consolidated financial report - … · financial report 3 corporate ... sunrise over the south gobi...

TRANSCRIPT

CONSOLIDATED FINANCIAL REPORT

HALF YEAR ENDED31 DECEMBER 2016

TERRACOM RESOURCES

CONTENTS

FINANCIAL REPORT

3 Corporate Information

4-9 Directors’ Report

10 Auditor’s Independence Declaration

11 Interim Consolidated Statement of Comprehensive Income

12 Interim Consolidated Statement of Financial Position

13 Interim Consolidated Statement of Changes in Equity

14 Interim Consolidated Statement of Cash Flows

15-31 Notes to the Financial Statements

32 Directors’ Declaration

33-34 Auditor’s Review Report

ON THE COVER

Sunrise over the South Gobi Desert, Mongolia.

TerraCom’s Mongolian subsidiary Terra Energy, controls

both coking coal and thermal coal tenements located

in the coal bearing basins of the South and Middle Gobi.

TERRACOM RESOURCESCORPORATE DIRECTORY

PEOPLE

DIRECTORSCameron McRaeCraig WallaceMichael AveryDavid StoneTsogt TogooJames SoorleyPhilip Forrest

COMPANY SECRETARYNathan Boom

CORPORATE INFORMATION

REGISTERED OFFICE 34 Hewitts AvenueThirroul New South Wales 2515Telephone: +61 2 4268 6258

INTERNET ADDRESSwww.terracomresources.com

COUNTRY OF INCORPORATIONAustralia

AUSTRALIAN BUSINESS NUMBERABN 35 143 533 537

STOCK EXCHANGE LISTINGAustralian Securities Exchange LtdASX Code : TER

SERVICE PROVIDERS

SHARE REGISTRYLink Market Services LimitedLevel 12, 680 George StreetSydney NSW 2000Australia

SOLICITORSHerbert Smith Freehills101 Collins StreetMelbourne Victoria 3000Australia

BANKERSWestpac Banking Corporation LtdShop 6, 270 Princes HighwayCorrimal, New South Wales, 2518Australia

AUDITORSErnst & Young200 George StreetSydney, New South Wales, 2000Australia

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

4

Directors Report The directors present their report, together with the interim financial statements of The Group, being TerraCom Limited (the Company) and its controlled entities, for the half year ended 31 December 2016. Directors The names of the Company’s directors in office during the half-year and until the date of this report are set out below. Directors were in office for this entire period unless otherwise stated. Names Mr Cameron McRae (Executive Chairman) The Hon. Craig Wallace Mr Michael Avery Mr David Stone Mr Tsogt Togoo Mr Philip Forrest Mr James (Jim) Soorley (appointed 8 March 2017) Ms Loo Hwee Fang (resigned 8 March 2017)

Results of operations The consolidated comprehensive loss of the Group for the financial period after providing for income tax was $28.539 million (2015: $71.448 million).

Results of financial performance Before analysing the operating performance of the Group for the half year ended 31 December 2016 it is important to outline the following highlights during the period and subsequent to period end.

During the 6 month period to 31 December 2016 the Group has achieved the following: Mongolia

i. Executed binding long form definitive offtake agreements with a wholly owned subsidiary of the Kingho Group, one of the largest private coal companies in China, for a 5.5 year offtake of hard coking coal (HCC) produced from the BNU Coal Mine.

ii. Recommenced mining activities at its BNU North mining operation following the suspension of production to optimise the supply and washing chain in country.

Australia – Blair Athol

i. Executed a binding Sale and Purchase Agreement (SPA) to acquire the Blair Athol Coal Mine in Queensland, with the only conditions outstanding relating to government regulatory approvals. The Blair Athol Mine provides the Group with an established mining operation that can also be used as a regional hub in Queensland to support the Company’s expansion plans.

ii. Secured funding for ongoing working capital at the Blair Athol mine. Funding includes a US$12.000 million facility

in 2 tranches – US$3.000 million was triggered on execution of the Sale and Purchase Agreement and the remaining US$9.000 million will be eligible for draw down in stages upon completion of milestones associated with the Blair Athol coal mine. This facility is secured against the Blair Athol inventory stockpile.

iii. Executed a contract with Link Mining Pty Ltd for a full service mining contract at the Blair Athol coal mine. The

agreement is for 5 years and will cover all operational aspects. A key element of this contract is the provision, through Link Mining, of a AU$11.600 million working capital facility with AU$4.100 million to be utilised for general working capital requirements and A$7.500 million for upfront recommencement mining and beneficiation costs. The provision of the funding has resulted in Link Mining funding all material mining and beneficiation recommencement costs.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

5

Directors Report (continued) Corporate

i. Continued to work closely with various financiers and secured four equity placements for AU$4.000 million, AU$1.342 million, AU$1.144 million and US$0.954 million.

ii. Engaged Foster Stockbroking Pty Ltd to provide corporate advisory and capital market services in Australia, including the preparation of institutional research coverage on TerraCom.

Subsequent to 31 December 2016 the following significant milestones were also achieved by the Group: Australia – Blair Athol

i. On 20 February 2017 the Company announced that the Queensland Government (Department of Natural Resources and Mines) provided formal Indicative Approval for the transfer of the mining lease for the Blair Athol Coal Mine, Central Queensland. The approval is subject to certain conditions relating to infrastructure access and financial securities. TerraCom has advised the Queensland Government that it can meet the conditions, which the TerraCom Board does not believe are onerous. TerraCom is expediting the satisfaction of these conditions to enable completion of title transfer and commencement of mining and rehabilitation activities at Blair Athol Mine within the second quarter of 2017.

Mongolia

i. On 25 January 2017 the Company announced that coal production had recommenced at its BNU North operation 10 days ahead of schedule, in preparation to supply the product for the recently executed offtake agreement for sales of hard coking coal (HCC) to the Kingho Group. Additionally, the first 100% USD Irrevocable Letter of Credit (LC) was received for sales of January / February 2017 hard coking coal production tonnes from the BNU coal mine.

ii. On 9 February 2017 the Company announced that coal delivery will begin to Kingho from 10th February, when

the Mongolia/Chinese Border re-opened following Chinese New Year.

iii. On 9 February TerraCom announced that following on from the BNU on site CHPP feasibility study being approved by Mineral Professional Council (MPC) in December 2016, the Company has received the Final Resolution of the Chairman of the MPC Meeting.

Income Statement Analysis

The consolidated comprehensive loss of the Group for the financial period after providing for income tax was $28.539 million (2015: $71.448 million). A range of factors have impacted the result:

Finance costs of $14.598 million (2015: $15.998 million), represent 51% of the comprehensive loss.

During the period the Group recorded and accrued finance costs with respect to the Listed Bond and Super Senior Notes facilities. These finance costs include interest not payable until 30 June 2017 and amortisation of Bond. The Group has the option to capitalise 50% of the accrued interest due and payable to the outstanding principal sum of each ordinary note and make repayments in June 2021 with the principal bullet payment.

Mongolian alternate supply chain implementation expenses $4.753 million (2015: $nil), which represents 17% of the comprehensive loss.

During the period the Mongolia Business Unit incurred costs to maintain the workforce and operations while undertaking the implementation of an alternate supply chain. This culminated in the execution of a 5.5 year, 7.5 million tonnes offtake with Kingho with prices linked to seaborne export markets.

Share Based Payment expense of $2.713 million (2015: $nil), which represents 10% of the comprehensive loss.

At the Company’s AGM held on 30 November 2016 shareholders approved a $600,000 sign-on bonus (fully paid ordinary shares for nil consideration) to Cameron McRae, through the Executive Chairman Consultancy Agreement with Tarva Investment and Advisory LLC a company which he controls, with a conditions precedent that shareholder approval be obtained before granting the bonus. At the time of agreeing this bonus with, the average VWAP of TerraCom’s shares were $0.008183 which entitled Mr McRae to 73,813,740 fully paid ordinary shares for nil consideration. For accounting standard purposes a share based payment expense of $2,712,793 was recognised in the profit and loss statement for the 6 months ended 31 December 2016 as the grant date for the shares was not until 30 November 2016 (the date shareholder approval was obtained) and the fair value of the shares was determined using the market value of the shares as at 30 November 2016, which was $0.037 per fully paid ordinary share. As at 31 December 2016 these shares have not yet been issued to Tarva.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

6

Directors Report (continued)

Net Asset Analysis

The total net assets of the Group as at 31 December 2016 was a deficit of $36.085 million. This represents an increase in deficiency of $18.434 million when compared to the net assets of the Group as at 30 June 2016.

The key contributors to the decline in the net assets of the Group related primarily to finance costs during the period.

Functional Currency

Effective 1 July 2016, the Company changed functional currencies from Australian Dollars (AUD) and Mongolian Tugrik (MNT) to United States Dollars (USD) for the parent entity and the Mongolian subsidiaries. The change in functional currency has been accounted for prospectively from the date of change, whilst the presentation currency of the Group currently remains AUD.

The successful completion of the USD offtake agreement with Kingho in Mongolia, and the progress made on the Blair Athol acquisition were the key triggers for this change, as it was determined that USD is now the currency which mainly influences sales prices, labour, material and other costs of producing and selling coal.

Review of operations

Mongolia

i. Operations BNU operations recommenced on 18 November 2016 after an extensive induction and equipment competency training process. Mine planning and operations is well advanced and focused on meeting the initial requirements of the 5.5-year offtake agreement with Kingho Group. Wagner Asia mobilised a full fleet of Caterpillar equipment in support of BNU operations and will manage heavy equipment maintenance going forward. Site infrastructure has been upgraded after the standby period and all is ready to support mining production.

ii. Safety The BNU site maintained its LTI free status over 1.72 million hours.

iii. Production Production focused on recommencement of mining activities and the removal of overburden to expose HCC. The 6 months ended 31 December 2016 production is as follows:

Rom coal production (tonnes) 0

Overburden removed (BCM) 288,012

EOM ROM Stocks (tonnes) 41,007

Australia i. Blair Athol The Company has progressed the Blair Athol Mine acquisition substantially over the period. This culminated in the Company being awarded an Indicative Approval subsequent to the reporting period. On 20 February 2017 the Company announced that the Queensland Government (Department of Natural Resources and Mines) provided formal Indicative Approval for the transfer of the mining lease for the Blair Athol Coal Mine, Central Queensland. The approval is subject to certain conditions relating to infrastructure access and financial securities. TerraCom has advised the Queensland Government that it can meet the conditions, which the TerraCom Board does not believe are onerous. TerraCom is expediting the satisfaction of these conditions to enable completion of title transfer and commencement of mining and rehabilitation activities at Blair Athol Mine within the second quarter 2017.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

7

Directors Report (continued) ii. Queensland Exploration Tenements A focus on cost conservation on projects as a result of the 2015 Strategic Review has restricted exploration for the reporting period. The North Galilee and Springsure Project remains the focus and there have been discussions with potential joint venture or offtake partners to self-fund these projects through the development phase into operating mines. The Company continues to seek investment partners for the next stage of development of its Australian assets.

Dividends Paid or Recommended

No dividends were paid or declared for future payment during the financial period.

Risks Relating to the Group’s Future Prospects

The Company operates in the coal industry in both Mongolia and Australia. There are a number of factors, both specific to the Company and to the coal industry in general, which may, either individually or in combination, affect the future operating and financial performance of the Group, its prospects and/or the value of TerraCom shares. Many of the circumstances giving rise to these risks are beyond the control of the Company’s Directors and its management. The major risks believed to be associated with investment in TerraCom are as follows:

Development Risks

There is a risk that circumstances (including unforeseen circumstances) may cause a delay to project development, exploration milestones or other operating factors, resulting in receipt of revenue at a later date than expected. Additionally, the construction of new projects/expansion by the Company may exceed the currently envisaged timeframe or cost for a variety of reasons outside of the control of the Company.

Country Risks

There is a risk that circumstances (including unforeseen circumstances) in either Mongolia or Australia may cause a delay to project development, exploration milestones or other operating factors, resulting in receipt of revenue at a later date than expected. There is also a risk that a change in laws may impact the viability of the projects.

Financing Risks

To meet ongoing working capital requirements, ongoing interest and principal payments and capital expenditure commitments for the Group’s growth plans, additional funding may be required. If adequate funds are not available on acceptable terms, the Company may be unable to fund its operations and/or any expansion plans.

Competition Risk

The industry in which the Company is involved is subject to domestic and global competition. While the Company will undertake all reasonable due diligence in its business decisions and operations, the Company will have no influence or control over the activities or actions of its competitors, which activities or actions may, positively or negatively, affect the operating and financial performance of the Company’s projects and business.

Resources and Reserves Risk

The future success of the Company will depend on its ability to find or acquire coal reserves that are economically recoverable. There can be no assurance that the Company’s planned exploration activities will result in significant resources or reserves or that it will have success mining coal. Even if the Company is successful in finding or acquiring coal reserves or resources, reserve and resource estimates are estimates only and no assurance can be given that any particular level of recovery from coal resources or reserves will in fact be realised or that an identified coal resource will ever qualify as commercially viable which can be legally and economically exploited. Market fluctuations in the price of coal, as well as increased production costs or reduced recovery rates may render coal reserves and resources containing relatively lower grades of mineralisation uneconomic and may ultimately result in a restatement of reserves and or resources. Short-term operating factors relating to the coal reserves and resources, such as the need for orderly development of the ore bodies and the processing of new or different mineral grades may cause a mining operation to be unprofitable in any particular accounting period and may adversely affect the Company’s profitability. The mining of coal involves a high degree of risk, including that the coal mined may be of a different quality, tonnage or strip ratio from that estimated.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

8

Directors Report (continued)

Exploration and Evaluation Risk

Mineral exploration and development are high risk undertakings. While the Company has attempted to reduce this risk by selecting projects that have identified prospective mineral targets, there is still no guarantee of success. Even if an apparently viable deposit is identified, there is no guarantee that it can be economically exploited. The Company’s exploration and appraisal activities are dependent upon the grant and maintenance of appropriate licences, permits, resource consents, access arrangements and regulatory authorities (authorisations) which may not be granted or may be withdrawn or made subject to limitations. Although the authorisations may be renewed following expiry or granting (as the case may be), there can be no assurance that such authorisations will be renewed or granted on the same terms. There are also risks that there could be delays in obtaining such authorisations. If the Company does not meet its work and/or expenditure obligations under its authorisations, this may lead to dilution of its interest in, or the loss of such authorisations. The business of commodity development and production involves a degree of risk. Amongst other factors, success is dependent on successful design, construction and operation of efficient gathering, processing and transportation facilities. Even if the Company discovers or recovers potentially commercial quantities of coal from its exploration activities, there is no guarantee that the Company will be able to successfully transport these resources to commercially viable markets or sell the resources to customers to achieve a commercial return.

Operational Risk

If the Company decides to develop and commission a mine, the operations of the Company including mining and processing may be affected by a range of factors. These include failure to achieve predicted grade in exploration, mining and processing, technical difficulties encountered in commissioning an operating plant and equipment, mechanical failure, metallurgical problems which affect extraction rates and costs, adverse weather conditions, industrial and environmental accidents, industrial disputes, unexpected shortages or increase in the costs of consumables, spare parts, plant and equipment.

Environmental Risk

The Company’s projects are subject to laws and regulations regarding environmental matters. Many of the activities and operations of the Company cannot be carried out without prior approval from and compliance with all relevant authorities. The Company intends to conduct its activities in an environmentally responsible manner and in accordance with all applicable laws. However, the Company could be subject to liability due to risks inherent to its activities, such as groundwater contamination, subsidence, accidental spills, leakages or other unforeseen circumstances. As at the date of signing this report, the Company has not breached any environmental laws in jurisdictions in which it operates during the financial year and up to the date of signing this report.

Market Risks

The Company’s plans for any revenue are to be derived mainly from the sale of coal and/or coal products. Consequently, the Company’s financial position, operating results and future growth will closely depend on the market price of each of these commodities. Market prices of coal products are subject to large fluctuations in response to changes in demand and/or supply and various other factors. These changes can be the result of uncertainty or several industry and macroeconomic factors beyond the control of the Company, including political instability, governmental regulation, forward selling by producers, climate, inflation, interest rates and currency exchange rates. If market prices of the commodities sold by the Company were to fall below production costs for these products and remain at that level for a sustained period of time, the Company would be likely to experience losses, having a material adverse effect on the Company.

Key Management Personnel Risk

If TerraCom is unable to attract and retain qualified employees, loses key personnel, fails to integrate replacement personnel successfully, or fails to manage its employee base effectively, it may be unable to support or maintain its current activities, effectively expand its business, or otherwise maintain or increase its revenues.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 20169

Directors Report (continued)

Events Subsequent to Reporting Date

i. On 25 January 2017 the Company announced that coal production had recommenced at its BNU North operation 10 days ahead of schedule, in preparation to supply the product for the recently executed offtake agreement forsales of hard coking coal (HCC) to the Kingho Group. Additionally, the first 100% USD Irrevocable Letter ofCredit (LC) was received for sales of January / February 2017 hard coking coal production tonnes from the BNUcoal mine.

ii. On 9 February 2017 TerraCom announced that following on from the BNU on site CHPP feasibility study beingapproved by Mineral Professional Council (MPC) in December 2016, the Company received the Final Resolution of the Chairman of the MPC Meeting.

iii. On 20 February 2017 TerraCom announced its wholly owned and operated subsidiary, Orion Mining Pty Limited,had received formal Indicative Approval from the Queensland Government Department of Natural Resourcesand Mines for the transfer of the mining lease for the Blair Athol Coal Mine, Central Queensland. The Conditionswith respect to the Indicative Approval were in line with the announcement made on 1 February.

iv. TerraCom announced the appointment of James (Jim) Soorley to the TerraCom Limited and Orion Mining PtyLimited board of directors, as well as the resignation of Hwee Fang Loo from the TerraCom board of directors.Both of these were effective from 8 March 2017.

Except for the above, no other matters or circumstances have arisen since the end of the financial period which significantly affected or could significantly affect the operations of the Group, the results of those operations or the state of affairs of the Group in future financial years.

Auditor’s Independence Declaration

The auditor's independence declaration in accordance with section 307C of the Corporations Act 2001, for the half year ended 31 December 2016 has been received and can be found on the proceeding page of the interim financial report.

This director's report is signed in accordance with a resolution of the Board of Directors.

..................................

Mr Cameron McRae Executive Chairman 16 March 2017

A member firm of Ernst & Young Global LimitedLiability limited by a scheme approved under Professional Standards Legislation

Ernst & Young200 George StreetSydney NSW 2000 AustraliaGPO Box 2646 Sydney NSW 2001

Tel: +61 2 9248 5555Fax: +61 2 9248 5959ey.com/au

.

Auditor’s Independence Declaration to the Directors of TerraComLimited

As lead auditor for the review of TerraCom Limited for the half-year ended 31 December 2016, I declareto the best of my knowledge and belief, there have been:

a) no contraventions of the auditor independence requirements of the Corporations Act 2001 inrelation to the review; and

b) no contraventions of any applicable code of professional conduct in relation to the review.

This declaration is in respect of TerraCom Limited and the entities it controlled during the financialperiod.

Ernst & Young

Anthony JonesPartner16 March 2017

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

11

Interim Consolidated Statement of Profit and Loss and Other Comprehensive Income For the six months ended 31 December

2016 2015

AUD AUD

Sales 2 - 6,796,634 Costs of sales 3 - (9,008,642)

Gross profit - (2,212,008) Other income 2 2,508 5,686 Employee benefits expense 3 (4,839,100) (1,602,829) Depreciation and amortisation expense (276,757) (3,141,681) Marketing fees (164,330) (1,067,336) Rent expense (321,955) (366,995) Consulting fees 3 (2,680,765) (2,506,997) Travel expense (408,095) (379,936) Impairment losses 3 - (36,808,252) Other operating expenses 3 (5,576,211) (2,659,344) Finance costs 3 (14,597,619) (15,997,989) Foreign currency loss (166,562) (7,233,005) Share of loss of associates (3,454) (1,974)

Loss for the period before income tax (29,032,340) (73,972,660) Income tax benefit/(expense) - (208)

Loss for the period from continuing operations (29,032,340) (73,972,868)

Other comprehensive income, net of income tax Items that will be reclassified to profit or loss when specific conditions are met Exchange differences on translating foreign controlled entities 493,543 2,524,525 Other comprehensive (loss)/income for the period, net of tax 493,543 2,524,525

Total comprehensive loss for the period (28,538,797) (71,448,343)

Loss for the period attributable to: Members of the parent entity (28,964,514) (73,618,240) Non-controlling interest (67,826) (354,628)

Total loss (29,032,340) (73,972,868)

Total comprehensive loss attributable to: Members of the parent entity (28,435,829) (71,029,879) Non-controlling interest (102,968) (418,464)

Total comprehensive loss (28,538,797) (71,448,343) Earnings Per Share (EPS): Basic earnings/ (loss) per share (cents) (1.14) (6.72) Diluted earnings/ (loss) per share (cents) (1.14) (6.72)

The accompanying notes form part of these financial statements.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

12

Interim Consolidated Statement of Financial Position As at

The accompanying notes form part of these financial statements.

31 December

2016 30 June

2016 AUD AUD

ASSETS CURRENT ASSETS Cash and cash equivalents 1,218,235 1,199,183 Inventory 631,186 539,220 Trade and other receivables 219,755 201,407 Other assets 1,004,491 470,073 TOTAL CURRENT ASSETS 3,073,667 2,409,883 NON-CURRENT ASSETS Trade and other receivables 6,554,836 8,077,393 Other assets 1,106,665 2,125,927 Property, plant and equipment 5 118,100,775 115,197,021 Investment in associate 1,318,149 1,386,455 Intangible assets 852,144 761,860 Exploration and evaluation assets 6 49,743,977 49,351,960 TOTAL NON-CURRENT ASSETS 177,676,546 176,900,616 TOTAL ASSETS 180,750,213 179,310,499 LIABILITIES CURRENT LIABILITIES Trade and other payables 14,868,625 26,915,749 Short-term provisions 277,684 262,938 Borrowings 7 45,271,331 27,657,970 TOTAL CURRENT LIABILITIES 60,417,640 54,836,657 NON-CURRENT LIABILITIES Trade and other payables 8,181,036 - Borrowings 7 139,389,124 133,547,849 Long-term provision 759,660 696,190 Other financial liabilities 8 8,087,376 7,880,454 TOTAL NON-CURRENT LIABILITIES 156,417,196 142,124,493 TOTAL LIABILITIES 216,834,836 196,961,150 NET ASSETS (36,084,623) (17,650,651) EQUITY Issued capital 9 202,516,386 195,276,818 Reserves (29,470,981) (32,864,923) Retained earnings (213,305,554) (184,341,040) Total equity attributable to equity holders of the Company (40,260,149) (21,929,145) Non-controlling interest 4,175,526 4,278,494 TOTAL EQUITY (36,084,623) (17,650,651)

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

13

Interim Consolidated Statement of Changes In Equity For the six months ended 31 December 2016

Note Issued capital Accumulated

losses Acquisition

reserve

Foreign currency

translation reserve

Share based payments/Option

reserve

Total attributable to Equity holders

of the Company

Non-controlling interests Total

$ $ $ $ $ $ $ $

Balance at 1 July 2016 195,276,818 (184,341,040) (36,684,681) (4,139,090) 7,958,848 (21,929,145) 4,278,494 (17,650,651) (Loss) attributable to equity holders of the Company - (28,964,514) - - - (28,964,514) - (28,964,514) (Loss) attributable to non-controlling interests - - - - - - (67,826) (67,826) Other comprehensive income for the half year - - - 528,685 - 528,685 (35,142) 493,543

Unlisted options - - - - 152,464 152,464 - 152,464

Employee share based payment - - - - 2,712,793 2,712,793 - 2,712,793

Issue of share capital (note 9) 7,239,568 - - - - 7,239,568 - 7,239,568

Balance at 31 December 2016 202,516,386 (213,305,554) (36,684,681) (3,610,405) 10,824,105 (40,260,149) 4,175,526 (36,084,623)

Note Issued capital

Accumulated losses

Acquisition reserve

Foreign currency

translation reserve

Share based payments/Option

reserve

Total attributable to Equity holders

of the Company

Non-controlling interests Total

$ $ $ $ $ $ $ $

Balance at 1 July 2015 186,354,850 (132,933,210) (36,684,681) (2,864,418) 7,958,847 21,831,388 4,664,159 26,495,547 (Loss) attributable to equity holders of the Company - (73,618,240) - - - (73,618,240) - (73,618,240) (Loss) attributable to non-controlling interests - - - - - - (354,628) (354,628) Other comprehensive income for the half year - - - 2,588,361 - 2,588,361 (63,836) 2,524,525

Balance at 31 December 2015 186,354,850 (206,551,450) (36,684,681) (276,057) 7,958,847 (49,198,491) 4,245,695 (44,952,796)

The accompanying notes form part of these financial statements.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

14

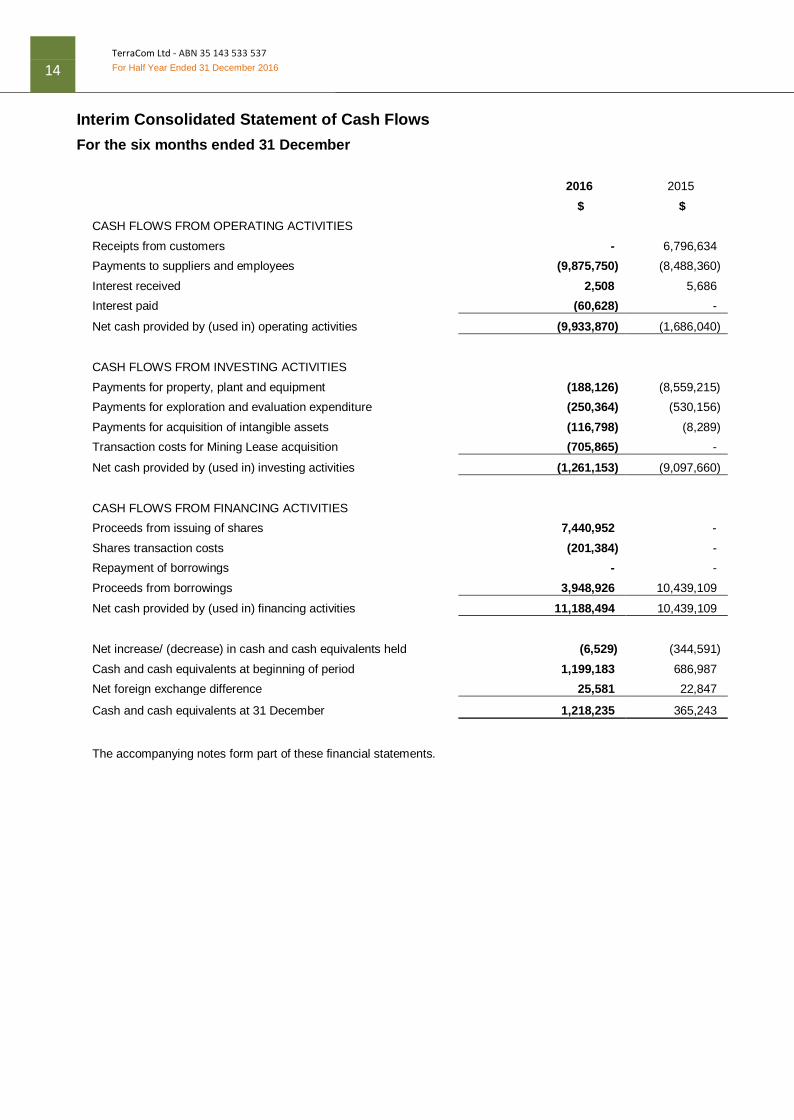

Interim Consolidated Statement of Cash Flows For the six months ended 31 December

2016 2015

$ $ CASH FLOWS FROM OPERATING ACTIVITIES Receipts from customers - 6,796,634 Payments to suppliers and employees (9,875,750) (8,488,360) Interest received 2,508 5,686 Interest paid (60,628) -

Net cash provided by (used in) operating activities (9,933,870) (1,686,040)

CASH FLOWS FROM INVESTING ACTIVITIES Payments for property, plant and equipment (188,126) (8,559,215) Payments for exploration and evaluation expenditure (250,364) (530,156) Payments for acquisition of intangible assets (116,798) (8,289) Transaction costs for Mining Lease acquisition (705,865) -

Net cash provided by (used in) investing activities (1,261,153) (9,097,660)

CASH FLOWS FROM FINANCING ACTIVITIES Proceeds from issuing of shares 7,440,952 - Shares transaction costs (201,384) - Repayment of borrowings - - Proceeds from borrowings 3,948,926 10,439,109

Net cash provided by (used in) financing activities 11,188,494 10,439,109

Net increase/ (decrease) in cash and cash equivalents held (6,529) (344,591) Cash and cash equivalents at beginning of period 1,199,183 686,987 Net foreign exchange difference 25,581 22,847

Cash and cash equivalents at 31 December 1,218,235 365,243

The accompanying notes form part of these financial statements.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

15

Notes to the Financial Statements

For the six months ended 31 December 2016

Note 1 Corporate Information, Basis of Preparation and Changes to the Group’s Accounting Policies

The interim consolidated financial statements of TerraCom Limited (TerraCom) and its subsidiaries (collectively, the Group) for the six months ended 31 December 2016 were authorised for issue in accordance with a resolution of the directors on 16 March 2017.

TerraCom Limited (the Company) is a for profit company limited by shares, incorporated and domiciled in Australia, whose shares are publicly traded. The Group’s principal activities are mine site operations and exploration of tenements.

• Basis of Preparation

These general purpose interim financial statements for the half year reporting period ended 31 December 2016 have been prepared in accordance with requirements of the Corporations Act 2001 and Australian Accounting Standard AASB 134: Interim Financial Reporting. The Group is a for-profit entity for financial reporting purposes under Australian Accounting Standards.

This interim financial report is intended to provide users with an update on the latest interim financial statements of TerraCom Limited and its controlled entities (referred to as the “consolidated group” or “group”). As such, it does not contain information that represents relatively insignificant changes occurring during the half year within the Group. It is therefore recommended that this financial report be read in conjunction with the annual financial statements of the Group for the year ended 30 June 2016, together with any public announcements made during the following half year.

The significant accounting policies used in the preparation and presentation of these interim financial statements are provided below and are consistent with prior reporting periods unless otherwise stated.

Certain comparative figures have been reclassified to conform to the financial statement presentation adopted for the current period.

The interim financial statements have been prepared on an accrual basis and are based on historical costs, except for the measurement at fair value of selected financial assets and financial liabilities.

• Going Concern

The financial report has been prepared on the going concern basis which contemplates the continuity of normal business activities and the realisation of assets and the settlement of liabilities in the ordinary course of business.

As at 31 December 2016, the Group’s current liabilities exceed current assets by $57,343,973 with trade and other payables of $14,868,625 and current debt obligations of $45,271,331. As disclosed in Note 7, the Group has significant debt and interest repayment obligations that fall due on 30 June 2017 and 31 December 2017. In order for the Group to meet these ongoing debt repayment requirements, fund its minimum exploration, development and administrative costs, settle its outstanding trade and other payable obligations and provide the necessary funding to the Group’s operation, to operate as a going concern, the following activities are required:

i. Achievement of profitable mining activities at BNU North;

ii. Receipt of final government approval and successful commencement of profitable mining operations at Blair Athol, including achievement of production milestones agreed under the working capital facility;

iii. Support from debt holders to not call the debt should the Company not meet its interest and principal repayment obligations due and payable at 30 June 2017 and 31 December 2017 for which the Company has no current entitlement to roll into the core debt facilities under the bond agreements and;

iv. Continued co-operation of existing creditors in Mongolia to defer and manage payment obligations for the balances that remain outstanding at 31 December 2016.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

16

Notes to the Financial Statements (continued)

Should the above items not sufficiently fund the obligations of the Company, the Company may be required to raise additional funds through debt, equity or asset sales.

In the event the entity is unable to continue as a going concern it may be required to realise assets and extinguish liabilities at amounts other than those recorded in the financial statements. No adjustments have been made relating to the recoverability and classification of recorded asset amounts and classifications of liabilities that might be necessary should the Parent and Company not continue as a going concern.

The directors believe the going concern basis of presentation is appropriate and, as detailed below, have operating and financing strategies in place to support the presentation of these accounts on this basis. Whilst there remains uncertainty with the execution of those plans the directors believe such actions will be successful and additional funding required can be obtained.

During the 6 month period to 31 December 2016 and subsequent to period end, the Company has:

- Executed a binding Sale and Purchase Agreement (SPA) to acquire the Blair Athol Coal Mine in Queensland, with the only conditions outstanding relating to government regulatory approvals. The Blair Athol Mine will provide the Company with an established mining operation that can also be used as a regional hub in Queensland to support the Company’s expansion plans. In addition, the Company has received indicative approval from the Queensland Government (Department of Natural Resources and Mines) for the transfer of the mining lease for the Blair Athol Coal Mine, Central Queensland. The approval is subject to certain conditions relating to infrastructure access and financial securities that TerraCom has advised the Queensland Government it can meet. TerraCom is working on the satisfaction of these conditions to enable completion of title transfer and commencement of mining and rehabilitation activities at Blair Athol Mine.

Funding of the recommencement of the Blair Athol operations will be sourced from a USD$12.000 million working capital facility triggered on execution of the Sale and Purchase Agreement (US$3.000 million upfront received in October 2016 and a further US$9.000 million on achievement of production milestones). This facility is secured against the Blair Athol inventory stockpile and recourse mechanisms are in place should the government regulatory approvals not be received.

- Executed a contract with Link Mining Pty Ltd for a full service mining contract at the Blair Athol coal mine. The agreement is for 5 years and will cover all operational aspects. A key element of the contract is the provision, through Link Mining, of a AU$11.600 million financing facility for working capital and upfront recommencement and beneficiation costs.

- Continued to work closely with various financiers and secured four equity placements for AUD$4.000 million, AUD$1.100 million, AU$1.000 million and US$1.000 million.

- Executed binding offtake agreements with a wholly owned subsidiary of the Kingho Group, one of the largest private coal companies in China, for a 5.5 year offtake of hard coking coal (HCC) produced from the BNU Coal Mine. As a result, the Company has recommenced coal production at BNU North operation.

- The BNU on site CHPP feasibility study was approved by the Mineral Professional Council (MPC) in December 2016.

The Directors believe that the Group has a strong platform from which to generate operating cash flows and ensure it can continue to raise additional debt or equity to meet its obligations when required and prepare the financial statements on a going concern basis given the:

i. Recommencement of operations at BNU North; and

ii. Acquisition of the Blair Athol coal mine, subsequent commencement of mining operations (subject to regulatory approval) and achievement of the working capital facility production milestones.

• Functional Currency

Effective 1 July 2016, the Company changed functional currencies from Australian Dollars (AUD) and Mongolian Tugrik (MNT) to United States Dollars (USD) for the Parent entity (TerraCom Limited) and the Mongolian subsidiaries (respectively). The change in functional currency has been accounted for prospectively from the date of change.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

17

Notes to the Financial Statements (continued)

The successful completion of the USD offtake agreement with Kingho in Mongolia, and the progress made on the Blair Athol acquisition were the key triggers for this change, as it was determined that USD is now the currency which mainly influences sales prices, labour, material and other costs of producing and selling coal.

The functional currency of the parent is now USD, whilst the presentation currency of the Company is AUD.

• Critical accounting estimates and judgements

The directors evaluate estimates and judgments incorporated into the financial statements based on historical knowledge and best available current information. Estimates assume a reasonable expectation of future events and are based on current trends and economic data, obtained both externally and within the Group.

Key judgments – commercial production start date

The Group assesses the stage of each mine development to determine when a mine moves into the production phase. This being when the mine is substantially complete and ready for its intended use. The criteria used to assess the start date are determined based on the unique nature of each mine development project, such as the complexity of the project and its location. The Group considers various relevant criteria to assess when the production phase is considered to have commenced. Some of the criteria used to identify the production start date include, but are not limited to:

i. Level of capital expenditure incurred compared with the original construction cost estimate; ii. Completion of a reasonable period of testing of the mine plant and equipment; iii. Ability to produce coal in saleable form (within specifications); and iv. Ability to sustain ongoing production of coal.

When a mine development moves into the production phase, the capitalisation of certain mine development ceases and costs are either regarded as forming part of the cost of inventory or expensed, except for costs that qualify for capitalisation relating to mining asset additions or improvements, underground mine development or mineable reserve development. It is also at this point that depreciation/amortisation commences.

Key judgments – exploration and evaluation expenditure

The Group capitalises expenditure relating to exploration and evaluation where it is considered likely to be recoverable or where the activities have not reached a stage which permits a reasonable assessment of the existence of reserves. While there are certain areas of interest from which no reserves have been identified, the directors are of the continued belief that such expenditure should not be written off since limited exploration and evaluation has been conducted to date and further exploration and evaluation activities in these areas is intended and feasibility studies in such areas have not yet concluded. Such capitalised expenditure is carried at the end of the reporting period.

Key estimates – impairment

The Group assesses the recoverable amount of its non-financial assets for impairment whenever there are indicators impairment might exist. When calculating recoverable amount, management makes various estimates and assumptions, including assumptions around recoverable reserves and resources, coal prices and costs of production. In addition management considers any likely transactions to dispose of the assets subject to testing. Actual results may differ from such assumptions.

Key estimates – recoverable reserves and resources

Estimated recoverable reserves and resources are used to determine the depreciation of mine production assets, in accounting for deferred stripping costs and in performing impairment testing. Estimates are prepared by appropriately qualified persons, but will be impacted by forecast commodity prices, exchange rates, production costs and recoveries amongst other factors. Changes in assumptions will impact the carrying value of assets and depreciation and impairment charges recorded in the Statement of Comprehensive Income.

Key estimates – environmental rehabilitation costs

The provisions for rehabilitation costs are based on estimated future costs using information available at the balance sheet date. To the extent the actual costs differ from these estimates, adjustments will be recorded and the income statement may be impacted.

Key judgments – recognition of asset acquisitions

In determining the recognition of asset and business acquisitions, an assessment of the underlying assets and operations of the acquired entity is completed. Where the Group acquires an entity for tenements only, rather than acquiring an operation with clear distinct processes, the acquisition is deemed to be an asset acquisition, rather than a business combination.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

18

Notes to the Financial Statements (continued) Key judgements – valuation of financial liabilities Non-derivative financial liabilities, including the long term borrowings and the special interest component of the long term bond facility, are recorded on initial recognition at fair value. When available, the fair values on initial recognition is measured based on quoted prices in active markets and observable market data. When not available, their fair value is measured with using valuation techniques, including present value income approaches. The inputs to these models are taken from observable markets where possible, but where this is not feasible, a degree of judgement is required in establishing fair values. The assumptions applied in the determination of the valuation of these financial instruments are described in more detail in Note 10.

• Adoption of new and revised accounting standards

The Group has adopted all mandatory new and amended standards and interpretations applicable for the current period. The adoption of these standards and interpretations had no material impact on these financial statements or on the financial position or performance of the Group. The Group has not elected to early adopt any other new Standards or Amendments that are issued but not yet effective.

Note 2 Sales and Other Income

31 December

2016 31 December

2015 $ $

Sales revenue - Coal sales - 6,796,634

Other Income

- Interest Received 2,508 5,686 Note 3 Expenses The following expense items are relevant in explaining the financial performance for the interim period:

31 December

2016 31 December

2015 $ $

Cost of sales - Cost of coal sales - 9,008,642

The Company’s BNU mining operation, in Mongolia, recommenced mining activities on the 18th November 2016 following the implementation of an alternate supply chain strategy and the execution of a 5.5-year offtake agreement with a wholly owned subsidiary of the Kingho Group. No coal sales were recognised for the reporting period as no shipments were made. Finance costs:

- Interest expense on interest bearing loans 60,628 3,685,181 - Interest expense on bond and super senior notes 11,959,979 10,118,726 - Amortisation of bond 2,271,395 - - Interest on Fuel Agreement 305,617 2,194,082 14,597,619 15,997,989

Consulting fees: - Legal fees 989,745 1,061,621 - Project costs and other professional fees 1,691,020 1,445,376 2,680,765 2,506,997

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

19

Notes to the Financial Statements (continued) Employee benefits expense: - Salaries and wages 1,430,674 1,039,506 - Directors' fees 456,979 382,515 - Share based payment (a) 2,712,793 - - Other employee expenses 238,654 180,808 4,839,100 1,602,829

(a) At the Company’s AGM held on 30 November 2016 shareholders approved a $600,000 sign-on bonus (fully paid

ordinary shares for nil consideration) to Cameron McRae, through the Executive Chairman Consultancy Agreement with Tarva Investment and Advisory LLC a company which he controls, with a conditions precedent that shareholder approval be obtained before granting the bonus. At the time of agreeing this bonus, the average VWAP of TerraCom’s shares were $0.008183 which entitled Mr McRae to 73,813,740 fully paid ordinary shares for nil consideration. As at 31 December 2016 these shares have not yet been issued to Tarva.

For accounting standard purposes a share based payment expense of $2,712,793 was recognised in the profit and loss statement for the 6 months ended 31 December 2016 as the grant date for the shares was not until 30 November 2016 (the date shareholder approval was obtained) and the fair value of the shares was determined using the market value of the shares as at 30 November 2016, which was $0.037 per fully paid ordinary share.

Other operating expenses - Listing fees and charges 56,833 37,053 - Mongolian alternate supply chain implementation expenses (a) 4,752,896 2,376,836 - Insurance costs 152,121 62,020 - Other expenses 614,361 183,435

5,576,211 2,659,344

(a) During the period the Mongolia Business Unit incurred costs to maintain the workforce and operations while undertaking the implementation of an alternate supply chain. This culminated in the execution of a 5.5 year, 7.5 million tonnes offtake with Kingho with prices linked to the seaborne coal export market.

Impairment losses - South gobi - 19,701,150 - Mid gobi - 3,746,658 - Australian tenements - 13,360,444

- 36,808,252

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

20

Notes to the Financial Statements (continued)

Types of products and services by reportable segment

The principal products and services of each of these operating segments are as follows:

Segment Activities

Australia Coal exploration and development activities

Mongolia Coal exploration and extraction activities

Note 4 Operating Segments

Identification of reportable segments

The Group has identified its operating segments based on the internal reports that are reviewed and used by the Board of Directors (chief operating decision makers) in assessing performance and determining the allocation of resources. Reportable segments disclosed are based on aggregating operating segments where the segments are considered to have similar economic characteristics and are also similar with respect to the following:

• the products sold and/or services provided by the segment;

• the geographical location of the segment; and

• any external regulatory requirements.

Performance is measured based on segment profit after income tax as included in the internal financial reports.

Basis of accounting for purposes of reporting by operating segments

(a) Accounting policies adopted

All amounts reported to the Board of Directors, being the chief operating decision maker with respect to operating segments, are determined in accordance with accounting policies that are consistent to those adopted in the annual financial statements of the Group.

A number of inter segment transactions, receivables, payables or loans occurred during the period or existed at balance date.

(b) Segment assets

Where an asset is used across multiple segments, the asset is allocated to the segment that receives the majority of economic value from the asset. In the majority of instances, segment assets are clearly identifiable on the basis of their nature and physical location.

(c) Segment liabilities

Liabilities are allocated to segments where there is direct nexus between the incurrence of the liability and the operations of the segment. Segment liabilities include trade and other payables, and borrowings are not allocated to segments.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

21

Notes to the Financial Statements (continued)

(d) Segment performance Six Months Ended 31 December 2016 Australia Mongolia Total Segments Unallocated Consolidated Reconciliation of segment net loss to consolidated net loss after tax: Revenue - - - - - Cost of sales - - - - - Other income 808 1,700 2,508 - 2,508 Other expense (5,359,545) (5,765,654) (11,125,199) (2,865,257) (13,990,456) Depreciation & Amortisation (18,429) (258,328) (276,757) - (276,757) Exploration permits for coal - - - - - Impairment - - - - - Finance costs - - - (14,597,619) (14,597,619) Foreign exchange loss - - - (166,562) (166,562) Share of loss of associate (3,454) - (3,454) - (3,454) Income taxes - - - - - Net loss after tax per Statement of Comprehensive Income (5,380,620) (6,022,282) (11,402,902) (17,629,438) (29,032,340)

Six Months Ended 31 December 2015 Australia Mongolia Total Segments Unallocated Consolidated Reconciliation of segment net loss to consolidated net loss after tax: Revenue - 6,796,634 6,796,634 - 6,796,634 Cost of sales - (9,008,642) (9,008,642) - (9,008,642) Other income 1,807 3,879 5,686 - 5,686 Other expense (4,772,270) (3,444,172) (8,216,442) - (8,216,442) Depreciation & Amortisation (27,731) (3,113,950) (3,141,681) - (3,141,681) Exploration permits for coal (366,995) - (366,995) - (366,995) Impairment (13,360,444) (23,447,808) (36,808,252) - (36,808,252) Finance costs - - - (15,997,989) (15,997,989) Foreign exchange loss - - - (7,233,005) (7,233,005) Loss on disposal of subsidiary - - - - - Share of loss of associate (1,974) - (1,974) - (1,974) Income taxes - (208) (208) - (208) Net loss after tax per Statement of Comprehensive Income (18,527,607) (32,214,267) (50,741,874) (23,230,994) (73,972,868)

Finance costs, foreign exchange losses, business development and executive incentives are included in “Unallocated”. They are not allocated to individual segments as they are managed at the group level.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

22

Notes to the Financial Statements (continued) (e) Segment assets and liabilities

Australia Mongolia Total Segments Unallocated Total

31 Dec 2016 31 Dec 2016 31 Dec 2016 31 Dec 2016 31 Dec 2016 $ $ $ $ $

Segment assets Plant and equipment 121,880 117,978,895 118,100,775 - 118,100,775 Exploration and evaluation assets 34,346,454 15,397,523 49,743,977 - 49,743,977 Inventory - 631,186 631,186 - 631,186 Trade and other receivables 353,820 6,420,771 6,774,591 - 6,774,591 Cash and cash equivalents 909,283 308,952 1,218,235 - 1,218,235 Investment in associate 1,318,149 - 1,318,149 - 1,318,149 Intangible assets 30,069 822,075 852,144 - 852,144 Other assets 1,067,855 1,043,301 2,111,156 - 2,111,156 Total assets per Statement of Financial Position 38,147,510 142,602,703 180,750,213 - 180,750,213 Segment Liabilities

Trade and other payables 2,797,825 20,251,836 23,049,661 - 23,049,661 Borrowings - - - 184,660,455 184,660,455 Other financial liabilities - - - 8,087,376 8,087,376 Provisions 229,987 807,357 1,037,344 - 1,037,344 Total liabilities per Statement of Financial Position 3,027,812 21,059,193 24,087,005 192,747,831 216,834,836

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

23

Notes to the Financial Statements (continued) (e) Segment assets and liabilities (continued)

Australia Mongolia Total

Segments Unallocated Total 30 Jun 2016 30 Jun 2016 30 Jun 2016 30 Jun 2016 30 Jun 2016 $ $ $ $ $

Segment assets Plant and equipment 131,075 115,065,946 115,197,021 - 115,197,021 Exploration and evaluation assets 35,164,100 14,187,860 49,351,960 - 49,351,960 Inventory - 539,220 539,220 - 539,220 Trade and other receivables 392,968 7,885,832 8,278,800 - 8,278,800 Cash and cash equivalents 723,526 475,657 1,199,183 - 1,199,183 Investment in associate 1,386,457 - 1,386,457 - 1,386,457 Intangible assets 30,114 731,744 761,858 - 761,858 Other assets 495,380 2,100,620 2,596,000 - 2,596,000 Total assets per Statement of Financial Position 38,323,620 140,986,879 179,310,499 - 179,310,499 Trade and other payables 2,259,349 24,705,004 26,964,353 - 26,964,353 Borrowings - - - 161,157,215 161,157,215 Other financial liabilities - - - 7,880,454 7,880,454 Provisions 211,425 747,703 959,128 - 959,128 Total liabilities per Statement of Financial Position 2,470,774 25,452,707 27,923,481 169,037,669 196,961,150

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

24

Notes to the Financial Statements (continued)

(f) Segment cash flow information Australia Mongolia Total

31 December

2016 $

31 December

2015 $

31 December

2016 $

31 December

2015 $

31 December

2016 $

31 December

2015 $

Payments for property, plant and equipment 5,432 211,521 182,694 8,347,694 188,126 8,559,215

Payments for acquisition of exploration and evaluation 10,000 13,102 240,364 517,054 250,364 530,156

Note 5 Property, plant and equipment Movement in the carrying amounts for each class of property, plant and equipment between the beginning and the end of the current half year:

Capital works

in progress

Plant and Mine

Buildings equipment development Total $ $ $ $ $

Balance at 1 July 2016 12,436,420 39,021 4,495,394 98,226,186 115,197,021

Additions 36,190

- 36,875 115,061 188,126 Effects of foreign exchange on opening balance 328,101

691 106,919 2,584,114 3,019,825

Disposal -

- (59,425) - (59,425) Depreciation expense - (7,769) (237,003) - (244,772) Balance at 31 December 2016 12,800,711 31,943 4,342,760 100,925,361 118,100,775

Capital works in

progress

Plant and Mine

Buildings

equipment

development Total $ $ $ $ $

Balance at 1 July 2015 12,328,921 62,159 3,730,916 113,018,553 129,140,549 Additions 28,725 - 251,462 2,653,543 2,933,730 Effects of foreign exchange on opening balance 247,608 -

65,846

1,314,448

1,627,902

Acquisition of Subsidiary - - 781,470 - 781,470 Disposal - - (684) - (684) Transfers from plant and equipment (168,834) - 168,834 - - Impairment Expense - - - (15,476,581) (15,476,581)

Depreciation expense -

(23,138)

(502,450)

(3,283,777)

(3,809,365) Balance at 30 June 2016 12,436,420

39,021

4,495,394 98,226,186 115,197,021

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

25

Notes to the Financial Statements (continued) Note 6 Exploration and evaluation assets

31 December 2016 30 June

2016 $ $

Exploration and evaluation assets 49,743,977

49,351,960

(a) Movements in carrying amounts of exploration and evaluation assets During the 6 months ended 31 December 2016, the Group capitalised $250,364 (30 June 2016: $564,532) worth of expenditure as exploration expenditure. These costs relate to the acquisition and evaluation of mining tenements, including drilling, consulting and rent. A summary of movements for capitalised exploration and evaluation expenditure is as follows:

31 December 2016 30 June

2016 $ $

Beginning of financial period/year 49,351,960

58,573,488 Exploration expenditure 250,364 564,532 Acquisition of subsidiary - 12,005,190 Write-off from relinquishment of tenements (244,464) (646,224) Impairment losses - (21,331,671) Effects of foreign exchange on opening balance 386,117 186,645

End of financial period/year 49,743,977

49,351,960

(b) Interest in mining tenements Tenure Number

Location

Percentage Interest

31 December

2016

30 June 2016

1250 1260 1300 1394 1477 1478 1479 1480

Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Mount Isa, Queensland Australia

64.4% 64.4% 100% 100% 100% 100% 100% 100%

64.4% 64.4% 100% 100% 100% 100% 100% 100%

1574 1674 MDL 3002 1822 1872 1890 1892 1893 1962 1963 1964 2047 2049 2105 2256 2503 2504

Charters Towers, Queensland Australia Emerald, Queensland Australia Emerald, Queensland Australia Rockhampton, Queensland Australia Rockhampton, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Mount Isa, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia Charters Towers, Queensland Australia

100% 35.78% 35.78%

100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

100% 35.78% 35.78%

100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

26

Notes to the Financial Statements (continued)

XV-12929 XV-13780 MV-19149 XV-12600 XV-15466 MV-16971 MV-17162 MV-17163 XV-5264 XV-18111 XV-18513 XV-20268 XV-18142 XV-18797 XV-18802 XV-20281 XV-20539 XV-20139 XV-20329 14522X 13352X 5262X 25374NE

Mid Gobi, Mongolia South Gobi, Mongolia South Gobi, Mongolia South Gobi, Mongolia Mid Gobi, Mongolia South Gobi, Mongolia South Gobi, Mongolia South Gobi, Mongolia South Gobi, Mongolia South Gobi, Mongolia South Gobi, Mongolia South Gobi, Mongolia Uvs, Mongolia Uvs, Mongolia Uvs, Mongolia Uvs, Mongolia Uvs, Mongolia East Gobi, Mongolia East Gobi, Mongolia South Gobi, Mongolia Mid Gobi, Mongolia South Gobi, Mongolia Baruun Termes, Mongolia

100% 100% 100% 100%

- 83.87%

100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

- - - -

100% 100% 100% 100% 100%

83.87% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

83.87% 100%

Note 7 Borrowings 31 December

2016 30 June

2016 $ $

CURRENT Super senior note facility A (a) 16,583,748 16,159,439 Fuel exclusivity agreement (b) 12,069,285 11,449,927

Working capital facility (d) 4,145,937 - Finance costs accrued (e) 12,472,361 48,604

45,271,331 27,657,970

NON-CURRENT Listed (Euroclear) bond (a) 128,333,292 122,741,684 Super senior note facility B (a) 6,909,895 6,733,100 Non-Interest Bearing Loans (c) 4,145,937 4,073,065

139,389,124 133,547,849 Total Borrowings 184,660,455 161,205,819

BORROWINGS EXPRESSED IN USD (DENOMINATED CURRENCY)

USD$ USD$ CURRENT Super senior note facility A (a) 12,000,000 12,000,000 Interest bearing loans (fuel exclusivity facility) (b) 8,733,335 8,502,716 Working capital facility (d) 3,000,000 - Finance Costs Accrued (e) 9,025,000 36,093 32,758,335 20,538,809 NON-CURRENT Listed (Euroclear) bond (a) 92,861,970 91,147,975 Super senior note facility B (a) 5,000,000 5,000,000 Non-Interest Bearing Loans (c) 3,000,000 3,000,000 100,861,970 99,147,975 Total Borrowings 133,770,033 119,686,784

The above USD amounts have been translated using the year end USD to AUD exchange rate of 0.7236.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

27

Notes to the Financial Statements (continued) (a) Listed (Euroclear) Bond, Super Senior Note A and Super Senior Note B

On 30 June 2016, the Company entered into 3 new facilities (Listed Bond, Super Senior Note A and Super Senior Note B). The proceeds from these facilities were used to extinguish the Company’s existing facilities except for the Fuel Exclusivity Agreement and non-interest bearing loan acquired from Enkhtunkh Orchlon LLC. Super Senior Note A The Super Senior Note A facility was fully drawn down on 30 June 2016 for the amount of US$12,000,000. The facility bears an interest rate of 15% with interest payable on the repayment date. The total principal and interest repayment is due on 30 June 2017. Super Senior Note B The Super Senior Note B facility was fully drawn down on 30 June 2016 for the amount of US$5,000,000. The facility bears an interest rate of 15% repayable at 30 June 2017. On this date, the Group has an unconditional right to convert the principal amount and 50% of the interest charge into the Listed (Euroclear) bonds with repayment due on the same terms and conditions of the bond. On this basis the Company has classified the principle amount as non-current. Listed (Euroclear) Bond The Listed (Euroclear) Bond was fully drawn down on 30 June 2016 for the amount of US$97,000,000 (purchase value of the bonds). The facility bears a cash interest rate of 12% per annum, payable 6 monthly in arrears except for the first interest payment which is not due until 12 months from bond issue. The maturity date of the facility is 30 June 2021 at which point the redemption value of the bonds is due and payable for the amount of US$124,000,000. The value uplift applied between the redemption value and purchase price, along with the interest, implies an annual cumulative interest rate of 21.09%. At each interest repayment date, 50% of the interest charge can be capitalised into the principal amount of the loan. This facility includes a special interest component which has been treated as a separate non-derivative financial liability. This instrument, which represents an incremental cost that is directly attributable to the issue of the bond, has been treated as a transaction cost and offset against the fair value on initial recognition. The facilities are subject to debt covenants and obligations to make interest and principal payments on set dates. Should these terms not be met by the Company an event of default may eventuate.

(b) Fuel exclusivity agreement

On 14 November 2013, the Company entered into a Fuel Exclusivity agreement with Noble Resources International Pte Limited (Noble) for US$8,000,000. The facility has an implied interest rate of 9.7%. The US$8,733,335 carrying value of the facility at 31 December 2016 represents the principal and interest which remains due.

(c) Non-interest bearing loan

This amount relates to US$3,000,000 due by the Group to Noble and is payable by the recently acquired Enkhtunkh Orchlon LLC. This amount is due for repayment on 1 October 2020.

(d) Working capital facility

On 13 September 2016, the Company entered into a Blair Athol Prepayment Facility Agreement with Noble for US$12,000,000. US$3,000,000 was received on 28 October 2016 when certain conditions precedent were met with respect to the acquisition of the Blair Athol open cut thermal coal mine in Queensland. The repayment is US$250,000 per month commencing at the earlier of 31 March 2017 or commercial production at Blair Athol with an interest rate of 9% per annum. The remaining US$9,000,000 will be eligible for draw down in stages upon completion of milestones associated with the Blair Athol coal mine.

(e) Finance costs accrued

Accrued finance costs relate to interest accrued to 31 December 2016 on the following facilities;

i. Listed Euroclear Bond – US$7,750,000 ii. Super senior note facility A - US$900,000 iii. Super senior note facility B – US$375,000

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

28

Notes to the Financial Statements (continued)

(f) Securities pledged

As part of the Bond and Super Senior Note facilities establishment, in June 2016, there is a general security agreement in place which encompasses TerraCom, its subsidiaries assets and its subsidiaries equity, except for the stockpile pledges.

Note 8 Other financial liabilities

31 December 2016 30 June

2016 $ $

Non-current special interest liability 8,087,376 7,880,454

In connection with the issuance of the Listed (Euroclear) Bond, a special interest instrument was granted to the bond holders. This instrument requires the Company to pay a non-refundable payment equal to 0.75% to 1.75% of mine gate revenues for the duration of the bond (5 years). The key terms include: - Special interest is payable at a rate of 1.75% of mine gate revenue until the Company acquires the Blair Athol mine in Queensland - Once the Blair Athol mine is acquired, the special interest decreases to 0.75% of total mine gate revenue generated by the Company;

- The special interest is payable on 30 June 2017 and every 6 months subsequent, up to the maturity date of the Bonds (30 June 2021); This special interest has been treated as a cost of issuing the Listed (Euroclear) bond and has been offset against the carrying value of the debt in note 7.

Note 9 Issued Capital

31 December

2016 30 June

2016 $ $

2,714,933,556 Ordinary Shares 202,516,386 195,276,818

(a) Ordinary shares No. $ Balance at 1 July 2016 2,400,931,258 195,276,818 Ordinary shares issued during the 6 months’ period 314,002,298 7,440,952 Share issuance expenses - (201,384) End of financial period 2,714,933,556 202,516,386 Ordinary shares issued during the 6 month period consisted of: i. 9 August 2016 – 80,849,502 shares issued at a placement issue price of $0.0166 per ordinary share ii. 6 September 2016 – 55,407,834 shares issued at a placement issue price of $0.0206 per ordinary share iii. 6 September 2016 – 44,411,629 shares issued at a placement issue price of $0.0215 per ordinary share iv. 14 December 2016 – 133,333,333 shares issued at a placement issue price of $0.0300 per ordinary share

(b) Capital Management Management controls the capital of the Group in order to achieve a manageable debt to equity ratio, provide the shareholders with adequate returns and ensure that the Group can fund its operations and continue as a going concern.

The Group’s debt and capital includes ordinary share capital and financial liabilities, supported by financial assets. There are no externally imposed capital requirements.

Management effectively manages the Group’s capital by assessing the Group’s financial risks and adjusting its capital structure in response to changes in these risks and in the market. These responses include the management of debt levels, distributions to shareholders and share issues.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

29

Notes to the Financial Statements (continued)

Note 10 Fair Value Measurement

The Group measures all of its financial assets and financial liabilities at amortised cost. No financial instruments are measured at fair value on a recurring basis.

Fair value hierarchy AASB 13 Fair Value Measurement requires all assets and liabilities measured at fair value to be assigned to a level in the fair value hierarchy as follows:

Level 1 - Measurement based on unadjusted quoted prices in active markets for identical assets or liabilities that the entity can access at the measurement date.

Level 2 - Measurement based on inputs other than quoted prices included within Level 1 that are observable for the asset or liability, either directly or indirectly.

Level 3 - Measurement based on unobservable inputs for the asset or liability.

The table below shows the assigned categorisation within the fair value hierarchy for each financial asset and liability that is required to disclose fair value:

Fair Value & Hierarchy Level

31 December 2016

Carrying Value Level 1 $

Level 2 $

Level 3 $

Total $

Non-Recurring fair value measurements for which fair value is disclosed

Trade and other receivables 6,774,591 - - 6,774,591 6,774,591

Other Assets 2,111,156 - 2,111,156 - 2,111,156

Trade and other payables 23,049,661 - 23,049,661 - 23,049,661

Borrowings 7 184,660,455 - 180,514,519 3,446,457 183,960,976

Special interest liability 8 8,087,376 - - 7,963,252 7,963,252

Fair Value & Hierarchy Level

30 June 2016

Carrying Value Level 1 $

Level 2 $

Level 3 $

Total $

Non-Recurring fair value measurements for which fair value is disclosed

Trade and other receivables 8,278,800 - - 8,278,800 8,278,800

Other Assets 2,596,000 - 2,596,000 - 2,596,000

Trade and other payables 26,915,749 - 26,915,749 - 26,915,749

Borrowings 7 161,205,819 - 157,132,754 4,073,065 161,205,819

Special interest liability 8 7,880,454 - - 7,880,454 7,880,454

Valuation techniques and inputs used to measure fair values are detailed below.

Trade and other receivables

The carrying value of current trade and other receivables approximates its fair value given the short term nature of the receivable.

Non-current trade and other receivables are measured at amortised cost. The fair value of these receivables is determined by discounting the future expected payments using an appropriate discount rate. Maturities of these amounts are not fixed, and determined upon meeting certain milestones (such a generating revenues to recover VAT receivables), and operational outcomes which have been estimated by management.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

30

Notes to the Financial Statements (continued)

Other Assets

The carrying value of current other assets approximates its fair value given the short term nature of the asset. Non-current other assets are measured at amortised cost. The fair value of these assets is determined by discounting the future expected payments using an appropriate discount rate. These asset fair values are assumed at their carrying value as they represent cash held on deposit with no fixed maturity.

Trade and other payables

The carrying value of current trade and other payables approximates its fair value given the short term nature of the liability.

Borrowings

The fair value of Listed Bond, Super Senior Note A and Super Senior Note B are measured at amortised cost. There has not been a significant change in fair value since the issuance date on 30 June 2016 as the liability is carried at amortised cost and the effective interest rate used to discount future principal and interest cash flows has not changed significantly from the market rate on issuance.

The Non-interest bearing loan was acquired by the Group during the acquisition of Enkhtunkh Orchlon LLC on 1 October 2015 and has been fair valued as at the date of acquisition. As the loan is interest free the fair value has been calculated using a market rate of interest at 31 December 2016.

The fair value of the Fuel Exclusivity Facility approximates its carrying value at 31 December 2016 due to its short term nature.

Special interest liabilities

The fair value of special interest liability is determined by applying a present value income approach to the estimated mine gate revenues projected over the duration of the instrument, multiplied by the special interest rate and discounted using an appropriate discount rate.

There were no changes during the period in the valuation techniques used by the Group to determine fair values.

Note 11 Related Party Disclosures

Transactions between related parties are on normal commercial terms and conditions no more favourable than those available to other parties unless otherwise stated. Other than stated below, there are no other changes from the disclosures included within the 30 June 2016 audited financial statements.

Transactions with director

The Company made payments to Mr Cameron McRae, for his services as Executive Chairman, through consultancy firm Tarva Investments and Advisory LLC (Tarva) to which he is the appointed Executive Director of $132,430 during the period. At 30 November 2016, – 73,318,740 fully paid ordinary shares were approved as a sign-on bonus to be allocated to Tarva. The sign-on share bonus was granted upon approval at the Company’s AGM on 30 November 2016 (refer to note 13). At 31 December 2016 the amount payable to Tarva is $4,186, which includes reimbursable business related travel expenses.

Note 12 Share Based Payments The following share based payments were made during the reporting period:

i. 29 August 2016 – 30,000,000 unlisted options issued to Fosters Stockbroking Pty Ltd for the provision of institutional research coverage services. The options were issued in two tranches of 15,000,000 at a strike price of $0.03 and $0.045 respectively and an expiry date of 31 August 2018.

This transaction is a share based payment for services to be provided over a 12-month period from 29 August 2016. This share based payment has been prorated over the service period with the relevant portion expensed up to the 31 December 2016. An expense of $152,464 has been recognised within consulting fees in the income statement.

ii. 30 November 2016 – 73,318,740 fully paid ordinary shares were approved as a sign-on bonus to be allocated to

Tarva, a company that Cameron McRae controls. The sign-on share bonus was granted upon approval at the Company’s AGM on 30 November 2016. As at 31 December 2016 these shares have not yet been issued to Tarva.

TerraCom Ltd - ABN 35 143 533 537 For Half Year Ended 31 December 2016

31

Notes to the Financial Statements (continued)

At the Company’s AGM held on 30 November 2016 shareholders approved a $600,000 sign-on bonus (fully paid ordinary shares for nil consideration) to Cameron McRae, through the Executive Chairman Consultancy Agreement with Tarva Investment and Advisory LLC a company which he controls, with a conditions precedent that shareholder approval be obtained before granting the bonus. At the time of agreeing this bonus, the average VWAP of TerraCom’s shares were $0.008183 which entitled Mr McRae to 73,813,740 fully paid ordinary shares for nil consideration. For accounting standard purposes a share based payment expense of $2,712,793 was recognised in the profit and loss statement for the 6 months ended 31 December 2016 as the grant date for the shares was not until 30 November 2016 (the date shareholder approval was obtained) and the fair value of the shares was determined using the market value of the shares as at 30 November 2016, which was $0.037 per fully paid ordinary share. As at 31 December 2016 these shares have not yet been issued to Tarva.

Note 13 Contingencies Contingent Liabilities

There are no changes to contingent liabilities from the disclosures included within the 30 June 2016 audited financial statements.

Note 14 Events after the end of the Interim Period