completing the accounting cycle

DESCRIPTION

4. Completing the Accounting Cycle. Principles of Financial Accounting, 11e Reeve • Warren • Duchac. After studying this chapter, you should be able to:. 4. Describe the accounting cycle. - PowerPoint PPT PresentationTRANSCRIPT

1

4

Completing the Accounting Cycle

Principles of Financial Accounting, 11eReeve • Warren • Duchac

2

After studying this chapter, you should be able to:

Completing the Accounting Cycle

1 Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance and financial statements.

2 Prepare financial statements from adjusted account balances.

3 Prepare closing entries.

4-2

After studying this chapter, you should be able to:4 Describe the accounting cycle.

1-34-33

4-3

Completing the Accounting Cycle (continued)

5 Illustrate the accounting cycle for one period.

6 Explain what is meant by the fiscal year and the natural business year.

1-44-44

1

4-4

Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance and financial statements.

1-54-55

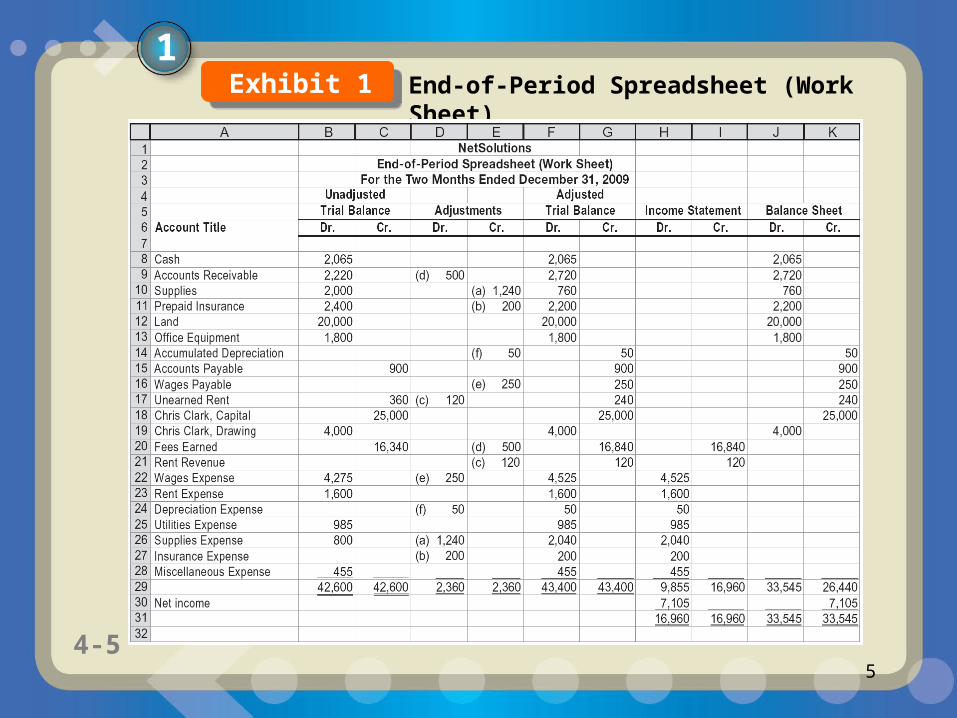

1End-of-Period Spreadsheet (Work Sheet)Exhibit 1

1-64-66

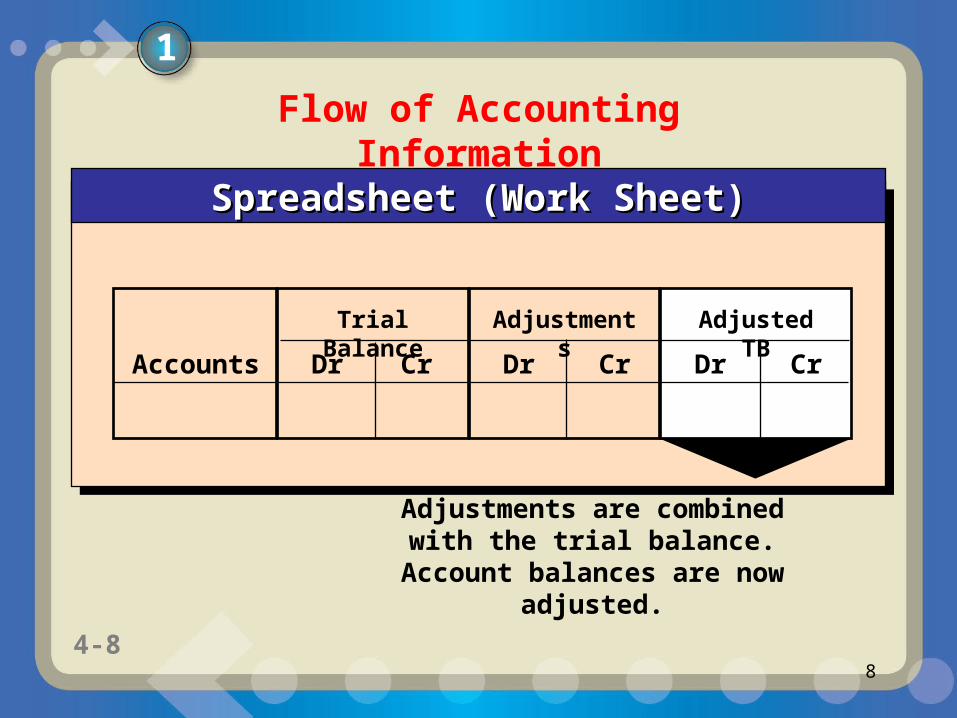

Spreadsheet (Work Sheet)Spreadsheet (Work Sheet)

Trial Balance

Accounts Dr Cr Dr Cr Dr Cr

Adjustments Adjusted TB

Accounts are listed in the Trial Balance column using the ending balance found in the general ledger.

Flow of Accounting Information

1

1-74-77

Flow of Accounting Information

Spreadsheet (Work Sheet)Spreadsheet (Work Sheet)

Trial Balance

Accounts Dr Cr Dr Cr Dr Cr

Adjustments Adjusted TB

Adjustments are entered here. Two possibilities:

1. Deferrals – Existing balances are changed.2. Accruals – New information is entered.

1

1-84-88

Adjustments are combined with the trial balance. Account

balances are now adjusted.

Trial Balance

Accounts Dr Cr Dr Cr Dr Cr

Adjustments Adjusted TB

Spreadsheet (Work Sheet)Spreadsheet (Work Sheet)

Flow of Accounting Information

1

1-94-99

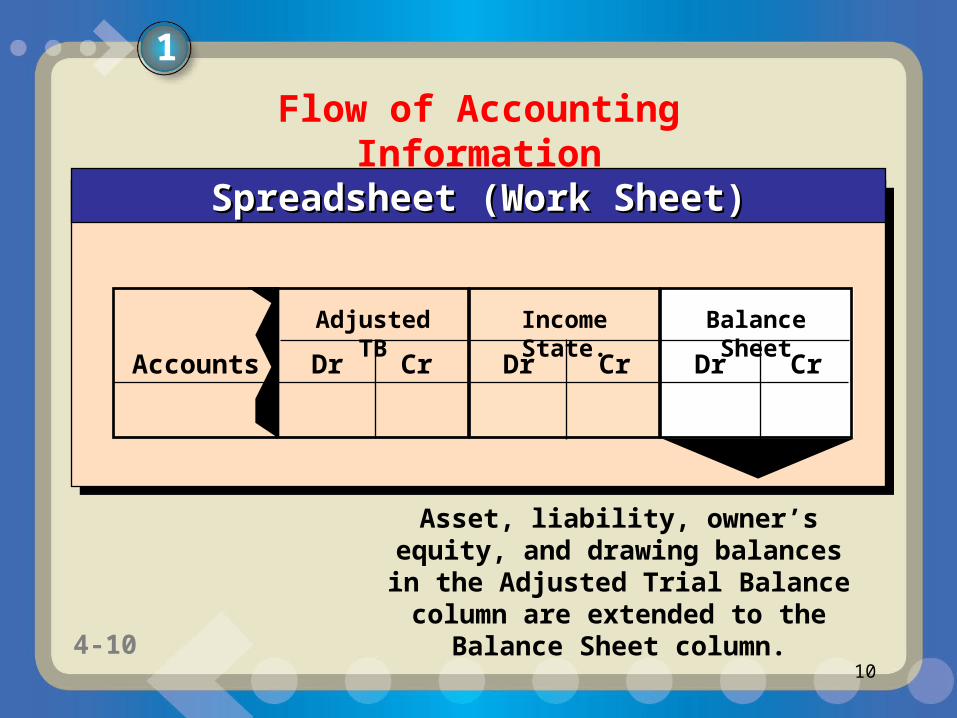

Revenue and expense balances in the Adjusted Trial Balance column are extended

to the Income Statement column.

Adjusted TB

Accounts Dr Cr Dr Cr Dr Cr

Income State. Balance Sheet

Spreadsheet (Work Sheet)Spreadsheet (Work Sheet)

Flow of Accounting Information

1

1-104-1010

Asset, liability, owner’s equity, and drawing balances in the Adjusted

Trial Balance column are extended to the Balance Sheet column.

Adjusted TB

Accounts Dr Cr Dr Cr Dr Cr

Income State. Balance Sheet

Spreadsheet (Work Sheet)Spreadsheet (Work Sheet)

Flow of Accounting Information

1

1-114-1111

The balances for the accounts listed below appear in the Adjusted Trial Balance columns of the end-of-period spreadsheet (work sheet). Indicate whether each balance should be extended to (a) an Income Statement column or (b) a Balance Sheet column.

1. Amber Bablock, Drawing2. Utilities Expense3. Accumulated

Depreciation—Equipment4. Unearned Rent

5. Fees Earned6. Accounts Payable7. Rent Revenue8. Supplies

4-11

Example Exercise 4-11

Flow of Accounts into Financial Statements

1-124-1212

1. Balance Sheet column2. Income Statement column3. Balance Sheet column4. Balance Sheet column5. Income Statement column6. Balance Sheet column7. Income Statement column8. Balance Sheet column

1Example Exercise 4-1 (continued)

4-12

For Practice: PE 4-1A, PE 4-1B

Follow My Example 4-1

1-134-1313

Prepare financial statements from adjusted account balances.

2

4-13

1-144-1414

The income statement is prepared directly from the Income Statement or Adjusted Trial Balance columns of the spreadsheet (work sheet).

2

1-154-1515

to statement of owner’s equity

2

Financial Statements Prepared from Work SheetExhibit 2

1-164-1616

In the Balance Sheet columns of the end-of-period spreadsheet (work sheet) for Dimple Consulting Co. for the current year, the Debit column total is $678,450, and the Credit column total is $599,750 before the amount of net income or net loss has been included. In preparing the income statement from the end-of-period spreadsheet (work sheet), what is the amount of net income or net loss?

4-16

Example Exercise 4-22

Determining the Net Income from End-of-Period Spreadsheet

1-174-1717

2Example Exercise 4-2 (continued)

A net income of $78,700 ($678,450 – $599,750) would be reported. When the Debit column of the Balance Sheet columns is more than the Credit column, net income is reported. If the Credit column exceeds the Debit column, a net loss is reported.

4-17

For Practice: PE 4-2A, PE 4-2B

Follow My Example 4-2

1-184-1818

The first item presented on the statement of owner’s equity is the balance of the owner’s capital account at the beginning of the period.

2

1-194-1919

from the income statement

to the balance sheet

2Financial Statements Prepared from Work Sheet (continued)

Exhibit 2

1-204-2020

Zack Gaddis owns and operates Gaddis Employment Services. On January 1, 2009, Zack Gaddis, Capital had a balance of $186,000. During the year, Zack invested an additional $40,000 and withdrew $25,000. For the year ended December 31, 2007, Gaddis Employment Services reported a net income of $18,750. Prepare a statement of owner’s equity for the year ended December 31, 2009.

Example Exercise 4-32

4-20

Statement of Owner’s Equity

1-214-2121

2Example Exercise 4-3 (continued)

Zack Gaddis, capital, January 1, 2009 $186,000Additional investment during 2009 40,000 Total $226,000Withdrawals $ 25,000Less net income 18,750Decrease in owner’s equity 6,250Zack Gaddis, capital, December 31, 2009 $219,750

4-21

For Practice: PE 4-3A, PE 4-3B

GADDIS EMPLOYMENT SERVICESSTATEMENT OF OWNER’S EQUITY

For the Year Ended December 31, 2009

Follow My Example 4-3

1-224-2222

The balance sheet is prepared directly from the Balance Sheet or Adjusted Trial Balance columns of the spreadsheet (or worksheet).

2

1-234-2323

A classified balance sheet is a balance sheet that was expanded by adding subsections for current assets; property, plant, and equipment; and current liabilities.

2

1-244-2424

Cash and other assets that are expected to be converted into cash, sold or used up usually within a year or less, through the normal operations of the business, are called current assets.• Cash

• Accounts Receivable

• Supplies

2

1-254-2525

Notes receivable are written promises by the customer to pay the amount of the note and possibly interest at an agreed rate.

2

1-264-2626

Property, plant, and equipment (also called fixed assets) include assets that depreciate over a period of time. Land is an exception as it is not subject to depreciation.• Equipment

• Machinery

• Buildings

• Land

2

1-274-2727

Liabilities that will be due within a short time (usually one year or less) and that are to be paid out of current assets are called current liabilities.• Accounts payable

• Wages payable

• Interest payable

• Unearned fees

2

1-284-2828

Liabilities not due for a long time (usually more than one year) are long-term liabilities. • Notes payable

• Mortgage payable

• Bond payable

2

1-294-2929

Owner’s equity is the owner’s right to the assets of the business. Owner’s equity is added to the total liabilities, and the total must be equal to the total assets.

2

1-304-3030

from the statement of owner’s equity

2Financial Statements Prepared from Work Sheet (continued)Exhibit 2

1-314-3131

The following accounts appear in the adjusted trial balance of Hindsight Consulting. Indicate whether each account would be reported in the (a) current asset; (b) property, plant, and equipment; (c) current liability, (d) long-term liability; or (e) owner’s equity section of the December 31, 2009 balance sheet of Hindsight Consulting.

1. Jason Corbin, Capital 5. Cash2. Notes Receivable (due 6. Unearned Rent

in 6 months) 7. Accumulated Depr.—

3. Notes Payable (due in Equipment2011) 8. Accounts Payable

4. Land

Example Exercise 4-42

4-31

Classified Balance Sheet

1-324-3232

2Example Exercise 4-4 (continued)

Follow My Example 4-4

1. Stockholders’ equity2. Current asset3. Long-term liability4. Property, plant, and

equipment

5. Current asset6. Current liability7. Property, plant, and

equipment

8. Current liability

4-32

For Practice: PE 4-4A, PE 4-4B

Follow My Example 4-4

1-334-3333

Prepare closing entries.

3

4-334-33

1-344-3434

Accounts that are relatively permanent from year to year are called real accounts. Accounts that report amounts for only one period are called temporary accounts or nominal accounts.

3

Closing Entries

1-354-3535

To report amounts for only one period, temporary accounts should have zero balances at the beginning of the period. At the end of the period the revenue and expense account balances are transferred to Income Summary.

3

Closing Entries

1-364-3636

The balance of Income Summary is then transferred to the owner’s capital account. The balance of the owner’s drawing account is also transferred to the owner’s capital account. The entries that transfer these balances are called closing entries.

3

Closing Entries

1-374-3737

3

The Closing ProcessExhibit 3

1-384-3838

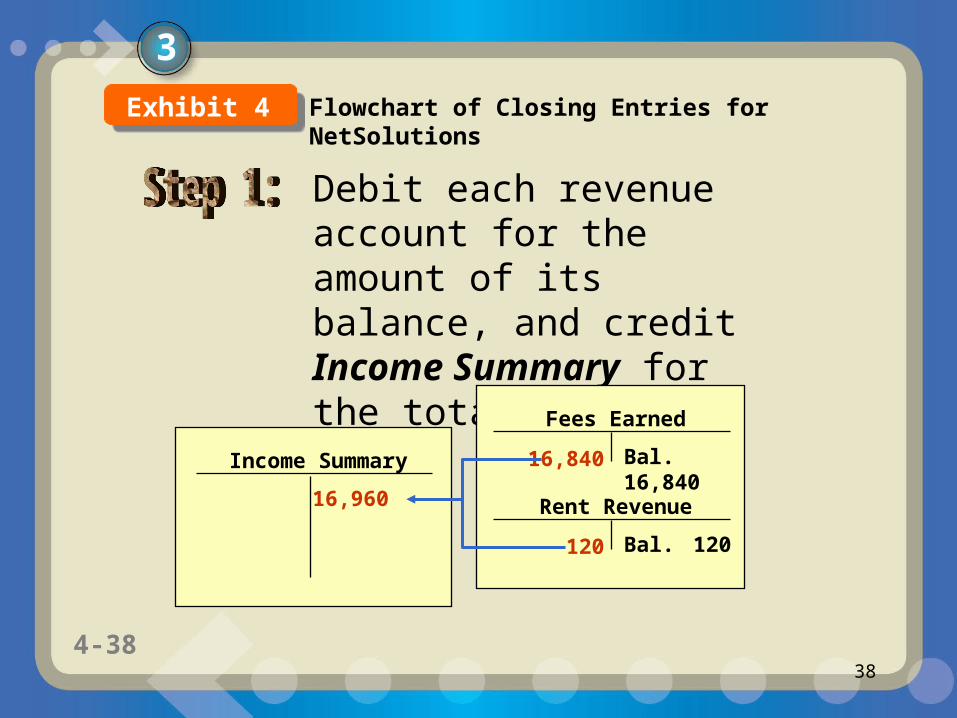

Debit each revenue account for the amount of its balance, and credit Income Summary for the total revenue.

Fees Earned

Bal. 16,840

Rent Revenue

Bal. 120

Income Summary 16,840

120

16,960

3

Flowchart of Closing Entries for NetSolutions Exhibit 4

1-394-3939

Wages Expense

Rent Expense

Depreciation Expense

Utilities Expense

Supplies Expense

Insurance Expense

Bal. 200

Miscellaneous Expense

Bal. 455

Income Summary

Debit Income Summary for the total expenses and

credit each expense account for its balance.

16,960

Bal. 4,525

Bal. 1,600

Bal. 50

Bal. 985

Bal. 2,040

9,855

455

200

2,040

985

50

1,600

4,525

3Flowchart of Closing Entries for NetSolutions (continued)Exhibit 4

1-404-4040

Chris Clark, Capital

Bal. 25,000

Chris Clark, Drawing

Bal. 4,000

Income Summary

16,9609,8557,105

7,105

Debit Income Summary for the

amount of its balance (in this case, the net

income) and credit the capital account.

3Flowchart of Closing Entries for NetSolutions (continued)

Exhibit 4

1-414-4141

Chris Clark, Capital

Bal. 25,0007,105

Chris Clark, Drawing

Bal. 4,000 4,000

4,000 Debit the capital account for the balance

of the drawing account, and credit

drawing for the same amount.

3

Flowchart of Closing Entries for NetSolutions (continued)

Exhibit 4

1-424-4242

3

Flowchart of Closing Entries for NetSolutions (summary)

Exhibit 4

1-434-4343

3

Closing Entries for NetSolutions

Step 2

Step 3

Step 1

Step 4

Exhibit 5

1-444-4444

After the closing entries are posted, all of the temporary accounts have zero balances.

3

1-454-4545

3Ledger for NetSolutionsExhibit 6

1-464-4646

Ledger for NetSolutions (continued)

3Exhibit 6

1-474-4747

3

Ledger for NetSolutions (continued)Exhibit 6

1-484-4848

3

Ledger for NetSolutions (continued)Exhibit 6

1-494-4949

After the accounts have been adjusted at July 31, the end of the fiscal year, the following balances are taken from the ledger of Cabriolet Services Co.

Terry Lambert, Capital

$615,850Terry Lambert, Drawing

25,000Fees Earned

380,450Wages Expense

250,000Rent Expense

65,000Supplies Expense

18,250Miscellaneous Expense

6,200

Journalize the four entries required to close the accounts.

Example Exercise 4-53

Closing Entries

4-49

1-504-5050

3Example Exercise 4-5 (continued)

July 31 Fees Earned…………………………….. 380,450Income Summary…………………. 380,450

31 Income Summary……………………… 339,450Wages Expense…………………… 250,000Rent Expense……………………… 65,000Supplies Expense………………… 18,250Miscellaneous Expense…………. 6,200

31 Income Summary………………………. 41,000Terry Lambert, Capital…………… 41,000

31 Terry Lambert, Capital………………… 25,000Terry Lambert, Drawing………….. 25,000

4-50

For Practice: PE 4-5A, PE 4-5B

Follow My Example 4-5

1-514-5151

A post-closing trial balance is prepared after the closing entries have been posted. The purpose of the PCTB is to verify that the ledger is in balance at the beginning of the next period.

3

1-524-5252

3

Post-Closing Trial BalanceExhibit 7

1-534-5353

Describe the accounting cycle.

4

4-53

1-544-5454

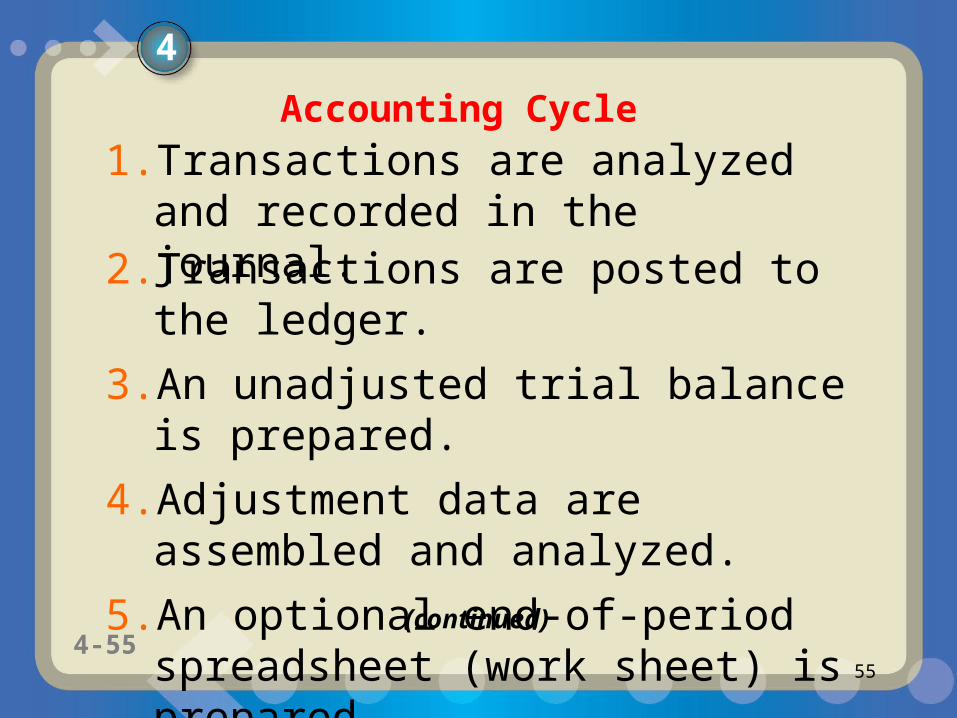

The accounting process that begins with analyzing and journalizing transactions and ends with preparing the accounting records for the next period’s transactions is called the accounting cycle. There are ten steps in the accounting cycle.

4

1-554-5555

2. Transactions are posted to the ledger.

3. An unadjusted trial balance is prepared.

4. Adjustment data are assembled and analyzed.

5. An optional end-of-period spreadsheet (work sheet) is prepared.

1. Transactions are analyzed and recorded in the journal.

(continued)

Accounting Cycle

4

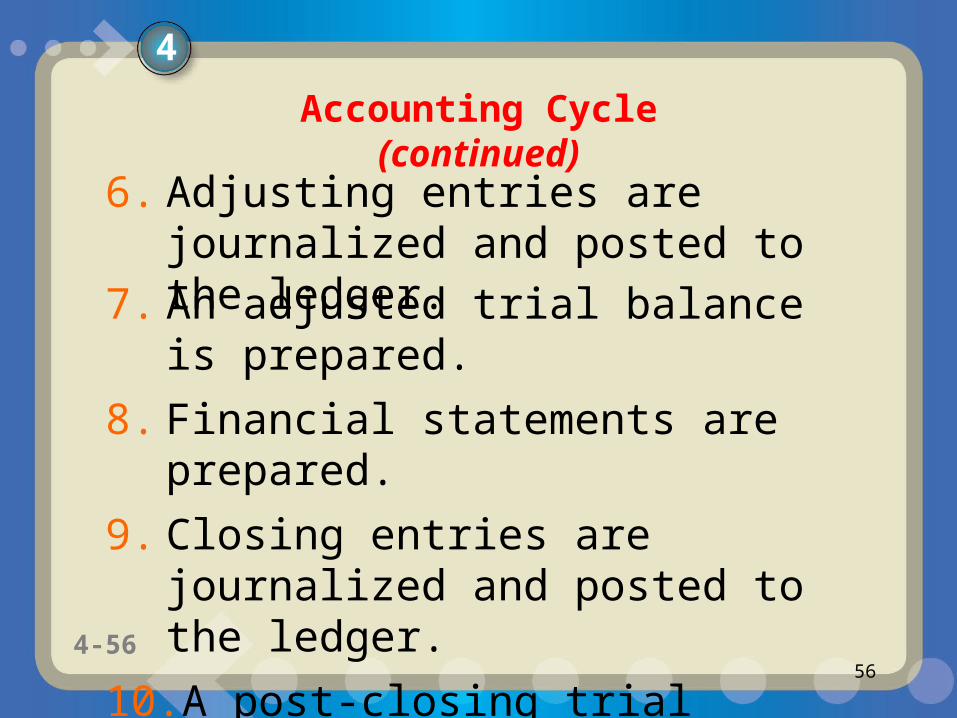

1-564-5656

7. An adjusted trial balance is prepared.

8. Financial statements are prepared.

9. Closing entries are journalized and posted to the ledger.

10. A post-closing trial balance is prepared.

6. Adjusting entries are journalized and posted to the ledger.

Accounting Cycle (continued)

4

1-574-5757

From the following list of steps in the accounting cycle, identify what two steps are missing.

a. Transactions are analyzed and recorded in the journal.b. Transactions are posted to the ledger.c. Adjustment data are assembled and analyzed.d. An optional end-of-period spreadsheet (work sheet) is

prepared.e. Adjusting entries are journalized and posted to the

ledger.f. Financial statements are prepared.g. Closing entries are journalized and posted to the ledger.h. A post-closing trial balance is prepared.

Example Exercise 4-64

4-57

Accounting Cycle

1-584-5858

The following two steps are missing: (1) the preparation of an unadjusted trial balance and (2) the preparation of the adjusted trial balance. The unadjusted trial balance should be prepared after step (b). The adjusted trial balance should be prepared after step (e).

4Example Exercise 4-6 (continued)

4-58

For Practice: PE 4-6A, PE 4-6B

Follow My Example 4-6

1-594-5959

5

Illustrate the accounting cycle for one period.

4-59

1-604-6060

5

Journal entries for April, Kelly Consulting

Exhibit 9

1-614-6161

5

Journal entries for April, Kelly Consulting (continued)

Exhibit 9

1-624-6262

5Unadjusted Trial Balance, Kelly ConsultingExhibit 10

1-634-6363

5

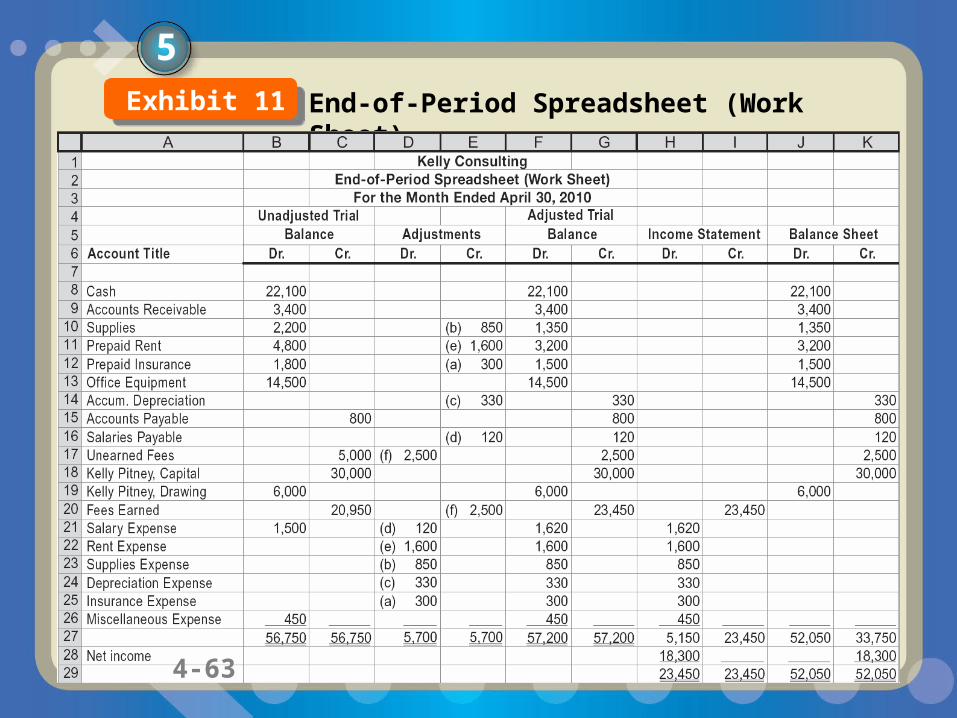

End-of-Period Spreadsheet (Work Sheet)Exhibit 11

4-63

1-644-6464

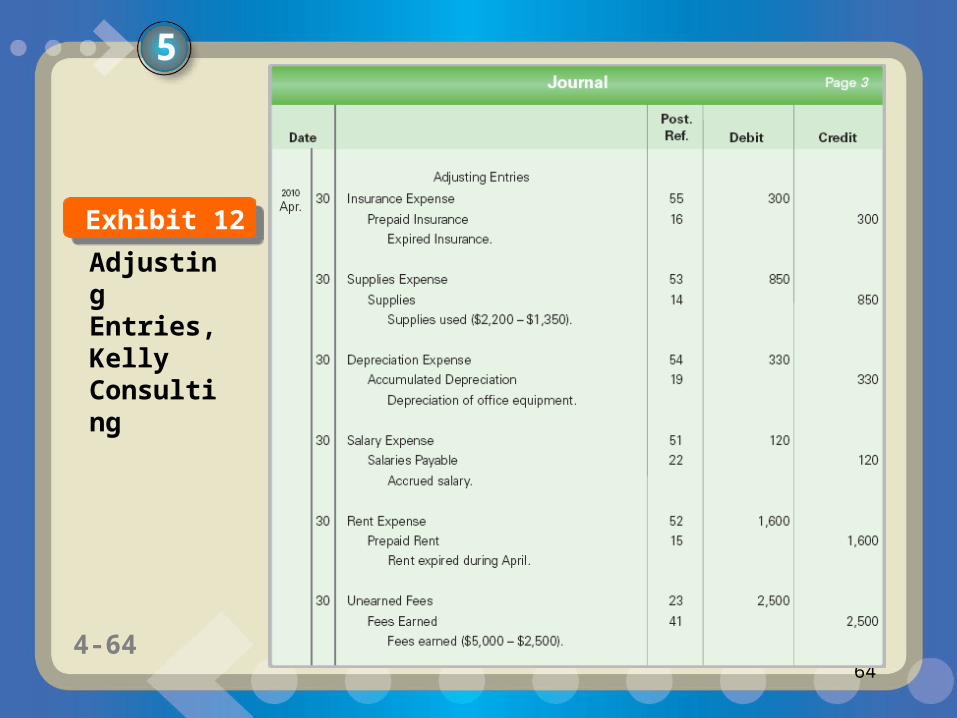

5

Adjusting Entries, Kelly Consulting

Exhibit 12

1-654-6565

5Adjusted Trial Balance, Kelly ConsultingExhibit 13

1-664-6666

5

Financial Statements, Kelly ConsultingExhibit 14

1-674-6767

5

Financial Statements, Kelly Consulting (continued)

Exhibit 14

1-684-6868

Financial Statements, Kelly Consulting (continued)

Exhibit 14

5

1-694-6969

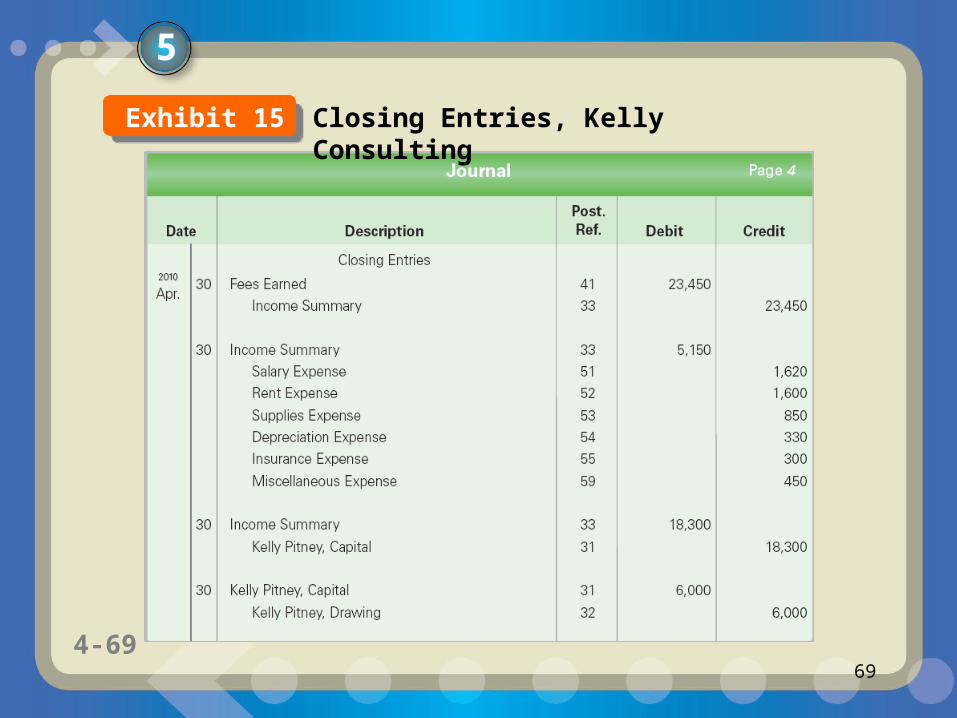

5

Closing Entries, Kelly ConsultingExhibit 15

1-704-7070

5

Post-Closing Trial Balance, Kelly ConsultingExhibit 16

1-714-7171

5

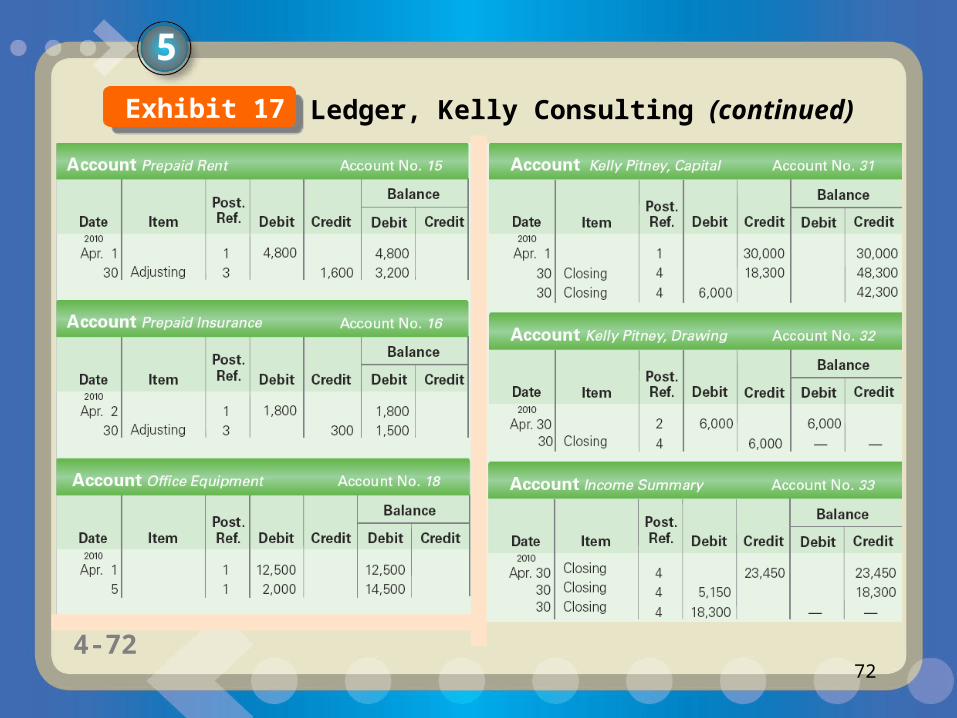

Ledger, Kelly ConsultingExhibit 17

1-724-7272

5

Ledger, Kelly Consulting (continued)Exhibit 17

1-734-7373

5

Ledger, Kelly Consulting (continued)Exhibit 17

1-744-7474

5

Ledger, Kelly Consulting (continued)Exhibit 17

1-754-7575

6

Explain what is meant by the fiscal year and the natural business year.

4-75

1-764-7676

The annual accounting period adopted by a business is known as its fiscal year. When a business adopts a fiscal year that ends when business activities have reached the lowest point in its annual operation, such a fiscal year is also called the natural year.

6

1-774-7777

Financial History of a Business

6

1-784-7878

Appendix 1: End-of-Period Spreadsheet (Work Sheet)

4-78

1-794-7979

Account Title Debit Credit Debit Credit Debit Credit

123456789

10111213141516171819202122232425

The The unadjusted unadjusted trial balance trial balance is checked is checked

for equalityfor equality..

Trial Balance Adjustments Trial Balance

Adjusted

Cash 2,065Accounts Receivable 2,220Supplies 2,000Prepaid Insurance 2,400Land 20,000Office Equipment 1,800Accumulated Depr.Accounts Payable 900Wages PayableUnearned Rent 360Chris Clark, Capital 25,000Chris Clark, Drawing 4,000Fees Earned 16,340Rent RevenueWages Expense 4,275Rent Expense 1,600Depreciation ExpenseUtilities Expense 985Supplies Expense 800Insurance ExpenseMiscellaneous Exp. 455

42,600 42,600

4-79

1-804-8080

Account Title Debit Credit Debit Credit Debit Credit

123456789

10111213141516171819202122232425

Trial Balance Adjustments Trial Balance

Adjusted

4-80

Supplies Supplies needs needs adjusting adjusting

Cash 2,065Accounts Receivable 2,220Supplies 2,000Prepaid Insurance 2,400Land 20,000Office Equipment 1,800Accumulated Depr.Accounts Payable 900Wages PayableUnearned Rent 360Chris Clark, Capital 25,000Chris Clark, Drawing 4,000Fees Earned 16,340Rent RevenueWages Expense 4,275Rent Expense 1,600Depreciation ExpenseUtilities Expense 985Supplies Expense 800Insurance ExpenseMiscellaneous Exp. 455

42,600 42,600

1-814-8181

Account Title Debit Credit Debit Credit Debit Credit

123456789

10111213141516171819202122232425

(a) 1,240

(a) 1,240

Trial Balance Adjustments Trial Balance

Adjusted

4-81

Cash 2,065Accounts Receivable 2,220Supplies 2,000Prepaid Insurance 2,400Land 20,000Office Equipment 1,800Accumulated Depr.Accounts Payable 900Wages PayableUnearned Rent 360Chris Clark, Capital 25,000Chris Clark, Drawing 4,000Fees Earned 16,340Rent RevenueWages Expense 4,275Rent Expense 1,600Depreciation ExpenseUtilities Expense 985Supplies Expense 800Insurance ExpenseMiscellaneous Exp. 455

42,600 42,600

(a) Cost of supplies on hand at December 31 is $760.

1-824-8282

Account Title Debit Credit Debit Credit Debit Credit

123456789

10111213141516171819202122232425

(b) 200

(b) 200

Trial Balance Adjustments Trial Balance

Adjusted

4-82

(a) 1,240

Cash 2,065Accounts Receivable 2,220Supplies 2,000Prepaid Insurance 2,400Land 20,000Office Equipment 1,800Accumulated Depr.Accounts Payable 900Wages PayableUnearned Rent 360Chris Clark, Capital 25,000Chris Clark, Drawing 4,000Fees Earned 16,340Rent RevenueWages Expense 4,275Rent Expense 1,600Depreciation ExpenseUtilities Expense 985Supplies Expense 800Insurance ExpenseMiscellaneous Exp. 455

42,600 42,600

(a) 1,240

(b) The insurance expense for December is $200 ($2,400 ÷ 12).

1-834-8383

Account Title Debit Credit Debit Credit Debit Credit

123456789

10111213141516171819202122232425

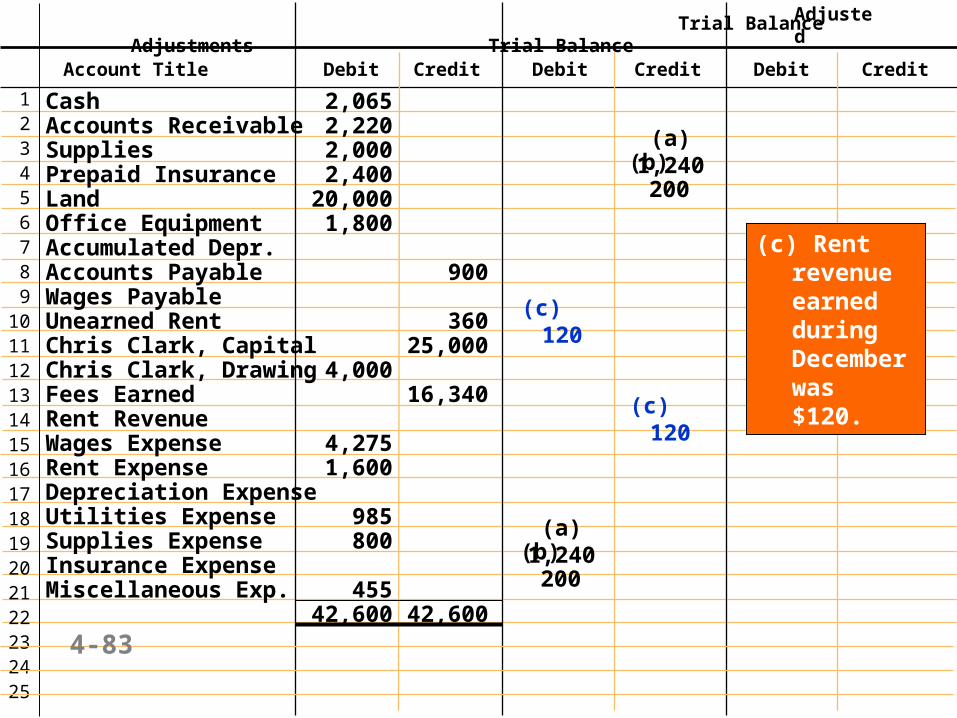

(c) 120

(c) 120

Trial Balance Adjustments Trial Balance

Adjusted

4-83

(b) 200(a) 1,240

(b) 200

Cash 2,065Accounts Receivable 2,220Supplies 2,000Prepaid Insurance 2,400Land 20,000Office Equipment 1,800Accumulated Depr.Accounts Payable 900Wages PayableUnearned Rent 360Chris Clark, Capital 25,000Chris Clark, Drawing 4,000Fees Earned 16,340Rent RevenueWages Expense 4,275Rent Expense 1,600Depreciation ExpenseUtilities Expense 985Supplies Expense 800Insurance ExpenseMiscellaneous Exp. 455

42,600 42,600

(a) 1,240

(c) Rent revenue earned during December was $120.

1-844-8484

Account Title Debit Credit Debit Credit Debit Credit

123456789

10111213141516171819202122232425

Trial Balance Adjustments Trial Balance

Adjusted

4-84

(b) 200(a) 1,240

(b) 200

(c) 120

(c) 120

(d) 500

(d) 500

Cash 2,065Accounts Receivable 2,220Supplies 2,000Prepaid Insurance 2,400Land 20,000Office Equipment 1,800Accumulated Depr.Accounts Payable 900Wages PayableUnearned Rent 360Chris Clark, Capital 25,000Chris Clark, Drawing 4,000Fees Earned 16,340Rent RevenueWages Expense 4,275Rent Expense 1,600Depreciation ExpenseUtilities Expense 985Supplies Expense 800Insurance ExpenseMiscellaneous Exp. 455

42,600 42,600

(a) 1,240

(d) Fees accrued at the end of December, but not recorded, totaled $500.

1-854-8585

Account Title Debit Credit Debit Credit Debit Credit

123456789

10111213141516171819202122232425

(e) 250

Trial Balance Adjustments Trial Balance

Adjusted

4-85

(b) 200(a) 1,240

(d) 500

(b) 200

(c) 120

(c) 120

Cash 2,065Accounts Receivable 2,220Supplies 2,000Prepaid Insurance 2,400Land 20,000Office Equipment 1,800Accumulated Depr.Accounts Payable 900Wages PayableUnearned Rent 360Chris Clark, Capital 25,000Chris Clark, Drawing 4,000Fees Earned 16,340Rent RevenueWages Expense 4,275Rent Expense 1,600Depreciation ExpenseUtilities Expense 985Supplies Expense 800Insurance ExpenseMiscellaneous Exp. 455

42,600 42,600

(d) 500

(e) 250

(a) 1,240

((e) Wages accrued but not paid at the end of December totaled $250.

1-864-8686

Account Title Debit Credit Debit Credit Debit Credit

123456789

10111213141516171819202122232425

Trial Balance Adjustments Trial Balance

Adjusted

4-86

(b) 200(a) 1,240

(d) 500

(c) 120

(c) 120(d) 500

(f) 50

(f) 50

(b) 200

Cash 2,065Accounts Receivable 2,220Supplies 2,000Prepaid Insurance 2,400Land 20,000Office Equipment 1,800Accumulated Depr.Accounts Payable 900Wages PayableUnearned Rent 360Chris Clark, Capital 25,000Chris Clark, Drawing 4,000Fees Earned 16,340Rent RevenueWages Expense 4,275Rent Expense 1,600Depreciation ExpenseUtilities Expense 985Supplies Expense 800Insurance ExpenseMiscellaneous Exp. 455

42,600 42,600

(e) 250

(a) 1,240

(e) 250

(f) Depreciation of office equipment is $50 for December.

1-874-8787

Account Title Debit Credit Debit Credit Debit Credit

123456789

10111213141516171819202122232425

2,360 2,360

Trial Balance Adjustments Trial Balance

Adjusted

4-87

(b) 200(a) 1,240

(d) 500

(c) 120

(c) 120

(f) 50

(b) 200(a) 1,240

(e) 250

(e) 250

(d) 500

Cash 2,065Accounts Receivable 2,220Supplies 2,000Prepaid Insurance 2,400Land 20,000Office Equipment 1,800Accumulated Depr.Accounts Payable 900Wages PayableUnearned Rent 360Chris Clark, Capital 25,000Chris Clark, Drawing 4,000Fees Earned 16,340Rent RevenueWages Expense 4,275Rent Expense 1,600Depreciation ExpenseUtilities Expense 985Supplies Expense 800Insurance ExpenseMiscellaneous Exp. 455

42,600 42,600 Summed and ruled

(f) 50

1-884-8888

The next step is to add or subtract the adjustments from (to) the amounts found in the Unadjusted Trial Balance columns and enter the results in the Adjusted Trial Balance columns.

1-894-8989

Account Title Debit Credit Debit Credit Debit Credit

Trial Balance Adjustments Trial Balance

123456789

10111213141516171819202122232425

Adjusted

4-892,360 2,360

(b) 200(a) 1,240

(d) 500

(c) 120

(c) 120(d) 500

(f) 50

(b) 200(a) 1,240

(e) 250

Cash 2,065 2,065Accounts Receivable 2,220 2,720Supplies 2,000 760Prepaid Insurance 2,400 2,200Land 20,000 20,000Office Equipment 1,800 1,800Accumulated Depr. 50Accounts Payable 900 900Wages Payable 250Unearned Rent 360 240Chris Clark, Capital 25,000 25,000Chris Clark, Drawing 4,000 4,000Fees Earned 16,340 16,840Rent Revenue 120Wages Expense 4,275 4,525Rent Expense 1,600 1,600Depreciation Expense 50Utilities Expense 985 985Supplies Expense 800 2,040Insurance Expense 200Miscellaneous Exp. 455 455

42,600 42,600 43,400 43,400

(f) 50

1-904-9090

Because of space constraints, the Unadjusted Trial Balance and the Adjustments columns will not be shown in the following slides.

1-914-9191

The next step is to extend amounts in the Adjusted Trial Balance columns to the Income Statement and Balance Sheet columns.

1-924-9292

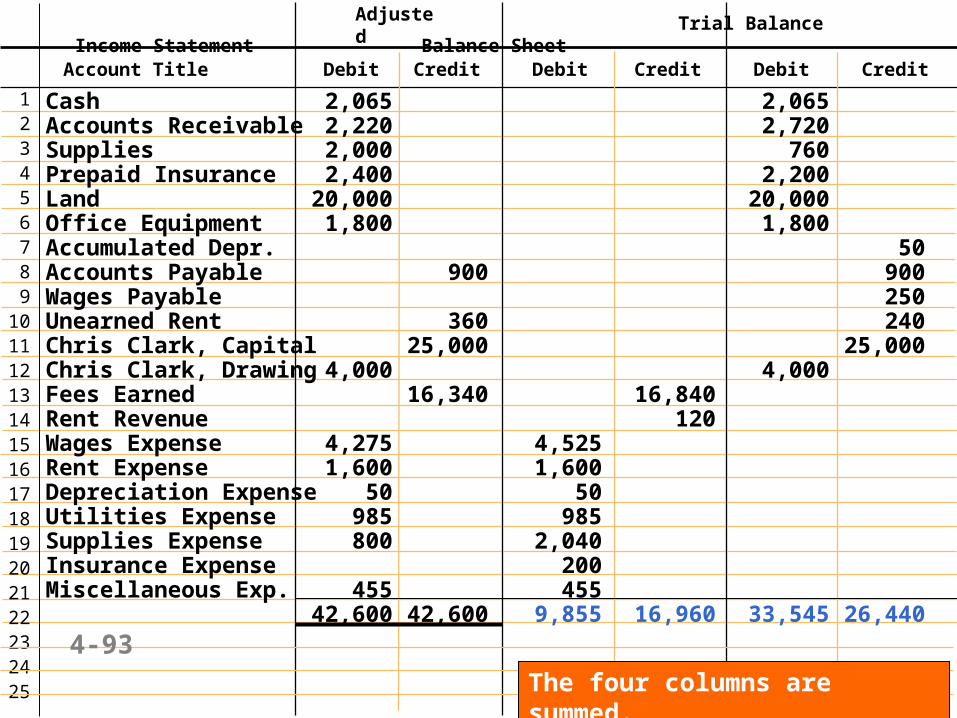

Account Title Debit Credit Debit Credit Debit Credit

Trial Balance Income Statement Balance Sheet

123456789

10111213141516171819202122232425

Adjusted

4-92

Cash 2,065 2,065Accounts Receivable 2,220 2,720Supplies 2,000 760Prepaid Insurance 2,400 2,200Land 20,000 20,000Office Equipment 1,800 1,800Accumulated Depr. 50Accounts Payable 900 900Wages Payable 250Unearned Rent 360 240Chris Clark, Capital 25,000 25,000Chris Clark, Drawing 4,000 4,000Fees Earned 16,340 16,840Rent Revenue 120Wages Expense 4,275 4,525Rent Expense 1,600 1,600Depreciation Expense 50 50Utilities Expense 985 985Supplies Expense 800 2,040Insurance Expense 200Miscellaneous Exp. 455 455

42,600 42,600

1-934-9393

Account Title Debit Credit Debit Credit Debit Credit

Trial Balance Income Statement Balance Sheet

123456789

10111213141516171819202122232425

Adjusted

The four columns are summed.

4-93

Cash 2,065 2,065Accounts Receivable 2,220 2,720Supplies 2,000 760Prepaid Insurance 2,400 2,200Land 20,000 20,000Office Equipment 1,800 1,800Accumulated Depr. 50Accounts Payable 900 900Wages Payable 250Unearned Rent 360 240Chris Clark, Capital 25,000 25,000Chris Clark, Drawing 4,000 4,000Fees Earned 16,340 16,840Rent Revenue 120Wages Expense 4,275 4,525Rent Expense 1,600 1,600Depreciation Expense 50 50Utilities Expense 985 985Supplies Expense 800 2,040Insurance Expense 200Miscellaneous Exp. 455 455

42,600 42,600 9,855 16,960 33,545 26,440

1-944-9494

9,855 16,960 33,545 26,4407,105 7,105

16,960 16,960 33,545 33,545

Income Statement Balance Sheet

Net IncomeNet Income

The difference between the Income Statement columns totals is the net income (or net loss) for the period.

1-954-9595

Account Title Debit Credit Debit Credit Debit Credit

Trial Balance Income Statement Balance Sheet

123456789

10111213141516171819202122232425

Adjusted

Cash 2,065 2,065Accounts Receivable 2,220 2,720Supplies 2,000 760Prepaid Insurance 2,400 2,200Land 20,000 20,000Office Equipment 1,800 1,800Accumulated Depr. 50Accounts Payable 900 900Wages Payable 250Unearned Rent 360 240Chris Clark, Capital 25,000 25,000Chris Clark, Drawing 4,000 4,000Fees Earned 16,340 16,840Rent Revenue 120Wages Expense 4,275 4,525Rent Expense 1,600 1,600Depreciation Expense 50 50Utilities Expense 985 985Supplies Expense 800 2,040Insurance Expense 200Miscellaneous Exp. 455 455

42,600 42,600 9,855 16,960 33,545 26,440Net income 7,105 7,105

16,960 16,960 33,545 33,5454-95