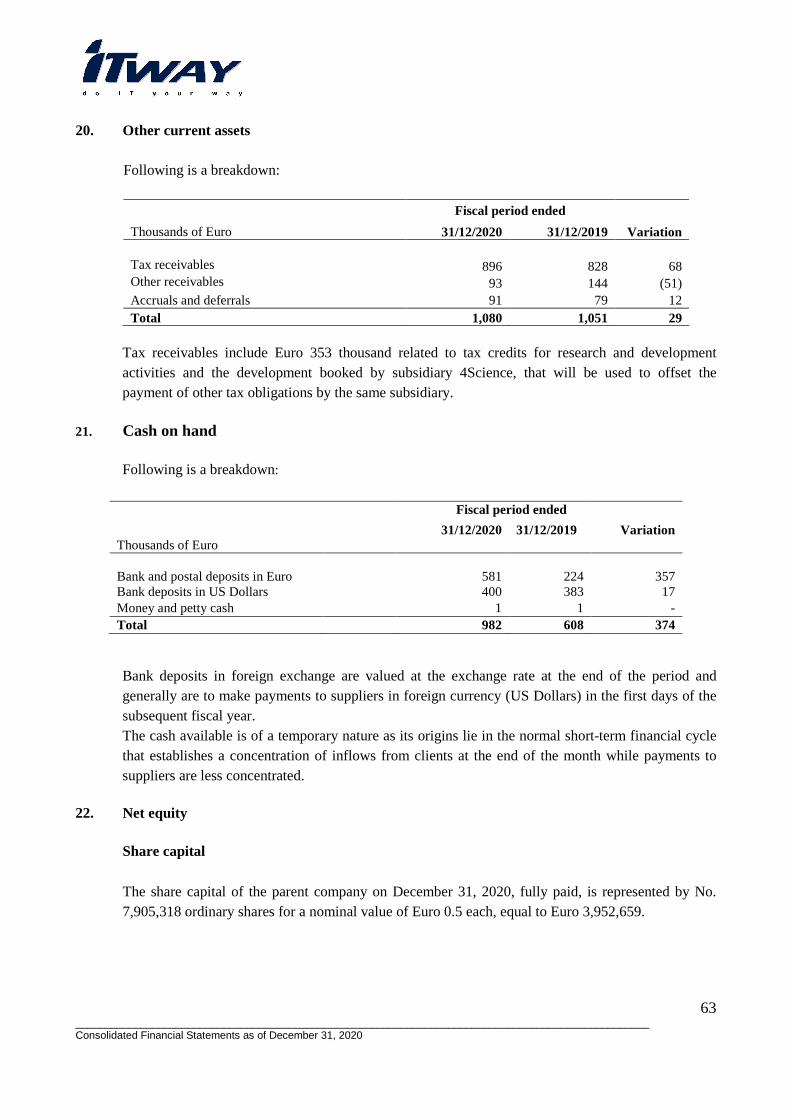

consolidated financial statements and separate financial

TRANSCRIPT

Directors’ Report on Operations for the fiscal year ended December 31, 2020

1

Consolidated Financial Statements and Separate Financial Statements

for the year ended December 31, 2020

Directors’ Report on Operations for the fiscal year ended December 31, 2020

2

Index:

• Directors’ Report on operations for the fiscal period ended December 31, 2020…………….......pag. 1

• Consolidated Group Financial Statements.................................................................................. pag. 23

• Explanatory Notes to the consolidated Financial Statements ..................................................... pag. 29

• Separate Financial Statements Itway S.p.A................................................................................. pag. 87

• Explanatory Notes to the Separate Financial Statements........................................................... pag. 93

Attachments

• Report of Auditing Company

Directors’ Report on Operations for the fiscal year ended December 31, 2020

3

Directors’ report on operations for the

Fiscal year ended December 31, 2020

Directors’ Report on Operations for the fiscal year ended December 31, 2020

4

Social Bodies

Board of Directors (Until the approval of the December 31, 2022 Financial Statements)

Name and last name Position Giovanni Andrea Farina President and Chief Executive Cesare Valenti Managing Director Valentino Bravi Independent Director Piera Magnatti Independent Director Annunziata Magnotti Independent Director Board of Statutory Auditors (Until the approval of the December 31, 2022 Financial Statements)

Name and last name Position Daniele Chiari President Silvia Caporali Member Rita Santolini Member Manager mandated to draft corporate accounting documents The board of directors named Sonia Passatempi (Administrative Manager of the Group) as the Manager in charge of drafting corporate accounting documents for the Itway Group. Auditing company

Analisi S.p.A.

The General Meeting gave the mandate for the auditing on July 2, 2018 for a period of nine years until the approval of the financial statements for the year ending December 31, 2026 and, pursuant to the regulations in force, it cannot be renewed.

Directors’ Report on Operations for the fiscal year ended December 31, 2020

5

Report on the ownership and on corporate governance In accordance to current laws, please note the Report on Ownership and Corporate Governance, approved by the Board of Directors of Itway S.p.A (hereinafter the “Company” or “Parent Company”) is available for the public at the administrative headquarters in Ravenna, via Braille 15, and can be consulted on the Internet site www.itway.com in the Investor Relation section. Activities and structure of the Group Following is the structure of the Itway Group at December 31, 2020:

The Company has its legal headquarters in Milan in Viale Achille Papa, 30 and the administrative headquarters in Ravenna in Via L. Braille, 15.

ITWAY S.p.A.

Itway France S.A.S.

100%

Itway Iberica S.L.

100%

Itway International

S.r.l. 100%

Itway Hellas S.A.

100%

Itway Turkyie Ltd

100%

Business-e

Infrastrutture S.r.l.

30%

Itway MENA FZC

17,1%

4 Science S.r.l.

100%

BE Innova S.r.l.

50%

Itway RE S.r.l.

100%

iNebula S.r.l. in

liquidazione 75%

Idrolab S.r.l.

10%

Dexit S.r.l.

9%

Directors’ Report on Operations for the fiscal year ended December 31, 2020

6

Structure of the Management Report The current management Report is drafted along with the financial statements and the consolidated financial statements of Itway S.p.A.

Performance of the Group and the reference market

The accounting principles, the evaluation principles and the consolidation principles referred to in preparing the Financial Statements for the fiscal year ended December 31, 2020 are, as in the previous fiscal year, the international accounting principles defined as IFRS. In particular, these principles require forward looking statements, as indicated in the continuation of the current report, in particular in the section “Foreseeable Evolution of operations” and in detail in the Explanatory Notes. In the context of the economic uncertainty illustrated below, please note that these forecasts have a component of risk and uncertainty. Therefore, it cannot be ruled out that in the near future the results achieved could be different from those forecast, therefore possibly requiring revisions that today cannot be either estimated or forecasted.

On December 30, 2020, the Group finalized an agreement with Mercatoria S.p.A., the main creditor of the Group (with receivables totalling Euro 5.4 million) for the execution of a recovery plan drafted according to art. 67, paragraph 3, letter d), of R.D. 267/1942 that envisages a debt reduction of 67% with payments in 36 monthly instalments starting from June 2020; the deal foresees a further debt reduction of 62% in case of early repayment by December 31, 2021. The Itway-Mercatoria agreement, defined based on the 2020-2023 Industrial and Financial Plan, approved by the Board of Directors on September 14, 2020, and subsequently integrated and updated along with the related financial package, was certified on October 5, 2020, according to article 67, paragraph 3, letter d) of R.D. 267/1942 by an independent expert and subsequently integrated and updated on December 29, 2020, confirming the truthfulness of corporate data and the feasibility of the plan, as well as its conformity to pursue the objectives of recovery and rebalancing of the financial and capital position of Itway. In light of the double-digit growth rates expected for emerging sectors of IoT, AI, and Big Data, and the in-depth knowledge and reputation in Cybersecurity developed over almost 25 years, the Group during the fiscal year focused on implementing its industrial plan that envisages significant growth over the next few years considering and valuing the investments already made in the sectors above. Furthermore, the Group continued to invest in the Patent Pending ICOY ® (I Care Of You) product that will position Itway as a leader in the Environment Health Safety (EHS) segment. The Group continues it positioning on the Digital Product Oriented model, focusing on business segments with higher value added, through three Business Units.

- Cybersecurity; - Data Science;

Directors’ Report on Operations for the fiscal year ended December 31, 2020

7

- Safety. The Itway Group in the fiscal year, also through its subsidiaries, continued to invest in Cybersecurity, IoT, Artificial Intelligence (AI), and Big Data, all of which are connected and correlated. As already disclosed to the market, during the fiscal year the Group took back full control of the Itway Hellas and Itway Turkiye subsidiaries, which operate in the historical Value Added Distribution (VAD) segment. Business unit areas:

• Itway S.p.A. is specialized in consultancy, planning, and system integration in the field of cybersecurity, in particular on the GDPR, Internet of Things (IoT) and work safety in the EH&S (Environment, Health & Safety) sector. The IoT and Safety sectors are covered and approached with the iNebula brand, of which Itway purchased, during the liquidation process underway, part of the products developed, and the brand name

• 4Science S.r.l. offers Data Science, Data Management services, and solutions for the scientific, and cultural heritage markets as well as Big Data

• Be Innova S.r.l. carries out Managed Security Services (MSS) with cybersecurity and network monitoring services through its NOC-SOC located in Trento. To date, there are approximately 50,000 protected digital devices. The main client of Be Innova is the Province of Trento for which it handles 24/365 days/year Cybersecurity. Also worthy of mention is the strong partnership established with IBM, for which in March 2019 it became a Service Center for Information Security

• Be Innova also has Smartys or the commercial name of the so-called ADAPT project co-financed with the Ministry of Education (MIUR) in the pre-commissioning phase in some Veneto region healthcare boards, the Fire Department, and the Trento Public Service Answering Point (PSAP). SMARTYS gathers biometric and environmental data used on the Environmental Healthcare Record (Fascicolo Socio Sanitario Elettronico-FSSE) of citizens, both in the private and public health care system, affiliated and not, in full safety and with the help of wearable sensors and IoT devices. Furthermore, there is also a Covid-19 App developed with the Bruno Kessler Foundation in Trento. The project was developed with a Security by design logic fully respecting privacy regulations and GDPR. SMARTYS is part of the emerging Health Data Security (HDS) segment of Cybersecurity.

General context and performance of the ICT Market: To date, there is only partial data on the ICT market performance in 2020 considering how the economic scenario has changed after Covid-19. GDP fell by 8.9% in 2020 (source: Istat, March 2021) and projections for the ICT market indicate an overall contraction of -3.1% with a significant rebound in 2021 (source: Assinform 2020).

Directors’ Report on Operations for the fiscal year ended December 31, 2020

8

In 2020, the digital market dynamics turned negative (ICT Services -3.7%, ICT Software and Solutions -1.1%, Devices, and Systems -3.5%, Network Services -3.9%, Digital Content, and Digital Advertising -1.5%) but were more resilient than almost all other markets. Double-digit growth rates are still expected for the more innovative segments of digital innovation, or the so-called Digital Enablers, starting with Cloud, from Cybersecurity to IoT and AI and the collaborative and remote work platforms (including smart working).

It is also worth mentioning that some sectors that are fundamental to western economies, in particular the Italian one, were weighed down by the Covid-19 pandemic in 2020 with significant drops in turnover: manufacturing (-14.7%), metallurgical (-16.7%), mechanical (-18.8%), automotive (-25.9%), energy (-10%), furniture (-15.4%), fashion (-18.6%) and reported significantly to the wage guarantee fund and the layoff ban. On the other hand, other sectors like those related to healthcare (+3.6%) and pharmaceutical (+4.2%) recorded significant growth (Assolombarda 2002, source Prometeia-Intesa S.Paolo). Also, the bank and insurance sector grew with the former benefiting from their roles as intermediaries in the Covid support and recovery decrees, with an increase in online clients of 17%, in digital transactions of 32%, and newly acquired clients through digital channels of 75% (Source: Fintech & Insuretech Observatory, School of Management of the Milan Polytechnic, December 2020). Construction, which represents some 9% of Italian GDP in 2020, also saw solid growth (+1.8%). This sector, along with infrastructure, is seen recording a sharp recovery thanks to the Euro 209 billion Recovery Plan. These are the sector that offset digital investments.

Market positioning: The Itway Group during the fiscal year continued to invest in Cybersecurity, IoT, Artificial Intelligence and Big Data, all of which are connected. Furthermore, the repositioning on new product lines continued, with the aim of replacing lower-margin lines with higher value added ones that also allow a smaller use of working capital.

Group’s industrial policy: The industrial policy of the Group continued to focus on higher value added business lines represented by the new Business Unit described above.

Directors’ Report on Operations for the fiscal year ended December 31, 2020

9

Following is the consolidated condensed income statement at December 31, 2020 compared with that of the same period a year earlier:

* The definition of Ebitda and Ebit is given in the Notes of the consolidated Financial Statements attached to the

current Report. In the 2020 fiscal year, Group revenues rose in volume terms by approximately 9% while EBITDA was Euro 2,203 thousand, down compared with Euro 3,358 thousand in 2019. The result after taxes is Euro 1,222 thousand compared with Euro 2,037 thousand in 2019. One-off items mainly related to the write-off of trade and financial payables for over Euro 2.8 million in 2019 and approximately Euro 2.3 million in 2020 impacted the results. Regarding the drop in operating Results, please note that the Group in the past fiscal years invested more significantly in the development of products than in 2020, and this, combined with investments in highly-skilled human resources is allowing the Group to broaden its presence on the market through products and services that are proprietary to Itway. At the same time, the lower capitalization for product development and the higher personnel costs, combined with a prudential write-down of receivables by the Parent Company, influenced the 2020 results. ICOY™ in the Safety Business Unit was the product line that most suffered from the slowdown caused by Covid-19. The product line is continuing its development road map, from an industrial prototype to a market product, a process that was slowed due to the Covid-triggered crisis of the sectors that it targets: manufacturing, metallurgical, oil & gas, and transport & logistics. The unit did not meet its budgeted sales, with a delay in part to 2021 and 2022. However, there was constant and growing sincere interest towards this innovative product that is proprietary to Itway from potential clients who increased their awareness towards the work safety of their workers.

(Thousands of Euro) December 31, 2020

December 31, 2019

Itway Group Itway Group

Turnover Sales revenue 35,786 31,219 Other operating revenue 2,968 4,125 Total turnover 38,754 35,344 Operating costs Cost of products 30,759 26,925 Personnel costs 2,511 2,260 Other costs and operating charges 3,461 2,801 Total operating costs 36,731 31,986 EBITDA* 2,023 3,358 Amortization and writedowns 577 639 EBIT* 1,446 2,719 Net financial charges (190) (287) Result before taxes 1,256 2,432 Income taxes (34) (395) Net result 1,222 2,037

Directors’ Report on Operations for the fiscal year ended December 31, 2020

10

During the year there were Euro 468 thousand non-recurring costs, broadly unchanged from Euro 460 thousand in 2019, related to the restructuring underway due to the remodulation of financial debt and the management of extraordinary transactions. Sector performance: Value Added Distribution Through the Value Added Distribution sector, the Group operates in Greece and Turkey in the distribution of specialized software and hardware products, certification products on the software technologies distributed, and pre and post-sales technical assistance services. Following are the main economic indicators of the VAD SBU, compared with those of the previous fiscal year:

Thousands of Euro 31/12/2020

31/12/2019

Total revenue 33911 30288

EBITDA* 1927 1551

EBIT* 1819 1449

Result before taxes 2089 1472

Result of the period 1820 1124

* The definition of Ebitda and Ebit is given in the Notes of the consolidated Financial Statements attached to the

current Report

The Covid-19 pandemic hit harshly continental Europe, but much less so Greece and Turkey, and, in these countries, a faster recovery is expected compared with the European average. Following is the breakdown by Country: Itway Turkiye posted a +35% rise in revenue in local currencies compared with 2019 thanks to the addition of new product lines to its portfolio. Even considering the foreign exchange devaluation (Euro to Turkish Lira), revenue was up +7%, with higher margins than the previous year, thereby confirming its position as one of the leading Cyber Security operators in Turkey. The Greek subsidiary, Itway Hellas, posted significant growth both in terms of revenue (+21%) and in market share. The Company, which specializes in Cyber Security, witnessed a jump in demand generated by the increase in smart working and the need of public and private organizations to protect data and information. Furthermore, the newly introduced product lines are giving the expected results. In particular, the Imperva product line, which is the leader in the WAF (Web Application Firewall) segment, quadrupled revenue in one year. Itway Hellas received Euro 300 thousand of aid from the Greek State at very favourable interest rates as part of its measures to support companies under lockdown due to the Covid-19

Directors’ Report on Operations for the fiscal year ended December 31, 2020

11

pandemic. This confirms its ability to dialogue with the local financial system and the proven bankability of the Company, even in a difficult year like 2020. Sector performance: Activities of the Parent Company and Subsidiaries in the “Scale-up” phase Itway S.p.A. is the parent company listed on Borsa Italiana S.p.A. that supplies services of different nature to the operating subsidiaries and includes new sectors described hereinafter that are investing in the realization of products and that are in the operational and commercial scale-up phase.

• Itway S.p.A., is an operational holding, dealing with consultancy, planning, and system integration in the field of cybersecurity, in particular on the GDPR, Internet of Things (IoT) and work safety in the EH&S (Environment, Health & Safety) sector. The IoT and Safety sectors are covered and approached with the iNebula brand, of which Itway purchased, during the liquidation process underway, part of the products developed, and the brand name

• 4Science S.r.l. offers Data Science, Data Management services, and solutions for the scientific, and cultural heritage markets as well as Big Data.

Following is the condensed income statement compared with the previous fiscal year including data from the ASA activities of the Parent Company and other sectors in the scale-up phase: (Thousands of €uro)

31/12/20

31/12/19

Revenue 4,843 5,056 Ebitda 96 1,807 Ebit (373) 1,270 Result before taxes (833) 960 Result for the period (598) 914

Following is a brief comment on the performance of 4Science and Itway: The positioning of the Cybersecurity and Safety Business Units, with the ICOY product line, continued in Itway S.p.A. with new technical and sales staff. The sales pipeline is growing. Bugnion S.p.A. completed the complex patent authorization procedure for ICOY in Italy and the EU and it is now Patent Pending. The ICOY MOVER Bridge Crane product line completed commissioning and is now ready for launch, while FORKLIFT completed commissioning in February 2021 with positive results despite the 13-month delay. Itway had to adapt the speed of commissioning to its Client/Partner with whom it executed the Proof of Concept (POC). Covid-19 had a significant adverse impact on this important partner, active in the metallurgical sector, and this affected also the progress in the POC, which was completed only in March 2021.

Directors’ Report on Operations for the fiscal year ended December 31, 2020

12

As previously described, the product line is continuing its development path, from an industrial prototype to a market product, a process that has been delayed by the Covid-triggered crisis in the sectors it targets: manufacturing, metallurgical, oil & gas, and transport & logistics. The product line did not achieve its 2020 sales budget, with a delay into 2021 and 2022. However, there has been constant and increasing sincere interest towards this innovative proprietary Itway product from potential clients who have increased their awareness towards the safety of their workers. Despite the 14-month accumulated delay, which has weighed on operating results, the prospects for this innovative product line are very positive. In this context, it is worth remembering that both Itway S.p.A. and 4Science S.r.l. in the past few years invested more significantly in product development than in 2020 and this, combined with the investments in highly skilled human resources, is allowing to broaden its market presence through proprietary products and services. At the same time, the lower product development capitalization and higher personnel costs, combined with a prudential write-down of receivables of Euro 900 thousand by Itway S.p.A., has impacted 2020 results. 4Science S.r.l., after a few years of activity, is now a reference player in the emerging markets of Data Science, Data Management, and Big Data (Data Curation). It also has a leading role as a Digital Repository and Preservation of digital assets related to scientific research and cultural and artistic assets, the so-called Digital Libraries. The unit recorded constant growth since its establishment in 2017 and this trend continued in 2020 despite the complex period caused by the Covid-19 pandemic. At the end of 2020, it had over 100 in-house projects, acquired over three years, 75% of which on behalf of foreign Clients, namely in Europe, the US, LATAM, and the Far East.

Furthermore, in 2020 there was also an increase in the average value of the order that generated an increase of approximately 22% in sales revenue, while the Euro 1,400 thousand investment in DSpace CRIS (Current Research Information Systems) and in GLAM (Gallery Library Archive Museum) and their related add-ons has been almost completed, so the weight on capitalizations has been reduced to under 20% of total sales revenue, confirming the company’s ability to transform R&D efforts into sales

During the fiscal year, the Peruvian national consortium for research and science, CONCYTEC awarded 4Science the USD 1.3 million CRIS contract financed by the World Bank. This was possible thanks to the skills in the field of Big Data and Digital Repository that 4Science has developed over the years and that required a high degree of specialization and experience in the creation and management of CRIS (Current Research Information Systems) aimed at the research sector and the scientific community.

The skills acquired over the years, combined with the strategic choice to operate in the Open Source software sector, allowed 4Science to position itself at a global level as a reference point for CRIS solutions and to include among its clients prestigious universities (including the Institute for Advanced Study of Princeton University in New Jersey, where Albert Einstein taught).

Directors’ Report on Operations for the fiscal year ended December 31, 2020

13

Precisely because of the specific skills developed on CRIS systems, many clients mandated 4Science to develop projects related to the research sector that in this period of the pandemic have assumed an even greater strategic role both in the scientific community and in government and political circles as they are part also of the digitalization of public administration at a global level.

Also the Cultural Heritage segment, with the GLAM product, which covers a very interesting and current market like the Long Term Preservation and Data Curation of digital information of cultural heritage, including collections, persons, events, concepts, places, and projects, recorded significant growth of 270%. In Italy, national points of excellence including the Naples National Library and the Giuseppe Verdi Conservatory in Milan chose 4Science to digitalize their cultural assets.

4Science recorded a net profit of Euro 220 thousand and an Ebitda of Euro 416 thousand, in line with the budget.

iNebula S.r.l. continues with its liquidation process that started 2018 with settlement agreements with its main creditors.

Personnel

The average number of employees of the Group during the 2020 fiscal year was of 50 units while the punctual number at the end of the fiscal period was of 53 units. The nine-unit increase from a year ago is due to the hiring of technical staff in Itway and 4Science. Following is a breakdown by category, compared with the previous fiscal period. 31/12/2020 31/12/2019 31/12/2020 31/12/2019 Avg Avg Punctual Punctual Managers 3 2 3 2 Mid-managers

5 6 5 6

Employees 42 35 45 36

Total 50 43 53 44

Directors’ Report on Operations for the fiscal year ended December 31, 2020

14

Net financial position Following is the net financial position of the Group:

Following is the net financial position of the Parent Company:

Please see the Statement on Cash Flows for a more detailed analysis on the movements that generated the change in the Net Financial Position. There was a marked improvement in the net financial position of both the Group and the Parent Company as of December 31, 2020, mainly due to the write-off of certain debt positions, in particular the agreement reached with Mercatoria, the main creditor, for the execution of a recovery plan drafted pursuant to article 67, paragraph 3, letter d) of R.D. 267/1942 Furthermore, on December 15, 2020, the financing terms with Iccrea were redefined, allowing to reclassify debt as medium-term while in previous fiscal years it was included among current liabilities due to covenant breaches.

Thousands of Euro

31/12/2020

31/12/2019

Cash on hand 982 608 Financial receivables 2,275 2,498 Current financial assets 1,080 1,210 Current financial liabilities (2,947) (7,985) Convertible bonds (473) -

Current net financial position 917 (3,669)

Non-current financial assets 2,098 2,098

Non-current financial liabilities (4,389) (1,785)

Non-current net financial position (2,291) 313

Total net financial position (1,374) (3,356)

Thousands of Euro

31/12/2020

31/12/2019

Cash on hand 271 21 Financial receivables 2275 2498 Current financial assets (2625) (7161) Current financial liabilities (473) - Convertible bonds (552) (4642) Current net financial position 2098 2098 Non-current financial assets (3574) (1830)

Non-current financial liabilities (1476) 268

Non-current net financial position (2028) (4374)

Directors’ Report on Operations for the fiscal year ended December 31, 2020

15

Non-current liabilities included the impact that was not significant from the application of IFRS 16 “Leasing” that became mandatory from January 1, 2019. Reconciliation between Parent Company and Consolidated data Following is the reconciliation sheet of the consolidated net equity and consolidated results with those of the parent company: 2020 2019

Recurrent

assets

Non-recurrent

assets Total Recurrent

assets

Non-recurrent

assets Total

Net result of the Parent Company 1222 - 1222 2036

2036

Results of subsidiaries

807 807 1439

1439

Adjustment to values already included in the consolidated financial statements (807) - (807) (901) (1439)

Consolidated net result 1222 - 1222 2036

2036

2020 2019

Recurrent

assets

Non-recurrent

assets Total Recurrent

assets

Non-recurrent

assets Total

Net equity of the Parent Company 8701 - 8701 7831 - 7831

Results of subsidiaries

-

- -

Other consolidated entries

157 - 157 176

- 176

Consolidated net equity 8858 - 8858 8007

- 8.007

Risk management

The Group is exposed to financial risks deriving from the economic situation at a global level; the Group uses, as a reference currency and for its purchasing and sales activities mainly the Euro and in a minor way the US Dollar and the Turkish lira. In order to analyze the financial risk management we refer to the half-year consolidated Financial Statements Explanatory Notes.

Going concern The Consolidated financial statements of the Itway Group as of December 31, 2020, show a positive result of Euro 1,222 thousand while that of the Parent Company ended with a net profit of approximately Euro 416 thousand (net of the results of subsidiaries booked under IAS 27).

Directors’ Report on Operations for the fiscal year ended December 31, 2020

16

From a financial point of view, as of December 31, 2020, the Parent Company concluded an agreement with Mercatoria S.p.A., the main creditor of the Group (with receivables totalling Euro 5.4 million). The agreement defined based on the 2020-2023 Industrial and Financial Plan, approved by the Board of Directors on September 14, 2020, and subsequently integrated and updated along with the related financial plan, that received, pursuant to article 67, paragraph 3, letter d) of the Bankruptcy Law, the certification from an independent expert that confirmed its feasibility, the truthfulness of the data, as well as its suitability to pursue the objective of restructuring and rebalancing of the financial and capital position of Itway. The agreement with Mercatoria includes, among other things, a 67% reduction in debt with payment in 36 monthly instalments starting from June 2020 and a further reduction to 62% in case of early repayment by December 31, 2021. The financial statements to December 31, 2020, include the impact of the 67% reduction through the recording of Euro 1,792 thousand of non-recurring income within the Other Revenue and Proceeds. Itway is committed to respecting some financial parameters both on a quarterly and an annual basis and has granted Mercatoria a two-year call option, starting from January 1, 2023, on No. 390,000 own shares at a strike price of Euro 1. The failure of the company to pay two instalments, even not consecutively, unless agreed upon, could determine the resolution of the contract with the resulting payment of the entire debt outstanding before the write-off. Itway paid Euro 606 thousand at the signing of the agreement and to date another two instalments for a further Euro 202 thousand, leaving the residual debt towards Mercatoria and Socrate at Euro 2.8 million, to date. The plan also foresees:

(i) The repayment in instalments of around Euro 100 thousand per month of the financial debt towards Mercatoria by the May 30, 2023 deadline;

(ii) The repayment of the remaining financial debt by the December 31, 2021 deadline, according to the terms agreed in the rescheduling agreements that are being or that will be defined;

(iii) The payment of expired trade payables totalling approximately Euro 2 million; (iv) The issue of up to Euro 5.5 million of Convertible Bonds deliberated by the

Extraordinary Shareholders’ meeting of Itway on October 30, 2020, reserved for the Swiss institutional investor Nice & Green SA (“N&G”).

These are the essential elements of the 2020-2023 Plan aimed at developing the business of the Itway Group that will focus on: 1) The consolidation of the VAD Business Unit in Greece and Turkey; 2) The valuing and development of the Cybersecurity, Safety, and Data Science Business Unit 3) Supporting working capital through the issue of convertible bonds in favour of N&G with

whom a Warrant and Convertible Notes Funding Program investment contract was signed for an overall Euro 6 million.

The investment contract with Nice & Green SA aims at supporting working capital of the Company, strengthen its financial structure, and broaden the shareholder structure. The capital

Directors’ Report on Operations for the fiscal year ended December 31, 2020

17

raised from the N&G transaction will equip Itway with additional capital and financial resources that will be used to accelerate the development of the Company’s growth and investment strategies in the market segments in which Itway operates without any additional burden for the Company. The Program foresees an issuance period for an overall 36 months from the date of signing of the contract and comprises: (i) A tranche of warrants to buy up to Euro 500 thousand own shares of Itway already in its portfolio (the Warrants); (ii) 11 tranches of bonds, each with a nominal value of Euro 500 thousand convertible into newly issued Itway shares (Bonds). It envisages the commitment by N&G to subscribe to several tranches following a specific request from Itway. The contract foresees that the loan will be non-interest bearing and that each Bond will have a 12-month duration from the issue date. Furthermore, in case of failure to request the repayment by the maturity date, the Company shall be obliged to automatically convert the Bonds in circulation into newly issued shares. The Investor is entitled to ask for the conversion of the bonds into shares at any time following the conversion request. Upon conversion request, the Issuer, instead of issuing new shares, shall have the option to repay the Bonds in cash. The Bonds are non-interest bearing and will not be listed on any regulated market.

To execute the Bond issuance program, an extraordinary shareholders’ meeting took place on October 30, 2020, that deliberated the issue of bonds and a capital increase without option rights to service the conversion. To the date of writing of the current Report, the company entirely exercised the warrant during the 2020 financial year, using shares that it already held in its portfolio, while of the 11 tranches of Bonds one tranche (comprising 50 Bonds with a nominal value of Euro 10 thousand each) was issued and underwritten, upon request of the Company, and partially exercised by Nice&Green SA through the request to covert No. 20 bonds for an overall value of Euro 200 thousand.

The number of shares that are subject to the conversion was determined conforming to the terms of the Contract based on 91% of the minimum price (defined as the VWAP –volume-weighted average price) recorded in the eight trading days before the date of conversion request and totalled No. 286,286 newly issued ordinary shares of Itway, with regular dividend rights, representing 3.49% of share capital after the capital increase.

As of December 31, 2020, the Itway Group had a current net financial indebtedness of approximately Euro 3.4 million, of which Euro 1.3 million already expired at the date of the financial statements, an expired indebtedness with tax and social security bodies for a total of Euro 475 thousand (that will be paid within the terms foreseen by regulations in force), and expired indebtedness towards suppliers of Euro 2.7 million (of which approximately Euro 0.8 million for amounts being contested, also through legal means and Euro 1.8 million of suppliers

Directors’ Report on Operations for the fiscal year ended December 31, 2020

18

no longer present on the market but that for prudential reasons are still booked in the balance sheet).

After the agreement reached with Mercatoria described above, to date negotiations are still underway with financial institutions or companies (art. 115 of TULPS) that acquired debt from certain banks for smaller amounts. The Company deems it reasonable to be able to conclude these negotiations, according to the plan, on the repayment terms. Based on the 2020-2023 Industrial and Financial Plan approved by the Board of Directors that an independent legal expert certified pursuant to article 67, paragraph 3, letter d) of the Bankruptcy Law, confirming the truthfulness of the corporate data and the feasibility of the plan as well as its conformity in pursuing the objectives of recovery and rebalancing the Company’s financial and capital position, the Directors, also comforted by the positive results achieved in these past years, drafted the financial statements on a going concern basis. Subsequent events In February 2021, No 286,286 new shares were issued following the request of conversion into shares for Euro 200 thousand of the first tranche of convertible bonds, increasing the Share Capital to Euro 4,085,802.

Foreseeable evolution of operations

As highlighted in the 2020-2023 Industrial Plan, which was approved by the Board of Directors and which was certified by an independent third party, the Group is expected to focus in the sectors of Cybersecurity, Data Science, and Safety. Furthermore there will be a growing focus on the Be Innova S.r.l. and the 4Science S.r.l. subsidiaries.

It is difficult to assess today whether there will be a significant impact on performance from the effects of the Covid-19 pandemic. However, it is important to remember that the activities of the Itway Group, mostly related to cybersecurity, have proven essential also, and above all, in these moments of global emergency, proving that Cybersecurity, dealing with the security of the core activities of companies, can be considered anti-cyclical compared to other market sectors. The measures adopted by almost all organizations in terms of smart working multiplies exponentially the risks related to security, resulting in greater demand for Cybersecurity solutions to mitigate these risks. The activities of Itway, being mainly made up of services, continued also with the new modality of remote working that the COVID emergency imposed. There was no significant impact on the Greek and Turkish subsidiaries, given the limited spread of the pandemic in these countries. However, as described above, the Safety ICOY Business Unit in 2020 and partially also in 2021 suffered from a lack of growth due to the segments it targets -- manufacturing, metallurgical, oil & gas, transport & logistic. The 2020 sales budget has been delayed in part to 2021 and in part in 2022. There was, however, constant and growing interest towards this innovative product that is proprietary to Itway from potential clients who

Directors’ Report on Operations for the fiscal year ended December 31, 2020

19

are more aware of the safety of their workers. Despite an expected 14-month delay, the outlook for this innovative product line is still very positive. Following is the foreseeable evolution of operation, divided by SBU: 4Science s.r.l. The company is fully operational with highly specialized personnel to carry out its objectives: becoming the reference company in the emerging Data Science, Data Management, Big Data (Data Curation), and Digital Repository and Preservation of cultural and artistic assets, the so- called Digital Library. The Big Data market is grew at an annual average of 23.1% from 2016-2019(Assinform) and 48% of companies forecasts investments in the sector in the future.

4Science offers services that place it in a highly specialized sector. On the one hand, it operates in the so-called Big Data segment, on the other hand, this sector is very broad and it is necessary to have a focus. Our skills are in data management for digital libraries and digital repositories, which in 2021 is forecast to be worth Euro 11.73 billion globally, with Europe worth, Euro 2.73 billion, and Italy Euro 188 million (Source: CiC Research and IDC Research, February 2021).

The Digital Libraries & Digital Repositories market is related to Business Analytics, Deep Learning, and Artificial Intelligence (AI) or Augmented Intelligence. This brings us to consider how to interact and collaborate with companies that are specialized in this sector.

Furthermore, we count on developing alliances with single players with whom we have synergies, with skills, therefore, that are complementary to our own and with whom to take part in projects from which we are excluded. In confirmation of this, the 2021 fiscal year started with an order portfolio of almost Euro 1 million that will be invoiced during 2021

Itway S.p.A. The company deals with consultancy, planning, and system integration in the field of cybersecurity, in particular, GDPR, Internet of Things (IoT), and work safety in the Environment, Health & Safety (EH&S) sector. In the Safety market, particular focus will be placed on developing and commercializing ICOY solutions. The ICOY line offers Artificial Intelligence and Deep Learning support to operators who work in dangerous work environments, to prevent and avert accidents. ICOY is today available with the ICOY MOVER®:

− MOVER CRANE for Bridge Crane, Quay Crane, Container; − MOVER FORKLIFT for forklift, forklift trucks that move in factories, docks,

and/or construction sites −

ICOY, which is in the start-up phase, was hit by slowdowns caused by Covid-19, which we count on starting to overcome in 2021.

Directors’ Report on Operations for the fiscal year ended December 31, 2020

20

Following the positive commissioning of ICOY MOVER Bridge Crane and MOVER Forklift, the pipeline prospect, which we presented and saw concrete interest, is significant with a market potential of thousands of retrofit aftermarket installations. Itway Turkiye Ltd. and Itway Hellas S.A. The value-added distribution activities continued to grow significantly, confirming also in 2020 a solid ability to grow. The Business Plan of the two countries foresees growth in 2021 in line with previous years, confirming their strategic leadership position in cybersecurity in Greece and Turkey. Significant, non-recurrent, atypical and/or unusual transactions In the fiscal period ended December 31, 2020, there were no atypical and/or unusual transactions with third parties or between Companies of the Group as defined by Consob Communication dated July 28, 2006, while the previous paragraphs extensively described significant and non-recurring transactions related to the write-off of some debt positions. Relationships with third parties In the 2020 fiscal period the Group had commercial and financial relationships with related parties. These relationships were part of normal management activity, regulated at market conditions that are established by contract by the parties in line with the standard procedures. Following is a summary: Thousands of €uro Receivables Payables Costs Revenue Itway S.p.A. vs Giovanni Andrea Farina & Co. S.r.l. 304 - 198 2

Itway S.p.A. vs Be Innova S.r.l. 4,587 117 177 175

Itway S.p.A. vs Fartech S.r.l. 34 142 31 33

TOTAL 4,25 259 406 210

Itway directs and coordinates its subsidiaries in Italy. This activity consists in indicating the general strategic and operational direction of the Group, defining and adjusting the organizational Model and elaborating the general policies to manage human and financial resources. No company directs or controls Itway S.p.A

Directors’ Report on Operations for the fiscal year ended December 31, 2020

21

Research & Development activities During the period a total of Euro 244 thousand (compared with Euro 763 thousand in the previous fiscal year) was invested in the development of new products and services in particular in the business units described above, which were capitalized in intangible assets. Own shares

The Parent Company as of December 31, 2020, owned No. 203,043 own shares (equal to 2.57% of share capital) for a nominal value of Euro 101,522 and an overall cost of the shares held in the portfolio of Euro 320 thousand (equal to the amount reflected in the Own Share reserve deducted from net equity of the fiscal period and at a consolidated level). Of these, No 136,400 own shares (equal to 1.73% of share capital) were allocated on loan to Nice & Green SA to service the previously described financial transaction. The reduction in the number of shares compared with the previous fiscal year is due to the exercising of the warrant underwritten by Nice & Green. Stakes held by the directors The following table sums up the information requested by the Consob regulation regarding the stakes in the parent company held by Directors, Auditors, Managing directors their spouses, minors, both directly or through controlling companies, trusts, or delegated third parties. Please note that the data are normally updated with communication carried out between the Shareholders and the Company Number of shares

Last name and name Ownership at

31/12/2019 Purchased Sold

Owned at 31/12/2020

Giovanni Andrea Farina & Co. S.r.l. 2,573,787 - - 2,573,787 Gavioli Anna Rita (*) 179,412 - - 179,412 Valenti Cesare 1,012,284 - - 1,012,284 Total 3,765,483 - - 3,765.483

(*) Spouse of G. Andrea Farina

The only shareholder that exceeds 10% of share capital is the company G. Andrea Farina & Co. S.r.l. and Cesare Valenti (Director of the Parent Company).

Directors’ Report on Operations for the fiscal year ended December 31, 2020

22

Proposed allocation of the result of the fiscal period In terms of the allocation of the result reported in the financial statements of the company, it has been proposed to allocate the Euro 1,222 thousand profit of the 2020 fiscal year to reserve.

Ravenna, March 29, 2021 FOR THE BOARD OF DIRECTORS Il President e Chief Executive Officer G. Andrea Farina

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

23

ITWAY GROUP CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31 , 2020

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

24

CONSOLIDATED INCOME STATEMEMT Thousand of Euro Fiscal year as of 31 Dec 2020 31 Dec 2019

Net amount Itway Group

Net amount Itway Group

Revenues from sales 35,786 31,219

Other operating revenues 2,968 4,125

Products (30,759) (26,925) Costs of services (2,304) (2,269) Costs of personnel (2,511) (2,260) Other operating expenses (1,157) (532)

EBITDA 2,023 3,358 Depreciations and amortisations (577) (639) EBIT 1,446 2,719 Financial proceeds 63 22 Financial charges (253) (309)

Profit before taxes 1,256 2,432

Taxes (34) (395)

Result for the period 1,222 2,037

Attributable to: Sharedholders of parent company 1,224 2,041 Minorities (2) (4) Result per share

From operations:

Basic 0.17 0.29 Diluited 0.17 0.29

* With regard to relations with related parties, reference should be made to Note 31. ** The definition of EBITDA and EBIT is provided in the following paragraph “Presentation of the financial statements”.

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

25

COMPREHENSIVE CONSOLIDATED INCOME STATEMENT

Fiscal year as of Euro migliaia 31 Dec 2020 31 Dec 2019 Net

amount Itway Group

Net amount Itway Group

Net result

1,222 2,037

Components that can be reclassified to the income statement:

Profit/(Losses) from the conversion of the balance sheet of foreign subsidiaries

(798) (265)

Components that cannot be reclassified to the income statement:

Actuarial gain (losses) on defined-benefit plans

(53) -

Comprehensive result 371 1,772

Attributable to:

Sharedholders of parent company 373 1,776

Minorities (2) (4)

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

26

CONSOLIDATED FINANCIAL STATEMENT Fiscal year as of

Thousand of Euro 31 Dec 20 31 Dec 19 ASSETS Net current assets Property, plans and machinery 942 991 Goodwill 1,849 1,852 Other intangible assets 2,183 2,319 Rights of use 2,605 2,801 Investments 709 1,765 Deferred tax assets 871 791 Non-current financial assets 2,098 2,098 Other non current assets 30 34

Total 11,287 12,651 Current assets Inventories 361 653 Account receivables - Trade 18,921 19,203 Other current assets 1,080 1,051 Cash on hand 982 608 Other financial credits 2,275 2,498 Current financial assets 1,080 1,210

Total 24,699 25,223 Total assets 35,986 37,874 NET EQUITY AND LIABILITIES Share capital and other reserves Share capital and reserves 7,987 6,323 Net result of the period 1,224 2,041 Total Net Equity 9,211 8,364 Share capital and reserves of minorities (353) (357) Total Group Net Equity 8,858 8,007 Non current liabilities Severance indemnity 483 406 Non current account payable – Trade 348 - Deferred tax liabilities 241 516 Non current financial liabilities 4,389 1,785

Total 5,461 2,707 Current liabilities Financial current liabilitites 3,420 7,985 Current account payable – Trade 13,389 14,158 Tax payable 2,656 2,447 Other current liabilities 2,202 2,570

Total 21,667 27,160 Total liabilities 27,128 29,867 Total Net Equity and Liabilities 35,986 37,874

* With regard to relations with related parties, reference should be made to Note 31.

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

27

Consolidated statement of charges in equity Cumulated profit (loss) Thousand of Euro Share

capital Own share

reserve

Share premiu

m reserve

Legal reserve

Voluntary reserve

Other reserve

Transaltion

reserve

Result for the period

Net equity of Group

Minority interests

Total Net Equity

Balance at January 1, 2019

3,953

(1,346)

17,584

485

4,792

(16,691)

(2,710)

520

6,587

(352)

6,235

Variation in own shares

-

-

-

-

-

-

-

-

-

-

-

Total operations with shareholders

-

-

-

-

-

-

-

-

-

-

-

Allocation of the result for the year

- - - - - 520 - (520) - - -

Result of the period - - - - - - - 2,041 2,041 (4) 2,037 Other operations - - - - - - - - - - - Other components of comprehensive results at 31 Dec 2019:

Gain/(Losses) on defined benefit plans

- - - - - - - - - - -

Overall result

-

-

-

-

-

-

(265)

-

(265)

-

(265)

Comprehensive result - - - - - - (265) 2,041 1,776 (4) 1,772 Balance at December 31, 2019

3,953

(1,346)

17,584

485

4,792

(16,171)

(2,975)

2,041

8,363

(356)

8,007

Cumulated profit (loss) Thousand of Euro Share

capital Own share

reserve

Share premiu

m reserve

and other

operations

Legal reserve

Voluntary reserve

Other reserve

Transaltion

reserve

Result for the period

Net equity of Group

Minority interests

Total Net Equity

Balance at January 1, 2020

3,953

(1,346)

17,584

485

4,792

(16,171)

(2,975)

2,041

8,363

(356)

8,007

Variation in own shares

-

1,026

(547)

-

-

-

-

-

479

-

479

Total operations with shareholders

-

1,026

(547)

-

-

-

-

-

479

-

479

Allocation of the result for the year

- - - - - 2,041 - (2,041) - - -

Result of the period - - - - - - - 1,224 1,224 (2) 1,222 Other operations - - - - - - - - - - - Other components of comprehensive results at 31 Dec 2020:

Gain/(Losses) on defined benefit plans

- - - - - (53) - - (53) - (53)

Overall result

-

-

-

-

-

-

(798)

-

(798)

-

(798)

Comprehensive result - - - - - (53) (798) 1,224 373 (2) 371 Balance at December 31, 2020

3,953

(320)

17,037

485

4,792

(14,187)

(3,773)

1,224

9,211

(354)

8,858

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

28

CONSOLIDATED STATEMENT OF CHARGES IN FINANCIAL POSI TION

Esercizio chiuso al

Euro migliaia 31/12/20 31/12/19

Risultato prima delle imposte "Netto Gruppo Itway" 1.222 2.039

Rettifiche per voci che non hanno effetto sulla liquidità:

Ammortamenti immobilizzazioni materiali 107 99

Ammortamenti attività immateriali 308 326

Ammortamento diritti d'uso 162 168

Accantonamento ai fondi svalutazione crediti 900 7

Accantonamento benefici ai dipendenti al netto dei versamenti vso ist. previd. 72 60

Variazione di attività/passività non correnti - (141)

Cash flow da attività operativa al lordo della variazione del capitale d'esercizio 2.771 2.558

Pagamenti di benefici a dipendenti (48) 25

Variazione dei crediti commerciali ed altre attività correnti (294) (529)

Variazione delle rimanenze 292 (189)

Variazione dei debiti commerciali ed altre passività correnti (927) (888)

Cash flow da attività operativa generato (assorbito) dalle variazioni di CCN (977) (1.581)

Cash flow da attività operativa (A) 1.794 977

Investimenti in immobilizzazioni materiali (al netto dei disinvestimenti) (58) 2.628

Incrementi/(Decrementi) di diritti d'uso 34 (2.969)

Investimenti in altre attività immobilizzate (al netto dei disinvestimenti) 884 625

Cash flow da attività di investimento (B) 860 284

Accensione/(Rimborsi) di passività finanziarie correnti (4.565) (1.262)

Accensione/(Rimborsi) di passività finanziarie non correnti nette 2.604 (77)

Operazioni su azioni proprie 479 -

Cash flow da attività di finanziamento (C) (1.482) (1.339)

Variazione netta della riserva di traduzione di valute non Euro (798) (265)

Cash flow da attività cedute (D) - -

Incremento/(Decremento) disponibilità liquide e mezzi equivalenti (A+B+C+D) 374 (343)

Disponibilità liquide e mezzi equivalenti di inizio periodo 608 951

Disponibilità liquide e mezzi equivalenti di fine periodo 982 608

Financial charges paid during the year amounted to Euro 136 thousand (Euro 106 thousand in the previous year).

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

29

EXPLANATORY NOTES OF THE CONSOLIDATED FINANCIAL STA TEMENTS GENERAL INFORMATION Itway S.p.A. (the “Company” or the “Parent Company”) is a public limited company constituted in Italy. The Company moved its legal headquarter to Milan, in Viale Achille Papa, and its administrative headquarters in Ravenna in Via L. Braille 15.

Going concern

The Consolidated financial statements of the Itway Group as of December 31, 2020, show a positive result of Euro 1,222 thousand while that of the Parent Company ended with a net profit of approximately Euro 416 thousand (net of results of the subsidiaries booked under IAS 27). From a financial point of view, on December 30, 2020, the Parent Company sealed an agreement for the execution of a recovery plan drafted pursuant to article 67, paragraph 3, letter d) of R.D. 267/1942 with Mercatoria S.p.A., the main creditor of the Group (with receivables totalling Euro 5.4 million). The agreement defined based on the 2020-2023 Industrial and Financial Plan, approved by the Board of Directors on September 14, 2020, and subsequently integrated and updated along with the related financial plan, that received, pursuant to article 67, paragraph 3, letter d) of the Bankruptcy Law, the certification from an independent expert that confirmed its feasibility, the truthfulness of the data, as well as its suitability to pursue the objective of restructuring and rebalancing of the financial and capital position of Itway.

The agreement with Mercatoria includes, among other things, a 67% reduction in debt with payment in 36 monthly instalments starting from June 2020 and a further reduction to 62% in case of early repayment by December 31, 2021. The financial statements to December 31, 2020, include the impact of the 67% reduction through the recording of Euro 1,792 thousand of non-recurring income within the Other Revenue and Proceeds. Itway is committed to respecting some financial parameters both on a quarterly and an annual basis and has granted Mercatoria a two-year call option, starting from January 1, 2023, on No. 390,000 own shares at a strike price of Euro 1. The failure of the company to pay two instalments, even not consecutively, unless agreed upon, could determine the resolution of the contract with the resulting payment of the entire debt outstanding before the write-off. Itway paid Euro 606 thousand at the signing of the agreement and to date another two instalments for a further Euro 202 thousand, leaving the residual debt towards Mercatoria and Socrate at Euro 2.8 million, to date.

The plan also foresees: (i) The repayment in instalments of around Euro 100 thousand per month of the financial debt

towards Mercatoria by the May 30, 2023 deadline; (ii) The repayment of the remaining financial debt by the December 31, 2021 deadline, according to

the terms agreed in the rescheduling agreements that are being or that will be defined; (iii) The payment of expired trade payables totalling approximately Euro 2 million; (iv) The issue of up to Euro 5.5 million of Convertible Bonds deliberated by the Extraordinary

Shareholders’ meeting of Itway on October 30, 2020, reserved for Swiss institutional investor Nice & Green SA (“N&G”).

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

30

These are the essential elements of the 2020-2023 Plan aimed at developing the business of the Itway Group that will focus on: 1) The consolidation of the VAD Business Unit in Greece and Turkey; 2) The valuing and development of the Cybersecurity, Safety, and Data Science Business Unit 3) Supporting working capital through the issue of convertible bonds in favour of N&G with whom a Warrant and Convertible Notes Funding Program investment contract was signed for an overall Euro 6 million.

The investment contract with Nice & Green SA aims at supporting working capital of the Company, strengthening its financial structure, and broadening the shareholder structure. The capital raised from the N&G transaction will equip Itway with additional capital and financial resources that will be used to accelerate the development of the Company’s growth and investment strategies in the market segments in which the Company operates without any additional burden for the Company. The Program foresees an issuance period for an overall 36 months from the date of signature of the contract and comprises:

(i) A tranche of warrants to buy up to Euro 500 thousand own shares of Itway already in its portfolio (the Warrants);

(ii) 11 tranches of bonds, each with a nominal value of Euro 500 thousand convertible into newly issued Itway shares (Bonds). It envisages the commitment by N&G to subscribe to several tranches following a specific request from Itway

The contract foresees that the loan will be non-interest bearing and that each Bond will have a 12-month duration from the issue date. Furthermore, in case of failure to request the repayment by the maturity date, the Company shall be obliged to automatically convert the Bonds in circulation into newly issued shares. The Investor is entitled to ask for the conversion of the bonds into shares at any time following the conversion request. Upon conversion request, the Issuer, instead of issuing new shares, shall have the option to repay the Bonds in cash. The Bonds are non-interest bearing and will not be listed on any regulated market. To execute the Bond issuance program, an extraordinary shareholders’ meeting took place on October 30, 2020, that deliberated the issue of bonds and a capital increase without option rights to service the conversion. To the date of writing of the current Report, the company entirely exercised the warrant during the 2020 financial year, using shares that it already held in its portfolio, while of the 11 tranches of Bonds, on December 15, 2020, one tranche (comprising 50 Bonds with a nominal value of Euro 10 thousand each) was issued and underwritten, upon request of the Company, and partially exercised by Nice&Green SA through the request to convert, in February 2021, No. 20 bonds for an overall value of Euro 200 thousand. The number of shares that are subject to the conversion was determined conforming to the terms of the Contract based on 91% of the minimum price (defined as the volume-weighted average price - VWAP) recorded in the eight trading days before the date of the conversion request and totalled No. 286,286 newly issued ordinary shares of Itway, with regular dividend rights, representing 3.49% of share capital after the capital increase.

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

31

As of December 31, 2020, the Itway Group had a current net financial indebtedness of approximately Euro 3.4 million, of which Euro 1.3 million already expired at the date of the financial statements, an expired indebtedness with tax and social security bodies for a total of Euro 475 thousand (that will be paid within the terms foreseen by regulations in force), and expired indebtedness towards suppliers of Euro 2.7 million (of which approximately Euro 0.8 million for amounts being contested, also through legal means and Euro 1.8 million of suppliers no longer present on the market but that for prudential reasons are still booked in the balance sheet).

After the agreement reached with Mercatoria described above, to date negotiations are still underway with financial institutions or companies (art. 115 of TULPS) that acquired debt from certain banks for smaller amounts. The Company deems it reasonable to be able to conclude these negotiations, according to the plan, on the repayment terms.

Based on the 2020-2023 Industrial and Financial Plan approved by the Board of Directors, that an independent legal expert certified pursuant to article 67, paragraph 3, letter d) of the Bankruptcy Law, confirming the truthfulness of the corporate data and the feasibility of the plan as well as its conformity in pursuing the objectives of recovery and rebalancing the Company’s financial and capital position, the Directors, also comforted by the positive results achieved in these past years, drafted the financial statements on a going concern basis.

ACCOUNTING PRINCIPLES General principles In the consolidated Financial Statements and in the comparative data the Group adopted the International Reporting Standards (IFRS) issued by IASB, the updates of those pre-existing (IAS) as well as the International Financial Reporting Interpretations Committee (IFRIC) and those issued by the Standing Interpretation Committee (SIC), that were deemed as applicable to the transactions carried out by the Group. The Financial Statements items were assessed based on an accrual basis. For the purpose of book entries, prevalence was given to the economic substance of transactions rather than their legal form.

The accounting principles adopted are consistent and, as those adopted in the drafting of the consolidated Financial Statements as of December 31, 2019, except the new accounting principles that entered into force in the current fiscal year, as better described hereinafter. These principles require estimates that, in the context of the current economic uncertainty, have for their own component of risk and uncertainty. Therefore, it cannot be ruled out that in the near future the results achieved could be different from those forecast, therefore requiring revisions that today cannot be either estimated or forecast.

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

32

Presentation of the Financial Statements For a better reading, the presentation of the consolidated financial statement, the consolidated income statement, the consolidated statement of comprehensive income, the consolidated statement of changes in financial position, the consolidated statement of changes in net equity and the data inserted in the notes are all expressed in thousands of Euro, unless otherwise indicated. In some cases the tables could be rounded down due to the fact they are expressed in thousands of Euro. The Financial Statements are drafted in the following way:

� In the financial statement, current and non-current assets are reported separately. The consolidated financial statement as at December 31, 2020 was compared with the balances of the previous fiscal year, which ended on December 31, 2019

� In the income statement, the representation of the costs is carried out on the basis of their own

nature. The income statement on December 31, 2020 was compared with that of the previous fiscal year;

� The consolidated statement of comprehensive income acknowledges those changes to net equity which, not being pertinent to the transactions with shareholders, do not have an impact on the result of the fiscal year;

� The indirect method was used for the consolidated statement of changes in financial position;

� EBITDA (gross operating result) is an economic indicator not defined in the International

Accounting Standards and does not have to be considered an alternative measure to assess the performance of the operating results. Ebitda is used by the management of the Company to monitor and assess the operational performance of the Company and of the Group. Management considers Ebitda an important parameter to measure the performance of the Group, as it is not impacted by the volatility generated by the different criteria used to determine taxable income, by the amount and the characteristics of employed capital as well as the related amortization and depreciation policies. Ebitda is defined as Profit/Loss before amortizations of material and immaterial assets, financial charges and income and income taxes. Since the composition of Ebitda is not regulated by the reference accounting principles, the criteria to determine here applied may not be homogeneous with that adopted by other entities and therefore not be comparable;

� EBIT (operating Result) is an economic indicator not defined in the International Accounting

Standards and does not have to be considered an alternative measure to assess the performance of the operating results. It is defined as the Profit/Loss net of depreciation of material and immaterial assets and before financial charges and proceeds and income taxes. Since the composition of Ebit is not regulated by the reference accounting principles, the criteria to determine here applied may not be homogeneous with that adopted by other entities and therefore not be comparable.

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

33

Consolidation criteria The Financial Statements include the Financial Statements of the parent company and of the companies that it controls as of December 31, 2020, approved by the respective Board of Directors with the opportune adjustments, where necessary, to make them consistent with the accounting principles of the parent company. The full consolidation method can be summarized as indicated later. The accounting data of the subsidiaries purchased by the Group are booked with the acquisition method according to what was established by IFRS 3 “Business Combinations”:

� Assets and liabilities are measured at their acquisition-date fair value at the date of their purchase; � The excess of cost of the acquisition, respect to the fair value of the stake attributable to the Group in

net assets of the company purchased is booked as goodwill. Such goodwill, as detailed subsequently, is periodically, at least once every fiscal year, reviewed to check if it can be recovered through future cash flows generated from the underlying investment. The higher values of the acquired assets and liabilities, since booked at the fair value on the date of their purchase, compared with values recognized for fiscal purposes, are considered for the purpose of deferred taxes. Profits and losses deriving from transaction between subsidiaries that have not yet been carried out on behalf of third parties, and the credits and debts, costs, revenues among consolidated companies were eliminated. Consolidation of foreign companies with exchange rates other than the Euro The balances of the foreign subsidiary Itway Turkiye expressed in Turkish lira are converted into Euro applying the end-period exchange rate for assets and liabilities. For the conversion of the income statement items the average exchange rate of the period is used. The differences in exchange rate emerging from the conversion are booked to the translation reserve of the consolidated income statement. Following are the exchange rates used for the conversion in Euro of the values of the company of the Group outside the Euro area: December 31, 2020 December 31, 2019 Avg. Punctual Avg. Punctual New Turkish Lira 8.0547 9.1131 6.3578 6.6843

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

34

Consolidation area The consolidated Financial Statements of the Itway Group include the results of the parent company Itway S.p.A and the companies it controls. Following is a list of companies consolidated with the full consolidation method:

NAME HEADQUARTERS SHARE CAPITAL

EURO

% Direct ownership

% Indirect ownership

% Total ownership

Itway Iberica S.L.

Argenters 2, Cerdanyola del Vallès, Barcelona

560,040

100%

-

100%

Itway France S.A.S.

4,Avenue Cely – Asniere Sur Seine, Cedex

100,000

100%

-

100%

Itway Hellas S.A.

Agiou Ioannou Str , 10 Halandri, Athens

846,368

-

100%

100%

Itway Turkiye Ltd.

Eski Uscudar Yolu NO. 8/18, Istanbul

1,500,000 *

-

100%

100%

iNebula S.r.l. in liquidation

Via A. Papa, 30, Milan

10,000

75%

-

75%

Itway RE S.r.l.

Via L. Braille 15, Ravenna

10,000

100%

-

100%

4Science S.r.l.

Via A. Papa, 30, Milan

10,000

100%

-

100%

* The value is expressed in the New Turkish Lira (YTL) For the sake of completeness, please note that Itway S.p.A. also owns 100% of Itway International S.r.l. (that has a share capital of Euro 10 thousand), which, in turn, has full ownership of Itway Hellas and Itway Turkyie. Itway International S.r.l. was constituted as a vehicle for the sale of these foreign subsidiaries, upon conferral of their respective stakes, based on agreements with Cyber 1 AB, which subsequently lapsed as extensively described hereinafter. Hence, this reorganization qualifies as business combinations under common control pursuant to paragraph B1 of IFRS 3 and, therefore, the acquisition method under IFRS 3 is not applicable to book business combinations. This transaction did not change the perimeter of the Group, intended as a group of entities subject to the control of Itway. The consolidation process was conducted by neutralizing the effects of the corporate reorganization, which took place only formally, as indicated above. Also, Itway International is a pure holding company that does not have any operating activity and did not carry out any management transactions, if not ownership of the two foreign companies. The net equity and the net result of Itway International are insignificant, excluding the value of the shareholdings included in its assets. The following associates are valued with the net equity method: NAME HEADQUARTERS SHARE

CAPITAL Euro % direct

ownership

BE Innova S.r.l. Via Cesare Battisti 26, Trento 20,000 50% BE Infrastrutture S.r.l.

Via Trieste, 76, Ravenna

100,000 30%

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

35

Following are the minority interests valued at a cost basis since there is no quoted market price on an active market available and the fair value cannot be determined in a reliable way:

NAME HEADQUARTERS SHARE

CAPITAL Euro

% direct ownership

Serendipity Energia S.p.A. Piazza Bernini 2 – Ravenna 1,117,758 10.5%

Dexit S.r.l.

Via G. Gilli 2 – Trento

700,000

9% Idrolab S.r.l. Via dell’Arrigoni, 220 – Cesena (FC) 52,500 10%

Itway MENA FZC PO Box 53314, HFZ, Sharjah, United Arab Emirates 35,000*

17.1%

* The value is expressed in Dirham of the United Arab Emirates (AED) Use of estimates The drafting of the consolidated Financial Statements, applying IFRS principles, requires making estimates and assumptions that affect the value of assets and liabilities and information regarding potential assets and liabilities to the reference date. The estimates and assumptions are based on historical experience and on other factors that are considered to be relevant; the estimates and assumptions are reviewed periodically and the effects of each variation are reflected in the consolidated statement. Following are the balance sheet items that require greater subjectivity from directors in elaborating forecasts and for which a change in the conditions of the underlying assumptions used can have a significant impact on the financial statements. � assessment on shareholdings; � assessment on inventories; � assessment on the allowance for doubtful accounts; � assessment on deferred tax assets; � assessment on employee benefits; � assessment of the provision for risks and charges. Estimates and hypothesis are reviewed periodically and the impact of each variation is immediately reflected in the income statement of the fiscal year. Goodwill is mainly referred to the Itway Hellas Cash Generating Unit (CGU). The Group adopted the methodology described in the Note on Impairment to verify whether there was a loss of value of the goodwill booked in the balance sheet. The recoverable value was determined based on the calculation of the value in use. The cash flows of the cash-generating units to which goodwill is attributed were inferred from the Business Plan approved by the Board of Directors. A weighted average cost of capital (WACC) of 15.02% was punctually calculated as the discount rate, in line with previous fiscal years and with a focus on risk factors and uncertainties related to the current market. Sensitivity analyses on this rate were carried out considering changes in interest rates and other financial parameters (WACC, g rate, Ebitda of the terminal value). The assessment of the eventual loss of the value of assets (goodwill), the conclusion of which is in Note 12 “Goodwill”, was carried out with reference to December 31, 2020.

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

36

Following is the summary of the valuation processes and the estimate/assumptions deemed receptive, should the forecasted events not take place, in full or in part, of producing significant effects on the economic and financial situation of the Itway Group. Property, plant and equipment Tangible assets are recognized at cost including accessory charges net of the relative accumulated depreciation. Ordinary maintenance expenses are fully charged to the income statement. Costs for improvements, modernization and transformations of an enhancing nature are accounted as assets. The accounting value of tangible assets is subject to review in order to detect possible losses in value either annually or when events or changes in the situation indicate that the carrying value can no longer be recovered (for details please seen paragraph “loss of value – impairment”). Depreciation begins when assets are ready to be used. Property, plants, and equipment are systematically depreciated each year based on economic-technical rates considered to be representative of the residual possibility of using the assets. Goods made up of components, of significant amounts, with different useful lives are considered separately when determining depreciation Depreciation is calculated on a straight basis, as a function of the expected useful lives and of the relative assets, periodically reviewed if necessary, applying the following percentage rates:

Plants 2% Furniture 12% Computers and electronic office equipment 20% Vehicles 25% Electronic telephone systems 20%

Profits and losses deriving from the sale or dismissal of assets are determined as a difference between revenue and the net book value of the asset and are booked in the income statement, respectively in other operating revenues and other operating expenses. Leasing Starting from January 1, 2019, following the first application of IFRS 16 – ‘Leases”, the Group recognizes for all leasing contracts, except short term ones, therefore within 12 months, and low-value ones, a right of use at the lease commencement date that corresponds to the date in which the underlying asset is available for use. The lease fee related to short-term contracts and low-value ones are booked as cost in the income statement throughout the lease term. The right of use is booked at cost, net of accrued depreciation and loss of value (impairment loss) and adjusted following each re-measurement of the lease liability. The value assigned to the right of use corresponds to the amount of the lease liability and it is amortized on a straight-line basis over the estimated useful life, or the term, of the contract, if lower. The financial lease liability is

_________________________________________________________________________________________________ Consolidated Financial Statements as of December 31, 2020

37