consequences of non-compliance with u.s. import laws and regulations

DESCRIPTION

CLE Presentation: Nikolas Takacs, International attorney at Armstrong Teasdale Foreign suppliers are an increasingly popular source for products sold in the United States. The complex framework of import laws and non-compliance associated with importing goods into the U.S. can result in significant penalties or unanticipated costs to companies. This seminar will identify key areas of concern and strategies for reducing the risk of non-compliance with U.S. import laws and regulations. The choice of a lawyer is an important decision and should not be based solely on this presentation. All rights are reserved and content may not be reproduced, disseminated or transferred, in any form or by means, except with the prior written consent of Armstrong Teasdale.TRANSCRIPT

The Grapes of Wrath: Consequences of Non-Compliance with U.S. Import Laws and Regulations

Nikolas E. Takacs April 24, 2013

Agenda

Legal Framework

Import Compliance in Key Areas

Duty Savings Opportunities

Consequences

Penalties (civil and criminal)

Back duties

Seizures

Delays in customs clearance

Audits or investigations

Benefits

Predictable costs

Competitive advantage

Duty savings

Faster import clearance

Import Revenue

U.S. Customs total revenue collected in 2012: $39.4 billion1

Estimated undercollection for 2012: $484 million1

U.S. Customs looking outside the box to increase collection

1 United States Customs and Border Protection, “Import Trade Trends: Fiscal Year 2012, Year-End Report”, http://nemo.cbp.gov/ot/fy12_yearend.pdf

Who Enforces U.S. Import Laws?

Customs and Border Protection • Collects import duties • Facilities international trade • Division of the Department of Homeland

Security

The Department of Commerce • Enforces U.S. unfair trade laws

(anti-dumping and countervailing duties)

International Trade Commission • Independent quasi-judicial agency

enforcing unfair trade laws and intellectual property import investigations

Who Enforces U.S. Import Laws?

Court of International Trade (CIT) • Article III court with universal subject-matter jurisdiction over appeals from CBP,

Commerce, and certain ITC cases. Court of Appeals for the Federal Circuit

• Hears appeals from the CIT and appeals from the ITC concerning IP issues. Office of the United States Trade Representative

• Develops and recommends trade policy, negotiates free trade agreements. Food and Drug Agency

• Safety and labeling requirements for food, drugs, and cosmetics. Consumer Product Safety Commission

• Product safety laws for imported products. Federal Trade Commission

• Statements concerning country of origin. Securities and Exchange Commission

• Review of “conflict mineral” prohibitions under the Dodd-Frank Act. Department of Agriculture Environmental Protection Agency Fish and Wildlife Service

International Legal Framework

World Trade Organization • Reduction of tariff and non-tariff barriers to trade

World Customs Organization International standardization of norms associated with import

procedures

Bilateral or Multilateral Trade Agreements (i.e. U.S.-Chile Free Trade Agreement, NAFTA).

• Negotiated by the U.S. Trade Representative • Not valid until implemented by Congress

U.S. Legal Framework

Tariff Act of 1930 (19 U.S.C. ch. 4) • Most important statute governing customs and import law

• Governs all aspects of the importation process

Import Regulations under Title 19

• The regulations interpreting the Tariff Act are also very important, as the statute is very general in nature

• Agency officials have tremendous discretion in enforcing customs and import laws

U.S. Legal Framework: Reasonable Care

Customs Modernization Act (“Mod Act”), 19 U.S.C. §§ 1508-10: • Importers must exercise reasonable care on three issues or else

face customs penalties: (1) customs entry, (2) valuation, and (3) classification.

• Ways to exercise reasonable care include: consulting with customs expert, seeking a binding customs ruling or request for internal advice, having internal controls for trade compliance, etc.

• Consult “Informed Compliance” Publications on import topics released by CBP: http://www.cbp.gov/xp/cgov/trade/legal/informed_compliance_pubs/

U.S. Legal Framework: Penalties

Penalties for Non-Compliance (19 U.S.C. § 1592) • CBP can review customs entries for compliance going back

five years from the time of entry.

• Amount of penalty depends on level of culpability (negligence, gross negligence, or fraud).

• CBP can assess penalties up to 100% of the value of each importation.

• Importer can mitigate penalties by submitting a “Prior Disclosure” – a voluntary disclosure of the violations, permitted as long as CBP has not yet initiated a formal investigation.

U.S. Legal Framework: Penalties

Other Penalties • Recordkeeping penalties (19 U.S.C. 1509)

− Up to $100,000 or 75% of the appraised value of the merchandise (whichever is less) for failure to produce a record upon demand.

• Drawback penalties (19 U.S.C. 1593a)

• Counterfeit trademark penalties (19 U.S.C. 1526(f))

CBP Priority Trade Issues

Revenue Antidumping and Countervailing Duties

Penalties

Intellectual Property Rights

Areas of Import Enforcement

I. Clearance II. Classification III. Valuation IV. Country of Origin/Marking V. Other Issues:

A. Anti-Dumping and Countervailing Duties

B. Intellectual Property Rights Enforcement

C. Customs Investigations/Inquiries

Customs Clearance Process

Steps: • Arrival of goods at port of entry

• Entry

• Classification

• Inspection

• Liquidation (final ascertainment of duties)

Customs Classification

How are import duties calculated?

• Ad valorem (% of value) or per unit (per kg, per liter, etc.)

• May vary by country

14.9% 3.9¢/kg

Customs Classification

Harmonized Tariff Schedule (HTSUS):

• Tariff classification system used for imported goods

• Organized in chapters from 0-99, with 21 sections

• 17,000 potential classifications, each good has an associated tariff rate

• Classification can be extremely complex

Customs Classification

Example: Classification:

• Ch. 16: Preparations of meat, of fish or of crustaceans, mollusks or other aquatic invertebrates.

− Heading 1604: Prepared or preserved fish; caviar and caviar substitutes prepared from fish eggs.

• Subheading 1604.14: Tunas, skipjack, and bonito in airtight containers.

» Provision 1604.14.10: Packed in Oil.

Customs Classification

Issues with customs classification:

• Product may have functions that are described in multiple tariff headings

• No tariff provision may accurately reflect the product

• Tariff Schedule does not change as fast as technology

Customs Classification

How is classification determined? • Plain language of each chapter, section, and heading, and

corresponding notes

• General Rules of Interpretation

• Prior CBP rulings, precedent by the Court of International Trade and the Court of Appeals for the Federal Circuit

• Harmonized System Explanatory Notes

Customs Classification

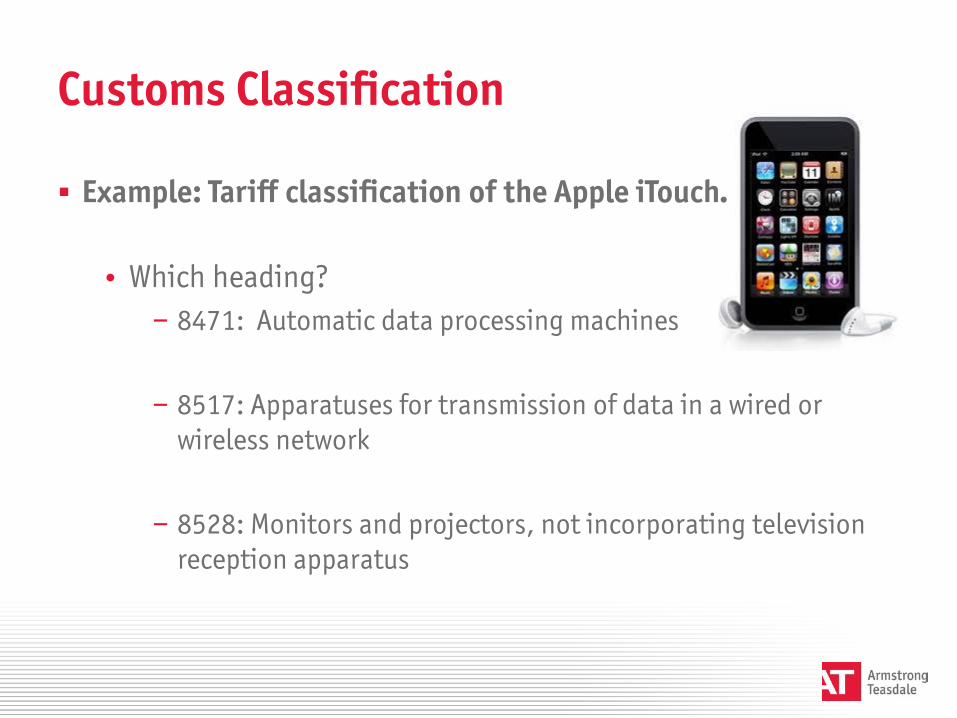

Example: Tariff classification of the Apple iTouch.

• Which heading? − 8471: Automatic data processing machines

− 8517: Apparatuses for transmission of data in a wired or wireless network

− 8528: Monitors and projectors, not incorporating television reception apparatus

Customs Classification

Example: Tariff classification of an Apple iTouch. • Heading 8471: Automatic data processing machines. • Why?

− CBP looked at prior rulings and judicial precedent for similar products and determined that the iTouch met the requirements of 8471 by being “freely programmable”.

• Classification: 8471 Automatic data processing machines and units thereof; magnetic or optical readers, machines for transcribing data onto data media in coded form and machines for processing such data, not elsewhere specified or included: 8471.30.01 Portable automatic data processing machines, weighing no more than 10kg, consisting of at least a central processing unit, a keyboard and a display …

Customs Classification

Challenging a Classification Decision by CBP:

• If CBP classifies an import under a tariff classification that the importer does not agree with, it can file a “protest” and submit arguments against CBP’s decision.

• CBP will review their decision and make a redetermination. • Importer can ultimately file an appeal to the Court of

International Trade after CBP’s review.

Customs Classification

Takeaways:

• Clear descriptions on the merchandise on the commercial invoice

• Not reasonable care to rely on customs brokers

• When in doubt, request for internal advice or a customs ruling

Customs Valuation

Importer must declare a value for the imported merchandise Value declared to CBP directly impacts how much duty is paid

Area of focus for customs compliance

Customs Valuation

Transaction Value:

• Most common method of customs valuation

• = “price paid or payable for the imported merchandise.

• Must have a bona fide sale (i.e. transfer of title and risk of loss from seller to buyer) to use transaction value

Customs Valuation

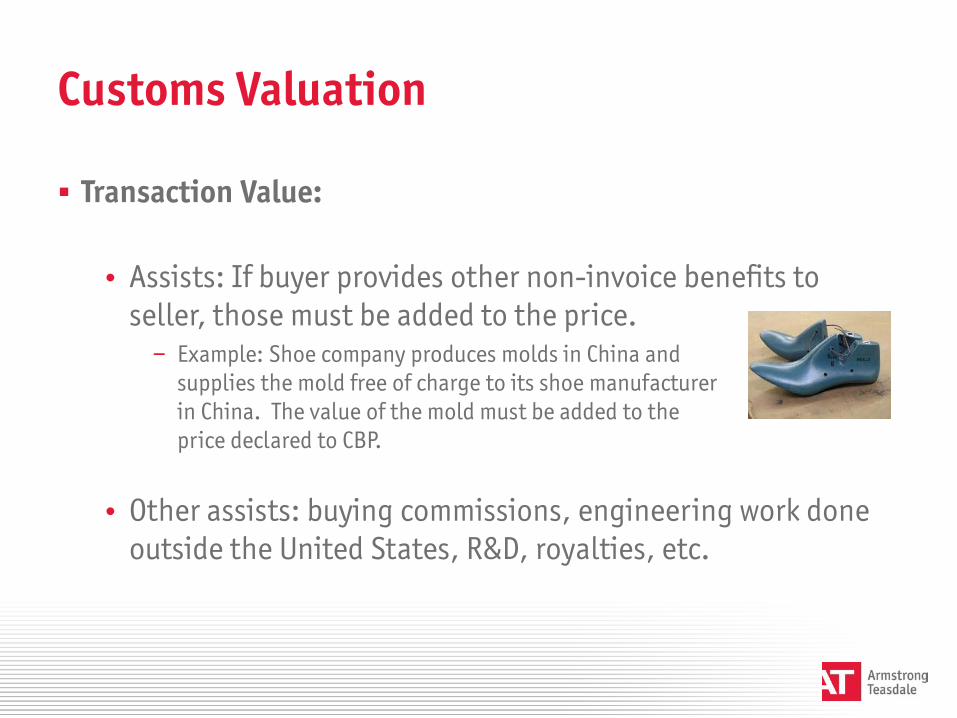

Transaction Value:

• Assists: If buyer provides other non-invoice benefits to seller, those must be added to the price.

− Example: Shoe company produces molds in China and supplies the mold free of charge to its shoe manufacturer in China. The value of the mold must be added to the price declared to CBP.

• Other assists: buying commissions, engineering work done outside the United States, R&D, royalties, etc.

Customs Valuation

Related Parties:

• Transaction value is presumed to be unacceptable for related party sales unless additional requirements are met.

• Must demonstrate that the relationship did not influence the price. • Not exercising reasonable care to rely on either: (1) an internal transfer

pricing study; or (2) an Advance Pricing Agreement approved by IRS. • Different test than the IRS “arm’s length” test.

• This is a high risk area and increased area of CBP enforcement.

Customs Valuation

Takeaways:

• Consider whether the commercial invoice accounts for the entire value of the imported goods.

• Ask: − Is there a sale? − Does the seller receive any benefits that are not reflected on

the invoice?

• Advance planning required if selling from an overseas related party.

Marking and Country of Origin

Unless there is a specific exception, all products (or their packaging) must be marked with the country of origin.

Each imported product will only have one country of origin.

Importer has burden of ensuring that country of origin is correct.

In the case of an assembled product, CBP will apply the “substantial transformation” test.

• If an unfinished product is shipped from country A and assembled in country B, CBP will see if the assembly in country B transforms the item into a new product that is a now a product of Country B.

Special rules of origin to qualify for free trade agreements.

Marking and Country of Origin

Takeaways:

• Perform country of origin analysis for products assembled in multiple countries

• Substantial transformation as a duty saving strategy

• Due diligence of suppliers to ensure that country of origin is correct

Antidumping and Countervailing Duties

Protection for U.S. manufacturers from unfair import competition Increasingly a priority concern for the U.S. government

Dumping: sales of products at “less than fair value”

Countervailable Subsidy: Subsidy granted by foreign

government that is specific to export

Antidumping and Countervailing Duties

U.S. industry: petition Commerce and ITC for AD/CV duties against imports of a product from a certain country

Standard: “Material injury” or “threat of material injury”

Examples of cases: Petroleum Wax Candles from China, Ball Bearings from Germany, Solar Panels from China, Frozen Fish Fillets from Vietnam

U.S. industry = domestic producers or workers of the merchandise in question

Purpose: protect U.S. manufacturing, not U.S.-based companies with overseas production

Antidumping and Countervailing Duties

AD/CV Duty Investigation Process:

• ITC: material injury investigation

• Commerce: calculates dumping margin (% below fair value) or countervailing duty margin (% of subsidies)

• If the U.S. industry is successful, Commerce and the ITC will impose an antidumping duty or countervailing duty “order

Antidumping and Countervailing Duties

AD/CV Duty Rates:

• Importers from the country in question must pay a deposit for AD or CV duties at time of entry

• Commerce conducts annual reviews of the AD and CV duty rates

• Final AD/CV duty rate not calculated until years after entry

• These AD and CV duty rates can be extremely high and can bring importers into bankruptcy

• All AD and CV proceedings are subject to judicial review at the Court of International Trade

Antidumping and Countervailing Duties

Takeaways: • Require counsel approval before importing products subject

to AD/CV duties

• Retrospective nature of the duty assessment process

• Consider options for advocating for removal of products from AD/CV duty order, or for obtaining lower margins

Intellectual Property Rights Protections

Counterfeits • CBP has authority to seize suspected counterfeit goods for trademarks

registered with CBP

Gray Market Goods • “Authentic” goods that are not authorized for importation by the

trademark holder • CBP can seize certain gray goods if the trademark holder has requested

gray market protection (known as Lever Rule protection)

IP Infringement • The ITC can bring exclusion proceedings (section 337) for goods that

violate U.S. IP rights

Intellectual Property Safeguards

Counterfeits • Importers: make sure you are not buying counterfeit goods • U.S. manufacturers: register your trademarks with CBP and provide CBP with

information on trademarks

Gray market • Importers: make sure the manufacturer is licensed by the trademark

holder to import, or ensure an exception applies allowing importation • U.S. manufacturers:

− Consider applying for Lever Rule protection against gray market imports − Ensure that you have obtained and own the foreign trademark for your

products

Criminalization of Import Laws

Deterrent against Non-Compliance • Bases:

− 18 U.S.C. § 1519 (Sarbanes-Oxley Anti-Obstruction Statute): • Whoever knowingly alters, destroys, mutilates, conceals, covers up,

falsifies, … any record, document, or tangible object with the intent to impede, obstruct, or influence the investigation or proper administration of any matter within the jurisdiction of any department or agency of the United States … or contemplation of any such matter or case, shall be fined under this title, imprisoned not more than 20 years, or both.

− False Claims Act (31 U.S.C. §§ 3929-3733). − Customs criminal provisions under 18 U.S.C. ch. 27. − Application of other statutes not specific to import, such as the

Lacey Act or the Food, Drug and Cosmetic Act.

Criminalization of Import Laws

Transshipment of Goods: United States v. Wolff (N.D. Ill.)

• Honey from China is subject to AD duties • Defendants accused of transshipping Honey from China through a

third country, and falsely declaring the third country as the country of origin for customs purposes to avoid payment of AD duties

• DOJ brought claim under the SOX anti-obstruction statute

• Led to prison sentences, individual fines in the millions of dollars,

and corporate forfeitures of $120 million

Criminalization of Import Laws

Mislabeling Goods: United States v. Blyth (S.D. Alabama)

• Seafood wholesalers charged with mislabeling imported fish

to avoid antidumping duties on Vietnamese catfish

• Defendants sentenced to prison for violating 18 U.S.C. 542 and 545

Important to realize gravity of customs investigations – basic

inquiries can turn into serious criminal matters

Customs Investigations and Inquiries

CF 28: Request for Information

CF 29: Notice of Action

Focused Assessment • Priority is on major importers or high risk areas

Quick Response Audit

• Single issue audits • Usually based on prior identification of a concern

Pre-Penalty Notice or Penalty Notice

Customs Investigations and Inquiries

Treat all inquiries from CBP seriously Notify in-house counsel and outside counsel of CBP inquiries

Consider whether to file a Prior Disclosure before it is

precluded

Best Practices

Strong document retention system (7 years or longer). • Need to produce documents upon request • Files should be easy to locate

Establish strong customs and trade policies and procedures.

• Should be specific to the import activities that are actually taking place (and activities that may take place)

• Periodically review for updates • Consider outside audit by a law firm

Show your work • Wrong answer does not necessarily mean a violation of reasonable care • Demonstrate how you arrived at your conclusions and why those conclusions were

reasonable Importation as a legal function

In-house counsel should be actively involved in import decisions

Duty Saving Strategies

Duty Deferral/Refunds

• Foreign Trade Zones − Goods entering the zone are not dutiable until they enter the

commerce of the United States for consumption

• Drawback − Duty refund of 99% on imported goods that are exported or

destroyed

Duty Saving Strategies

Duty Reduction • First Sale for Export

− Multi-tiered sales structure (i.e. sales with a middleman) − Instead of declaring the value to CBP in the sale from the middleman

to the importer, the importer can declare the value from the manufacturer to the middleman in certain circumstances

• Substantial transformation/shift in country of origin − Beneficial if the duty rate is lower in the final country

• Deduction of freight and shipping costs

− Ocean freight, marine insurance, and containerization can be deducted from the value declared to CBP

Duty Saving Strategies

Preferential Trade Programs • Traditional Trade Agreements

− Free trade agreements with 20 countries − Specific rules on qualifications

• Special Duty Programs

− Generalized System of Preferences (GSP) • Preferential duty treatment for 5,000+ products imported from 127

designated countries − African Grown and Opportunity Act (AGOA)

• Preferential duty treatment for imports from sub-Saharan African countries

− Caribbean Basin Initiative (CBI) • Duty-free treatment for imports from Caribbean nations

Trending Trade Topics

Trans Pacific Partnership • Proposed multi-lateral trade agreement with Pacific Rim

countries • May have impact on IP protections

U.S.-EU Free Trade Agreement First Sale for Copyright

• Supreme Court Decision in Kirtsaeng v. John Wiley & Sons, Inc.

• New Rule: Copyright is exhausted upon first sale abroad

Contact and Questions?

Nikolas Takacs Associate Armstrong Teasdale LLP 314.552.6602 [email protected] www.armstrongteasdale.com