compensation and benefits trends africa … · compensation and benefits trends africa and middle...

TRANSCRIPT

COMPENSATION AND BENEFITS TRENDSAFRICA AND MIDDLE EAST

Brad BieraManaging Consultant, Marsh Africa

Joe BarberSenior Associate, Mercer UAE

1MERCER

Contents

• Introduction

• Compensation and Benefit trends in Africa and the GCC

• The Case for Flexible Benefits – Supporting transformation of the Compensation Mix

Appendix– Overview of the GCC region– Compensation and Benefit trends for the GCC– Emerging trends and Future Outlook in the GCC– Overview of the Economic trends in Sub Sharan Africa – Compensation and Benefit trends in Sub Sharan Africa– Common Themes and Future Opportunitites

2MERCER

• Is the market really changing?

• Conventional and unconventional wisdom

• EMEA and the ME(N)A economy

Perspective

3MERCER

“The ‘environment’ is where we live; and development is what we all do in attempting to improve our lot within that abode. The two are inseparable.”

Our Common FutureGEO 4 – United Nations Environment Programme

4MERCER

Points to ponder – 35 000 foot view

• Common Language for Compensation and Benefits (Redruth)

• Moral Hazards of economic prosperity– Access to non renewable resources and related strategies– Eurozone paradox (impacts of revised purchase power and status)– Infrastructure investment– Rapid hyper inflation of compensation and benefts

5MERCER

Who is at risk

6MERCER

Points to ponder – 35 000 foot view

• Road to Nationalisation – “State of Africa” / “Arab Spring”– Importation of skills– Growth of insurance markets– Lead indicators – white goods, cars, houses and medical inflation– Employment Equity – BEE/Saudirisation– Resource taxation

• Variable / fixed compensation models and the evolution of TCTC (African Sustainability report 2004)

7MERCER

8MERCER

Points to ponder – 35 000 foot view

• Maturation of market– Skills shift to national resourcing / resource scarcity / impact on quality /

parity of benefits– Regulators and formalised pension structures– (de risking of social exposure through structured social taxation and

compulsory savings)– Broader compensation strategies

Compensation and Benefit Trends in Africa and the GCC

10MERCER

Common Themes

Developing compensation and benefit strategies that appeal to a broad employee demographic

Nationalisation programs within the private sector

Increasing levels of legislation to protect foreign employees

Pay increases of between 3% and 8% can be expected in 2012 dependent upon city / country

Re-design and review of cash allowances

There is a clear move to reduce fixed employment costs and increase “at risk” pay through short and long term incentives, moving towards rewarding individual performance

11MERCER

Compensation Trends in the GCCRemuneration mix 2011

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

UAE KSA QR OM KW

BenefitsLong-term incentivesShort-term incentivesGuaranteed allowancesBase salary

Total Remuneration Mix (all functions & levels)• In the UAE, LTIs have

a stronger representation in the pay mix this year.

• The pay mix for KSA shows that base salary has a larger ratio in 2011.

• Base pay constitutes a higher percentage of the pay mix in Oman and Kuwait in 2011 compared to last year, while the ratio of benefits and STIs was higher in 2010 in both countries.

12MERCER

Compensation Mix – SSA (TRS Countries only)

1207 March 2012

49%54% 56% 58% 59% 57% 56%

53%

20%19%

19% 17% 16%15%

14%14%

4%5%

6% 7% 8%8%

8% 13%

27%23% 20% 18% 18% 20% 22% 21%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

S1 (PC 40 - 41) S2 (PC 42 - 44) S3 (PC 45) S4 (PC 46 - 49) S5 (PC 50 - 52) S6 (PC 53 - 56) S7 (PC 57 - 58) S8 (PC 60 - 64)

Basic Salary Other Guaranteed Cash Non-Guaranteed Bonus (Variable) Employment Benefits

13MERCER

Emerging Definition and the Scope of Total Rewards

Compensation

Base pay

Guaranteed “bonuses”

Short term incentives

Long term incentives

Financial allowances

Financial recognition programs

Deferred compensation

Development & Career

Performance management

Learning and development

Career opportunity and paths

Tuition reimbursement

Mobility opportunities

Benefits

Retirement

Savings and other wealth creation programs

Medical / Dental / Vision / Prescription Drug, etc.

Life insurance

Short and long term disability

Accident coverage

Job-related perquisites

Work Lifestyle

Time off

Wellness programs

Dependent care

Workplace flexibility

Commuter programs

Workplace facilities and perquisites

Experiential rewards

Non-financial and status recognition

14MERCER

Future Opportunities

Re-define the provision of cash allowances

Manage healthcare benefits on a regional basis

Evaluate the feasibility for expatriate retirement benefits

Developing long term and short term disability provisions

Reviewing the case for Flexible Benefits

The Case for Flexible BenefitsSupporting transformation of the Compensation Mix

MERCER

Key drivers of flexible benefitsGlobal and regional themes

Global perspective• The cost of insured benefits are constantly rising• Shift to total compensation philosophies and defined contribution strategies

• Workforces are more demographically diverse• Focus on employee empowerment and communication• Promote internal employee equity but especially for benefits harmonisation in M&A• EU placing greater emphasis on employment diversity and employee choice. Trade

unions beginning to debate merits of flex

Middle East perspective• High and escalating costs of insured benefits, especially medical• High levels of western expatriates with experience of / preferences for flexible benefits • Western multinationals with flexible benefits plans around the world, especially Pharma

and Hi-Tech / IT• Higher disposable income and allowances culture – ready made flexible benefits

spending account

• High inter-regional employee mobility

17MERCER

Key drivers of flexible benefitsBusiness case / reasons why / return on investment

Better attraction and retentionIncreased employee satisfactionIncreased awareness of total rewardImproved self-service behaviours Reduced HR effortImproved recruitment efficiencyIncreased flexible workingBetter targeting of rewardSimplification / harmonisation of terms

Reduction in benefit costsIncreased control of volatility in benefit costsIncreased risk-sharing with employeesReduced tax and social security payments

What can flex, in itself, achieve?

What can be achievedthrough flex?

18MERCER

Key drivers of flexible benefitsWhat to consider: Four perspectives

What are the key metrics that we will use to measure the flex plan’s effectiveness and return on investment (ROI)?

How should the flex plan be designed and delivered in order to maximize ROI for the company?

Can the flex plan be designed at an affordable and sustainable cost

If not, how should the design be modified to be financially viable?

What type of plan design best differentiates the company from competing employment opportunities?

How do employees place value on different elements of plan design?

What are the labour and related rewards environments in which the company competes?

How do they influence the optimal design of the flex plan and therefore restrict the company’s flex goalS?

EMPLOYER PERSPECTIVE

COST PERSPECTIVE

EXTERNAL PERSPECTIVE

EMPLOYEE PERSPECTIVE

Overview of the GCC region

20MERCER

Regional Overview and Economic TrendsFocus on the Gulf Cooperation Council (GCC) countries

• GCC countries:– Bahrain– Kuwait– Oman– Qatar– Saudi Arabia– UAE (seven emirates

including Abu Dhabi; Dubai)

21MERCER

Regional Overview and Economic TrendsAll countries are experiencing rapid population growth• Population growth of 3.4% across GCC over past ten years driven by immigration

• Economist Intelligence Unit forecast population to grow by 33% by 2020

• Young population with over 50% aged 20 or below

• Expatriates represent majority of workforce in all except Saudi Arabia and Oman

0

5

10

15

20

25

30

35

Bahrain Kuwait Oman Qatar SaudiArabia

UAE

Population (in millions)

Source: Economist Intelligence Unit

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

UAE Qatar Kuwait Bahrain Saudi Oman

Expatriate workforce as % of total (2009)

Source: Nationalisation surveys

2000

2010

2020 forecast

22MERCER

Regional Economic & Business Trends

• 2012 average GDP forecast for the region 3.3%

• UAE tried to blunt the financial crisis by increasing spending and boosting liquidity in the Banking sector

• Crisis hit Dubai the hardest, as it was heavily exposed to the depressed real estate prices

• Long term challenges:- Dependence on oil- Large expatriate workforce- Growing inflation pressures

• Strategic plans focus on diversification and creating opportunities for nationals through improved education and increased employment ofnationals in the private sector

• The economy is expected to continue a slow rebound

23MERCER

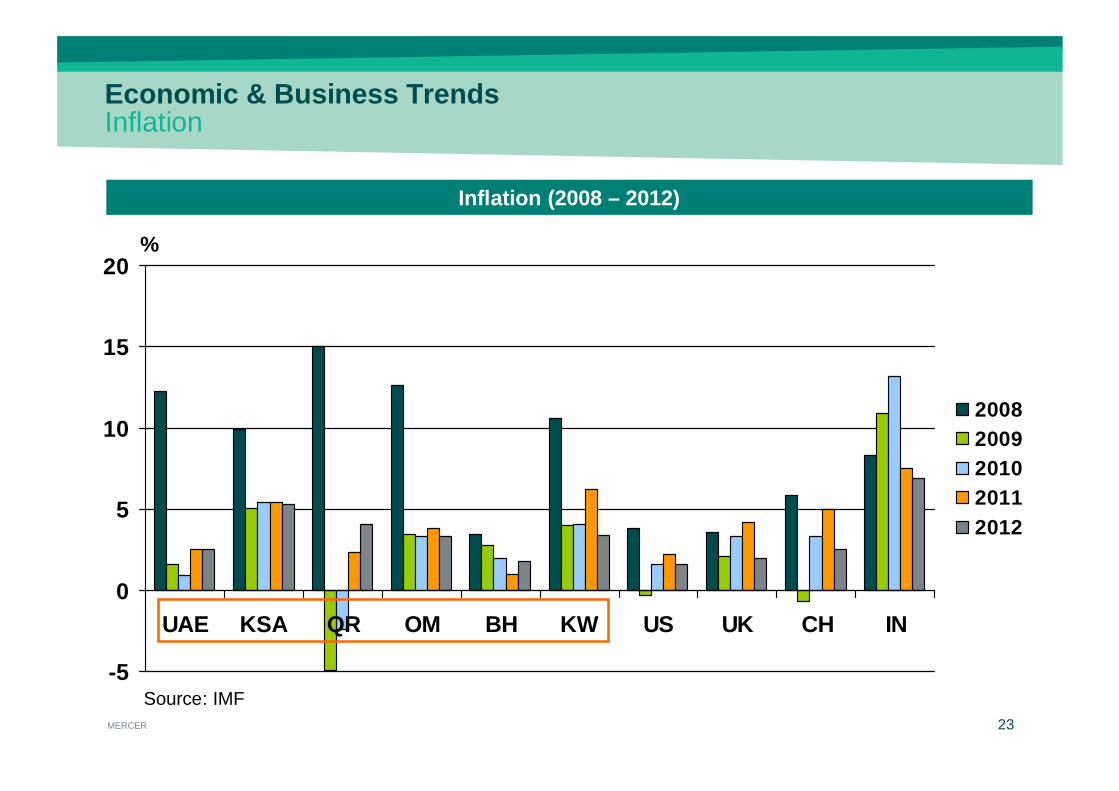

Economic & Business TrendsInflation

-5

0

5

10

15

20

UAE KSA QR OM BH KW US UK CH IN

20082009201020112012

%

Inflation (2008 – 2012)

Source: IMF

24MERCER

Economic & Business TrendsCost of Living

164146--Doha6

181

176

152

144

139

55

50

2010

COST of Living Ranking

8

7

5

4

3

2

1

GCC

109

-

77

90

82

20

26

2009

185126Jeddah

184-Muscat

94

119

112

52

65

2008

159

135

-

81

61

2011

Kuwait

Riyadh

Manama

Dubai

Abu Dhabi

City

Cost of Living: lower across the GCC compared to 2010, most expensive city is Abu Dhabi

Source: 2011 Mercer Cost of Living Survey

Compensation and Benefit Trends in the GCC

26MERCER

2011 Actual Salary Increases & 2012 ForecastsIndustry Specific

Companies from the consumer goods,services and durable sectors provide increases above the market.

0.0

2.0

4.0

6.0

8.0

2011 actual 6.6 5.2 5.1 4.5 4.2 6.02012 forecast 6.6 5.4 5.3 6.2 4.8 6.1

Consumer goods Services Durable High-tech Energy Others

2011 actual salary increases & 2012 forecasts – by industry

Companies from the high-tech and energy sector provide increases slightly below the overall market level.

The consumer goods and high-tech sectorsforecast the highest increases for 2012.

%

27MERCER

Guaranteed Cash Allowances

0 50,000 100,000 150,000 200,000 250,000 300,000 350,000 400,000

Para-professionals

Professionals

Management

ExecutivesHousing

National

Transportation

Utilities

Meal/LuncheonVoucher

Fuel

Furniture

Shift

AED

Guaranteed allowances by career stream

28MERCER

Employee BenefitsIntroduction and comments

• In the five years prior to 2010 a steady increase of benefit levels was evident particularly in the areas of medical, death and disability

• The economic climate has not, broadly speaking, changed the prevalence or level of benefits being offered, although employers are:– looking for alternatives to cash as differentiators in their employment

brand – looking to manage increasing medical costs– showing an increasing interest in employee engagement and retention

- Retirement savings plans- Flexible benefit plans

29MERCER

90%94%

86%

93%

100%

93%

0%

17%

34%

52%

69%

86%

103%

UAE Saudi Arabia Qatar Bahrain Oman Kuwait

% Prevalence of medical benefits

Regional Employee Benefits High prevalence of medical benefits

• Mandatory cover for expats and families– Introduced in KSA in 2006– Introduced in Abu Dhabi in 2007– Certain Dubai free zones in 2008– Expected across Dubai in 2011– Debated in Qatar and Bahrain

• Mandatory model requires core level of benefits under approved plans with limitations on co-pays / deductibles

• Uncertainty over legislative requirements has resulted in rich benefit provisions

• High prevalence of diabetes and obesity together with high benefit levels is driving premium escalation

• Need for employers to manage healthcare costs proactively going forward

30MERCER

Medical careWidespread provision of private health benefits to employees

• Legislation in place in KSA and Abu Dhabi requiring employer sponsored medical insurance for employees (expats and Nationals in KSA) and their dependants

• Legislation planned to make medical insurance compulsory in Qatar. The timing of the introduction is uncertain

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Cover for employee'sfamily

Premium sharing forfamily cover

Fully insured

UA

E

Qatar

KS

A KS

A

KS

AQatar

UA

E

UA

E

Qatar

31MERCER

Medical carePrevalence of benefits within medical plans

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dental Maternity Vaccines Pre-existingconditions

Emergencyout of area

cover

Vision

UAE Qatar KSA

• Dental and vision cover are becoming more prevalent

• Prevalence of cover for vaccines has remained stable

Data for Management Level Employees

32MERCER

Supplemental death and disability benefits

65%

75%

64%

79%

87%

82%

59%

40%

82%

22%27%

15%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Death benefits Accidental death cover Long term disability Short term disability

UAE Saudi Arabia Qatar

• Lump sum death and permanent disability benefits are most commonly provided through fully insured plans insured

• Provision of supplemental short term disability benefits varies widely as do the funding mechanisms

33MERCER

End of service benefitsAn integral part of the region’s rewards framework

Built on basic or gross salary depending on the country

Broadly one month’s salary per year of service

Originally designed as severance protection

Increasingly cited as an alternative to a retirement benefit

Reductions in benefit for voluntary employee termination

Varied practices in relation to funding and accounting for EOSB

34MERCER

End of service benefitsOrganizations providing enhanced end of service benefits

42%

41%

43%

40%

41%

41%

42%

42%

43%

43%

Enhanced EOSB

UAEQatar

KSA

• Approximately 40% of organisations enhance EOSB above statutory minimum

• Broadly equal numbers of companies enhance salary or service component of EOSB

• Formal funding policies increasing across the Gulf

31%

36%

30%

27%

28%

29%

30%

31%

32%

33%

34%

35%

36%

Funded EOSB

UAE

QatarKSAU

AE U

AEQ

atar

Qatar

KS

A

KS

A

35MERCER

Other key benefitsPrevalence of other benefits

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Share PurchasePlans

Loans Annual Air Fares FurnitureAllowance

Mobile Phones ClubSubscription

UAE Qatar KSA

• Organizations continue to review benefits for locally contracted staff with a view to curtailing or removing benefits usually associated with expatriate assignees or seconded personnel

• There is also a trend to reduce expatriate benefits as the UAE is no longer seen as a hardship posting

Overview of Africa – Economic trends

37MERCER

Regional Overview and Economic TrendsAfrica countries

GDP Growth Forecasts 2012:

• Immense natural resources

• Large investments in people

• Region dominated by West Africa (oil-based economies)

• East Africa to be the fastest growing region

38MERCER

Regional Overview and Economic TrendsAll countries are experiencing rapid population growth

• Population growth of over 8% across Sub-saharan African Region

• Surging external demand (from China & India) hungry for oil & mineral resources

• A drive towards “consumerisation” (demand for modern goods and services)– Telecommunications and banking are key industries in this area

Source: Economist Intelligence Unit

Sub-saharan African population:

39MERCER

Economic & Business TrendsInflation: Sub-saharan & North Africa

Inflation:

Source: Economist Intelligence Unit

40MERCER

Economic & Business Trends Cost of Living

Tunis

Cape Town

Johannesburg

Victoria

Niamey

Libreville

N’Djamena

Luanda

1316

COST of Living Ranking

8

7

5

4

3

2

1

Africa Ranking

207

158

25

23

12

3

1

World RankingCity

Cost of Living: Cities across Africa, most expensive for expats is Luanda

Source: 2011 Mercer Cost of Living Survey

Compensation and Benefit trends in Africa

42MERCER 4207 March 2012

Annual Increases – SSA

0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%

Rw

and

aM

adag

Tanz

Mo

zU

gand

aK

enya

Bu

run

di

Ethio

pia

Gab

on

Cam

Co

ngo

Eq G

uin

eaB

otsw

ana

DR

CM

alawi

ZimZam

bia

An

gola

Senegal

CD

IM

aliTo

goB

urkin

a FLib

eriaB

enin

Nigeria

Sierra LG

han

aG

uin

ea

2011 Actual 2012 Forecast 2012 Revised Forecast

43MERCER 4307 March 2012

Provision of Medical Care – SSA

0%

20%

40%

60%

80%

100%

EQ G

uin

ea

Zamb

ia

Libe

ria

Bu

run

di

Mo

z

Sierra L

Mali

Gu

ine

a

Ethio

pia

Bo

tswan

a

Sen

egal

An

gola

Ke

nya

Nige

ria

Gh

ana

Zim

Tanz

Gab

on

Malaw

i

Cam

Ug

and

a

Be

nin

Bu

rkina F

CD

I

Co

ngo

DR

C

Mad

ag

Rw

and

a

To

go

Provide Medical Care Average SS Africa

44MERCER 4407 March 2012

Average Company Medical Expenses – SSA (TRS Countries only)

$ 0

$ 500

$ 1 000

$ 1 500

$ 2 000

$ 2 500

$ 3 000

Malaw

i

Gh

ana

Rw

an

da

Gu

ine

a

Tanz

Mali

Sen

eg

al

DR

C

Zamb

ia

Ke

nya

Bo

tswan

a

Cam

Nige

ria

Mo

z

Zim

Gab

on

CD

I

Co

ngo

An

gola

Be

nin

Ug

and

a

Average Company Medical Expenses p.a. Average SS Africa

45MERCER 4507 March 2012

Private Retirement Provision – SSA

0%10%20%30%40%50%60%70%80%90%

100%

DR

C

Mo

z

Ta

nz

Bu

rkin

a F

Gu

ine

a

Ma

li

Ga

bo

n

Co

ng

o

Be

nin

Sie

rra L

CD

I

Rw

an

da

Ug

an

da

Ma

da

g

To

go

Za

mb

ia

Se

ne

ga

l

Gh

an

a

Libe

ria

Bu

run

di

Ma

law

i

Bo

tswa

na

Eth

iop

ia

Ke

ny

a

Nig

eria

An

go

la

Ca

m

Provide Private Retirement Average SS Africa

46MERCER 4607 March 2012

Total Contribution ( % of Basic Pay to Private Retirement ) – SSA (TRS Countries only)

0%2%4%6%8%

10%12%14%16%18%20%

Tan

z

Rw

an

da

An

gola

Mali

CD

I

Se

ne

ga

l

Be

nin

Co

ng

o

Ga

bo

n

Mo

z

Ke

ny

a

DR

C

Ug

and

a

Ca

m

Zam

bia

Gh

an

a

Nig

eria

Ma

lawi

Bo

tswa

na

Gu

ine

a

Zim

Total Contribution (% of Basic Pay to Private Retirement) Average SS Africa

47MERCER 4707 March 2012

Provide of Company Cars – SSA

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ken

ya

Ug

an

da

Bo

tswa

na

Ta

nz

Be

nin

Ca

m

Gh

an

a

Mo

z

Nig

eria

Zam

bia

Ma

li

Gu

ine

a

Liberia

Co

ng

o

DR

C

Rw

an

da

To

go

An

go

la

Ga

bo

n

Sen

egal

Bu

rkina

F

CD

I

Ma

law

i

Zim

Sierra L

Ma

da

g

Eth

iop

ia

EQ

Gu

ine

a

Bu

run

di

Provide Company Cars Average SS Africa

48MERCER 4807 March 2012

Pay Car Allowance – SSA (TRS Countries only)

0%

5%

10%

15%

20%

25%

30%

35%

40%

CDI

Congo

Guin

ea

Mali

Rw

anda

Gabon

DRC

Benin

Zim

Senegal

Botsw

ana

Tanz

Moz

Ghana

Cam

Nigeria

Malaw

i

Zambia

Kenya

Uganda

Pay Car Allowance Average SS Africa

49MERCER 4907 March 2012

Average Company Car Benefit per annum – SSA (TRS Countries only)

$ 0

$ 5 000

$ 10 000

$ 15 000

$ 20 000

$ 25 000

$ 30 000

$ 35 000

$ 40 000

Tan

z

DR

C

Gu

inea

Ug

and

a

Bo

tswan

a

Gh

an

a

Nig

eria

Ken

ya

Mali

Zim

Sen

ega

l

An

gola

Ben

in

Zam

bia

Co

ng

o

Gab

on

CD

I

Cam

Rw

and

a

Ma

law

i

Mo

z

Average Company Car Benefit p.a. Average SS Africa

50MERCER 5007 March 2012

Car Allowance Value – SSA (TRS Countries only)

$ 0.00

$ 5 000.00

$ 10 000.00

$ 15 000.00

$ 20 000.00

$ 25 000.00

$ 30 000.00

$ 35 000.00

Gu

ine

a

Gh

an

a

Ga

bo

n

Rw

an

da

An

go

la

Ta

nz

Ma

li

Be

nin

Co

ng

o

Nig

eria

Ug

an

da

Bo

tswa

na

Ken

ya

Se

ne

ga

l

Zim

CD

I

Ca

m

DR

C

Zam

bia

Ma

law

i

Mo

z

Car Allowance Value p.a. Average SS Africa

Mercer (Polska) Sp. z o.o. Al. Jerozolimskie 94, 00-807 Warszawa zarejestrowana w S dzie Rejonowym dla m.st. Warszawy w Warszawie XII Wydzia Gospodarczy KRS: 0000043554, NIP: 525-21-41-429, REGON: 016094276 Wysoko kapita u zak adowego: 400 000,00z , kapita wp acony w ca ci