%-30% from 2008, so using 2009 volumes would artificially inflate

estimates of reserve capacity. It is also likely, however, that the major container ports will have

somewhat more reserve capacity than was estimated herein until the trade recovers.

Page 3

Tioga

Exhibit 3 summarizes the implied reserve container port capacity by coast and for the East and

Gulf port total. Generally speaking, the system as a whole could handle roughly double the 2008

volume before hitting CY or berth capacity constraints. That result would obtain, however, only

if the increased trade were distributed according to the available capacity – an unlikely outcome.

It is far more likely that some ports and terminals would see a disproportionate share of the cargo

growth and hit capacity constraints while other ports and terminals remained underutilized.

Exhibit 3: Reserve Container Port Capacity by Coast

MetricN. Atlantic

Ports*

S. Atlantic

PortsGulf Ports

East & Gulf Coast

Ports

2008 TEU 8,744,838 6,676,245 2,229,877 17,650,961

Reserve CY Capacity - TEU 10,612,402 13,869,035 2,669,003 25,491,439

Reserve Crane Capacity - TEU 20,895,164 12,501,742 4,423,466 37,820,372

Reserve Berth Capacity - Vessel Calls 8884 4189 1555 12024

Reserve Berth Capacity - Avg. Vessel Basis 11,832,051 1,922,907 2,799,609 16,554,568

Reserve Berth Capacity - Max. Vessel Basis 29,332,298 3,193,986 2,554,332 35,080,616

Exhibit 4 provides key measures of terminal space and CY utilization. The North and South

Atlantic ports taken together are about 10 times the size of the Gulf ports and have about 90% of

the CY capacity. In 2008 these ports averaged about 2,307 TEU per gross acre. This sort of

relatively low density is often compared to much higher throughput per acre achieved in Asia

and Europe. Asian and European terminals, however, typically devote almost all their terminal

space to CY functions and rarely have on-dock rail, chassis storage, warehousing, or other

functions in the terminal acreage. As Exhibit 4 shows, however, East and Gulf Coast terminals

devote an average of only 48% of the gross acres to CY functions. The average throughput for

actual CY space was 4,842 TEU per acre, a more accurate basis of comparison.

Exhibit 4: Terminal Space and CY Utilization

MetricN. Atlantic

Ports*

S. Atlantic

PortsGulf Ports

East & Gulf Coast

Ports

2008 TEU 8,744,838 6,676,245 2,229,877 17,650,961

Gross Acres 3,227 3,839 717 7,783

CY Acres 1,542 1,715 442 3698.5

CY/Gross Ratio 48% 45% 62% 48%

Annual CY Capacity - TEU 17,698,240 20,545,280 4,898,880 43,142,400

Reserve CY Capacity - TEU 10,612,402 13,869,035 2,669,003 25,491,439

Annual TEU/Gross Acre 2,918 1,739 3,109 2,268

Annual TEU/CY Acre 5,973 3,893 5,045 4,772

Est. CY TEU Slots 267,620 366,880 84,360 718,860

Avg. CY Slots/ Acre - Density 174 214 191 194

Avg. Annual TEU/CY Slot (Turns) 36 18 26 25

CY Utilization 55% 32% 46% 41%

Exhibit 5 compares 2008 TEU and estimated CY TEU capacity. Reserve capacity is greatest at

NYNJ, Charleston, and Savannah. This chart, however, does not take into account current and

announced terminal expansion projects in Mobile, Houston, and elsewhere. terms of shear size

PANYNJ, Charleston, Savannah, and Jacksonville are the largest ports. The Delaware River

Ports include Philadelphia and Wilmington, DE. The Port of Virginia includes Norfolk, Newport

Page 4

Tioga

News, and Portsmouth terminals. The APM Portsmouth terminal is new and not part of the Port

of Virginia and is therefore shown separately.

Exhibit 5: 2008 TEU and CY TEU Capacity

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

Bost

on

NYNJ

Del

awar

e Riv

er

Bal

timore

VPA

APM

Port

smouth

N. A

tlantic

Port

s*

Char

lest

on

Savan

nah

Jack

sonvi

lle

Port E

verg

lades

Mia

mi

S. Atla

ntic P

orts

Mobile

New

Orlea

ns

Houst

on

Gulf

Ports

East &

Gulf

Coas

t Port

s

Reserve CY Capacity - TEU

2008 TEU

Exhibit 6 compares CY storage densities. Those terminals with the largest shares of land set up

for RTG operations, such as Boston, Baltimore, Charleston, and Savannah show the highest slot

densities, although not all those slots are regularly occupied. The highest density is at the APM

Portsmouth terminal, which is the only U.S. terminal using RMGs. The available TEU “slots”

were estimated by applying rule-of-thumb storage densities to the acreage used for wheeled,

stacked, straddle carrier, RTG, or RMG handling. Annual throughput capacity is therefore a

function of TEU slots and annual turnover per slot. The ports analyzed averaged 194 TEU slots

per acre against a rough maximum of 300 for all-RTG storage. As the data suggest, almost all

the terminals examined use a mix of storage types and densities. The East and Gulf Coast ports

averaged an estimated 25 annual turns per slot against a benchmark maximum of 70. Annual

turns per slot are noticeably higher in the North Atlantic (largely due to PANYNJ and the Ports

of Virginia).

Page 5

Tioga

Exhibit 6: Average TEU Slots per CY Acre

243

160

125

206

124

306

174

260 261

153 155166

214

176

158

205191 194

-

50

100

150

200

250

300

350

Bost

on

NYNJ

Del

awar

e Riv

er

Bal

timore

VPA

APM

Port

smouth

N. A

tlantic

Port

s*

Char

lest

on

Sav

annah

Jack

sonvi

lle

Port

Eve

rgla

des

Mia

mi

S. A

tlantic

Port

s

Mobile

New

Orlea

ns

Houst

on

Gulf

Port

s

Eas

t & G

ulf Coas

t Port

s

As Exhibit 7 shows, crane utilization in terms of annual TEU is relatively low, averaging 33%

This relatively low utilization might imply an excess of crane capacity. Yet the primary purpose

of crane capacity is to turn vessels quickly. Whether there is one vessel per week or five, each

vessel will need two or more cranes. Not coincidently, the terminals surveyed averaged two

cranes per berth. Crane utilization is therefore co-determined with berth and vessel utilization.

Exhibit 7: Container Cranes and Utilization

Container CranesN. Atlantic

Ports*

S. Atlantic

PortsGulf Ports

East & Gulf Coast

Ports

Cranes 120 77 27 224

Cranes per Berth 2.1 1.8 2.1 2.0

Annual Crane Capacity - TEU 29,640,002 19,177,987 6,653,344 55,471,333

Reserve Crane Capacity - TEU 20,895,164 12,501,742 4,423,466 37,820,372

Annual TEU/Crane 76,709 86,704 82,588 78,799

Annual Moves/Crane 43,140 48,739 47,017 45,532

Crane Utilization 30% 35% 34% 32%

Berth and vessel utilization, shown in Exhibit 8, are tightly linked. In 2007, the ports and

terminals averaged 103 annual vessel calls per berth – roughly two per week. The average was

higher in the South Atlantic. Against a benchmark maximum of 260 calls per year (one each

week day) and a rule-of-thumb sustainable maximum of 208 (80%), the average of 103 calls

implies 49% utilization. In practical terms, berths that are handling two vessels per week could

probably handle four. This conclusion, however, depends on vessel size and the total cargo

discharged and loaded. The vessels calling at these ports in 2007 had an average capacity of

3,710 TEU (estimated from DWT data). The average discharge and load was 9,553 TEU, or

42% of vessel capacity. The theoretical maximum is actually 200% of capacity – 100%

CY Storage TEU Slots per Acre

Wheeled Chassis 80

Grounded Straddle Carrier 160

Grounded Stacked 200

Grounded RTG 300

Grounded RMG 360

Page 6

Tioga

discharged and 100% loaded. That only 49% of the capacity is discharged and loaded implies

that the vessels themselves are not sailing full or that the capacity is shared between multiple port

calls, or most likely, both.

Exhibit 8: Berth and Vessel Capacity and Utilization

Berths and VesselsN. Atlantic

Ports*

S. Atlantic

PortsGulf Ports

East & Gulf Coast

Ports

Berths 57 44 13 114

Berth Feet 58,200 38,608 12,900 109,708

Annual Vessel Calls (2007) 5,576 4,963 1,149 11,688

Annual Vessel Calls per Berth (2007) 80 113 88 103

Berth Utilization - Vessel Call Basis 39% 54% 42% 49%

Reserve Berth Capacity - Vessel Calls 8884 4189 1555 12024

Annual TEU per Berth 164,997 151,733 171,529 154,833

Annual TEU/Foot of Berth 159 173 173 161

Average Vessel Capacity - TEU 3,762 3,727 3,387 3,710

Average TEU per Vessel (2007) 1,568 1,345 1,941 1,510

Avg. Vessel Ute. - % Discharge/Load 42% 36% 57% 41%

Berth Capacity - Avg. Vessel Basis 20,576,889 8,599,152 5,029,487 34,205,528

Berth Utilization - Avg. Vessel Basis 42% 78% 44% 52%

Reserve Berth Capacity - Avg. Vessel Basis 11,832,051 1,922,907 2,799,609 16,554,568

Reserve Berth Capacity - Max. Vessel Basis 29,332,298 3,193,986 2,554,332 35,080,616

The average vessel capacities shown in Exhibit 8 are low compared to the maximum vessel sizes

that ports say that they can accommodate with the available draft. Ports typically receive few if

any calls from the maximum size vessels, so most calls are made by a mix of smaller container

ships.

Throughput could be increased by using larger vessels for the same number of calls, making

more calls with the same vessels, discharging and loading more of the vessel capacity at each

call, or any combination of these changes. In each case more container cranes and/or crane time

would be required to handle the increased cargo while keeping the vessel on schedule. The crane

capacity estimates are based on availability for two shifts per day, 250 days per year (4,000

annual hours). The cranes are, in fact, available 24 hours per day if the terminal operator needs

the additional shifts to turn the vessel on schedule and is willing to pay for overtime.

The study team also briefly reviewed the capabilities of the secondary East Coast and Gulf Ports,

detailed in the Appendix.

Wilmington, NC

Palm Beach, FL

Tampa, FL

Gulfport, MS

Freeport, TX

Beaumont, TX

Port Arthur, TX

Texas City, TX

Galveston, TX

Corpus Christi, TX.

Generally speaking, the secondary ports supplement the capacity of the major ports and handle

trades and cargoes that do not fit in well with the large, dedicated container terminals. These

Page 7

Tioga

ports handle a mix of containerized, bulk, and break-bulk shipments, so their container capacities

are difficult to determine with precision. This mix of capabilities, does however, provide

flexibility, particularly for project cargoes and other limited-duration needs. While these ports

handle relatively small volumes of containers, several have specific importance to the imported

fruit trade (e.g. bananas) and other niche markets. Some, such as Wilmington and Beaumont, are

part of larger complexes that include major military shipping points. Tampa, Gulfport, Freeport,

and Corpus Christi have expansion plans in various stages of progress.

Overall, the North Atlantic, South Atlantic, and Gulf ports have substantial inherent capacity for

near-term growth. That growth can be achieved through more intensive use of existing

terminals, cranes, and berths. The existence of aggregate reserve capacity does not preclude slot

shortages at ports and terminals that receive more than their share of growth.

Page 8

Tioga

II. Background and Approach

Background

The capacity of U.S. container ports is the single most critical factor in the nation’s ability to

participate in containerized trade. Beginning in the 1950s and accelerating in the decades that

followed, containerization transformed both international merchandise trade and the ports that

serve it. Efficient handling of containerized trade requires far more than just dockside space and

labor – it requires sophisticated facilities, equipment, and systems manned by trained operators.

The facilities, equipment, systems, and manpower needed for container terminals are all costly.

There is an inherent tension between having enough capacity for trade peaks and expected

growth and creating excess capacity that ties up valuable resources.

Within this port network the Corps of Engineers’ primary focus is on navigation improvements –

developing and maintaining the channels, berths, and other aids that give container ships access

to port terminals. That responsibility is also a balancing act. Dredging and related activities are

costly and time consuming, and have serious environmental implications. Moreover, in an era of

limited resources, the Corps cannot meet every port’s desire for unlimited vessel access. There

is little benefit to providing deeper channels if terminals do not have capacity to match, or to

expanding terminals if channels become a bottleneck.

There are few, if any, concerns over container port capacity for the immediate future. The global

recession has drastically eroded containerized trade, with most ports seeing 2009 volumes 10-30

percent below the 2006-2007 peaks. Trade began to recover its momentum in early 2010 as this

report was being prepared, but it will likely take 5-7 years to regain 2006-2007 volumes.

At those 2006-2007 peaks, however, there were legitimate concerns over the capacity of U.S.

container ports to accommodate foreseeable long-term growth. The San Pedro Bay ports were

severely congested during the 2004 peak shipping season. Spot capacity shortages have

developed from time to time at many ports (and have persisted in some cases despite the

recession). Given the high cost and long lead times required to expand container terminal

capacity, it is reasonable to ask whether the capacity will be available when it is eventually

needed.

There is a particular concern over capacity at East Coast (North Atlantic and South Atlantic) and

Gulf Coast ports. Before the recession, growth and maturation of supply chains had led major

importers to diversity their routings away from the past concentration in Southern California.

The emergence of multi-coast import strategies shifted market share and volume from the West

Coast to the East and Gulf Coasts. Concern over potential congestion and cost increases in

Southern California added impetus to this trend. Some East Coast ports have also been very

successful in attracting new distribution centers to their region, in sync with the diversification of

import supply chains.

Page 9

Tioga

The planned opening of the new, higher-capacity Panama Canal locks in 2014 will permit

carriers to deploy larger, more economical vessels in Asia-East Coast and Asia-Gulf services.

The increase in vessel sizes is likely to be gradual for several reasons.

While the new locks will accommodate vessels of 12,000-13,000 TEU, such

vessels are presently dedicated to the Asia-Europe trade. The vessel fleet required

to provide 12,000+ TEU capacity in trans-Panama service does not yet exist.

Given the drastic decline in container vessel orders, it is unlikely that such a fleet

will exist in 2014. Carriers are more likely to use smaller vessels presently laid

up.

The recession has led to a fall-off in trans-Panama trades and a withdrawal of

some all-water services. The volume needed to support a tripling of pre-recession

capacity (from 4,000 TEU vessels to 12,000 TEU vessels) is unlikely to emerge

by 2014.

Consolidation of services through vessel-sharing agreements may achieve some

economies of scale, but is unlikely to fill 12,000 TEU vessels at the same service

frequency as the 3,000-4,000 TEU vessels now deployed.

While a more gradual increase in the size of trans-Panama container vessels will likely give the

ports and the Corps more time to respond, the response will still be necessary. Moreover, the

East Coast and Gulf ports also serve the trans-Atlantic and round-the-world (RTW) trades in

which vessel sizes are also increasing.

This study was initiated to obtain a broad overview of East Coast and Gulf Coast container port

capacity as an input to the Corps’ planning and as a supplement to the many documents and

studies produced in the course of project feasibility studies. The study team attempted to address

the following questions.

What are the near-term and long-term capacities of the major East Coast and Gulf

Coast container ports?

What factors constrain the capacities of those ports?

How well is capacity currently utilized?

How well are the major ports prepared to handle larger vessels?

How do the smaller container ports or terminals fit into the picture?

This report does not address the capacity of highways, railroads, and intermodal connector to

move containers to and from the ports. Trade growth through 2006-2007 was creating concern

among local, regional, and state transportation officials regarding impacts on road and rail

infrastructure. The recession has provided a multi-year reprieve, but the issue will eventually

return.

This report likewise does not address the supply of drayage trucks and drivers needed to pick up

and deliver more containers. The drayage tractor supply can be increased as required, although

Page 10

Tioga

meeting stringent emissions requirements will add to the cost. The supply of drivers may be

more problematical. Until the recession, motor carriers nationwide were experiencing a

persistent driver shortage. Some Southern California drayage firms were offering signing

bonuses for new drivers. TWIC requirements have further reduced the pool of drivers eligible

for port drayage. As trade recovers, there could be a shortage of drayage drivers.

Finally, this study does not address the need for trained personnel to operate expanded terminals.

Labor supply cannot be taken for granted. A major contributor to the 2004 peak season

congestion in Southern California was a Longshore labor shortage. The pool of Longshore labor

has since expanded, but has shrunk somewhat as longshoremen idled by the recession have

moved to other jobs.

Overall Approach

The study team analyzed the following major container ports (Exhibit 9).

Exhibit 9: Major Ports Analyzed

North Atlantic South Atlantic Gulf

Boston Charleston Mobile

New York/New Jersey Savannah New Orleans

Philadelphia Jacksonville Houston

Wilmington Port Everglades

Baltimore Miami

Virginia

No two container terminals are exactly alike, despite having a great deal in common. Port

planners and terminal operators have preferences for different operating types and

configurations, and those preferences change over time. Moreover, each terminal design must be

adapted to its site.

These differences are particularly apparent in the definition and configuration of the container

yard (CY). There are frequently disparities between what they port lists as CY acreage and what

the consultant team identified as working CY acreage from aerial photos. Depending on local

practice, land used for chassis storage, land used for equipment maintenance, or land not

presently used at all may or may not be included as CY acreage. The study team focused on land

being used for container storage, so the figures in this report tend to be conservative.

There are several possible ways to estimate container port capacity. All rely heavily on industry

rules of thumb and a variety of assumptions as well as quantifiable engineering relationships.

The general approach used in this study was chosen primarily to suit the readily available port

and terminal data elements. More precise estimates are possible, but would require a much

greater investment in data collection and analysis and would change frequently as ports and

terminals change their facilities and operations.

Marine container terminal capacity has five long-term constraints or dimensions, as illustrated in

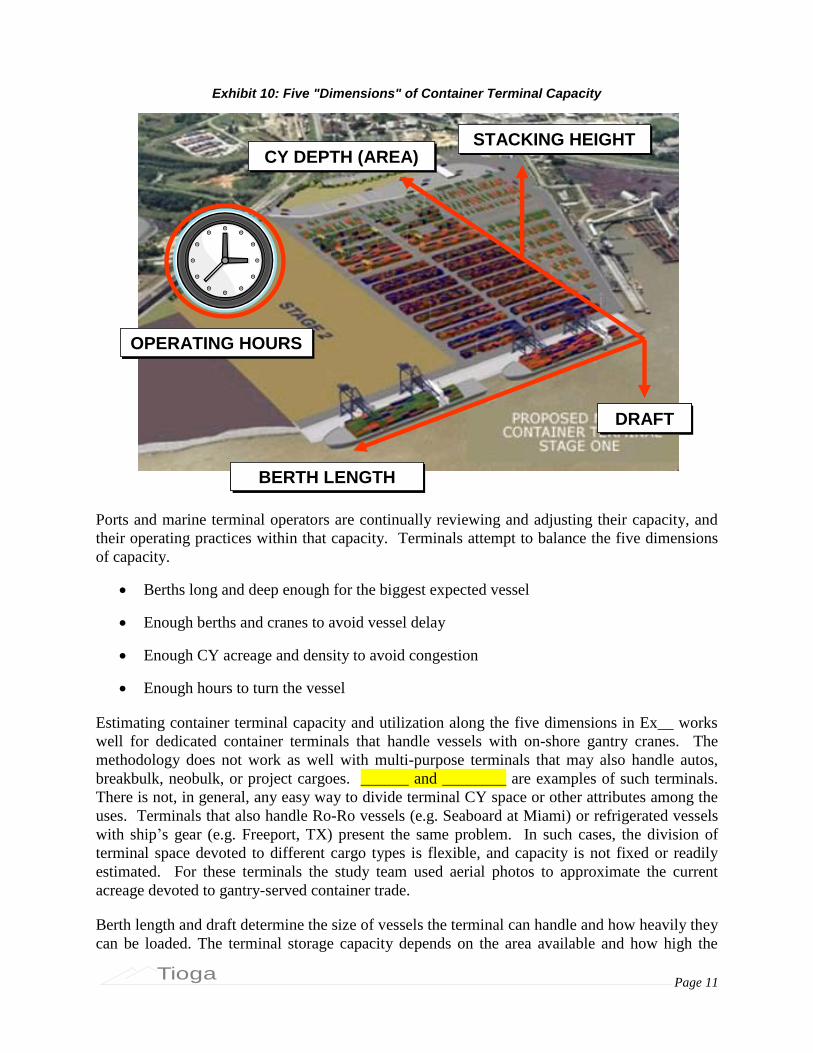

Exhibit 10.

Page 11

Tioga

Exhibit 10: Five "Dimensions" of Container Terminal Capacity

DRAFTDRAFT

BERTH LENGTHBERTH LENGTH

STACKING HEIGHTSTACKING HEIGHTCY DEPTH (AREA)CY DEPTH (AREA)

OPERATING HOURSOPERATING HOURS

DRAFTDRAFT

BERTH LENGTHBERTH LENGTH

STACKING HEIGHTSTACKING HEIGHTCY DEPTH (AREA)CY DEPTH (AREA)

OPERATING HOURSOPERATING HOURS

Ports and marine terminal operators are continually reviewing and adjusting their capacity, and

their operating practices within that capacity. Terminals attempt to balance the five dimensions

of capacity.

Berths long and deep enough for the biggest expected vessel

Enough berths and cranes to avoid vessel delay

Enough CY acreage and density to avoid congestion

Enough hours to turn the vessel

Estimating container terminal capacity and utilization along the five dimensions in Ex__ works

well for dedicated container terminals that handle vessels with on-shore gantry cranes. The

methodology does not work as well with multi-purpose terminals that may also handle autos,

breakbulk, neobulk, or project cargoes. ______ and ________ are examples of such terminals.

There is not, in general, any easy way to divide terminal CY space or other attributes among the

uses. Terminals that also handle Ro-Ro vessels (e.g. Seaboard at Miami) or refrigerated vessels

with ship’s gear (e.g. Freeport, TX) present the same problem. In such cases, the division of

terminal space devoted to different cargo types is flexible, and capacity is not fixed or readily

estimated. For these terminals the study team used aerial photos to approximate the current

acreage devoted to gantry-served container trade.

Berth length and draft determine the size of vessels the terminal can handle and how heavily they

can be loaded. The terminal storage capacity depends on the area available and how high the

Page 12

Tioga

container can be stacked. The other variable is operating hours. Most terminals will operate a

second shift as required to turn the vessel, but second shifts are expensive and third shifts are still

more expensive. Most terminals still open the gates for just one shift.

Port authorities are commonly charged by their communities, regions, or states with promoting

growth of trade, economic development, and jobs. To do so, port and terminal operators attempt

to build and maintain sufficient capacity for foreseeable and attainable growth. Most container

terminal parameters, however, can only be adjusted in large, costly, and time-consuming

commitments. Development of new terminals, expansion of berths, and dredging are multi-year,

multi-million dollar projects. Expansion of existing terminal space can be undertaken more

easily and inexpensively, but can still take months or years in congested seaport areas.

In the shorter term, ports and terminals can add container cranes at a cost of $5-$10 million each,

with a lead time of multiple months rather than multiple years.

In the very short term ports and container terminals can adjust capacity along two dimensions:

container yard stacking density and operating hours. These are also ordinarily the only means by

which container terminals reduce capacity. Except in rare circumstances, terminal areas do not

shrink, berths do not get shorter, channels do not become shallower, and the number of cranes

does not decline. During seasonal or economic trade downturns, however, marine terminal

operators can reduce operating hours, reduce manning during operating hours, and revert to low-

density, low-cost container yard operations.

Berth Length

Berth length is published in many places. Berth length also tends to remain stable over long

periods, so the sources tend to be accurate. Container terminal berths are typically 600-1,000

feet. At many ports, however, the berth face is continuous across multiple berths or even across

multiple terminals (need example). Two 1,000-foot berths on a 2,000-foot face, therefore, can

accommodate vessels longer than 1,000 feet although not two at a time.

As most container vessels in service are less than 1,000 feet long and 1,000-foot berths are

common, berth length per se has seldom been a limiting factor. That will eventually change as

Post-Panamax and Super-Post-Panamax vessels become more common on the East and Gulf

Coasts.

The “Panamax” length limit is 965 feet and the width limit is 105 feet. Vessels

that transit the Canal can be as large as 5000 TEU, although most are much

smaller.

Typical “Post-Panamax” vessels are 1000+ feet long and 130+ feet wide.

Capacities range up to 10,000 TEU. These are the vessels targeted by the Panama

Canal expansion.

The largest “super-post-Panamax” vessels now being built in the 13,000-15,000

TEU range such as the Maersk E-Class, however, are 184 feet wide and 1300+

feet long.

Page 13

Tioga

Draft (Berth Depth)

Berth depth (and the depth of the channel required to reach the berth) is also commonly

published. It is seldom clear, however, whether the published figure is the authorized depth

(which may or may not have been fully maintained) or a measured and maintained depth. Given

the long-term outlook of the capacity estimates, it was assumed that the published depths would

be maintained.

It should be noted that the current draft limit for the Panama Canal is 39.5 feet, which is more

restrictive than most East Coast and Gulf ports. The new Canal locks are expected to allow

vessel with drafts if up to 60 feet, widths of up to 180 feet, and lengths of up to 1400 feet transit

the Canal.

Ports and terminal operators can provide capacity, but throughput is limited by the capacity of

the vessels than call and the percentage of that capacity that is discharged and loaded.

Berth depth was used to estimate the maximum vessel size that each port could accommodate.

The relationship between vessel design or maximum draft and size measured in deadweight tons

(DWT) or twenty-foot equivalent units (TEU) varies considerably, especially in very large

vessels (e.g. over 8,000 TEU). To develop a working relationship the study team assembled a

database of 350+ container vessels. A regression analysis yielded the relationship shown in

Exhibit 11.

Exhibit 11: Container Vessel DWT vs. TEU Capacity

Container Ship TEU vs. DWT

y = 0.0838x - 253.39

R2 = 0.9599

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

- 20,000 40,000 60,000 80,000 100,000 120,000 140,000 160,000 180,000

DWT

TE

U

N=353

This analysis is likely to be most reliable where there is the most data available, which is the

range of 20,000 to 80,000 DWT or 2,000 to 6,000 TEU. At the upper end of the range there are

fewer data available. It appears, moreover, that vessel designers have kept maximum drafts

within boundaries, and that the largest vessels are becoming wider rather than deeper.

Exhibit 12 compares the reported versus estimated TEU capacities where available. Significant

differences in reported and estimate TEU capacities should be expected because there are

substantial variations in the way the carriers themselves rate vessel capacity. A vessel can hold

Page 14

Tioga

more containers if they are light or empty, so a TEU capacity based on an illustrative average of

12 metric tons per TEU will be higher than an estimate for the same vessel at 13 or 14 metric

tons per TEU. These variations account for much of the disparity between vessels of similar size

and tonnage but different TEU capacities.

Exhibit 12: Reported vs. Estimated Container Vessel TEU

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Reported TEU

Est TEU

Exhibit 13 shows the relationship between DWT and draft, where both data items were available

for a given vessel.

Exhibit 13: DWT vs. Draft

y = 939e0.0972x

R2 = 0.9559

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

20 25 30 35 40 45 50 55

DW

T

Draft (ft)

N=119

Vessels rarely sail at their full design draft. To do so would entail a full load of loaded

containers, which is uncommon. USACE guidance (Exhibit 14) suggests that maximum

effective cargo capacity is typically about 95% of DWT. Applying this ratio to design draft

versus sailing draft suggests that a vessel designed for 50 feet draft would, for example, usually

Page 15

Tioga

sail at a maximum of 47.5 feet. While not a precise relationship, this guideline was adopted for

the capacity analysis.

Exhibit 14: USACE Guidance on Cargo Capacity as a Percentage of DWT TABLE 28

Adjustments for Estimating Actual Vessel Capacity

Short Tons of Cargo as a Percentage of Vessel DWT

Vessel DWT % Cargo to DWT

<20,000 90%

20,000 to 70,000 92%

70,000 to 120,000 95%

>120,000 97%

Source: IWR Report 91-R-13, National Economic Development

Procedures Manual, Deep-Drat Navigation, November 1991, p. 77.

Likewise, vessels rarely use the full channel depth. For safety reasons, pilot rules and common

practice typically require a minimum of 3 feet under keel. This rule is sometimes “bent”, and it

is common at some ports to “ride the tide” to gain additional clearance. Taking the long-term

view again, the capacity analysis incorporates the 3-foot minimum.

Together, these guidelines imply that a vessel with a 50-foot design draft would have a

maximum sailing draft of 47.5 feet and would need a channel depth of 50.5 feet to maintain a 3-

foot underkeel clearance.

This series of relationships was used to estimate the largest vessel size in TEU that could be

accommodated at each port, and the corresponding berth requirements for length and beam.

Exhibit 15 shows the estimated maximum vessel size for each port and the reported average

container vessel size for 2007. Most major ports receive a mix of vessels whose average size is

well below the maximum.

Exhibit 15: Maximum vs. Average Vessel Capacity - TEU

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Bost

on

NYNJ

Del

awar

e Riv

er

Bal

timore

VPA

Char

lest

on

Savan

nah

Jack

sonvi

lle

Port E

verg

lades

Mia

mi

Mobile

New

Orlea

ns

Houst

on

Avg. 2007 Vessel TEU Capacity

Est. Max Vessel TEU Capacity

Page 16

Tioga

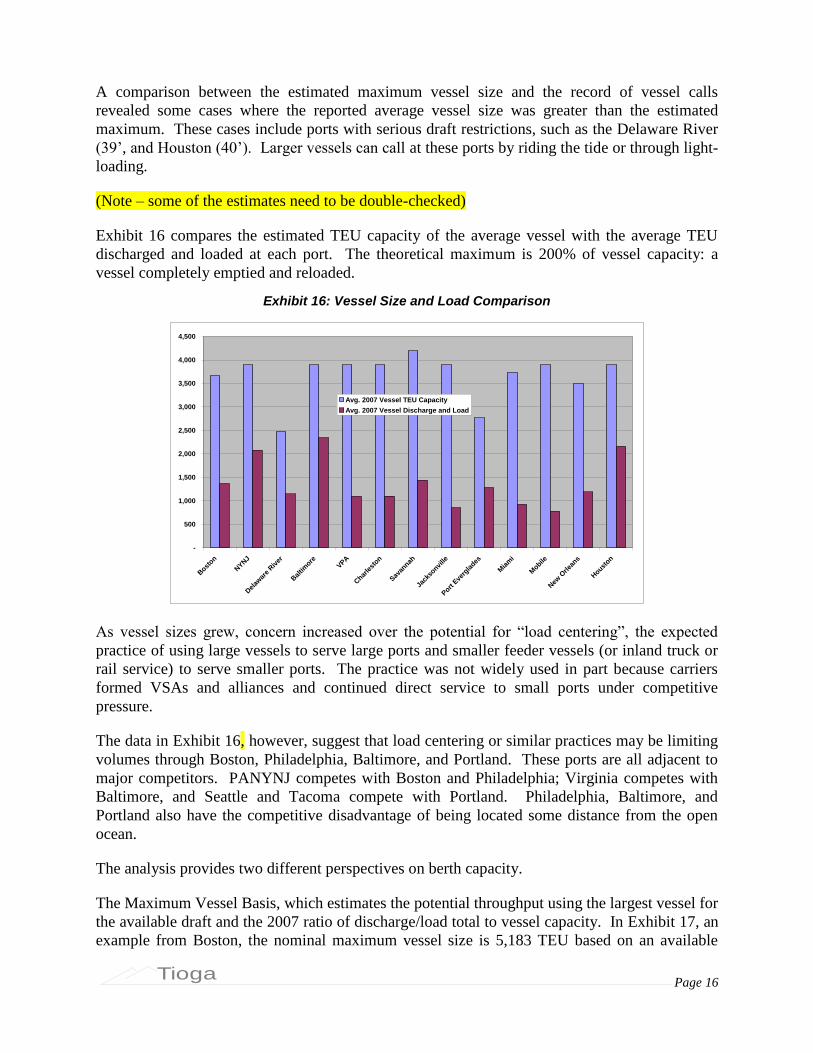

A comparison between the estimated maximum vessel size and the record of vessel calls

revealed some cases where the reported average vessel size was greater than the estimated

maximum. These cases include ports with serious draft restrictions, such as the Delaware River

(39’, and Houston (40’). Larger vessels can call at these ports by riding the tide or through light-

loading.

(Note – some of the estimates need to be double-checked)

Exhibit 16 compares the estimated TEU capacity of the average vessel with the average TEU

discharged and loaded at each port. The theoretical maximum is 200% of vessel capacity: a

vessel completely emptied and reloaded.

Exhibit 16: Vessel Size and Load Comparison

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Bost

on

NYNJ

Del

awar

e Riv

er

Bal

timore

VPA

Char

lest

on

Savan

nah

Jack

sonvi

lle

Port E

verg

lades

Mia

mi

Mobile

New

Orlea

ns

Houst

on

Avg. 2007 Vessel TEU Capacity

Avg. 2007 Vessel Discharge and Load

As vessel sizes grew, concern increased over the potential for “load centering”, the expected

practice of using large vessels to serve large ports and smaller feeder vessels (or inland truck or

rail service) to serve smaller ports. The practice was not widely used in part because carriers

formed VSAs and alliances and continued direct service to small ports under competitive

pressure.

The data in Exhibit 16, however, suggest that load centering or similar practices may be limiting

volumes through Boston, Philadelphia, Baltimore, and Portland. These ports are all adjacent to

major competitors. PANYNJ competes with Boston and Philadelphia; Virginia competes with

Baltimore, and Seattle and Tacoma compete with Portland. Philadelphia, Baltimore, and

Portland also have the competitive disadvantage of being located some distance from the open

ocean.

The analysis provides two different perspectives on berth capacity.

The Maximum Vessel Basis, which estimates the potential throughput using the largest vessel for

the available draft and the 2007 ratio of discharge/load total to vessel capacity. In Exhibit 17, an

example from Boston, the nominal maximum vessel size is 5,183 TEU based on an available

Page 17

Tioga

draft of 45 feet and a corresponding sailing draft of 42 feet. The current average vessel capacity

(2007) is estimated at 3,675 TEU, with a 37% discharge/load rate. At the same rate, a 5,183

TEU vessel would load and discharge 1,930 TEU at Boston. Based on a maximum of 260 calls

per year per berth (5 per week) and a sustainable estimate of 208 (80%) per berth. The annual

TEU capacity would be 803,012.

Exhibit 17: Berth Capacity - Maximum Vessel Basis Example

Berth Capacity - Max Vessel Basis Conley Port Total

Berths 2 2

Berth length 2,000 2000

Berth Depth - Feet 45 45

Max Sailing Draft 42 42

Corresponding Design Draft @ 95% 44 44

Corresponding DWT 63,678 63,678

Nominal Max Vessel TEU 5,183 5,183

Corresponding Vessel Length - Feet 1,000 1,000

Vessel Spacing (Beam) 140 140

Length requirement 1,140 1,140

Available Berths for Max Vessel 2.0 2.0

Port average TEU/container 1.73 1.73

2007 TEU 220,339 220,339

Avg. TEU/Vessel 1,369 1,369

Avg. Vessel DWT 45,571 45,571

Average Est. Vessel Capacity TEU 3,675 3,675

Average Discharge & Load % 37% 37%

Average TEU per Max Vessel 1,930 1,930

Max annual calls per berth 260 260

Sustainable Calls per berth @ 80% 208 208

Total Sustainable Vessel Calls 416 416

Annual Berth Capacity TEU 803,012 803,012

2008 Annual TEU 208,626 208,626

Berth Utilization, Max Vessel Basis 26% 26%

Alternatively, the berth capacity can be more conservatively estimated using the current average

vessel size and simply maximizing the number of calls (Exhibit 18).

Exhibit 18: Berth Capacity Estimate- Vessel Call Basis Example

Berth Utilization - Vessel Call Basis Conley Port Total

Max Calls per berth 5 / wk 260 260

Available Berths 2.0 2.0

Sustainable Calls per berth @ 80% 208 208

Total Sustainable Vessel Calls 416 416

2007 Vessel calls 161 161

2007 Berth Utilization 39% 39%

Container Yard Storage Density (Stacking Height)

Marine container terminal operators adjust container yard (CY) storage density and stacking

height by reconfiguring the CY, changing handling equipment, and varying container storage

practices. Typical handling equipment types are shown in Exhibit 19.

Page 18

Tioga

Exhibit 19: Container Yard Handling Equipment Types

TOP-PICK EMPTY HANDLERTOP-PICK EMPTY HANDLER REACH STACKERREACH STACKER SIDE LOADERSIDE LOADER

STRADDLE CARRIERSTRADDLE CARRIER RUBBER-TIRED GANTRY (RTG)RUBBER-TIRED GANTRY (RTG) RAIL-MOUNTED GANTRY (RMG)RAIL-MOUNTED GANTRY (RMG)

TOP-PICK EMPTY HANDLERTOP-PICK EMPTY HANDLER REACH STACKERREACH STACKER SIDE LOADERSIDE LOADER

STRADDLE CARRIERSTRADDLE CARRIER RUBBER-TIRED GANTRY (RTG)RUBBER-TIRED GANTRY (RTG) RAIL-MOUNTED GANTRY (RMG)RAIL-MOUNTED GANTRY (RMG)

Exhibit 20 displays the progression of terminal handling methods from lowest to highest density.

Virtually all U.S. marine container terminals use a mix of the handling methods shown in Exhibit

19 and Exhibit 20, and vary that mix to provide sufficient capacity at minimum cost. Terminal

operators gravitate to low-density, low-cost operating methods whenever possible.

Exhibit 20: Progression of Terminal Handling Methods

DENSITY TYPE COMMENT

Ro/Ro or Ship’s gear Very small, barge, specialized

Wheeled Combination Small, mixed, legacy

Dedicated Wheeled Older terminals when new

Wheeled/Top-pick Transition temrinals

Top-pick/Wheeled Transition temrinals

Straddle/Top-pick/Wheeled Hybrid terminal

RTG/Top-pick/Wheeled Dominant hyrbid type

Straddle Carrier NIT Virginia

RTG No US Example

VERY HIGH DENSITY Pure RMG APM Portsmouth

VERY LOW DENSITY

LOW DENSITY

MID DENSITY

HIGH DENSITY

Faced with a need to accommodate more trade, terminals move progressively up the density

scale.

Terminal operators start increasing density by stacking empty containers instead

of leaving them parked on chassis. Empties can be handled with inexpensive

equipment and stacked first-in/last-out since they are largely interchangeable.

Page 19

Tioga

As additional capacity is required, terminal operators begin stacking loaded

export containers. Export containers typically build up over the week prior to

vessel arrival and need not be accessed until it is time to load that vessel. Loaded

containers are heavier than empties, however, and must be accessed in a sequence

tied to vessel loading plans. Loaded export storage therefore usually requires

more expensive RTGs or straddle carriers.

Terminal operators typically leave loaded import containers parked on chassis

(“wheeled”) as long as possible to both minimize handling cost and maximize

responsiveness to customer needs. When loaded imports are eventually stacked,

they require RTG or straddle carriers for flexible access.

Containers with special requirement are rarely stacked, and most terminals

reserve space to keep such movements on chassis. Specialized movements

include refrigerated containers, containers with hazardous cargo, over-size or

over-weight containers, tank containers, and containers held for CBP inspection.

In peak periods, such as the annual holiday import surge, terminals shift the balance of

operations to higher densities. In slack periods, the operators park more containers on chassis.

In protracted downturns, such as the current recession, terminal operators will idle costly

handling equipment and revert to wheeled operations, even on space configured for stacking

(Exhibit 21).

Exhibit 21: Wheeled Containers on RTG Layout

IDLE RTGsIDLE RTGs

EMPTIES

STACKED WITH

TOP-PICKS

EMPTIES

STACKED WITH

TOP-PICKS

WHEELED

CONTAINERS

PARKED ON

RTG LAYOUT

WHEELED

CONTAINERS

PARKED ON

RTG LAYOUT

IDLE RTGsIDLE RTGs

EMPTIES

STACKED WITH

TOP-PICKS

EMPTIES

STACKED WITH

TOP-PICKS

WHEELED

CONTAINERS

PARKED ON

RTG LAYOUT

WHEELED

CONTAINERS

PARKED ON

RTG LAYOUT

The CY capacity estimation method used in this study is necessarily a compromise, based on a

“snapshot” of current stacking density. As shown in the example below, the team used the most

recent aerial photos available on Google Earth and estimated the CY acreage configured for each

storage density category. The precision of this method is necessarily limited in several respects.

The latest available aerial photos vary from a few months old to 2 to 3 years old,

and terminal configurations and uses can change on short notice.

Page 20

Tioga

Aerial estimates of acreage and uses are imprecise although probably sufficiently

accurate for high-level capacity estimates.

The container yard capacities were estimated by dividing the CY acreage by handling type and

applying the storage factors for each to derive estimated TEU slot totals. The typical storage

densities for terminal handling methods are shown in Exhibit 22.

Exhibit 22: Typical CY Storage Densities

CY Storage Method TEU Slots per Acre

Wheeled Chassis 80

Grounded Straddle Carrier 160

Grounded Stacked 200

Grounded RTG 300

Grounded RMG 360

The focus on capacity, rather than current throughput, led the team to rely more on terminal

configuration rather than on current usage or estimates. For example, terminal space configured

to use RTGs was assigned an inherent capacity of 300 TEU per acre even though it may

currently be used for wheeled storage at 80 TEU per acre. This estimation practice is also

necessarily imprecise as the ability to use the full inherent capacity of may depend on the

availability of handling equipment, operating systems, and other factors beyond the scope of this

study.

Exhibit 23 shows an example of CY acreage allocation in which the 79 total CY acres were

divided into 20 acres of wheeled storage at 80 TEU/acre, 43 acres of straddle carrier operation at

160 TEU/acre, 8 acres of stacked storage at 200 TEU/acre, and 8 acres of RTG storage at 300

TEU per acre for a total storage capacity of 12,480 TEU slots (Exhibit 24). If the terminal

needed more CY capacity, the operator would like stack more containers or expand RTG

operations at the expense of low-density wheeled storage. The average of 158 slots per acre is

between the low density of wheeled operations and the higher density of stacked or RTG

operations.

Exhibit 23: CY Acreage Example: Port of New Orleans

Terminal Space Napolean Port Total

Total Acres 128 128

Wheeled CY Acres 20 20

Straddle Carrier CY Acres 43 43

Stacked CY Acres 8 8

RTG CY Acres 8 8

RMG CY Acres -

Total CY Acres 79 79

On-Dock Rail Acres 10 10

Other Non-CY Acres 16 16

Net Berth/Gate/Yard Acres 105 105

Undeveloped Acres - -

Page 21

Tioga

Exhibit 24: CY Capacity Example: Port of New Orleans

Container Yard Capacity Napolean Port Total

Wheeled Chassis Slots 1,600 1,600

Grounded Straddle Carrier Slots 6,880 6,880

Grounded Stacked Slots 1,600 1,600

Grounded RTG Slots 2,400 2,400

Grounded RMG Slots - -

TEU Storage Slots 12,480 12,480

Avg TEU Slots/CY Acre 158 158

Maximum Annual Slot Turnover 70.0 70.0

Maximum Annual CY TEU Capacity 873,600 873,600

Sustainable CY TEU Capacity @ 80% 698,880 698,880

2008 Annual TEU 313,765 313,765

2008 TEU per CY Slot 25 25

2008 CY Capacity Utilization 45% 45%

As Exhibit 24 shows, the team estimated the maximum annual TEU capacity based on a

maximum annual slot turnover of 70 turns annually, an aggressive average of more than one turn

per week and equivalent to an average container dwell time of slightly over 5 days. While

theoretically possible, particularly in periods of peak demand, operation at this level of intensity

is unlikely to be sustainable day-in and day-out. Moreover, if this level of density were routine

there would be no reserve capacity to handle the inevitable trade surges. The study team

therefore also estimated sustainable CY TEU capacity at 80% of the maximum, following a

common industry rule-of-thumb. There is only one major container terminal at the Port of New

Orleans, so in the examples above the port total is the same as the Napoleon terminal total.

2008 annual TEU counts were compared with the estimated sustainable TEU capacity to

estimate the annual TEU per storage slot (25 in the example) and average annual CY capacity

utilization (45% in the example).

Under greater pressure, such as was experienced in Southern California before the current

recession, marine terminals can also increase capacity by reducing container dwell times. By

shortening “free time” allowances and raising or vigorously enforcing charges for excess dwell

time, terminal operators have succeeded in reducing dwell times for import loads and therefore

increasing storage turnover. On the export side, terminals can limit the time in advance of vessel

arrival during which export containers will be accepted. To reduce the dwell time of empty

containers, terminal operators and their ocean carrier clients can move empties to off-terminal

depots or return leased containers to leasing company depots.

Operating Hours

Port terminals occasionally vary operating hours to handle additional vessels or cope with trade

surges. Marine container terminals typically maintain full cargo handling and gate functions for

a single shift five to six days per week. Additional shifts are often operated to handle arriving or

departing vessels and complete loading or unloading, even if full gate and truck handling

functions are not supported. In peak periods, terminals will extend gate hours to handle inbound

and outbound truck movements. At the busiest ports, such as NYNJ or LALB, extended age

hours are a regular feature.

Page 22

Tioga

Labor agreements specify the options available to terminal operators and the attendant costs.

Marine terminal operators attempt to match labor supply and costs with vessel and trade

requirements. The rigidities of these agreements make it difficult and costly for terminal

operators to extend operating hours or to match labor supply closely with trade and vessel

requirements. So although container terminal throughput and capacity could be greatly increased

by adding shifts, that option is usually the last choice for any extended period.

Vessels and Crane Use

Container terminal throughput is limited by the size and utilization of the vessels that call. As

Exhibit 16 suggests, the average vessel that calls at most ports discharges and loads substantially

less than its full capacity. There are two basic reasons for this disparity.

Vessels almost invariably call at multiple U.S. ports on each voyage, and the

vessel’s total cargo discharge and load is split among those ports.

Ocean carriers, like ports and terminals, offer and deploy sufficient capacity to

accommodate growth as well as current cargo volumes. Only in peak periods of

peak years will vessels be completely full.

The ability to handle a given vessel size depends on the berth length and draft available at the

terminal. The ability to handle the cargo from that vessel depends on the number of cranes

available, the hourly throughput capability of those cranes, and the hours those cranes are

available in a day or week.

A typical marine terminal, such as the one shown in Exhibit 25, might have two berths and four

cranes. This configuration gives the terminal operator the flexibility to assign from one to four

cranes to a vessel as required. as the vessel discharge and load averages increase, the number of

cranes may limit the number of vessels that can be handled simultaneously and therefore

annually. As this limit is approached the port or terminal operator will add cranes.

Page 23

Tioga

Exhibit 25: Typical Two-Berth/Four-Crane Terminal

The primary goal of terminal operators is to service the vessel or schedule and at minimum cost.

The number of cranes installed and used is determined primarily by the need to “turn” the vessel,

with annual crane productivity a secondary consideration. This set of priorities results in

relatively low container crane utilization, as suggested by Exhibit 26. A vessel is far more costly

to own and operate than the cranes that serve it, so crane utilization is effectively sacrificed to

vessel utilization.

Exhibit 26: Container Cranes and Utilization

Container CranesN. Atlantic

Ports*

S. Atlantic

PortsGulf Ports

East & Gulf Coast

Ports

Cranes 120 77 27 224

Cranes per Berth 2.1 1.8 2.1 2.0