competitivenss and comparative advantage s3. · pdf file1 02 03 4 0 200 400 600 800 1000 1200...

TRANSCRIPT

Competitiveness and comparative Advantage of Tomato in Syria

Basima Atiya [email protected]

Paper prepared for presentation at the I Mediterranean Conference of Agro-Food Social Scientists. 103rd EAAE Seminar ‘Adding Value to the Agro-Food Supply Chain in the Future Euromediterranean Space’. Barcelona, Spain, April 23rd - 25th, 2007 Copyright 2007 by [Basima Atiya]. All rights reserved. Readers may make verbatim copies of this document for non-commercial purposes by any means, provided that this copyright notice appears on all such copies.

Competitiveness and comparative Advantage of Tomato in Syria

By: Basima Atiya

NAPC

Abstract

The paper investigates Syrian tomato to asses the efficiency and sustainability in the use of domestic resources and tradable inputs, in order to identify new and more stable opportunities for Syrian exports.

In this study, the commodity system has been broken down into four representative systems: packed open field tomato exported to regional markets, packed greenhouse tomato exported to regional, packed greenhouse tomato exported to EU, and tomato paste.

Private and social profitabilities are assessed using the Policy Analysis Matrix (PAM).

All results indicate that the Syrian tomato has a comparative advantage for the four representative systems, both under the current policies and in the absence of government intervention. Moreover, the results indicate that the systems of fresh greenhouse packed tomato and tomato paste display negative transfers, meaning that these systems are taxed. Explicit taxes are applied mainly on the packaging materials, whereas implicit taxes are imposed by the high transaction costs and the presence of non-tariff barriers.

The sensitivity analysis indicates that fresh tomato and tomato paste enjoy comparative advantage under all prices and yields observed over the last decade, and parity prices of the main output and yield are the crucial parameters influencing the value of the DRC.

Finally, despite the implicit taxation of tomato sub-sector, it still has a strong comparative advantage, and this report stresses the importance of improving and diversifying Syrian tomato industry to cope with the evolving demands of international markets.

COMPETITIVENSS AND COMPARATIVE ADVANTAGE OF TOMATO IN SYRIA

2006

1. INTRODUCTION

1.1 Background of the Research

In 2005, the agricultural sector contributed to 24% of total GDP, in which the vegetable and

fruit sector increasingly plays a crucial role. During the last three decades, vegetable production

has significantly improved due to the expansion of cropped area and the intensification of

cropping practices. Therefore, it accounted for a good share of total plant production (10.8%).

Supplies of such crops have significantly increased responding to increasing consumption

caused by population growth1.

In 2004, the total cultivable area of vegetables accounted 170 thousand ha from which 11% was

under tomato. The total production of tomato increased from 409 to 965 thousand metric tons

(MT) during the period 1996-2004 with an annual growth rate of 10%. Moreover, it accounts for

about 30% of the value of the total vegetable production.

Indeed, this high growth rate has caused a saturation of the local demand leading to a significant

surplus of tomato products (Figure 1). New export market opportunities are emerging in the

region and beyond, which might contribute to income growth of the sector particularly rural

population. Furthermore, the domestic demand of processed food (such as tomato paste and

other processed tomato) is also likely to grow at a rapid pace as a result of population and

income growth. The changing patterns of consumption in urban areas (where female

employment is increasing and time for processing food at home is reduced), the increase in

consumption of fast food and food outside the households will most probably boost demand for

processed tomato. The agro-industry should, therefore, expand considerably to cope with the

growing demand.

1 Estimated at 2.45% per year.

3

Figure 1 Tomato production, import, export and total supply,local& total demand 1996-2004

0

200

400

600

800

1000

1200

1996

1997

1998

1999

20002001

20022003

2004

0

200

400

600

800

1000

1200

production import export

total supply local demand total demand

Production

In 2004, 98% of tomato output was produced using irrigation, while the rest (2%) was from

rainfed tomato fields. Irrigated tomato is grown in three seasons (summer, autumn, and spring)

to meet the high growing local demand for fresh and processed consumption. Besides, there is a

high demand of tomato from foreign markets, especially from the neighboring countries. Syrian

farmers have therefore strong incentives to grow tomato, in both irrigated and rainfed area.

Tomato harvest results from two types of production systems namely open field and greenhouse

tomatoes.

Field Tomatoes

Open field tomato is grown in different climates from June to October. It spreads out from the

Yarmok basin of Dara’a in the south, to Aleppo in the north. The total area under irrigated field

tomato accounted for 7.6% of the total irrigated vegetables. Farmers have recently been using

intensification and diversification strategies instead of expansion. Yields per hectare have grown

substantially, and the value of production per hectare rose from SP 158 thousand in 2000 to SP

4

221 thousand in 2004. The area under field tomatoes shares about 68% from total area of

tomato.

There are two major utilizations of field tomato; field tomato is either consumed fresh or

processed into tomato paste. Each product is retained in the study as a main final output.

Greenhouse tomatoes

Tomato is also grown in greenhouses adopting new irrigation technologies and high yielding

varieties. This production activity provides high returns to farmers. The growing local demand

for fresh tomato consumption and the high tomato demand from foreign markets, especially

from the neighboring countries (for early season tomato), caused a 15% increase in the total

number of greenhouses. As a result, the production increased by 72%, (from 1997-2004),

greenhouse tomato contributes by about 42% to total tomato production due to the high yield of

greenhouses. Greenhouse tomatoes is consumed as fresh and mainly exported as packed fresh

tomato.

Processing

Tomato is a delicate and a very perishable commodity and must be handled with care. For this

reason, it is packed in the same region of production. In addition, the increase in tomato

production necessitates improving its marketing and processing activities. Indeed, this

improvement will serve to get good fresh product suitable for ultimate consumption, to supply

good raw material for processing, to improve the quality of the final product, to minimize losses,

and to increase the income of all economic agents dealing with this product.

Figure 2 shows the main channels of tomato commodity system in Syria.

5

Figure 2 Tomato commodity chain, 2004

Open field 62% of total tomato

Green house 38% of total tomato

Wholesale market

Wholesale market

Middlemen

Exported packed fresh open field & tomato paste

3%

80%63%

100% 2%2%

Means out of chainNoteProcessors means both packed and tomato paste

Processors

35%

2%

Policy issues

Syria has been performing relatively well in exporting fruit and vegetables especially to the Arab

countries. Currently, Syrian Government interest is devoted to improve its export performance

to other countries; for example, EU, eastern and central Europe markets. To this end,

Government has removed all the taxes related to the agricultural production and the tax on

export profit2.

The Government supports local production of tomato (and other vegetables) by a favorable

trade policy through the Agricultural Calendar of the Great Arab Free Trade Area (GAFTA). In

1998, GAFTA agreement approved a gradual elimination of tariffs between 1998 and 2007. This

tariff elimination is to be applied by an annual tariff reduction of 10% until 2007, when all tariffs

should be eliminated. In the last two years, and before the full implementation of GAFTA, 20%

2Decree no. 15 dated 3/7/ 2001.

6

of tariff reduction has been applied. In fact, only in given periods during the year, tomato is

exempted from import tax, while outside such periods, tomato imports are subject to a tax of

29%. Noticeably, tomato paste imports are subject to a 102% tax3.

The Syrian-EU Partnership Agreement has allowed Syria to take significant shares of tomato

(about 15000 tons) to be exported to the EU and exempted from the custom duties. This is

expected to be applied as soon as the Agreement is signed.

1.2 Research Objective

The questions underlying the investigation are: 1) how competitive is tomato business, 2) what

impact does the Government intervention have on the competitiveness of tomato operations, 3)

does Syria have a comparative advantage in tomato (fresh and tomato paste), 4) to what extent

Syria still has comparative and competitive advantage in the regional and international markets.

Tomato commodity system has been broken down into representative systems on the basis of

the following criteria.

The type of the main output produced: Tomatoes are being processed into different final

outputs that don't have the same importance in the system such as packed fresh tomato and

tomato paste.

Farm level technology: Tomato can be produced through two different techniques at farm level

namely open field and greenhouse.

Targeted Market: Tomato is exported to Gulf and EU markets.

Therefore, this paper is focused on analyzing the comparative advantage for four systems:

packed open field tomato exported to regional market, packed greenhouse tomato exported to

regional market, packed greenhouse tomato exported to the EU, and tomato paste exported to

regional market.

3 Ministry of Finance - General Customs Department . Customs tariff spreadsheet by harmonies system.

7

2. Research methods

2.1 The Policy Analysis Matrix Approach

In this study, the PAM methodology is used to examine the economics of packed field tomato,

greenhouse tomato and tomato paste systems. PAM can also be used to investigate the entire

commodity system including farmer, processor and trader. Measures of profitability both social

and private and net transfers are the most important results of the PAM analysis. However, the

matrix format makes it possible to break down the end of results into the various components

including output transfers, tradable input transfers, and domestic resource transfers. These can

be presented in ratio forms such as the DRC, the PCR and the NPC.

2.2 Data collection

To obtain the estimates of private and social profitability, data of farmer, processor and exporter

budgets are needed. Both primary and secondary sources are used. The former are obtained

through interviews and structured questionnaires at farm level data gathered from the two

governorates mainly producing tomato: Dara’a for open field and Tartous for the greenhouse

tomatoes. Data on post-harvest operation concentrated in three governorates: Latakia, Tratous

and Damascus.

2.3 Budget

Three budgets have been constructed (farmer, processor and exporter). These budgets present

revenues, costs and profits. Costs are disaggregated into three main groups: fixed costs,

intermediate input costs, and direct labor costs. Also, budgets distinguish, within each cost

category, tradable goods and domestic resources (labor and capital).

8

2.4 Macro economic environment

The PAMs are computed in Syrian Pound (SP). Therefore, the exchange rate is an important

determinant of the value of tradable input on the world market because it has to be converted

into SP. No distortion is observed between the current and social exchange rate: Lebanon border

exchange rate is 51.5 SP/US$. Given the relative stability of this rate in the past years, it was

applied to estimate the private and the social value of the tradables. For the capital market, the

private rate of return is 5.5% representing the official interest rate offered by the Commercial

Bank of Syria, while the social one is 3% (equivalent to the weighted rate computed by the

International Monetary Fund).

For labor market, it is assumed that there is no distortion and the current wages correspond to

the real value of labor. A correction factor of 22.5 is applied to the value of skilled labor to take

account of the pension effect and health insurance fee on the value of this domestic factor. For

major tradables such as agricultural inputs, the latest uniform duty is used to compute the social

price after deduction of the taxes applied whenever imported. For composite good or services,

such as building or mechanized labor a weighted rate is computed using the standard budget

developed to compute the disaggregation coefficient. For energy, a comparison between the

current market price for fuel in Syria and that prevailing at the international market results in a

difference of 40% to the benefit of the Syrian operators. It means that there is a transfer of 40%

from the oil-producing sector to the other sectors of the economy.

2.5 Parity prices

Parity prices are calculated as FOBs. The FOB price at the Syrian border for packed fresh open

field tomato equals 195 US$/ton , while the FOB price at the Syrian border for packed fresh

greenhouse tomato equals 283 US$/ton, and Price of tomato paste at the Syrian border equals

9

980 US$/ton. With reference to the EU market, the parity price is calculated for packed

greenhouse tomato and equals 775 US$/ton.

3 PAM analysis results

The first step in the PAM analysis of packed and processed tomato was to construct an input-

out put table showing the physical inputs that were required to produce a unit of out put. Private

and social prices were then used to construct budgets that showed private and social profits. The

results of PAMs analysis of tomato systems are shown in the following tables.

Table 1 PAM of Packed field tomato

Costs Item Revenue

Tradable inputs

Domestic factors

Profits

Private Price A 15133 B 4732 C 4446 D 5955

Social Price E 11661 F 4603 G 3802 H 3256

Divergences I 3473 J 129 K 644 L 2699

Table 2 PAM of Packed Greenhouse EU

Private Price A 25182 B 5956 C 6331 D 12895

Social Price E 45504 F 6755 G 5516 H 33233

Divergences I -20322 J -798 K 815 L -20339

Table 3 PAM of Tomato paste

Private Price A 40000 B 14054 C 9826 D 16119

Social Price E 48925 F 14664 G 8956 H 25305

Divergences I -8925 J -610 K 870 L -9186

10

Table 4 Packed Greenhouse Regional

Private Price A 25182 B 5851 C 6257 D 13074

Social Price E 20284 F 6627 G 5440 H 8217

Divergences I 4898 J -776 K 817 L 4857

Table 5 Indicators

Main Indicators Fresh open

field regional market

Fresh greenhouse

regional market

Fresh greenhouse EU

market

Tomato paste open field low

concentrate

FCB 0.427 0.324 0.329 0.379

DRC 0.539 0.398 0.142 0.261

NPC 1,298 1.241 0.553 0.818

EPC 1.474 1.415 0.496 0.757

PS 0.231 0.239 -0.447 -0.188

PSE 0.178 0.193 -0.808 -0.230

3.1 Profitability

The financial cost-benefit ratios (FCB) computed for each system are below 1, indicating that for

2004, all the systems are profitable. The most profitable systems are in decreasing order are

fresh greenhouse regional, fresh greenhouse EU market, tomato paste regional, fresh open field

regional.

3.2 Economic efficiency

Looking at the profit obtained at social price, the systems maintain their profitability under the

new policy and market environment.

In terms of return to Domestic Factors invested at social price, all systems had strong

comparative advantage (DRC is below 0.5) and the most efficient systems in decreasing order

are fresh packed greenhouse tomato EU market (DRC=0.142), tomato paste (DRC=0.261) fresh

packed greenhouse tomato regional (DRC=0.398) fresh packed regional (DRC=0.539).

11

3.3 Transfer of resources

• The lower FCB ratios obtained from both packed open field and greenhouse regional

market systems compared to the DRC indicates that both systems are more profitable at

private price than they are at social price. However, for the other systems (packed

greenhouse and tomato paste), the FCB is higher than DRC indicating that both systems

are more profitable at social price than at private price.

• Both fresh systems at the regional market have an Effective Protection Coefficient (EPC)

above the unity, and accordingly, the benefit on aggregate from a positive transfer of

resources from the rest of the economy.

• The Producer Subsidy Equivalent (PSE), which compares the share of the revenue

earned by each system due to transfer of resources from the rest of the economy, is

positive for the packed field and greenhouse regional systems indicating a transfer of

resources from the economy to these systems. For the remaining systems, the PSEs are

negative indicating a transfer of resources from these systems to the whole economy.

• Regarding the structure of these transfers of resources, the largest share of the transfer is

due to price distortions affecting the revenue of the systems (62% on average for all the

selected systems), while distortions induced by the current policy environment and

market imperfection have a more limited impact on the value of tradable input (17% on

average for all the systems).

• The ratio of the EPC to the NPC can be used as an indication of the respective impact of

the current policy on the prices of tradable outputs and tradable inputs. For most of the

systems, the ratios of NPC to EPC are rather small, meaning that most of the distortion

between the private price and the social price situation is due to divergence on tradable

outputs.

12

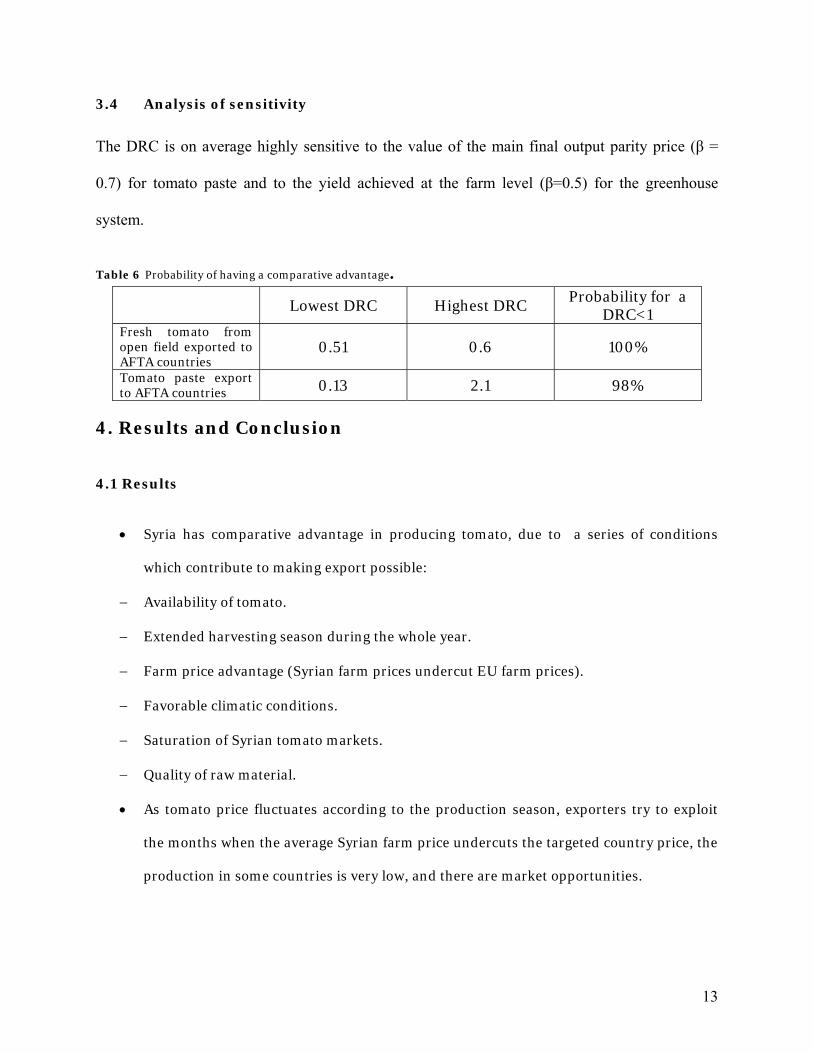

3.4 Analysis of sensitivity

The DRC is on average highly sensitive to the value of the main final output parity price (β =

0.7) for tomato paste and to the yield achieved at the farm level (β=0.5) for the greenhouse

system.

Table 6 Probability of having a comparative advantage.

Lowest DRC Highest DRC Probability for a

DRC<1 Fresh tomato from open field exported to AFTA countries

0.51 0.6 100%

Tomato paste export to AFTA countries 0.13 2.1 98%

4. Results and Conclusion

4.1 Results

• Syria has comparative advantage in producing tomato, due to a series of conditions

which contribute to making export possible:

− Availability of tomato.

− Extended harvesting season during the whole year.

− Farm price advantage (Syrian farm prices undercut EU farm prices).

− Favorable climatic conditions.

− Saturation of Syrian tomato markets.

− Quality of raw material.

• As tomato price fluctuates according to the production season, exporters try to exploit

the months when the average Syrian farm price undercuts the targeted country price, the

production in some countries is very low, and there are market opportunities.

13

• Tomato sector is fairly protected and this sector has gotten benefit from the subsidies

concerning irrigation, and the protection of the local production by imposing high tariff

quota on tomato import according to the agricultural calendar. However, this sector has

also an implicit tax especially for packaging. Since the tax levied on packing material is

very high the share of these costs is very significant (about 10-15% for fresh tomato and

more than 40% for tomato paste).

• To penetrate international markets, Syrian tomato products should be compatible with

the international standards.

4.2 Recommendations

• Improving the policies concerning quality to produce high quality raw material to cope

with consumer preferences at international markets, as well as to comply with the

required specifications in these markets.

• Adopting high technology for processed tomato in order to improve conversion rate and

enhance the feature of final products in terms of consumption and processing by

reducing raw material costs.

• Complying with the competitive prices by reducing raw material costs and increasing the

yield per area unit.

• Encouraging the adoption of a special tomato variety that has a high share of the solid

material either by improving researches or by imports.

• Strengthening international trade cooperation that aim to reduce fees and facilitate

tomato products flows.

• Improving market information and transparency to comply with international challenges

and to improve the elasticity and market efficiency of tomato sub-sector.

• Reducing the applied fees related to tomato sub-sector.

14

• References

4 Coque, J. Opportunities for Syrian fruit and vegetable exports in the EU market. NAPC, Damascus, may 2003.

5 D. Rama. Agricultural Marketing and Processing. 2000.

6 Lancon, Frederic. Comparative advantage technical note. NAPC, 2004.

7 NAPC. SOFAS. 2002.

8 NAPC. SOFAS. 2005.

15