confidential investor update - saka energi...neither pgn saka nor any of its respective affiliates,...

TRANSCRIPT

Confidential

4Q-2016

INVESTOR UPDATE

1

This presentation has been prepared by PT Saka Energi Indonesia (“PGN Saka” of the “Company”) and is only for informational purposes and does not constitute arecommendation regarding the securities or debt of PGN Saka or any of its subsidiaries, or an investment in the Company. The information in this presentation is confidential andnone of the information appearing in this presentation may be distributed to the press or other media or reproduced or redistributed in whole or in part in any form at any timewithout the prior written consent from the Company. This document remains the property of PGN Saka and on request must be returned and any copies destroyed.

Neither PGN Saka nor any of its respective affiliates, shareholders, directors, employees, agents, advisors or representatives makes any representation or warranty, eitherexpressed or implied, in relation to the accuracy, completeness or reliability of the information contained in this presentation, nor is this presentation intended to be a completestatement or summary of the state and condition of the Company. The information set out herein may be subject to updating, completion, revision, verification and amendmentwithout notice and such information may change materially. The information in this presentation should not be regarded by recipients as a substitute for the exercise of their ownjudgement.

This presentation is not intended as, and does not form part of, any offer to sell or subscription of or solicitation or invitation to buy or subscribe for any securities. Neither thispresentation nor anything contained herein shall form the basis of, or be relied on in connection with, any contract or commitment whatsoever.

This presentation contains forward-looking statements relating to PGN Saka operations that are based on management’s current expectations, estimates and projections aboutthe petroleum. Words or phrases such as “expects,” “forecast,” “projects,” “estimates,” “may,” “could,” “outlook,” “on schedule,” “on track,” and similar expressions areintended to identify such forward-looking statements. These statements are not guarantees of future performance and are subject to certain risks uncertainties and otherfactors, many of which are beyond the company’s control and are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed orforecasted in such forward-looking statements. The reader should not place undue reliance on these forward-looking statements, which speak only as of the date of thispresentation. Unless legally required, PGN Saka undertakes no obligation to update publicly any forward-looking statements, whether as a result of new information, futureevents or otherwise.

Among the important factors that could cause actual results to differ materially from those in the forward-looking statements are: changing crude oil and natural gas prices;changing refining, marketing and chemicals margins; the company’s ability to realize anticipated cost savings and expenditure reductions; actions of competitors or regulators;timing of exploration expenses; timing of crude oil lifting's; the competitiveness of alternate-energy sources or product substitutes; technological developments; the business,results of operations and financial condition of the company’s suppliers, vendors, partners, and equity affiliates, particularly during extended periods of low prices for crude oiland natural gas; the inability or failure of the company’s joint-venture partners to fund their share of operations and development activities; the potential failure to achieveexpected net production from existing and future crude oil and natural gas development projects; potential delays in the development, construction or start-up of plannedprojects; changing economic, regulatory and political environments in the various countries in which the company operates; the potential liability for remedial actions orassessments under existing or future environmental regulations and litigation; significant business, operational, investment or product changes required by existing or futureenvironmental statutes and regulations, the company’s future acquisition or disposition of assets and gains and losses from asset dispositions or impairments; government-mandated sales, divestitures, recapitalizations, industry-specific taxes, changes in fiscal terms or restrictions on scope of company operations; foreign currency movementscompared with the U.S. dollar; the effects of changed accounting rules under generally accepted accounting principles promulgated by rule-setting bodies. Other unpredictable orunknown factors not discussed in this presentation could also have material adverse effects on forward-looking statements. No assurance can be given that further events willoccur, that projections will be achieved, or that the Company’s assumptions are correct. Actual results may differ materially from those projected.

Any opinions expressed in the presentation are subject to change without notice and may differ or be contrary to opinions expressed by other businesses areas or groups of theCompany as a result of using different assumptions and criterion or otherwise.

Cautionary statement

1

Business Profile and Corporate Strategy

Section 1

3

Business strategy

Identify and pursue new growth focus areas that align with PGN Saka’s mission and strategy

Together, with PGN control, support critical operations and infrastructure segments of the oil and gas value chain

Pursue value driven investment opportunities to support organic value creation

Team of highly motivated professionals with vast industry knowledge and experience

Leverage PGN’s strong sponsor commitment and synergiesTo be Indonesia’s leading upstream natural gas focused development and production company

Vision

To deliver value to its stakeholders through:

A balanced gas-focused portfolio of assets

Exploit synergies with PGN and its other subsidiaries

Operatorship of strategic oil and gas assets (both conventional and non-conventional)

Mission

Drive for results

Excellent service

Ethics

Professionalism

Safety

Values

3

4

Historical milestonesPGN Saka has grown into a major player in Indonesia’s O&G sector soon since its founding by PGN and backed by from strong parental capital support of more than US$1.9bn

Cap

ital

Su

pp

ort

Op

era

tio

nal

Ex

celle

nce

2011 2012 2013 20152014 2016

Established in June 2011

Stra

tegi

c A

cqu

isit

ion

s

Organizational and expertise build up

Pangkah: took over OperatorshipKetapang & Muriah: completion of

production facilitiesSouth Sesulu: 3D acquisition

Pangkah: Sidayu 3 discoveryKetapang & Muriah: first production

South Sesulu: Sis#A discoveryBangkanai: completion of

production facilities

Pangkah: Sidayu 4 discoverBangkanai: first production

(commissioning)

Review ofselectedtargets

20% PI in Ketapang PSC25% PI in Pangkah PSC

30% PI in Bangkanai PSC

Rem. 75% PI in Pangkah PSC

100% PI in South Sesulu PSC36% PI in Fasken block

8.9% PI in S.east Sumatra PSC20% PI in Muriah PSC

30% PI in W. Bangkanai PSC11.67% PI in Muara Bakau PSC

100% PI in Wokam PSC

37.81% PI in Sanga-Sanga PSC

US$81 million shareholder loanUS$528 million equity conversion

US$367 million shareholder loanUS$529 million equity conversion

US$390 million shareholder loanUS$4 million

equity injection by PGN

Notes:1 US$500 million drawn down as of 31 December 2016, US$100 million available2 US$100 million drawn down as of 31 December 2016, US$50 million available

Fun

din

g

US$600 million syndicated loan1 US$150 million bank loan2

4

5

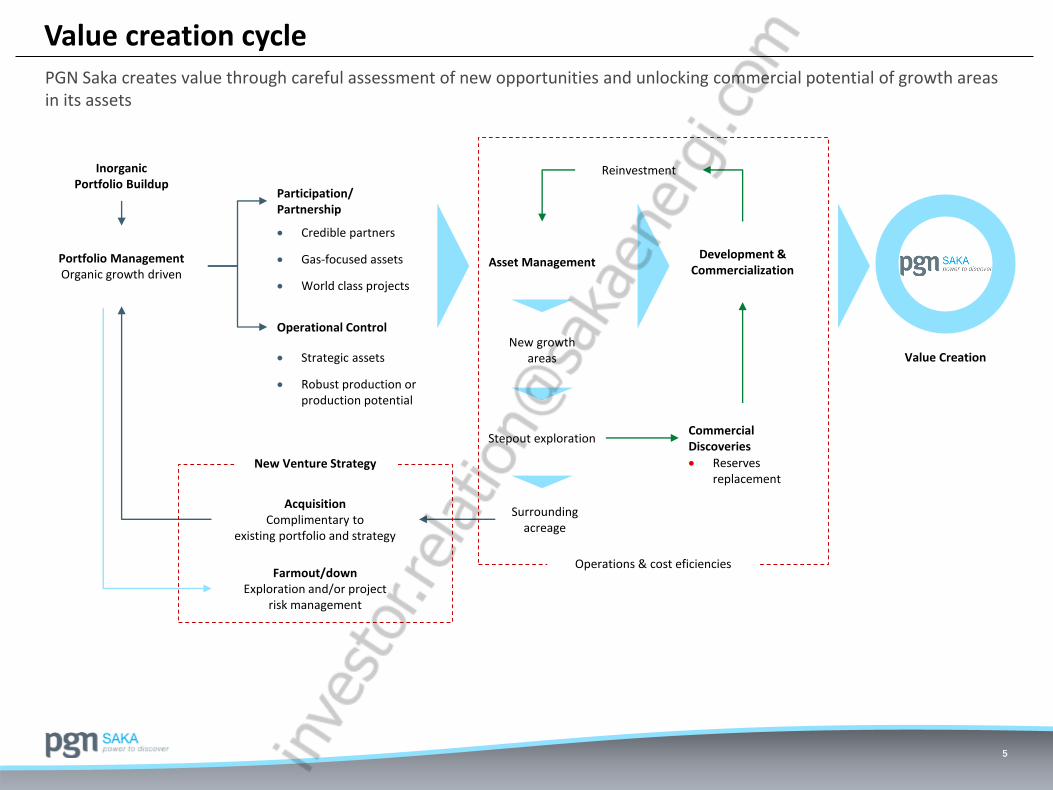

Value creation cyclePGN Saka creates value through careful assessment of new opportunities and unlocking commercial potential of growth areas in its assets

Portfolio ManagementOrganic growth driven

Participation/ Partnership

Operational Control

Value Creation

AcquisitionComplimentary to

existing portfolio and strategy

Inorganic Portfolio Buildup

Farmout/downExploration and/or project

risk management

New Venture Strategy

Credible partners

Gas-focused assets

World class projects

Strategic assets

Robust production or production potential

Asset Management

New growth areas

Stepout exploration

Development & Commercialization

Reinvestment

Surrounding acreage

Commercial Discoveries

Reserves replacement

Operations & cost eficiencies

5

6

Shareholding and organizational structurePGN Saka is a 100%-owned subsidiary of PGN, and is ultimately majority owned by the Indonesian government.

100%

0.10%

0.10%

0.10%

0.10%

0.05%

0.05%

0.025%

0.05% 99.95%

99.975%

99.50%

99.50%

99.90%

99.90%

99.90%

99.90%

0.003%

46.03%56.97%

99.997%

PT Saka Energi

Investasi (SEInv)

PT Saka Energi

Sumatra (SES)

PT Saka Ketapang

Perdana (SKP)

PT Saka Indonesia

Sesulu (SIS)

PT Saka Bangkanai

Klemantan (SBK)

PT Saka Energi

Muara Bakau (SEMB)

PT Saka Energi

Internasional (SEInt)

PT Saka Energi

Bangkanai Barat

PT Saka Energi

Wokam (SEW)

PT Saka Energi

Sepinggan (SEPP)

Saka Energi Fasken

LLC (SEFLLC)

Saka Indonesia

Pangkah BV (SIPBV)

Saka Energi Overseas

Holding BV (SEOH)

Saka Indonesia

Pangkah Ltd (SIPL)

Saka Pangkah LLC

(SPLLC)

Saka Energi Explor.

Prod. BV (SEEP)

Saka Energi Muriah

Ltd (SEML)

100%

100%

100%100%

100%

100%

99.90%

99.90%

0.10%

0.10%

Effectively, 100%

Credit ratings (Moody’s / S&P / Fitch):

Republic of Indonesia: Baa3 / BB+ / BBB-

PGN: Baa3 / BB+ / BBB-

PGN standalone: Baa3 / BBB- / BBB

Saka Energi Asia

Pte.Ltd.

Saka Energi East

Kalimantan Pte LtdSaka Energi Sanga

Star Pte.Ltd

Saka Energi East

Kalimantan Pte LtdUnimar LLC

100%

100%

100%

100%

Virginia International

Co.LLC

Virginia Indonesia

Co.LLC

50%50%

Saka Energi Pekawai

(SEP)Saka Eksplorasi

Baru (SEB)

99.90%

Saka Eksplorasi

Timur (SET)

0.10%

99.90%

99.90%

50%

0.10%

0.10%

Effectively, 100%

7

Balanced mixed portfolio in strategic locations

7

PGN Saka’s assets in Indonesia are clustered around current and future PGN hubs, securing upstream gas resource for PGN's infrastructure build-up

Note:

FSRU = Floating Storage Regasification Unit

1. Future planned FSRU

Production Development/Discovery Exploration

Existing PGN pipeline Planned PGN pipeline

• Location : Webb County, Texas, United States

• Working Interest : 36%

• Operator & Partner : Swift Energy (64%)

Fasken

• Location : offshore southeast Sumatra

• Working Interest : 8.9%

• Operator : CNOOC (66%)

• Partners : Pertamina (20%)KUFPEC (5%)

• Location : offshore Java sea

• Working Interest : 20%

• Operator & Partner : Petronas (80%)

Muriah PSC

• Location : offshore Java sea

• Working Interest : 100%

• Operator : PGN Saka

Pangkah PSC

• Location : offshore East Java

• Working Interest : 20%

• Operator & Partner : Petronas (80%)

Ketapang PSC

Wokam II

TangguhLNG Facility

4SES

FSRU

MuaraBakau

KetapangFSRU

Pontianak

West YamdenaFSRU1

FSRU1

Future MaselaLNG Facility

FSRU1

Sanga Sanga

South Sesulu

Pekawai

Pangkah

Muriah

Palangkaraya

Banjarmasin

Wokam II

• Location : offshore Papua

• Working Interest : 100%

• Operator : PGN Saka

Wokam II PSC

• Location : onshore Kutei basin

• Working Interest : 30%

• Operator & Partner : OPHIR (70%)

Bangkanai PSC

• Location : onshore Kutei basin

• Working Interest : 30%

• Operator & Partner : OPHIR (70%)

West Bangkanai PSC

Southeast Sumatra (SES) PSC

Java Sea Hub

• Location : offshore Kutei basin

• Working Interest : 100%

• Operator : PGN Saka

South Sesulu PSC

• Location : offshore Kutei basin

• Working Interest : 11.7%

• Operator : ENI (55%)

• Partners : Engie (33.334%)

Muara Bakau PSC

Strategy: “Expanding Energy Infrastructure”

1) Java Sea Hub : Java – South Eastern Indonesia

2) Kutei Hub : Kalimantan – Eastern Indonesia

3) Western Indonesia Hub : Sumatra – Java

4) Papua Hub : Papua

3b

3a

1

2

4Kutei Hub

Timika

Merauke

Tangguh LNG Facility

• Location : onshore Kutei basin

• Working Interest : 37.8%

• Joint operators : PGN Saka,ENI (37.8%)

• Partners : CPC (20%), UniverseGas & Oil (4.4%)

Sanga Sanga PSC

International

ArunLNG Facility

Bontang LNG Facility

Donggi-SenoroLNG Facility

Tarakan

Tj. Selor

Samarinda

The Industry

Section 2

9

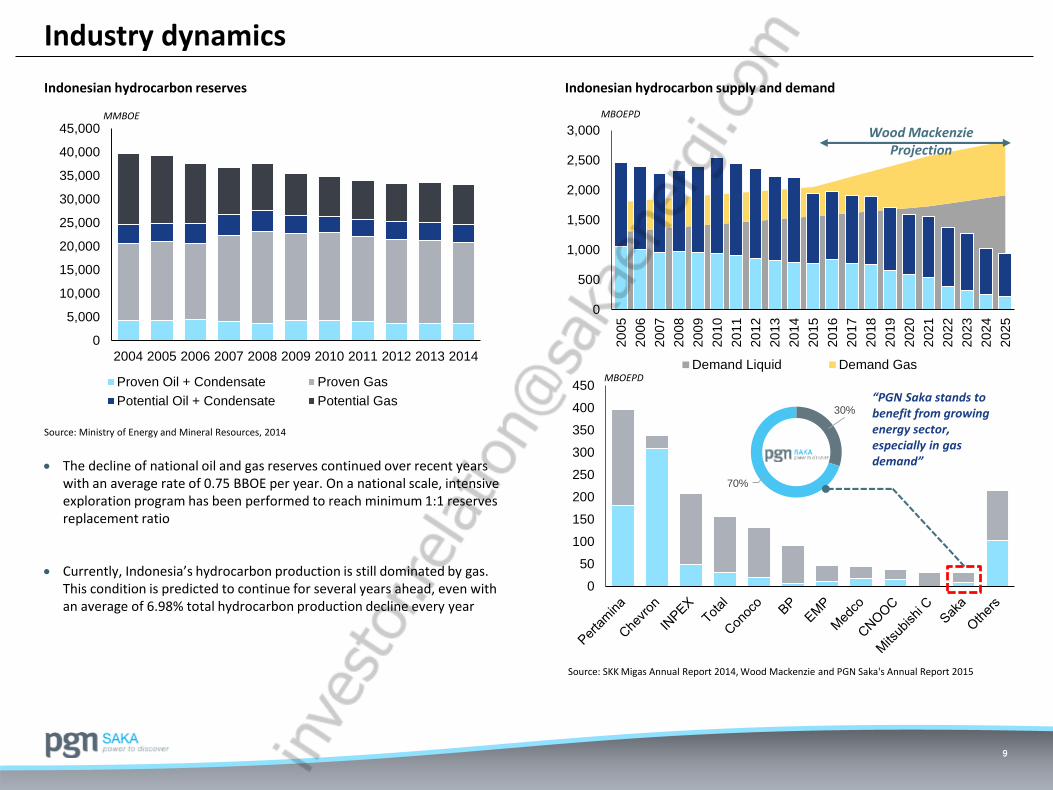

Industry dynamics

The decline of national oil and gas reserves continued over recent years with an average rate of 0.75 BBOE per year. On a national scale, intensive exploration program has been performed to reach minimum 1:1 reserves replacement ratio

Currently, Indonesia’s hydrocarbon production is still dominated by gas. This condition is predicted to continue for several years ahead, even with an average of 6.98% total hydrocarbon production decline every year

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Proven Oil + Condensate Proven Gas

Potential Oil + Condensate Potential Gas

Indonesian hydrocarbon reserves

Source: Ministry of Energy and Mineral Resources, 2014

MMBOE

0

50

100

150

200

250

300

350

400

450

Indonesian hydrocarbon supply and demand

0

500

1,000

1,500

2,000

2,500

3,000

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

Demand Liquid Demand Gas

Wood Mackenzie Projection

30%

70%

MBOEPD

MBOEPD

Source: SKK Migas Annual Report 2014, Wood Mackenzie and PGN Saka's Annual Report 2015

“PGN Saka stands to benefit from growing energy sector, especially in gas demand”

9

10

Industry background

Government Contractor

ETS x Government Share

FTP x Government Share FTP x Contractor Share

Cost Recovery

ETS x Contractor Share

DMO Fee to ContractorDMO to State

Tax from Contractor

DMO Fee to Contractor DMO to State

(+) (+)

(+)

(+) (+)

(-)

(+)

(-)

(+)

Tax to Government(-)(+)

Gross Production

FTP = 20% x GrossProduction

Cost Recovery

ETS (Equity to be Split)

Government Entitlement

Contractor Entitlement

Contractor and Government split FTP according to the agreed split ratio right after gross production

PSC specifies that a portion of gross production (after deducted by FTP) will be the maximum amount available for cost recovery

Contractor is entitled to recover all current cost (subject to SKK Migas approval) for the working area that has the approved Plan of Development (POD), including but not limited to production costs, amortized exploration costs, and capital expenditures

Remaining amount generated from subtraction of gross production with FTP and cost recovery will produce ETS, which will be split according to the agreed split ratio

After 60 months from the commencing of production, contractor requires to supply a share of production to satisfy Domestic Market Obligation (DMO). The quantity and price of DMO oil is stipulated in the PSC

Start of PSC

Start FEED

Start of EPCI

Contractor Cash Flow

Onstream

End

of PSC

Pre-POD

POD

EXPLORATION EXPLOITATION (APPRAISAL, DEVELOPMENT AND PRODUCTION) DECOMMISSIONING

Business process PSC accountingEXPLORATION

1 – 6 Yr 1 – 8 Yr 10 – 30 Yr 1 – 2 Yr

Prospect

Appraisal

Preliminary

Development Study

Discovery

Concept

Project

Project First Production

Operation and Production

Restoration

End of Economic Life

Exploration

Pre-Project

APPRAISAL AND DEVELOPMENT

PRODUCTION DECOMMISSIONING

10

Operational & Financial Performance

Section 3

12

Operational Performance

12

Crude Oil Production (MMBBL) Crude Oil & Condensate (BBLS)

Gas (MMBTU)

LPG (MT)

LIFT

ING

2015 2016

Total Crude Oil Lifting 2,609,407 3,095,186

2015 2016

Total LPG Lifting 43,321 50,518

2015 2016

Total Gas Lifting 33,673,024 40,793,792

LNG (MMBTU)

2015 2016

Total LNG Lifting 0 3,066,186

0.25

-

0.01

-

-

-

1.27

0.37

-

-

1.04

1.08

2.23

2.36

2016

2015

2016

2015

2016

2015

2016

2015

2016

2015

2016

2015

2016

2015

San

ga-

San

gaB

angk

anai

Mu

riah

Ket

apan

gFa

sken

SES

Pan

gkah

5,357

-

247

1

6,866

2,341

908

241

20,212

20,446

5,059

4,354

19,460

17,451

2016

2015

2016

2015

2016

2015

2016

2015

2016

2015

2016

2015

2016

2015

San

ga-

San

gaB

angk

anai

Mu

riah

Ket

apan

gFa

sken

SES

Pan

gkah

2015 2016

Total Crude Oil Production 3.81 4.80

2015 2016

Total GasProduction 44,834 58,109

Gas Production (MMSCF)

1,072,000

269,000

650,316

806,001

1,372,870

1,534,406

2016

2015

2016

2015

2016

2015

Ket

apan

gSE

SP

angk

ah

716

0

49,803

43,321

2016

2015

2016

2015

San

ga-S

anga

Pan

gkah

308,377

0

0

6,140,158

2,080,713

429,141

0

16,841,832

16,747,018

1,659,184

1,375,677

15,415,099

13,469,617

2016

2015

2016

2015

2016

2015

2016

2015

2016

2015

2016

2015

2016

2015

San

ga-

San

gaB

angk

anai

Mu

riah

Ket

apan

gFa

sken

SES

Pan

gkah

3,066,186

0

2016

2015

San

ga-S

anga

13

10.37

8.27

5.08

2014 2015 2016

Financial KPIs

13

Debt to EBITDA

Capital Structure

EBITDA

Million USD

Revenues

Million USD

Total Debt to Equity

ISCR

Max: 4.5 x

35.97%

21.46%4.29%

38.28%

SHL

CL

RCF

Equity

297.80 263.70

314.11

2014 2015 2016

0.44

1.25

1.61

2014 2015 2016

Max: 1.86 x

1.75

3.30

2014 2015 2016

Min

: 4

.0 x

“Despite low oil price environment and uncertainty of the energy market, SAKA kept

on ramping up its production volume to maintain its revenue level and recorded

$182.88 million of EBITDA, 18.6% increase compared to that of in 2015.”

in USD million

Consolidated Comprehensive Income Statement

2014 2015 2016

(Audited) (Audited) (Audited)

Revenues 297.80 263.70 314.11

Cost of Revenues (172.40) (251.85) (302.70)

Gross Profit 125.40 11.85 11.41

Operating Expense (10.75) (6.80) (10.82)

Operating Profit 114.65 5.05 0.59

Total Other Income (Expense) (36.19) (194.60) (32.22)

EBITDA 205.22 154.15 182.80

Profit (Loss) before Tax Benefit (Expense) 78.46 (189.56) (31.63)

Total Tax Benefit (Expense) (57.67) 76.39 8.28

Profit (Loss) for this Year 20.79 (113.19) (23.35)

Consolidated Balance Sheet 2014 2015 2016

(Audited) (Audited) (Aaudited)

Current Assets 288.88 320.77 546.36

Non-Current Assets 1,605.19 2,021.03 2,123.29

Total Assets 1,894.07 2,341.80 2,669.65

Current Liabilities 660.16 192.19 334.57

Non-Current Liabilities 207.42 1,235.92 1,443.02

Total Equity 1,026.48 913.69 892.06

Total Liabilities and Equity 1,894.06 2,341.80 2,669.65

205.22

154.15

182.88

2014 2015 2016

14

2016 Revenue Performance

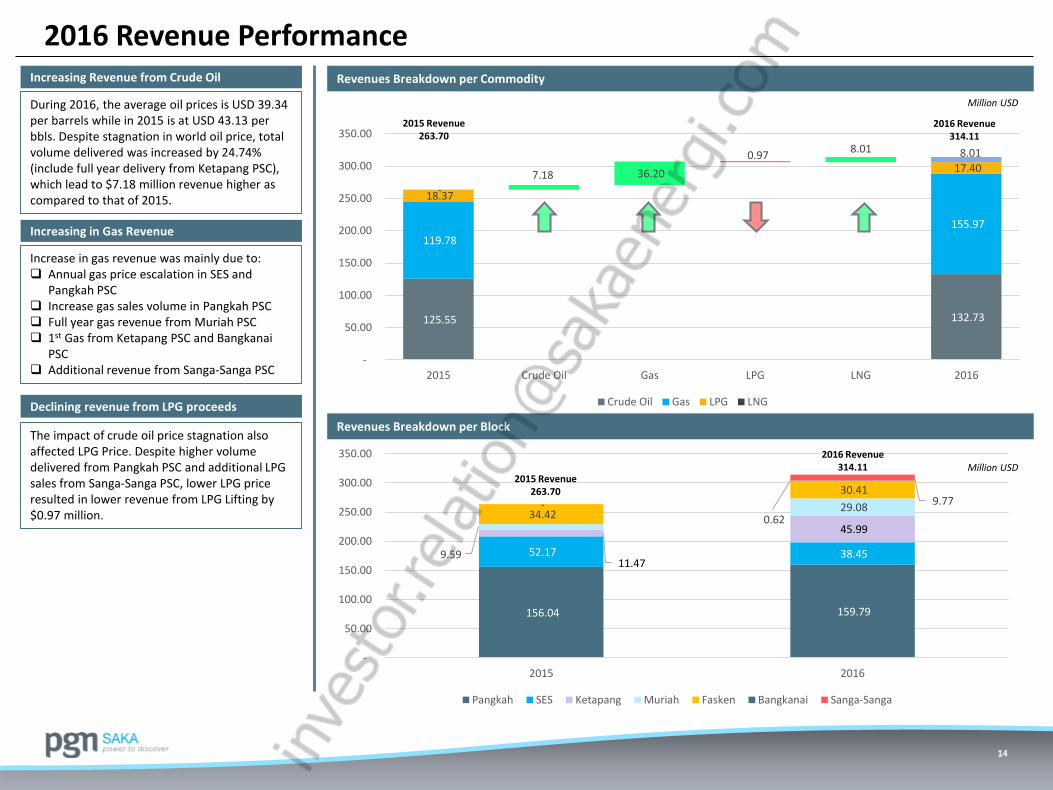

14

Revenues Breakdown per Commodity

During 2016, the average oil prices is USD 39.34 per barrels while in 2015 is at USD 43.13 per bbls. Despite stagnation in world oil price, total volume delivered was increased by 24.74% (include full year delivery from Ketapang PSC), which lead to $7.18 million revenue higher as compared to that of 2015.

Increasing Revenue from Crude Oil

Increase in gas revenue was mainly due to: Annual gas price escalation in SES and

Pangkah PSC Increase gas sales volume in Pangkah PSC Full year gas revenue from Muriah PSC 1st Gas from Ketapang PSC and Bangkanai

PSC Additional revenue from Sanga-Sanga PSC

Increasing in Gas Revenue

The impact of crude oil price stagnation also affected LPG Price. Despite higher volume delivered from Pangkah PSC and additional LPG sales from Sanga-Sanga PSC, lower LPG price resulted in lower revenue from LPG Lifting by $0.97 million.

Declining revenue from LPG proceeds

Million USD

125.55 132.73

119.78

155.97

18.37

17.40

8.01

-7.18 36.20

0.97 8.01

-

50.00

100.00

150.00

200.00

250.00

300.00

350.00

2015 Crude Oil Gas LPG LNG 2016

Crude Oil Gas LPG LNG

Million USD

2015 Revenue263.70

2016 Revenue314.11

156.04 159.79

52.17 38.45 11.47

45.99

9.59

29.08 34.42

30.41 -

0.62

9.77

-

50.00

100.00

150.00

200.00

250.00

300.00

350.00

2015 2016

Pangkah SES Ketapang Muriah Fasken Bangkanai Sanga-Sanga

Revenues Breakdown per Block

2015 Revenue263.70

2016 Revenue314.11

Corporate Update and Project Initiatives

Section 4

16

Pangkah PSC – Operational Update

16

Pangkah PSCType of Contract : PSCArea : 784 Km2Contract Expiration : May 2026Participating Interest : Saka Indonesia Pangkah Ltd

(65%, Operator) Saka Pangkah LLC (10%) Saka Indoensia Pangkah BV (25%)

Location : East JavaFTP Rate : 20%After Tax Split : Oil - 85 : 15

Gas - 70 : 30Tax Rate : 44%DMO Holiday : 60 month after production commencedDMO Price : 15% of ICPInvestment Credit : 15.78% of tangible CAPEXStatus : Production (since 2007)

No Activity 2016 Progress Next Plan

1 Exploration Completed 2 development wells (UPA-1X and UPA-08X) with cost effective approach and executed under the approved budget.

Preparation of 2017 development program for SKK Migas approval.

Exploration drilling on Ronggolawe-2

2 Workover Program Completed 2 workover works in UPA-02ST2 and UPA-05 to optimize the well’s production rate and successfully delivered 300 BOPD and 7 MMSCFD gain to 2016 production rate.

Succesfully compeleted conversion of water disposal (UPA-WD1) to producer well which resulted 8 MMSCFD additional production and under budget.

Preparation of 2017 workover program which consist of 6 potential workover wells and expected additional 9.8 BCF and 1.47 MMBO

Workover program on xx wells

3 Well Intervention Well intervention works with coiled tubing in 17 wells have delivered significant contribution to achieve production target by having initial gain of 4,100 BEOPD.

Well intervention on xx wells

4 Interruptible Line Tie-in to Pangkah Facility

Facility Sharing Agreement (FSA) discussion between Petronas and SIPL is still in progress.

Completion is expected by end of 2017

5 Commercial Update Signed 1-year Crude Oil Sales Agreement with Itochu

6 Gross Production2016

Crude Oil: 4,372 BOPD Gas: 53.17 MMSCFD

17

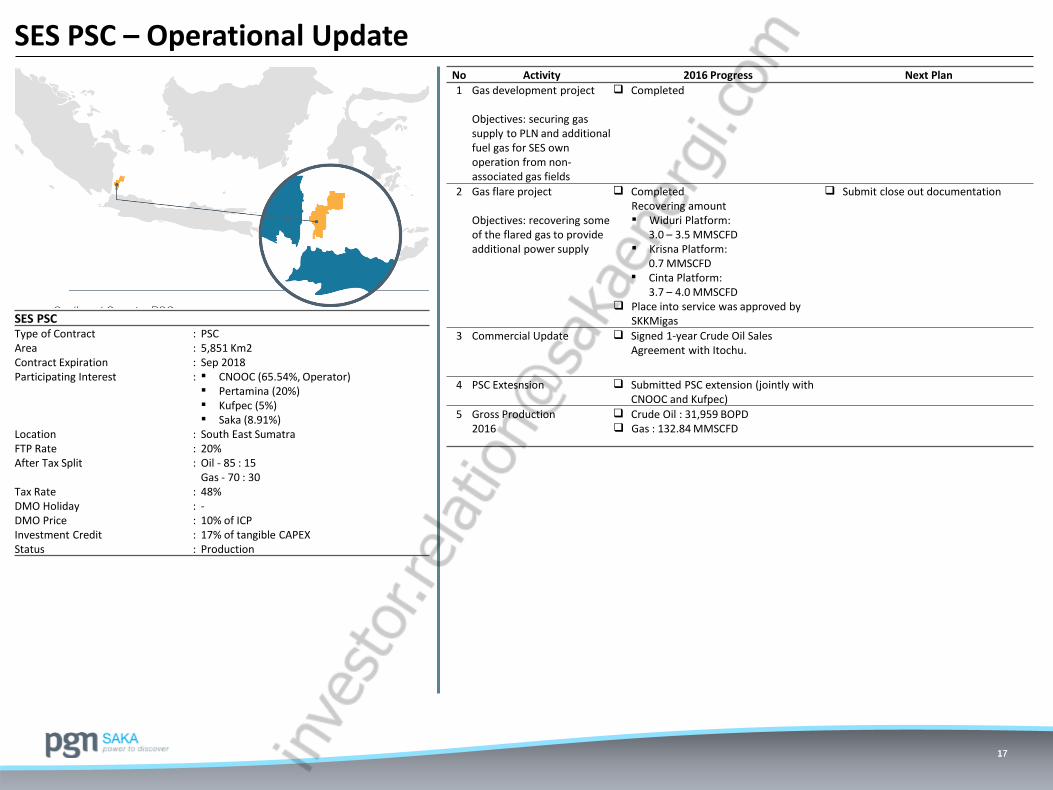

SES PSC – Operational Update

17

SES PSCType of Contract : PSCArea : 5,851 Km2Contract Expiration : Sep 2018Participating Interest : CNOOC (65.54%, Operator)

Pertamina (20%) Kufpec (5%) Saka (8.91%)

Location : South East SumatraFTP Rate : 20%After Tax Split : Oil - 85 : 15

Gas - 70 : 30Tax Rate : 48%DMO Holiday : -DMO Price : 10% of ICPInvestment Credit : 17% of tangible CAPEXStatus : Production

No Activity 2016 Progress Next Plan

1 Gas development project

Objectives: securing gas supply to PLN and additionalfuel gas for SES own operation from non-associated gas fields

Completed

2 Gas flare project

Objectives: recovering some of the flared gas to provide additional power supply

CompletedRecovering amount Widuri Platform:

3.0 – 3.5 MMSCFD Krisna Platform:

0.7 MMSCFD Cinta Platform:

3.7 – 4.0 MMSCFD Place into service was approved by

SKKMigas

Submit close out documentation

3 Commercial Update Signed 1-year Crude Oil Sales Agreement with Itochu.

4 PSC Extesnsion Submitted PSC extension (jointly with CNOOC and Kufpec)

5 Gross Production 2016

Crude Oil : 31,959 BOPD Gas : 132.84 MMSCFD

18

Ketapang PSC – Operational Update

18

Ketapang PSCType of Contract : PSCArea : 885 Km2Contract Expiration : Jun 2028Participating Interest : Petronas (80%, Operator)

PT Saka Ketapang Perdana (20%)Location : East JavaFTP Rate : 20%After Tax Split : Oil - 85 : 15

Gas - 70 : 30Tax Rate : 44%DMO Holiday : 60 month after production commencedDMO Price : 15% of ICPInvestment Credit : 15.78% of tangible CAPEXStatus : Production (since 2015)

No Activity 2016 Progress Next Plan

1 Project Facility Completed Installation of artificial lift (gas lift) in Bukit Tua wells (BTJT-Z2 and BTJT-Z5).

2 Operation Prepare POD submission for Bukit Tuaphase II.

3 Drilling & Completion Completed BTJT-Z1 in July 2016 with the result of 20 MMSCFD of gas.

To Start opening Kujung I formation for well Z1 to ramp up and increase gas production as per nomination 43 MMSCFD in 2017.

4 Commercial Update Crude OilSigned 1-year Crude Oil Sales Agreement with Itochu.

Gas Started PJU’s pipeline

commissioning on 25 Jul 2016. Gas allocation and price approval

has been obtained from Ministry of Energy and Mineral Resources. Year-1 price is $5.50/MMBTU.

5 Interruptible line tie-in to Pangkah facility

FSA (Facility Sharing Agreement) draft sent to SKK Migas.

Continue tie in work execution inside SIPL. Excavation, trenching and pipe welding is ongoing. Bore piling is in progress.

FSA finalization between SIPL and Petronas

Continue rectification compressor and cooler on GTC-1

6 PJU PJU’s LPG plant completed to reduce Gross Heating Value (GHV) from thegas sales transported to PLN.

The additional 700m pipeline to PLN’s re-boiler has been completed (prepared as the backup plan if PJU’s LPG plant encounter any problems).

PJU has obtained trading license for trading the gas from Ketapang.

Discussion is underway between PJU and PLN to accommodate higher gas rate of Ketapang Gas in 2017.

7 Condensate Handling Continue receiving condensate and burn intermittently.

Preparing strategy on condensate handling.

To be discussed with SKK Migas

8 Gross Production2016

Crude Oil: 17,328 BOPD Gas: 12.45 MMSCFD

19

Muriah PSC – Operational Update

19

Muriah PSCType of Contract : PSCArea : 2,823 Km2Contract Expiration : May 2026Participating Interest : Petronas (80%, Operator)

Saka Energi Muriah Ltd (20%)Location : Java SeaFTP Rate : 20%After Tax Split : Oil - 85 : 15

Gas - 70 : 30Tax Rate : 48%DMO Holiday : -DMO Price : -Investment Credit : 17% of tangible CAPEXStatus : Production (since 2015)

No Activity 2016 Progress Next Plan

1 Production recovery Lowering down sales gas nomination to 82 MMSCFD.

Installed new flow line to new development well to maintain production level.

Obtained approval from SKKMigas to drill 2 more additional wells.

Increased choke size to maintain gas production.

Compressor re-staging with the estimate of commissioning and installation in Q1-2017.

Well intervention.

2 Drilling Well KEJT-C4 Spudded on 30 Oct 2016 @ 11:00.

Clean out 24” conductor casing from 478 ft to 660 ft and drill formation to 690 ft.

Continue drilling 17-1/2“ OH to section TD @ 2093 ft. Reached TD for casing 13-3/8” @ 2,093 ft. RIH and cement casing 13-3/8”.

Skid to C-3

Well KEJT-C3 Completed drilling Took 8 points of pressure test

using LWD TestTrak with 7 good results and 1 lost seal. Average pressure 870 psi / 6.4 ppg. Lower than original pressure of LTA-1 (1100 psi).

1st

Gas was on Dec 2016

1st

Gas is expected on Q1-2017.

3 Facility / Operation Kepodang Tie-in & Flowline: EPCC tie in has been awarded. All PO in place for Wet Gas Metering, Wellhead Control Panel & Choke Valve.

Continue optimization and monitor glycol circulation rate to prevent glycol carry over.

Re-Staging delivery and operating in series configuration will be delivered in Q1-2017.

4 Gross production 2016

Gas: 93.80 MMSCFD

20

Fasken – Operational Update

20

FaskenType of Contract : Lease ContractArea : 8,300 acreContract Expiration : Expires when production endsParticipating Interest : Swift Energy (64%, Operator)

Saka Energi Fasken LLC (36%)Location : Webb County, TexasRoyalty : 20%After Tax Split : -

Tax Rate :DMO Holiday : -DMO Price : -Investment Credit : -Status : Production

No Activity 2016 Progress Next Plan

1 Chapter 11 case Swift as the operator of Fasken hasannounced newly constituted BOD in conjunction with the Company’s emergence from Chapter 11.

2 Completion Completion activities on 8 wells (perforation and fracturing) have been completed in July 2016 with the significant production gain from 120 MMSCFD to 190 MMSCFD

Completed tubing installation in 19 wells for maintaining wells performance and stability.

Tubing exchange program for 3 wells has been completed.

Completed 4 wells in PAD I.

Drilling and Completion activities in 11 wells.

To complete PAD I in Q1-2017 Preparing PAD II for drilling in

completion (expected to complete in Q2-2017).

Preparing PAD II for drilling in completion (expected to complete in Q3-2017).

Preparing clean out program (Frac Hit Remediation program and to be completed by end of 2017.

Preparing tubing installation program in 15 wells and to be completed in Q4-2017.

3 Operation Completed Amine unit removal to Howards has been completed to reduce operational activities in Fasken area.

Lowering pressure program is in progress.

To complete lowering pressure program by Q3-2017

Preparing gathering line extension by Q1-2017.

4 Reserves replacement program

Study on production potential in Upper Eagleford, Austin Chalk and Olmos are still in progress.

To complete the study

5 Gross Production 2016

Gas: 153.40 MMSCFD

21

Bangkanai PSC – Operational Update

21

Bangkanai PSCType of Contract : PSCArea : 1,395 Km2Contract Expiration : December 2033Participating Interest : Ophir (70%, Operator)

PT Saka Bangkanai Klemantan (30%)Location : Kalimantan (Kutei)FTP Rate : 20%After Tax Split : Oil - 85 : 15

Gas - 70 : 30Tax Rate : 44%DMO Holiday : 60 month after production commencedDMO Price : 15% of ICPInvestment Credit : 15.78% of tangible CAPEXStatus : Production (2016)

No Activity 2016 Progress Next Plan

1 Gas Kerendan Production Facility (KGPF) and Operation

Completed the full capacity commissioning of KGPF plant with flow rate up to 20.9 mmscfd in 20 minute of the 25 mmscfd max capacity.

Ramp up and deliver sales gas until 20 mmscfd

Methanol supply award kick-off in Q1-2017

2 PLN power plant PLN power plant main facility and transmission line to Tanjung was reported to achieve 100% completion (All transmission line to PLN Facility has been completed)

3 CNG facility project Completed

4 G&G and survey 3D seismic with BGP has signed Basecamp construction ongoing QAQC field seismic tender is awarded

to PT Ceria and Air Energy Forestry permit & UKL/UPL is

completed UKL/UPL is completed

Completed 3D seismic and data processing by end of Q2-2017

Completed basecamp construction by end of Q2-2017

5 Commercial Update Currently waiting SKK Migas instruction

letter for Ophir to continue the partial

gas delivery 5 MMSCFD after 31

October 2016.

GSA amendment is still not signed yet.

PLN is still querying several items of the

GSA amendment.

Condensate Commercialization:

As requested by SKK Migas, there is

ongoing process to select an

independent consultant that will

calculate/estimate handling cost

w.r.t lifting of the condensate.

Pending outcome of estimation of

handling cost, as temporary

arrangement, SKK Migas has

stipulated interim price for the

condensate (56% of ICP Senipah)

hence lifting can be done.

Gas Sales to Perusda: All necessary

documents for re‐due diligence are in

progress.

To finalize condensate delivery procedure.

To finalize condensate handling strategy to prevent tank top and production interruption.

To complete re-due diligence process with Perusda.

To finalize GSA Amendment by 31 Dec 2016.

To finalize the condensate price mechanism.

6 WK-1 Well POP WK-1 POP has been approved by SKK

Migas

Working with PLN plan to absorb additional gas from WK-1 POP.

7 Gross Production 2016

Gas: 1.33 MMSCFD

Condensate : 46 BOPD

22

Sanga-Sanga PSC – Operational Update

22

No Activity 2016 Progress

1 Commercial Update Signed Crude oil sales agreement to BP IST for Badak crude oil and BRC until end of PSC life

2 PSC Extension Submitted to SKK Migas

3 Drilling Program 12 new wells were successfully drilled in Mutiara and Semberah fields.

4 Oil Development Program Rigless program: successfully contributed to 1.4 MBOPD (doubled that original target).

Permanent Coiled Tubing Gas Lift (PCTGL): installed 30 PCTGL installations and resulted in 2.6 MBOPD

5 Gross Production 2016

Crude Oil : 51.89 MBOPD Gas : 210.92 MMSCFD

23

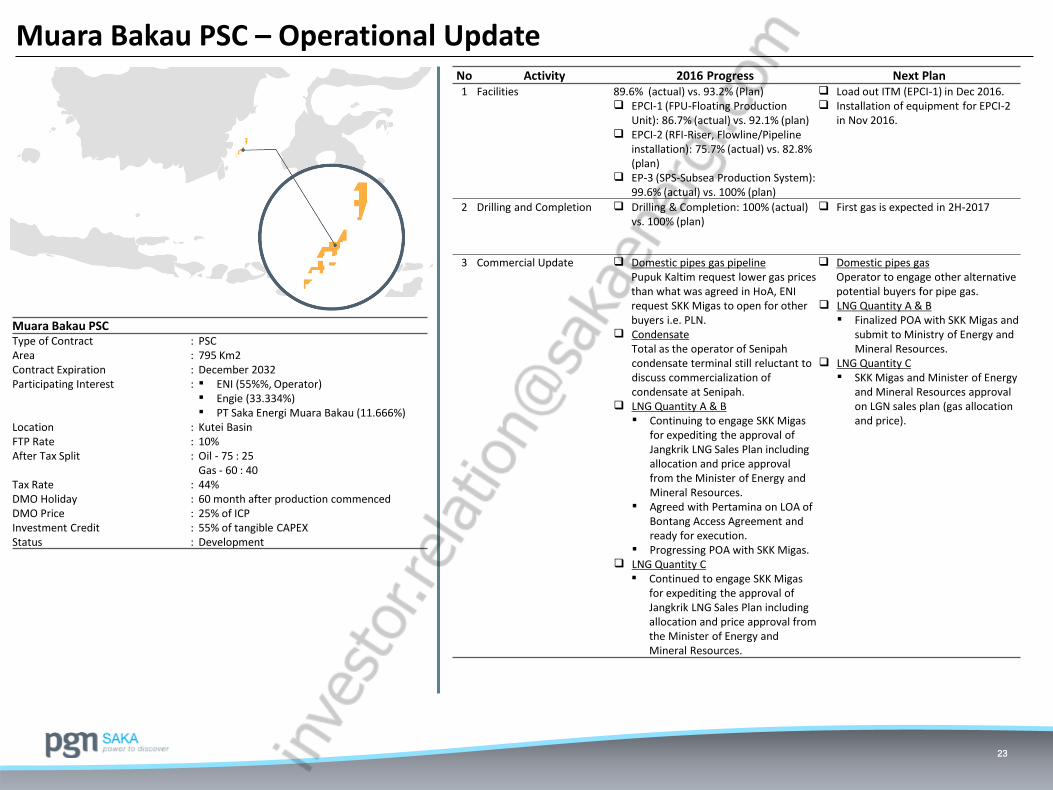

Muara Bakau PSC – Operational Update

23

Muara Bakau PSCType of Contract : PSCArea : 795 Km2Contract Expiration : December 2032Participating Interest : ENI (55%%, Operator)

Engie (33.334%) PT Saka Energi Muara Bakau (11.666%)

Location : Kutei BasinFTP Rate : 10%After Tax Split : Oil - 75 : 25

Gas - 60 : 40Tax Rate : 44%DMO Holiday : 60 month after production commencedDMO Price : 25% of ICPInvestment Credit : 55% of tangible CAPEXStatus : Development

No Activity 2016 Progress Next Plan1 Facilities 89.6% (actual) vs. 93.2% (Plan)

EPCI-1 (FPU-Floating Production Unit): 86.7% (actual) vs. 92.1% (plan)

EPCI-2 (RFI-Riser, Flowline/Pipeline installation): 75.7% (actual) vs. 82.8% (plan)

EP-3 (SPS-Subsea Production System): 99.6% (actual) vs. 100% (plan)

Load out ITM (EPCI-1) in Dec 2016. Installation of equipment for EPCI-2

in Nov 2016.

2 Drilling and Completion Drilling & Completion: 100% (actual) vs. 100% (plan)

First gas is expected in 2H-2017

3 Commercial Update Domestic pipes gas pipelinePupuk Kaltim request lower gas prices than what was agreed in HoA, ENI request SKK Migas to open for other buyers i.e. PLN.

CondensateTotal as the operator of Senipahcondensate terminal still reluctant to discuss commercialization of condensate at Senipah.

LNG Quantity A & B Continuing to engage SKK Migas

for expediting the approval of Jangkrik LNG Sales Plan including allocation and price approval from the Minister of Energy and Mineral Resources.

Agreed with Pertamina on LOA of Bontang Access Agreement and ready for execution.

Progressing POA with SKK Migas. LNG Quantity C

Continued to engage SKK Migasfor expediting the approval of Jangkrik LNG Sales Plan including allocation and price approval from the Minister of Energy and Mineral Resources.

Domestic pipes gasOperator to engage other alternative potential buyers for pipe gas.

LNG Quantity A & B Finalized POA with SKK Migas and

submit to Ministry of Energy and Mineral Resources.

LNG Quantity C SKK Migas and Minister of Energy

and Mineral Resources approval on LGN sales plan (gas allocation and price).

24

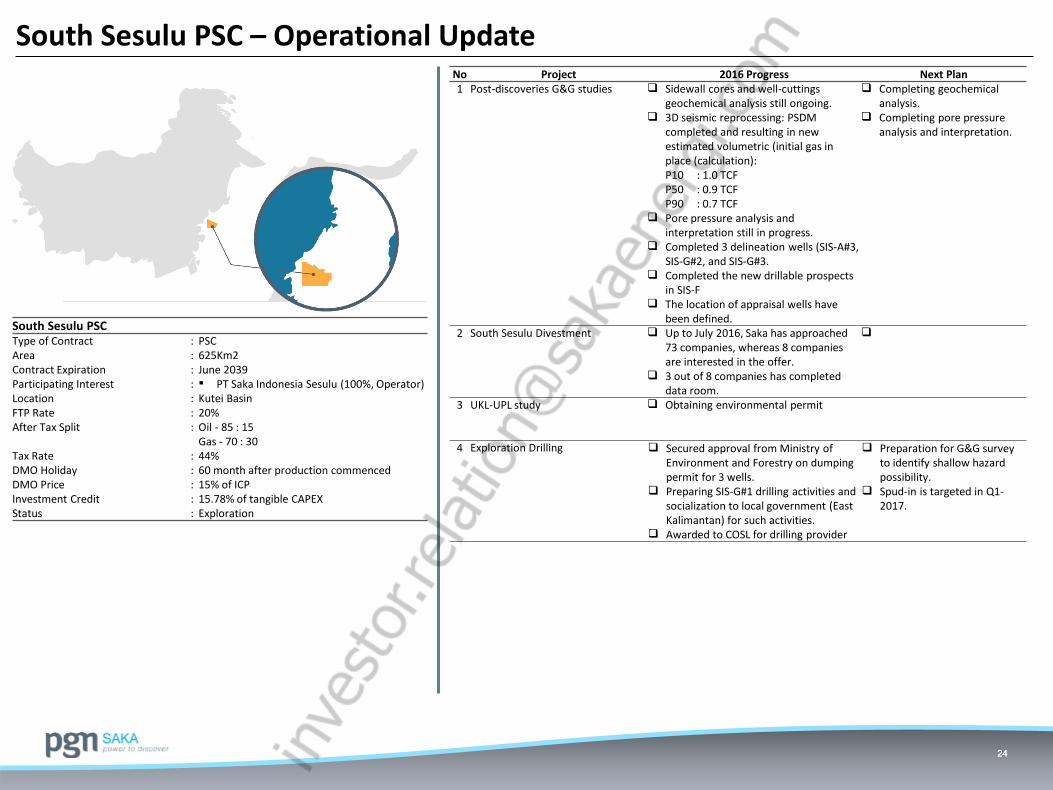

South Sesulu PSC – Operational Update

24

South Sesulu PSCType of Contract : PSCArea : 625Km2Contract Expiration : June 2039Participating Interest : PT Saka Indonesia Sesulu (100%, Operator)Location : Kutei BasinFTP Rate : 20%After Tax Split : Oil - 85 : 15

Gas - 70 : 30Tax Rate : 44%DMO Holiday : 60 month after production commencedDMO Price : 15% of ICPInvestment Credit : 15.78% of tangible CAPEXStatus : Exploration

No Project 2016 Progress Next Plan1 Post-discoveries G&G studies Sidewall cores and well-cuttings

geochemical analysis still ongoing. 3D seismic reprocessing: PSDM

completed and resulting in new estimated volumetric (initial gas in place (calculation):P10 : 1.0 TCFP50 : 0.9 TCFP90 : 0.7 TCF

Pore pressure analysis and interpretation still in progress.

Completed 3 delineation wells (SIS-A#3, SIS-G#2, and SIS-G#3.

Completed the new drillable prospects in SIS-F

The location of appraisal wells have been defined.

Completing geochemical analysis.

Completing pore pressure analysis and interpretation.

2 South Sesulu Divestment Up to July 2016, Saka has approached 73 companies, whereas 8 companies are interested in the offer.

3 out of 8 companies has completed data room.

3 UKL-UPL study Obtaining environmental permit

4 Exploration Drilling Secured approval from Ministry of Environment and Forestry on dumping permit for 3 wells.

Preparing SIS-G#1 drilling activities and socialization to local government (East Kalimantan) for such activities.

Awarded to COSL for drilling provider

Preparation for G&G survey to identify shallow hazard possibility.

Spud-in is targeted in Q1-2017.

25

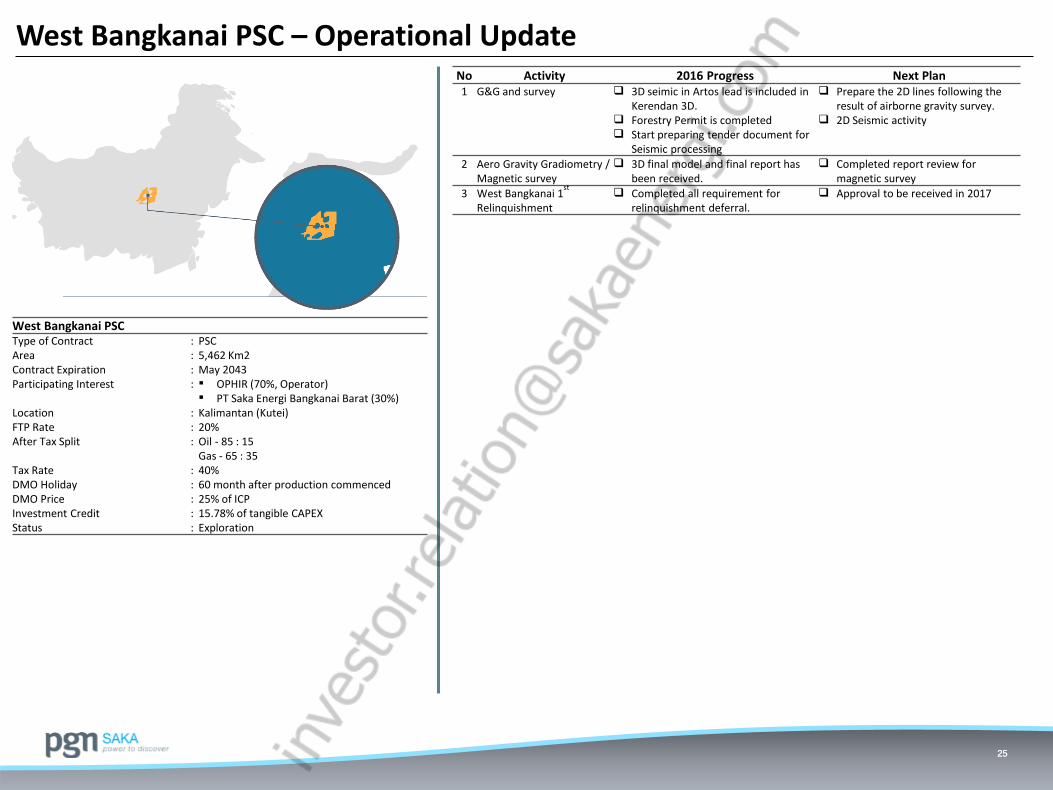

West Bangkanai PSC – Operational Update

25

West Bangkanai PSCType of Contract : PSCArea : 5,462 Km2Contract Expiration : May 2043Participating Interest : OPHIR (70%, Operator)

PT Saka Energi Bangkanai Barat (30%)Location : Kalimantan (Kutei)FTP Rate : 20%After Tax Split : Oil - 85 : 15

Gas - 65 : 35Tax Rate : 40%DMO Holiday : 60 month after production commencedDMO Price : 25% of ICPInvestment Credit : 15.78% of tangible CAPEXStatus : Exploration

No Activity 2016 Progress Next Plan1 G&G and survey 3D seimic in Artos lead is included in

Kerendan 3D. Forestry Permit is completed Start preparing tender document for

Seismic processing

Prepare the 2D lines following the result of airborne gravity survey.

2D Seismic activity

2 Aero Gravity Gradiometry / Magnetic survey

3D final model and final report hasbeen received.

Completed report review for magnetic survey

3 West Bangkanai 1st

Relinquishment

Completed all requirement for relinquishment deferral.

Approval to be received in 2017

26

Wokam II PSC – Operational Update

26

Wokam II PSCType of Contract : PSCArea : 5,462 Km2Contract Expiration : May 2043Participating Interest : OPHIR (70%, Operator)

PT Saka Energi Bangkanai Barat (30%)Location : Kalimantan (Kutei)FTP Rate : 20%After Tax Split : Oil - 85 : 15

Gas - 65 : 35Tax Rate : 40%DMO Holiday : 60 month after production commencedDMO Price : 25% of ICPInvestment Credit : 15.78% of tangible CAPEXStatus : Exploration

No Activity 2016 Progress Next Plan1 G&G and survey Started reprocessing 3D seismic To completed reprocessing and

starting 2D seismic

2 Exploration Extension Received approval from SKK Migas on extension of exploration period

3 Exploration Commitment Completed New Commitment to drill 1 exploration well