consolidated report & accounts 1 - euronext · ii – consolidated management report appendix...

TRANSCRIPT

2013FIRSTHALFRESULTS

CONSOLIDATED REPORT & ACCOUNTS

1ST Half 2015

R&A - 1st Half 2015

Index

INDEX

I – Consolidated Management Report

Message from the Chairman and CEO - Pedro Soares dos Santos 3

1. Sales Analysis 3

2. Results Analysis 4

3. Balance Sheet 5

4. Outlook for 2015

6

II – Consolidated Management Report Appendix

1. Sales Evolution 7

2. Stores Network 7

3. EBITDA Margin Breakdown 7

4. Financial Costs Breakdown 7

5. Working Capital 8

6. Net Debt 8

7. Definitions 8

8. Information Regarding Individual Financial Statements 8

III – Other Information 9

IV – Statement of the Board of Directors 11

V – Consolidated Financial Statements

1. Financial Statements 12

2. Notes to the Financial Statements 16

3. Auditor’s Report 26

R&A - 1st Half 2015 Consolidated Management Report

3

CONSOLIDATED MANAGEMENT REPORT

Message from the Chairman and CEO – Pedro Soares dos Santos

‘As we expected, the first half year results show the positive effects of the strategy being executed in Biedronka. The Company’s performance in the period validates the effectiveness of the measures being implemented, its capacity to reinforce the leadership in the market and its relevance for consumers, even in a context of uncertainty regarding food deflation. Both Pingo Doce and Recheio continued to outperform the market in Portugal. In Colombia, a new distribution centre is being finalised and we will start operations in the second region in the third quarter of this year. Reassured by the performance of our established businesses, we will continue implementing our plan and we will deliver our targets for the year.’

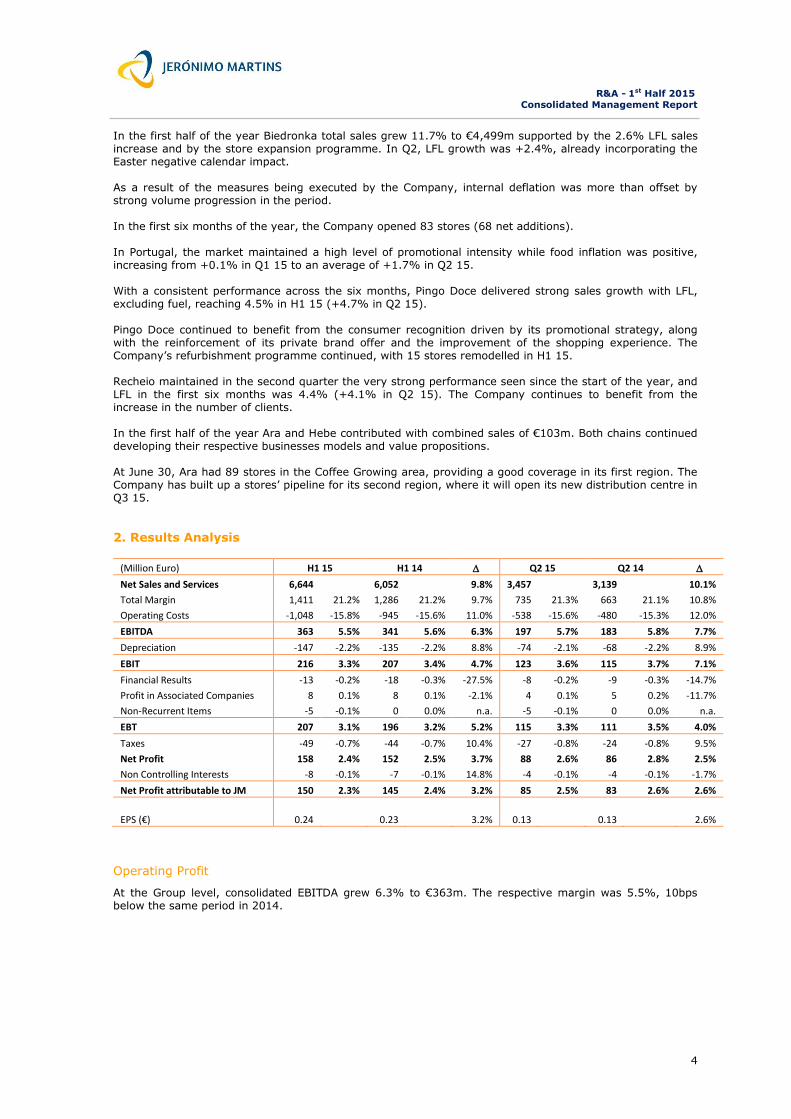

1. Sales Analysis

(Million Euro) H1 15 H1 14 Q2 15 Q2 14

%

total %

total Pln Euro %

total %

total Pln Euro

Biedronka 4,499 67.7% 4,029 66.6% 10.6% 11.7% 2,327 67.3% 2,076 66.1% 9.8% 12.1%

Pingo Doce 1,623 24.4% 1,556 25.7%

4.3% 850 24.6% 812 25.9%

4.7%

Recheio 393 5.9% 374 6.2%

5.0% 213 6.2% 201 6.4%

5.8%

Mkt. Repr. and Rest. Serv. 37 0.5% 36 0.6%

1.3% 18 0.5% 19 0.6%

-1.0%

Others & Cons. Adjustments 93 1.4% 57 0.9% n.a. 48 1.4% 31 1.0% n.a.

Total JM 6,644 100% 6,052 100% 9.8% 3,457 100% 3,139 100% 10.1%

In the first half of the year, consolidated sales increased 9.8% to €6,644m (+9.1% excluding the positive currency impact).

The performance in the period reflects the good sales progression in all banners driving Group LFL growth to reach 3.1%. In Poland, the competitive landscape maintained a strong focus on promotional activities and food deflation prevailed in the market, despite softening from -3.7% in Q1 15 to -2.1% in Q2 15.

I

R&A - 1st Half 2015 Consolidated Management Report

4

In the first half of the year Biedronka total sales grew 11.7% to €4,499m supported by the 2.6% LFL sales increase and by the store expansion programme. In Q2, LFL growth was +2.4%, already incorporating the Easter negative calendar impact. As a result of the measures being executed by the Company, internal deflation was more than offset by strong volume progression in the period. In the first six months of the year, the Company opened 83 stores (68 net additions). In Portugal, the market maintained a high level of promotional intensity while food inflation was positive, increasing from +0.1% in Q1 15 to an average of +1.7% in Q2 15. With a consistent performance across the six months, Pingo Doce delivered strong sales growth with LFL, excluding fuel, reaching 4.5% in H1 15 (+4.7% in Q2 15). Pingo Doce continued to benefit from the consumer recognition driven by its promotional strategy, along with the reinforcement of its private brand offer and the improvement of the shopping experience. The Company’s refurbishment programme continued, with 15 stores remodelled in H1 15. Recheio maintained in the second quarter the very strong performance seen since the start of the year, and LFL in the first six months was 4.4% (+4.1% in Q2 15). The Company continues to benefit from the increase in the number of clients. In the first half of the year Ara and Hebe contributed with combined sales of €103m. Both chains continued developing their respective businesses models and value propositions. At June 30, Ara had 89 stores in the Coffee Growing area, providing a good coverage in its first region. The Company has built up a stores’ pipeline for its second region, where it will open its new distribution centre in Q3 15.

2. Results Analysis

(Million Euro) H1 15 H1 14 Q2 15 Q2 14

Net Sales and Services 6,644

6,052

9.8% 3,457

3,139

10.1%

Total Margin 1,411 21.2% 1,286 21.2% 9.7% 735 21.3% 663 21.1% 10.8%

Operating Costs -1,048 -15.8% -945 -15.6% 11.0% -538 -15.6% -480 -15.3% 12.0%

EBITDA 363 5.5% 341 5.6% 6.3% 197 5.7% 183 5.8% 7.7%

Depreciation -147 -2.2% -135 -2.2% 8.8% -74 -2.1% -68 -2.2% 8.9%

EBIT 216 3.3% 207 3.4% 4.7% 123 3.6% 115 3.7% 7.1%

Financial Results -13 -0.2% -18 -0.3% -27.5% -8 -0.2% -9 -0.3% -14.7%

Profit in Associated Companies 8 0.1% 8 0.1% -2.1% 4 0.1% 5 0.2% -11.7%

Non-Recurrent Items -5 -0.1% 0 0.0% n.a. -5 -0.1% 0 0.0% n.a.

EBT 207 3.1% 196 3.2% 5.2% 115 3.3% 111 3.5% 4.0%

Taxes -49 -0.7% -44 -0.7% 10.4% -27 -0.8% -24 -0.8% 9.5%

Net Profit 158 2.4% 152 2.5% 3.7% 88 2.6% 86 2.8% 2.5%

Non Controlling Interests -8 -0.1% -7 -0.1% 14.8% -4 -0.1% -4 -0.1% -1.7%

Net Profit attributable to JM 150 2.3% 145 2.4% 3.2% 85 2.5% 83 2.6% 2.6%

EPS (€) 0.24 0.23 3.2% 0.13 0.13 2.6%

Operating Profit

At the Group level, consolidated EBITDA grew 6.3% to €363m. The respective margin was 5.5%, 10bps below the same period in 2014.

R&A - 1st Half 2015 Consolidated Management Report

5

Biedronka’s EBITDA, in the first six months, reached €305m, a growth of 8.6% on previous year (+8.6% in Q2 15). EBITDA margin stood at 6.8%, 20bps down on H1 14. The margin evolution reflected the strong food deflation together with the marketing investments made in the business. Pingo Doce delivered EBITDA of €77m, broadly in line with previous year. EBITDA margin was 20bps down on previous year, as the company focused in maintaining strong top line performance. To support its strong LFL growth, Recheio posted an EBITDA margin 10bps below previous year and delivered an EBITDA of €19m.

Financial Results

Financial charges for the Group were €13m, €5m below the same period last year due to lower average net debt and lower cost of debt.

Net Results

As a result of the solid operating performance, Net Profit attributable to Jerónimo Martins was €150m, 3.2% higher than in the prior year, already incorporating the start-up losses in Ara and Hebe of €29m at the EBITDA level, in the six months.

3. Balance Sheet

(Million Euro) H1 15 2014 H1 14 *

Net Goodwill 646 640 648

Net Fixed Assets 3,002 2,940 2,846

Total Working Capital -1,732 -1,778 -1,519

Others 110 111 114

Invested Capital 2,026 1,912 2,091

Total Borrowings 743 714 904

Leasings 0 1 3

Accrued Interest 6 4 8

Marketable Sec. & Bank Deposits -364 -446 -308

Net Debt 386 273 607

Non Controlling Interests 238 243 230

Share Capital 629 629 629

Reserves and Retained Earnings 773 767 625

Shareholders Funds 1,640 1,639 1,484

Gearing 23.5% 16.7% 40.9%

* Restated values - see note 2.3 of the Consolidated Financial Statements.

After the dividend payment of €154m in May, Net Debt for the Group was €386m and Gearing stood at 24%.

R&A - 1st Half 2015 Consolidated Management Report

6

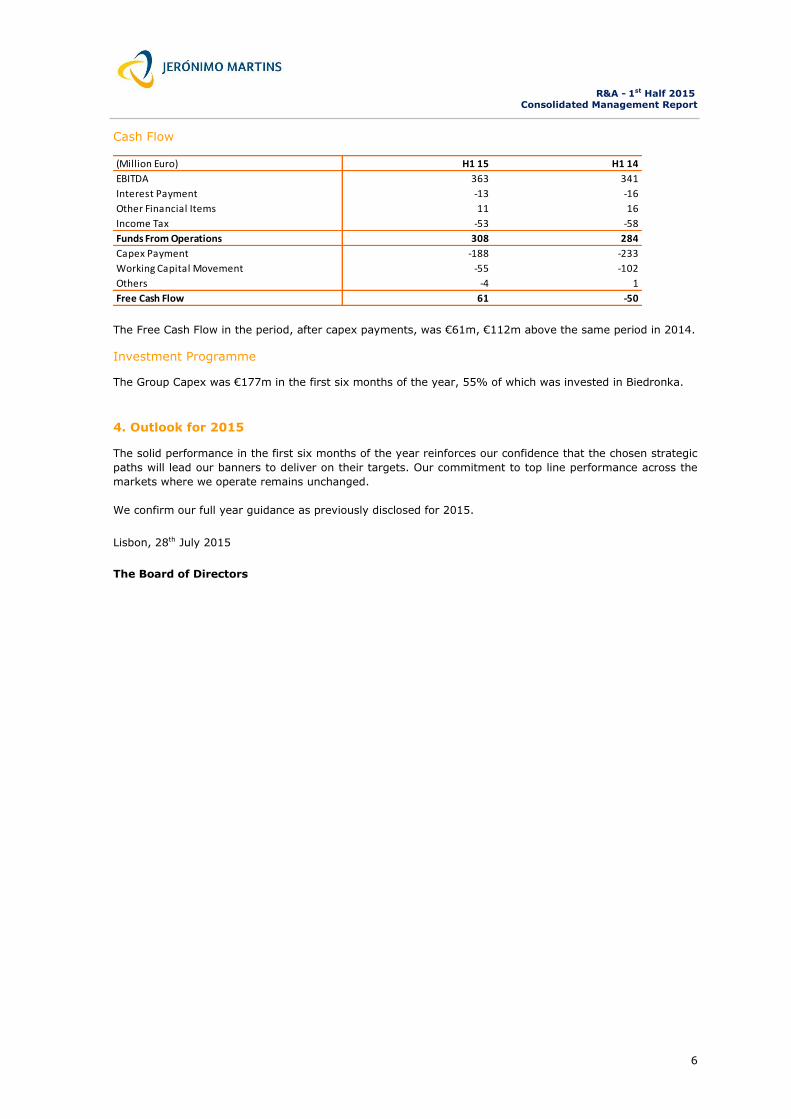

Cash Flow

(Million Euro) H1 15 H1 14

EBITDA 363 341

Interest Payment -13 -16

Other Financial Items 11 16

Income Tax -53 -58

Funds From Operations 308 284

Capex Payment -188 -233

Working Capital Movement -55 -102

Others -4 1

Free Cash Flow 61 -50

The Free Cash Flow in the period, after capex payments, was €61m, €112m above the same period in 2014.

Investment Programme

The Group Capex was €177m in the first six months of the year, 55% of which was invested in Biedronka.

4. Outlook for 2015

The solid performance in the first six months of the year reinforces our confidence that the chosen strategic

paths will lead our banners to deliver on their targets. Our commitment to top line performance across the

markets where we operate remains unchanged.

We confirm our full year guidance as previously disclosed for 2015.

Lisbon, 28th July 2015

The Board of Directors

R&A - 1st Half 2015

Consolidated Management Report Appendix

7

CONSOLIDATED MANAGEMENT REPORT APPENDIX

1. Sales Evolution

Q1 15 Q2 15 H1 15 Q1 15 Q2 15 H1 15

Biedronka

Euro 11.2% 12.1% 11.7%

PLN 11.4% 9.8% 10.6% 2.9% 2.4% 2.6%

Pingo Doce 3.9% 4.7% 4.3% 3.4% 4.2% 3.8%

Ex-Fuel 4.7% 5.2% 4.9% 4.2% 4.7% 4.5%

Recheio 4.1% 5.8% 5.0% 4.7% 4.1% 4.4%

Total Sales Growth LFL Sales Growth

2. Stores Network

Closings

Q1 15 Q2 15 H1 15 H1 15 H1 14

Biedronka 2,587 58 25 15 2,655 2,473

Pingo Doce 380 2 4 1 385 378

Recheio 41 0 0 0 41 41

Closings/

Remodellings

Q1 15 Q2 15 H1 15 H1 15 H1 14

Biedronka 1,649,889 40,870 17,991 1,214 1,707,535 1,567,382

Pingo Doce 460,863 1,252 4,540 500 466,155 459,113

Recheio 128,665 0 0 0 128,665 128,665

Network

NetworkNumber of Stores 2014

Openings

Sales Area (sqm) 2014Openings

3. EBITDA Margin Breakdown

H1 15 % total H1 14 % total

Biedronka 6.8% 84.0% 7.0% 82.2%

Pingo Doce 4.7% 21.1% 4.9% 22.5%

Recheio 4.8% 5.2% 4.9% 5.4%

Others & Cons. Adjustments n.a. -10.3% n.a. -10.0%

JM Consolidated 5.5% 100% 5.6% 100%

4. Financial Costs Breakdown

(Million Euro) H1 15 H1 14

Net Interest -12 -16

Exchange Differences 1 0

Others -2 -2

Financial Results -13 -18

II

R&A - 1st Half 2015

Consolidated Management Report Appendix

8

5. Working Capital

(Million Euro) H1 15 2014 H1 14

Inventories 648 578 600

in days of sales 18 17 18

Customers 56 49 54

in days of sales 2 1 2

Suppliers -2,088 -2,134 -1,961

in days of sales -57 -61 -59

Trade Working Capital -1,384 -1,507 -1,307

in days of sales -38 -43 -39

Others -348 -271 -212

Total Working Capital -1,732 -1,778 -1,519

in days of sales -47 -51 -45

6. Net Debt

(Million Euro) H1 15

Long Term Debt 334

as % of Total Borrowings 45.0%

Average Maturity (years) 3.0

Bond Loans 0

Other Debt 334

Short Term Debt 409

as % of Total Borrowings 55.0%

Total Borrowings 743

Average Maturity (years) 1.7

Leasings 0

Accrued Interest & Hedging 6

Marketable Securities & Bank Deposits -364

Net Debt 386

% Debt in Euros (Total Borrowings + Leasings) 30.3%

% Debt in Zlotys (Total Borrowings + Leasings) 58.5%

% Debt in Pesos (Total Borrowings + Leasings) 11.2% 7. Definitions

Like-for-like sales: sales made by stores that operated under the same conditions in the two periods. Excludes stores opened or closed in one of the two periods. Sales of stores that underwent profound remodelling are excluded for the remodelling period (store closure).

Gearing: Net Debt / Shareholder Funds.

8. Information Regarding Individual Financial Statements

In accordance with section b) of paragraph 3 of article 246 of the Portuguese Securities Code, the first half individual financial statements of Jerónimo Martins SGPS, S.A. will not be disclosed as they do not include additional relevant information, compared to the one presented in this report.

R&A - 1st Half 2015

Other Information

9

OTHER INFORMATION Disclosures required by sub-paras. a) and c) of no. 1 of Article 9 and no. 7 of Article 14 of Securities Market Commission (CMVM) regulation no. 5/2008 (with reference to

the first half of 2015)

1. Securities issued by the Company, Controlled or Controlling Companies or Companies in the same Group held by Company Officers

Board of Directors

Members of the Board of Directors

Held on

31.12.14

Increases

during the

period

Decreases

during the

period

Held on

30.06.15

Shares Bonds Shares Bonds Shares Bonds Shares Bonds

Pedro Manuel de Castro Soares dos Santos 274,805 - - - - - 274,805 -

Alan Johnson 30,075 - - - - - 30,075 -

Andrzej Szlezak - - - - - - - -

António Pedro de Carvalho Viana-Baptista - - - - - - - -

Artur Stefan Kirsten n.a. - - - - - - -

Clara Christina Streit n.a. - - - - - 800 -

Francisco Seixas da Costa - - - - - - - -

Hans Eggerstedt 19,700 - - - - - 19,700 -

Henrique Manuel da Silveira e Castro Soares dos Santos n.a. - - - - - 26,455 1 -

José Manuel da Silveira e Castro Soares dos Santos2 20,509 - - - - - n.a. -

Belonging to company in which is a Director 3 353,260,814 - - - - - n.a. -

Nicolaas Pronk - - - - - - - -

Belonging to company in which is a Director 4 31,464,750 - - - - - 31,464,750 -

Sérgio Tavares Rebelo - - - - - - - -

1 Of which 1,500 shares held by spouse. 2 Ceased his duties as Director on April 9, 2015. 3 Sociedade Francisco Manuel dos Santos, B.V. 4 Asteck, S.A.

Note: On April 9, 2015 the following members were appointed to the Board of Directors as Non-Executive Directors: Artur Stefan Kirsten, Clara Christina Streit and Henrique Manuel da Silveira e Castro Soares dos Santos.

Statutory Auditor

As at June 30th 2015, the Statutory Auditor PricewaterhouseCoopers & Associados, SROC, Lda., did not hold any shares and bonds of Jerónimo Martins, SGPS, S.A. and had not made any transactions in securities with Jerónimo Martins, SGPS, S.A..

III

R&A - 1st Half 2015

Other Information

10

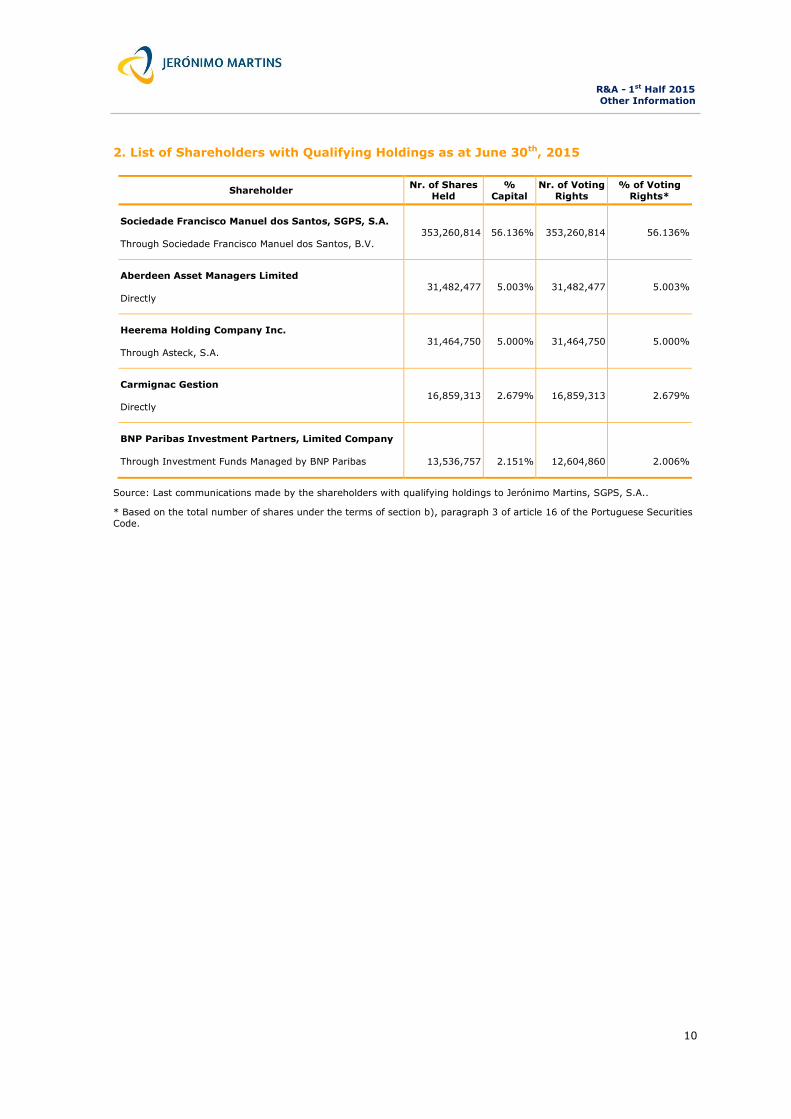

2. List of Shareholders with Qualifying Holdings as at June 30th, 2015

Shareholder Nr. of Shares

Held

%

Capital

Nr. of Voting

Rights

% of Voting

Rights*

Sociedade Francisco Manuel dos Santos, SGPS, S.A.

Through Sociedade Francisco Manuel dos Santos, B.V.

353,260,814 56.136% 353,260,814 56.136%

Aberdeen Asset Managers Limited

Directly

31,482,477 5.003% 31,482,477 5.003%

Heerema Holding Company Inc.

Through Asteck, S.A.

31,464,750 5.000% 31,464,750 5.000%

Carmignac Gestion

Directly

16,859,313 2.679% 16,859,313 2.679%

BNP Paribas Investment Partners, Limited Company

Through Investment Funds Managed by BNP Paribas

13,536,757

2.151%

12,604,860

2.006%

Source: Last communications made by the shareholders with qualifying holdings to Jerónimo Martins, SGPS, S.A..

* Based on the total number of shares under the terms of section b), paragraph 3 of article 16 of the Portuguese Securities

Code.

R&A - 1st Half 2015 Statement of the Board of Directors

11

STATEMENT OF THE BOARD OF DIRECTORS

Statement of the Board of Directors

Within the terms of paragraph c) n.º1 of article 246 of Portuguese Securities Code, we hereby inform you that to the best of our knowledge:

i) the information contained in the interim management report is a faithful statement of the

evolution of the businesses, of the performance and of the position of Jerónimo Martins, SGPS, S.A. and the companies included within the consolidation perimeter, and contains a description of the main risks and uncertainties which they face; and

ii) the information contained in the consolidated financial statements, as well as their annexes, was produced in compliance with the applicable accounting standards and gives a true and fair view of the assets and liabilities, the financial situation and the results of Jerónimo Martins, SGPS, S.A.

and the companies included in the consolidation perimeter.

Lisbon, 28th July 2015 Pedro Manuel de Castro Soares dos Santos (Chairman of the Board of Directors and Chief Executive Officer)

Alan Johnson (Member of the Board of Directors)

Andrzej Szlezak (Member of the Board of Directors)

António Pedro de Carvalho Viana-Baptista (Member of the Board of Directors and Member of the Audit Committee)

A. Stefan Kirsten (Member of the Board of Directors)

Clara Christina Streit (Member of the Board of Directors)

Francisco Seixas da Costa (Member of the Board of Directors)

Hans Eggerstedt (Member of the Board of Directors and Chairman of the Audit Committee)

Henrique Soares dos Santos (Member of the Board of Directors)

Nicolaas Pronk (Member of the Board of Directors)

Sérgio Tavares Rebelo (Member of the Board of Directors and Member of the Audit Committee)

IV

R&A - 1st Half 2015

Consolidated Financial Statements

12

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED INCOME STATEMENT BY FUNCTIONS

FOR JUNE 2015 AND 2014

Euro thousand

Notes 1st Half 2015

1st Half 2014

2nd Quarter 2015

2nd Quarter 2014

Sales and services rendered 3 6,643,998 6,051,713 3,456,824 3,139,255

Cost of sales 4 (5,232,736) (4,765,732) (2,721,822) (2,475,848)

Total margin 1,411,262 1,285,981 735,002 663,407

Distribution costs 4 (1,085,703) (973,115) (557,248) (494,888)

Administrative costs 4 (109,262) (106,308) (54,437) (53,349)

Exceptional operating profits/losses 4 (4,713) (493) (4,672) (218)

Operating profit 211,584 206,065 118,645 114,952

Net financial costs 5 (12,939) (17,837) (7,836) (9,189)

Gains in joint ventures and associates 9 7,924 8,095 4,483 5,080

Profit before taxes 206,569 196,323 115,292 110,843

Income tax 6 (48,988) (44,371) (26,800) (24,471)

Profit before non-controlling interests 157,581 151,952 88,492 86,372

Attributable to:

Non-controlling interests 8,071 7,031 3,759 3,824

Jerónimo Martins Shareholders 149,510 144,921 84,733 82,548

Basic and diluted earnings per share- Euros 14 0.2379 0.2306 0.1348 0.1314

To be read with the attached notes to the consolidated financial statements

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

Euro thousand

To be read with the attached notes to the consolidated financial statements

(*) Restated – See note 2.3

1st Half

2015

1st Half

2014 (*)

2nd Quarter

2015

2nd Quarter

2014 (*)

Net profit 157,581 151,952 88,492 86,372

Other comprehensive income:

Items that will not be reclassified to profit or loss

- - - -

Items that may be reclassified to profit or loss

Currency translation differences 25,120 (3,913) (13,129) (735)

Change in fair value of cash flow hedges 1,578 528 1,044 (532)

Change in fair value of hedging instruments on foreign

operations (14,680) 1,036

(4,716) 1,663

Change in fair value of available-for-sale financial

assets 68 50

(100) (74)

Related tax (841) (181) (1,296) (13)

11,245 (2,480) (18,197) 309

Other comprehensive income, net of income tax 11,245 (2,480) (18,197) 309

Total comprehensive income 168,826 149,472 70,295 86,681

Attributable to:

Non-controlling interests 8,350 7,415 3,911 3,923

Jerónimo Martins Shareholders 160,476 142,057 66,384 82,758

Total comprehensive income 168,826 149,472 70,295 86,681

V

R&A - 1st Half 2015

Consolidated Financial Statements

13

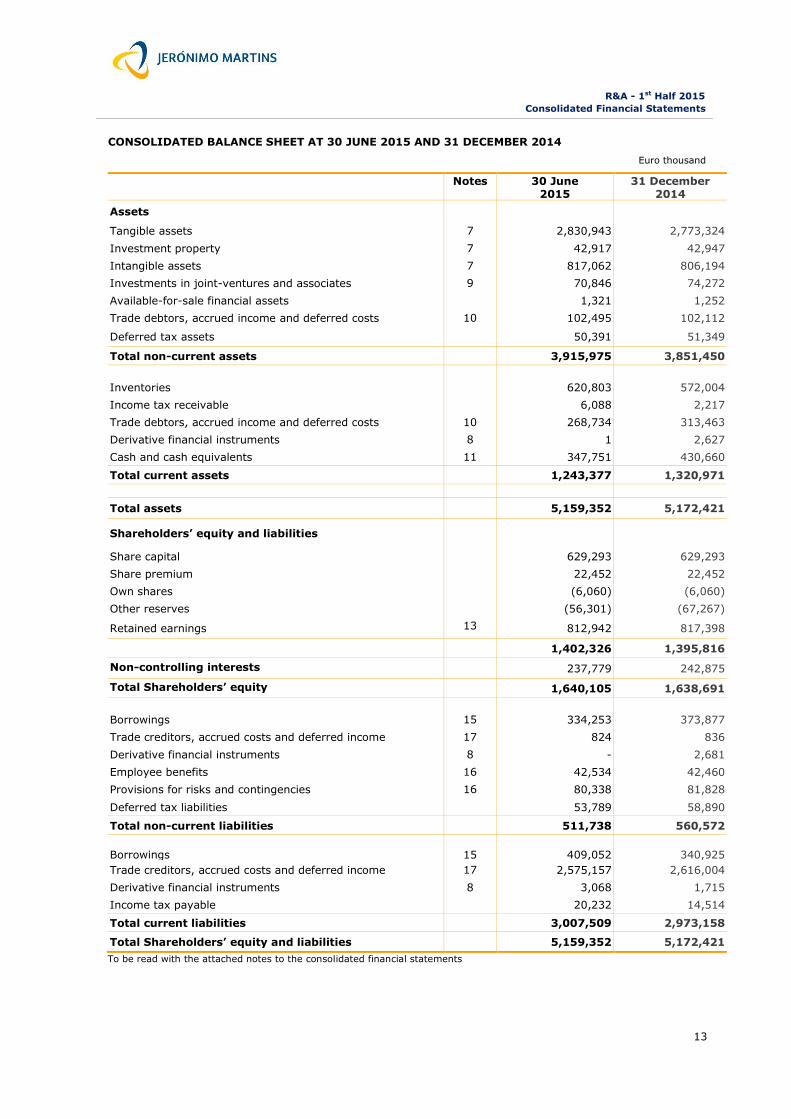

CONSOLIDATED BALANCE SHEET AT 30 JUNE 2015 AND 31 DECEMBER 2014

Euro thousand

Notes 30 June 2015

31 December 2014

Assets

Tangible assets 7 2,830,943 2,773,324

Investment property 7 42,917 42,947

Intangible assets 7 817,062 806,194

Investments in joint-ventures and associates 9 70,846 74,272

Available-for-sale financial assets 1,321 1,252

Trade debtors, accrued income and deferred costs 10 102,495 102,112

Deferred tax assets 50,391 51,349

Total non-current assets 3,915,975 3,851,450

Inventories 620,803 572,004

Income tax receivable 6,088 2,217

Trade debtors, accrued income and deferred costs 10 268,734 313,463

Derivative financial instruments 8 1 2,627

Cash and cash equivalents 11 347,751 430,660

Total current assets 1,243,377 1,320,971

Total assets 5,159,352 5,172,421

Shareholders’ equity and liabilities

Share capital 629,293 629,293

Share premium 22,452 22,452

Own shares (6,060) (6,060)

Other reserves (56,301) (67,267)

Retained earnings 13 812,942 817,398

1,402,326 1,395,816

Non-controlling interests 237,779 242,875

Total Shareholders’ equity 1,640,105 1,638,691

Borrowings 15 334,253 373,877

Trade creditors, accrued costs and deferred income 17 824 836

Derivative financial instruments 8 - 2,681

Employee benefits 16 42,534 42,460

Provisions for risks and contingencies 16 80,338 81,828

Deferred tax liabilities 53,789 58,890

Total non-current liabilities 511,738 560,572

Borrowings 15 409,052 340,925

Trade creditors, accrued costs and deferred income 17 2,575,157 2,616,004

Derivative financial instruments 8 3,068 1,715

Income tax payable 20,232 14,514

Total current liabilities 3,007,509 2,973,158

Total Shareholders’ equity and liabilities 5,159,352 5,172,421

To be read with the attached notes to the consolidated financial statements

R&A - 1st Half 2015

Consolidated Financial Statements

14

CONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

Euro thousand

Shareholders’ equity attributable to Shareholders of Jerónimo Martins, SGPS, S.A.

No

t

es

Share

capital

Share

premium

Own

shares

Other reserves

Retained

earnings Total

Non-

controlling

interests

Shareholders’

equity Cash flow

hedge

Available-for-

sale financial

assets

Currency

translation

reserves

Balance Sheet as at 1

January 2014 (*) 629,293 22,452 (6,060) (2,453) (1,251) (48,111) 709,661 1,303,531 235,835 1,539,366

Equity changes in the 1st

Half of 2014

Currency translation

differences 1 (3,915) (3,914) (3,914)

Change in fair value of cash

flow hedging (36) (36) 384 348

Change in fair value of

hedging instruments on foreign operations

1,036 1,036 1,036

Change in fair value of

available-for-sale financial investments

1,300 (1,250) 50 50

Other comprehensive

income - - - (35) 1,300 (2,879) (1,250) (2,864) 384 (2,480)

Net profit 144,921 144,921 7,031 151,952

Total comprehensive

income - - - (35) 1,300 (2,879) 143,671 142,057 7,415 149,472

Dividends (191,672) (191,672) (13,121) (204,793)

Balance Sheet as at 30

June 2014 (*) 629,293 22,452 (6,060) (2,488) 49 (50,990) 661,660 1,253,916 230,129 1,484,045

Balance Sheet as at 1

January 2015 629,293 22,452 (6,060) (2,548) (157) (64,562) 817,398 1,395,816 242,875 1,638,691

Equity changes in the 1st

Half of 2015

Currency translation

differences (38) 24,656 24,618 24,618

Change in fair value of cash flow hedging

975 975 279 1,254

Change in fair value of

hedging instruments on

foreign operations

(14,680) (14,680) (14,680)

Change in fair value of

available-for-sale financial

investments

53 53 53

Other comprehensive income

937 53 9,976 10,966 279 11,245

Net profit 149,510 149,510 8,071 157,581

Total comprehensive income

937 53 9,976 149,510 160,476 8,350 168,826

Dividends 13 (153,966) (153,966) (13,446) (167,412)

Balance Sheet as at 30

June 2015 629,293 22,452 (6,060) (1,611) (104) (54,586) 812,942 1,402,326 237,779 1,640,105

To be read with the attached notes to the consolidated financial statements

(*) Restated – see note 2.3

R&A - 1st Half 2015

Consolidated Financial Statements

15

CONSOLIDATED CASH FLOW STATEMENT FOR JUNE 2015 AND 2014

Euro thousand

Notes 2015 2014

Operating Activities

Cash received from Customers 7,485,487 6,821,511

Cash paid to suppliers (6,656,561) (6,109,332)

Cash paid to employees (524,375) (472,123)

Cash generated from operations 12 304,551 240,056

Interest paid (14,264) (17,165)

Income taxes paid (52,899) (57,980)

Cash Flow from operating activities 237,388 164,911

Investment activities

Disposals of tangible assets 1,705 2,239

Disposals of available-for-sale financial assets - 3,382

Interest received 953 1,118

Dividends received 11,373 16,264

Acquisition of tangible assets (179,879) (225,654)

Acquisition of financial investments and Investment property (2) -

Acquisition of intangible assets (9,508) (12,984)

Cash flow from investment activities (175,358) (215,635)

Financing activities

Received from loans 116,002 336,494

Reimbursement of loans (95,100) (136,082)

Dividends paid 13 (167,412) (204,793)

Cash Flow from financing activities (146,510) (4,381)

Net changes in cash and cash equivalents (84,480) (55,105)

Cash and cash equivalents changes

Cash and cash equivalents at the beginning of 1st Half 430,660 371,671

Net changes in cash and cash equivalents (84,480) (55,105)

Effect of currency translation differences 1,571 (4,630)

Cash and cash equivalents at the end of 1st Half 11 347,751 311,936

To be read with the attached notes to the consolidated financial statements

CONSOLIDATED CASH FLOW STATEMENT FOR THE INTERIM PERIOD

Euro thousand

1st Half 2015

1st Half 2014

2nd Quarter 2015

2nd Quarter 2014

Cash Flow from operating activities 237,388 164,911 177,877 148,627

Cash Flow from investment activities (175,358) (215,635) (81,630) (77,591)

Cash Flow from financing activities (146,510) (4,381) (227,296) (125,936)

Cash and cash equivalents changes (84,480) (55,105) (131,049) (54,900)

R&A – 1st Half 2015

Notes to the Consolidated Financial Statements

16

Index to the Notes to the Consolidated Financial Statements Page

1 Activity ................................................................................................................................................ 17

2 Accounting policies ................................................................................................................................ 17

3 Segments reporting ............................................................................................................................... 19

4 Total margin and operating costs ............................................................................................................ 20

5 Net financial costs ................................................................................................................................. 21

6 Income tax recognised in the income statement ........................................................................................ 21

7 Fixed assets, intangible assets and investment property ............................................................................ 21

8 Derivative financial instruments .............................................................................................................. 22

9 Investments in joint ventures and associates ............................................................................................ 22

10 Trade debtors, accrued income and deferred costs .................................................................................... 22

11 Cash and cash equivalents ..................................................................................................................... 23

12 Cash generated from operations ............................................................................................................. 23

13 Dividends ............................................................................................................................................. 23

14 Basic and diluted earnings per share ....................................................................................................... 23

15 Borrowings ........................................................................................................................................... 23

16 Provisions and employee benefits ............................................................................................................ 24

17 Trade creditors, accrued costs and deferred income ................................................................................... 24

18 Contingencies ....................................................................................................................................... 25

19 Related parties...................................................................................................................................... 25

20 Events after the balance sheet date ......................................................................................................... 25

R&A – 1st Half 2015

Notes to the Consolidated Financial Statements

17

1 Activity

Jerónimo Martins, SGPS, S.A. (JMH), is the parent Company of Jerónimo Martins Group (Group) and has its head office in Lisbon.

Jerónimo Martins Group is devoted to the production, distribution and sale of food and other fast moving consumer goods products. The Group operates in Portugal, Poland and Colombia.

Head Office: Rua Actor António Silva, n.º 7, 1649-033 Lisboa

Share Capital: 629,293,220 euros

Registered at the Commercial Registry Office of Lisbon and Tax Number: 500 100 144

JMH has been listed on Euronext Lisbon since 1989.

The Board of Directors approved these consolidated financial statements on 28th July 2015.

2 Accounting policies

All amounts are shown in thousand euros (EUR thousand) unless otherwise stated.

The amounts presented for quarters, and the corresponding changes are not audited.

The JMH consolidated financial statements were prepared in accordance with the interim financial reporting standard (IAS 34), and all other International Financial Reporting Standards (IFRS) issued by International Accounting Standards Board (IASB) and with the interpretations of the International Financial Reporting Interpretations Committee (IFRIC) as adopted by the European Union.

The consolidated financial statements were prepared in accordance with the same standards and accounting policies adopted by the Group in the preparation of the annual financial statements, including an explanation of the events and relevant changes for the understanding of variations in the financial position and Group performance since the last annual report. Thus, some of the notes from the 2014 annual report are omitted because no changes occurred or they are not materially relevant for the understanding of the interim financial statements.

As mentioned in the Consolidated Financial Statements chapter of the 2014 Annual Report, point 30 - Financial risks, the Company, as a result of its normal activity, is exposed to several risks which are monitored and mitigated throughout the year. During the first six months of 2015, there was no material changes in addition to the notes detailed below, that could significantly change the assessment of the risks that the group is exposed to.

2.1 New standards, amendments and interpretations adopted by the Group

In 2014, the EU issued the following Regulations, which were adopted by the Group from January 1st 2015:

EU Regulation IASB Standard or IFRIC Interpretation

endorsed by EU

Issued in Mandatory for

financial years

beginning on or after

Regulation no. 1361/2014

Annual Improvements to IFRS’s 2011–2013 Cycle: IFRS 1

First-time Adoption of IFRS, IFRS 3 Business Combinations, IFRS 13 Fair Value Measurement and IAS 40 Investment

Property (Amendment)

December 2013 January 1, 2015

The Group adopted the new improvements, with no significant impact on the Consolidated Financial Statements.

2.2 New standards, amendments and interpretations endorsed by EU but not effective for the financial year beginning 1 January 2015 and not early adopted

The EU adopted several improvements to IFRS’s, issued by the IASB and Interpretations issued by the IFRIC:

EU Regulation IASB Standard or IFRIC Interpretation

endorsed by EU

Issued in Mandatory for

financial years

beginning on or after

Regulation no. 28/2015

Annual Improvements to IFRS’s 2010–2012 Cycle: IFRS 2 Share-Based Payment, IFRS 3 Business Combinations, IFRS

8 Operating Segments, IFRS 13 Fair Value Measurement,

IAS 16 Property, Plant and Equipment, IAS 24 Related Party

Disclosures and IAS 38 Intangible Assets (Amendment)

December 2013 February 1, 2015

Regulation no. 29/2015 IAS 19 Employee Benefits: Defined Benefit Plans - Employee

Contributions (Amendment) November 2013 February 1, 2015

These amendments to standards are effective for annual periods beginning on or after February 1, 2015, and have not been applied in preparing these consolidated financial statements. None of these amendments is expected to have a significant impact on the Group’s Consolidated Financial Statements.

R&A – 1st Half 2015

Notes to the Consolidated Financial Statements

18

2.3 Restatement of financial statements (change of accounting policies)

The Group has decided to adopt the historical cost for land (classified as tangible assets) in the financial statements prepared as at December 31, 2014, with restatement of the opening balances at January 1, 2014 and January 1, 2013. In accordance with IAS 8, the effects of the change in the accounting policy were applied retrospectively. There are no impacts on the Income Statement for the first six months of 2014. The Balance Sheet opening and closing balances for the year 2014, Statement of Comprehensive Income and Statement of Changes in Shareholders’ Equity were impacted as follows:

CONSOLIDATED BALANCE SHEET

30 June 2014

Published

Change of accounting

policies Restated

Assets

Tangible assets 2,811,908 (129,875) 2,682,033

Investment property 44,087 - 44,087

Intangible assets 812,567 - 812,567

Investments in joint ventures and associates 73,285 (2,897) 70,388

Other non-current assets 140,525 - 140,525

Total non-current assets 3,882,372 (132,772) 3,749,600

Inventories 594,167 - 594,167

Other current assets 294,257 - 294,257

Cash and cash equivalents 311,936 - 311,936

Total current assets 1,200,360 - 1,200,360

Total assets 5,082,732 (132,772) 4,949,960

Shareholders’ equity and liabilities

Attributable to Jerónimo Martins Shareholders 1,333,029 (79,113) 1,253,916

Non-controlling interests 260,898 (30,769) 230,129

Total shareholders’ equity 1,593,927 (109,882) 1,484,045

Borrowings 609,550 - 609,550

Deferred tax liabilities 80,288 (22,890) 57,398

Other non-current liabilities 120,409 - 120,409

Total non-current liabilities 810,247 (22,890) 787,357

Borrowings 297,228 - 297,228

Other current liabilities 2,381,330 - 2,381,330

Total current liabilities 2,678,558 - 2,678,558

Total shareholders’ equity and liabilities 5,082,732 (132,772) 4,949,960

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

30 June 2014

Published

Change of

accounting

policies

Restated

Net profit 151,952 - 151,952

Other comprehensive income:

Items that will not be reclassified to profit or loss

- - -

Items that may be reclassified to profit or loss

Currency translation differences (3,929) 16 (3,913)

Change in fair value of cash flow hedging 528 - 528

Change in fair value of hedging instruments on foreign operations 1,036 - 1,036

Change in fair value of available-for-sale financial assets 50 - 50

Related tax (179) (2) (181)

(2,494) 14 (2,480)

Other comprehensive income, net of income taxes (2,494) 14 (2,480)

Total comprehensive income 149,458 14 149,472

Attributable to:

Non-controlling interests 7,415 - 7,415

Jerónimo Martins Shareholders 142,043 14 142,057

Total comprehensive income 149,458 14 149,472

R&A – 1st Half 2015

Notes to the Consolidated Financial Statements

19

CONSOLIDATED STATEMENT OF CHANGES IN SHAREHOLDERS’ EQUITY

Shareholders’ equity attributable to Shareholders of Jerónimo Martins, SGPS, S.A.

Share

capital

Share

premium

Own

shares

Fair value and other reserves

Retained

earnings Total

Non-

controlling interests

Shareholders’

equity

Land revaluation

Cash

flow hedge

Available-

for-sale financial

assets

Adj. in

joint ventures

and

assoc.

Currency translation

reserves

Balance Sheet as at 1 January 2014 - Published

629,293 22,452 (6,060) 76,230 (2,453) (1,251) 2,897 (48,111) 709,661 1,382,658 266,604 1,649,262

Change of accounting policies - - - (76,230) - - (2,897) - - (79,127) (30,769) (109,896)

Balance Sheet at at 1 January 2014 - Restated

629,293 22,452 (6,060) - (2,453) (1,251) - (48,111) 709,661 1,303,531 235,835 1,539,366

Comprehensive income

restated - - - - (35) 1,300 - (2,879) 143,671 142,057 7,415 149,472

Dividends (191,672) (191,672) (13,121) (204,793)

Balance Sheet as at 30 June 2014 - Restated

629,293 22,452 (6,060) - (2,488) 49 - (50,990) 661,660 1,253,916 230,129 1,484,045

2.4 Transactions in foreign currencies

Transactions in foreign currencies are translated into Euros at the exchange rate prevailing on the transaction date.

On the balance sheet date, monetary assets and liabilities expressed in foreign currencies are translated at the exchange rate prevailing on that date and exchange differences arising from this conversion are recognised in the income statement. When qualifying as hedges on investments in foreign subsidiaries the exchange differences are deferred in equity.

The main exchange rates applied on the balance sheet date are as follows:

3 Segments reporting

Segment information is presented in accordance with internal reporting to Management. Based on this report, the Management evaluates the performance of each segment and allocates the available resources.

Management monitors the performance of the business based on a geographical and business perspective. In accordance with this, the segments are defined as Portugal Retail, Portugal Cash & Carry and Poland Retail. Apart from these there are also other businesses but due to their low materiality are not reported separately.

Business segments:

Portugal Retail: comprises the business unit of JMR (Pingo Doce supermarkets);

Portugal Cash & Carry: includes the wholesale business unit Recheio;

Poland Retail: the business unit with the brand Biedronka;

Others, eliminations and adjustments: includes i) the business units with reduced materiality (Marketing Services and Representations, Restaurants in Portugal, Health and Beauty Retail in Poland, retail business in Colombia); ii) the Holding companies; and iii) the Group’s consolidation adjustments.

Management evaluates the performance of segments based on the Earnings Before Interest and Taxes (EBIT). This indicator excludes the effects of exceptional operating profits/losses.

Euro foreign exchange reference rates

(foreign exchange units per 1 Euro)

Rate on

30 June

2015

Average rate for

the half year

Polish Zloty (PLN) 4.1911 4.1356

Swiss Franc (CHF) 1.0413 -

Colombian Peso (COP) 2,892.4800 2,764.0700

R&A – 1st Half 2015

Notes to the Consolidated Financial Statements

20

Detailed Information by Business Segments at June 2015 and 2014

Portugal Retail

Portugal Cash & Carry

Poland Retail Others, eliminations

and adjustments Total JM Consolidated

2015 2014 2015 2014 2015 2014 2015 2014 2015 2014

Net sales and services 1,776,493 1,706,767 392,847 374,113 4,499,036 4,029,084 (24,378) (58,251) 6,643,998 6,051,713

Inter-segments 150,226 146,919 3,028 903 765 723 (154,019) (148,545) - -

External customers 1,626,267 1,559,848 389,819 373,210 4,498,271 4,028,361 129,641 90,294 6,643,998 6,051,713

Operational cash flow (EBITDA) 76,695 76,665 18,864 18,313 304,906 280,665 (37,378) (34,208) 363,087 341,435

Depreciations and amortisations (47,359) (49,042) (5,830) (5,783) (86,793) (74,609) (6,808) (5,443) (146,790) (134,877)

Operational result (EBIT) 29,336 27,623 13,034 12,530 218,113 206,056 (44,186) (39,651) 216,297 206,558

Exceptional operating profits/losses (4,713) (493)

Financial results and gains in

investments (5,015) (9,742)

Income tax (48,988) (44,371)

Net result attributable to JM 149,510 144,921

Total assets (1) 1,685,164 1,656,090 350,645 330,131 2,755,314 2,826,930 368,229 359,270 5,159,352 5,172,421

Total liabilities (1) 1,198,779 1,158,612 308,254 281,931 2,115,802 2,100,836 (103,588) (7,649) 3,519,247 3,533,730

Investments in fixed assets 43,156 10,676 10,763 5,343 98,142 141,215 24,940 15,080 177,001 172,314

(1) The comparative report is 31th December of 2014

Reconciliation between EBIT and Operational Result

June 2015 June 2014

EBIT 216,297 206,558

Non recurrent results (4,713) (493)

Operational Result 211,584 206,065

4 Total margin and operating costs

June 2015 June 2014

Net sales and services 6,643,998 6,051,713

Net cost of products sold (5,215,211) (4,753,145)

Net cash discount and interest paid to suppliers (3,877) (2,734)

Electronic payment commissions (9,573) (6,579)

Other supplementary costs (4,075) (3,274)

Cost of sales (5,232,736) (4,765,732)

Total margin 1,411,262 1,285,981

Supplies and services (244,093) (225,349)

Advertising costs (36,617) (29,586)

Rents (164,622) (148,456)

Staff costs (523,819) (463,605)

Amortization (145,686) (133,742)

Profit/loss with tangible and intangible assets (903) (1,113)

Transportation costs (72,605) (73,069)

Other operational profit/loss (6,620) (4,503)

Distribution and administrative costs (1,194,965) (1,079,423)

Legal contingencies (162) -

Losses from organizational restructuring programmes (4,753) (469)

Assets write-offs and gains/losses in sale of tangible assets (8) (24)

Others 210 -

Exceptional operating profits/losses (4,713) (493)

Operating profit 211,584 206,065

R&A – 1st Half 2015

Notes to the Consolidated Financial Statements

21

5 Net financial costs

June 2015 June 2014

Interest expense (13,164) (16,994)

Interest received 1,080 1,141

Dividends 23 23

Net foreign exchange 1,063 (85)

Other financial costs and gains (1,942) (1,926)

Fair value of financial investments held for trade:

Derivative instruments (note 8) 1 4

(12,939) (17,837)

The interest expense heading includes the interest regarding loans measured at amortized cost, as well as interest on fair value and cash flow hedging instruments (note 8).

Other financial costs and gains include costs with debt issued by the Group.

6 Income tax recognised in the income statement

June 2015 June 2014

Current income tax

Current tax of the year (55,048) (43,715)

Adjustment to prior year estimation 356 1,167

(54,692) (42,548)

Deferred tax

Temporary differences created and reversed 5,392 (1,933)

Change to the recoverable amount of tax losses and temporary differences

from previous years (405) (606)

4,987 (2,539)

Other gains/losses related to taxes

Impact of changes in estimates for tax litigations 717 716

717 716

Total income tax (48,988) (44,371)

Income tax expense is recognised based on the weighted average annual income tax rate expected for the year 2015.

In 2015 the income tax rate for the companies operating in Portugal was reduced to 21% (23% in 2014). The estimation includes the effect of 1.5% as municipal surcharge and a state tax rate of 3% and 5% for tax profits over EUR 1,500 thousand and EUR 7,500 thousand, respectively.

7 Fixed assets, intangible assets and investment property

Tangible assets

Investment

property

Intangible

assets Total

Net value at 31 December 2014 2,773,324 42,947 806,194 3,622,465

Foreign exchange differences 31,847 - 8,883 40,730

Increases 167,493 2 9,508 177,003

Disposals and write-offs (2,316) - (90) (2,406)

Transfers 1 - (1) -

Depreciation and impairment losses (139,406) - (7,432) (146,838)

Transfers to/from investment properties - - - -

Fair value changes - (32) - (32)

Net value at 30 June 2015 2,830,943 42,917 817,062 3,690,922

As a consequence of currency translation adjustment of the assets in the Group’s businesses reported in foreign currency, the net amount of tangible and intangible assets increased by EUR 40.730 thousand, which includes an increase of EUR 6,056 thousand related to Goodwill from business in Poland.

The difference to total of amortisations stated in note 4, relates mainly to the production activities that were attributable to the cost of the goods sold.

R&A – 1st Half 2015

Notes to the Consolidated Financial Statements

22

8 Derivative financial instruments

Notional

June 2015 Notional

December 2014

Assets Liabilities Assets Liabilities

Current Non-

current Current

Non-

current Current

Non-

current Current

Non-

current

Derivatives held for trading

Currency forwards (PLN) 22.6million

PLN 1 - - - - - - - -

Cash flow hedging derivatives

Interest rate swap (EUR) 225 million

EUR - - 994 -

225 million

EUR - - 1,715 -

Interest rate swap (PLN) 500 million

PLN - - 2,074 - 500 million

PLN - - - 2,681

Investments in foreign entities

hedging derivatives

Currency forwards (PLN) - - - - 600 million

PLN 2,627 - - -

Total derivatives held for trading 1 - - - - - - -

Total hedging derivatives - - 3,068 - 2,627 - 1,715 2,681

Total assets/liabilities derivatives 1 - 3,068 - 2,627 - 1,715 2,681

In June 2015 the values shown include interest receivable or payable related with these financial instruments that are due. The net payable amount is EUR 626 thousand.

9 Investments in joint ventures and associates

During the 1st half of 2015, the movement under this heading was as follows:

Joint ventures Associates Total

Balance at 1 January 73,537 735 74,272

Equity method:

Net result 7,929 (5) 7,924

Dividends and other income received (11,350) - (11,350)

Other comprehensive income - - -

Balance at 30 June 70,116 730 70,846

10 Trade debtors, accrued income and deferred costs

June 2015 December 2014

Non-current

Other debtors 79,899 79,131

Collateral deposits associated to financial debt 19,367 19,367

Deferred costs 3,229 3,614

102,495 102,112

Current

Commercial customers 56,756 50,868

Other debtors 86,757 97,649

Other taxes receivable 8,291 16,011

Accrued income and deferred costs 116,930 148,935

268,734 313,463

Non-current debtors are mainly related to additional tax liquidation as well as pre-paid tax, which the Group has

already contested and made a legal claim for reimbursement.

The debtor’s amount is registered at the recoverable value. The Group constitutes provisions for impairment losses whenever there are signs of uncollectable amounts.

R&A – 1st Half 2015

Notes to the Consolidated Financial Statements

23

11 Cash and cash equivalents

June 2015 December 2014

Bank deposits 226,689 171,790

Short-term investments 117,464 255,043

Cash and cash equivalents 3,598 3,827

347,751 430,660

12 Cash generated from operations

June 2015 June 2014

Net results 149,510 144,921

Adjustments for:

Non-controlling interests 8,071 7,031

Income tax 48,988 44,371

Depreciations and amortisations 146,790 134,877

Provisions and other operational gains and losses 4,559 450

Net financial costs 12,939 17,837

Profit/ Losses in associated companies (7,924) (8,095)

Profit/ Losses on tangible and intangible assets 700 581

363,633 341,973

Changes in working capital:

Inventories (42,119) (18,496)

Trade debtors, accrued income and deferred costs (7,804) (6,650)

Trade creditors, accrued costs and deferred income (9,159) (76,771)

304,551 240,056

13 Dividends

Dividends distributed in 2015 in the amount of EUR 167,412 thousand, include an amount of EUR 153,962 thousand paid to JMH Shareholders, and an amount of EUR 13,446 thousand paid to non-controlling interests in the Group companies.

14 Basic and diluted earnings per share

Basic net results per share are calculated based on the net profit of EUR 149,510 thousand (2014: profit of EUR 144,921 thousand) and on the weighted average outstanding ordinary shares numbering 628,434,220 (2014: 628,434,220).

June 2015 June 2014

Ordinary shares issued at the beginning of the year 629,293,220 629,293,220

Own shares at the beginning of the year (859,000) (859,000)

Weighted average number of ordinary shares 628,434,220 628,434,220

Diluted net results of the year attributable to ordinary shares 149,510 144,921

Basic and diluted earnings per share – Euros 0.2379 0.2306

15 Borrowings

JM Nieruchomosci - Sp. Komandytowo-akcyjna contracted a loan on a total amount of PLN 415.000 thousand with maturity in 2020.

R&A – 1st Half 2015

Notes to the Consolidated Financial Statements

24

15.1 Current and non-current loans

June 2015 December 2014

Non-current loans

Bank loans 334,101 373,651

Financial lease liabilities 152 226

334,253 373,877

Current loans

Bank overdrafts 8,599 58,327

Bank loans 175,172 56,544

Bond loans 225,000 225,000

Financial lease liabilities 281 1,054

409,052 340,925

Compared to the report as at 31 December 2014 (note 19) there are no relevant changes in the Group’s average financing rate.

15.2 Financial debt

As the Group contracted several foreign exchange rate risk and interest risk hedging operations, as well as short-term investments, the net consolidated financial debt as at 30 June is as follows:

June 2015 December 2014

Non-current loans (note 15.1) 334,253 373,877

Current loans (note 15.1) 409,052 340,925

Derivative financial instruments (note 8) 3,067 1,769

Interest on accruals and deferrals 3,108 2,622

Bank deposits (note 11) (226,689) (171,790)

Short-term investments (note 11) (117,464) (255,043)

Collateral deposits (note 10) (19,367) (19,367)

385,960 272,993

16 Provisions and employee benefits

Risks and

contingencies Employee benefits

Balance at 1 January 81,828 42,460

Set up, reinforced and transfers 2,786 1,582

Unused and reversed (1,076) -

Foreign exchange difference 17 -

Used (3,217) (1,508)

Balance at 30 June 80,338 42,534

17 Trade creditors, accrued costs and deferred income

June 2015 December 2014

Non-current

Accrued costs and deferred income 824 836

824 836

Current

Other commercial creditors 2,121,542 2,182,406

Other non-commercial creditors 162,240 175,726

Other taxes payables 86,593 79,456

Accrued costs and deferred income 204,782 178,416

2,575,157 2,616,004

R&A – 1st Half 2015

Notes to the Consolidated Financial Statements

25

18 Contingencies

Following the contingencies mentioned in the 2014 Annual Report, changes occurred on the headings f) and i):

f) The Portuguese Tax Authorities carried out some corrections of VAT rates applied to certain goods sold by some Group companies. With these corrections the total amount of assessments for the years 2005 to 2012 in Pingo Doce, Feira Nova and Recheio SGPS amounted to EUR 1,814 thousand, EUR 1,300 thousand and EUR 551 thousand, respectively. The Board of Directors believes that the Tax Authorities have no grounds to request this

payment and these assessments have been challenged;

i) Sociedade Ponto Verde (SPV) claimed through a judicial proceeding against Pingo Doce, in September 2014, an amount of EUR 3,397 thousand (including outstanding interest), related to the Management of the secondary and tertiary packaging waste system. Pingo Doce contested considering that SPV does not manage that kind of waste and therefore no amount is due. The Civil Court, having the same understanding of Pingo Doce, declared itself materially incompetent to decide the case, saying that it should be judged by the administrative courts. SPV filed an appeal to the Court of Appeal. The Court of Appeal ruled in favor of SPV and the case returned to the Civil Court, where the procedure stands by.

19 Related parties

56.14% of the Group is owned by the Sociedade Francisco Manuel dos Santos, and no transactions occurred between this Company and any other company of the Group in the first half of 2015, neither were there any amounts payable or receivable between them on June 30th 2015.

Balances and transactions of Group companies with related parties are as follows:

Sales and services rendered Stocks purchased and services supplied

June 2015 June 2014 June 2015 June 2014

Joint ventures 2 220 50,430 46,130

Associates - - - 9

Other related parties (*) 49 49 73 119

Trade debtors, accrued income and

deferred costs

Trade creditors, accrued costs and

deferred income

June 2015 December 2014 June 2015 December 2014

Joint ventures 570 640 22,337 5,774

Associates - - - -

Other related parties (*) 50 17 7 -

(*) Entities controlled by the major Shareholder of Jerónimo Martins and entities owned or controlled by members of the Board of Directors.

All the transactions with these related parties were made under normal market conditions, i.e. the transaction value corresponds to prices that would be applicable between non-related parties.

Outstanding balances between Group companies and related parties, being a result of a trade agreement, are settled in cash, and are subject to the same payment terms as those applicable to other agreements celebrated between Group companies and their suppliers.

The amounts receivable are not covered by insurance and no guarantees are given or received, as the Group holds a relevant influence over these companies.

There are no adjustments for doubtful debts and no costs were recognised during the year related with bad or

doubtful debts with these related parties.

20 Events after the balance sheet date

At the conclusion of this Report there were no relevant events to highlight that are not disclosed in the Financial Statements. Lisbon, 28th July 2015

The Certified Accountant The Board of Directors

pwc

Limited Reuiew Report Prepared by Auditor Registered with theSecurities Market Commission (CMVM) on the Consolidated HalfYearInformation

(Free translationfrom the original in Portuguese)

Introduction

1 In accordance with the Portuguese Securities Market Code (CVM), we present our limitedreview report on the consolidated financial information for the six-month period ended June 30, 2015of Jerónimo Martins, SGPS, S.A. included in the consolidated Management Report, consolidatedbalance sheet (which shows total assets of Euro 5,159,352 thousand and total sharehoiders’ equity ofEuro 1,640,105 thousand, including non-controliing interests of Euro 237,779 thousand and a netprofit of Euro 149,510 thousand), consolidated income statement by functions, consolidated statementof comprehensive income, consoiidated statement of changes in shareholders’ equity and consolidatedstatement of cash flows for the period then ended, and the corresponding notes to the accounts.

2 The amounts in the consolidated financial statements, as well as those in the additionalfinancial information, are derived from the respective accounting records.

Responsibilities

3 It is the responsibility of the Board of Directors: (a) to prepare consolidated financialinformation which present fairiy, in ali material respects, the financial position of the companiesincluded in the consolidation, the consolidated results and the consoiidated comprehensive income oftheir operations, the changes in consolidated equity and the consolidated cash fiows; (b) to preparehistorical financial information in accordance with International Accounting Standard 34 — InterimFinancial Reporting as adopted by the European Union and which is complete, true, up-to-date, clear,objective and lawful as required by the CVM; (c) to adopt appropriate accounting policies and criteria;(d) to maintain appropriate systems of internal control; and (e) to disclose any significant matterswhich have influenced the activity, financial position or results.

4 Our responsibility is to verify the financial information included in the documents referred toabove, namely as to whether it is complete, true, up-to-date, clear, objective and lawful, as required bythe CVM, for the purpose of issuing an independent and professional report based on our work.

Scope

5 Our work was performed with the objective of obtaining moderate assurance about whetherthe financial information referred to above is free from material misstatement. Our work wasperformed in accordance with the Standards and Technical Recommendations issued by the Instituteof Statutory Auditors, planned according to that objective, and consisted primarily, in enquiries andanalytical procedures, to review: (i) the reliability of the assertions included in the financialinformation; (ii) the appropriateness and consistency of the accounting principles used, as applicable;(iii) the applicability, or not, of the going concern basis of accounting; (iv) the presentation of thefinancial information; (v) as to whether the consolidated financial information is complete, true, upto-date, clear, objective and lawful.

PricewaterhouseCoopers & Associados - Sociedade de Revisores Oficiais de Contas, Lda.Sede: Palácio Sottomayor, Rua Sousa Martins, 1 - 30,1069~316 Lisboa, PortugalTel +351213 599 000, Fax +351 213 599 999, www.pwc.ptMatriculada na CRC sob o NUPC 506 628 752, Capital Social Euros 314.000Inscrita na lista das Sociedades de Revisores Oficiais de Contas sob o n°183 e na CMVM sob o n° 9077

PncewatertioaseCoopers & Associados - Sociedade de Revisores Oficiais de Contas. Lda. pertence à rede de entidades que são membrosda PricewatemouneCoopers Intemational Limited, cada uma das quais é uma entidade legal autónoma e independente.

6 Our work also covered the verification that the consolidated financial information included inthe consolidated Management Report is consistent with the remaining documents referred to above.

7 We believe that the work performed provides a reasonable basis for the issue of this limitedreview report on the half year information.

Conclusions

8 Based on the work, which was performed with the objective of obtaining a moderate levei ofassurance, nothing has come to our attention that leads us to conclude that the consolidated financialinformation for the six-month period ended June 30, 2015 contam material misstatements that affectits conformity with International Accounting Standard 34 — Interim Financial Reporting as adopted bythe European Union and that it is not complete, true, up-to-date, clear, objective and lawful.

Report on other requirements

9 Based on the work, nothing has come to our attention that leads us to believe that theconsolidated financial information included in the consolidated Management Report is not consistentwith the consolidated financial information for the period.

July 31, 2015

PricewaterhouseCoopers & Associados- Sociedade de Revisores Oficiais de Contas, LdaRegistered in the Comissão do Mercado de Valores Mobiliários with no. 9077represented by:

José Pereira Alves, R.O.C.

(This is a transiation, not lo be signed)

Limited Review Report Prepared by Auditor Registeredwith the Securities Market Commission (CMVM)on the Consolidated Half Year Information Jerónimo Martins, SGPS, S.A.June 30, 2015 PwC 2 of 2