conduct estimation via ownership · pdf fileconduct estimation via ownership change...

TRANSCRIPT

Conduct Estimation via Ownership ChangePreliminary Draft

Christian Michel∗

August 10, 2012

Abstract

This paper proposes a new form of estimating industry conduct in differentiated product in-

dustries. As an identification strategy, I use the structural ownership changes that occur due to

a merger. Given both pre-merger and post-merger industry data, I look for the form of conduct

that best predicts the market outcome before and after the merger. I provide identification results

for a new form of direct industry conduct estimation. Using both pre- and post-merger data also

enables me to provide a new evaluation criterion when selecting the form of competition among

a discrete “menu” of outcomes. I estimate industry conduct using data around a merger from

the Ready-to-Eat (RTE) cereal industry. Depending on the specification, I find that between

8.0% and 31.7% of industry markups can be attributed to cooperative industry behaviour, while

the rest of the markup is due to product differentiation of multi-product firms. My approach

also allows me to estimate the degree of profit internalization between merging firms post-merger

conditional on a specific form of competition. Furthermore, I provide ways to directly estimate

synergies resulting from a merger.

Keywords: Conduct Estimation, Identification of Market Structure, Ex-post Merger Evaluation,

Profit Internalization, Estimation of Synergies

JEL Classification: L11 (Production, Pricing, and Market Structure), L16 (Industrial Structure

and Structural Change), C52 (Model Evaluation, Validation, and Selection)

∗Graduate School of Economics and Social Sciences, University of Mannheim; Email: [email protected] am grateful to my advisors Volker Nocke and Philipp Schmidt-Dengler for their support throughout the project. I also wouldlike to thank Steve Berry, Pierre Dubois, David Genesove, Alex Shcherbakov, Andre Stenzel, Andrew Sweeting, Yuya Takahashi,Otto Toivanen, and seminar participants at Mannheim and Toulouse, as well as participants of the 2012 CEPR Applied IOSummer School for helpful comments. I am furthermore grateful to the Kilts Center of Marketing at the Graduate School ofBusiness, University of Chicago, for the Dominicks Finer Foods data.

1

1 Introduction

One of the key questions in industrial organization is which factors are the key determi-

nants for prices in specific industries. Such factors can be production costs, the degree of

product differentiation, and the form of market competition. Modern empirical research

in industrial organization often involves a detailed industry demand model, combined with

a game-theoretic formalization of supply side behavior. Very often, the form of supply side

competition is imposed by assumption rather than being tested for. This can be problematic:

If the imposed supply side specification turns out to be wrong, impacts of structural changes

in an industry, for example mergers or product entry, are likely to be mispredicted. The

main challenge is to jointly identify marginal costs and industry conduct in a differentiated

product model.

In this paper, I propose a new approach of estimating conduct in differentiated product

markets by using both pre-merger and post-merger industry data. My identification strategy

searches for the form of supply side competition that best predicts both pre-merger and post-

merger industry behavior. The intuition is the following. Given a well-specified demand-side

estimation and valid instruments, one can consistently estimate consumer price elasticities

irrespective of supply-side behavior. As is common in the literature, I assume that marginal

costs in the market are not observed by the researcher. Hence, different game-theoretic

assumptions about the competition in the market yield different estimates for marginal costs.

I make the common assumption that merging firms internalize the profits after the merger.

Given marginal cost estimates and the price-elasticities obtained from the demand side-

estimation, I can predict the effects of an ownership change on prices ex-post. By varying

the form of supply side competition (i.e. industry conduct), and accounting for input price

changes on the cost side, I look for the form of competition that most accurately predicts

the effects of the merger-induced ownership change on prices. I estimate the predicted post-

merger prices using only pre-merger data and compare them with the actual post-merger

prices. The differences of actual prices and predicted prices I then use to form moments in

order to obtain the model’s underlying conduct parameters using a Generalized Methods of

Moments estimation. I use data from the RTE cereal industry around a merger to test my

proposed method. In November 1992, Philip Morris with its Post cereal line purchased the

Nabisco ready to eat cereal branch. The antitrust court decision to clear the merger relied

heavily on empirical analysis, see for example Rubinfeld (2000) for a detailed analysis.

My approach has several advantages over the existing literature. I show that using proper

supply side variation, it is indeed possible to estimate industry conduct directly in differen-

tiated product models. This is something that is very unlikely to be achieved using demand

side variation, see for example Nevo (1998). I set up conduct moment conditions that rely

on orthogonality conditions between predicted price residuals and the true underlying form

of industry conduct. This helps me to overcome the problem of correctly estimating the un-

derlying level conduct parameters, instead of estimating only the responsiveness of industry

2

conduct with respect to cost variation. Moreover, my framework enables me to approach

various merger related supply-side issues. To my knowledge, this is the first paper to focus

on estimating post-merger intra-firm conduct of a merged entity, as well as to propose a

method to estimate merger related cost synergies directly in differentiated product models.

Advances in game theory, computational power, as well as econometric techniques have

lead to structural models that are able to recover the empirical counterparts to the theoretical

models. This has lead to a plethora of applications with respect to estimating demand or

production functions. While estimating industry conduct played a big role in the beginning

of the structural evolution, not much progress has been made over the past 15 years. Several

reasons contribute to this. Historically, conduct estimation has been closely related to the

concept of conjectural variations.1 Previous attempts to estimate both marginal costs and

industry conduct have mostly been made using demand side variation. In differentiated

product models these approaches usually face two kind of problems. The first problem is

the difficulty to find a sufficient number of demand rotators when estimating conduct in

differentiated product markets. Without such rotators, these approaches are not able to

identify industry conduct.2 The second problem relates to the estimation techniques, which

only estimate the economic parameters of interest accurately in special cases, see Corts

(1999). Corts critically discusses the identification of conjectural variation parameters.3 His

critique is twofold. Firstly, he argues that conjectural variation parameters usually differ from

the “as-if conduct parameters” one is interested in. A conjectural variation parameter only

estimates the marginal responsiveness of the marginal cost function with respect to changes

in a demand shifter. As a researcher, one is however interested in the average slope of the

marginal cost function instead of the marginal slope.

My approach differs significantly from the conjectural variations approach and is not sub-

ject to this critique. In my framework, each firm sets prices for its portfolio of brands instead

of quantities. Furthermore, instead of forming conjectures about other brands’ reactions,

each firm has an underlying objective function that takes into account preferences for profits

of other firms, thus allowing for cooperation among different firms. The preference parame-

ters with respect to other firms’ profits are essentially the conduct parameters I am interested

in. I assume that these conduct parameters, as well as the marginal costs of all brands, are

common knowledge in the industry, but not observed by the researcher. Using first order

conditions of all brands’ objective functions, my identification strategy then allows to esti-

mate both marginal cost parameters and the level conduct parameters, which amount to the

“as-if conduct parameters” in Corts (1999).

1Using a Cournot-style setting, one was able to derive equations from which conjectural variation parameters as a form ofresponsiveness towards industry competitors could be estimated, see for example Bresnahan (1989). In these models, a firmforms a “conjecture” about the responses of their competitors towards an increase in its own quantity. A conjecture can be seenas a reduced-form game theoretic best response function in symmetric quantity setting games. Conjectural variation modelsusually neglect any higher order effects of the best response functions. When accounting for higher-order rationality in the bestresponse correspondences, one can however show that only Cournot competition itself survives iterated deletion of dominatedstrategies.

2See for example Nevo (1998)3While his critique addresses homogeneous product models, his arguments are also valid for differentiated product models.

3

Corts second critique is related to the static game character of most conduct estimation

models. My approach is not fully exempt from this critique. I account for some industry

dynamics by modeling the merger-induced industry change. Nonetheless, it may be that my

static approach does not detect certain dynamic collusion patterns. One big advantage of

a static approach is a higher degree of tractability. Modeling repeated games makes identi-

fication of conduct even more difficult due to a multitude of potential dynamic equilibrium

strategies. With my approach, I am also able to identify patterns of full collusion as well as

patterns of collusion between only a subset of firms.

Related literature In this paper, I estimate conduct in differentiated product markets using

supply-side driven variation. Up until now the work in this area is relatively sparse, and

exclusively covers the airline industry. Oliveira (2011) uses marginal profit ratios in a dynamic

model to distinguish between market competition and efficient “stick-and-carrot” collusion

in the airline market. Orcholski (2010) sets up profit equations in a reduced form model and

backs out conjectural variation parameters that distinguish between Cournot-competition

and collusion. Ciliberto and Williams (2010), develop an approach that relies on multi-

market contact for estimating conduct in the the airline industry. Their model includes

conduct parameters that can have three different values, accounting for different degrees of

cooperation among profit-maximizing firms. In a differentiated demand model, Bresnahan

(1987) tests the hypothesis of a change in supply side competition in the US car market from

collusive to competitive against other options. Feenstra and Levinsohn (1995) formalize an

oligopoly setting which allows to estimate conduct in differentiated product industries for

different non-nested oligopoly models.

Bresnahan (1982) and Lau (1982) provide identification results for estimating conduct in

the homogeneous good case. Lau finds that if the inverse demand function is not separable

in the demand shifters, i.e. if it rotates rather than shifts due to demand shocks, then an

oligopoly solution is identified. Genesove and Mullin (1998) compare predictions from a

homogeneous good conduct estimation in the sugar industry with results from a direct cost

estimation. They find that a model with a freely estimated conduct parameter yields more

accurate cost estimates than estimates obtained from pre-specified models.

Nevo (2000) and Nevo (2001) use a random coefficient logit demand estimation to estimate

marginal costs and market power in the RTE cereal industry, and to predict effects of a merger

using only pre-merger data, respectively. Nevo (1998) theoretically discusses advantages and

disadvantages of a direct conduct estimation compared to a non-nested menu approach.

He argues that in practice estimating conduct directly will be impossible due to a lack of

sufficiently many distinct demand shifters. Hence, testing different non-nested models and

choosing the best fit for the data often seems to be the only viable alternative. For such non-

nested tests Vuong (1989) derives asymptotic results using a likelihood ratio test foundation.

Rivers and Vuong (2002) derive results on a more general basis. Gasmi, Laffont, and Vuong

(1992) further provide likelihood ratio tests for different oligopoly specifications in the soft

4

drink industry.

This paper is also related to other open questions in the field of industrial organization,

outlined in the following.

Ex-post evaluation of mergers One important question is how well different demand-side

models are capable of accurately predicting effects of mergers. Over the last decade, merger

simulations have become a regularly-used tool in antitrust cases. However, different demand

side models, such as logit, nested logit, or the Almost Ideal Demand Model will lead to

different estimates for price-elasticities, and therefore also different inferred marginal costs.

So far there is only a small number of papers exploring these issues, see for example Weinberg

and Hosken (2009) and Yoshimoto (2011). Not surprisingly, these models find that more

sophisticated estimation techniques, such as the Random-coefficient Logit model, yield more

accurate results than less sophisticated approaches such as the IV Logit model. Whereas

these papers test different demand side specifications, they ignore differences resulting from

supply side effects.

Estimating profit internalization of merging firms Different economic theories predict dif-

ferent degrees of post-merger profit internalization. From a neoclassical viewpoint, thus

neglecting agency problems within a firm, it makes sense to maximize joint profits of all

brands of the same firm. This is most important if a company has several brands that are

relatively close substitutes for consumers. However, there might be delays in post-merger

harmonization of firm strategies due to old contractual agreements and incentive structures.

Furthermore, from a theory of the firm point of view, it is possible that the different branches

remain different profit centers and thus compete within the firm. With my framework, I am

able to estimate intra-firm conduct conditional on a specific form of industry competition.

Direct estimation of synergies I use the availability of pre-and post-merger data to propose

a method to directly estimate synergies for merging firms resulting from a merger conditional

on a specific form of conduct. Examples for synergies are economies of scale or more efficient

production. Such synergies are often cited as a reason for allowing a merger that significantly

increases market power of merging firms. However, without having post-merger data it is

impossible to estimate synergies.

Selection methods – “menu approach” My baseline approach reflects the case in which I

estimate the conduct parameters and the marginal cost parameters directly using a moment

estimator. The advantage of this approach is that the possible values of the conduct parame-

ters are unconstrained, thus yielding a high degree of flexibility for the researcher. The menu

approach on the other hand selects the best fit among a discrete set (“menu”) of supply side

models, for example multi-brand Bertrand-Nash competition or a single profit-maximizing

5

monopolist. One advantage of this approach is that it does not include any conduct param-

eters directly, but rather pre-imposes them. Hence, there are less parameters to estimate

which often relaxes identification problems. There are two popular ways to select among

different non-nested models. However, both methods have significant weaknesses.

The first method relies on non-nested tests that only use pre-merger data, such as Vuong

(1989) or Rivers and Vuong (2002). These tests are based on a Kullbach-Leibler measure, and

test how far away a non-nested model is from the true data generating process pre-merger.

However, these tests tend to have relatively low predictive power. The second method relies

on recovering marginal cost estimates for different supply specifications, and comparing them

to accounting data. Such accounting data is problematic for various reasons. Firstly, the

data does not accurately reflect economic marginal costs. Secondly, these costs are usually

only available on an aggregate level. Therefore, it is very difficult to use these approaches

to test for some more advanced patterns of cooperative behavior, such as collusion among a

subset of firms.

My test is based on the fit of the data pre-merger and post-merger, and I exploit changes

in ownership as well as variation in the input cost data to select among different non-nested

models.

In the following, I will at first focus on the model setup and on identification issues regarding

the estimation of industry conduct. Section 2 introduces the baseline model and discusses

the conduct estimation strategy in detail. Section 3 will provide identification results to

estimate conduct and marginal costs jointly. Section 4 presents the data and estimation

results. Section 5 introduces several extensions to the baseline model as outlined above.

Section 6 concludes with a discussion of both the results and some open questions.

2 Empirical Model

My framework relies on two basic steps. In the first step, I estimate industry demand using a

discrete choice model to back out price elasticities. In a second step I then estimate industry

conduct either using a direct conduct estimation routine or using a menu approach. Both

approaches rely on forecasting post-merger prices giving pre-merger data and then to compare

them with the actual post-merger prices. In the second step I will also be able to compute

price-cost margins of the different products and to estimate the influences of different input

prices on marginal costs.

2.1 Demand side

My demand specification is closely related to Nevo (2001). There is a total number of J

brands in the market.

Denote the number of individual consumers in every market by I, and denote the number

of time periods by T . Using a Random Coefficient Logit model, individual i’s indirect utility

6

of consuming product j at time t can be written as

uijt = xjtβi + αipjt + ξjt + εijt; (1)

i = 1, .., I; j = 1, .., J ; t = 1, .., T .

xjt denotes firm j’s observable brand characteristics, pj denotes the price of product j, and

ξjt brand-specific mean valuation that is unobservable to the researcher but observable to the

firms. In some specifications I will decompose the brand-specific unobservable component

into several parts: ξjt = ξj + ξt + ∆ξjt. In this case, ξj denotes a mean unobservable brand-

valuation across all stores, ξt denotes a time-trend across all brands, while ∆ξjt is a store

and time specific component that is treated as an error term.4 Finally, εijt is an idiosyncratic

error term. The coefficients β and α are indiviual specific coefficients. These coefficients

depend on their mean valuations, on demographics in each region, Di and their associated

coefficients Π, as well as on an unobserved vector of shocks, vi that is interacted with a

scaling matrix Σ:(αi

βi

)=

(α

β

)+ ΠDi + Σvi, vi ∼ N(0, IK+1). (2)

Because not all of the potential consumers purchase a good in each period, I also require

an outside good. The indirect utility of the not purchasing any product and thus consuming

the outside good can be written as

ui0t = ξ0 + π0Di + σ0vi0 + εi0t.

As is common in the literature, I normalize ξ0 to zero.

Denote γD the vector of all demand side parameters. This vector can be decomposed

into a vector of linear parameters, γD1 = (α, β), and a vector of nonlinear parameters γD2 =

(vec(Π), vec(Σ)), respectively.

The indirect utility of consuming a product can be decomposed into a mean utility part

δjt and a mean-zero random component µijt+εijt that takes into account hetereogeneity from

demographics and captures other shocks. The decomposed indirect utility can be expressed

as

uijt = δjt(xj, pjt, ξjt, γD1 ) + µijt(xj, pjt, vi, Di; γ

D2 )

δjt = xjβ − αpjt + ξjt, µijt = [pjt, xj]′ ∗ (ΠDi + Σvi), (3)

where [pjt, xj] is a (K + 1)× 1 vector.

Consumers either buy one unit of a single product or take the outside good. They will

choose the option which yields the highest indirect utility. Using these assumptions, this

4The time trend ξt is not present in Nevo (2001). Since I use pre-and post-merger data for my demand-side estimation, usingsuch a time trend for post-merger data will increase my accuracy when relevant.

7

characterizes the set Ajt of unobservables that yield the highest utility for a specific choice j:

Ajt(x.t, p.t, ξ.t, γD2 ) = (Di, vi, εt)|uijt ≥ uilt∀l ∈ 0, .., J,

where dotted indices indicate vectors over all J brands. The market shares predicted by

the model can then be obtained via integrating over the different shocks, using population

moment functions P ∗():

sj(x.t, p.t, ξ.t, γD2 ) =

∫Ajt

dP ∗ε (ε)dP ∗v (v)dP ∗D(D). (4)

There are several possibilities to estimate the model that depend on different distribu-

tional assumptions. The most general case is a Random Coefficients Logit model. Its main

advantage is a very flexible form of substitution patterns. This is desirable because it enables

a detailed analysis of the substitution patterns between different brands that does not rely

on any model structure. To be able to integrate out the market shares, one needs to make

distributional assumptions with respect to the unobservable variables (Di, vi, εijt) and then

estimate the model using a GMM routine. Because of the non-linear aspect of the random

coefficients, such a model is relatively complicated and also computationally intense. As an

alternative, more rigid random utility models, such like Multinomial Logit model, can be

used. The main advantage is computational simplicity, for all heterogeneity is attributed to

an error term with known distribution. However, this also implies that substitution patterns

are proportional to market shares only, and not related to other factors like product charac-

teristics or brand proximity. As Nevo (2001) points out, this leads to a downward bias with

respect to the substitution to other inside goods.

When using a standard multinomial logit assumption, the error term follows an extreme

value distribution, i.e. the cumulative density function has the form F (ε) = exp(−exp(−ε)).

2.2 Industry technology

The J brands in the industry are produced by N ≤ J firms. Each brand can only be

produced by one firm. An important part of the model is the representation of marginal

cost. As is common in the literature, I assume that marginal costs can be decomposed

into cost factors that are observed to the researcher as well as factors unobserved to the

researcher. I allow for unobserved cost factors to be correlated with unobserved brand effects

and for observed cost factors to be correlated with observed brand characteristics x. I use

a linear relationship between marginal costs and the observable cost factors. This reflects a

relatively weak substitutability of input production factors over the medium- and short-run

in the RTE cereal industry. Denote the vector of brand j′s observed cost drivers by wj, and

j’s unobserved cost component by ωj. The marginal cost can be written as

mcj = wjγS + ωj (5)

8

where γS is a vector of marginal cost parameters. The estimated parameters will later be

used together with post-merger input cost data to predict post-merger marginal costs. The

baseline specification implies that marginal costs are constant for different output levels. This

is a relatively strict assumption, which can be relaxed by introducing scale effects. Denote

qi firm i′s total units sold in a period. If one assumes scale effects, i.e. decreasing marginal

costs in total production together with a Cobb-Douglas production function, then this can

be written as mcj = τ log(qj) + wjγS + ωj, where τ is the scale parameter.

2.3 Industry conduct

The key of this paper is to test for the form of competition in the market rather than to

pre-assume it. This is why I allow a firm’s objective function to potentially depend on other

firm’s profits. A firm can have a portfolio of different brands. Denote firm’s f portfolio by

Ff . Each brand maximizes its objective function with respect to its price. This can also

include profits of other firms’ brands. I make the assumption that all firms fully internalize

the profits of all the brands in their portfolio. Denote by θij the degree to which brand i takes

into account brand j’s profits when setting its optimal price, which reflects my interpretation

of a conduct parameter in my model. The conduct parameters are normalized to lie in

between 0 and 1. The assumption that each firm fully internalizes the profits of all of its

firms implies θii = 1∀i = 1, .., J , i.e. a brand fully cares about its own profits, and if i, j ∈ Ff ,θij = 1. Note that since only relative weights matter for the first order condition, this is a

normalization without loss of generality. Not allowing for negative conduct parameters also

implies that a firm does not derive a positive utility from “ruining” another firm.

The marginal costs of all brands in the industry are common knowledge as well as how each

brand takes into account all other brands. Both marginal costs and the conduct parameters

are however not observed by the econometrician. Brand j′s objective function can be written

as

Πj = (pj −mcj)sj +∑r 6=j

θjr(pr −mcr)sr, (6)

where sr denotes the market share of brand r.

Furthermore, the profit of all other brands enters the objective function additively. One

feature of such a framework is a linear structure that is easy to estimate. In any case, the

first order condition for brand j with respect to its own price can be written as

sj(p) +J∑r=1

θjr(pr −mcr)∂sr∂pj

= 0. (7)

Denote by Θ the pre-merger ownership matrix which can be defined as the matrix that

9

consists of entries

Θjr = θjr.

This leads to leads to

Θ =

1 θ12 .. θ1J

θ21 1 .. θ2J

.. .. .. ..

θJ1 θJ2 .. 1

The key of my estimation technique is to find the form of conduct and marginal costs

that best rationalizes pre-merger and post-merger prices. Since marginal costs conditional

on a specific form of conduct can be inferred using pre-merger data, I am interested in

recovering the matrix of conduct parameters Θ that best predicts these price changes with

respect to observed post-merger data. Because I assume that the merger-induced change in

conduct is known, the overall objective is to recover the pre-merger ownership conduct. As

a convention, the pre-merger ownership matrix does not contain a subscript “pre”. Define

Ωjr ≡ −θjr ∗ ∂sr∂pj

. When estimating the demand side using the pre merger data only and

being given proper demand side instruments, one can already infer the marginal costs of

production mc(γD,Θ,Ωpre(γD,Θ)) conditional on the form of conduct Θ.

mc(γD,Θ,Ωpre(γD,Θ)) = ppre − (Ωpre(γD,Θ))−1spre. (8)

Combining this equation with equation (5), one obtains the following expression for the

unobserved cost component ω given only pre-merger data:

ω = p− Ωpre(Θ, γD)−1spre − w′γS (9)

I treat product characteristics with respect to demand, x, and cost characteristics, w, as

exogenous with respect to industry prices. This is arguably a simplification in the long run,

but will facilitate the computation of the model.5

Objective Function Taken a specific conduct matrix Θ as given, in combination with the

parameters γD from the demand side estimation, all parameters necessary to recover pre-

merger marginal costs and to estimate equation (5) are given. The change in ownership due to

the merger also has an effect on pricing. A key identifying assumption is that even though the

researcher does not know the underlying form of conduct, Θ, he knows exactly how the merger

will affect industry conduct. There are two channels for this, namely post-merger profit

internalization of merging firms, and how competitors consider the merged entity post-merger.

5One short run effect that might be overlooked is how add-on toys in kids cereal boxes is affected by competitors’ prices. There is however anecdotal evidence with respect to collusive agreements regarding limits for kids toys in the RTE cerealindustry, see Corts (1995).

10

I will elaborate on the second channel in detail in section 3.1. Given the underlying form

of pre-merger conduct, Θ, the post-merger conduct can then be expressed as via a function

b : Θ→ Θ which maps the pre-merger conduct matrix Θ into the post-merger conduct matrix

Θpost = b(Θ). This is because all merger-induced ownership transformations are known by

assumption. This then allows to compute the post-merger markup Ωpost((γD, b(Θ)))−1s,

where Ωpost is the markup matrix which depends on the demand elasticities and the form or

post-merger conduct b(Θ). The predicted post-merger prices given γD for a specific Θ can

be written as

ppost(γD, γS,Ωpre(γD,Θ),Ωpost(γD, b(Θ))) = mc(Ωpre(γD,Θ), γS)−(Ωpost(γD, b(Θ)))−1s. (10)

mc(Ωpre(γD,Θ), γS) reflects the predicted marginal costs using the observed pre-merger

cost parameters γS together with the post-merger input prices. I use the predicted prices

conditional on industry conduct to form moment conditions that enable the identification of

the conduct parameters. Overall, I am interested in the matrix Θ among all potential supply

sides that minimizes a weighted moment criterion explained in the next two sections.The

next section discusses the differences of these options in more detail, and presents some

identification results.

3 Identification

The key identification question is: Under what circumstances are firms’ marginal costs and

industry conduct jointly identified? One important point with respect to marginal costs is

whether a merger will lead to synergies for the merging firms. In the baseline case I implicitly

assume that a merger will either not lead to synergies or involve a known synergy level in

form of a certain percentage decrease in marginal costs. The latter case enables, for example,

to account for synergies that are claimed by merging parties prior to a merger. This is also a

standard convention in merger simulation models. In this section, I will present identification

results for the direct approach. Section 3.1 introduces further assumptions to decrease the

parameters space to meet necessary rank conditions. Section 3.2 discusses the identification

assumptions for estimating both the demand and supply side parameters of the model.

3.1 Rank Conditions

3.1.1 Direct approach

This section provides identification results for different specifications when estimating con-

tinuous conduct parameters “directly”. This is opposed to the menu approach, which selects

among different non-nested models without estimating conduct parameters. Recall the as-

sumptions made on firms’ own-profit maximization. As in standard unilateral merger models,

I also assume that a merger does not change the behavior between non-merging firms. There

11

are furthermore some global assumptions that further reduce the parameter space which I

will discuss in detail.

I only consider cases in which a firm treats all brands of a specific competitor’s firm in

the same way. This excludes the possibility that single brands of different firms collude

while others play against each other competitively. There are two reasons for this. Firstly,

from a pure rank condition perspective the number of parameters I would have to estimate

would easily exceed the number brands in the market. This makes it impossible to identify

the parameters. Secondly, my demand estimation uses the brand space J as the limiting

distribution.

Conduct between merging and non-merging firms My identification strategy also requires to

specify how conduct will change between merging and non-merging firms after the merger

has taken place. Assume for example that there are 3 firms, 1, 2, and 3. Firm 1 and 2 will

merge. Before the merger, firm 3 could potentially have had a different relationship towards

firm 1 than towards firm 2. Thus, in order to identify the conduct parameters, I have to make

an additional assumption concerning how the two parts of the merged entity are considered

by their competitors after the merger. Any assumption that fulfills the property of a known

change in post-merger conduct is theoretically feasible. Analytically, this means that the

mapping b from pre-merger to post-merger conduct is known. I allow for three specific cases.

In the first case, the merger does not change how competitors consider the two merging firms

in the short run. In this case, while the merging firms will fully internalize the profits after

the merger, the rest of the conduct parameters will remain constant. A second possibility is

that the fully merged entity is considered and behaves as the acquirer did pre-merger. The

third option I allow is the reverse, meaning that the merged entity behaves as the target.

This is summed up in the following assumption.

Assumption 1 (Conduct between merging and non-merging firms). Let f, g be two distinct

merging firms, and h a non-merging firm. Let θpreik and θpostik denote the pre- and post-merger

conduct parameters between firms i and k, respectively. Then, ∀i ∈ Ff , ∀j ∈ Fg, ∀k ∈ Fh, one

of the following three cases holds regarding the conduct between a merging and a non-merging

firm:

a. θpostik = θpreik ; θpostjk = θprejk (no change in conduct);

b. Go to “acquiring firm” values: θpostik = θpreik ; θpostjk = θpreik (acquiring firm standard).

c. θpostik = θprejk ; θpostjk = θprejk (target firm standard);

It is worthwhile discussing the implications of this assumption. I do not have to pre-

specify the values of the conduct parameters, but just the way in which the parameters

change. As long as the change in conduct between merging and non-merging firms is known

post-merger, other change patterns are possible that still allow identification of the system.

An even stronger possibility is to assume specific values of the conduct parameters. In this

12

case, identification of industry conduct is also possible. This will be discussed in more detail

in section 5.

Bilateral symmetry between firms One way to reduce the number of parameters to be esti-

mated is to restrict the model to cases in which all brands of two firms play against each other

in the same way. As a consequence, all brands have the same cross-conduct parameters for

all of their brand pairs. This still allows for partial collusion between two firms, but does not

allow for more elaborate strategies, such as for example collusion only between some brands

of two firms. In terms of the parameter space, this reduces the number of cross-conduct

parameters to N(N−1)2

.

Proposition 1 (Necessary conditions for bilateral symmetry between firms). Suppose As-

sumption 1 holds, and that for distinct firms f, g , θij = θik = θji = θki ∀i ∈ Ff ,∀ j, k ∈ Fg.Then industry conduct is identified only if N(N−1)

2≤ J .

Proof. The demand parameters γD can be estimated from equations 10 and 13, respectively.

Regarding the supply side, there are J estimable equations, one equation per brand post-

merger. Because each firm has one conduct parameter for each competitor, this leads to an

overall number of N(N − 1) parameters. The bilateral symmetry assumption reduces this

number to N(N−1)2

. This leads to J equations with N(N−1)2

parameters. The model is only

identified if there are at least as many equations as parameters, i.e. if N(N−1)2

≤ J . This

completes the proof.

Same responsiveness to all cross-firm brands Another possibility is a case in which each firm

behaves in the same way to all of its competitors.

The advantage of this specification is that it reduces the number of parameters to only N

different cross-conduct parameters. However, there are also several problems associated with

the assumption. Firstly, it is again no longer possible to detect partial collusion between

a subset of firms in the industry. Secondly, there is a consistency problem with respect to

a mutual responsiveness: Under this assumption, it can be possible that firm 1 is acting

collusively with firm 2, and firm 2 on the other hand acts competitively towards firm 1,

something which is hard to justify from an economic perspective.

Proposition 2 (Necessary conditions for same responsiveness to all cross-firm brands). Sup-

pose Assumption 1 holds, and that for distinct firms f, g, h , θij = θik ∀i ∈ Ff ,∀ j ∈ Fg,∀ k ∈Fh. Then rank conditions are met only if N ≤ J .

Proof. The demand parameters γD can be estimated from equations 10 and 13, respectively.

Regarding the supply side, there are J estimable equations, one equation per brand pre-

merger, and one equation per brand post-merger.Because each firm has one conduct param-

eter for all firms, this leads to an overall number of N conduct parameters. This leads to

13

Conduct specification No or known synergies

Bilateral symm btw. firms N(N−1)2 ≤ J

Same resp. to cross-firm br. N ≤ JSame resp. btw. all firms J ≥ 1 (always met)Menu approach J ≥ 0 (always met)

Table 1: Identification conditions for different specifications

J equations with N parameters. The model is only identified if there are at least as many

equations as parameters, i.e. if N ≤ J . This completes the proof.

It is easy to see that the necessary rank conditions hold trivially. It can still be the

case however that there are two or more identical conduct equations, which would violate

identification.

Same responsiveness between all firms The most restrictive specification assumes that the

cross-conduct parameters are identical for all brands in the market. The biggest advantage is

that this returns a single cross-conduct parameter instead of a complicated matrix, and thus

always meets the rank conditions. The big disadvantages are that very often this parameter

will severely restricts the set estimable of economic models. For example, one will not be able

to test for partial collusion in the market, or for differences in competitive behavior between

different firms.

Proposition 3 (Necessary conditions for same responsiveness between all firms). Suppose

for distinct firms f, g, h , θij = θji = θik = θjk = θkj ∀i ∈ Ff ,∀ j ∈ Fg,∀ k ∈ Fh. Then the

rank condition for industry conduct is always met.

Proof. Using the same reasoning as in the proof for Proposition 2, there are J equations and

one parameter to estimate, so that the result trivially holds.

Overall, the direct approach requires more structure and a larger parameter space. This

is because the free-floating conduct parameters require more degrees of freedom. Therefore, I

will provide results specifically tailored for the different assumptions provided in the beginning

of this section. Clearly, the most important trade-off is the one between the allowed flexibility

of industry conduct and the number of parameters that have to be estimated.

3.1.2 Other forms of identification

Identifying conduct via product entry or exit Besides using a merger as an identification

strategy for estimating industry conduct, one can also think about using other structural

changes. Concerning product entry, there is the problem of comparing competition with and

without the entrant. While one can still make the assumption that entry does not change

how existing brands compete with each other, one has to define how a new product will

interact with the existing products. The menu approach is theoretically feasible under entry.

14

Unlike product entry, using product exit as an identification strategy is still feasible.

However, one has to ask why a product will exit. One reason can be that it is just not

profitable, which will then probably imply that its impact on the market is relatively low.

Therefore, a reduction of the brand space would not result in a big shift for firms strategies.

Another possibility would be that a brand is profitable on its own, but it would be more

profitable for a multi-brand firm to exit the product out of the market. This would result in

an endogeneity problem when estimating conduct using product exit.

3.2 Model identification

My estimation method requires identification of three sets of parameters: demand-side pa-

rameters, γD, cost parameters γS, and the conduct parameters Θ. The correlation between

price and both unobserved brand and cost characteristics requires instrumentation for each

brand in the demand and pricing equations, respectively.

3.2.1 Identification of demand parameters

Concerning the demand side, I assume that when being assessed at the true parameter values

γD0 , the unobservable demand components ξj for each brand are uncorrelated with respect to

a set of exogenous instruments, Zξ:

E[ξj(γD0 )|Zξ] = 0 (11)

Note that I implicitly assume that the demand estimation can be done independently of

the conduct and marginal cost estimation, respectively. The mean independence assumption

would be violated if industry conduct or a change in production costs, not prices, would

influence consumer choice through the unobserved brand-specific component.6 As common

in the literature, I assume that the product locations of the different goods is exogenous, and

therefore are does not respond changes in industry pricing or demand. Also accounting for

potential brand replacement or additional brand introductions would make traction of the full

model nearly impossible. Because of the inherent endogeneity between price and unobserved

brand characteristics, I need to find adequate instruments for the demand estimation. I use

four different sets of instruments to do so.

First-order basis functions of product characteristics The first set of instruments results from

setting up optimal instrument functions that result from the different product characteristics.

The economic intuition of these instruments is that product characteristics can influence

markups of the different products. A good with closer substitutes will have lower markups

than a less substitutable good. Furthermore, in a competitive oligopoly model, these markup

6This assumption would be violated if the merger caused a change in the perceived “brand values” of the merged entities,which would affect the ξ components in the demand equation.

15

effects will be even stronger for goods that have substitutes from other firms than from the

same firm. BLP (1995) argue that the computation of the optimal set of instruments when

only conditional moment conditions are available is very difficult and numerically complex.

As a less computationally demanding approximation, they use polynomials resulting from

first order basis functions of the product characteristics. The validity of these basis functions

as instruments relies on exchangeability assumptions of firms’ own characteristics with respect

to permutations in the order of competitors’ product characteristics. Because I allow for the

possibilty of collusion among firms, this changes the structure of potential Nash equilibria.

Cost shifters My second set of instruments relies on production cost shifters. The economic

assumption is that input cost variation should be correlated with variation in prices, but not

with consumers’ preferences for unobservable product characteristics. I use both cost factors

that affect all products in similar fashion, such as labor costs, packaging, and transporta-

tion, as well as factors that differ among products, such as interactions between product

characteristics and input prices for wheat, sugar, and corn.

Ownership change My third set of instruments is the ownership change itself. As argued

above, a merger should cause a change in industry prices. Similar to a cost shift, one can

assume that the merger affects prices, but not the demand characteristics. This assumption

would be violated if the merger caused a change in brand value which would affect the ξ’s of

the merging firms. Because the actual brand names of the cereals involved did not change

after the merger, such a brand effect seems unlikely.

Average prices in other zones A prominent set of instruments are prices from other pricing

zones, see for example Hausman (1996) and Nevo (2001). In my dataset, stores are located

in thirteen different zones within the same metropolitan area, and different zones are priced

differently. For validity of the instruments, the pricing decisions have to be uncorrelated

among different zones. Furthermore, demand shocks should not spill over across zones. Thus,

under the assumption that unobserved demand shocks are independent across clusters, prices

of other zones are valid instruments. This seems to be a very strong assumption in my dataset,

due to common advertising campaigns within the same metropolitan area and retailer. Still,

in non-sale periods, there are up to 20% price differences for the same product over different

stores.

3.2.2 Identification of cost parameters

Unlike the estimation of demand parameters, the estimation of both industry conduct and

cost estimates is unavoidably interlinked. In my approach, conditional on a specific form of

conduct, I can back out the marginal cost via a first order condition and then regress them

on observable product characteristics combined with input prices. This will then allow me

to predict the post merger marginal costs using post-merger input data and the estimated

16

parameters. My identifying assumption concerning marginal cost is that the unobserved cost

characteristics ω are mean independent to a set of exogenous cost instruments:

E[ωj(γS0 ,Θ, γ

D)|Zω] = 0 (12)

Note that in this stage, I do not use any information on conduct. This is because I use the

obtained cost parameters in order to forecast the marginal cost in the second stage. Together

with the change in ownership, this will influence the post-merger prices in the market. I will

then use both marginal cost and conduct effects in order to estimate industry conduct. I use

three different sets of instruments to identify the unobservable brand component.

First-order basis functions of cost characteristics Similar to the demand side estimation, I use

first-order basis function of the cost characteristics to instrument for the unobservable cost

component. The brand specific unobservable marginal cost component ω may be correlated

with unobservable product characteristics. Therefore it is essential to look for instruments

that are correlated with marginal costs, but not with the error term. To account for the

effects of unobserved cost drivers on prices, I use first order basis functions of the own

brand characteristics, own firm characteristics, and competitors’ characteristics. This again

relies on an exchangeability argument of product characteristics when facing a unique Nash

equilibrium, see for example Berry et al. (1995).

Retail margin In my data, I also observe a proxy for the retail margin, namely average

acquisition costs. This component is highly volatile over time. When not distinguishing

between the retail margin and the marginal cost of production in the estimation, but rather

treating both together as overall marginal cost, the data on the change in retail margin can

thus help me to identify the constant product-specific unobservable component ωj.

3.2.3 Identification of conduct parameters

To identify the conduct parameters, I use further orthogonality assumptions. Because I

assume that firms act according to my model and given a specific underlying form of conduct,

I can use the obtained predicted post-merger prices to generate two more sets of moments.

The first moment uses economic assumptions on the price effects within a single firm, whereas

the second one uses assumptions on prices between two different firms. As section 3.1 has

shown, the number of parameters varies with the conduct specification, between 1 and N(N−1)2

parameters.

Own firm conditions Denote df a dummy variable that equals one whenever a product

belongs to firm f and zero otherwise. The sum of the difference between predicted and

actual post-merger prices of a firms’ products should on average be uncorrelated to its own

dummy-variable df . This identification condition relies on the oligopoly structure of the

17

game. If the sum of the firm’s price residuals is on average correlated to this dummy, this

would imply that a firm is not pricing optimally given its preference structure, which is ruled

out by assumption. Therefore, a correlation between the firm’s dummy and the sum of its

own-residuals indicates a supply side misspecification to the researcher. Formally, define the

average squared price residual of firm f as

ϕownf (Θ, γS, γD) ≡ 1

TN

ST∑t=1

1

Jf

∑i∈Ff

(pposti,t (γD, γS,Ωpre(γD,Θ),Ωpost(γD, b(Θ)))−pposti,t )2. (13)

Here, Jf denotes the number of brands of firm f. Following the argument above, this leads

to the identification condition

E[ϕownf (Θ0, γS, γD)|df ] = 0 ∀i ∈ Ff∀j /∈ Ff , (14)

where Θ0 denotes the true vector of all conduct parameters. Overall, this will yield at

least N − 1 different moment conditions under Assumptions 1b and 1c. Under these two

assumptions, one conduct parameter will disappear post-merger. This will not be the case

under Assumption 1a. If one assumes the same behavior to all firms, then the involved

cross-conduct parameters θij turn to the single parameter θi. One can also use higher order

moments of the own-firm residuals to form even more moment conditions. As an alternative,

one can use assumption on the cross-conduct between two firms.

Cross-firm conditions Denote dfg a dummy variable that equals one whenever firms’ f and

g are interacting with respect to price setting, i.e. whenever firm f sets a price and takes

into the account the effects on firm g or vice versa. Given the true underlying supply side

model, the product of the average residuals between the predicted and actual post-merger

prices of two different firms should be mean independent of the underlying cross-conduct

parameter. The reasoning is similar to the one in case of own firm conditions: On average,

the price-residuals between two firms should not be correlated with the conduct parameters.

For notational simplicity, I now drop the expressions for pre- and post-merger markup,

Ωpre(γD,Θ), and Ωpost(γD, b(Θ)), respectively, from the equation for the predicted post-

merger prices. The average product of the squared price residuals between two firms f

and g can then be defined as

ϕcrossf,g (Θ, γS, γD) ≡ 1

TN

ST∑t=1

(1

Jf

∑i∈Ff

(pposti,t (γD, γS,Θ)−pposti,t )2)(1

Jg

∑j∈Fg

(ppostj,t (γD, γS,Θ)−ppostj,t )2).

(15)

From the above reasoning, one can now set up the following identification condition:

E[ϕcrossf,g (Θ0, γS, γD)|dfg] = 0 ∀i ∈ Ff , ∀j ∈ Fg. (16)

18

This yields at least (N−1)2

2and a maximum of N(N−1)

2different cross-firm moment con-

ditions. The number of cross-firm moment conditions depends on the selected assumption

regarding conduct between merged and non-merged firms. When adding up both cross-firm

and own-firm moment conditions, one obtains at least (N−1)(N+1)2

moments, which is sufficient

for estimating the N(N−1)2

parameters under bilateral firm symmetry.

Why has conduct to be known among firms? Suppose conduct where not known among

different firms. This would cause several problems. Firstly, this would make the assumption

on symmetry between two different firms harder to sustain. Secondly, I would have to specify

beliefs of the different firms regarding other firms’ behavior, which would further complicate

the model.

4 Data and Estimation

4.1 Industry Overview and Data

Industry description There are several factors that make the RTE cereal industry an ideal

starting point for oligopoly analysis.7 Economies of scale in packaging different cereals, as

well as in the distribution of products, cause barriers to entry for new firms. R&D expendi-

tures are relatively low, and only amount to 1% of gross sales per year. Still, there is a quite

frequent introduction of new products, which goes in line with large advertising campaigns in

the beginning of a product’s life.8 Market shares of successful brands over time are relatively

steady, which can easily be attributed to habit formation by consumers. The cereals differ

with respect to their product characteristics, such as sugar content or package design, and

target different audiences. It is common to classify these cereals into different groups, such as

adult, family, and kids cereals, see also Nevo (2001). Table 11 shows the classification of the

different cereal brands into different segments. At the start of the period I analyze , the in-

dustry consists of 6 main nationwide manufacturers: Kelloggs, General Mills, Post, Nabisco,

Quaker Oats, and Ralston Purina. See table 4 for the market shares of the different products.

Kelloggs as the firm with the biggest market share has a big presence in all segment. General

Mills is mainly present in the family and kids segments, whereas Post and Nabisco have their

main strengths in the adult segments. On a retail level, cereals are mostly distributed via su-

permarkets. Supermarket promotions via price reductions or quantity discounts are a further

tool used to increase quantities sold for a period of time. Furthermore, many retailers also

own private labels that compete locally with the nationwide manufacturers. I use scanner

data from January 1991 until May 1997 from the Dominick’s Finer Food database. Further-

more, I use input price data from the Thomson Reuters Datastream database over the same

7This industry has already been studied extensively, see for example Schmalensee (1978), Nevo (2000), and Corts (1995).Although Corts presents a detailed industry description, to my knowledge the dynamic aspects on the supply side have not beeninvestigated in detail.

8Hitsch (2006) studies the determinants of successful brand introductions. While I observe some product entry in the dataset,these products do not have a large share market share, such that I will leave them out in my main estimation.

19

time. My main dataset for the conduct estimation includes 28 brands from the 6 different

nationwide firms. The scanner data involves 68 stores from the Chicago Metropolitan area,

see Fig. 1 for a geographic map of the stores. In particular, the dataset includes data with

respect to product prices, quantities sold, data on promotions, as well as 1990 census data

yielding demographic variables for the different store locations. Even though I also observe

data on Dominick’s private label cereal, I do not include it in my conduct estimation. There

are two reasons for this. Firstly, I want to focus on the degree of competition between firms

that are operating nationwide. Because a private label is only present for one retailer, and

in my case a locally operating retailer, it will have different underlying objectives than the

nationwide operating manufacturers. Secondly, a private label firm belongs to its retailer,

thus leading to a joint maximization of profits upstream and downstream. This would need

more assumptions to be compatible with estimating “upstream ” industry conduct. I also

abstract from dynamic storage behavior, as well as couponing and shelf-space competition.

While these factors may influence competition, they would render the model intractable.

Industry development over time and the 1992-1993 Post-Nabisco merger Between 1990 and

1993, industry prices steadily increased in the industry, see Fig. 2 and Fig. 3 for the price

development including and excluding sale periods for products, respectively. On November

12, 1992, Kraft Foods purchased RJR Nabisco’s Ready-To-Eat cereal line. The acquisition

was cleared by the FTC on January 4, 1993. On February 10th, 1993, the New York State

attorney however sued for a divestiture of the Nabisco assets, which was finally turned down

3 weeks later.9 Table 8 shows the price development for several quarters after the merger.

Average prices for the merging firms increase over time. The same holds for other firms’

products in the adult segment, which is the segment in which Post and Nabisco have a large

presence. Only the prices for General Mills products slightly decrease in this period. This

can be attributed to both a change in General Mills high management in 1993, in which the

company responded to soaring market shares, and to the fact that General Mills was mostly

present in the kids and family segment that was not affected as much by the merger. Overall

industry behavior however remained stable. Between 1993 and March 1996, industry-wide

prices for branded RTE cereal increased very moderately. In April 1996, Post-Nabisco started

a price war and decreased the prices for all of its products by 20%, thereby permanently

increasing its markets share. This was followed by significant price cuts two months later by

General Mills and Kelloggs. Overall, margin over production cost fell by 12% in 1996 due to

these actions.10 Finally, in December 1996, the Ralston Purina cereal line was acquired by

General Mills, effectively resulting in a nationwide 4 firm oligopoly at the end of my merger.

As this merger fell into a period of significant industry-wide price cuts, there were no obvious

upward price effects on the industry. Furthermore, the change in pricing behavior make my

identification assumption not suitable for this merger.

9See Rubinfeld (2000) for a detailed description.10See for example Food Review (2000), Volume 23, Issue 2, pages 21-28.

20

Retail margin In the data, I also observe a proxy for the gross retail margin. From an

economic perspective, the variable’s economic interpretation reflects the weighted profit share

sold for each product in a period. Thus, it is a weighted average in terms of the time of

purchase of the products in inventory, and does not reflect a product’s current replacement

value.11 As a consequence, this proxy averages the retail margins over time for a given

period. Table C shows the development of the retail margin over time for the different firms

in the dataset. There are several interesting features. The retail margin varies significantly

across the different firms. Fig. 9 shows the mean brand specific retail margins. On average

retail margins are highest for Ralston, the firm with the smallest market share, followed

by Kelloggs, the firm with the highest market share. Thus, there is no clear relationship

between retail margin and firm size, suggesting that there is no higher bargaining power

for Kelloggs.12 Another interesting fact is that the retail margin drops significantly around

the time of the merger, from over 15% to single digit figures for several firms, including the

merging firms. It is not clear whether this drop is due to the merger, which would imply

some form of renegotiation between manufacturers and retailer in the period, or whether it

is rather a pure coincidence. Lastly, one year after merger the retail margin increases and

becomes higher than in the pre-merger period. One reason for this may be the price cut

induced by Post-Nabisco in 1996. If the retail margin is not solely negotiated on percentage

terms, but rather gives a retailer a relatively constant markup per package sold, then a lower

retail price due to the wholesale price cut will yield a higher retail margin.

Exogeneity of merger From an estimation standpoint, it is important to discuss concerns

and potential effects of merger endogeneity. After the 1988 leveraged buyout of RJR Nabisco,

the ownership group accumulated a relatively high pile of debt. There is a popular claim that

company divestitures were used to reduce the overall debt level, and not to increase industry

profits. Even if this claim was not true, this would only bias the results if the merger had lead

to unknown synergies, or if an anticipation of the merger by firms in the industry had lead to

a change in behavior. Using my data, I can test for the former case. As discussed before, the

temporary decline in retail margin might be such a source for synergies if the merger caused

a period of renegotiation with low retail margins. Because this low retail margin period lasts

only for about 4 months, it does not seem likely that these temporary savings will offset

transaction costs from merging. Concerning the case of merger anticipation, such change in

behavior pre-merger seems unlikely due to the relative steadiness in pricing strategies over

time prior to the merger.

11Dominick’s uses the following formula for the average acquisition costs (AAC): AAC(t+1) = (Inventory bought in t) Pricepaid(t) + (Inventory, end of t-l-sales(t)) AAC(t).

12Another potential source for bargaining power not modeled her is bargaining power in form of more premium shelf spaces.

21

Figure 1: Geographical location of stores in dataset

4.2 Estimation technique

Estimation algorithm In the following I will outline each step of the estimation algorithm

in some detail.

1. Estimate demand parameters consistently Using the instruments discussed above,

I estimate the demand parameters, without already having to specify supply-side com-

petition.

2. Choose set of supply-side specifications When using a direct estimation, I have

to specify the appropriate assumptions to reduce the parameter space. When using a

selection method, I have to predetermine the set of supply side models to choose from.

3. Infer marginal costs and predict post-merger prices for the different speci-

fications, and compute appropriate moments Having estimated the demand side

parameters, I can infer the marginal costs of production conditional on the form of

conduct Θ using proper instruments. Using post-merger cost input cost data and the

estimated cost-parameters, I can predict post-merger marginal costs. Given the conduct

matrix Θ and the estimated demand parameters γD from the demand side estimation

in step 1, I can then predict post-merger prices for a specific conduct Θ.

For each specification, I can then compute the moments ϕ that depend on the difference

between predicted and actual post-merger prices conditional on the form of conduct Θ.

4. Evaluate the different models using GMM I estimate the model using a General-

ized Method of Moments (GMM) routine to find the model’s conduct parameters that

minimize the weighted moment criterion using the moments generated in step 4 for each

form of conduct.

22

Overall, the above steps can be decomposed into two parts. In the first part, I estimate

the demand elasticities using a discrete choice model. Using these elasticities, I then estimate

marginal costs and industry conduct using a second GMM estimation routine in the second

part.

4.3 Demand estimation

I use the technique of Nevo (2001) to recover the structural demand side parameters and

unobservable error term ξ. Using Nevo’s estimation strategy on the demand side allows

me to estimate all the structural demand side parameters independently of the supply side.

This has major advantages when it comes to estimating industry conduct with respect to

computational complexity. For the most flexible specification, I use a random coefficient

Logit model estimated via a GMM routine.

Denote the vector of the mean utility level across all brands at time t by δ.t. I solve for δ.t

as to match the empirical market shares sjt(x.t, p.t, ξ.t, γD) from equation (4) with the actual

market shares sjt observed in the data. Denote by $(γD) an error term depending on the

demand side parameters, and denote by Zξ a matrix of demand side instruments. Then,

using a GMM estimator, the objective is to find

γD = arg minγD

$(γD)′ZξA−1ξ Z ′ξ$(γD); (17)

where A−1ξ is an estimate of the asymptotically efficient covariance function E[Z ′ξ$$

′Zξ].

Market size Defining the market size is an important assumption, for it has implications

on the different market shares and also on the differences between markets. I assume that

the market size is correlated with store specific characteristics. In fact, I observe a proxy for

weekly volume in the data, which I use to compute one variant of market size. A second

variant uses average output in foods as a proxy for the overall market size. Figure 8 shows

the variation in market size across stores for the different size measures.

There are several potential sources of endogeneity in the model. Firstly, from the demand

side, prices may be correlated with unobserved product characteristics. Secondly, unobserved

cost components may also be correlated with price. I will explain the use of my instruments.

Input prices Table 10 shows data on some of the cost-side variables. There is variation both

over time and also across different input cost factors, even if many of them are positively

correlated. I also interact some of the input cost data with observable brand characteristics,

which will further lead to more variation on the cost side.

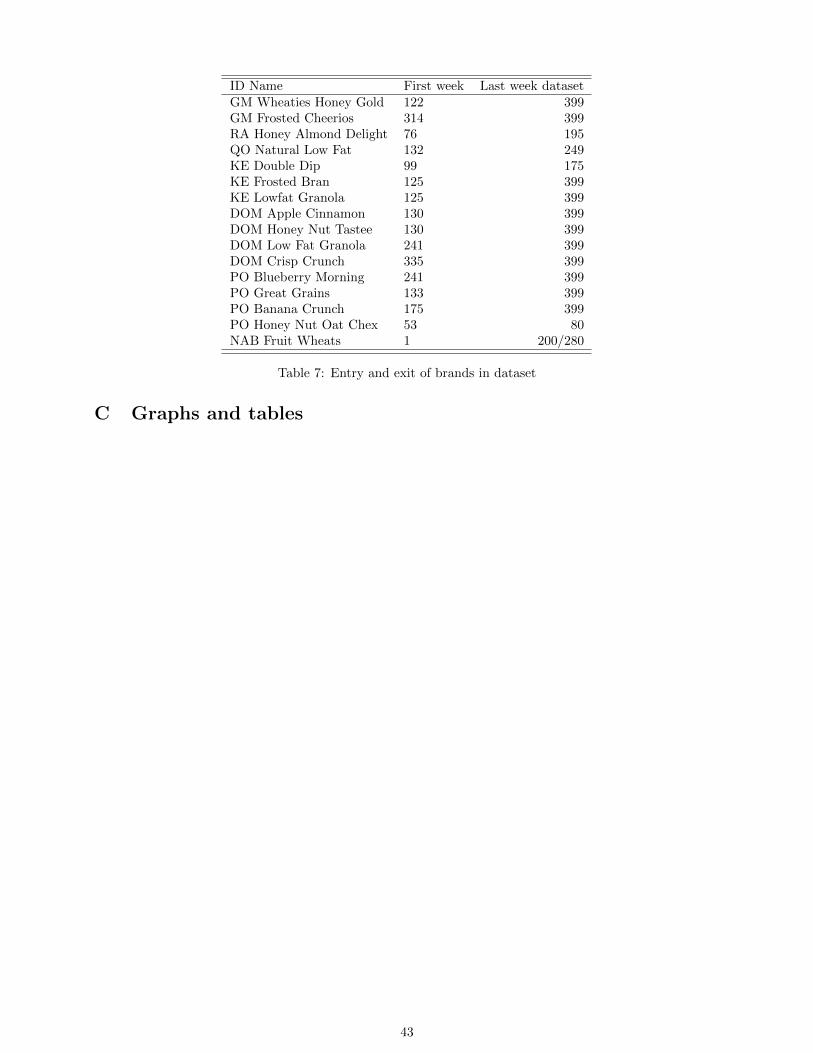

Implication of choice set In my dataset, I observe exit and entry of some brands. Table 7

shows the brand names as well as time of entry and exit. There are 11 entries and 5 exits

23

overall. Around week 130, which is about 10 months prior to the merger, 3 new private

label products and two national brands also become available in the Dominick’s stores. This

causes variation in the consumers’ choice spaces. Since I do not include these products in

my estimation, these entries should have effects on the substitutability from inside products

to the outside good. Furthermore, brands with a similar product characteristics should face

higher competition, which might cause a change in these prices.

Demand Elasticities Individual market shares depend on the mean utility as well as on the

random and demographic components.

sijt =exp(δjt + µijt)

1 +∑J

k=1 exp(δkt + µikt)(18)

Integrating over the whole distribution of individuals yields the aggregated market shares

from the model. The cross-price elasticity between goods j and k at time t, ηjkt, can be

written as

ηjkt =

−pjtsjt

∫αisijt(1− sijt)dPD(D)dPv(v) j = k

pktsjt

∫αisijtsiktdPD(D)dPv(v) j 6= k

(19)

There are several options to compute these elasticities depending on how much model

structure one wants to use. When using the random coefficients model, one needs to compute

the individual market shares using the model structure and equation (18). However, there

are two different options how to account for the aggregated market share sjt. Either one

integrates the individual market shares over all individuals, or uses the post merger market

share at time t together with the post-merger prices. In the second case, the only remaining

model component stems from the price coefficient α.

When using a regular Logit model instead of a Random Coefficient Logit model, all het-

erogeneity will be accounted for by the error term, such that the price elasticity of good j

with respect to good k at time t can be written as

ηjkt =

−pjtsjt

αsjt(1− sjt) j = k

pktsjtαsjtskt j 6= k

Estimates Table 2 shows demand side estimation results for several specifications of the

Logit model. Overall, using input prices, prices of other zones, brand characteristics or the

ownership change as instruments for the sales price in all but one specification yields a more

elastic demand curve than specification (3) without instruments. Accounting for brand-

specific fixed effects increases the the price-responsiveness even more dramatically. This can

be seen when comparing specifications (1) and (2). Both specifications use input prices and

the ownership change as instruments for the unobserved brand components. When accounting

for brand-specific fixed effects, however, the price coefficient is in absolute terms more than

24

four times higher then without accounting for these effects, with a value of −9.39 compared

to −2.08. Table 12 shows results for a random coefficients logit demand model. In this

specification I include random coefficients for price, a constant, sugar content and sogginess

of cereal. Furthermore, I use demographic data on mean income, income standard deviation,

household size and on number of small children to estimate these random coefficients. The

results show a positive relationship between income and price, which is consistent with higher

markups in high income neighborhoods. Price also interacts positively with the number of

small children, which might account for their responsiveness to advertising. Income interacts

negatively with sugar, which might be attributed to more health-consciousness of higher

income households.

Table 5 shows the mean elasticities over all markets for a random coefficient Logit model.

The own-price elasticities are highly negative for all firms, ranging from −7.55 for GM Trix

to −3.11 for Kellogg’s Corn Flakes. There is furthermore significant variation in different

brands’ subsitution patterns. GM Cheerios has the highes corss-price elasticities, going up

to .67 to GM Total Corn Flakes, while implied elasticities of KE Smacks and NAB Shredded

wheat are usually around .05. Table 6 shows the mean elasticities over all markets from

the IV Logit specification (1), i.e. using ownership change, input prices, as well as brand

dummies as instruments. Both own- and cross-price elasticities are much smaller in absolute

magnitude, with the own-price elasticities now ranging from −2.43 to −1.08, again for GM

Trix and KE Corn Flakes, respectively. The cross-price elasticities are now very close to

0, which can partly be amounted to the relatively high share of the outside good in the

estimation.

4.4 Supply side and conduct estimation

On the supply side, I use a nested two-step routine. In the first step, I back out marginal

cost conditional on a specific form of conduct as the outer loop. In the second step, I recover

the supply side parameters by regressing the backed out marginal costs on the observable

cost characteristics while controlling for unobserved brand characteristics.

Backing out marginal costs via first order conditions I make two assumptions regarding

marginal costs across stores and across time. I assume that at a given point in time, marginal

costs are constant across all stores. This is a natural assumption when considering that

all stores are within the same metropolitan area and are operated by the same retailer.

Therefore, the only channels through which marginal costs could differ across stores are

either a difference in the retail margin across stores, or a difference in distribution costs. I

do not find evidence for structural differences regarding the former in the data. Differences

in the latter also do not seem likely because of the relative proximity of the stores. Thus,

when backing out marginal cost across stores, I average them for a given time period.

Secondly, I explicitly allow marginal costs to vary over time. This is because I am in-

25

terested in finding the determinants for marginal costs pre-merger and then predicting post

merger prices using variation in input prices over time. Therefore, I recover marginal costs

over several pre-merger periods and use the estimates to predict post-merger also for different

post-merger periods. This is a further difference to conventional merger simulations. There,

one often only predicts the equilibrium for one post-merger period which also assumes only

one predicted vector of post-merger marginal costs.

Post-merger price equilibrium There are several ways to predict the price changes caused

by a merger. The main difference lies in how to account for post merger market shares.

I treat the observed post-merger prices in the data as equilibrium prices. Methodically

this is a fundamental difference to the existing literature regarding merger simulation. In

this literature, one usually simulates for a new price equilibrium using a specific form of

competition and the parameters recovered from the demand simulation. As a convergence

criterion one looks for a price vector that constitutes a mutual best response of prices given

the predicted market shares using demand estimates.13 There are several advantages from

using the actual post-merger prices instead of simulating a post-merger price equilibrium.

Firstly, when simulating for a new price equilibrium, one needs to make an assumption

regarding competition in the market. Already without estimating industry conduct, this is

computationally demanding. Furthermore, it does not make use of all the available post-

merger data, i.e. market shares and prices. Secondly, by using post-merger price simulation,

one also risks averaging out specific competitive patterns and introduces a simulation error.

Inner loop - cost parameter estimation In the second step of my supply side estimation

procedure, I use the marginal costs that were backed out conditional on a specific form of

industry conduct and estimate the marginal cost equation 8 via minimizing the following

GMM objective function:

γS = arg minγS

ω(Θ, γS, γD)′ZωA−1ω Z ′ωω(Θ, γS, γD). (20)

A−1ω is a consistent estimate of the covariance E[Z ′ωω(Θ, γS, γD)ω(Θ, γS, γD)′Zω]. The brand

specific marginal cost fixed effect ωj may be correlated with unobservable product charac-

teristics. Therefore it is essential to look for instruments that are correlated with marginal

costs, but not with the error term. To account for the effects of unobserved cost drivers on

prices, I use first order basis functions of the own brand characteristics, own firm characteris-

tics, and competitors’ characteristics. This relies on an exchangeability argument of product

characteristics when facing a unique Nash equilibrium, see for example Berry et al. (1995).

Outer loop - conduct estimation Having obtained the demand side coefficients γD and the