construction of optimal portfolio using sharpe index model...

TRANSCRIPT

[ VOLUME 2 I ISSUE 2 I APRIL - JUNE 2015 ] E ISSN 2348 –1269, PRINT ISSN 2349-5138

168 IJRAR- International Journal of Research and Analytical Reviews Research Paper

Construction of Optimal Portfolio Using Sharpe Index Model

& Camp for BSE Top 15 Securities

Chintan A. Shah Assistant Professor

Bhagwan Mahavir College of Business Administration, Vesu – Surat.

Received June 2, 2015 Accepted June 7, 2015

ABSTRACT Portfolio is the combination of securities such as stocks, bonds and money market instruments. The process of blending together the broad asset classes so as to obtain optimum return with minimum risk if called portfolio construction. Diversification of investments helps to spread risk over many assets. Investment management, also referred to as portfolio management, is a complex process or activity that may be divided into seven broad phases. Markowitz Model had serious practical limitations due the rigors involved in compiling the expected returns, standard deviation, variance, covariance of each security to every other security in the portfolio. Sharpe Model has simplified this process by relating the return in a security to a single Market index. In the CAPM theory, the required rate return of an asset is having a linear relationship with asset’s beta value i.e. undiversifiable or systematic risk. For the fulfillment of our research objectives which are, to construct an optimal portfolio, evaluate the performance of BSE15, Rank the optimal portfolio constructed, and compares the performance of BSE15 securities through Sharpe Model. We have used the Descriptive Research Design and used the Secondary data collection methods. Finally, the results will be drawn out on the basis of expected risk & return with help of Sharpe index model and comparison between Sharpe index model & CAPM model.

Key Words: Portfolio, Securities, Diversification, Portfolio Management, Investment, Expected Risk & Return.

INTRODUCTION:

CONCEPT OF PORTFOLIO:

Portfolio is the combination of securities such as stocks, bonds and money market instruments.

The process of blending together the broad asset classes so as to obtain optimum return with

minimum risk if called portfolio construction.

CONSTRUCTION OF THE OPTIMAL PORTFOLIO

SHARPE MODEL

Markowitz Model had serious practical limitations due the rigors involved in compiling the

expected returns, standard deviation, variance, covariance of each security to every other security

in the portfolio. Sharpe Model has simplified this process by relating the return in a security to a

single Market index

Single Index Model

[ VOLUME 2 I ISSUE 2 I APRIL - JUNE 2015 ] E ISSN 2348 –1269, PRINT ISSN 2349-5138

Research Paper IJRAR- International Journal of Research and Analytical Reviews 169

The single index model is based on the assumption that stocks vary together because of

the common movement in the stock market and there are no effects beyond the market that

account the stocks co- movement. The expected return, standard deviation and co-variance of the

single index model represent the joint movement of securities.

𝐑𝐢 = 𝛂𝐢 + 𝛃𝐢𝐑𝐦 + 𝐞𝐢

Where,

Ri – expected return on security i

αi - intercept of the straight line or alpha co-efficient

βi- slope of straight line or beta co-efficient

Rm- the rate of return on market index

ei- error term

The variance of the security has two components namely, systematic risk or market risk and

unsystematic risk or unique risk. The variance explained by the index is referred to systematic

risk. The unexplained variance is called residual variance or unsystematic risk.

Systematic Risk = βi2 * Variance of market index

= βi2 * σ2m

Unsystematic Risk = Total variance – Systematic Risk

ei2 =σi_ Systematic Risk

Thus, Total Risk = Systematic Risk + Unsystematic Risk

= βi2 * σ2m + ei2

From this, the portfolio variance can be derived

𝛔 𝒑𝟐 = ∑𝐗𝐢𝛃𝐢

𝟐 𝛔𝟐𝐦 + ∑𝐗𝐢 𝟐𝛔𝟐𝐞𝐢

σ2p= Variance of Portfolio

σ2 =Expected Variance of Index

ei2= Variation in Security’s return not related to the market index

Xi = the portion of stock i in the portfolio

SHARPE’S OPTIMAL PORTFOLIO

Sharpe had provided model for the selection of appropriate securities in a portfolio. The

selection of any stock is directly related to its excess return-beta ratio.

Ri − Rf

βi

Where,

Ri = the expected return on stock i

Rf = the return on a riskless asset

[ VOLUME 2 I ISSUE 2 I APRIL - JUNE 2015 ] E ISSN 2348 –1269, PRINT ISSN 2349-5138

170 IJRAR- International Journal of Research and Analytical Reviews Research Paper

βi = the expected change in the rate of return on stock i associated with one unit change in

the market return.

CONSTRUCTION OF THE OPTIMAL PORTFOLIO

After determining the securities to be selected, the portfolio manager should find out how

much should be invested in each security. The percentage of funds to be invested in each security

can be estimated as follows.

X1 = Zi

N ∑i = 1 Zi

Zi = βi Ri − Rf

βi− C∗

The first expression indicates the weights on each security and they sum up to one. The second

shows the relative investment in each security. The residual variance or the unsystematic risk has

a role in determining the amount to be invested in each security.

RESEARCH METHODOLOGY:

A. Problem Statement :“To construct an optimal portfolio using Sharpe Index Model for BSE

Top 15 securities”

B. Research Objectives:

To construct an optimal portfolio using Sharpe Index Model and CAPM model.

To analyze the Portfolio risk and Portfolio return of stocks listed at BSE.

To analyze and compare the portfolios prepared through Sharpe Index Model & CAPM and

identify the difference in results.

C. Research Design: Here, researcher is used Descriptive Research Design because; in this

research design the researcher has got very specific objectives, clear-cut data requirements.

D. Literature Review:

1. Optimal Portfolio Construction in Stock Market- An Empirical Study on Selected Stocks in

Manufacturing Sectors of India

Dr. Sathya SwaroopDebasish, Jakki Samir Khan(December 2012)

2. Optimal Portfolio Construction by Using Sharpe’s Single Index Model (An Empirical Study on

Stocks of Some Selected Public Sector Enterprises in India)

Dr.Niranjan Mandal (2013)

3. Sharpe’s single index model and its application to construct optimal portfolio: an empirical

study

Niranjan Mandal

[ VOLUME 2 I ISSUE 2 I APRIL - JUNE 2015 ] E ISSN 2348 –1269, PRINT ISSN 2349-5138

Research Paper IJRAR- International Journal of Research and Analytical Reviews 171

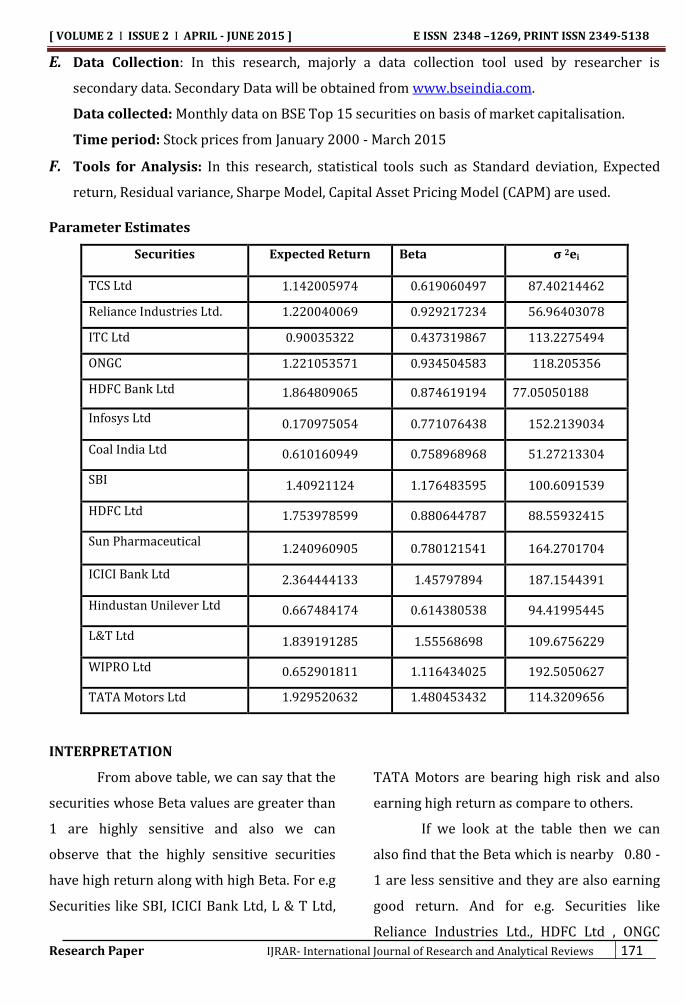

E. Data Collection: In this research, majorly a data collection tool used by researcher is

secondary data. Secondary Data will be obtained from www.bseindia.com.

Data collected: Monthly data on BSE Top 15 securities on basis of market capitalisation.

Time period: Stock prices from January 2000 - March 2015

F. Tools for Analysis: In this research, statistical tools such as Standard deviation, Expected

return, Residual variance, Sharpe Model, Capital Asset Pricing Model (CAPM) are used.

Parameter Estimates

Securities Expected Return Beta σ 2ei

TCS Ltd 1.142005974 0.619060497 87.40214462

Reliance Industries Ltd. 1.220040069 0.929217234 56.96403078

ITC Ltd 0.90035322 0.437319867 113.2275494

ONGC 1.221053571 0.934504583 118.205356

HDFC Bank Ltd 1.864809065 0.874619194 77.05050188

Infosys Ltd 0.170975054 0.771076438 152.2139034

Coal India Ltd 0.610160949 0.758968968 51.27213304

SBI 1.40921124 1.176483595 100.6091539

HDFC Ltd 1.753978599 0.880644787 88.55932415

Sun Pharmaceutical 1.240960905 0.780121541 164.2701704

ICICI Bank Ltd 2.364444133 1.45797894 187.1544391

Hindustan Unilever Ltd 0.667484174 0.614380538 94.41995445

L&T Ltd 1.839191285 1.55568698 109.6756229

WIPRO Ltd 0.652901811 1.116434025 192.5050627

TATA Motors Ltd 1.929520632 1.480453432 114.3209656

INTERPRETATION

From above table, we can say that the

securities whose Beta values are greater than

1 are highly sensitive and also we can

observe that the highly sensitive securities

have high return along with high Beta. For e.g

Securities like SBI, ICICI Bank Ltd, L & T Ltd,

TATA Motors are bearing high risk and also

earning high return as compare to others.

If we look at the table then we can

also find that the Beta which is nearby 0.80 -

1 are less sensitive and they are also earning

good return. And for e.g. Securities like

Reliance Industries Ltd., HDFC Ltd , ONGC

[ VOLUME 2 I ISSUE 2 I APRIL - JUNE 2015 ] E ISSN 2348 –1269, PRINT ISSN 2349-5138

172 IJRAR- International Journal of Research and Analytical Reviews Research Paper

Ltd, HDFC Bank Ltd and are having beta less

than 1, so we can say that they are stable

earning securities with low level of risk.

1. Construction of an optimal portfolio

Step 1 : Find out the “ excess return to beta ” ratio for each stock under consideration.

Securities have to be ranked from the highest return to beta to the lowest

Securities Ri βi Ri-Rf Ri-Rf

βi

TCS Ltd 1.142005974 0.619060497 0.575616985

0.929823478

Reliance Industries

Ltd. 1.220040069 0.929217234

0.653651079

0.703442699

ITC Ltd 0.90035322 0.437319867

0.333964231

0.763661238

ONGC

1.221053571 0.934504583 0.654664582

0.700547214

HDFC Bank Ltd

1.864809065 0.874619194 1.298420075 1.484554746

Infosys Ltd

0.170975054 0.771076438 -0.395413935 -0.512807701

Coal India Ltd

0.610160949 0.758968968 0.04377196 0.057672924

SBI

1.40921124 1.176483595 0.842822251 0.716390993

HDFC Ltd

1.753978599 0.880644787 1.18758961 1.348545551

Sun Pharmaceutical

1.240960905 0.780121541 0.674571916 0.674571916

ICICI Bank Ltd 2.364444133 1.45797894 1.798055144 1.233251795

Hindustan Unilever

Ltd 0.667484174 0.614380538 0.101095184 0.164548155

L&T Ltd 1.839191285 1.55568698 1.272802295 0.818160923

WIPRO Ltd 0.652901811 1.116434025 0.048753555 0.043668998

TATA Motors Ltd 1.929520632 1.480453432 1.325372376 0.895247596

Step 2: Rank them from the highest to the lowest

[ VOLUME 2 I ISSUE 2 I APRIL - JUNE 2015 ] E ISSN 2348 –1269, PRINT ISSN 2349-5138

Research Paper IJRAR- International Journal of Research and Analytical Reviews 173

Ranked table

Securities Ri-Rf

βi

(Ri-Rf) βi

σ 2ei

∑(Ri-Rf)βi

σ 2ei

Βi2

σ 2ei

∑ Βi2

σ 2ei

C*

HDFC Bank Ltd

1.48455

0.01473 0.01473 0.00992 0.00992 0.48836

HDFC Ltd 1.34854 0.01180 0.02654 0.00875 0.01868 0.68182

ICICI Bank Ltd 1.23325 0.01400 0.04055 0.01135 0.03004 0.80635

TCS 0.92982 0.00407 0.04463 0.00438 0.03442 0.81625

TATA Motors Ltd 0.89524 0.01716 0.06179 0.01917 0.05359 0.8367

6 L&T 0.81816 0.01805 0.07985 0.02206 0.07566 0.83248

ITC Ltd 0.76366 0.00128 0.08113 0.00168 0.07735 0.83129

SBI 0.71639 0.00985 0.09099 0.01375 0.09111 0.81709

Reliance Industries

Ltd

0.70344 0.01066 0.10165 0.01515 0.10627 0.80348

ONGC 0.70054 0.00517 0.10683 0.00738 0.11365 0.79780

Sun Pharma 0.67457 0.00320 0.11003 0.00370 0.11736 0.79960

HUL 0.16454 0.00065 0.11069 0.00399 0.12136 0.78167

Coal India 0.05767 0.00064 0.11134 0.01123 0.13259 0.72845

Wipro 0.04366 0.00028 0.11162 0.00647 0.13907 0.70062

Infosys -0.51281 -0.0020 0.10962 0.00390 0.14297 0.67159

Step 3: Proceed to calculate Ci for all the stocks according to the ranked order using the following

formula.

C* =

σ2m N ∑i = 1 Ri – Rf βi

σ2ei

1+ σ2m N ∑i = 1βi2 (σ2m = 35.22)

C* = 0.836761963

Step 4: The cumulated values of Ci start declining after a particular Ci and that point is taken as

cut off point and that stock ratio is the cut off point C.

According to highest C*, the optimal portfolio consists of following securities.

1. HDFC Bank Ltd.

2. HDFC Ltd.

[ VOLUME 2 I ISSUE 2 I APRIL - JUNE 2015 ] E ISSN 2348 –1269, PRINT ISSN 2349-5138

174 IJRAR- International Journal of Research and Analytical Reviews Research Paper

3. ICICI Bank Ltd.

4. TCS

5. TATA Motors Ltd.

Construction of Optimal Portfolio:

The proportions are

X1 = Zi

N ∑i=1 Zi Zi = βi

Ri−Rf

βi− C∗

Zi = 0.01694778

PORTFOLIO RETURN

Rp = N ∑Xi( αi + βiRm )

Rp = 1.897367059%

PORTFOLIO VARIANCE

σ 𝑝2 = ∑Xiβi

2 σ2m + ∑Xi

2σ2ei

∑Xiβi 2

= 0.999763319 ∑Xiβi 2

σ2m = 49.3671097

∑Xi 2σ2ei = 29.06738784 σ2p = 78.43449754

PORTFOLIO RISK σp = 8.856325284

PORTFOLIO BETA βp = βi*Xi

∑βp = 0.999881652

INTERPRETATION:-

According to Sharpe Model, Portfolio

Return 1.89% it means an investor is getting

1.89% of Portfolio Return by constructing an

Portfolio of BSE Top 15 securities, and

against it he is bearing 8.86% Portfolio Risk.

Now, after constructing an Optimal

Portfolio of BSE Top 15 security with the help

of Sharpe Model, we have also applied Capital

Asset Pricing Model (CAPM) to select set of

securities that an investor should consider

for investment. This will help to investor for

taking buying and selling decisions by

comparing the output of both models.

CAPITAL ASSET PRICING MODEL (CAPM)

Markowitz, William Sharpe, John Lintner and Jan Mossin provided the basic structure for

the CAPM model. It is a model of linear general equilibrium return. In the CAPM theory, the

required rate return of an asset is having a linear relationship with asset’s beta value i.e.

undiversifiable or systematic risk.

The assumptions of CAPM are that the market is in equilibrium and the expected rate of

return is equal to the required rate of return for a given level of risk or Beta. CAPM presents a

[ VOLUME 2 I ISSUE 2 I APRIL - JUNE 2015 ] E ISSN 2348 –1269, PRINT ISSN 2349-5138

Research Paper IJRAR- International Journal of Research and Analytical Reviews 175

linear relationship between the required rate of return of a security and relates it to market

related risk or Beta, which cannot be avoided. The equation for the CAPM Theory is

Ri = Rf + βi ( Rm − Rf)

Ri = expected rate of return on security ‘i’.

Rf = risk free return

βi = Beta coefficient – a risk measure for the non-diversifiable part of total Risk.

Rm = Return on market portfolio

Rm - Rf = The excess return for the extra risk

2. CAPITAL ASSET PRICING MODEL

Securities

Estimated Return

Ri =∑Xi/N

Expected Return

Ri = Rf+ β (Rm - Rf )

Remarks

TCS 1.142005974 1.101489976 Underpriced

Reliance Industries Ltd. 1.220040069 1.151155013 Underpriced

ITC Ltd. 0.90035322 0.841598908 Underpriced

ONGC 1.221053571 0.691760465 Underpriced

HDFC Bank Ltd. 1.864809065 1.116795902 Underpriced

Infosys Ltd. 0.170975054 1.051635373 Overpriced

Coal India Ltd. 0.610160949 0.694913175 Overpriced

SBI 1.40921124 1.306762294 Underpriced

HDFC Ltd. 1.753978599 1.12058787 Underpriced

Sun Pharma 1.240960905 1.05732755 Underpriced

ICICI Bank Ltd 2.364444133 1.483910228 Underpriced

HUL 0.667484174 0.953025021 Overpriced

Larsen Turbro Ltd. 1.839191285 1.545398909 Underpriced

WIPRO Ltd. 0.652901811 1.264576014 Overpriced

TATA Motors Ltd. 1.929520632 1.479912089 Underpriced

Interpretation:

As we can see that above table is

showing the result of CAPM which emphasis

on individual security. As we can see that

some securities are overpriced and some are

[ VOLUME 2 I ISSUE 2 I APRIL - JUNE 2015 ] E ISSN 2348 –1269, PRINT ISSN 2349-5138

176 IJRAR- International Journal of Research and Analytical Reviews Research Paper

underpriced. The securities which are bold

indicate that they are underpriced and it

suggests that investors should invest in these

underpriced securities as there are chances of

return to be increased in the future. Whereas

the securities which are overpriced indicate

that they should not be purchased by

investors as it is overvalued.

3. Comparison of output of SHARPE Model and CAPM Model

Interpretation:-

As we know that Sharpe model

indicates the portfolio of securities whereas

CAPM emphasis on individual security. In

above table, CAPM consists of securities

which are underpriced; it means it says that

investors can purchase any of the above

mentioned 11 securities.

According to Sharpe model which

emphasis on Portfolio of securities rather

than holding an individual security. As we

know that investor is not always sure that

whether market trend will always support

him. So there are chances that market does

not perform well so if investor has invested in

individual securities based on CAPM then he

may incur a loss. Whereas in case of portfolio

constructed based on Sharpe model if any

securities make loss then it can be easily

covered by other securities which is not

possible by holding individual security as

specified by CAPM model.

SHARPE MODEL CAPM

1. HDFC Bank Ltd 1. TCS

2. HDFC Ltd 2. Reliance Industries Ltd.

3. ICICI Bank Ltd 3. ITC Ltd.

4. TCS 4. ONGC

5. TATA Motors Ltd. 5. HDFC Bank Ltd.

6. SBI

7. HDFC Ltd.

8. Sun Pharma

9. ICICI Bank Ltd

10. Larsen Turbro Ltd.

11. TATA Motors Ltd.

[ VOLUME 2 I ISSUE 2 I APRIL - JUNE 2015 ] E ISSN 2348 –1269, PRINT ISSN 2349-5138

Research Paper IJRAR- International Journal of Research and Analytical Reviews 177

FINDINGS:

As per Sharpe model, the portfolio will

consist of 5 securities and its weightage of

investment is as follows.

HDFC Bank Ltd. 43.39% , HDFC Ltd.

30.03%, ICICI Bank Ltd. 18.23%, TCS Ltd.

3.89%, and TATA Motors Ltd. 4.47%.

As per CAPM model, 11 securities are

undervalued and will be profitable for

investor if he invest in them. The

securities are TCS Ltd, Reliance Industries

Ltd., ITC Ltd., ONGC, HDFC Bank Ltd., SBI,

HDFC Ltd., Sun Pharma, ICICI Bank Ltd,

Larsen Turbro Ltd., TATA Motors Ltd.

According to Sharpe model, portfolio

return 1.89% it means an investor is

getting 1.89% of portfolio return by

constructing an portfolio of BSE top 15

securities, and against it he is bearing

8.86% portfolio risk.

According to Sharpe Model, portfolio

return 1.89% it means an investor is

getting 1.89% of portfolio return by

constructing an portfolio of BSE top 15

securities, and against it he is bearing

8.86% portfolio risk.

CONCLUSION:

Sharpe model gives exact number of

securities along with weightage for

investment, while this is not possible in CAPM

model.

CAPM model only suggest different securities

where investor can invest but it does not give

a particular portfolio and weightage to

investment in different securities.

From the comparison of Sharpe Model and

CAPM, it can be said that CAPM fails to

capture the return behaviour of BSE Top 15

individual security. Sharpe Model suggests

the portfolio of equities whereas CAPM

indicates individual securities, so in portfolio

of equities if some securities returns are

negative then investor can cover his loss from

other securities included in his portfolio.

SUGGESTION:

Based on the study of returns of top 15

BSE securities for past 16 years using

Sharpe Model, an investor can invest in

following securities.

HDFC Bank Ltd, HDFC Ltd., ICICI Bank

Ltd.,TCS, TATA Motors

From the comparison of Sharpe Model

and CAPM, investor should hold the

portfolio of equities suggested by Sharpe

Model rather than CAPM model.

BIBLIOGRAPHY:

BOOKS:

1. Berry G.C, (2000), “Marketing Research”, 3rd

Ed, Tata Mc Grew-hill co. ltd, New Delhi.

2. Punithvanthy Pandean, (3rd Ed) “Security

Analysis and Portfolio management”, Vikas

Publishing House Pvt. Ltd.

ARTICLE:

[ VOLUME 2 I ISSUE 2 I APRIL - JUNE 2015 ] E ISSN 2348 –1269, PRINT ISSN 2349-5138

178 IJRAR- International Journal of Research and Analytical Reviews Research Paper

1. http://is.muni.cz/do/econ/soubory/aktivity/

fai/35724989/FAI_issue2012_03_Kamal.pdf

2. http://www.oeconomica.uab.ro/upload/lucra

ri/1520132/19.pdf

3. http://www.cpmr.org.in/opinion/vol2/issue

2/articles/4.pdf

4. http://www.ijambu.in/assets/48_54.pdf

5. http://apjor.com/files/1383064654.pdf

http://ijbarr.com/downloads/2014/vol2-

issue3/16.pdf

6. http://www.theglobaljournals.com/ijar/file.p

hp?val=January_2014_1388584281_ee78c_84.

7. http://is.muni.cz/do/econ/soubory/aktivity/

fai/35724989/FAI_issue2012_03_Kamal.pdf

8. http://www.ipeindia.org/main/uploads/IPE/

JIPE/JIPE_36_12_2.pdf

9. http://www.ijmra.us/project%20doc/IJPSS_A

UGUST2012/IJMRA-PSS1409.pdf

10. http://www.wjsspapers.com/static/documen

ts/November/2013/6.%20Mokta.pdf

WEBSITE

1. www.bseindia.com in.investing.com/rate-

bonds/india-15-year-bond

2. http://www.torinwealth.com

Courage is going from failure to failure without losing enthusiasm.

– Winston Churchill