compliance with global standards: basel, coso, iso, …

TRANSCRIPT

1 | P a g e

COMPLIANCEWITHGLOBALSTANDARDS:BASEL,COSO,ISO,NIST,&SARBOX

TheEnterpriseRiskManagement(ERM)methodsdeployedbyanyorganizationshouldatleastconsider

compliancewithglobalstandardsifnotexactlymirroringCOSO(CommitteeofSponsoringOrganizations

oftheTreadwayCommission,withrespecttotheirorganizingcommitteesatAAA,AICPA,FEI,IMA,and

IIA),InternationalStandardsISO31000:2009,theU.S.Sarbanes–OxleyAct,theBaselIIIrequirementsfor

OperationalRisk(fromtheBaselCommitteethroughtheBankof InternationalSettlements),andNIST

800‐37. The parallels and applications of ROV methodologies closely mirror these regulatory and

internationalstandardsand,attimes,exceedthesestandards.Figures1‐10illustratesomeexamplesof

compliance with ISO 31000:2009, and Figures 11‐20 show compliance with Basel II and Basel III

requirements.Thesefiguresandthesummarylistsbelowassumethatthereaderisalreadyfamiliarwith

theIRMmethodologyemployedbyRealOptionsValuation,Inc.

CompliancewithInternationalStandardsOrganizationISO31000:2009

ThefollowingprovidesaquicksummarypertainingtoISOcompliance:

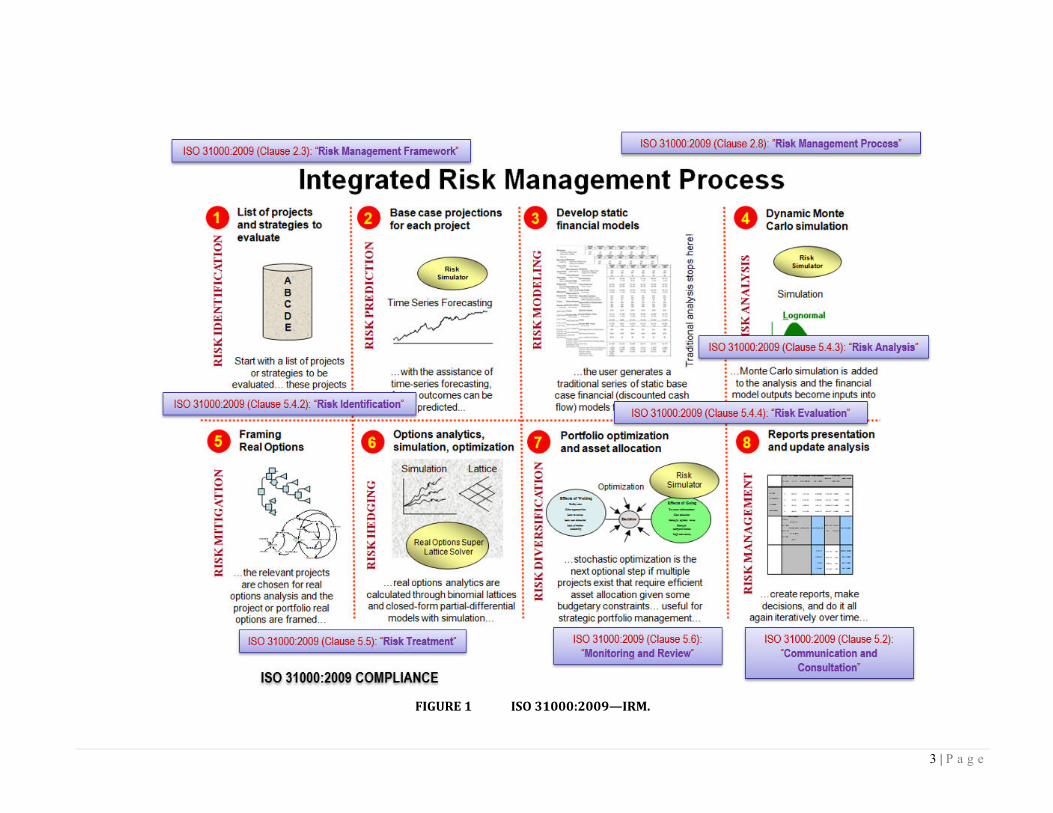

TheIRMmethodologyweemployisinlinewithISO31000:2009Clauses2.3and2.8requiring

ariskmanagementprocess(Figure1),aswellasClause5(5.4.2requiringriskidentification

where we use Tornado analysis and scenario analysis; 5.4.3. requiring quantitative risk

analysis where we apply Monte Carlo risk simulations; 5.4.4 where existing Excel‐based

evaluationmodelsareusedandoverlaidwithIRMmethodologiessuchassimulations;etc.).

SeeModelingRisk,3rdEdition’sChapter1fordetailsontheIRMmethodology. ISO31000:2009Clause5.4.4 looksat therisk tolerance levelsandcomparingvariousrisk

levels in a portfolio optimization and efficient frontier analysis employed in our IRM

methodology(Figure2).SeeModelingRisk,3rdEdition’sChapters10and11foroptimizationandefficientfrontiermodeling.

Figure3showsquantifiedconsequencesand the likelihoods (probabilitiesandconfidence

levels)ofpotentialeventsthatcanoccurusingsimulations,asrequiredinISO31000:2009

Clauses2.1and5.4.3.

ISO 31000:2009 Clause 5.4.3 requires viewing the analysis from various stakeholders,

multiple consequences, andmultiple objectives to develop a combined level of risk. This

perspective isachieved throughamulticriteriaoptimizationandefficient frontieranalysis

(Figure 4) in the IRM process. SeeModeling Risk, 3rd Edition’s Chapters 10 and 11 foroptimizationandefficientfrontiermodeling.

ISO31000:2009Clause3Frequiresthathistoricaldataandexperienceaswellasstakeholder

feedback and observation coupled with expert judgment be used to forecast future risk

events. The IRMprocess employs a family of 16 forecastingmethods (Figure 5 shows an

exampleoftheARIMAmodel)coupledwithrisksimulationswithhighfidelitytodetermine

thebestgoodness‐of‐fitwhenhistoricaldataexists,orusingsubjectmatterexpertestimates

andstakeholderassumptions,wecanapplytheDelphimethodandcustomdistributiontorun

risksimulationsontheforecasts.SeeModelingRisk,3rdEdition’sChapters8and9forforecastmethodsandanalyticaldetails.

2 | P a g e

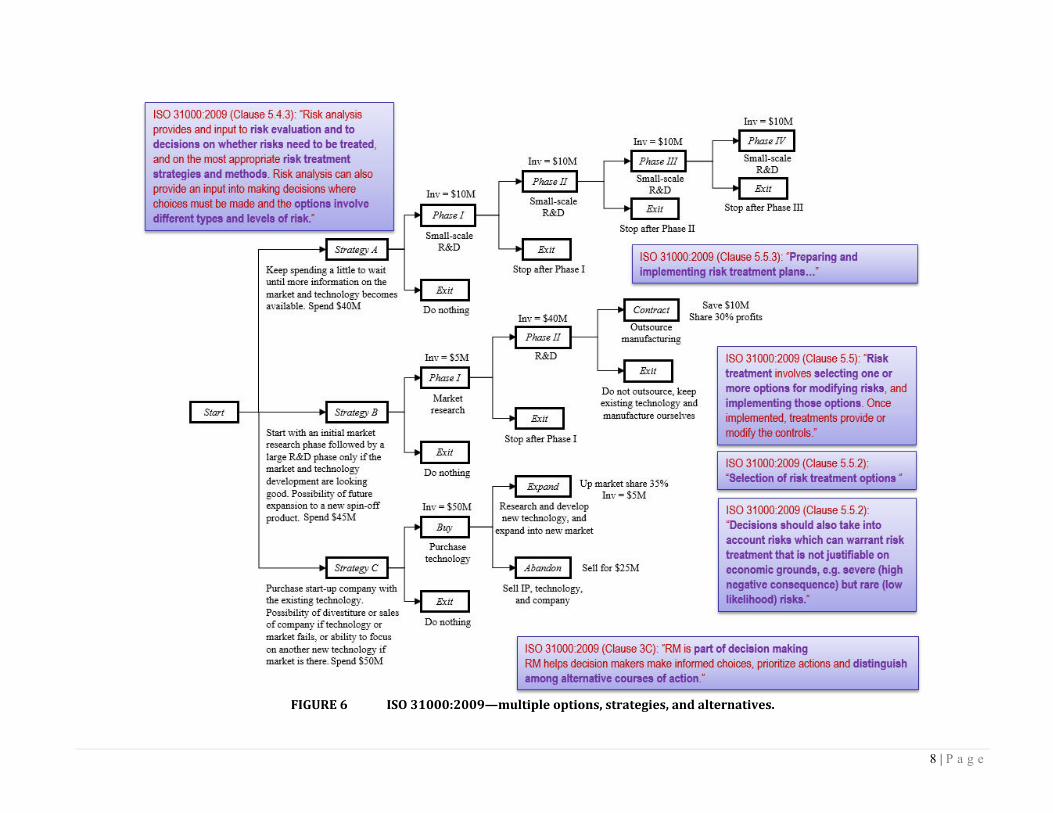

ISO31000:2009Clauses3C,5.4.3,5.5,and5.5.2requireriskevaluationsonrisktreatments,

optionstoexecutewhentherearedifferenttypesofrisks,andselectingandimplementing

variousrisktreatmentstrategicoptionsthatarenotsolelyreliantoneconomics.TheIRM’s

strategic real optionsmethodology allows users tomodelmultiple path‐independent and

path‐dependentimplementationstrategiesoralternatecoursesofactionthataregenerated

tomitigatedownsiderisksandtakeadvantageofupsidepotentials(Figure6).SeeModelingRisk,3rdEdition’sChapters12and13fordetailsonrealoptionsanalysismodelingtechniques.

Figure7illustrateshowISO31000:2009Clauses3D,3E,and5.4.3aresatisfiedusingtheIRM

process of probability distribution fitting of uncertain variables and how their

interdependencies(correlations)areexecuted.

Riskcontrolsarerequired in ISO31000:2009Clauses2.26,4.43,and5.4.3(Figure8).The

controlchartsandRiskEffectivenesscalculationsinPEATERMhelpdecisionmakersidentify

if aparticular riskmitigationstrategyandresponse thatwasenactedhadsufficientlyand

statisticallysignificantlyaffectedtheoutcomesoffutureriskstates.

Scenarios, cascading, and cumulative effects (consequences) are also the focus of ISO

31000:2009 Clause 5.4.2. The IRM method employs Tornado analysis, scenario analysis,

dynamicsensitivityanalysis,andrisksimulations(Figure9)toidentifywhichinput(s)have

thehighestimpactontheorganization’srisksandmodeltheirimpactsonthetotalrisksof

theorganization.

ISO 31000:2009 Clause 5.2 requires proper communication of risk exposures and

consequences,andanunderstandingofthebasisandreasonsofeachrisk.ThePEATERM

Risk Dashboards provide details and insights for a better understanding of the issues

governingeachoftheriskissuesinanorganization(Figure10).

3 | P a g e

FIGURE1 ISO31000:2009—IRM.

4 | P a g e

FIGURE2 ISO31000:2009—risktolerance.

5 | P a g e

FIGURE3 ISO31000:2009—consequencesandlikelihood.

6 | P a g e

FIGURE4 ISO31000:2009—multiplestakeholderobjectivesandconsequences.

7 | P a g e

FIGURE5 ISO31000:2009—historicaldataandfutureforwardforecast.

8 | P a g e

FIGURE6 ISO31000:2009—multipleoptions,strategies,andalternatives.

9 | P a g e

FIGURE7 ISO31000:2009structuredapproach,fitting,andcorrelations.

10 | P a g e

FIGURE8 ISO31000:2009—riskcontrolefficiencyandeffectiveness.

11 | P a g e

FIGURE9 ISO31000:2009—consequences,cascades,andscenarios.

12 | P a g e

FIGURE10 ISO31000:2009—communicationandconsultation.

13 | P a g e

CompliancewithBaselIIandBaselIIIRegulatoryRequirements

ThefollowingprovidesasummaryofBaselIIandBaselIIIcompliancewhenusingtheIRMmethodology:

Figure11showsMonteCarlorisksimulationsappliedtodetermineconfidencelevels,percentiles,

and probabilities of occurrence using historically fitted data or forecast expectations. These

methodsareinlinewithBaselIIandBaselIIIrequirementsSections16and161concerningtheuse

ofhistorical simulations,MonteCarlo simulations, and99thpercentile confidence intervals. See

ModelingRisk,3rdEdition’sChapters5and6fordetailsonsimulationsanddatafittingtechniques. Figure12showsacorrelatedsimulationofaportfolioofassetsandliabilities,whereassetreturns

are correlated against one another in a portfolio and optimization routines were run on the

simulated results.Theseprocessesprovide compliancewithBasel II andBasel III requirements

Sections178, 232, and527(f) involving correlations, Value atRisk orVaRmodels, portfolios of

segments,andpooledexposures(assetsandliabilities).SeeModelingRisk,3rdEdition’sChapter5for correlated simulations and Chapter 7’s case study on Basel II and Basel III Credit, Market,

Operational,andLiquidityRiskswithAssetLiabilityManagementfordetailsonhowVaRmodels

arecomputedbasedonhistoricalsimulationresults.

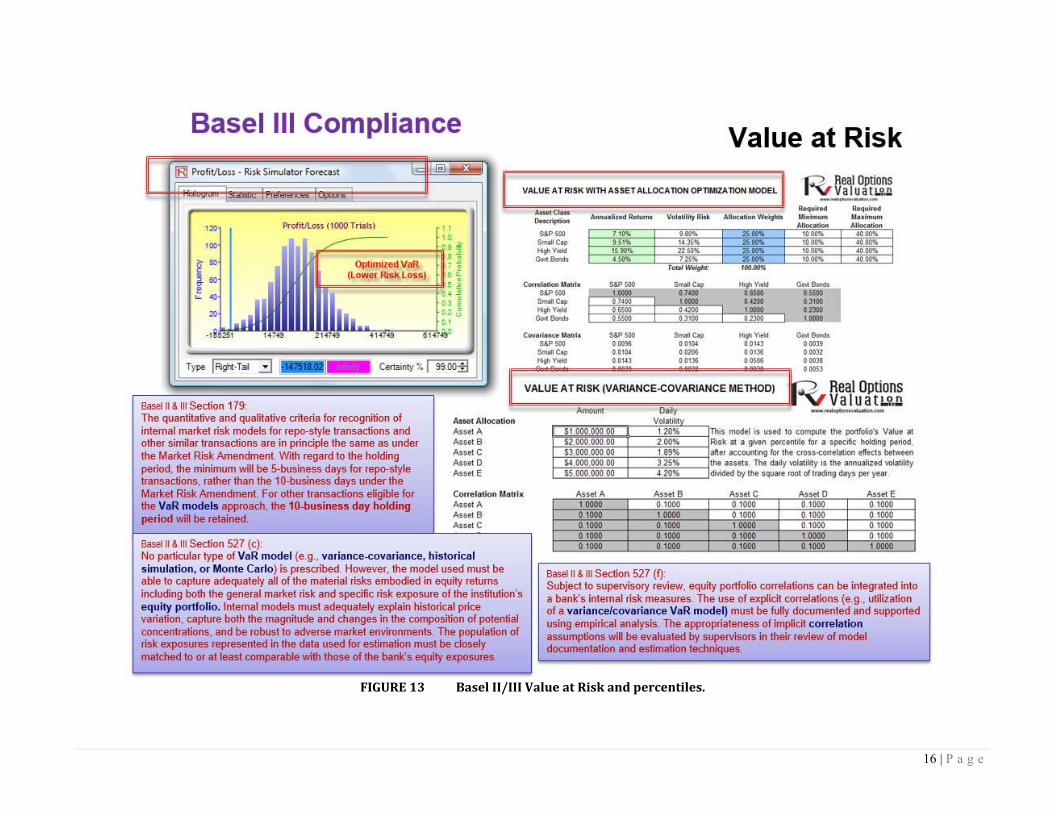

Figure13showsValueatRiskpercentileandconfidencecalculationsusingstructuralmodelsand

simulationresultsthatareinlinewithBaselIIandBaselIIIrequirementsSections179,527(c),and

527(f).Asnotedabove,seeModelingRisk,3rdEdition’sChapter7’scasestudyfordetailsonhowVaRmodelsarecomputedbasedonhistoricalsimulationresults.

Figure14showsthecomputationsofprobabilityofdefault(PD)asrequiredintheBaselAccords,

specificallyBaselIIandBaselIIISection733andAnnex2’sSection16.PDcanbecomputedusing

structuralmodelsorbasedonhistoricaldatathroughrunningbasicratiostomoreadvancedbinary

logisticmodels.ModelingRisk,3rdEdition’sChapter7’scasestudyaswellasChapter14’sCreditandMarketRiskcasestudyprovidemoreinsights intohowPDcanbecomputedusingthesevariousmethods.

Figure15showsthesimulationandgenerationofinterestrateyieldcurvesusingRiskSimulator

andModelingToolkitmodels.ThesemethodsareinlinewithBaselIIandBaselIIIrequirements

Section763requiringtheanalysisofinterestratefluctuationsandinterestrateshocks.

Figure16 showsadditionalmodels for volatile interest rate, financialmarkets, andother liquid

instruments’ instantaneous shocks using Risk Simulator’s stochastic process models. These

analysesconformtoBaselIIandBaselIIIrequirementsSections155,527(a),and527(b).

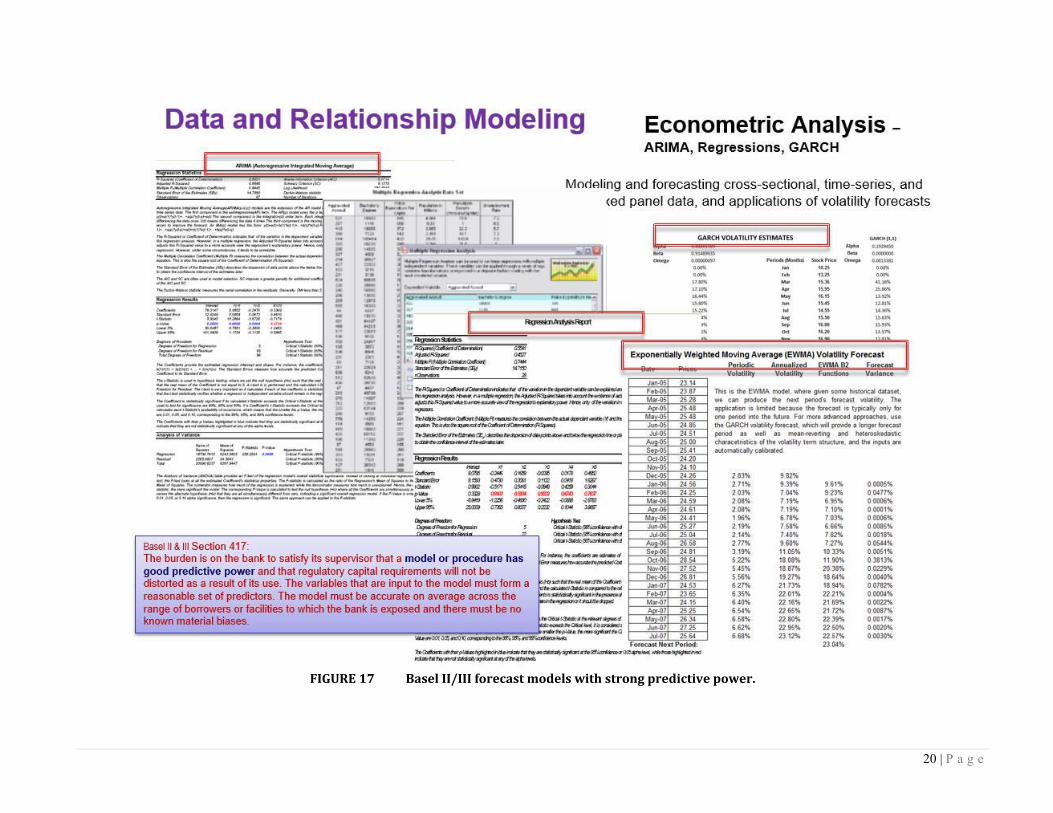

Figure17showsseveralforecastmodelswithhighpredictiveandanalyticalpower,whichisapart

oftheRiskSimulatorfamilyofforecastmethods.SuchmodelingprovidescompliancewithBaselII

andBaselIIIrequirementsSection417requiringmodelsofgoodpredictivepower.

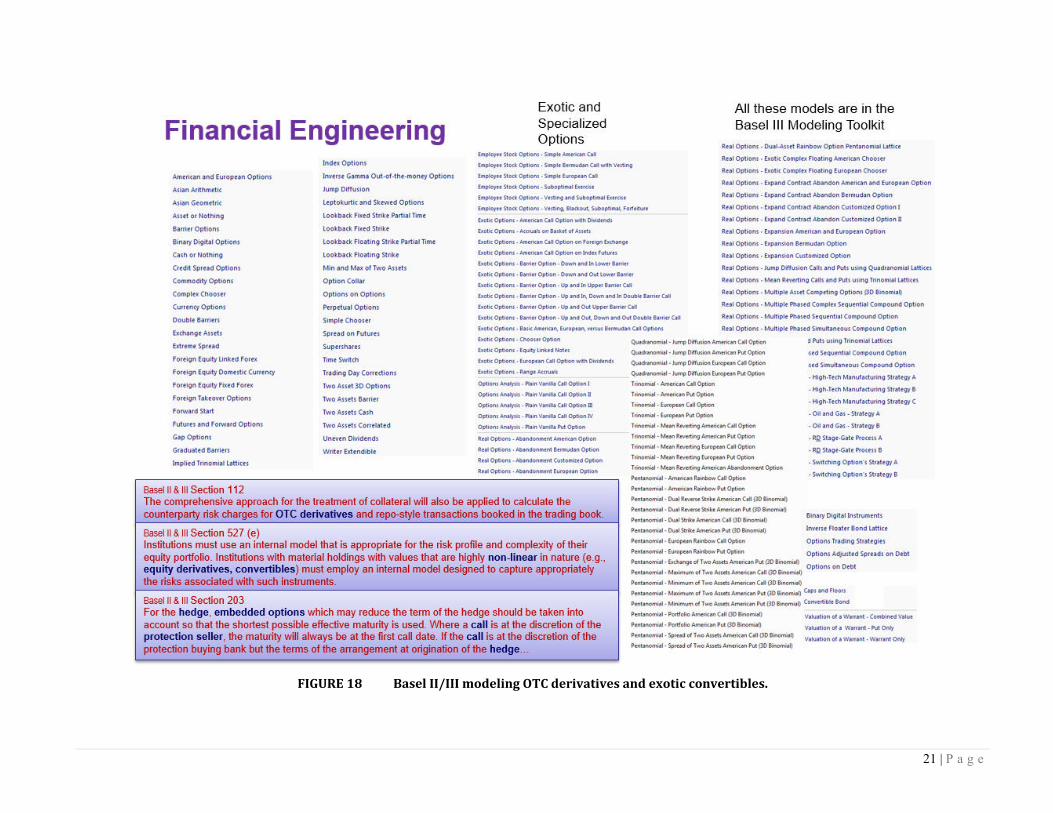

Figure18showsthelistoffinancialandcreditmodelsavailableintheROVModelingToolkitand

ROV Real Options SLS software applications. These models conform to Basel II and Basel III

requirementsSections112,203,and527(e)requiringtheabilitytovalueover‐the‐counter(OTC)

derivatives,nonlinearequityderivatives,convertibles,hedges,andembeddedoptions.

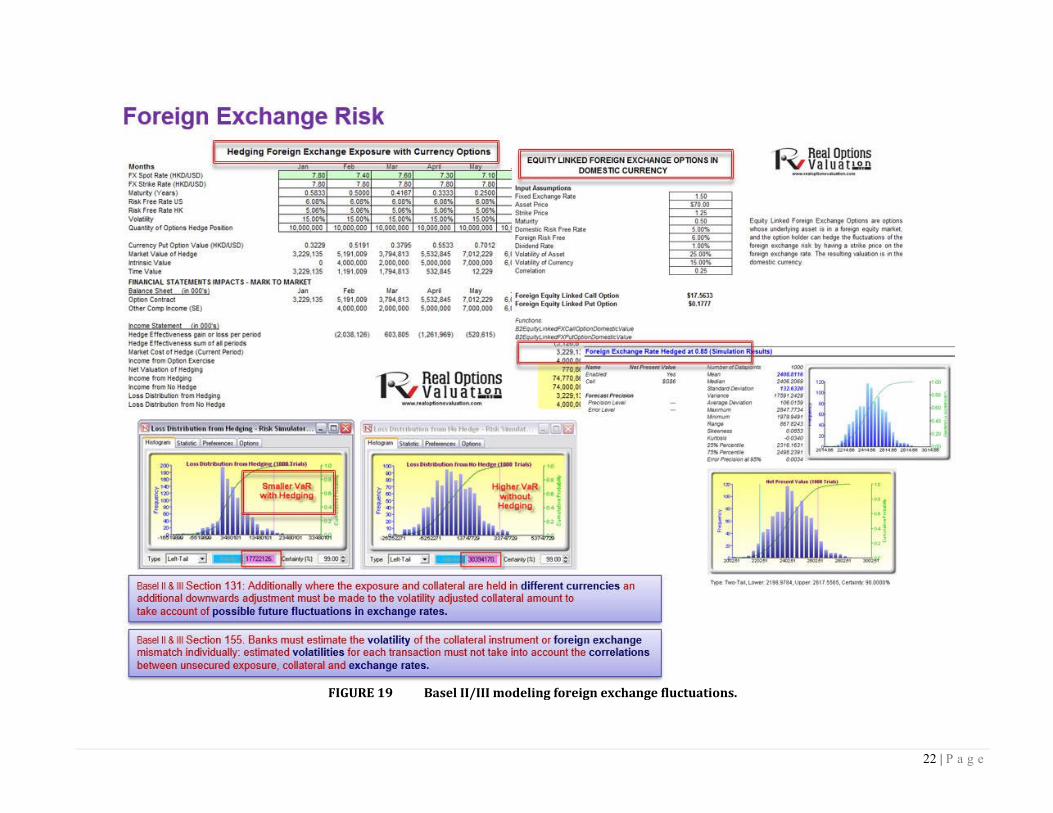

Figure19showsthemodelingofforeignexchangeinstrumentsandhedgestodeterminetheefficacy

and effectiveness of foreign exchange hedging vehicles and their impact on valuation, portfolio

profitability,andVaR,inlinewithBaselIIandBaselIIISections131and155requiringtheanalysis

ofdifferentcurrencies,correlations,volatility,andhedges.

Figure20showstheoption‐adjustedspread(OAS),creditdefaultswaps(CDS),andcreditspread

options(CSO)modelsinROVModelingToolkit.ThesemodelsprovidecompliancewithBaselIIand

BaselIIIrequirementsSections140and713pertainingtomodelingandvaluingcreditderivatives

andcredithedges.

14 | P a g e

FIGURE11 BaselII/IIIconfidencelevels,MonteCarlosimulations,andcreditrisk.

15 | P a g e

FIGURE12 BaselII/IIIcorrelatedportfoliosandcorrelatedsimulations.

16 | P a g e

FIGURE13 BaselII/IIIValueatRiskandpercentiles.

17 | P a g e

FIGURE14 BaselII/IIIcreditriskanalysis.

18 | P a g e

FIGURE15 BaselII/IIIinterestrateriskandmarketshocks.

19 | P a g e

FIGURE16 BaselII/IIIvolatilityandadverseinstantaneousshocks.

20 | P a g e

FIGURE17 BaselII/IIIforecastmodelswithstrongpredictivepower.

21 | P a g e

FIGURE18 BaselII/IIImodelingOTCderivativesandexoticconvertibles.

22 | P a g e

FIGURE19 BaselII/IIImodelingforeignexchangefluctuations.

23 | P a g e

FIGURE20 BaselII/IIIcreditderivativesandhedging.

24 | P a g e

CompliancewithCOSOIntegratedERMFramework

ThefollowingprovidesaquicksummaryofCOSOIntegratedERMFrameworkcompliancewhenusing

theIRMmethodology:

Figure21(16.45)showsthePEATERMmodule’sRiskRegistertabwheremitigationcostsand

benefits(grossrisksreducedtoresidualrisklevels),likelihoodandimpactmeasures,andspreads

withvaryingprecisionlevelsreadyforMonteCarlorisksimulationaresituated,incompliance

withCOSOERMFrameworkSections5&6.

Figure22(16.46)showsthePEATERMmodulewherethelikelihoodandimpactwithinarisk

mapisgenerated,incompliancewithCOSOAT/Exhibit5.13.

Figure 23 (16.47) shows compliance with COSO AT/Exhibit 6.5 and COSO ERM Integrated

FrameworkSection6,whereentity‐wideportfolioandbusinessunit,department,andfunctional

areas’grossandresidualrisksarecomputed.

Figure 24 (16.48) continues by showing a sample of the Risk Dashboard reports also in

compliancewithCOSOAT/Exhibit6.5andCOSOERMIntegratedFrameworkSection6,where

entity‐wideportfolioandbusinessunit,department,andfunctionalareas’grossandresidualrisks

arecomputedandcomparedagainsteachother.

Figure25(16.49)showsthePEATDCFmodule’sefficientfrontiermodel,consistentwithCOSO

AT/Exhibit3.7requiringananalysisofthecapitalinvestmentinrelationtothereturnswithina

diversified(optimized)portfolio.

Figure26(16.50)showsthePEATERMandDCFmodules’simulatedresults,whereValueatRisk,

percentiles,andstatisticalprobabilitiescanbeobtained,incompliancewithCOSOAT/Exhibit5.5

requiringarangeofoutcomesbasedondistributionalassumptions,andCOSOERMIntegrated

Framework Exhibit 5.2 requiring historical or simulated outcomes of future behaviors under

probabilisticmodels.

Figure 27 (16.51) shows compliancewith COSOAT/Exhibit 3.1 requiring the use of scenario

modelingandstresstesting.

Figure28(16.52)showstheCMOLmoduleinPEATwherescenarioanalysis,stresstesting,and

gap analysis are performed, in compliance with COSO AT/Exhibit 5.10, to complement

probabilisticmodels.

Figure29(16.53)showscompliancewithCOSOAT/Exhibits5.8&5.9requiringthemodelingof

operational and credit loss distributionswith back‐testing or historical simulation, sensitivity

analysis,andValueatRiskcalculations.

25 | P a g e

FIGURE21 PEATERMandCOSOIntegratedFramework.

26 | P a g e

FIGURE22 PEATERMheatmapandriskmatrix.

27 | P a g e

FIGURE23 PEATERMportfolioandcorporatevieworresidualrisk.

28 | P a g e

FIGURE24 PEATERMportfolio,businessunit,department,functionview

29 | P a g e

FIGURE25 PEATDCFmodulefeaturingcapitalversusreturnsefficientfrontier

30 | P a g e

FIGURE26 PEATERM&DCFmoduleswithrisksimulationresultswithValueatRisk

31 | P a g e

FIGURE27 PEATERM&DCFmoduleswithscenarioanalysisandheatmapregions

32 | P a g e

FIGURE28 CMOLmodulewithscenarioanalysisandstresstesting

33 | P a g e

FIGURE29 CMOLmodulewithhistoricalsimulation(back‐testing)andValueatRisk