consolidated statement of financial position...

TRANSCRIPT

BC ENERGBANK SACONSOLIDATED STATEMENT OF FINANCIAL POSITIONAs at 31 December 2015

Notes 2015 2014M DL’000 M DL’000

ASSETSCash and balances with National Bank 3 528,344 450,730Current accounts and deposits with banks 4 356,409 221,062Financial investments, debt securities - held to maturity 5 271,970 132,274Loans, net 6 866,852 1,036,815Financial investments, equity securities - available-for-sale 7 1,044 1,139Investments in associates 8 3,455 3,416Investment property 9 47 47Intangible assets 10 2,426 3,171Property and equipment 11 118,098 119,485Current income tax asset 1,345Other assets 12 76,113 109,113

Total assets 2,226,103 2,077,252

LIABILITIESDue to banks 13 - 553Due to customers 14 1,541,115 1,416,706Other borrowings 15 188,196 200,853Other liabilities 16 10,033 7,871Current income tax liability - 197Deferred tax liabilities 17 2,784 20,241

Total liabilities 1,742,128 1,646,421

Shareholders' equityOrdinary shares 18 1 0 0 ,0 0 0 1 0 0 ,0 0 0

Property revaluation reserve 15,966 15,803

Other reserves 19 134,210 145,813

Retained earnings 233,799 167,780

Equity attributable to equity holders of the parent 483,975 429,396

Non-controlling interest - 1,435

Total equity 483,975 430,831

Total liabilities and shareholders’ equity 2,226,103 2,077,252

The accompanying notes are an integral part of these consolidated financial statements.

The consolidated financial statements were authorized for i*suc on 1R April 2016 by the Executives o f the Bank represented by:

President d ? f i , /?if /

Mr. Iurii Vasilachi / k . *

Chiel Accountant f (A

XJ Mr. Sergiu Slobodean\ . >

\

BC ENERGBANK SACONSOLIDATED STATEMENT OF COMPREHENSIVE INCOMEFor the Year Ended 31 December 2015

Notes 2015M DL’000

2014M DL’000

Interest and similar income Interest expense and similar charges

2323

158,848(75,290)

117,984(66,466)

Net interest income 83,558 51,518

Fee and commission income Fee and commission expense

2424

43,047(7,194)

44,200(6,951)

Net fee and commission income 35,853 37,249

Financial income, net Other operating expense, net

2526

69,971(1,284)

35,795(437)

Total operating income 188,098 124,125

•Impairment of loansImpairment of receivables and other assets

6 (31,137)(22,618)

1,454(259)

Net operating income 134,343 125,320

Personnel expensesGeneral and administrative expensesDepreciation and amortization

2728

10,11

(55,619)(25,928)

(5,318)

(51,496)(27,203)

(5,030)Total operating expenses (86,865) (83,729)

Share of profit o f an associate 8 37 (163)Profit before tax 47,515 41,428

Income tax expense 17 10,455 (4,894)Profit for the vear 57,970 36,534

Other comprehensive income 174 (173)Total comprehensive income for the year 58,144 36,361

Profit attributable to:Equity holders of the parent Non-controlling interests

59,405(1,435)

36,574(40)

57,970 36,534Total comprehensive income attributable to:Equity holders of the parent Non-controlling interests

59,579(1,435)

36,401(40)

58,144 36,361

Earnings per share (MDL per share) 33 29.07 18.18

The accompanying notes are an integral part o f these consolidated financial statements.

The consolidated financial statements were authorized for issue on 18 April 2016 by the Executives o f the Bank represented by:

President //£ ~ r\ fo il __ Chief Accountant / ̂

Mr. lurii Vastlachi * -// I : Mr. Sergiu Slobodean

2

BC ENERGBANK SACONSOLIDATED STATEMENT OF CHANGES IN EQUITYFor the Year Ended 31 December 2015

Attributable to equity holders of the Parent

Ordinaryshares

M DL’000

Propertyrevaluation

reserveM DL’000

Available for sale investments

revaluation reserve

M DL’000

Otherreserves

M DL’000

Retainedearnings

M DL’000

Noncontrolling

interestsM DL’000

TotalMDL’000

Balance at 1 January 2015 100,000 15,803 145,813 167,780 1,435 430,831Dividends - - ■ ■ (5,000) - (5,000)Transfer to reserves - - - (11,603) 11,603 - -Transfer to reserves - ( 11) - - 11 - -

Transactions with owners - (11) (11,603) 6,614 - (5,000)Profit for the year - - - - 59,405 (1,435) 57,970Impairment of non-current assets held for sale - 174 - * 174

Total comprehensive income - 174 - - 59,405 (1,435) 58,144

Balance at 31 December 2015 100,000 15,966 - 134,210 233,799 . 483,975

Balance at 1 January 2014 100,000 15,976 126,451 156,568 1,475 400,470Dividends - - - - (6,000) - (6,000)Transfer to reserves - - - 19,362 (19,362) - -

Transactions with owners - - 19,362 (25,362) - (6,000)Profit for the year 36,574 (40) 36,534Impairment of non-current assets held for sale (173) - - (173)

Total comprehensive income - (173) - - 36,574 (40) 36,361

Balance at 31 December 2014 100,000 15,803 - 145,813 167,780 1,435 430,831) —

The accompanying notes are an integral part o f these consolidated financial statements.

3

BC ENERGBANK SACONSOLIDATED STATEMENT OF CASH FLOWSFor the Year Ended 31 December 2015

Notes 2015 2014M DL’000 M DL’000

Cash flows from operating activitiesInterest receipts 155,138 114,087

Interest payments (73,524) (64,705)Net fee and commission receipts 35,853 37,249Net financial and other operating income 82,982 45,269Staff costs paid (51,062) (47,243)Payments of general and administrative expenses (25,529) (26,723)Cash flows before working capital changes 123,858 57,934

(Increase) /decrease in operating assets:Due from NBM (15,848) (17,257)

Current accounts and deposit^ with banks - ( 1 2 0 )

Investment debt securities over 90 days (30,167) (15,227)

Loans 104,284 (65,840)Other assets 48,680 2,051Increase /(decrease) in operating liabilities:Due to banks (553) 243

Due to customers 123,061 54,936Other liabilities (2,530) (6,192)Net cash from operating activities before income tax 350,785 10,528

Income tax paid (7,800) (2,417)Net cash from/(used in) operating activities 342,985 8,111

Cash flows from investing activitiesPurchase of intangible assets (163) (1,927)

Purchase of property and equipment (5,010) (4,236)Proceeds from disposal of property and equipment 31 -Payments of tangible assets available for sale (71) -Proceeds from the sale of financial investments 459 -Net cash used in investing activities (4,754) (6,163)

Cash flows from financing activitiesProceeds from loans and borrowings 174,366 68,434

Repayment of loans and borrowings (187,441) (58,587)Dividends paid (5,000) (6 ,0 0 0 )

Net cash from/(used in) financing activities (18,075) 3,847

Net foreign exchange difference (11,819) (9,977)

Net increase/(decrease) in cash and cash equivalents 308,337 (4,182)

Cash and cash equivalents at 1 January 567,932 572,114

Cash and cash equivalents at 31 December 22 876,269 567,932

The accompanying notes are an integral part of these consolidated financial statements.

4

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

1. Corporate information

BC Energbank SA (“the Bank”) was established in the Republic o f Moldova on 16 January 1997 as a closed joint stock company. The Bank is principally engaged in retail banking operations in the Republic o f Moldova. The Bank operates through its head office located in Chisinau, 22 branches (22 branches as at 31 December2013) and 44 agencies (49 agencies as at 31 December 2014) located throughout the country.

At year-end 2015 the Bank possessed a license granted by the National Bank of Moldova, which allows the Bank to be engaged in all banking activities.

As at 31 December 2014 the Bank had one subsidiary (together referred as “the Group”): Oldex SA, a brokerage company, having a shareholding of 51%. The Bank is the ultimate parent of the Group.

In April 2015 the Bank sold share in the company Oldex SA.

The number of employees employedt by the Group as at 31 December 2015 was 588 (597 as at 31 December2014).

Fhe registered office o f the Bank is located at 23/3 Tighina Street, Chisinau, Republic of Moldova.

As Bank’s operations do not have significantly different risks and returns and considering the regulatory environment, the nature o f its services, the business process, as well as the types o f customers for the products and services and the methods used to provide the services are homogenous for all Bank’s activities, the Bank operates as a single business segment unit and its activities are exclusively carried out in the Republic of Moldova.

The Board of Directors formulates policies for the operation of the Group and supervises their implementation. The Board is composed o f 7 members appointed by the General Meeting of Shareholders.

As at 31 December 2015 the Board of Directors comprised the following members:

- Mr. Vladimir Tonciuc, Chairman o f the Board;- Mr.Valeriu Usatii, Energoimpex, Member of the Board;- Mr.Mihail Pop, Member of the Board;- Mrs. Natalia Cecetova, Gamaiun SRL, Member of the Board;- Mrs.Maximenco Galina, Member of the Board;- Mrs.Natalia Covanji, Member of the Board;- Mr. Dimov Ghennadi, Member of the Board.

These consolidated financial statements were authorised for issue on 18 April 2016 by the Executives of the Bank represented by the President and the Chief Accountant.

2. Accounting policies

2.1 Basis of preparation

Statement of complianceThe consolidated financial statements of the Group have been prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB).

Basis of measurementThe financial statements have been prepared under the historic cost convention, except for land and buildings, investment properties and available-for-sale assets that have been measured at fair value.

5

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.1 Basis of preparation (continued)

Functional and presentation currencyThe consolidated financial statements are presented in Moldovan lei (“MDL”), which is also its functional currency and the currency of the country in which the Group operates. All financial information presented in MDL has been rounded to the nearest thousands, except when otherwise indicated.

Basis of consolidationThe consolidated financial statements comprise the financial statements of the Bank as at and for the year ended 31 December each year. The financial statements of the subsidiary are prepared for the same reporting year, using consistent accounting policies.

All intra-group balances, transactions, income and expenses and profits and losses resulting from intra-group transactions are eliminated in.full.

Subsidiaries are fully consolidated from the date on which control is transferred to the Bank. Control is achieved where the Bank has the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities. The results o f subsidiaries acquired or disposed o f during the year are included in the consolidated income statement from the date of acquisition or up to the date of disposal, as appropriate.

Non-controlling interests represent the portion of profit or loss and net assets not owned, directly or indirectly,by the Bank and are presented separately in the income statement and within equity in the consolidated balance sheet, separately from parent shareholders’ equity. Acquisitions of non-controlling interests are accounted for using the parent entity extension method, whereby, the difference between the consideration and the fair value of the share of the net assets acquired is recognised as goodwill. Any deficiency of the cost o f acquisition below the fair values of the identifiable net assets acquired (i.e. a discount on acquisition) is recognised directly in the income statement in the year of acquisition.

2.2 Significant accounting judgments and estimates

The Group makes estimates and assumptions that affect the reported amounts of assets and liabilities within thenext financial year. Estimates and judgements are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances.

(i) Impairment losses on loans and advancesThe Group reviews its loan portfolios to assess impairment at least on a monthly basis. In determining whether an impairment loss should be recorded in the income statement, the Group makes judgements as to whether there is any observable data indicating that there is a measurable decrease in the estimated future cash flows from a portfolio o f loans before the decrease can be identified with an individual loan in that portfolio. This evidence may include observable data indicating that there has been an adverse change in the payment status of borrowers in a group, or national or local economic conditions that correlate with defaults on assets in the group. Management uses estimates based on historical loss experience for assets with credit risk characteristics and objective evidence o f impairment similar to those in the portfolio when scheduling its future cash flows. The methodology and assumptions used for estimating both the amount and timing of future cash flows are reviewed regularly to reduce any differences between loss estimates and actual loss experience.

Where the final outcome o f these factors is different from the amounts that were initially recorded, such differences could materially impact the provision for loan impairment in the period in which such determination is made.

6

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.2 Significant accounting judgments and estimates (continued)

(ii) Going concernThe Group’s management has made an assessment of the Group’s ability to continue as a going concern and is satisfied that the Group has the resources to continue in business for the foreseeable future. Furthermore, the management is not aware of any material uncertainties that may cast significant doubt upon the Group’s ability to continue as a going concern. Therefore, the financial statements continue to be prepared on the going concern basis.

(iii) Fair value o f financial instrumentsThe fair value o f financial instruments that are not traded in an active market is determined by using valuation techniques. The management uses its judgment to select the valuation method and make assumptions that are mainly based on market conditions existing at each balance sheet date.

2.3 Change in accounting policies

The accounting policies adopted are consistent with those o f the previous financial year. The adoption of new standards and interpretations effective for the Group from 1 January 2015 did not have any impact on the accounting policies, financial position or performance of the Group.

2.4 Summary of significant accounting policies

The principal accounting policies applied in the preparation o f these consolidated financial statements are set out below.

a. Foreign currency translation

Foreign currency transactions are translated into the functional currency using the exchange rates prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of such transactions and from the translation at year-end exchange rates o f monetary assets and liabilities denominated in foreign currencies are recognized in the income statement.

Changes in the fair value o f monetary securities denominated in foreign currency classified as available for sale are analysed between translation differences resulting from changes in the amortised cost of the security and other changes in the carrying amount of the security. Translation differences related to changes in the amortised cost are recognized in profit or loss, and other changes in the carrying amount are recognized in equity.

Translation differences on non-monetary items, such as equity investments classified as available-for-sale financial assets, are included in the fair value reserve in equity. The year-end and average rates for the year were:

2015 2014USD EURO USD EURO

Average for the period Year end

18.816119.6585

20.898021.4779

14.038815.6152

18.632118.9966

7

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.4 Summary of significant accounting policies (continued)

b. Financial assetsThe Group classifies its financial assets in the following categories: loans and receivables, held-to-maturity investments and available-for-sale financial assets. Management determines the classification of its investments at initial recognition.

(i) Loans and receivablesLoans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market, other than: (a) those that the entity intends to sell immediately or in the short term, which are classified as held for trading, and those that the entity upon initial recognition designates as at fair value through profit or loss; (b) those that the entity upon initial recognition designates as available for sale; or (c) those for which the holder may not recover substantially all of its initial investment, other than because of credit deterioration.

(ii) Held-to-maturityHeld-to-maturity investments are non-derivative financial assets with fixed or determinable payments and fixed maturities that the Group’s management has the positive intention and ability to hold to maturity. If the Group were to sell other than an insignificant amount of held-to-maturity assets, the entire category would be tainted and reclassified as available-for-sale. Included in this category are, also, treasury bills and NBM certificates.

(Hi) Available-for-saleAvailable-for-sale investments are those intended to be held for an indefinite period of time, which may be sold in response to needs for liquidity or changes in interest rates, exchange rates or equity prices.

Regular - way purchases and sales o f financial assets at fair value through profit and loss, held-to-maturity and available-for-sale are recognized on trade-date - the date on which the Group commits to purchase or sell the asset.

Financial assets are initially recognized at fair value plus transaction costs for all financial assets not carried at fair value through profit or loss. Financial assets carried at fair value through profit and loss are initially recognized at fair value, and transaction costs are expensed in the income statement. Financial assets are derecognized when the rights to receive cash flows from the financial assets have expired or where the Group has transferred substantially all risks and rewards of ownership. Financial liabilities are derecognized when they are extinguished, that is, when the obligation is discharged, cancelled or expired.

Available-for-sale financial assets and financial assets at fair value through profit or loss are subsequently carried at fair value. Loans and receivables and held-to-maturity investments are carried at amortized cost using the effective interest method. Gains and losses arising from changes in the fair value of the ‘financial assets at fair value through profit or loss’ category are included in the income statement in the period in which they arise. Gains and losses arising from changes in the fair value of available-for-sale financial assets are recognized directly in equity, until the financial asset is derecognized or impaired. At this time, the cumulative gain or loss previously recognized in equity is recognized in profit or loss.

However, interest calculated using the effective interest method and foreign currency gains and losses on monetary assets classified as available for sale are recognized in the income statement. Dividends on available- for-sale equity instruments are recognized in the income statement when the entity’s right to receive payment is established.

8

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.4 Summary of significant accounting policies (continued)

b. Financial assets (continued)The fair values of quoted investments in active markets are based on current bid prices. If the market for a financial asset is not active (and for unlisted securities), the Group establishes fair value by using valuation techniques. These include the use o f recent arm ’s length transactions, discounted cash flow analysis, option pricing models and other valuation techniques commonly used by market participants.

c. Investments in associatesAn associate is an entity in which the Group has significant influence and which is neither a subsidiary nor a joint venture. In the separate financial statements of the Group, investments in associates are carried at equity method.

The reporting dates of the associate and the Group are identical and the associate’s accounting policies conform to those used by the Group for transactions and events in similar circumstances.

d. Offsetting financial instrumentsFinancial assets and liabilities are offset and the net amount reported in the balance sheet when there is a legally enforceable right to set off the recognized amounts and there is an intention to settle on a net basis, or realize the asset and settle the liability simultaneously.

This is not generally the case with master netting agreements, therefore, the related assets and liabilities are presented gross in statement of financial position.

e. Interest income and expenseInterest income and expense for all interest-bearing financial instruments, except for those classified as held for trading or designated at fair value through profit or loss are recognized in the income statement for all instruments measured at amortised cost using the effective interest method.

The effective interest method is a method of calculating the amortised cost o f a financial asset or a financial liability and of allocating the interest income or interest expense over the relevant period. The effective interest rate is the rate that exactly discounts estimated future cash payments or receipts through the expected life o f the financial instrument or, when appropriate, a shorter period to the net carrying amount of the financial asset or financial liability. When calculating the effective interest rate, the Group estimates cash flows considering all contractual terms of the financial instrument but does not consider future credit losses. The calculation includes all fees and commissions paid or received between parties to the contract that are an integral part o f the effective interest rate, transaction costs and all other premiums or discounts.

Once a financial asset or a group of financial assets has been written down as a result of an impairment loss, interest income is recognized using the rate of interest used to discount the future cash flows for the purpose of measuring the impairment loss.

9

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.4 Summary of significant accounting policies (continued)

f. Fee and commission incomeFees and commissions are generally recognized on an accrual basis when the service has been provided. Loan commitment fees for loans that are likely to be drawn down are deferred (together with related direct costs) and recognized as an adjustment to the effective interest rate on the loan. Commission and fees arising from negotiating, or participating in the negotiation of, a transaction for a third party - such as the arrangement of the acquisition of shares or other securities or the purchase or sale of businesses - are recognized on completion of the underlying transaction. Portfolio and other management advisory and service fees are recognized based on the applicable service contracts, usually on a time-apportion basis.

g. Sale and repurchase agreementsSecurities sold subject to repurchase agreements (‘repos’) are classified in the financial statements as available- for-sale securities (treasury bills) and the counter party liability is included in amounts due to banks or customers, as appropriate. Securities purchased under agreements to resell (‘reverse repos’) are recorded as loans and advances to other banks or customers, as appropriate. The difference between sale and repurchase price is treated as interest and accrued over the life o f the agreements using the effective interest method.

Securities held by the Group as collateral for lending activities with financial institutions are not recognized in the financial statements, unless these are sold to third parties, in which case the purchase and sale are recorded with the gain or loss included in trading income. The obligation to return them is recorded at fair value as a trading liability.

h. Impairment of financial assets

(i) Assets carried at amortized costsThe Group’s assesses at each balance sheet date whether there is objective evidence that a financial asset or group of financial assets is impaired. A financial asset or a group of financial assets is impaired and impairment losses are incurred if, and only if, there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition of the asset (a ‘loss event’) and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or group of financial assets that can be reliably estimated.

The criteria that the Group uses to determine that there is objective evidence o f an impairment loss include:

• Delinquency in contractual payments of principal or interest;• Cash flow difficulties experienced by the borrower (for example, equity ratio, net income percentage of sales);• Breach of loan covenants or conditions;• Initiation of bankruptcy proceedings;• Deterioration of the borrower’s competitive position;• Deterioration in the value of collateral; and• Downgrading below investment grade level.

The estimated period between a loss occurring and its identification is determined by management for each identified portfolio. In general, the periods vary from 6 months to 12 months.

10

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.4 Summary of significant accounting policies (continued)

h. Impairment of financial assets (continued)

The Group first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant, and individually or collectively for financial assets that are not individually significant. If the Group determines that no objective evidence o f impairment exists for an individually assessed financial asset, whether significant or not, it includes the asset in a group of financial assets with similar credit risk characteristics and collectively assesses them for impairment. Assets that are individually assessed for impairment and for which an impairment loss is or continues to be recognized are not included in a collective assessment of impairment.

The amount of the loss is measured tfS the difference between the asset’s carrying amount and the present value o f estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset’s original effective interest rate. The carrying amount of the asset is reduced through the use of an allowance account and the amount of the loss is recognized in the income statement. If a loan or held-to-maturity investment has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate determined under the contract. As a practical expedient, the Group may measure impairment on the basis of an instrument’s fair value using an observable market price.

The calculation of the present value of the estimated future cash flows o f a collateralized financial asset reflects the cash flows that may result from foreclosure less costs for obtaining and selling the collateral, whether or not foreclosure is probable.

For the purposes of a collective evaluation of impairment, financial assets are grouped on the basis o f similar credit risk characteristics (i.e., on the basis o f the Group’s grading process that considers asset type, industry, geographical location, collateral type, past-due status and other relevant factors). Those characteristics are relevant to the estimation of future cash flows for groups o f such assets by being indicative of the debtors’ ability to pay all amounts due according to the contractual terms of the assets being evaluated.

Future cash flows in a group o f financial assets that are collectively evaluated for impairment are estimated on the basis o f the contractual cash flows o f the assets in the Group and historical loss experience for assets with credit risk characteristics similar to those in the Group. Historical loss experience is adjusted on the basis of current observable data to reflect the effects o f current conditions that did not affect the period on which the historical loss experience is based and to remove the effects o f conditions in the historical period that do not exist currently.

Estimates of changes in future cash flows for groups of assets should reflect and be directionally consistent with changes in related observable data from period to period (for example, changes in unemployment rates, property prices, payment status, or other factors indicative o f changes in the probability o f losses in the group and their magnitude). The methodology and assumptions used for estimating future cash flows are reviewed regularly by the Group to reduce any differences between loss estimates and actual loss experience. When a loan is uncollectible, it is written off against the related provision for loan impairment. Such loans are written off after all the necessary procedures have been completed and the amount of the loss has been determined.

If in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognized (such as an improvement in the debtor’s credit rating), the previously recognized impairment loss is reversed by adjusting the allowance account. The amount of the reversal is recognized in the income statement in impairment change for credit losses.

11

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.4 Summary of significant accounting policies (continued)

h. Impairment of financial assets (continued)

(ii) Assets carried at fa ir valueThe Group assesses at each balance sheet date whether there is objective evidence that a financial asset or a group of financial assets is impaired. In the case o f equity investments classified as available-for-sale, a significant or prolonged decline in the fair value of the security below its cost is considered in determining whether the assets are impaired. If any such evidence exists for available-for- sale financial assets, the cumulative loss - measured as the difference between the acquisition cost and the current fair value, less any impairment loss on that financial asset previously recognized in profit or loss - is removed from equity and recognized in the income statement. If, in a subsequent period, the fair value of a debt instrument classified as available for sale increases and the increase can be objectively related to an event occurring after the impairment loss was recognized in profit or loss, the impairment loss is reversed through the income statement.

(iii) Renegotiated loansWhere possible, the Group seeks to restructure loans rather than to take possession o f collateral. This may involve extending the payment arrangements and the agreement of new loan conditions. Once the terms have been renegotiated any impairment is measured using the original Effective Interest Rate (“EIR”) as calculated before the modification of terms and the loan is no longer considered past due. Management continuously reviews renegotiated loans to ensure that all criteria are met and that future payments are likely to occur. The loans continue to be subject to an individual or collective impairment assessment, calculated using the loan’s original EIR.

i. Impairment of non - financial assetsAssets that have an indefinite useful life are not subject to amortization and are tested annually for impairment. Assets that are subject to amortization are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognized for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset’s fair value less costs to sell and value in use. For the purposes o f assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows (cash-generating units). Non-financial assets other than goodwill that suffered impairment are reviewed for possible reversal o f the impairment at each reporting date.

j. Cash and cash equivalentsFor the purposes o f the cash flow statement, cash and cash equivalents comprise balances with less than three months’ maturity o f the assets at acquisition dates including: cash, non-restricted balances with National Bank of Moldova, treasury bills, NBM certificates, amounts due from other banks and amounts due from quick payment systems.

12

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.4 Summary of significant accounting policies (continued)

k. Intangible assetsAcquired computer software licenses are capitalized on the basis of the costs incurred to acquire and bring to use the specific software. These costs are amortized on the basis o f the expected useful lives (three to five years) using the straight-line method.

Costs associated with developing or maintaining computer software programs are recognized as an expense as incurred. Costs that are directly associated with the production of identifiable and unique software products controlled by the Group, and that will probably generate economic benefits exceeding costs beyond one year, are recognized as intangible assets. Direct costs include software development employee costs and an appropriate portion of relevant overheads.

Computer software development costs recognized as assets are amortised using the straight-line method over their useful lives (not exceeding five years).

1. Property and equipmentBuildings are stated at revalued amounts less accumulated depreciation and less provision for impairment, where required. Other property and equipment is stated at historical cost less depreciation. Historical cost includes expenditure that is directly attributable to the acquisition of the items.

Land is not depreciated. Depreciation on other assets is calculated using the straight-line method to allocate their cost to their residual values over their estimated useful lives, as follows:

Asset type________________________ ______________________ YearsBuildings 25-75Furniture and equipment 2-20Motor vehicles 7-10Other 5-20

Assets under construction are not depreciated until there are brought in use.

The assets’ residual value and useful lives are reviewed, and adjusted if appropriate, at each balance sheet date. Assets that are subject to amortization are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount. The recoverable amount is the higher of the asset’s fair value less costs to sell and value in use.

Gains and losses on disposal of property, plant and equipment are determined by reference to their carrying amount. These are included in their operating expenses in the income statements.

13

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.4 Summary of significant accounting policies (continued)

m. Investment propertyProperty held for long-term rental yields or for capital appreciation or both, which is not occupied by the Group is classified as investment property.

Investment property comprises freehold land. Investment property is carried at fair value. Fair value is based on active market prices, adjusted, if necessary, for any difference in the nature, location or condition of the specific asset. If this information is not available, the Group uses alternative valuation method such as sales comparison method by comparing similar or substitute properties sold in the market with subject property. These valuations are reviewed annually by Directors.

I f an investment property becomes owner-occupied, it is reclassified as property, plant and equipment and its fair value at the date o f reclassification becomes its cost for accounting purposes o f subsequent recording. Property that is being constructed or developed for future use as investment property is classified as property, plant and equipment and stated at cost until construction or development is complete, at which time it is reclassified and subsequently accounted for as investment property.

If an item of property, plant and equipment becomes an investment property because its use has changed, any difference resulting between the carrying amount and the fair value of this item at the date of transfer is recognised in equity as a revaluation of property, plant and equipment under IAS 16. However, if a fair value gain reverses a previous impairment loss, the gain is recognised in the income statement. Upon the disposal o f such investment property, any surplus previously recorded in equity is transferred to retained earnings; the transfer is not made through the income statement.

n. LeasesThe determination of whether an arrangement is a lease or it contains a lease, is based on the substance of the arrangement and requires an assessment of whether the fulfilment o f the arrangement is dependent on the use of a specific asset or assets and the arrangement conveys a right to use the asset.

Group as a lesseeLease which does not transfer to the Group substantially all the risks and benefits incidental to ownership of the leased item are operating leases. Operating lease payments are recognised as an expense in the income statement on a straight line basis over the lease term.

Group as a lessorLeases where the Group does not transfer substantially all the risk and benefits o f ownership of the asset are classified as operating leases. Initial direct costs incurred in negotiating operating leases are added to the carrying amount o f the leased asset and recognised over the lease term on the same basis as rental income.

o. Defined contribution planThe Group, in the normal course of business makes payments to the Moldovan State funds on behalf o f its employees for pension, health care and unemployment benefit. All employees of the Group are members of the State pension plan.

The Group does not operate any other pension scheme and, consequently, has no further obligation in respect of pensions. The Group does not operate any other defined benefit plan or post-retirement benefit plan. The Group has no obligation to provide further services to current or former employees.

14

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.4 Summary of significant accounting policies (continued)

p. ProvisionsProvisions and legal claims are recognized when the Group has a present legal or constructive obligation to transfer economic benefits as a result of past events. It is probable that an outflow of resources will be required to settle the obligation and the amount has been reliably estimated.

Where there are a number of similar obligations, the likelihood that an outflow will be required in settlement is determined by considering the class of obligations as a whole. A provision is recognized even if the likelihood of an outflow with respect to any one item included in the same class of obligations may be small.

Provisions are measured at the present value of the expenditures expected to be required to settle the obligation using a pre-tax rate that reflects current market assessments o f the time value o f money and the risks specific to the obligation. The increase in the provision due to passage of time is recognized as interest expense.

q. Financial guarantee contractsFinancial guarantee contracts are contracts that require the issuer to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payments when due, in accordance with the terms of a debt instrument. Such financial guarantees are given to banks, financial institutions and other bodies on behalf o f customers to secure loans, overdrafts and other banking facilities.

Financial guarantees are initially recognized in the financial statements at fair value on the date the guarantee was given. Subsequent to initial recognition, the bank’s liabilities under such guarantees are measured at the higher o f the initial measurement, less amortization calculated to recognise in the income statement the fee income earned on a straight line basis over the life of the guarantee and the best estimate of the expenditure required to settle any financial obligation arising at the balance sheet date. These estimates are determined based on experience o f similar transactions and history o f past losses, supplemented by the judgment o f Management. Any increase in the liability relating to guarantees is taken to the income statement under other operating expenses.

r. TaxationIncome tax payable on profits, based on the applicable Moldovan tax law is recognized as an expense in the period in which profits arise. The tax effects o f income tax losses available for carry forward are recognized as an asset when it is probable that future taxable profits will be available against which these losses can be utilised.

Deferred income tax is provided in full, using the liability method, on temporary differences arising between the tax bases o f assets and liabilities and their carrying amounts in the financial statements. Deferred income tax is determined using tax rates (and laws) that have been enacted or substantially enacted by the balance sheet date and are expected to apply when the related deferred income tax asset is realized or the deferred income tax liability is settled.

The principal temporary differences arise from depreciation of equipment, provisions for loans and advances to customers, other assets and other liabilities. The rates enacted or substantively enacted at the balance sheet date are used to determine deferred income tax. However, the deferred income tax is not accounted for if.it arises from initial recognition of an asset or liability in a transaction other than a business combination that at the time o f the transaction affects neither accounting nor taxable profit nor loss.

Deferred tax assets are recognized where it is probable that future taxable profit will be available against which the temporary differences can be utilised.

15

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.4 Summary of significant accounting policies (continued)

s. BorrowingsBorrowings are recognised initially at fair value, being their issue proceeds (fair value of consideration received) net of transaction costs incurred. Subsequently borrowings are stated at amortised cost and any difference between net proceeds and the redemption value is recognized in the income statement over the period of the borrowings using the effective interest method.

t. DividendsDividends are not accounted for until they have been approved at the Annual General Meeting,

u. Assets for resaleAssets for resale include foreclosed collateral on non-performing loans. They are classified as assets held for sale as their carrying amount is to be recovered principally through a sale transaction and a sale is considered highly probable. They are stated at the lower o f carrying amount and fair value less costs to sell if their carrying amount is to be recovered principally through a sale transaction rather than through continuing use.

2.5 New and revised standards that are effective for annual periods beginning on or after 1 January 2015

A number of new and revised standards are effective for annual periods beginning on or after 1 January 2015. Information on these new standards is presented below.

2.6 Standards, amendments and interpretations to existing standards that are not yet effective and have not been adopted early by the Bank

At the date of authorisation of these financial statements, certain new standards, and amendments to existing standards have been published by the IASB that are not yet effective, and have not been adopted early by the B. Information on those expected to be relevant to the Bank’s financial statements is provided below.

Management anticipates that all relevant pronouncements will be adopted in the Bank’s accounting policies for the first period beginning after the effective date o f the pronouncement. New standards, interpretations and amendments not either adopted or listed below are not expected to have a material impact on the Bank’s financial statements.

IFRS 9 ‘Financial Instruments’ (2014)

The IASB recently released IFRS 9 ‘Financial Instruments’ (2014), representing the completion of its project to replace IAS 39 ‘Financial Instruments: Recognition and Measurement’. The new standard introduces extensive changes to IAS 39’s guidance on the classification and measurement of financial assets and introduces a new ‘expected credit loss’ model for the impairment of financial assets. IFRS 9 also provides new guidance on the application of hedge accounting.

The Bank’s management has yet to assess the impact of IFRS 9 on these financial statements. The new standard is required to be applied for annual reporting periods beginning on or after 1 January 2018.

16

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

2. Accounting policies (continued)

2.6 Standards, amendments and interpretations to existing standards that are not yet effective and have not been adopted early by the Bank (continued)

IFRS 15 ‘Revenue from Contracts with Customers’

IFRS 15 presents new requirements for the recognition o f revenue, replacing IAS 18 ‘Revenue’, IAS 11 ‘Construction Contracts’, and several revenue-related Interpretations. The new standard establishes a control- based revenue recognition model and provides additional guidance in many areas not covered in detail under existing IFRSs, including how to account for arrangements with multiple performance obligations, variable pricing, customer refund rights, supplier repurchase options, and other common complexities.

IFRS 15 is effective for reporting periods beginning on or after 1 January 2017. The Bank’s management believes that the adoption o f IFRS 15 will have a non-significant impact on financial statements because most of Bank’s revenues are recognized in accordance with IFRS 4 “Insurance contracts” .

Amendments to IFRS 11 Joint Arrangements

These amendments provide guidance on the accounting for acquisitions of interests in joint operations constituting a business. The amendments require all such transactions to be accounted for using the principles on business combinations accounting in IFRS 3 ‘Business Combinations’ and other IFRSs except where those principles conflict with IFRS 11. Acquisitions of interests in joint ventures are not impacted by this new guidance.

Bank’s management believes that those amendments will not impact the financial statements due to the fact that the Bank has not entered into any joint arrangements.

17

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

>. Cash and balances with National Bank

2015 2014M DL’000 M DL’000

Cash on hand 180,771 175,819Current account with NBM 226,685 169,031

Included in cash and cash equivalents (Note 22) 407,456 344,8501

Mandatory reserve 1 2 0 ,8 8 8 105,880

528,344 450,730

Current account and obligatory resen’esThe National Bank of Moldova (NBM) requires commercial banks to maintain for liquidity purposes minimum reserves calculated at a certain rate o f the average funds borrowed by banks during the previous month (between the 8th of the current month and the 7th of the following month), including all customer deposits. Based on the decision Nr 85 by the Administrative Council o f NBM dated 15 April 2004, the method for calculation and maintaining the compulsory reserves was changed. Funds attracted in Moldovan Lei (MDL) and in nonconvertible currencies are reserved in MDL. Funds attracted in freely convertible currencies are reserved in US Dollars (USD) and/or EURO (EUR). As of 31 December 2015 the rate for calculation of the minimum compulsory reserve in MDL was 35% (31 December 2014 14%), in USD/EUR was 14.0% (31 December 2014: 14.0%).

As at 31 December 2015 the balance reserved in the current account held with the NBM amounted to M DL’000 226,686 (31 December 2014: M DL’000 169,032). This balance included compulsory reserve on funds attracted in Moldovan Lei and non-convertible currencies. The balance reserved on USD and EUR compulsory reserve accounts amounted to USD’000 2,896 and EUR’000 2,977 respectively (31 December 2014: USD’000 3,036 and EUR’000 3,078).

The interest paid by NBM on the compulsory reserves during 2015 varied between 0.27% and 0.41% per annum for reserves in foreign currency and 7.46% - 16.50% for reserves in MDL (2014: 0.34% and 1.28% for reserves in foreign currency and 0.5% - 1.27% per annum for reserves in MDL). The compulsory reserves on funds attracted in USD and EUR are placed in Nostro accounts of NBM at correspondent banks incorporated in OECD countries.

The obligatory reserves held in the current account at NBM are available for use in the Bank’s day to day operations.

18

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

4. Current accounts and deposits with banks

2015M DL’000

2014M DL’000

Current accounts Overnight placements

130,619225,790

85,344135,598

Included in cash and cash equivalents (Note 22) 356,409 220,942

•Long term bank deposits with maturity more than 90 days 120

356,409 221,062

The major part of current accounts and deposits are held with local banks.

As at 31 December 2015 overnights include balances denominated in USD with Bank of New York during 2015 the interest rate on overnight deposits from 0.01% to 0.05%.

5. Financial investments, debt securities

2015M DL’000

2014M DL’000

State securitiesCertificates issued by the NBM

162,353109,617

132,274

271,970 132,274

Included in cash and cash equivalents (Note 22) Debt securities with maturity over 90 days

109,617162,353

99132,175

271,970 132,274

State securities as at 31 December 2015 represent MDL medium term securities issued by the Ministry of Finance of the Republic o f Moldova with interest rate ranging from 12.51% to 26.40% per annum (2014: 3.93%

to 10.70%).

Certificates issued by the National Bank of Moldova as at 31 December 2015 are 14 days original maturity bearing with interest rate ranging from 6.5% to 19.5% per annum (2014: from 3.5%- to 6.5%).

As o f 31 December 2015 and 2014 the Group did not hold any state securities as mortgage for loan from the NBM.

19

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

6. Loans, net

2015 2014M DL’000 M DL’000

Loans 890,981 1,063,587Less: Allowance for impairment losses (24,129) (26,772)

866,852 1,036,815

For the year ended 31 December 2015 the interest accrued on individually impaired loans amounted toM DL’000 5,679 (31 December 2014: M DL’000 5,383).

Analysis o f loan portfolio by industry is presented below:•

2015 2014M DL’000 M DL’000

Manufacturing and trade 315,675 377,848Agriculture and food industry 191,955 268,691Consumer loans 99,285 144,251Loans granted to financial non-banking sector 73,654 102,527Real estate, construction and land improvement 50,502 50,519Other 159,910 119,751

890,981 1,063,587

Range of loan interest rates practiced by the Bank is presented below:

2015 2014% %

Interest rate on loans (min/max) 4 .5 -2 1 .5 4 .7 5 -1 8 .0

The movement in provision for impairment of loans during the years 2015 and 2014 are presented below:

2015 2014M DL’000 M DL’000

Balance as at 1 January 26,772 33,732Write-offs (34,387) (6,131)

Recoveries 607 625

Charge for the year 31,137 (1,454)

Balance as at 31 December 24,129 26,772

Individual impairment 12,339 14,511

Collective impairment 11,790 12,261

24,129 26,772

20

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

6. Loans, net (continued)

Allowances fo r impairmentThe Group establishes an allowance for impairment losses that represents its estimate of incurred losses in its loan portfolio. The main components of this allowance are a specific loss component that relates to individually significant exposures, and a collective loan loss allowance established for groups of homogeneous assets in respect o f losses that have been incurred but have not been identified on loans subject to individual assessment for impairment.

Write o ff policyThe Group writes off a loan balance (and any related allowance for impairment losses) when the Group determines that the loans are uncollectible. This determination is reached after considering information such as the occurrence of significant changes in the borrower financial position such that the borrower can no longer pay the obligation, or that proceeds from eollateral will not be sufficient to pay back the entire exposure.

7. Financial investments, equity securities - available-for-sale

Investment securities available-for-sale include unlisted equity investments in local companies. The analysis o fequity investments is as follows:

Ownership Ownership Field of activity 2015 2014 2015 2014

% % M DL’000 M DL’000

Garant Invest SRL Deposit guarantee 9.92 9.92 440 440Birou de credit SRL Credit bureau 3.29 3.29 500 500Other 104 199

1,044__________1,139

All available-for-sale equity securities as at 31 December 2015 and 2014 are carried at cost because there is no quoted market price in an active market for them and the fair value cannot be reliably determined. No impairment was assessed in respect of these investments as at 31 December 2015 and 2014.

The movements in investment portfolio o f the Group are presented below:

2015 2014M DL’000 M DL’000

Balance as at 1 January 1,139 1,139

Additions 69 ■

Disposals (164) -Balance as at 31 December 1,044 1,139

21

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

8. Investments in associates

The following table illustrates summarised financial information of the Group’s investment in Electrosistem SA Electrosistem SA is an associated company, in which the Bank owns 24.83% (2014:24.83) of the share capital:

2015 201‘M DL’000 M DL’001

Share of the associate’s balance sheet:Assets 10,089 10,29;Liabilities (6,634) (6,879

Net assets 3.455 3,4 It

Share of the associate’s revenue and profit:Revenue 2,568 3,039Profit 37 (163)

9. Investment property

Movements in investment property are as follows:

2015 2014M DL’000 M DL’000

Balance as at 1 January 47 47Net change from fair value adjustment - -

Balance as at 31 December 47 47

As at 31 December 2015, the balance of investment property comprised of a plot o f land located in Onitcani (Republic of Moldova). Investment properties are stated at fair value, which has been determined based on valuations performed by Vlasercom Ltd, an independent specialist in valuing these types o f investment properties. The fair value of the investment property was determined using sales comparison approach.

22

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

10. Intangible assets

2015 2014M DL’000 M DL’000

CostBalance as at 1 January 9,387 7,502Additions 162 1,927

Disposals (2 ) (42)

Balance as at 31 December 9,547 9,387

Accumulated depreciationBalance as at 1 January 6,216 5,414Charge for the year 907 844Disposals (2 ) (42)

Balance as at 31 December 7,121 6,216

Net book value

At 31 December 2,426 3,171

The intangible assets represent computer software and workstation licenses.

As at 31 December 2015 the cost o f fully amortized intangible assets amounted to M DL’000 5,127 (as at 31 December 2014: M DL’000 2,477).

23

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

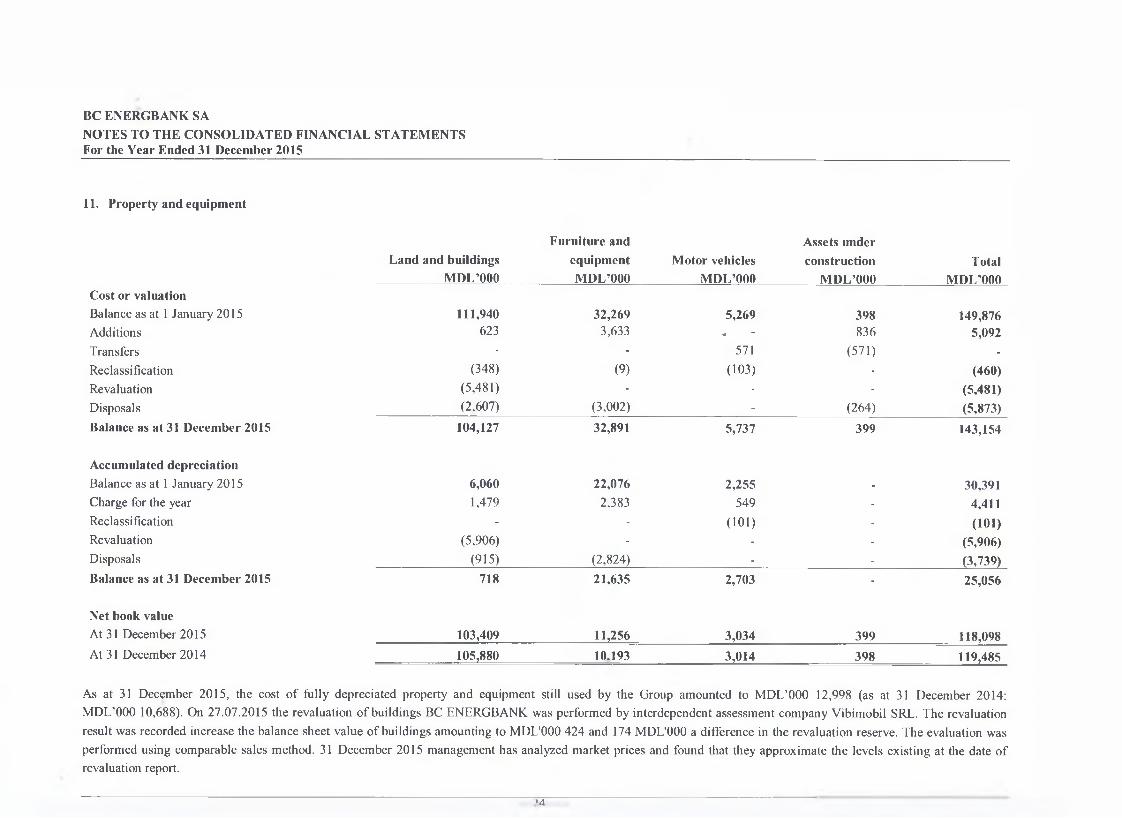

11. Property and equipment

Furniture and Assets imderLand and buildings equipment Motor vehicles construction Total

M DL’000 M DL’000 M DL’000 M DL’000 M DL’000Cost or valuationBalance as at 1 January 2015 111,940 32,269 5,269 398 149,876Additions 623 3,633 • “ 836 5,092Transfers - - 571 (571) -Reclassification (348) (9) (103) - (460)Revaluation (5,481) ■ ■ - (5,481)Disposals (2.607) (3,002) - (264) (5,873)Balance as at 31 December 2015 104,127 32,891 5,737 399 143,154

Accumulated depreciationBalance as at 1 January 2015 6,060 22,076 2,255 - 30,391Charge for the year 1,479 2,383 549 - 4,411Reclassification - - ( 1 0 1 ) - (101)Revaluation (5,906) - - - (5,906)Disposals (915) (2,824) - - (3,739)Balance as at 31 December 2015 718 21,635 2,703 - 25,056

Net book valueAt 31 December 2015 103,409 11,256 3,034 399 118,098At 31 December 2014 105,880 10.193 3,014 398 119,485

As at 31 December 2015, the cost o f fully depreciated property and equipment still used by the Group amounted to MDL’000 12,998 (as at 31 December 2014: MDL’000 10,688). On 27.07.2015 the revaluation of buildings BC ENERGBANK was performed by interdependent assessment company Vibimobil SRL. The revaluation result was recorded increase the balance sheet value of buildings amounting to MDL'000 424 and 174 MDL'000 a difference in the revaluation reserve. The evaluation was performed using comparable sales method. 31 December 2015 management has analyzed market prices and found that they approximate the levels existing at the date of revaluation report.

•4

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

1. Property and equipment (continued)

Furniture and Assets underLand and buildings equipment Motor vehicles construction Total

M DL’000 M DL’000 M DL’000 M DL’000 MDL’000Cost or valuationBalance as at 1 January 2014 110,711 31,888 5,171 1,225 148,995

Additions 31 3,106 - 1,324 4,461

Transfers 1,198 - 953 (2,151) -

Reclassification ■ ■ .(59) - (59)

Disposals - (2,725) (796) - (3,521)

Balance as at 31 December 2014 111,940 32,269 5,269 398 149,876

Accumulated depreciationBalance as at 1 January 2014 4,304 22,441 2,635 - 29,380

Charge for the year 1,756 2,213 458 - 4,427

Disposals - (2,578) (838) - (3,416)

Balance as at 31 December 2014 6,060 22,076 2,255 - 30,391

Net book valueAt 31 December 2014 105,880 10,193 3,014 398 119,485

At 31 December 2013 106,407 9,447 2,536 1,225 119,615

25

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

12. Other assets

2015 2014M DL’000 M DL’000

Receivables from money transfer systems 2,787 2,041Settlements with other individuals 682 1,398Debtors on capital investments 173 -

Assets for resale 81,385 96,533Inventory and spare parts 1,583 1,367Prepayments 928 471Other assets 4,259 7,303Less: Allowance for losses on assets taken in possession (15,684) -

• 76,113 109,113

Assets acquired include land and buildings, taken into possession by the Bank in exchange for repayment ofloans. Management analysed and established that there are assets.

no significant indicators of impairment of acquired

13. Due to banks

2015 2014M DL’000 M DL’000

Term deposits - 553- 553

26

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

14. Due to customers

2015 2014

Corporate customersM DL’000 M DL’000

Current accounts 450,835 372,608

Term deposits 83,598 84,885

Individuals534,433 457,493

Current accounts 123,198 84,062Term deposits 883,484 875,151

1,006,682 959,213

11,541,115 1,416,706

The annual interest rates paid by the Group for the MDL and FCY deposits o f individuals and companies ranged as follows:

%

2015MDL FCY

% % % %

2014MDL

%FCY

% %

E nterprisesDemand deposits 0 8 .0 0.1 1.5 ■ - - - - -Term deposits up to 3 months 0.5 16.5 0.1 0.1 0 .0 - 1 ■ - -Term deposits >3 months< 1 year 0 .0 17.5 0.1 4.25 0 .0 - 2.25 0.5 - 1

Term deposits over 1 year 0 .0 18.0 0 .0 4.1 0 .0 - 10.5 0.5 - 6

IndividualsDemand deposits ■ - - - - - - - - -

Term deposits up to 3 months 0.5 17.2 0.1 0.1 0.5 - 1 0.1 - 0.5

Term deposits >3 months< 1 year 1.5 17.7 0.3 1.1 1.5 - 3 1 - 4.5

Term deposits over 1 year 0.3 18.5 0.1 5.5 0.3 - 9.7 0.1 - 6

5. Other borrowings

2015 2014Interest rate, % M DL’000 M DL’000

Subsidiary loansRISP loans with floating rate due 1.55-7.00 84,017 78,688

FIDA loans with floating rate due 0.80-7.00 56,029 80,662

PAC loans with floating rate due 1.55-7.00 13,333 13,608

KFW loans with floating rate due 1.55-7.00 2,659 4,300

Filiera Vinului loans with floating rate due 1.24-7.00 30,460 22,315

Interest accrued 1,698 1,280

____ 188,196 200,853

During 2015 and 2014 the Group didn’t have any defaults o f principal, interest or other breaches of contractual terms.

27

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

16. Other liabilities

2015 2014M DL’000 M DL’000

Suspense accounts 193 213Amounts in transit 91 115Settlements with employees 4,691 4,217Settlements with other individuals and institutions 4,010 3,049Dividends payable 28 18Other 1 ,0 2 0 259

10,033 7,871

Suspense accounts represent balances o f customers with incomplete information, which after the clearance aretransferred to customers’ accounts.

17. Taxation

The major components of tax expense and the reconciliation of the expected tax expense based on the effectivetax rate of 12% (2014: 12%) and the reported tax expense in profit or loss are as follows:

2015 2014M DL’000 M DL’000

Profit before tax 47,515 41,428Moldovan statutory income tax rate 12% 12%Expected tax expense 5,702 4,971

Effect o f deductible/non-deductible expenses/revenue 141 (77)Impact of tax facilities application (16,298) -Actual tax expense (10,455) 4,894

Tax expense comprises:Current tax expense 7,002 2,596Deferred tax expense:- Origination and reversal of temporary differences (17,457) 2,298Tax expense (10,455) 4,894

Impact of change in tax legislation refers to changing the allowance for losses on assets and conditional commitments, which entered into force on 1 May 2015. In accordance with changing tax laws o f the Republic of Moldova, financial institutions are allowed for deducting losses on assets and conditional commitments, calculated according to International Financial Reporting Standards (IFRS). Prior to this change, it was permitted deduction for losses calculated according to regulations approved by the National Bank of Moldova (NBM).

28

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

17. Taxation (continued)

Deferred taxes arising from temporary differences are summarized as follows:

Recognized inDeferred tax assets (liabilities) 1 January 2015 profit and loss 31 December 2015

M DL’000 M DL’000 M DL’000

AssetsLoans and advances to customers (16,298) 16,298 -

Property and equipment (4,086) 739 (3,347)

Other assets 143 (143) •

LiabilitiesOther liabilities - 563 563

(20,241) 17,457 (2,784)

Recognised as:Deferred tax asset - - ■

Deferred tax liability (20,241) 17,457 (2,784)

Deferred tax was calculated by applying the 2015 standard tax rate of 12% (2014 standard tax rate of 12%).

18. Ordinary shares

Share capital as at 31 December 2015 represents 2,000 thousand (31 December 2014: 2,000 thousand) ordinaryshares authorized and issued. As at 31 December 2015 and 2014 the nominal value per share is MDL 50. Allshares have equal voting rights and are fully paid.

Shareholders with a holding of more than or equal to 5% of the issued share capital are as follows:

2014 2014% %

ICS „RED UNION FENOSA” SA 9.98 9.98

Hostex Establishment 9.62 9.62

Esperan Property Consultants Ltd 9.60 9.60

Dima-Holding SRL 8.62 8.62

Sfinx-Impex SA 6.89 6.89

Enteh SA 8 .1 0 8 .1 0

Evident-Electro SA 7.33 7.33

DunavIM 6.07 6.07

Other, less than 5% each 33.79 33.79

1 0 0 .0 0 1 0 0 .0 0

There are 44 other shareholders (31 December 2014: 43) o f which 34 represent individuals and 10 - enterprises (31 December 2014: 33 individuals and 10 enterprises).

29

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

19. Reserves

2015 2014M DL’000 M DL’000

Statutory reserves 10,002 10,002General reserves for banking risks 124,208 135,811

134,210_______________ 145,813

In accordance with local legislation, the Group is required to create a legal reserve by appropriation of 5% of the net profit for the year until this reserve is equal to at least 10% of the issued and fully paid share capital. This is a non-distributable reserve.

General reserves for banking risks include amounts resulting from differences between assets impairment under IFRS and calculated but not provided for under prudential (NBM) norms. This reserve is non-distributable.

Revaluation reserves are made in respect o f property and equipment. This reserve is non-distributable.

20. Dividends per share

In year 2015 were proposed and distributed dividends for ordinary shares in the total amount of M DL’000 5,000 (MDL 2.5/share). In year 2014: M DL’000 5,000 (MDL 3/share).

21. Capital management

The Group’s objectives when managing capital are to safeguard the Group’s ability to continue as a going concern in order to provide returns for shareholders and benefits for other stakeholders and to maintain an optimal capital structure to reduce the cost o f capital.

In order to maintain or adjust the capital structure, the Group may adjust the amount of dividends paid to shareholders, return capital to shareholders, issue new shares or sell assets to reduce debt. No changes were made in the objectives, policies and processes from the previous years.

Capital adequacy and the use o f regulatory capital are monitored by the Group’s management, employing techniques based on the guidelines developed by the National Bank of Moldova.

The NBM requires each bank or banking group to hold the minimum level of the regulatory capital o f MDL’000 200,000 (31 December 2014: MDL’000 200,000) and maintain a ratio o f total regulatory capital to the risk- weighted asset at minimum of 16% (31 December 2014: 16%).

2015 2014M DL’000 M DL’000

Weighted average assets and contingent commitments inaccordance with NBM regulations 960,789 1,175,369Total normative capital in accordance with NBM regulations 340,206 272,113Risk weighted capital adequacy in accordance with NBMregulations, % 35.41 23.15

30

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

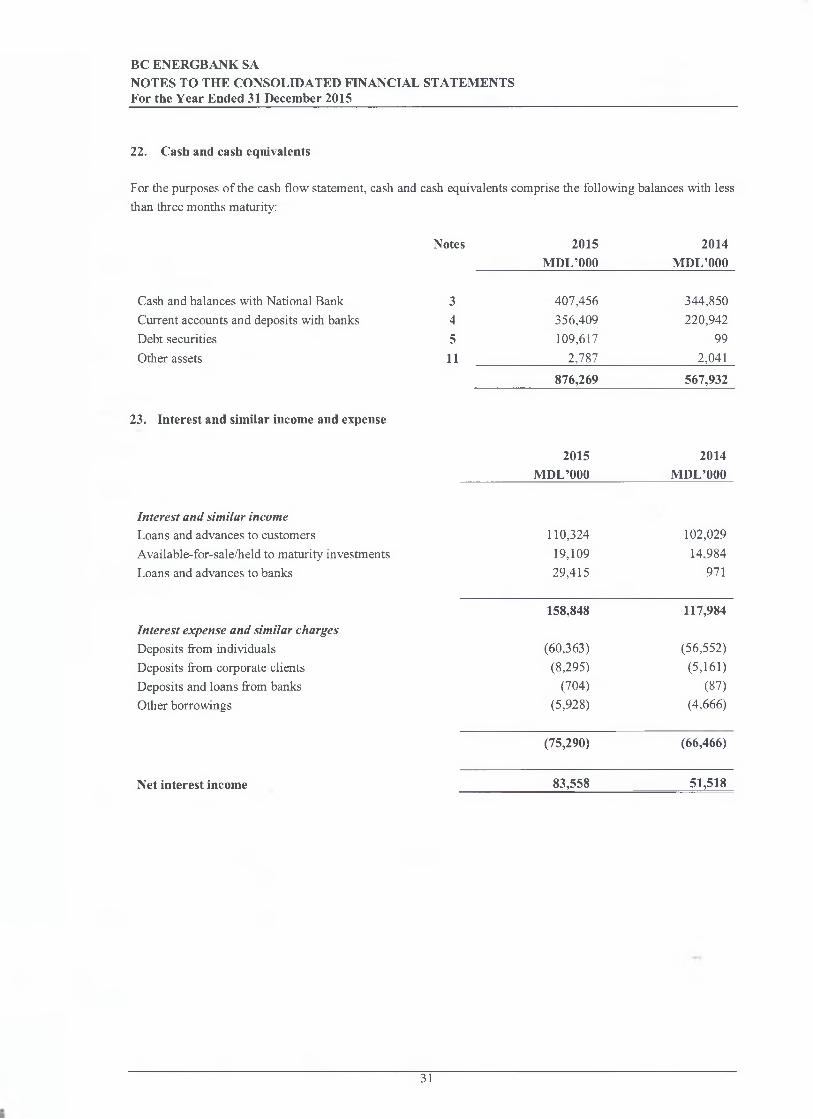

22. Cash and cash equivalents

For the purposes o f the cash flow statement, cash and cash equivalents comprise the following balances with less than three months maturity:

Notes 2015 2014M DL’000 M DL’000

Cash and balances with National Bank 3 407,456 344,850Current accounts and deposits with banks 4 356,409 220,942Debt securities 5 109,617 99Other assets 11 2,787 2,041

876,269 567,932

23. Interest and similar income and expense

2015 2014M DL’000 M DL’000

Interest and similar incomeLoans and advances to customers 110,324 102,029

Available-for-sale/held to maturity investments 19,109 14,984Loans and advances to banks 29,415 971

158,848 117,984Interest expense and similar chargesDeposits from individuals (60,363) (56,552)Deposits from corporate clients (8,295) (5,161)

Deposits and loans from banks (704) (87)

Other borrowings (5,928) (4,666)

(75,290) (66,466)

Net interest income 83,558 51,518

31

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

24. Net fee and commission income

Fee and commission income Processing of payments by clients Commission on guarantees and letters of credit Transactions with debit cards Other

Fee and commission expense Commissions on debit card services Payment transactions Other

Net fee and commission income

25. Financial income, net

Gains on trading of foreign currency, netForeign exchange lossesOther

26. Other operating expenses, net

Rent incomeGains/(losses) on disposal of property and equipment Gains/(losses) on disposal o f subsidiary company Other non-interest income

2015 2014M DL’000 M DL’000

38,194 38,8391,853 2,6551,173 9241,827 1,782

43,047 44,200

(3,751) (3,908)(3,302) (2,729)

(141) (314)

(7,194) (6,951)

35,853 37,249

2015 2014M DL’000 M DL’000

81,790 45,774(11,819) (9,979)

69,971 35,795

2015M DL’000

2014M DL’000

827 597157 (1,041)

(2,420) -152 7

(1,284) (437)

32

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

27. Personnel expenses

2015 2014M DL’000 M DL’000

Salaries and bonuses 36,065 33,094Social insurance and contributions 8,917 8,257

Medical insurance 1,647 1,396Other personnel expenses 4,907 4,981

Provision for unused vacation 4,083 3,768

55,619 51,496

The Group makes contributions to’ the State pension system of the Republic o f Moldova calculated as apercentage of gross salary. These contributions are charged to the income statement in the period in which therelated salary is earned by the employee.

28. General and administrative expenses

2015 2014M DL’000 M DL’000

Utilities and rent 5,744 5,497

Postage and telephone 2,244 2,419Safeguarding of assets and security costs 3,351 3,378

Advertising and charity 1,810 2,073

Stationery and supplies 1,307 1,475

Repairs and maintenance 5,543 6,262

Professional services 1,459 2,496

Guarantee fund 6 6 8 696

Taxes and penalties 486 319

Other 3,316 2,588

25,928 27,203

29. Guarantees and other financial commitments

The aggregate amounts o f outstanding financial guarantees, commitments, and other off-balance sheet items asat 31 December 2015 and 2014 are:

2015 2014M DL’000 M DL’000

Financial guarantees 76,739 -8 4 ,5 9 2

Financing commitments and other 53,204 60,060

129,943 144,652

33

i

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

29. Guarantees and other financial commitments (continued)

In the normal course of business, the Group issues guarantees and letters of credit on behalf of its customers. The credit risk on guarantees is similar to that arising from granting o f loans. In the event o f a claim on the Group as a result o f a customer's default on a guarantee these instruments also present a degree o f liquidity risk to the Group.

Financing commitments represent the Group’s commitments to grant loans and advances to customers. Financing commitments do not necessarily represent future cash requirements, since many o f these commitments will expire or terminate without being funded.

30. Capital commitments

There were no capital commitments as at 31 December 2015 and 2014.

31. Operating lease commitments

Where the Group is lessee, the future minimum lease payments under non-cancellable building and vehicles operating leases are as follows:

2015 2014M DL’000 M DL’000

No later than 1 year 3,172 915Later than 1 year and no later than 5 years 4,905 3,177Later than 5 years 2,374 1,180

10,451 5,272

32. Contingencies

As at 31 December 2015 and 2014 the Group is a defendant in a number of lawsuits arising out of normal corporate activities. In the opinion of Management and the Group’s legal department, the probability o f loss is remote.

33. Earnings per share

Ordinary shares Profit attributable to equity Basic earnings issued holders of the Parent per share

M DL’000 MDL

As at 31 December 2015 2,000,000 59,405 29.07As at 31 December 2014 _________ 2,000,000 36,574 18,18

Basic earnings per share are calculated by dividing net profit for the year attributable to ordinary equity holders by the weighted average number of ordinary shares issued during the year. As at 31 December 2015 and 2014 there were no dilutive equity instruments subscribed to by the Group.

34

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS For the Year Ended 31 December 2015

BC ENERGBANK SA

34. Fair value of financial instruments

Determination of fair value and fair value hierarchy

The Group uses the following hierarchy for determining and disclosing the fair value of financial instruments by valuation technique:Level 1: quoted (unadjusted) prices in active markets for identical assets or liabilities;Level 2: other techniques for which all inputs which have a significant effect on the recorded fair value are observable, either directly or indirectly; and Level 3: techniques which use inputs which have a significant effect on the recorded fair value that are not based on observable market data.

The following table shows an analysis o f financial instruments recorded at fair value by level o f the fair value hierarchy:2015 2014

Carryingvalue Level 1

Fairvalue

Carryingvalue Level 1Level 2 Level 3 value value Level 1 Level 2 Level 3

M DL’000 M DL’000 MDL’000 M DL’000 M DL’000 M DL’000 M DL’000 M DL’000 M DL’000

Financial assetsCash and balances with NBM 528,344Loans and advances to banks 356,409Investments held-to-maturity 271,970Loans and advances to customers 866,852

271,970

528,344356,409

832,503

528,344356,409271,970832,503

450,730220,942132,274

1,036,815

450,730220,942

132,2741,023,070

Financial liabilitiesDue to banks . . . . . 5 5 3 553

Other borrowings 188,196 188,196 - 188,196 200,853 200,853Due to customers 1,541,115 1,538,286 1,538,286 1,416,706 1,415,276

Fairvalue

MDL’000

450,730220,942132,274

1,023,070

553200,853

1,415,276

35

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

34. Fair value of financial instruments (continued)

(i) Loans and advances to banksLoans and advances to banks include inter-bank placements and loans. The fair value of floating rate placements and overnight deposits approximates their carrying amount. The estimated fair value o f fixed interest bearing placements is based on discounted cash flows using prevailing money-market interest rates for debts with similar credit risk and remaining maturity.

(ii) Held to maturity investmentsThe fair value of held to m aturity investm ents approxim ates the book value. Mainly rep resen t investm ents in securities issued by the National Bank of Moldova

(Hi) Loans and advances to customersLoans and advances are net o f provisions for impairment. The estimated fair value of loans and advances represents the discounted amount o f estimated future cash flows expected to be received. Expected cash flows are discounted at current market rates to determine fair value.

(iv) Liabilities, including due to other banks, due to customers and other borrowed fundsThe fair value of floating rate borrowings approximates their carrying amount. The estimated fair value o f fixed interest-bearing deposits and other borrowings without quoted market price is based on discounted cash flows using interest rates for new debts with similar remaining maturity.

36

BC ENERGBANK SANOTES TO THE CONSOLIDATED FINANCIAL STATEMENTSFor the Year Ended 31 December 2015

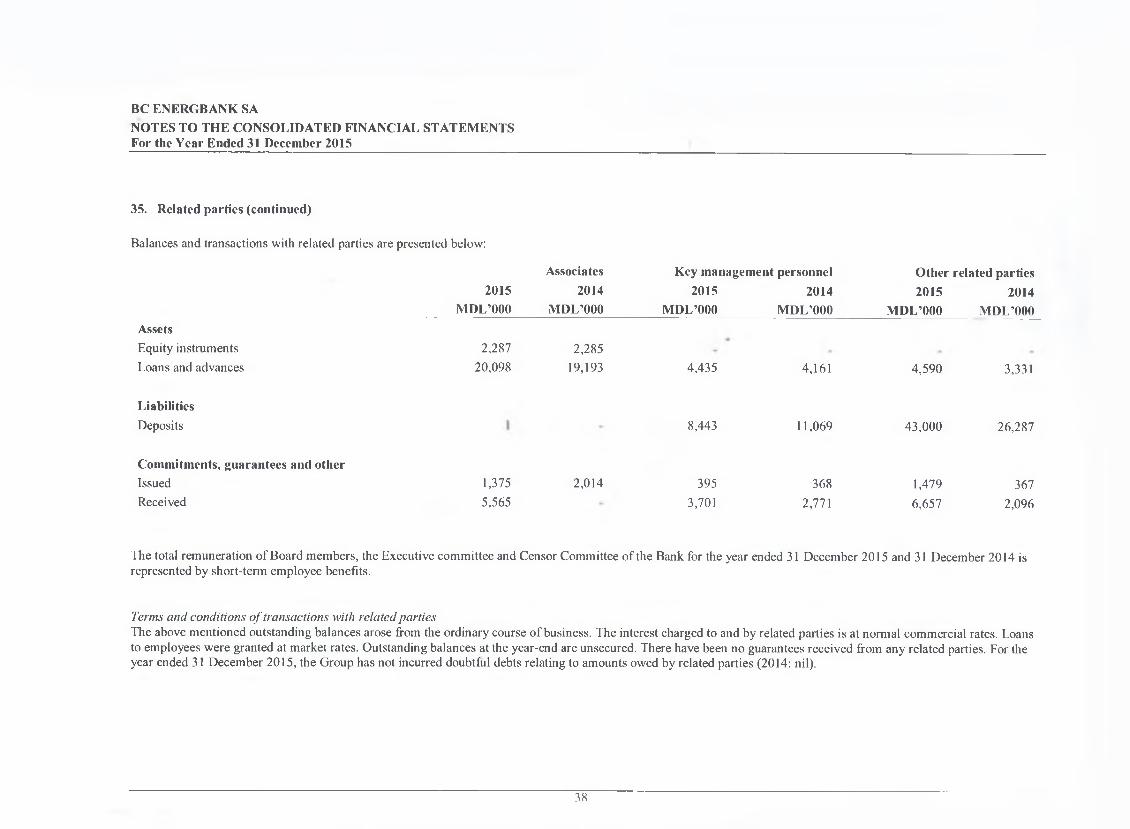

35. Related parties

During the year, a number of banking and non-banking transactions were entered into with related parties in the normal course of business. These include loans granting, deposit taking, trade finance, payment settlement, foreign currency transactions and acquisition of services and goods from related parties.