consumer discretionary reza aditya hakan altan adam barrick peter manuselis

TRANSCRIPT

Consumer DiscretionaryReza Aditya

Hakan Altan

Adam Barrick

Peter Manuselis

Agenda

• Sector Recommendation Recap

• Stock Selected Overview

• Financial Analysis

• Valuation Analysis

• Stock Recommendation

Current SIM Holdings

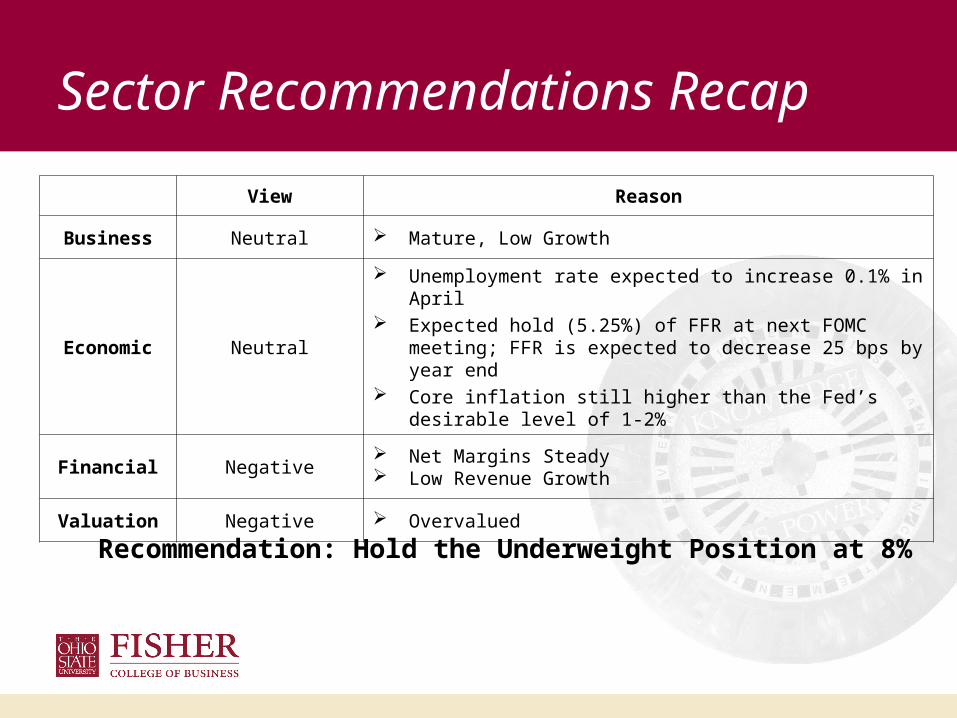

Sector Recommendations Recap

View Reason

Business Neutral Mature, Low Growth

Economic Neutral

Unemployment rate expected to increase 0.1% in April Expected hold (5.25%) of FFR at next FOMC meeting; FFR is

expected to decrease 25 bps by year end Core inflation still higher than the Fed’s desirable level of 1-

2%

Financial Negative Net Margins Steady Low Revenue Growth

Valuation Negative Overvalued

Recommendation: Hold the Underweight Position at 8%

Current Position

Shares Purchase Price

Current Price

(5/11/07)

Unrealized Gain/(Loss)

Market Value

SIM Weight

Coach 14,000 $42.78 $47.84 $70,840 $669,760 2.92%

Limited Brands

23,400 $26.08 $27.67 $37,206 $647,478 2.54%

Carnival 12,000 $39.83 $48.79 $107,520 $585,480 2.34%

Nike Overview

– 2006 Revenue $14,955 MM (8.8% increase from ‘05)

– 2006 Net Income $1,392 MM (14.9% increase from ‘05)

– 2006 EPS $2.64 (17.9% increase from ‘05)

– 52 week range: $37.76 – $55.10

– Completed a 2 – 1 stock split on April 2, 2007

– Current Price as of 5/14/07 - $52.87

– 1.4% Div. Yield

Catalysts• Strong market position and brand

– Number one shoemaker, holding a 40% market share of the global footwear industry

– World’s largest manufacturer of athletic apparel– Nike swoosh sign is one the most widely recognized logo– Relatively inelastic demand

• Robust financial performance– Strong cash position that will provide funding for future expansion strategies

• Strong product portfolio– Reduced dependence on footwear and has established a strong position in the

equipment and apparel markets– Offers specialized sports gear for sports including golf, hockey, skateboarding,

and cycling– Allows them to spread risk across its product segments

Financial AnalysisStockVal®NIKE INCORPORATED (NKE) Price 53.03

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 20081997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

PRICE12

16

20

24

32

44

56

HI 55LO 13ME 28CU 53GR 6.6%

05-09-199705-11-2007

REVENUE-PER-SHARE15

17

19

22

25

28

32

HI 31LO 15ME 18CU 31GR 7.5%

05-31-199702-28-2007

EARNINGS-PER-SHARE0.4

0.6

0.8

1.0

1.4

2.0

2.8

HI 2.68 LO 0.57 ME 1.31 CU 2.68 GR 7.4%

05-31-199702-28-2007

• Stock price, Revenue/share,EPS are increasing.

StockVal®NIKE INCORPORATED (NKE) Price 53.031997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 20081997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

PRICE RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0.2

0.3

0.4

0.6

0.8

1.1

HI 1.05 LO 0.27 ME 0.68 CU 0.91

05-09-199705-11-2007

REVENUE-PER-SHARE RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0.8

0.9

1.0

1.1

1.2

HI 1.18 LO 0.85 ME 1.01 CU 1.18

06-30-199703-31-2007

EARNINGS RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0.3

0.4

0.5

0.6

0.8

1.0

1.2

HI 1.18 LO 0.39 ME 0.92 CU 1.13 FY1 1.16 FY2 1.08

06-30-199703-31-2007

Financial Analysis

• Relative to Consumer discretionary sectorStock price, Revenue/share,EPS are increasing.

StockVal®NIKE INCORPORATED (NKE) Price 53.031997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

DIVIDENDS-PER-SHARE RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd1.0

1.2

1.4

1.6

1.8

2.0

2.4

HI 2.38 LO 1.00 ME 1.44 CU 2.34

06-30-199712-31-2006

TOTAL RETURN RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0.2

0.3

0.4

0.6

0.8

1.1

HI 1.05 LO 0.28 ME 0.68 CU 0.90

05-09-199705-11-2007

GROWTH RATE ESTIMATE RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0.6

0.7

0.8

0.9

1.0

1.1

HI 1.06 LO 0.70 ME 0.91 CU 1.05

05-09-199705-04-2007

Financial Analysis

• Dividends/shareare higher compared to Cons Disc.

•Growth rate estimates are going up compared to Cons Disc.

StockVal®NIKE INCORPORATED (NKE) Price 53.032002 2003 2004 2005 2006 20072002 2003 2004 2005 2006 2007 2008

PRICE / YEAR-FORWARD EARNINGS RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0.7

0.8

0.9HI 1.00 LO 0.71 ME 0.85 CU 0.83

05-10-200205-11-2007

PRICE / EBITDA RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0.8

1.0

1.2

1.4HI 1.75 LO 0.94 ME 1.27 CU 1.49

05-10-200205-11-2007

PRICE / SALES RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd1.2

1.4

1.6

1.8 HI 1.81 LO 1.34 ME 1.62 CU 1.71

05-10-200205-11-2007

PRICE / BOOK VALUE RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd1.2

1.4

1.6

1.8 HI 1.87 LO 1.27 ME 1.54 CU 1.35

05-10-200205-11-2007

Valuation Analysis – 5yr

CU < ME

Trending Down

CU > ME

Trending Down

CU > ME

Stable

CU < ME

Trending Down

Valuation Analysis – 5yrStockVal®NIKE INCORPORATED (NKE) Price 53.03

2002 2003 2004 2005 2006 20072002 2003 2004 2005 2006 2007 2008

PRICE / CASH FLOW ADJUSTED RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd1.24

1.30

1.35

1.40

1.45

1.50

1.55

1.60

1.65

1.70

1.75

1.80

1.85

1.90

1.95

2.00

2.05

HI 2.03 LO 1.29 ME 1.56 CU 1.54

05-10-200205-11-2007

CU < ME

Trending Down

Valuation Summary 5-yr

HI LO ME CU

P/E 1.00 0.71 0.85 > 0.83

P/EBITDA 1.75 0.94 1.27 < 1.49

P/S 1.81 1.34 1.62 < 1.71

P/BV 1.87 1.27 1.54 > 1.35

P/CF 2.03 1.29 1.56 > 1.54

StockVal®NIKE INCORPORATED (NKE) Price 53.031997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

PRICE / YEAR-FORWARD EARNINGS RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0

1

2HI 2.16 LO 0.45 ME 0.86 CU 0.83

05-09-199705-11-2007

PRICE / EBITDA RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0.8

1.2

1.6

2.4 HI 3.14 LO 0.88 ME 1.44 CU 1.49

05-09-199705-11-2007

PRICE / SALES RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0

1

2HI 2.33 LO 0.67 ME 1.52 CU 1.71

05-09-199705-11-2007

PRICE / BOOK VALUE RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0

1

2HI 2.13 LO 0.61 ME 1.43 CU 1.35

05-09-199705-11-2007

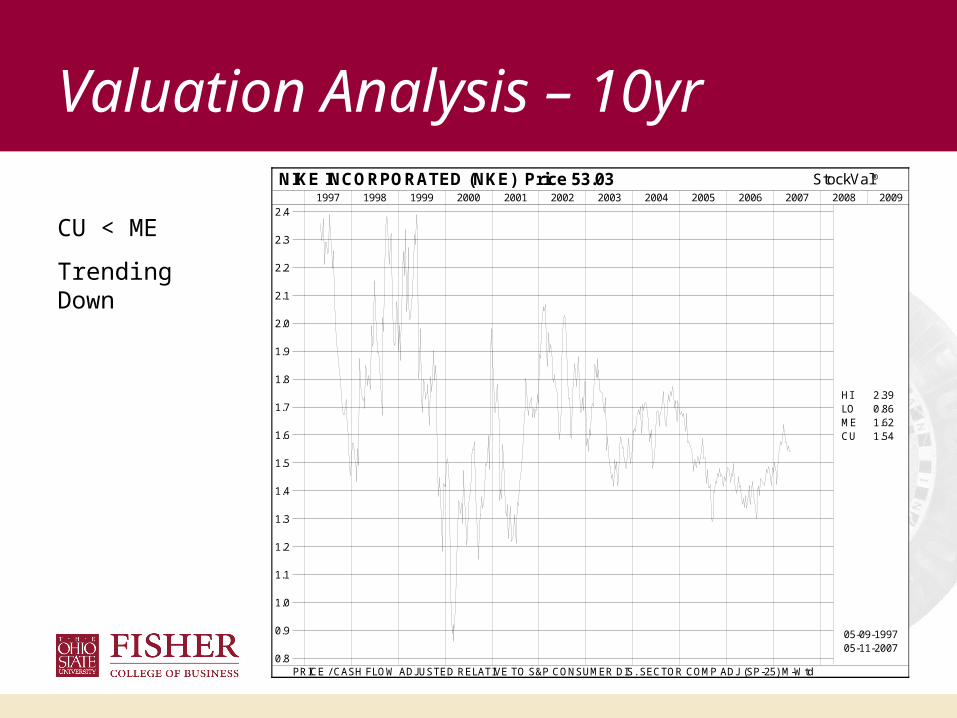

Valuation Analysis - 10yr

CU < ME

Stable

CU > ME

Trending Up

CU > ME

Stable

CU < ME

Stable

Valuation Analysis – 10yrStockVal®NIKE INCORPORATED (NKE) Price 53.03

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 20081997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

PRICE / CASH FLOW ADJUSTED RELATIVE TO S&P CONSUMER DIS. SECTOR COMP ADJ (SP-25) M-Wtd0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

2.3

2.4

HI 2.39 LO 0.86 ME 1.62 CU 1.54

05-09-199705-11-2007

CU < ME

Trending Down

DCF AnalysisNIKEDCF Valuation ($MM) 2007E 2008E 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016ERevenues $16,151 $17,443 $18,839 $19,875 $20,968 $22,174 $23,449 $24,856 $26,347 $27,928

% Growth 8.0% 8.0% 5.5% 5.5% 5.8% 5.8% 6.0% 6.0% 6.0%Operating Income (EBIT) $2,261 $2,442 $2,637 $3,826 $4,036 $4,268 $4,514 $4,785 $5,072 $5,376

% Revenues 14.0% 14.0% 14.0% 19.3% 19.3% 19.3% 19.3% 19.3% 19.3% 19.3%D&A $323 $349 $377 $497 $524 $665 $703 $746 $659 $698

% Revenues 2.0% 2.0% 2.0% 2.5% 2.5% 3.0% 3.0% 3.0% 2.5% 2.5%EBITDA $2,584 $2,791 $3,014 $4,323 $4,561 $4,934 $5,217 $5,530 $5,730 $6,074

CAPEX ($323) ($349) ($377) ($497) ($524) ($665) ($703) ($746) ($659) ($698)% Revenues 2.0% 2.0% 2.0% 2.5% 2.5% 3.0% 3.0% 3.0% 2.5% 2.5%

Net Change in WC ($350) ($226) ($244) ($199) ($210) ($111) ($117) ($124) ($263) ($279)% Revenues 2.2% 1.3% 1.3% 1.0% 1.0% 0.5% 0.5% 0.5% 1.0% 1.0%

Taxes ($791) ($855) ($923) ($1,339) ($1,413) ($1,494) ($1,580) ($1,675) ($1,775) ($1,882)Tax Rate 35% 35% 35% 35% 35% 35% 35% 35% 35% 35%Free Cash Flow $1,119 $1,361 $1,470 $2,288 $2,414 $2,664 $2,817 $2,986 $3,033 $3,215

Growth Rate 4%Discount Rate (CAPM) 10%Terminal Enterprise Value $55,730Implied Term. Value EBITDA Multiple

9.2x

Discounted Free Cash FlowNPV Free Cash Flow $1,018 $1,125 $1,105 $1,563 $1,499 $1,504 $1,445 $1,393 $1,286 $1,240NPV Terminal Value $21,486

Total Discounted Cash Flows$34,663 $1,018 $1,125 $1,105 $1,563 $1,499 $1,504 $1,445 $1,393 $1,286 $22,726

Summary DCF Valuation DCF Value per Share

DCF Enterprise Value $34,663 14.5 x EBITDA Discount Rate

Less: Net Debt $1,724 Growth 8.0% 9.0% 10.0%Equity Value $36,387 3.0% 89.2 73.8 62.8

Shares 528 4.0% 104.4 83.1 69.0DCF Value per Share $68.97 5.0% 129.8 97.1 77.6

6.0% 180.6 120.5 90.57.0% 333.0 167.3 112.0

Stock Recommendations

View Reason

Business Positive

Strong market position and brand Robust Financial Performance Strong product portfolio

Financial Positive Revenue, EPS, are going up relative to Consumer Discretionary

DCF Positive Target Price $69, 30% upside

Valuation Neutral On par with the mean

Recommendation: Buy

Risks

• Rising raw material cost

– Rising oil prices increase the price of synthetic rubber and plastic based products. Increasing raw material cost would increase the production cost and its profitability.

• Chinese products

– Chinese footwear has been flooding the EU and can significantly affect Nike’s market share in the EU

• Intense competition

– The launch of technologically superior products by competitors such as Adidas could lead to a fall in the company’s market share

Action RecommendationCorrelation with NKE

Current Weight

Proposed Weight

Proposed Change

Proposed $ Amount

Proposed # of Shares

Current # Shares

Change # of shares

COH .44 37% 19% -18% $356,398.41 7,450 14,647 (7,197)

LTD .37 33% 22% -10% $414,643.23 14,985 22,038 (7,053)

CCL .33 30% 24% -6% $446,293.96 9,147 11,525 (2,378)

NKE 1 NA 35% 35% $655,488.40 12,368 0 12,368

Sharpe 2.20 4.88 2.68

Questions?