consensus and market models: stylized facts in a sznajd world

DESCRIPTION

Consensus and Market Models: Stylized facts in a Sznajd World. Collective behaviour in markets. Trends Crashes We also know that: Traders talk to each other (sometimes through third parties…) Traders have similar constraints ( market regulation) - PowerPoint PPT PresentationTRANSCRIPT

Consensus and Market Models:

Stylized facts in a Sznajd World

Lorenzo Sabatelli1,2 and Peter Richmond1 1 Department of Physics, Trinity College Dublin, Ireland 2 Hibernian Investment Managers, IFSC, Dublin, Ireland

E-mail: [email protected]

Collective behaviour in markets

• Trends

• CrashesWe also know that:

• Traders talk to each other (sometimes through third parties…)

• Traders have similar constraints ( market regulation)

• Traders avail of common sources of information (press, databases, consultant reports, fundamental economic factors and models)

Consensus

Price changes depending on the difference between demand and supply

Demand and supply depend on

1. number of agents keen on buying or selling

2. amount of an asset individually traded by agents

Here we focus on

• number of buyers and sellers

• why they buy or sell

We model these features in terms of

Consensus dynamics

Sznajd Consensus Model:

‘United we stand, divided we fall’

Abraham Lincoln

Within human societies, it is generally easier to change someone‘s opinion by acting within from within a group than by acting alone.

Place agents (spins) on 2-d lattice:

• Each site carries a spin S that may be up or

down (two possible opinions, yes or no)

• Two neighbouring parallel spins are able to

convince other neighbours of their opinion.

• If these two neighbours are not parallel or in step, they have no influence on their neighbours.

Sznajd Model and synchronous updating

Allowing system to evolve via – random sequential updating

– always leads to total orientation of spins (total consensus)

We choose a synchronous updating mechanism:

It admits possibility of contradictory information.

Effects of single interaction may last for a certain time

In Sznajd model, synchronous updating carries new feature

frustration

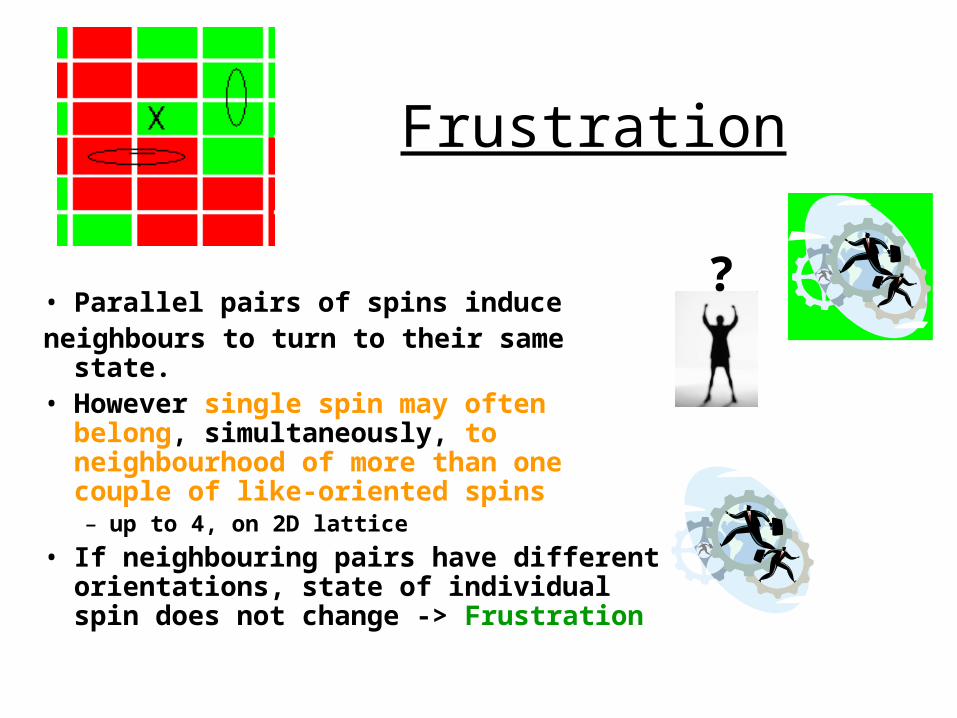

Frustration

• Parallel pairs of spins induceneighbours to turn to their same state. • However single spin may often belong,

simultaneously, to neighbourhood of more than one couple of like-oriented spins – up to 4, on 2D lattice

• If neighbouring pairs have different orientations, state of individual spin does not change -> Frustration

?

Phase transitions in a synchronously updated Sznajd Model

ΔP is absolute difference of opinions at t=0

ΔPc

Variation on a log-log scale of 1-Mc with lattice size, L, in the absence of noise or zero temperature. When the initial net magnetisation, M(0)>Mc the system evolves to complete consensus (M(equilibrium)=1). When the initial net magnetisation, M(0)<Mc the system never reaches complete consensus (M(equilibrium )<1).

_

N NM

N N

1 ~ 1/cM L

Introducing random noise (random change of individual opinions)

Non-monotonic Magnetization

Microscopic interpretation Spins surrounded by four others of the same sign, so forming cross-shaped islands, form a stable

state. At zero temperature, they are prevented, at any time, from flipping by frustration.

Random noise acts flipping one of the five spins, so allowing frustration to be removed.

What does the noise account for ?

• External factor influence

• Degree of ‘connection’ between neighbouring agents

• Independence of thought

Basic stylized facts…Minimum requirements for any market model

• Fat tails in the probability density distribution of returns, volumes and volatility

• (Almost) no time-correlation between the directions of price fluctuations

• Long lasting time correlation (power law decay) between the absolute values of price fluctuations.

A Market Model

• Price formation as a Consensus Process

• Noise as a measure of the degree of connection between agents and independence of thought.

• Risk perception (measured through volatility) may change the degree of connection.

Sznajd-like price formation process

Given N unbiased agents • p_initial=0.5, random configuration.

• before each transaction they interact for n time steps (on average).

• Each of them may change opinion (independently of the others) with probability q.

Volatility shocks and q changes• The updating of q may happen either through

deterministic or stochastic rules.

• In both cases q changes depend on the volatility changes– E.g.: one may use following stochastic rule

tRtBtB

tionMagnetizattchangeicetR

Nt

ttB

tBtRtq

volatility

volatility

11

~_Pr

1,0

1

1

Stylized facts in a Sznajd World

Lower tail exponent=2.7

Upper tail exponent=2.6

Example: for L=50 (2500 agents), p_initial=0.5, alpha=0.98, N_iterations=400

Lower cut-off tail exponent=3.9

Upper cut-offtail exponent=4.1

•(Almost) No-time-correlation between returns

•Significant time-correlation between absolute returns

Conclusions

• Opinion dynamics play role in price formation• Sznajd consensus model may describe price

formation process• Noise, as measure of independence of thought

and external influence, plays non trivial role in determining consensus

• Noise changes driven by Volatility changes may ( partly) explain some relevant stylized facts observed in financial time series – fat tails in histograms of returns and volatility – long memory and clustering of volatility)

Outlook :What’s next ?

• More realistic topologies for more realistic models

• Heterogeneous size of transactions

• Non-uniform time duration between consecutive transactions

• Other stylized facts

References

1. Mantegna R.N. and Stanley H.E An Introduction to Econophysics, Cambridge University Press 2000

2. Johnson N. F., Jefferies P., Huy P.M. Financial Market Complexity. Oxford Finance 2003

3. Bouchaud J. P. and Potter M. Theory of Financial Risks : From Statistical Physics to Risk Management. Cambridge University Press 2000.

4. Sznajd-Weron, K.; Sznajd, J. Opinion Evolution in Closed Community. Int. J. Mod. Phys. C 11 1157-1166 (2000).

5. Stauffer, D. Monte Carlo Simulations of the Sznajd model, Journal of Artificial Societies and Social Simulation 5, No.1 paper 4 (2002) (jasss.soc.surrey.ac.uk).

6. Stauffer, D. Frustration from Simultaneous Updating in Sznajd Consensus Model. (cond-mat/0207598 Preprint for J. Math. Sociology)

7. Sabatelli, L.; Richmond, P. Phase transitions, memory and frustration in a Sznajd-like model with synchronous updating. Int. J. Mod.Phys C 14 No. 9 (2003) (cond-mat/0305015).

8. Sabatelli, L.; Richmond, P. Non-monotonic spontaneous magnetization in a Sznajd-like Consensus Model. To be published in Physica A (cond-mat/0309375)

Stylised facts

• Why is the pdf tail equal to 3?– Is it a tunable parameter or more like a critical

exponent?

• What are minimum requirements needed to get the familiar stylised facts?

• Are we looking at all the relevant stylised facts?– Time?

• Shape, asymmetry of speculative peaks?• Log periodic oscillations?• Higher order correlations

Agents

• What form does heterogeneity take?• How do people differ?

• What do they order at the restaurant?

– Is only time heterogeneity required for fat tails and clustered volatility?

Networks

• How are we connected?• How do connections and nodes evolve?• Risk

– How do we evolve containment and innoculation strategies?

– Diffuse rumour & heresy– Social problems

• Eg Drug addiction, smoking, disease

Financial markets are only a part of the subject

• Many other economic systems• Impact on social and regulatory policy

• Electricity• Telecommunications• Transport

• Taxation– Impact on wealth

• Real options,• Weather derivatives, etc• Real worlds (Ormorod)