complete guide and checklist of purchasing a subsale ... · purchasing a subsale residential...

TRANSCRIPT

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

K C L a u & S u r i n t a A b r a h a m

E m a i l : s u p p o r t @ k c l a u . c o m

Produced by KCLau.com

Personal Finance Money Tips for Malaysians

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

CONTENTS

Complete Guide of PURCHASING A RESIDENTIAL SUBSALE PROPERTY IN MALAYSIA (APARTMENT/CONDO) FOR

YOUR OWN STAY ........................................................................................................................................................... 3

Preliminary questions to ask yourself:....................................................................................................................... 3

What are your key questions in determining what the right property for you is? ................................................ 3

The Property search: ................................................................................................................................................. 3

Things to do while you are property hunting ............................................................................................................ 3

Making the offer ........................................................................................................................................................ 3

Once you’ve made the offer and it has been accepted, next steps: ......................................................................... 4

Payment of earnest deposit fee & signing of booking form, with agent ............................................................... 4

Appointing lawyers ................................................................................................................................................ 5

Applying for Mortgage ........................................................................................................................................... 5

Determination of inventory list – what does the Vendor leave and what does he take? ..................................... 5

Signing of SPA (Sales and Purchase Agreement) ....................................................................................................... 5

Valuation Report .................................................................................................................................................... 6

Opening your home loan account ......................................................................................................................... 6

EPF withdrawal ...................................................................................................................................................... 6

Loan Agreement ........................................................................................................................................................ 7

Insurance on the property ......................................................................................................................................... 7

Partial disbursement & Full disbursement ................................................................................................................ 7

Vacant possession...................................................................................................................................................... 8

APPENDIX A: SAMPLE PROPERTY VIEWING CHECKLIST ............................................................................................... 10

APPENDIX A1: LIST OF DOCUMENTS FOR STANDARD LOAN APPLICATION : .............................................................. 13

APPENDIX B: SUMMARY OF ASKING/TRANSACTED PRICES : ....................................................................................... 14

APPENDIX C: SAMPLE INVENTORY LIST ....................................................................................................................... 15

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

APPENDIX D: GUIDE TO PARTIES INVOLVED IN THE TRANSACTION ............................................................................ 16

APPENDIX E: Sample Legal Fees .................................................................................................................................. 17

APPENDIX F : AGREED APPORTIONMENTS .................................................................................................................. 18

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

COMPLETE GUIDE OF PURCHASING A RESIDENTIAL SUBSALE PROPERTY IN MALAYSIA

(APARTMENT/CONDO) FOR YOUR OWN STAY

PRELIMINARY QUESTIONS TO ASK YOURSELF:

WHAT ARE YOUR KEY QUESTIONS IN DETERMINING WHAT THE RIGHT PROPERTY FOR YOU

IS?

- Location

- Size

- Facilities

- Age

- Tenure

- Proximity and access to work

- proximity and access to schools

- amenities including shopping, leisure, religious facilities, parks

- safety

- prestige

THE PROPERTY SEARCH:

- Star newspaper, Saturday edition

- Iproperty.com.my

- Propwall.my

- Mudah.my

1. Identify potential properties

2. Call up the agents/owners

3. Fix viewing appointments

Take a checklist with you when viewing properties. See Appendix A for a sample checklist.

THINGS TO DO WHILE YOU ARE PROPERTY HUNTING

- pre-qualification of loan - meet up with the bank and develop a relationship with an officer to assist with

pre qualification.

- Documents you will need at this stage will include those described in Appendix A1.

MAKING THE OFFER

- Once you’ve found the right ONE(s), you got to make the offer to purchase

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

- Do further research. Agents will often intimate that they have a large number of buyers “about” to make

an offer in order to bump up the price.

- Create a summary of units sold and last transacted prices in the last 1 year to get a better idea of the real

market price. You can do this by researching on the various websites. Look for other listed properties and

call up the agents to find out if the unit is still available. If it has been sold, ask for the transacted price.

Most likely the agents will tell you, if you call them up. See Appendix B for a template for creating a

summary of last transacted prices.

- Get your bank to do a valuation and assessment for loan. Be very careful here as a lot of Vendors simply

price their properties at prices far in advance of the actual valuation offered by Banks. Be wary of agents

who tell you that they “can get their valuer who is a personal friend, to give you a higher price if you use x

and y bank”. Don’t be fooled – if 3 independent banks give you the same valuation, and only the agent’s

“friend” is willing to go much higher, this only means that someone along the way is taking a kickback.

Such practices are unethical and in breach of the professional rules that govern registered valuers. So

even if the “friend” is able to come through with a higher valuation and justify a higher margin of

financing, the Purchaser is left to bear the risk that during a future sale, the valuation may not be as high;

or, at the point of an auction for default, the actual price of the property will be much lower based on

independent valuation. The ultimate loser here is the Purchaser (while the agent would have already

collected his fee).

- Plan your budget. It should include:

o Down payment: the proportion of the purchase price not covered by financing (banks will

typically lend 80-90% of the purchase price)

o Legal fees:

1% for the first RM100,000,

0.5% for the next RM4,900,000

o Property stamp duty:

1% for the first RM100,000,

2% for the next RM400,000

3% for the next RM500,000 – RM2million

4% above RM2million

o Loan agreement stamp duty: 0.5% of loan amount transfer

o Disbursement fees include fees for registration of charge, land search and bankruptcy search

(RM300–700 in Wilayah Persekutuan and Selangor)

o Processing fee: one-time fee charged by the financial institution for loan processing (RM50-1,000)

ONCE YOU’VE MADE THE OFFER AND IT HAS BEEN ACCEPTED, NEXT STEPS:

PAYMENT OF EARNEST DEPOSIT FEE & SIGNING OF BOOKING FORM, WITH AGENT

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

Earnest deposit is normally 1-2% of the agreed property price. Agent will have a standard template booking form

to facilitate the transaction.

APPOINTING LAWYERS

Appoint a firm of solicitors to act for you as the Purchaser. As part of the instruction, forward the firm a list of

parties involved in the transaction. See Appendix D for a sample list of parties involved in the transaction.

APPLYING FOR MORTGAGE

Loan letter of offer will be issued by the bank. It will contain the salient terms of your loan. A list of such terms

would include:

- Type of loan

- Amount of loan

- Purpose of loan

- Description of property

- Duration

- Processing /Set up Fee

- Monthly service charge

- Prevailing interest and Repayment

- Instalments

- Security Documents

- Interest rate on excess

- Prepayments

- GMTA – Group Mortgage Term Assurance or MRTA – Mortgage Reducing Term Assurance (if any)

- Conditions precedent to drawdown

DETERMINATION OF INVENTORY LIST – WHAT DOES THE VENDOR LEAVE AND WHAT DOES

HE TAKE?

- Do a recci (fact finding visit) of the property and note down what items you want the Vendor to remove

and what items you would like the Vendor to leave.

- Once agreed, this list becomes the agreed inventory list – a list of items that you will expect to find when

you take over vacant possession. This document also forms part of the SPA.

- See Appendix C for a sample inventory list

SIGNING OF SPA (SALES AND PURCHASE AGREEMENT)

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

- The signing of the SPA can take place separately ie. you sign and forward to your solicitor, and they will

forward to the vendor’s solicitor who will arrange for the vendor to sign and return to your solicitor. Your

solicitor then forwards to the Bank. You will need to issue the cheque for :

o The RPGT sum (2%) of the purchase price; and

o 8% being the remainder of the earnest deposit (10% - 2% already paid in the form of a booking

fee).

- *Make sure that the premises are correctly described in the SPA – ensure that any additional parcel

forming a car park that comes with the unit, is included in the description under the SPA.

- You may wish to arrange for all parties to sign at the same time. This is because after you have signed and

issued the cheques, you will want to go to EPF to get your reimbursement from Account 2 as soon as

possible. However, the signed and stamped SPA is needed before you can do this. As such, if you sign the

SPA separately, you could have a situation where the Vendor takes his own sweet time to sign and you

cannot go to EPF for your reimbursement – and yet, the money has already been debited from your

account. (It will be placed in a clients/stakeholder account with the Vendor’s solicitors – but still, the

money would have been debited from your account). Don’t be caught in this situation, make sure the

Vendor signs the SPA at the same time as you.

- Prepare to pay the solicitor’s bill. A typical bill at this stage will look as set out in Appendix E.

VALUATION REPORT

The Bank will send a representative from its selected firm of property valuers, to take photographs of

your apartment and prepare a valuation report.

The cost of the valuation report

OPENING YOUR HOME LOAN ACCOUNT

A separate account in which funds to service your loan and interest payments needs to be opened with

the bank granting you your loan. Your loan officer should sort this out for you. Choose a branch nearest

to your place of work to facilitate easy sorting out of administrative matters.

EPF WITHDRAWAL

Friends and family may tell you that this is a relatively straightforward process and that you can expect to

withdraw your money easily and without hassle.

Be warned – this may not necessarily be the case.

As a general rule, purchasers of property located in Selangor are advised to visit the PJ EPF branch, while

purchasers of property located in Wilayah Persekutuan are advised to go to the KL EPF branch. Trying to

process the paperwork for a KL-based property at the PJ branch can result in complications and confusion

over the type of forms from the Land Office which are required for the submission.

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

A list of documents required by EPF is set out on their website at www.kwsp.gov.my. The relevant forms

to be filled in prior to submission can also be downloaded from the website.

Be prepared however – sometimes, the EPF officers will ask for additional documents. It’s best to take all

documents that you have, with you just in case.

LOAN AGREEMENT

The bank will send their standard loan agreement and charge document to your solicitors (If your solicitors are also

on the bank’s panel, they will prepare the documents according to the Bank’s approved template.

There are lots of onerous terms, one-sided clauses etc. Unfortunately, the bank will not entertain any attempt by you

or your solicitor to amend the clauses.

INSURANCE ON THE PROPERTY

What often happens is the bank will send an automatically-generated notice requesting a copy of the

existing fire insurance policy for the property within 2 weeks of date of the letter failing which the bank

will take out a policy on the property without further notice.

The problem here is that for condos purchased on the sub-sale market, there should be a master fire

insurance policy maintained by the building management office for the whole condominium already valid

and in force. If this is the case, there is no reason for the bank to take out another policy over the same

unit and bill you for it, as you will already be paying management fees – a component of which is for your

existing policy.

What to do : Immediately contact the bank – use the number in the letter – get the email address and

name of the officer who picks up the phone and instruct them via email NOT to take out any additional

policy first

Next, contact the building management office and ask for a copy of the front page of the existing fire

insurance policy to be faxed/emailed to you. This page should contain the details of the policy including

validity period, unit number and details of the current owner.

Once received, email a copy of this document to the bank officer and ask for instructions what to do next.

Ideally, you should leave the existing insurance policy as is until the transfer of title is updated to reflect

your name as the new owner, after which you should notify the building management and get them to

update the policy accordingly.

Meanwhile, the bank should not be allowed to take out another insurance policy over the unit and bill you

extra.

PARTIAL DISBURSEMENT & FULL DISBURSEMENT

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

The bank will issue a cheque for the partial drawdown – sufficient for the Vendor to discharge the

outstanding on any loan he/she may have taken out over the property. This cheque will be sent to your

solicitors and they will forward it to the Vendor’s solicitors.

The MRTA portion will also be disbursed (if you have obtained financing for this portion).

Once the Vendor has utilized the partial drawdown to procure the discharge of the charge (assuming he had

charged the property to a bank earlier), the bank will release the original strata title to the Vendor’s solicitor.

This will then be forwarded to the Land Office for the updating of details, etc.

The Vendor’s solicitor will send it to the Bank’s solicitor (which could also be your solicitor as the

Purchaser).

The Bank’s solicitor will issue the advice to the Bank to proceed with full drawdown.

Once full drawdown has been issued by the Bank into the Vendor’s solicitor’s account, you will be notified.

From this point, the Vendor has a specified number of days within which to deliver vacant possession to

you, failing which you have the right to charge interest. The number of days is usually between 5 to 7 days

and is specified in the SPA.

VACANT POSSESSION

The next step is for the Vendor’s solicitor to release the Agreed Apportionments figure to your lawyer.

This is essentially, a list of all payments which the Vendor has already paid in part/full for items such as

management fee, sinking fund, water, etc.

You will need to reimburse the Vendor for the portion that he may have pre-paid, as he will not be

enjoying the use of the property from the date of vacant possession onward.

Conversely, there might be outstanding payments which are already due prior to the date of vacant

possession, which the Vendor should have paid. These amounts should be calculated as well and set off

against the total agreed apportionments figure outstanding.

See Appendix F for a sample agreed apportionment template.

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

This guide is provided to you absolutely FREE. You might have downloaded this or received it from friends who

forwarded to you (that means they care about you). We hope you enjoy this guide and make full use of it. If you

want to hear more from us, make sure you subscribe to my mailing list at http://KCLau.com

Wish you all the best!

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

APPENDIX A: SAMPLE PROPERTY VIEWING CHECKLIST

PROPERTY VIEWING RECORD

Date:

Name of Agent:

Contact No. of Agent:

Realtor firm:

INFO DETAIL

Name of apt/condo

Year of construction

Name of developer

Year CF issued

Year of issue of strata title

Has strata title been issued?

Tenure

Leasehold/Freehold

Density & Occupancy rate

Owner/tenant mix

Mostly owners?

Mostly tenants?

Breakdown of nationalities? [Local/foreign]

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

Facilities

Management Committee –

comments on performance

to date, any issues, etc

Unit No. (full address)

Currently occupied? If

not, how long unoccupied?

Square footage

Price per square foot

Asking price (sale)

Potential rental amount

Bank valuation

Monthly management fee

Sinking fund fee

Assessment fee

No. of rooms

No. of bathrooms

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

Renovations done (if any)

General comments on

condition of apartment &

assessment of extent of

renovations to be done

No. of covered carparks

If need to rent additional

covered/outdoor carpark,

available? How much per

month?

Apartment block built on

a slope ?

Any issues so far? Check for cracks along the outer structure or any signs of

problems

Are there any other

construction projects

coming up around the

area? What’s the long

term development plan for

the area?

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

APPENDIX A1: LIST OF DOCUMENTS FOR STANDARD LOAN APPLICATION :

DOCUMENT

Copy of IC

3 months payslips (fixed salary)

3 months bank statement showing crediting of

salary

Previous years’ income tax return with payment

receipt

Latest EPF statement

Liquidity backup, i.e.: Fixed Deposit, Saving/

Current Account

Other source of income such as rental income

substantiated by stamped tenancy agreement and

bank statement

Booking form

Application form

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

APPENDIX B: SUMMARY OF ASKING/TRANSACTED PRICES :

Name of Apartment/Condo : ………………………….

Period : …………… to …………….

DATE OF POSTING

(PROPWALL/IPROPERTY)

AGENT/

CONTACT

ASKING

PRICE

/PSF

SIZE TRANSACTED

PRICE

DATE OF

TRANSACTION

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

APPENDIX C: SAMPLE INVENTORY LIST

UNIT :

NO. OF UNITS LOCATION ITEM TO BE

REMOVED BY

VENDOR?

[Y/N]

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

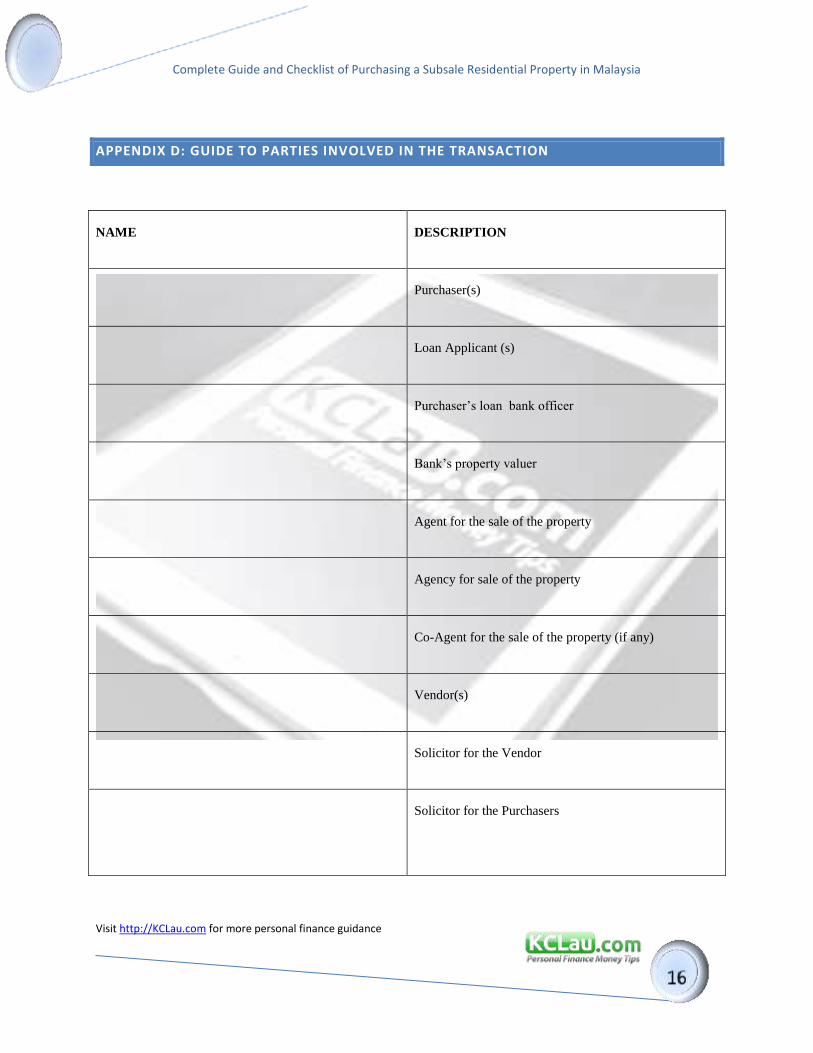

APPENDIX D: GUIDE TO PARTIES INVOLVED IN THE TRANSACTION

NAME DESCRIPTION

Purchaser(s)

Loan Applicant (s)

Purchaser’s loan bank officer

Bank’s property valuer

Agent for the sale of the property

Agency for sale of the property

Co-Agent for the sale of the property (if any)

Vendor(s)

Solicitor for the Vendor

Solicitor for the Purchasers

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

APPENDIX E: SAMPLE LEGAL FEES

Particulars

Legal Fees :

1. Sale and Purchase Agreement

2. Entry & withdrawal of private caveat

3. Submission of Borang CKHT 2A

6% government tax

Disbursements:

1. Stamp duty on the Sale and Purchase Agreement

2. Stamp duty on the transfer

3. Title search

4. Registration fee on the transfer

5. Registration fee on the entry and withdrawal of private caveat

6. Bankruptcy/winding up search

7. Affirmation fee on suratakuan

7. Transport charges

8. Telephone charges

TOTAL

Complete Guide and Checklist of Purchasing a Subsale Residential Property in Malaysia

Visit http://KCLau.com for more personal finance guidance

APPENDIX F : AGREED APPORTIONMENTS

ITEM SUM PAYABLE BY PURCHASER TO

VENDOR

SUM PAYABLE BY VENDOR TO

PURCHASER

Service Charges

Sinking fund

Assessment

Quit Rent

Fire Insurance

Water charges

Indah Water

Konsortium