concern in the us and danger in europe - · pdf fileconcern in the us and danger in europe ......

TRANSCRIPT

12 January 2015

Daily Market Outlook

1

Please see disclaimer on last page

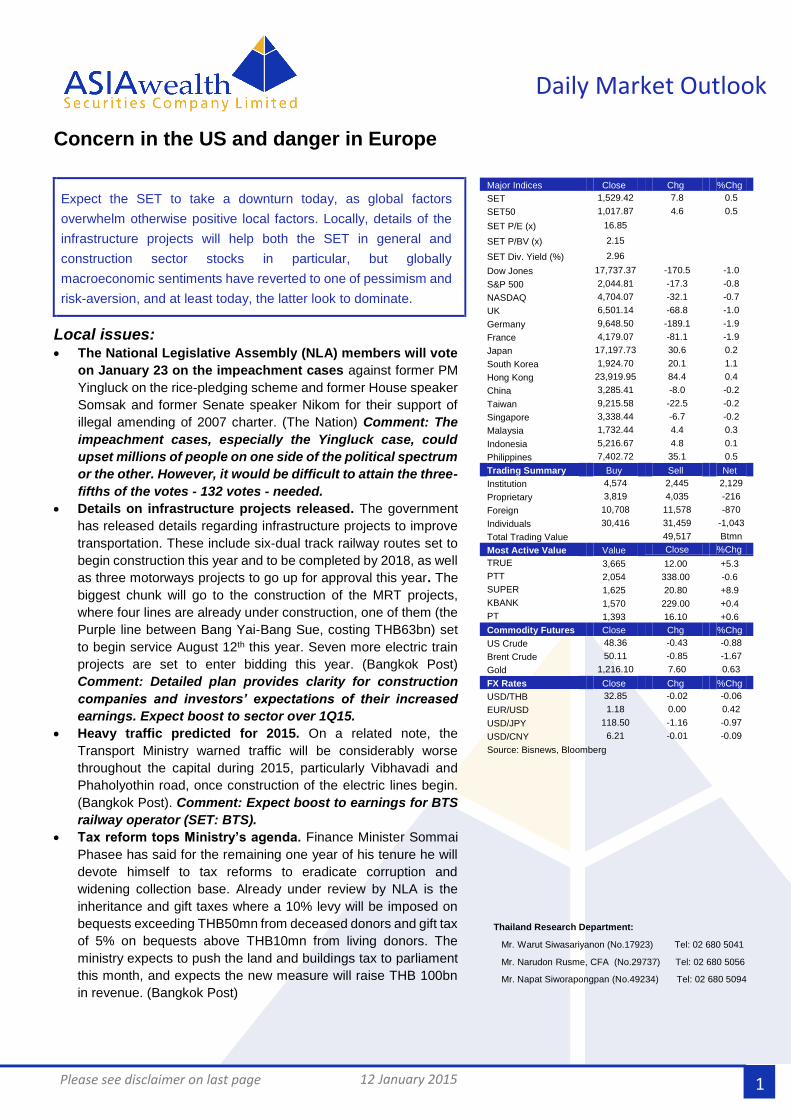

Concern in the US and danger in Europe

Expect the SET to take a downturn today, as global factors

overwhelm otherwise positive local factors. Locally, details of the

infrastructure projects will help both the SET in general and

construction sector stocks in particular, but globally

macroeconomic sentiments have reverted to one of pessimism and

risk-aversion, and at least today, the latter look to dominate.

Local issues: The National Legislative Assembly (NLA) members will vote

on January 23 on the impeachment cases against former PM

Yingluck on the rice-pledging scheme and former House speaker

Somsak and former Senate speaker Nikom for their support of

illegal amending of 2007 charter. (The Nation) Comment: The

impeachment cases, especially the Yingluck case, could

upset millions of people on one side of the political spectrum

or the other. However, it would be difficult to attain the three-

fifths of the votes - 132 votes - needed.

Details on infrastructure projects released. The government

has released details regarding infrastructure projects to improve

transportation. These include six-dual track railway routes set to

begin construction this year and to be completed by 2018, as well

as three motorways projects to go up for approval this year. The

biggest chunk will go to the construction of the MRT projects,

where four lines are already under construction, one of them (the

Purple line between Bang Yai-Bang Sue, costing THB63bn) set

to begin service August 12th this year. Seven more electric train

projects are set to enter bidding this year. (Bangkok Post)

Comment: Detailed plan provides clarity for construction

companies and investors’ expectations of their increased

earnings. Expect boost to sector over 1Q15.

Heavy traffic predicted for 2015. On a related note, the

Transport Ministry warned traffic will be considerably worse

throughout the capital during 2015, particularly Vibhavadi and

Phaholyothin road, once construction of the electric lines begin.

(Bangkok Post). Comment: Expect boost to earnings for BTS

railway operator (SET: BTS).

Tax reform tops Ministry’s agenda. Finance Minister Sommai

Phasee has said for the remaining one year of his tenure he will

devote himself to tax reforms to eradicate corruption and

widening collection base. Already under review by NLA is the

inheritance and gift taxes where a 10% levy will be imposed on

bequests exceeding THB50mn from deceased donors and gift tax

of 5% on bequests above THB10mn from living donors. The

ministry expects to push the land and buildings tax to parliament

this month, and expects the new measure will raise THB 100bn

in revenue. (Bangkok Post)

Thailand Research Department:

Mr. Warut Siwasariyanon (No.17923) Tel: 02 680 5041

Mr. Narudon Rusme, CFA (No.29737) Tel: 02 680 5056

Mr. Napat Siworapongpan (No.49234) Tel: 02 680 5094

Major Indices Close Chg %Chg

SET 1,529.42 7.8 0.5

SET50 1,017.87 4.6 0.5

SET P/E (x) 16.85 SET P/BV (x) 2.15 SET Div. Yield (%) 2.96 Dow Jones 17,737.37 -170.5 -1.0

S&P 500 2,044.81 -17.3 -0.8

NASDAQ 4,704.07 -32.1 -0.7

UK 6,501.14 -68.8 -1.0

Germany 9,648.50 -189.1 -1.9

France 4,179.07 -81.1 -1.9

Japan 17,197.73 30.6 0.2

South Korea 1,924.70 20.1 1.1

Hong Kong 23,919.95 84.4 0.4

China 3,285.41 -8.0 -0.2

Taiwan 9,215.58 -22.5 -0.2

Singapore 3,338.44 -6.7 -0.2

Malaysia 1,732.44 4.4 0.3

Indonesia 5,216.67 4.8 0.1

Philippines 7,402.72 35.1 0.5

Trading Summary Buy Sell Net

Institution 4,574 2,445 2,129

Proprietary 3,819 4,035 -216

Foreign 10,708 11,578 -870

Individuals 30,416 31,459 -1,043

Total Trading Value 49,517 Btmn

Most Active Value Value Close %Chg

TRUE 3,665 12.00 +5.3

PTT 2,054 338.00 -0.6

SUPER 1,625 20.80 +8.9

KBANK 1,570 229.00 +0.4

PT 1,393 16.10 +0.6

Commodity Futures Close Chg %Chg

US Crude 48.36 -0.43 -0.88

Brent Crude 50.11 -0.85 -1.67

Gold 1,216.10 7.60 0.63

FX Rates Close Chg %Chg

USD/THB 32.85 -0.02 -0.06

EUR/USD 1.18 0.00 0.42

USD/JPY 118.50 -1.16 -0.97

USD/CNY 6.21 -0.01 -0.09

Source: Bisnews, Bloomberg

12 January 2015

Daily Market Outlook

2

Please see disclaimer on last page

ADVANC (Bt248 BUY 2015TP Bt253) February plans to roll out fixed broadband

services in 10 provinces nationwide, using a combination of VDSL, fibre optic and

wireless broadband technologies. Digital content (video, games and commerce

application, cloud computing, machine-to-machine transaction), will be the

software that will leverage the company's new expansion in hardware over the

next 3-5 years. This is not to buy content but will be done by finding partners.

(Bangkok Post)

PTT expects its 2015 net profit will remain the same as last year, despite the huge

slump of crude price, as it will write off its oil inventory loss last year which will not

carry forward to this year. Moreover, the company would benefit from

government's policy to float the natural gas retail price structure and would

recognize a one-off profit from the planned sale of Bangchak stake, which are

expect to generate income of around Bt10. (Bangkok Post)

TASCO (Tipco Asphalt Plc), the country's biggest asphalt producer, expects sales

volume to grow by 26% this year, driven by domestic infrastructure projects. The

Transport Ministry has set aside a certain amount for new roads and maintenance

of existing ones, with Bt6.1bn to be spent by the Highway Department and Bt1.5bn

by the Rural Roads Department. The company also plan to expand in Vietnam,

Laos, Cambodia and Myanmar to take advantage of rising demand. The company

is due to report 2014 sales volume of 1.8 million tonnes and revenue of Bt46bn.

(Bangkok Post)

Global issues The end of last week saw a downturn of global macroeconomics sentiment, as

well as general resurgence in risk aversion. Ambiguous labor market data put the

strength of US labor market into question, while poor German performance

deepened concern over the Eurozone. The backdrop of geopolitical turmoil,

notably the recent spike in urban terrorist attacks, have augmented risk-aversion

amongst investors, as reflected in the flight to the proverbial safe haven, gold.

USA Wall Street stocks fell on Friday following a 2-day rally as December's jobs

report gave a mixed view of the economy, with financial shares leading the way

lower. All three major indexes posted slight losses for the week and fell back into

negative territory for 2015. US nonfarm payrolls rose in December, topping Wall

Street expectations, but hourly wages unexpectedly fell. (Reuters)

US job growth increased briskly in December. Nonfarm payrolls increased by

252,000 last month after an upwardly revised jump of 353,000 in November. The

jobless rate fell 0.2 percentage point to a 6-1/2-year low of 5.6%. December

marked the 11th straight month of payroll increases above 200,000, the longest

stretch since 1994. For last year as a whole, the economy generated 2.95 million

new jobs, the strongest annual showing since 1999.

US wages posted their biggest decline in at least 8 years. The surprise five-

cent, or 0.2%, decrease in average hourly earnings to US$24.57 took some shine

off the otherwise upbeat report.

The dollar eased on Friday after a US labor market report suggested a go-slow

approach to raising interest rates. The dollar traded at ¥118.56, a loss of 0.91%.

The euro rose 0.43% to US$1.1843. (Reuters)

12 January 2015

Daily Market Outlook

3

Please see disclaimer on last page

Europe European shares snapped a 2-day winning streak on Friday, ahead of key

US non-farm payrolls data, after Spain’s Banco Santander the largest bank in

Europe unveiled a capital hike and dividend cut. Adding to the negative

sentiment, industrial and trade data from Germany were weak. The pan-

European FTSEurofirst 300 index dipped back late on Friday to close 1.7% lower

at 1,345.60 points. (Reuters)

Industrial output from Germany, Europe's No. 1 economy, in November fell

0.1% MoM, compared with a Reuters consensus forecast gain of 0.4%. Exports

also fell sharply. (Reuters)

Asia Abe's ¥96.3tn (US$813bn) draft budget for the year from April, is to be

approved by the Cabinet on Wednesday and submitted to an upcoming session of Parliament, is up from this fiscal year's initial ¥95.9tn. (Reuters)

The People's Bank of China will continue to maintain "prudent" monetary policy in 2015, keeping credit growth stable while having its hands free to fine-tune policy when necessary. However, the central bank said it would quicken the pace of market-oriented interest rate reform and push forward on increasing yuan convertability in the capital account. (Reuters)

Commodities Global oil markets resumed their slide on Friday, with Brent and US crude

hitting April 2009 lows and ending down for a seventh straight week, although

prices recovered from their lows after a sharp drop in the US oil rig count. Brent

crude settled down 85 cents at US$50.11 a barrel. US crude settled down 43

cents at US$48.36. The number of US oil rigs fell by 61 units last week, the largest

drop in 24 years or since 1991, to 1,421 or the lowest since February 2014. The

number fell in 10 weeks out of the recent 13 weeks from the peak of 1,609 in the

middle of October. (Reuters)

Gold rose on Friday as the dollar and equities failed to react to a better-than-

forecast US jobs report, and the metal was set for the first weekly gain in 4 weeks

as political uncertainty in Greece boosted demand for assets seen as safe. Spot

traded up 0.8% at US$1,218.40 an ounce. US gold futures for February delivery

rose 0.6% to settle at US$1,216.10. (Reuters)

12 January 2015

Daily Market Outlook

4

Please see disclaimer on last page

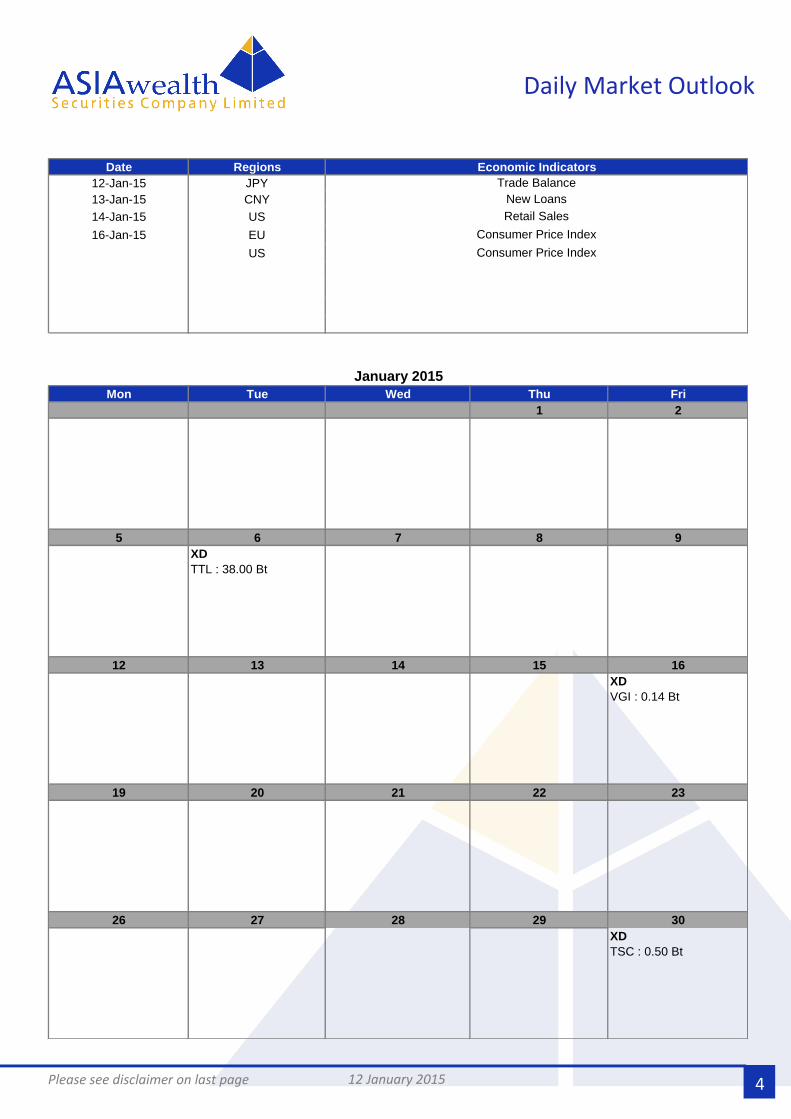

Date Regions

12-Jan-15 JPY

13-Jan-15 CNY

14-Jan-15 US

16-Jan-15 EU

US

Mon Tue Wed Thu Fri

1 2

5 6 7 8 9

XD

TTL : 38.00 Bt

12 13 14 15 16

XD

VGI : 0.14 Bt

19 20 21 22 23

26 27 28 29 30

XD

TSC : 0.50 Bt

January 2015

Economic Indicators

Trade Balance

New Loans

Retail Sales

Consumer Price Index

Consumer Price Index

12 January 2015 5

Please see disclaimer on last page

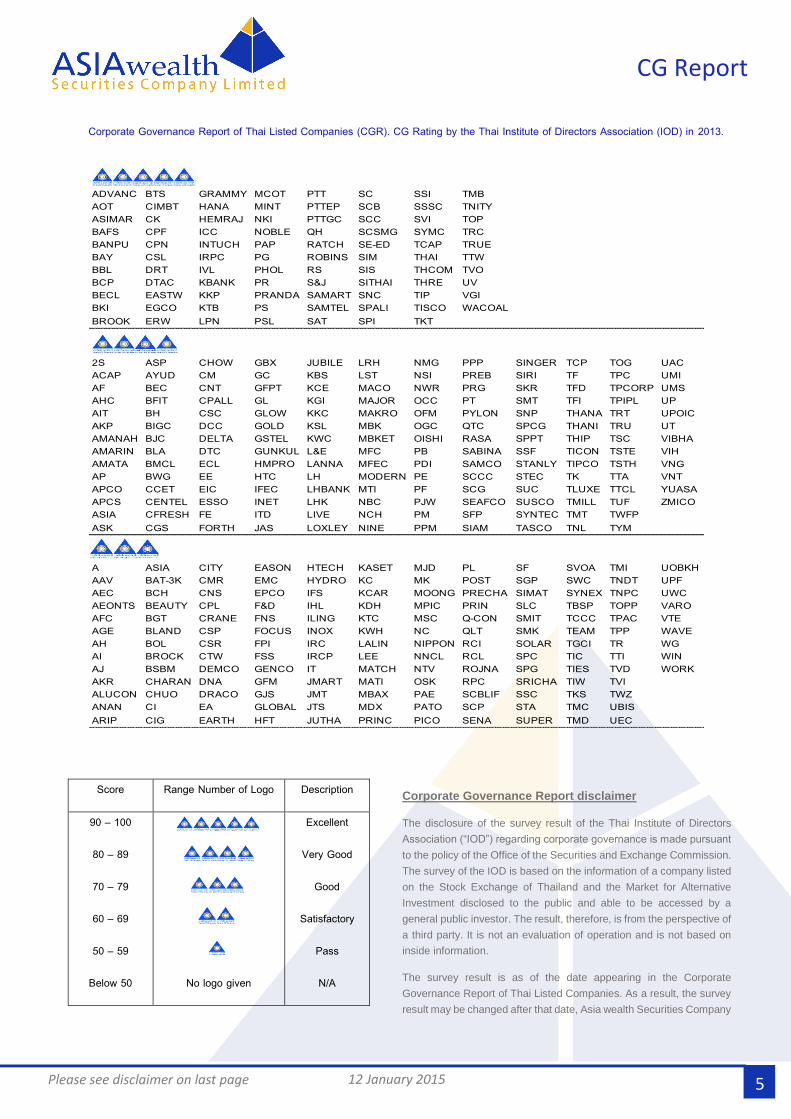

CG Report

Corporate Governance Report of Thai Listed Companies (CGR). CG Rating by the Thai Institute of Directors Association (IOD) in 2013.

ADVANC BTS GRAMMY MCOT PTT SC SSI TMBAOT CIMBT HANA MINT PTTEP SCB SSSC TNITYASIMAR CK HEMRAJ NKI PTTGC SCC SVI TOPBAFS CPF ICC NOBLE QH SCSMG SYMC TRCBANPU CPN INTUCH PAP RATCH SE-ED TCAP TRUEBAY CSL IRPC PG ROBINS SIM THAI TTWBBL DRT IVL PHOL RS SIS THCOM TVOBCP DTAC KBANK PR S&J SITHAI THRE UVBECL EASTW KKP PRANDA SAMART SNC TIP VGIBKI EGCO KTB PS SAMTEL SPALI TISCO WACOALBROOK ERW LPN PSL SAT SPI TKT

2S ASP CHOW GBX JUBILE LRH NMG PPP SINGER TCP TOG UACACAP AYUD CM GC KBS LST NSI PREB SIRI TF TPC UMIAF BEC CNT GFPT KCE MACO NWR PRG SKR TFD TPCORP UMSAHC BFIT CPALL GL KGI MAJOR OCC PT SMT TFI TPIPL UPAIT BH CSC GLOW KKC MAKRO OFM PYLON SNP THANA TRT UPOICAKP BIGC DCC GOLD KSL MBK OGC QTC SPCG THANI TRU UTAMANAH BJC DELTA GSTEL KWC MBKET OISHI RASA SPPT THIP TSC VIBHAAMARIN BLA DTC GUNKUL L&E MFC PB SABINA SSF TICON TSTE VIHAMATA BMCL ECL HMPRO LANNA MFEC PDI SAMCO STANLY TIPCO TSTH VNGAP BWG EE HTC LH MODERN PE SCCC STEC TK TTA VNTAPCO CCET EIC IFEC LHBANK MTI PF SCG SUC TLUXE TTCL YUASAAPCS CENTEL ESSO INET LHK NBC PJW SEAFCO SUSCO TMILL TUF ZMICOASIA CFRESH FE ITD LIVE NCH PM SFP SYNTEC TMT TWFPASK CGS FORTH JAS LOXLEY NINE PPM SIAM TASCO TNL TYM

A ASIA CITY EASON HTECH KASET MJD PL SF SVOA TMI UOBKHAAV BAT-3K CMR EMC HYDRO KC MK POST SGP SWC TNDT UPFAEC BCH CNS EPCO IFS KCAR MOONG PRECHA SIMAT SYNEX TNPC UWCAEONTS BEAUTY CPL F&D IHL KDH MPIC PRIN SLC TBSP TOPP VAROAFC BGT CRANE FNS ILING KTC MSC Q-CON SMIT TCCC TPAC VTEAGE BLAND CSP FOCUS INOX KWH NC QLT SMK TEAM TPP WAVEAH BOL CSR FPI IRC LALIN NIPPON RCI SOLAR TGCI TR WGAI BROCK CTW FSS IRCP LEE NNCL RCL SPC TIC TTI WINAJ BSBM DEMCO GENCO IT MATCH NTV ROJNA SPG TIES TVD WORKAKR CHARAN DNA GFM JMART MATI OSK RPC SRICHA TIW TVIALUCON CHUO DRACO GJS JMT MBAX PAE SCBLIF SSC TKS TWZANAN CI EA GLOBAL JTS MDX PATO SCP STA TMC UBISARIP CIG EARTH HFT JUTHA PRINC PICO SENA SUPER TMD UEC

Corporate Governance Report disclaimer

The disclosure of the survey result of the Thai Institute of Directors

Association (“IOD”) regarding corporate governance is made pursuant

to the policy of the Office of the Securities and Exchange Commission.

The survey of the IOD is based on the information of a company listed

on the Stock Exchange of Thailand and the Market for Alternative

Investment disclosed to the public and able to be accessed by a

general public investor. The result, therefore, is from the perspective of

a third party. It is not an evaluation of operation and is not based on

inside information.

The survey result is as of the date appearing in the Corporate

Governance Report of Thai Listed Companies. As a result, the survey

result may be changed after that date, Asia wealth Securities Company

Limited does not conform nor certify the accuracy of such survey result.

Score Range Number of Logo Description

90 – 100

80 – 89

70 – 79

60 – 69

50 – 59

Below 50

No logo given

Excellent

Very Good

Good

Satisfactory

Pass

N/A

12 January 2015

Contact

6

Please see disclaimer on last page

This report has been prepared by Asia Wealth Securities Company Limited (“AWS”). The information herein has been obtained from sources believed to be reliable and accurate, but AWS makes no representation as to the accuracy and completeness of such information. AWS does not accept any liability for any loss or damage of any kind arising out of the use of such information or opinions in this report. Before making your own independent decision to invest or enter into transaction, investors should study this report carefully and should review information relating. All rights are reserved. This report may not be reproduced, distributed or published by any person in any manner for any purpose without permission of AWS. Investment in securities has risks. Investors are advised to consider carefully before making decisions.

Branch Address Phone Fax

Head Office 540 Floor 7,14,17 , Mercury Tower, Ploenchit Road, Lumphini,

Pathumwan Bangkok 10330

02-680-5000 02-680-5111

Silom 191 Silom Complex Building,21st Floor Room 2,3-1 Silom Rd.,

Silom, Bangrak, Bangkok, 10500 Thailand

02-630-3500 02-630-3530-1

Asok 159 Sermmitr Tower, 17th FL. Room No.1703, Sukhumvit 21

Road, Klong Toey Nua, Wattana, Bangkok 10110

02-261-1314-21 02-261-1328

Pinklao

7/3 Central Plaza Pinklao Office Building Tower B, 16th Flr., Room

No.1605-1606 Baromrajachonnanee Road, Arunamarin,

Bangkoknoi, Bangkok 10700

02-884-7333 02-884-7357,

02-884-7367

Chaengwattana

99/99 Moo 2 Central Plaza Chaengwattana Office Tower, 22nd Flr.,

Room 2204 Chaengwattana Road, Bang Talad, Pakkred,

Nonthaburi 11120

02-119-2300 02-8353006

Chaengwattana 2

9/99 Moo 2 Central Plaza Chaengwattana Office Tower, 22nd Flr.,

Room 2203 Chaengwattana Road, Bang Talad, Pakkred,

Nonthaburi 11120

02-119-2388 02-119-2399

Mega Bangna 39 Moo6 Megabangna, 1st Flr., Room 1632/7 Bangna-Trad Road,

Bangkaew Bangplee, Samutprakarn 10540

02-106-7345 02-105-2070

Rayong 356/18 Sukhumvit Road, Nuen-Phra Sub District, Muang District,

Rayong Province 21000

038-808200 038-807200

Khonkaen 26/9 Srijanmai Road, Tamboonnaimuang, Khon Khaen

40000

043-334-700 043-334-799

Chonburi 44 Vachiraprakarn Road, Bangplasoi, Muang Chonburi, Chonburi

20000

038-274-533 038-275-168

Chaseongsao 233-233/2 Moo2 1st Flr., Sukprayoon Road, Na Meung Sub-

District, Meung District, Chachoengsao 24000

038-981-587 038-981-591