construction seta - masterbuilders.org.za 2... · ceta sector skills plan for the construction...

TRANSCRIPT

1

CONSTRUCTION SETA

CETA Sector Skills Plan for the Construction Industry

Skills Perspective

Friday 02 September 2016, Durban ICC Hall 5 (10:15-10:45)

Thapelo Madibeng: Core Business Executive -CETA

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

3

Strategic Overview of the CETA

Research Process and Methods

Chapter 1: Sector Profile(an overview of the sector economic, social and labour)

Chapter 2: Key Skills Issues(drivers of change, key skills issues impacting on economic performance)

Chapter 3: Extent of Skills Mismatches(imbalances on skills supply and demand)

Chapter 4: Sector Partnerships(who do we work with and why)

Chapter 5 Skills Priority Actions(what must we do)

www.limp.org.za, www.ceta.org.za www.dhet.gov.za

THE SSP HAS BEEN STRUCTURED AS FOLLOWS:

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

4

VISION

To be a firm pillar of skills for all in construction and nation-building

MISSION

To create a solid skills base as a foundation for infrastructural development and economic

empowerment

VALUES

• Responsiveness

• Respect

• Integrity

• Professionalism

ESTABLISHMENT OF THE CETAThe Construction Education and Training Authority (CETA) is a Schedule 3A public entity which was

established as a SETA under Skills Development Act, 1998 by the Minister of Labour on 20 March 2000. In

2010, all SETAs’ functions were transferred to the Department of Higher Education and Training (DHET),

which resulted in the CETA subsequently being re-established by the Minister of Higher Education and

Training with its current licensing period expiring on 31 March 2018. CETA CFO has addressed 111th MBSA

congress on 01 Sep 2016 regarding the new SETA Landscape post March 2018.

STRATEGIC OVERVIEW OF THE CETA

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

5

WHY DO WE EXIST AS THE CONSTRUCTION SETA?

• The mandate of the CETA is to facilitate and fund skills development in the construction sector

in South Africa

• Extended National Skills Development Strategy (NSDS) III, CETA Sector Skills Plan (SSP);

Strategic Plan and Annual Performance Plans

The CETA therefore is responsible for:

• Review, development and registration of qualifications;

• Accreditation of providers and the registration of practitioners;

• The implementation of quality assurance processes that will enhance and ensure quality

provision of training;

• Funding of critical and scarce skills in the sector through the allocation of discretionary grants;

• The disbursements of mandatory grants based on the submission of Workplace Skills Plans

(WSPs) and Annual Training Reports (ATRs) by levy paying companies in the construction

sector.

STRATEGIC OVERVIEW OF THE CETA: MANDATE

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

6

% ALLOCATION OF LEVIES

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

SETAs are financed from the skills development levy which is paid and distributed as follows as prescribed in the Grants Regulations and Skills Development Levies Act: % levies distribution as per the Gazette 35940 of SETA Grant Regulations of 03 December 2012, the new levy grants system guiding the CETA funding model:

Levy Grant system Element Allocation % Conditions

Total levy 100% 1% of Remuneration Costs

SARS Collection Fee 2.0% Maximum of 2%

NSF Administration 18% % prescribed by Minister

SETA Administration 10.5% Maximum of 0.5% is transferred by the CETA to QCTO

Mandatory Grant 20%

Unclaimed Mandatory Grants are transferred to

Discretionary Grants by 15 August

Discretionary Grant 49.5%Maximum of 80% is allocated by CETA to PIVOTAL and

20% to NON-PIVOTAL.

7

1: Desktop Research: (delving into and analysing secondary research sources)

2: Quantitative Research: (analysing and interpreting formal statistics)

3: Field Research (focus groups and interviews)

4: Action Research (data gathered as a source of intelligence leading to further analysis)

RESEARCH PROCESS:• The SSP Research is a continuous process commencing immediately after

submission for the next update. Stakeholders are invited to participate in this

review process.

• White Paper on Post School Education and Training System (PSET) & new

proposed SETA landscape emphasizes credible research to inform skills planning

and funding allocation.

• Labour market information intelligence project - LMIP

SSP RESEARCH WAS EXECUTED USING 4 METHODS:

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

8

CHAPTER 1: SECTOR PROFILE

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

9

CETA covers 72 SIC codes grouped under 4 sub-sectors representing 49 161 employers

• 1 Consolidated SSP for the Construction Sector.

• Regrouping or reclassification of the Codes per subsector

• OFO changes or new occupations – Industry OFO Workshop – WSP Feb 2016 (SDF)

* Registered with CETA as at 2016

** Includes Electrical Construction Contractors

CATEGORY # SIC CODES # EMPLOYERS*

Building Construction 13 10 461

Built Environment Professionals 16 7300

Roads and Civil Construction 27 27 553**

Materials Manufacturing 16 3 847

SIZE OF THE CONSTRUCTION SECTOR(By 4 Main Subsectors, Standard Industry Classification (SIC) Codes and CETA

registered Employers)

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

10

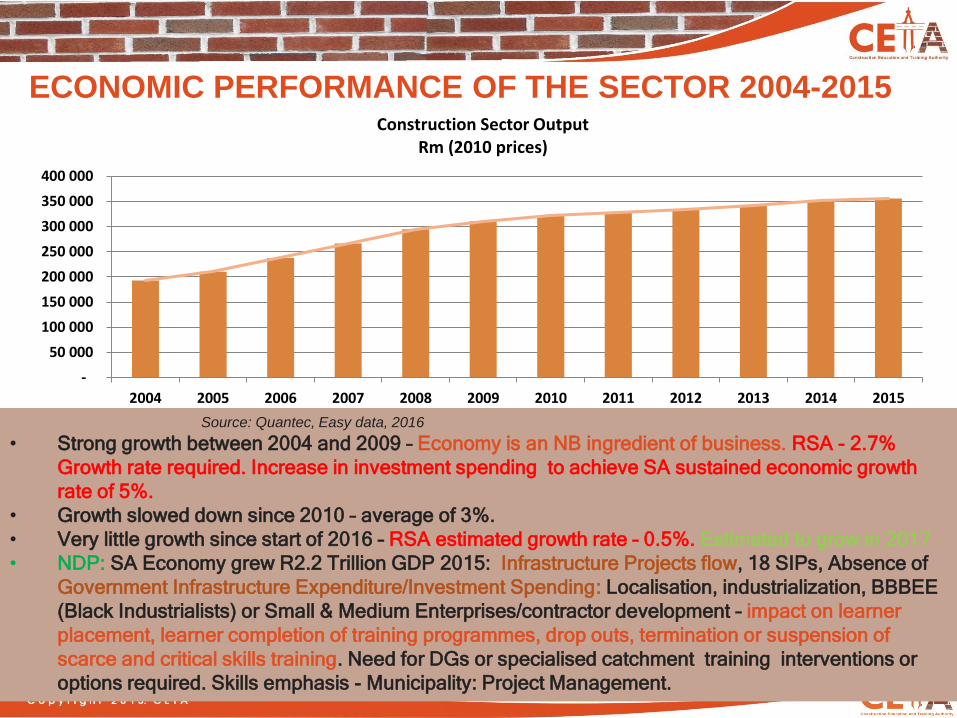

Source: Quantec, Easy data, 2016

• Strong growth between 2004 and 2009 – Economy is an NB ingredient of business. RSA - 2.7%

Growth rate required. Increase in investment spending to achieve SA sustained economic growth

rate of 5%.

• Growth slowed down since 2010 – average of 3%.

• Very little growth since start of 2016 – RSA estimated growth rate – 0.5%. Estimated to grow in 2017

• NDP: SA Economy grew R2.2 Trillion GDP 2015: Infrastructure Projects flow, 18 SIPs, Absence of

Government Infrastructure Expenditure/Investment Spending: Localisation, industrialization, BBBEE

(Black Industrialists) or Small & Medium Enterprises/contractor development – impact on learner

placement, learner completion of training programmes, drop outs, termination or suspension of

scarce and critical skills training. Need for DGs or specialised catchment training interventions or

options required. Skills emphasis - Municipality: Project Management.

-

50 000

100 000

150 000

200 000

250 000

300 000

350 000

400 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Construction Sector OutputRm (2010 prices)

ECONOMIC PERFORMANCE OF THE SECTOR 2004-2015

11

Source :BIM 2016

• It is anticipated that most investment will happen in Mpumalanga, followed

by KZN and Limpopo

• Gauteng is expected to only attract 11% of investment

PROVINCIAL DISTRIBUTION OF INFRASTRUCTURE INVESTMENT

Gauteng11%

Limpopo22%

Mpumalanga37%

North West0%

KwaZulu-Natal16%

Eastern Cape4%

Western Cape6%

Northern Cape4%

Free State0%

12

• Grade 1 and 2 employers can be regarded as small and emerging entities • This is further amplified by CETA WSP data that the majority of firms fall within the micro to small

category – 97%• SSP Implication: micro, small enterprises do not pay levies, no MG disbursements and therefore

dependent on discretionary grants for training interventions; technical training, contractor development programmes, Interdependencies exists.

• Sustained small or emerging contractors that are expanding to provide more opportunities for employment, workplace training for learners.

• Contractor Development Programme – No formalised Programme and certification –CIDB -Individual vs entity skills development approach, Skills Standard – implementation? NC: Construction Contracting, NQF Level 2, CETA provide learning materials to providers – accreditation of training providers.

EMPLOYERS IN THE CONSTRUCTION SECTOR BY GRADING CATEGORY

Category Grade 1 Grade 2 Grade 3 Grade 4 Grade 5 Grade 6 Grade 7 Grade 8 Grade 9

TenderValue Limit(R)

200 000 500 000 2 mil 4 mil 6.5 mil 13 mil 40 mil 130 mil >130 mil

# Reg. 136 138 5 797 2 336 2 887 1 891 2 159 1229 459 216

% of Tot. 89% 3.8% 1.5% 1.9% 1.2% 1.4% 0.8% 0.3% 0.1%

13

CONSTRUCTION EMPLOYERS SUBMITTING WSP-ATR TO THE CETA

PROVINCE TOTAL STAKEHOLDERS IN ATTENDANCE

KwaZulu Natal 20

Free-State 6

Eastern Cape 23

Northern Cape 10

Western Cape 29

Limpopo 13

Gauteng 73

North West 21

Mpumalanga 22

The CETA trained 217 Skills Development Facilitators (SDFs) in the compilation and submission of their WSPs and ATRs. The training was done through capacity building workshops which were conducted in all nine (9) provinces.

14

EMPLOYMENT IN THE CONSTRUCTION SECTOR

200

400

600

800

1 000

1 200

1 400

1 600

Jan

-Mar

20

08

Ap

r-Ju

n 2

00

8

Jul-

Sep

20

08

Oct

-Dec

20

08

Jan

-Mar

20

09

Ap

r-Ju

n 2

00

9

Jul-

Sep

20

09

Oct

-Dec

20

09

Jan

-Mar

20

10

Ap

r-Ju

n 2

01

0

Jul-

Sep

20

10

Oct

-Dec

20

10

Jan

-Mar

20

11

Ap

r-Ju

n 2

01

1

Jul-

Sep

20

11

Oct

-Dec

20

11

Jan

-Mar

20

12

Ap

r-Ju

n 2

01

2

Jul-

Sep

20

12

Oct

-Dec

20

12

Jan

-Mar

20

13

Ap

r-Ju

n 2

01

3

Jul-

Sep

20

13

Oct

-Dec

20

13

Jan

-Mar

20

14

Ap

r-Ju

n 2

01

4

Jul-

Sep

20

14

Oct

-Dec

20

14

Jan

-Mar

20

15

Ap

r-Ju

n 2

01

5

Jul-

Sep

20

15

Oct

-Dec

20

15

Jan

-Mar

20

16

Source : StatsSA QLFS, Q1 of 2016

• From 2012 to the second quarter 2015 employment was growing strongly• As from third quarter 2015 a gradual decline in employment• An alarmingly sharp decline as from first quarter 2016• SA elevated unemployment rate – 35%

15

GENDER DISTRIBUTION OF EMPLOYEES

0%

10%

20%

30%

40%

50%60%

70%

80%

90%

100%

Jan

-Mar

20

08

Ap

r-Ju

n 2

00

8

Jul-

Sep

20

08

Oct

-Dec

20

08

Jan

-Mar

20

09

Ap

r-Ju

n 2

00

9

Jul-

Sep

20

09

Oct

-Dec

20

09

Jan

-Mar

20

10

Ap

r-Ju

n 2

01

0

Jul-

Sep

20

10

Oct

-Dec

20

10

Jan

-Mar

20

11

Ap

r-Ju

n 2

01

1

Jul-

Sep

20

11

Oct

-Dec

20

11

Jan

-Mar

20

12

Ap

r-Ju

n 2

01

2

Jul-

Sep

20

12

Oct

-Dec

20

12

Jan

-Mar

20

13

Ap

r-Ju

n 2

01

3

Jul-

Sep

20

13

Oct

-Dec

20

13

Jan

-Mar

20

14

Ap

r-Ju

n 2

01

4

Jul-

Sep

20

14

Oct

-Dec

20

14

Jan

-Mar

20

15

Ap

r-Ju

n 2

01

5

Jul-

Sep

20

15

Oct

-Dec

20

15

Jan

-Mar

20

16

Female Male

Source : StatsSA QLFS, Q1 of 2016

• Vast majority of employees are male (±𝟖𝟖%)• Marginal growth in female employees – from 9% in 2008 to 12% in 2016

• Vast majority of employees are male (±88%)• Marginal growth in female employees – from 9% in 2008 to 12% in 2016. United Nations Sustainable Goal No.

5 “Gender Equality” – 50-50 target female representivity at all occupational levels.• Transformation makes business sense, diverse workforce -16th Employment Equity Report shows

improvement in representation of women in top management. 51.2% white males terminated at Top Management re-enter through recruitment – 42,1%, not lost in the system but come back to different organisations at the same level.

• Trends in Skills Development is dissapointing at Top/Senior Management: white group benefitted from skills development (males – 47.7% and females - 13.4%) - preferential treatment to white group at the expense of designated group in terms of skills development.

16

Source : CETA WSP submissions, 2016

• Low, mid-level and unskilled occupations – 70% of workforce• Similar to South African profile – 46%semi-skilled and 29% low/unskilled• 65% employed in the construction sub-sector

MAJOR OCCUPATIONAL GROUPS PER SUB-SECTOR

OFO Major Category Building sector

Built Environment Professions

Construction Materials Manufacturing

Total

Clerical support workers 957 2960 9198 1531 15071

Elementary occupations 8078 3511 62383 13460 90990

Managers 2165 3339 14306 1825 22070

Plant and machine operators and assemblers

2161 1355 19789 6276 30820

Professionals 728 9014 8392 492 19273

Service and sales workers 306 563 2329 439 3655

Skilled agricultural, forestry, fishery, craft and related trades workers

4679 2496 23657 2710 33995

Technicians and associate professionals

1452 6280 17193 2042 27753

Total 20526 29518 157247 28775 243627

17

A SWOT ANALYSIS OF THE CONSTRUCTION SECTORStrengths Weaknesses

Recovery from economic slump evident-InfrastructureInvestment - NDP

Business rescue plan has helped some companiessurvive closure

Strong research culture among industry bodies Inter-dependencies between small and large companies

means they can sustain each other

Reliance on government for work and poor spendingrecord of government negatively affects work flow

Many small companies do not pay levies Capital outlay prior to payment for work Large informal sector Project by project work means no benefits for workers

& casualization of labour Slow transformation within built environment industry

Opportunities Threats

SIPs spending pegged at R4 trillion over the next 15years. Public and Private Infrastructure

Poor maintenance culture by government(particularlyat municipal level) of roads, and buildings(infrastructure)leads to work

Large companies have opportunities for expansioninternationally and regionally within SADC and rest ofAfrica through inter-Africa investment: PIDA –Programme for Infrastructure Development in Africa

Contractor development programmes can uplift lowergraded contractors and also focus on the developmentof rural contractors to position them for SIPs

Sector growth partly depends on economic growth andstability

Shortage of material e.g. bitumen can affect outcomes Reduction of public sector spending will affect the

sector – so far reduction of up to 30% since 2008 Unfair tender or supply chain practices Small companies rely on local government and this is

where most poor spending is . R800b allocated bygovernment to Infrastructure Projects, R300bdisbursed

Adverse national and sectoral reputational riskaffecting investor confidence in turn SMMEdevelopment

18

CHAPTER 2: KEY SKILLS ISSUES

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

19

National Development Plan is a detailed blueprint for how the country can eliminate poverty

and reduce inequality by the year 2030.

Cutting across all infrastructural projects and initiatives is the operation and

maintenance of such infrastructure post establishment

DRIVERS OF CHANGE AND IMPLICATIONS FOR SKILLS PLANNING

DRIVERS OF CHANGE

Technological

advancement and

innovation-Advanced

mechanisation, robotics

and digitisation – new skills,

Dev. of localised

technology .

NDP Vision 2030 &

Campaign, National

Infrastructure Plan-

PICC (2011). 9 Point

Plan – Economic

Growth, Social

Development

Environmental

sustainability and Green

Economy-Curricula

review, top up skills for

technicians, artisans,

energy modelling

services

Occupational Health

and Safety – more

Specialised,

curricular review, top

up skills, changing

health and safety

stds, accredited

training

Construction Regulations -

Construction Health and

Safety (CHS) Professionals

– 3 Categories:Health and

Safety Agent (PrCHSA),

Health and Safety Manager

(CHSM), Health and Safety

Officer (CHSO)

20

IMPLICATIONS FOR SKILLS PLANNING

National Strategy/Plan CETA’s current and envisaged role

Strategic Infrastructure

Projects

• CETA will have to engage with all 18 SIPS as each has relevance to

construction industry.

• Skills forecasting for SIPS – skills development and WIL opportunities• SIPs Priority Occupations.• Presidential Infrastructure Coordinating Committee• Massive rail road infrastructure and water in Limpopo

National Development

Plan - NDP

• 40 High Impact Priority Projects includes Infrastructure to achieve high scale

economic impact to be implemented in 2017-18

• National Treasury – budget priorities on Infrastructure maintenance spend,

skills development.

• Sustainable social development and economic growth

• Strengthen public sector capacity to deliver on infrastructure• Procurement Bill – SMME, townships, rural, labour intensive Entities support• Procurement Plan – Office of Chief Procurement Officer, uniform single supply

chain office, modernized supply chain management

• CSD database and centralized procurement process, tax clearance

verification, verification processes.

• Reduction of red tape, compliance

• Commitment to SADC and rest of Africa, Presidential Champion Infrastructure

Coordination Committee (North South Corridor – 110 Projects, transport,

energy, water, mining projects. 87 Infrastructure Projects,

• DBSA’s role

• Reporting commitments to PICC

21

IMPLICATIONS FOR SKILLS PLANNING

National

Strategy/Plan

CETA’s current and envisaged role

Comprehensive Rural

Development

Programme

CETA to play role in registering rural contractors.

Facilitate training in supply chain management to assist in tendering

CETA Skills Development Centres are key.

Broad Based Black

Economic

Empowerment

• Prioritise skills development in small companies

• Assist large and medium enterprises in developing skills which

will assist with their BBBEE efforts

• Construction Charter Codes

• WSP-ATR Submissions approved by the CETA, BBBEE

Compliance Certificate is issued by the CETA

• Learning Programme Matrix emphases PIVITOAL Training

• Accredited training

• Grants Regulations – monitor/tracking of MG training by entities

National

Infrastructure

Maintenance Strat.

Municipal Infrastructure Maintenance. Engage with government,

especially local government on maintenance plans for infrastructure

to ensure that sufficient skills are available – Municipal services

activities to ensure infrastructure is delivered effectively, skills project

management, all government spheres to work together in planning

and coordination.

22

CHAPTER 3:

EXTENT OF SKILLS MISMATCHES

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

23

Source : Career junction index, 2016

• Vacancies are down by 55% compared to June 2015

• This further illustrates the downturn in the construction economy

• Vacancies tend to exist in the higher skills echelons

VACANCIES IN THE CONSTRUCTION SECTOR

0

100

200

300

400

500

600

700

Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 May-16 Jun-16

Building and Construction

24

Source : Quantec real data, 2016

Real wages tapered down after the construction boom in 2010 which

coincided with the world cup construction activities

WAGE TRENDS IN THE CONSTRUCTION SECTOR

-

5 000

10 000

15 000

20 000

25 000

30 000

35 000

40 000

45 000

50 000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Real remuneration per employee

25

Salaries by OccupationHighest paid are engineers (structural and civil), followed by quantity surveying and then

artisans/technologists (e.g. Architectural, draftsman, electrician, plumbers, etc.)

Occupational ScarcityShortages listed in trades e.g.. Electrical, plumbing

Shortages relate specifically to QUALIFIED tradesmen – there is a reported difference in

quality between qualified and uncertified tradesmen

Conditions of EmploymentThe sector relies heavily on project work – negatively affect long term stability of

employment and security of employment and skills development (Diagram on next slide

illustrates this relationship)

Impact of MigrationMigration across borders – very high outflow of professionals from South Africa to

elsewhere in Africa and further abroad

Internal migration – rural people migrating to cities and especially so with professionals,

draining rural areas of its skills

OTHER LABOUR DEMAND SIDE FACTORS

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

26

PIVOTAL SCARCE AND CRITICAL

SKILLS LIST

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

27

What are the top 10 scarce skills and how should the CETA intervene?

SCARCE SKILLS AND PIVOTAL INTERVENTIONS

OCCUPATION SPECIALISATION/ ALTERNATIVE TITLE INTERVENTION

Architects Building Architect Bursary (Degree); Internships;

Candidacy

Quantity Surveyor Construction Economist / Building Economist Degree; Candidacy

Civil Engineer Structural Engineer; Construction Engineer; Transportation and Urban

Planning Engineer; Site Design Engineer

Bursary (Degree); Candidacy

Construction Project Manager Construction Site Manager; Construction Manager; Property Development

Manager; Building and Construction Manager; Construction Project Director

Bursary (Certificate; Diploma;

Degree); Candidacy

Safety, Health, Environment

and Quality (SHE&Q)

Practitioner

Occupational Safety Advisor; Occupational Safety and Health (OSH) Advisor

/ Coordinator / Officer / Professional; Safety Coordinator; Health and Safety

Officer / Coordinator / Professional

Bursary (Certificate &

Diploma); Learnership

Building Associate Building Construction Supervisor; Clerk of Works Apprenticeship; Learnership;

Skills Programmes

Carpenter Construction Carpenter; Shutter hand; Carpenter Contractor Learnership; Apprenticeship

Plumber Hot Water System Installer; Plumbing Contractor; Maintenance Plumber Learnership; Apprenticeship

Electrician Electrical Fitter; Electrician (Engineering); Electrical Contractor Apprenticeship

Builder`s Worker Joinery Worker; Tiler hand; Road Construction / Maintenance Labourer;

Demolition Contractor / Labourer; Artisan Aide Building Trade; Bricklayer's

Assistant; Carpenter's Assistant; Pipe Layer

Learnership; Apprenticeship;

Skills Programmes

28

2016 SCARCE SKILLS AND WSP PIVOTAL INTEGRATION

WITH DG

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

SETA NAME

PERIOD OCCUPATION CODE

OCCUPATION QUANTITY NEEDED

Quantity projected to be supported by SETA – E.g Only Planning at Qual. Level

0-100 101-1000

1001 & ABOVE

CETA 2016/17 2015-216101 Architects 80 50 80

CETA 2016/17 2015-214904 Quantity Surveyor 50 50 50

CETA 2016/17 2015-214201 Civil Engineer 600 500 600

CETA 2016/17 2015-132301 Construction Project Manager 100 50 100

CETA 2016/17 2015-226302 Safety, Health, Environment and Quality (SHE&Q) Practitioner

50 50 50

CETA 2016/17 2015-312301 Building Associate 500 250 500

CETA 2016/17 2015-641502 Carpenter 150 150 150

CETA 2016/17 2015-642601 Plumber 100 100 100

CETA 2016/17 2015-671101 Electrician 100 100 100

CETA 2016/17 2015-831301 Builder`s Worker 150 150 150

29

CONDITIONS OF EMPLOYMENT AND ITS IMPACT

Nature of work contract - project based

• Limited time frame in line with tender/ contract

Employment type (limited duration)

• Temporary

• Fixed term

Impact on skills development (limited implementation to none)

• Shortened programmes in line with works contract

• As a result of project based nature of contracting, no stability in

employment

• Negative impact on morale, loyalty and labour productivity

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

30

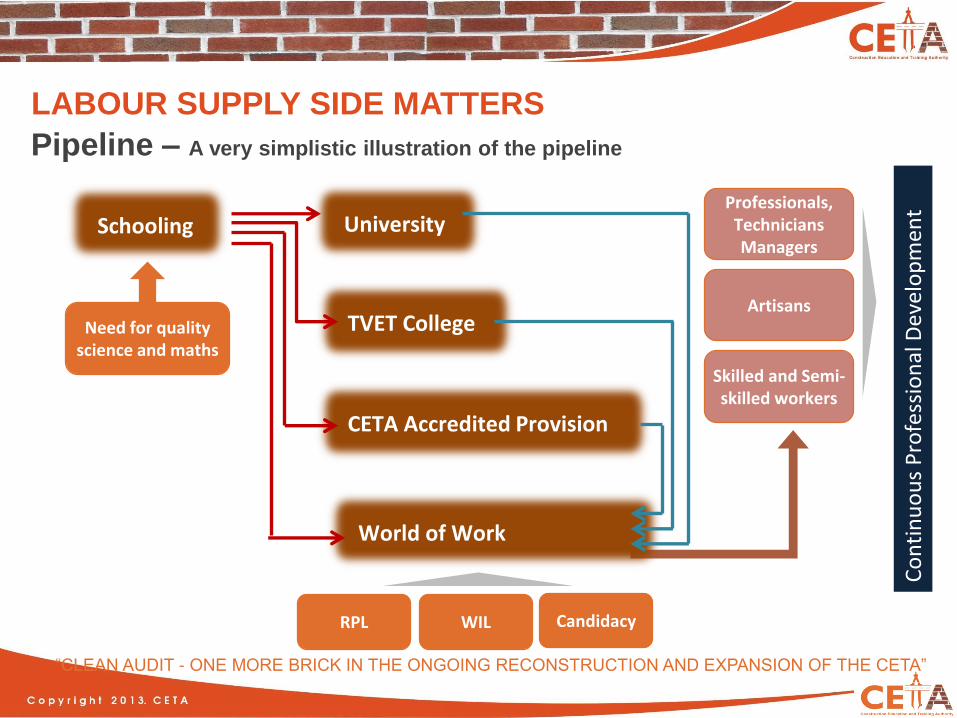

Pipeline – A very simplistic illustration of the pipeline

LABOUR SUPPLY SIDE MATTERS

Schooling University

TVET College

CETA Accredited Provision

World of Work

Co

nti

nu

ou

s P

rofe

ssio

nal

Dev

elo

pm

ent

Need for quality science and maths

RPL WIL Candidacy

Professionals,TechniciansManagers

Artisans

Skilled and Semi-skilled workers

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

31

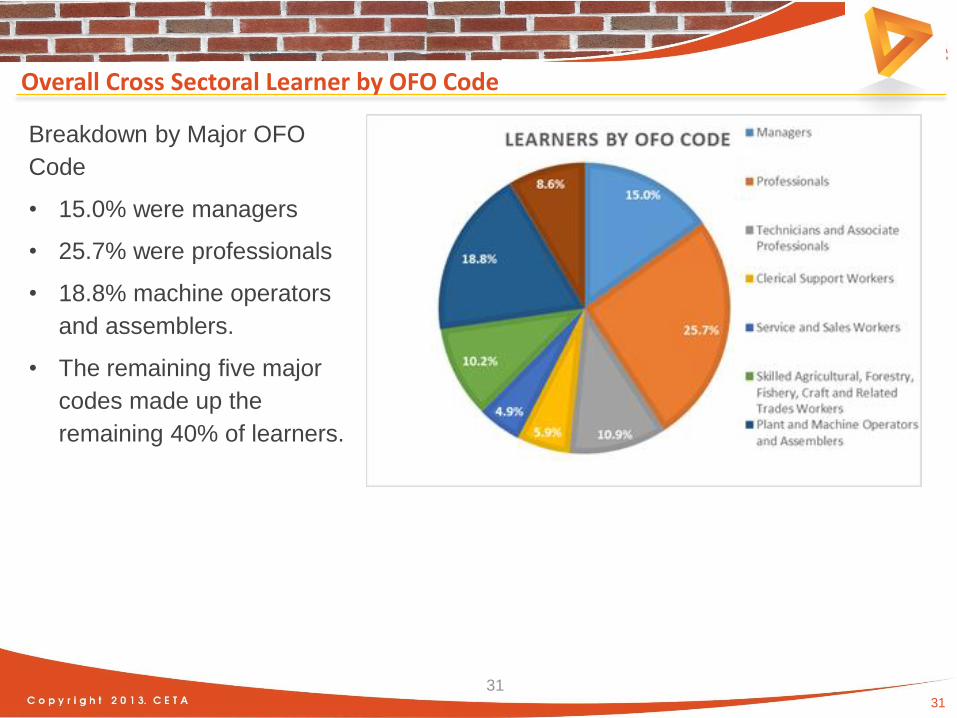

Overall Cross Sectoral Learner by OFO Code

Breakdown by Major OFO

Code

• 15.0% were managers

• 25.7% were professionals

• 18.8% machine operators

and assemblers.

• The remaining five major

codes made up the

remaining 40% of learners.

31

32

Alignment with Employment Vs Programmes implemented -SDPs

• Skills Development Providers Learners do not appear to be aligned to the

national employment breakdown

• Professional and Managers appear over represented

32

33

SAQA - Institutional Activity – Accredited Active SDPs – Upload?

Institutional activity (Institutions with at least one enrolled student) peaked in 2013 at

720, but has since started to drop to 606 in 2014 and 307 in 2015 => may point to

under- or late reporting of enrollments – In the construction sector to promote

upload of the learner assessments on the CETA MIS and in turn NLRD.

(blank)1900 1975 1978 1980 1990 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Number of Active Institutions 135 64 2 1 3 2 2 12 23 66 133 203 242 361 387 393 561 572 639 678 720 606 307 3

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Number of Active Institutions 361 387 393 561 572 639 678 720 606 307 3

34

CETA SUPPLY

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

35

CETA LEARNING PATHWAYS AND GRANT ALLOCATIONS

CETA SUPPLY:

Learning Intervention Cost per Learner Duration Total Grant

Learnerships 36 000 12 Months 36 000

Bursaries 60 000 3-4 Years 180 000

Internships 36 000 12 Months 36 000

Skills Programmes 13 500 3 Months 13 500

Artisan Development 50 000 3 Years 𝟏𝟓𝟎 𝟎𝟎𝟎

Candidacy Programmes 60 000 3 Years 180 000

RPL 3 500 1 Week - Month 𝟑𝟓𝟎𝟎

TVET Placements 36 000 12 – 24 Months 36 000

University Placements 36 000 12 Months 36 000

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

36

CETA SUPPLY - CETA LEARNING PATHWAYS..

Learning Intervention CHALLENGESSSP

Intervention

Learnerships • Opening of Workplaces, Qualified Mentors and dedication to learner

• Learner Tracer Study• Mentorship Programme• Skills Standard – access to workplace

learning – implementation process

Bursaries • “Fees Must Fall”; • Low throughput/completion rate;• Student Support, • study choices, oversupply of some

programmes,• Lecturer/Professionals non-

availability, lecturer development.

• NSFAS Intervention• CETA Managed Bursary Funding• Academic Development Programme

Internships • Opening of Workplaces• availability of Mentorships,• Liability insurance on site – H & S

• Mentorship Programme

Skills Programmes Non Credit bearing Programmes instead of SoR used in industry, learners not uploaded on CETA MIS, NLRD

• SDP Accreditation • Revised CETA MIS

37

CETA SUPPLY: CHALLENGES PER LEARNING PATHWAY

Learning Intervention ChallengesSSP

Intervention

Artisan Development • Opening of workplaces for placement of apprentices by employers or low industry uptake within the building, civil and electrical contractors subsectors.

• Short term Projects vs. 3 year Apprenticeships • Mentorship for Apprentices – (Mentor Training- Logbooks)• RPL – Mentors with experience but not qualified artisans• Observations as part of on the job training• Outdated trade tasks• Impact assessment - no exit opportunities for qualified

learners.• Lack of Guaranteed Funding• Currently no DSAP pilot for construction sector

• Workplace CapacityEvaluation

• Trade Testing Preparation Support

• NAMB RPL Toolkits• Updated Checklists• Learner Tracer

Study• Multi-Year

Extension Funding, DSAP

Candidacy Programmes • Transformation of built environment industry -registration with built environ. council

• Coaching and Mentorship of Candidates• Quarterly reports submissions not monitored• No structured top up training and learning materials• Candidate drop out due to better salary or relocation to

province affects mentorship

• Mentorship• Candidacy

Guideline

38

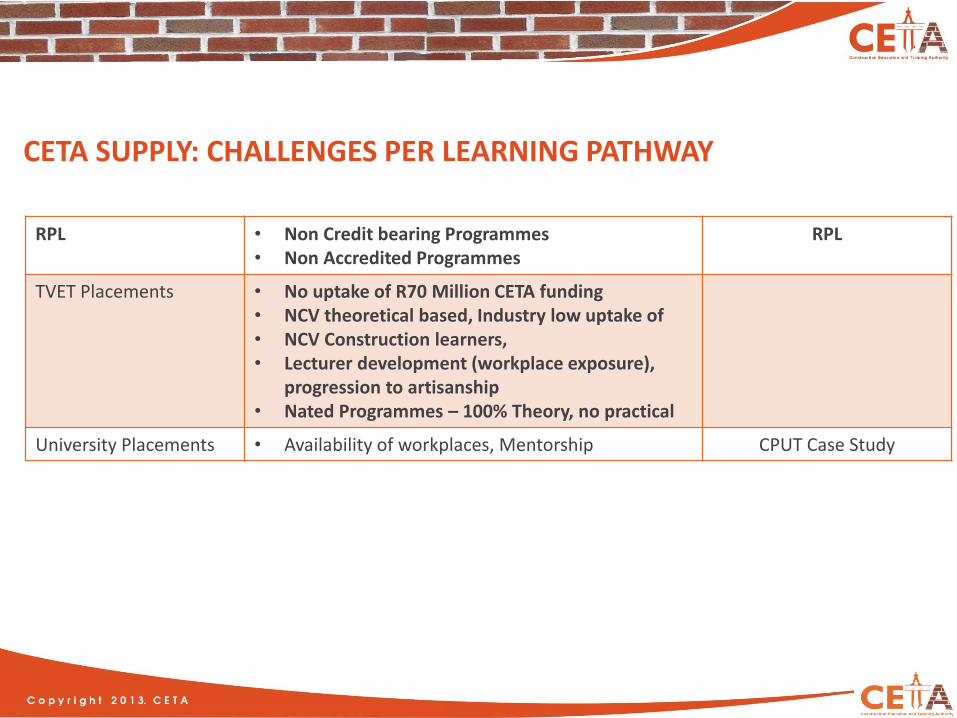

CETA SUPPLY: CHALLENGES PER LEARNING PATHWAY

RPL • Non Credit bearing Programmes• Non Accredited Programmes

RPL

TVET Placements • No uptake of R70 Million CETA funding • NCV theoretical based, Industry low uptake of• NCV Construction learners, • Lecturer development (workplace exposure),

progression to artisanship• Nated Programmes – 100% Theory, no practical

University Placements • Availability of workplaces, Mentorship CPUT Case Study

39

WHAT HAS THE CETA DONE TO

SUPPORT TRAINING IN THE

SECTOR?

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

40

CETA ON SKILLS DEVELOPMENT

CETA has made an allocation of more than R1.2 billion towards different skills development

interventions, through different types of entities, majority being public sector, covering all provinces.

Graph below depicts:

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

27%

4%

4%

3%24%

3%

14%

21%

Graph: Allocation Of Learner Per Learning Pathway

Apprenticeships Bursaries Candidacy

Internships Learnerships Work Integrated Learning

41

Where does CETA invest employers money?

CETA SUPPLY

Learning Intervention 2013/14 2014/15Δ % from 2013/14

2015/16Δ % from 2014/15

Learnerships 1039 3433 +230% 5045 +47%

Bursaries 2495 581 -77% 653 +12%

Internships 152 686 +351% 128 -81%

Skills Programmes 130 1289 +891% 2205 +71%

Artisan Development - 2982 ∞ 4541 +52%

Candidacy Programmes 557 342 -39% 507 +48%

RPL - 1218 ∞ 1234 +1%

TVET Placements 1655 58 -96% 29 -50%

University Placements 557 342 -39% 111 -68%

• Most of CETA’s funding flows towards learnerships, skills programmes, artisan development and RPL – in line with NSDS III objectives

• Largest growth in Learnerships, skills programmes, artisan development and candidacy – in line with call of Minister

42

CETA GRANT ALLOCATIONS

CETA SUPPLY:

Learning Intervention Total Allocation

Learnerships 36 000

Bursaries 60 000

Internships 36 000

Skills Programmes 13 500

Artisan Development 50 000

Candidacy Programmes 60 000

RPL 3 500

TVET Placements 36 000

University Placements 36 000

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

43

CETA SERVICE DELIVERY:

WHAT HAS THE CETA ACHIEVED?

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

44

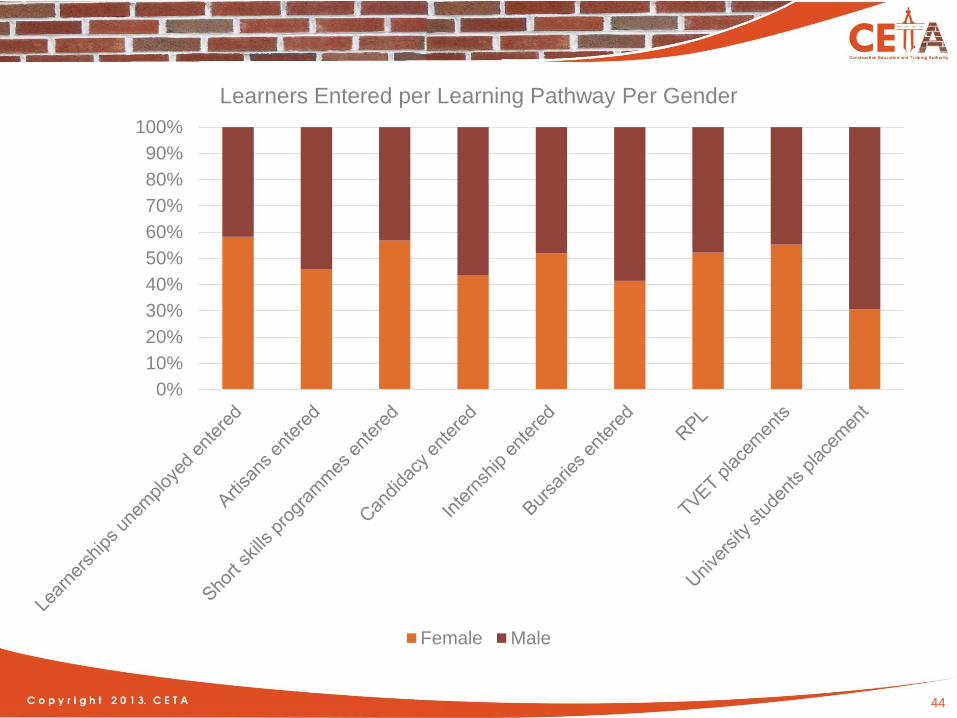

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Learners Entered per Learning Pathway Per Gender

Female Male

45

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

3433

1289

2982

581 686 342 58 342

9713

5045

2205

4498

653128 507

29 111

16323

Total Learners Entered - 2014/15 vs 2015/16

Total Entered 2014/15 Total Entered 2015/16

46

0

1000

2000

3000

4000

5000

6000

2240

1037

108 0 20 0 0 0

1218

4623

16362131

775

94 0 0 0 0

1234

5870

Total Learners Completed - 2014/15 vs 2015/16

Total Completed 2014/15 Total Completed 2015/16

47

6

25

8

5

46

41

8

10

0

5

10

15

20

25

30

35

40

45

50

TVET Partnerships SMMEs supported NGOs supported Cooperativessupported

TVET partnerships, SMMEs, NGOs and Cooperatives supported

Target Achievement

48

Sector Attractiveness:Construction is not always the immediate career choice for youth but an alternative second or even third option

Inadequate Career Counselling:How do learners choose their career? Bursary funded learners changing study in second year or academically achieving students dropping out of first year at university or programmes or over supply in one programme

Pegging of Career Advice in the schooling sector:Career Advice Programmes are targeting grade 11 and 12 pupils. Start at Grade 10 or Grade 8?

Admission Requirements into Built Environment ProgrammesEligibility based on admission points and subject choice/combinations Existing

Existing Career Advice Activities: Construction (Not Coordinated) • Youth in Construction – Maths and Science – CIDB• Public Works Schools Programme• SAFCEC Career Expo• World Skills Competition – construction• DHET-Khetha Career Services – Radio in all SA languages• “Try A Skill” CETA SSP CAREER GUIDE – UPDATED – 34 CAREER EXHIBITIONS

CAREER ADVICE SERVICES – HOW ATTRACTIVE IS THE CONSTRUCTION SECTOR TO NEW ENTRANTS?

49

CETA-SECTOR PARTNERSHIPS

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

50

KEY PARTNERSHIP ARRANGEMENTS

Partnerships

Public Sector support for Service

Delivery

Academia Development Programme

Innovative Qualification Development

Expanding Public TVET

Inter-SETA Collaboration

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

51

NO. 13 CETA SKILLS DEVELOPMENT CENTRESTVET COLLEGE CENTRE IS ALOCATED TO

PHYSICAL

LOCATION OF THE CENTRE

MUNICIPALITY

1. Gert Sibande TVET College Bethal Govan Mbeki

2. West Coast TVET College Vredendal Matsikama

3. UMgungundlovu TVET College Muden Umvoti

4. Esayidi TVET College Ixopo Ubuhlebezwe

5. Northern Cape Rural TVET College Springbok Namaqua

6. Mthashana TVET College Babanango UMzinyathi

7. Mnambithi TVET College Bergville UKhahlamba

8. Mthashana TVET College Phongola Phongola

9. University of Venda Venda Vhembe

10. Umfolozi TVET College Eskhawini Umhlathuze

11. Boland TVET College Bredasdorp Cape Agulhas

12. Mthashana TVET College Ingwavuma UMkhanyakude

13. Northern Cape Rural TVET College De Aar Pixley ka Seme

52

CETA/UNIVERSITY OF VENDA SKILLS DEVELOPMENT CENTRE

ARTISAN TRADES: Electrical Construction and Plumbing

53

CETA/VREDENDAL SKILLS DEVELOPMENT CENTRE

Linked to West Coast TVET College – Learnerships/Apprenticeships

54

CETA/ANENE BOOYSEN SKILLS DEVELOPMENT CENTRE

PSET: Pilot Community College, expansion to Boland TVET College Branch, SETA One Stop Shop Training; Potential forEvening/Part time Study Options, gender empowerment programmes.

55

Public Sector Support for Service Delivery

WITH WHOM? IN ORDER TO DO / ACHIEVE WHAT?

Dept. of Public Works Support Department with bursaries, candidacy programmes, learnerships and apprenticeships

Premiers’ OfficesSkills development relevant to Infrastructure delivery

DBE / DBSA – Pipeline as per SSP

Train local people to benefit Accelerated School Infrastructure Delivery Initiative

National Treasury –Pipeline as per SSP

Candidacy programmes to develop professionals to deliver on MIG

Dept. of Transport –Pipeline as per SSP

Forum for Integrated skills planning

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

56

PUBLIC UNIVERSITY PARTNERSHIP: BUILT ENVIRONMENT (Academia Development Programme : Masters & PHD Programmes)

WITH WHOM? IN ORDER TO DO / ACHIEVE WHAT?

UKZN: Develop academics for the country initially focusing

on BSc Property Development : 1 Prof, 2 Lecturers, 1 Senior

Lecturer/Associate Professor), bursaries for 116

undergraduate learners in BSc ProPDev.

WITS: BSc Construction Economics, BSc Construction

Planning. Academic Development Incubation Programme:

10 Professionals. PhD bursaries, paying salaries as junior

lecturers and funding their CPD and bursary for UKZN

UNIIVEN: 3 Masters Lecturers, 2 PHDs, Programme Dev. In

BSc in Construction Technology, bursaries for 27 learners,

Laboratory construction

Support their Civil Engineering, Geotechnical and

Transportation Departments. Laboratory

construction

• UKZN

• WITS

• UNIVEN

SUN and UP-

Pipeline

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

57

Expanding Public TVET Colleges

WITH WHOM? IN ORDER TO DO / ACHIEVE WHAT?

Capacitation through lecturer development

programmes and accreditation to deliver on CETA

occupational programmes – 46 out of 50 TVETs

accredited with the CETA.

Support 22 Public TVET Colleges with discretionary

grant funding to support a total of 6 866 learners in

construction learnerships, apprenticeships

programmes

Establish Skills Development Centres managed by

TVET colleges to the benefit of local communities –

13 such centres have already been established.

All TVET

Colleges

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

58

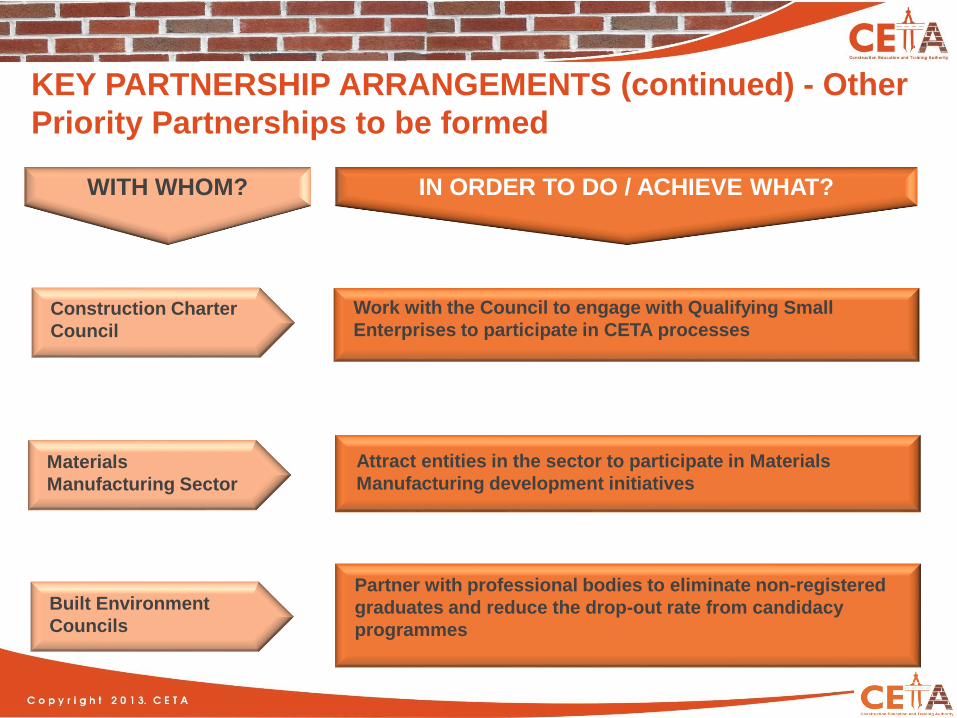

KEY PARTNERSHIP ARRANGEMENTS (continued) - Other

Priority Partnerships to be formed

WITH WHOM? IN ORDER TO DO / ACHIEVE WHAT?

Construction Charter

Council

Work with the Council to engage with Qualifying Small

Enterprises to participate in CETA processes

Materials

Manufacturing Sector

Attract entities in the sector to participate in Materials

Manufacturing development initiatives

Built Environment

Councils

Partner with professional bodies to eliminate non-registered

graduates and reduce the drop-out rate from candidacy

programmes

59

INTERSETA COLLABORATION – CETA-SERVICES SETA

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

Entity Projects Number of learners

1.Beaufort West Local Municipality Learnerships 508

Apprenticeship 103

Skills Centre

2. Inxuba Yathembe Local Municipality Apprenticeships 87

Learnerships 497

3. South African Military Veterans

Association (SANMVA)

Learnerships 833

4. Mining Development Agency (MDA) RPL 1000

Short Skills 111

Learnerships 82

Apprenticeship 58

Bursaries 170

5. Disabled People South Africa (DPSA) Short Skills 1500

Learnerships 700

6.Don Bosco Educational Project Learnership 175

Apprenticeship 200

Internship 10

Bursaries 50

Establishment of cooperatives 10

RPL 50

7. Motheo TVET College. Learnership 30

8. Mangaung Local Municipality Learnership 332

Apprenticeship 260

9.Sakhisiswe Local Municipality( Cala) Learnership 200

10. South African Homeless Peoples

Federation

Short Skills 111

Learnerships 165

Bursaries 10

11. Namaqua District Municipality Learnership 120

12. Prieska Learnership 200

13.Alexandra Bay Apprenticeship 100

OTHER SETA

PARTNERSHIPS

(joint MIS):

ETDP SETA, FP&M

SETA and

CATHSETA

60

INNOVATIVE QUALIFICATION DEVELOPMENT: FROM CURRENT TO NEW OCCUPATIONAL LANDSCAPE

WITH WHOM? IN ORDER TO DO / ACHIEVE WHAT?

PURPOSE: REPLACING OLD NQF CONSTRUCTION QUALIFICATIONS WITH INDUSTRY LED CURRICULUM DEVELOPMENT – Active June 2018

SAFCEC and FITA(Flooring

Industry Training Association)

MBSA, CESA Funded by CETA but current

no uptake.

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

CETA-SAFCEC PARTNERSHIP: Replacing: • NC: Construction Roadworks (24133), NQF Level 2• NC: Construction Roadworks (24173), NQF Level 3• NC: Construction Building and Civil Construction (65409), NQF Level 3With OFO-based: • Civil Road Construction Constructor• Civil Services Constructor• Civil Structures Construction Constructor (Incl. Construction Scafolding)

FITA: Replacing: NC in Flooring and Tiling, NQF Level 1

61

THE FUTURE: NEW CETA PILOT QUALITY ASSURANCE MODEL

• CETA pioneering Pilot AQP Model: Joint CETA-Industry Partner for quality of training,

quality of assessment, monitoring of training providers

• CETA is approved as an Assessment Quality Partner (AQP)

• CETA delegates the functions to an industry expert body

• CETA funds the quality assurance implementation

• Review of the First Phase of the AQP pilot model and make improvements where

required.

• Roll out of the AQP Model to other CETA new qualifications

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

62

CETA ON THE DRIVE TO MAINTAIN CLEAN ADMINISTRATION WHILE ENSURING SERVICE DELIVERY.

• Levies has increased from R551 million to R835 million in 2015/16,this reflects the level

of trust by the construction sector on skills development

• Mandatory grants of R248 million was paid to complying levy paying companies.

• 2190 number of companies submitted WSP’s and 1892 were approved and paid.

“CLEAN AUDIT - ONE MORE BRICK IN THE ONGOING RECONSTRUCTION AND EXPANSION OF THE CETA”

63

CONTINUOUS IMPROVEMENT PLAN

(CIP)

“CLEAN AUDIT-ONE MORE BRICK IN THE RECONSTRUCTION AND EXPANSION OF THE CETA”

64

SSP CONTINOUS IMPROVEMENT PLAN - CIP

• Subsector Skills Plan for each 4 construction subsector

(Subsector plans feed into the 1 Main SSP)

• Develop skills forecasting tool for Sector in partnership with a Public University

• Better use of previously research conducted by stakeholders

Improve data sources• Make extensive use of QLFS and HEMIS – ensure proper access

• Work with Councils to develop time series data for trend analysis, improve depth

• Expand research partners to improve labour information

Organising Framework for Occupations(OFO) and Sector PIVOTAL LIST• improve PIVOTAL skills submissions

Alignment to Government Policies/national imperatives• Work with stakeholders to identify policies that have an impact on skills development and

update CETA SSP

• Measure impact of partnerships on achieving aims of government programmes

Career Advice System – CETA SSP Career Guide• Partnerships with Councils to promote careers in the sector

• Supply side tracking tool for University and TVET graduates

Stakeholder participation, engagement and central coordination of activities-

SSP

Research agenda

65

THANK YOU!

66