company presentation - february · pdf filethat otherwise relate to objectives, strategies,...

TRANSCRIPT

Company Presentation - February 2013

2

Statements included or incorporated in these materials that use the words "believe", "anticipate", "estimate", "target", or "hope", or

that otherwise relate to objectives, strategies, plans, intentions, beliefs or expectations or that have been constructed as statements as

to future performance or events, are "forward-looking statements" within the meaning are not guarantees of future performance and

involve risks and uncertainties that could cause actual results to differ materially from historical results or those anticipated at the time

the forward-looking statements are made. MINT undertakes no obligation to publicly update or revise any forward-looking statement,

whether as a result of new information, future events or otherwise. MINT makes no representation whatsoever about the opinion or

statements of any analyst or other third party. MINT does not monitor or control the content of third party opinions or statements and

does not endorse or accept any responsibility for the content or the use of any such opinion or statement.

FORWARD LOOKING STATEMENT Disclaimer

Agenda 2012 Performance Recap

Hotel & Mixed Use Business Restaurant Business

Other Important Information

Avani Sepang Goldcoast Resort, Malaysia

2012 Performance Recap

Performance Recap ANOTHER RECORD-HIGH PERFORMANCE

MINT REPORTED RECORD-HIGH NET PROFIT OF THB 3.4 BILLION, A 78% INCREASE YoY EXCLUDING EXTRAORDINARY ITEMS (18% INCREASE FROM REPORTED NET PROFIT), ATTRIBUTABLE TO IMPROVEMENT OF ALL THREE BUSINESS UNITS, ESPECIALLY FROM THE HOTEL & MIXED USE BUSINESS, WHICH INCLUDES IMPROVED CORE HOTEL OPERATIONS TOGETHER WITH STRONG PERFORMANCE OF ANANTARA KIHAVAH AND ST. REGIS HOTEL, THE NOW PROFITABLE ANANTARA VACATION CLUB AND THE CONSOLIDATION OF OAKS.

5

1,000

2,000

3,000

4,000

2011A Hotel & Mixed Use Restaurant Retail Trading 2012A

One-time items

2,880

3,409

1,919

NPAT (THB Million)

5%

6%

7%

8%

9%

10%

11%

2011A Hotel & Mixed Use Restaurant Retail Trading 2012A

10.3%

7.0%*

NPAT Margin

+78% YoY (Excl one-time items)

* Excludes gain on reclassification of investments in S&P, netted off with impairment charge of China business

9.5%

Complete by 2015 64% of Total 50% of Total

KEY 2012 FINANCIAL & OPERATIONAL TARGETS ACHIEVED ALL KEY 2012 TARGETS ARE ACHIEVED / ON TRACK.

6

2011 Actual 2012 Target 2012 Actual

NPAT Growth

ROIC

Int’l Contribution - Revenue

Int’l Contribution - NPAT

Hotel Occupancy

Hotel ADR

Hotel RevPar

Sale of St. Regis Residences

Hotel Acquisition

Restaurant SSS Growth

Restaurant Outlet Expansion

Organic Revenue Growth

Sale of AVC

Restaurant Acquisition

55%* 15-20% p.a. 78%*

14.7%* >15% by 2016 13.2%

24% 40% by 2016 29%

7% 50% by 2016 21%

65% ~70% 69%

-5% ~0-3% 4%

17% High Single Digit 11%

49% of Total Complete by 2013 73% of Total

USD 19mn USD 40+ mn USD 51mn

Oaks N/A Bundarika

9.0% 4-5% 5.5%

8-10% 9.9%

11%* 12-15% 13%*

Ribs & Rumps; Remaining 30% of Thai Express;

Additional 5% of S&P N/A Riverside

On Track

On Track

On Track

On Track

Sale of The Estate Samui

Note: * Exclude one time items: gain in reclassification of investment in S&P, netted off with impairment charge of China business in 2011

On Track

Performance Recap

Hotel & Mixed Use Business

Pool Villa, Anantara Vacation Club Phuket

Key Development IMPROVING HOTEL OPERATIONS

ALL HOTEL STATISTICS SAW IMPRESSIVE IMPROVEMENTS YoY IN 2012. 2012 REVPAR IS STILL BELOW THE 2008 PEAK LEVEL BECAUSE OF THE CHANGE OF MIX WITH THE ADDITION OF OAKS. NEVERTHELESS, THE NOTABLY HIGHER NUMBER OF ROOMS IN THE PORTFOLIO LED TO A SUBSTANTIAL INCREASE IN TOTAL REVENUE AMOUNT.

8

THB

* Note: Hotel Statistics include Oaks Hotel & Resort

NUMBER OF HOTEL ROOMS

0

3,000

6,000

9,000

12,000

2008 2009 2010 2011 2012

MLR

Managed

Joint-venture

Owned3,102

3,552 4,114

9,575 10,348

OCCUPANCY

65%

52% 52%

65% 69%

20%

40%

60%

80%

2008 2009 2010 2011 2012

ADR

6,339 5,880 5,695

5,385 5,589

2,000

4,000

6,000

8,000

2008 2009 2010 2011 2012

REVPAR

4,142

3,076 2,976

3,479

3,871

1,000

2,000

3,000

4,000

5,000

2008 2009 2010 2011 2012

THB

THB

+4% YoY

+11% YoY

+8% YoY

+4% YoY

COMPANY OWNED HOTELS – 2012 TO DATE

THE ADDITION OF OWNED HOTELS WILL SUPPORT MINT’S STRATEGY TO GROW REVENUE AND NET PROFIT SIZE OF THE HOTEL BUSINESS. MINT CONTINUES TO LOOK FOR OPPORTUNITIES TO EXPAND ITS OWNED HOTEL PORTFOLIO IN THE RIGHT MARKETS.

9

Acquisition of Bundarika, Phuket (To be rebranded to Anantara)

• 15 minutes south of Phuket International Airport

Expected Launch Date:

• 2H13

• 77 keys on 23 rais of beachfront land

• Hoi An: a short walk from Ancient Town

• Quy Nhon: private beach

Location:

Size:

Location:

• Currently in operation, but rebranding expected to be within 6-12 months

• South- west coast of Sri Lanka

Launch Date: • Oct 2012

• 105 keys of beachfront land

Location:

Size:

• South- west coast of Sri Lanka

Expected Launch Date:

• 2014

• 60 keys on 6 rais of beachfront land

Location:

Size:

Size: • Hoi An: 96 keys • Quy Nhon: 63 keys

Ambalangoda

Key Development

PHUKET

KALUTARA, SRI LANKA

VIETNAM

AMBALANGODA, SRI LANKA

Acquisition of Life Resorts, Vietnam (Hoi An to be rebranded to Anantara, Quy Nhon to be rebranded to Avani)

Expected Launch Date:

Kani Lanka in Sri Lanka has successfully been rebranded to Avani Acquisition of Paradise Island Resorts, to be constructed into Avani

Bentota

Kalutara

HOTEL MANAGEMENT – 2012 TO DATE

AS MINT’S OWN BRANDS – ANANTARA, AVANI AND OAKS – GAIN THEIR RECOGNITION IN THE MARKET, MINT CONTINUES TO EXPAND ITS HOTEL MANAGEMENT PORTFOLIO. ASSET LIGHT HELPS SUPPORT MINT’S OVERALL STRATEGY IN THE IMPROVEMENT OF PROFITABILITY AS WELL AS IMPROVEMENT OF ROIC.

10

Egypt

Key Development

Eastern Mangroves Hotel & Spa by Anantara, Abu Dhabi

222 Rooms / Opened June 2012

Avani Sepang Goldcoast Resort, Malaysia 315 Rooms / Operated Nov 2012

Anantara Bali Uluwatu Resort & Spa 77 Rooms / Opened June 2012

Anantara Sanya Resort & Spa, China 122 Rooms / Opened Nov 2012

Oaks Bangkok Sathorn 115 Rooms / Opened Oct 2012

FURTHER ENHANCEMENT OF REVPAR

MINT CONTINUES TO STRENGTHEN ITS MARKETING AND DISTRIBUTION CHANNELS TO ENSURE CONTINUOUS GROWTH GOING FORWARD. MINT CONSISTENTLY LOOKS FOR CREATIVE WAYS TO FURTHER STRENGTHEN ITS EXISTING CUSTOMER BASE AS WELL AS INITIATES ITS PRESENCE IN NEW MARKETS.

11

Add sales offices in key strategic markets: 4 new sales offices in 2012 - China, Russia, India and UAE

Increase road shows in non-conventional markets

Initiate PR activities including face-to-face visits to key media regionally & internationally to increase awareness

Organize “Familiarization Trips” for travel agents and journalists to experience the properties

Strengthen Sales & Marketing Capability

Anantara.com website was upgraded with advanced internet booking engine

Increase conversion rate on-line using social media network

Increase On-Line Booking

Going Forward

Sales offices Sales offices opened in 2012

STRENGTHENING OF HOTEL’S NON-TRADITIONNAL MARKETS

ALTHOUGH CHINA AND RUSSIA REPRESENTED ONLY 10% OF MINT’S TOTAL FEEDER MARKETS BASED ON ROOM NIGHTS IN 2012, THE YIELDS THEY GENERATED WERE RELATIVELY MUCH HIGHER AS THEY MOSTLY STAYED AT HIGHER-ROOM-RATE HOTELS, E.G. IN MALDIVES AND PHUKET.

Going Forward

12

MINT’s 2012 Feeder Markets

China 6% Russia

4%

Others 90%

Maldives Hotels

19% Anantara

& JW Marriott Phuket

8% Four Seasons Group 17%

St. Regis 5%

Others 51%

Maldives Hotels

26%

Anantara & JW

Marriott Phuket

34%

Four Seasons Group

3%

St. Regis 1%

Others 36%

Average ADR*: Bt 10,058 Average ADR*: Bt 15,929

Average ADR: Bt 5,589

* The pie charts include total room nights of MINT hotel portfolio (excluding Oaks), while average daily rates of China and Russia markets are calculated from Maldives hotels, Anantara Phuket, JW Marriott Phuket, Four Seasons group and St. Regis (excluding others)

OAKS HOTELS & RESORTS – 2012 TO DATE

SINCE MINT’S STRATEGIC ACQUISITION OF OAKS, OAKS CONTINUES TO GROW BOTH WITHIN AUSTRALIA AND NEW MARKETS. OAKS WILL REMAIN ONE OF MINT’S MAJOR CONTRIBUTORS GOING FORWARD.

13

• Grand Hotel, Gladstone, to become a 140-room hotel (by 2013)

• 50% stake in Tidal Swell, the owner of four properties currently managed by Oaks

• Oasis Resort Caloundra, 158 hotel rooms and 9 apartments, together with MLR in Sunshine Coast

• Oaks Hyde Park Plaza, Sydney, 13 units

OAKS’ CONTRIBUTION TO MINT’S HOTEL & MIXED-USE BUSINESS IS SIGNIFICANT

2011 2012

Others

Oaks

OAKS’ REVENUE CONTRIBUTION TO TOTAL HOTEL

& MIXED-USE

OAKS’ EBITDA CONTRIBUTION TO TOTAL HOTEL

& MIXED-USE 23%

77%

31%

69%

32%

68%

2011 2012

Others

Oaks

23%

77%

31%

69%

Key Development

SELECTIVE ASSETS ACQUISITIONS ADDITIONAL MLR CONTRACTS

• Broome (140 rooms)

• Monkomo (56 rooms)

• Regis (90 rooms)

• William Street (220 rooms)

• New greenfield development to be settled between 2014 - 2015 • Oaks Carlyle (87 rooms) • Oaks Milton (298 rooms) • Oaks River Marque (152 rooms) • Oaks Emerald (120 rooms)

Oaks Bangkok Sathorn

EXPANSION OF OAKS OUTSIDE OF ITS HOME MARKETS

• First move into Asia through management contract of Oaks Bangkok Sathorn with 115 rooms (previously part of Anantara Sathorn)

• Opening Oaks Sanya in China and Oaks Liwa Suites in Abu Dhabi in 2013

OAK’S POST-ACQUISITION STRATEGIES

14

EXPANSION INTO MARKETS INSIDE AND OUTSIDE THAILAND WILL CONTRIBUTE WELL TO REVENUE & PROFIT IN COMING YEARS.

MINT’S HOTEL EXPANSION PLANS

Hotel Investment

2014

10 Hotels / 830 Rooms

• Xishuangbanna, China (103 Rooms)

• Layan, Thailand (77 Rooms)

• Doha, Qatar (117 Rooms)

• Palm Jumeirah, UAE (293 Rooms)

• Chengdu, China (150 Rooms)

• Al Yamm, UAE (30 Rooms)

• Al Sahael, UAE (30 Rooms)

20 Hotels & Properties / 2,323 Rooms

Management Contract

2013

Total

• Masai Mara Camp,

Kenya (16 Rooms)

• Amboseli Camp,

Kenya (16 Rooms)

• Grand Hotel,

Gladstone

Australia

(96 Rooms)

• Phuket –

Bundarika

(77 Rooms)

• Hoi An,

Vietnam

(96 Rooms)

• Sri Lanka

(141 Rooms)

• Chongqing, China (150 Rooms)

• Baoting, China (130 Rooms)

• Salalah, Oman (136 Rooms)

• Luang Prabang, Laos (115 Rooms)

• Al Akhdar, Oman (123 Rooms)

• Al Madina, Oman (120 Rooms)

• Mahabalipuram, India (130 Rooms)

• Qiandao Lake, China (120 Rooms)

• La Chaland, Mauritius (160 Rooms)

• Bangkok

(249 Rooms)

2015

• Ambalangoda,

Sri Lanka

(60 Rooms)

• Meru, Kenya

(16 Rooms)

• Sanya, China

(120 Rooms)

• Liwa Suites,

Abu Dhabi

(54 Rooms)

• William St.,

Melbourne

(220 Rooms)

• Udaipur, India (70 Rooms)

• Wayanad, India (95 Rooms)

• Quy Nhon,

Vietnam

(63 Rooms)

Going Forward

• Carlyle

(87 rooms)

• Milton

(298 rooms)

• Emerald

(120 rooms)

In the

process of

negotiation

2011 2012

2011 2012

Residential Properties

RESIDENTIAL PROPERTIES & AVC – 2012 TO DATE

REAL ESTATES IS ANOTHER IMPORTANT DRIVER, WITH REVENUE CONTRIBUTION OF APPROXIMATELY 20% TO THE HOTEL AND MIXED USE BUSINESS. WHILE WE PLAN A PIPELINE OF RESIDENTIAL PROPERTIES TO ENSURE THE CONTINUATION OF THE REVENUE FROM THE BUSINESS, AVC WILL HELP FURTHER STRENGTHEN THE REVENUE STREAM OF THE REAL ESTATES BUSINESS IN THE LONG TERM.

15

Anantara Vacation Club

Sold 64%

Inventory 36%

Sold 73%

Inventory 27%

Thailand 22%

Singapore 19%

Hong Kong 12%

Malaysia 11%

China 9%

Australia 4%

Japan 3%

UAE 2%

Others 18%

AVC Members

Revenue

Net Profit

Key Development

2006 2007 2008 2009 2010 2011 2012

22

46

59

2010 2012 Jan 2013

Inventories

Samui Phuket

Bangkok Bali

Queenstown

Phuket (Purpose-built)

Sanya + +

DRIVING ANANTARA VACATION CLUB

SALES OF AVC ARE EXPECTED TO CONTINUE RISING SIGNIFICANTLY WITH BOTTOM LINE STARTING TO CONTRIBUTE STRONGLY TO THE GROUP’S PROFITABILITY IN 2013-2014

16

Thailand

New Zealand

Bali

Sri Lanka

Middle East

Australia

China

Mauritius

Maldives

South Africa

More Inventories in More Destinations Horizontal Expansion into New Markets

Stable Revenue Stream

Bangkok Phuket Samui

Bali

+

4Q10A 2011A 2012A 2013E 2017E

22 +3 +21

+>100

22 25 46 >146 Up to 400 in 10 Destinations

Key focus for 2013 includes China and potentially the Middle East

Bangkok, Samui, Phuket, Bali, Queenstown, China

Vertical Efficiency to Maximize Profit

Improve efficiency of sales & marketing

Learn & better understand new markets

Cost & expenses to be gradually driven down by scale

Going Forward

2011 2012 2013F 2014F 2015F 2016F 2017F

Revenue

Sales Offices

RESIDENTIAL PROJECT OPPORTUNITIES

17

Egypt

AVC

Egypt

Possible Extension to Anantara Riverside & Avani Bangkok

Possible Extension to Anantara Vacation Club Phuket

Possible Project given Land Bank in Khao-Lak

Others as Opportunity Comes Along

MINT CONTINUES TO EXPLORE OPPORTUNITIES TO ADD RESIDENTIAL PROJECT ONTO EXISTING & NEW PROPERTIES, TO ENSURE CONTINUATION OF RESIDENTIAL PROPERTIES AS PART OF THE MIXED-USE BUSINESS OVER THE NEXT FIVE YEARS.

Going Forward

Restaurant Business

SSS & TSS Growth

RESTAURANT SALES GROWTH

RESTAURANT BUSINESS CONTINUES TO SEE ROBUST AND STABLE GROWTH. SAME-STORE-SALES SHOWED REASONABLE GROWTH IN 2012, ON THE BACK OF STRONG DOMESTIC CONSUMPTION IN THAILAND, TOGETHER WITH EFFECTIVE MARKETING CAMPAIGNS.

19

7.8%

12.3%

9.8%

6.5%

7.6% 6.5%

3.3%

4.6%

11.9%

17.4%

14.4%

12.7%

16.0%

13.6% 12.5%

11.4%

0%

5%

10%

15%

20%

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Same Store Sales Growth Total System Sales Growth

Key Development

1,043 1,112 1,148 No. of Outlets

1,257

3.9%

-2.7%

3.7%

9.0%

5.5%

19.1%

11.9%

9.8%

14.1% 15.1%

-5%

0%

5%

10%

15%

20%

2008 2009 2010 2011 2012

1,381

Top 3 2012 TSS:

Dairy Queen 30.2%

(SSS 17.5% + 17.5% outlet expansion)

Swensen’s 18.9%

(SSS 10.7% + 5.2% outlet expansion)

The Pizza Company 14.6%

(SSS 5.9% + 5.4% outlet expansion)

RESTAURANT OUTLET EXPANSION

MINT CONTINUES TO EXPAND NUMBER OF OUTLETS BY 8-10% PER ANNUM, WITH THE FOCUS PRIMARILY ON MARKETS THAT WE ALREADY HAVE PRESENCE IN.

20

SSS & TSS

2005 2011 2012 2017F

2005 2011 2012 2017F

34%

66%

34%

66% 7%

93%

36%

64% 558

2,749

Restaurant Outlets Breakdown by Geography

43%

57% 14% 86%

45%

55%

1,381

558

2,749

Restaurant Outlets Breakdown by Ownership

Franchised

Owned

1,257

1,257

45%

55%

1,381

Key Development

International

Thailand

2012 New Markets Expansion

+9.9% YoY

+9.9% YoY

Two equity-owned Swensen’s

outlets in the Maldives

First franchised The Coffee Club outlet in Egypt

First flagship The Coffee Club outlet

in Bangkok

Acquisition of Beijing Riverside & Courtyard in

China

RESTAURANT HIGHLIGHTS

MINT CONTINUES TO IMPROVE THE OPERATIONS OF ITS EXISTING FOOD BRANDS, WHILE LOOKING FOR OPPORTUNITIES TO ADD NEW BRANDS AND NEW CONCEPTS TO ITS ALREADY DIVERSE PORTFOLIO.

21

Key Development

Offered product variation with the aim to capture new

customers through the launch of its very own fried chicken

Developed store segmentation with

renovation of stores into new concept

Strengthened Western Dining Positioning

Aggressively expanded domestic franchising with additional 53 franchised

stores in 2012

Launched BK Grill concept at all stores

Continued efforts in the integration of Ribs and

Rumps since the acquisition

Rationalized outlets, relaunched Xin Wang menus

and put in place new management

Added Beijing Riverside to the portfolio through the

acquisition

BEIJING RIVERSIDE & COURTYARD

AS PART OF MINT’S FIVE-YEAR STRATEGY, IN ADDITION TO ORGANIC GROWTH, MINT ALSO LOOKS FOR ACQUISITION OPPORTUNITIES. MINT ACQUIRED BEIJING RIVERSIDE AT THE END OF 2012 WITH PLANS TO EXPAND BOTH IN ITS HOME COUNTRY, CHINA, AND POTENTIALLY INTO OTHER COUNTRIES.

22

Key Development

Basic Information

• Established in 2005

• Distinctive chain of casual-concept restaurants in China, specializing in Sichuan barbecue fish

• 21 restaurants across Beijing and Shanghai

Ownership

• Initial 49% stake, with MINT holding the majority of the Board seats

• Another 11-30% stake in Riverside in two years, subject to a performance hurdle

• The remaining shares of Riverside will continue to be held by the original founders

Investment Rationales

• China is a country of vast opportunities that arise from its rapidly growing middle class, accumulation of wealth, and increasing domestic consumption

• Riverside is already profitable, and therefore will bring in immediate earnings contribution to MINT

• Back office of the China operations will be combined for higher efficiency

• The acquisition will be a turning point MINT’s China food business operationally and financially in 2013

952

MINT RestaurantRevenues

100% ofRiverside

13,192

2012 Comparative Revenues

• Although contribution from Riverside is small initially, it is expected to become more meaningful as aggressive pace of growth is expected THB

Million

GROWING THAILAND RESTAURANT BUSINESS

THAILAND CONSUMPTION WILL CONTINUE TO GROW WITH THE EXPANSION OF THE MIDDLE CLASS, AS WELL AS URBANIZATION. MINT’S RESTAURANT BUSINESS WILL CONTINUE TO EXPAND WITH MALL OPERATORS.

23

34% 40%

2010 2020F

17% 41%

2009 2020F

+6pp

+24pp

Going Forward

Mid- to High Income Households % of Total

Urban Population % of Total Expansion of Mall Operators

Source: World Health Organization, National Statistical Office, Central Intelligence Agency

Key Strategies

Continue to expand outlets, in particular through franchise model in upcountry

Continue to improve efficiencies through distribution centers

Develop and expand new products

FURTHER GROWING RESTAURANT’S INTERNATIONAL BUSINESS

INTERNATIONAL BUSINESS CONTINUES TO BE A MAJOR PART OF MINT’S RESTAURANT BUSINESS. MINT WILL EXPAND PRIMARILY IN ITS MAJOR MARKETS – SINGAPORE, AUSTRALIA AND CHINA – AS WELL AS INTO OTHER COUNTRIES IN THE REGION.

24

Egypt

International Franchise China

Singapore Australia

Going Forward

Continue to grow existing markets

Expand into new markets including the Middle East and Indochina

Expand Riverside concept

Grow Sizzler while rationalize The Pizza Company

Selectively look for opportunities for Thai Express and The Coffee Club

Consolidate back office operations for efficiency

Expand Thai Express equity stores in Southeast Asia

Develop and introduce new concept under Thai Express Group

Continue the integration of Ribs and Rumps

Expand The Coffee Club franchise in the domestic Australian market

Internationalize The Coffee Club

Other Important Information

RETAIL TRADING

RETAIL TRADING BUSINESS SEES SIGNS OF IMPROVEMENT WITH STRONG SAME STORES SALE GROWTH IN THE FOURTH QUARTER OF 2012. MINT CONTINUES TO EXPAND ITS CURRENT BRAND PORTFOLIO, DESPITE THE CLOSING OF THREE COSMETICS BRANDS UPON EXPIRATION OF DISTRIBUTION CONTRACTS.

26

SSS & TSS

SSS & TSS - Quarterly

2011A Fashion Cosmetics Household 2012A

246

+20 -29

235

Number of Points of Sale

17.2%

52.8%

29.4%

-11.5% -6.8% -4.4% -10.1%

7.2%

21.0% 43.0%

26.0%

-4.0% 5.0%

23.0%

16.3%

24.2%

-20%

0%

20%

40%

60%

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

5.5%

-16.5%

14.4% 14.6%

-2.1%

9.0%

-17.0%

16.8% 18.9%

14.6%

-20%

-10%

0%

10%

20%

2008 2009 2010 2011 2012

-2

+6

+3

+2

+3

+2

+4

+3

-14

-12

-6

Three cosmetics brands have been closed

down during 2012 as distribution contracts

expired

Key Development

Comparable Sales Growth Total Store Sales Growth

SUSTAINABILITY PROGRAM

27

Focus on “Top Talent Development” across

Organization

Created Strategic CSR Platform around

Community Priorities that are Related to Our

Business:

• Education – English program at schools/ universities

• Hospitality Skills Development – top talent be assigned as trainer in the university

• Agriculture – support our farmers • Environment – manage the

environment impacts, especially at our hotel sites

MINT SEES SUSTAINABILITY AS A CRUCIAL PART OF ITS STRATEGY. THE GOAL IS TO DEVELOP FUTURE LEADERS TO SUSTAIN MINT’S SUCCESS AND IMPROVE COMMUNITIES’ AND THE COUNTRY’S HUMAN CAPITAL.

Going Forward

-

2.0

4.0

6.0

8.0

-

2,000

4,000

6,000

8,000

10,000

2012 2013F 2014F 2015F 2016F 2017F

28

CAPEX & BALANCE SHEET STRENGTH

IN ADDITION TO COMMITTED CAPEX, MINT ALSO SET ASIDE ADDITIONAL CAPEX FOR FUTURE ACQUISITIONS AND NEW INITIATIVES. WITH ITS BALANCE SHEET STRENGTH, MINT WILL BE ABLE TO FINANCE ITS CAPEX REQUIREMENTS.

Committed CAPEX & New Opportunities Leverage Ratios

X THB million

Additional CAPEX (non-committed average per annum) for New Opportunity/Acquisition(s)

Restaurant Hotel & Mixed-use Retail trading

EBITDA coverage on committed CAPEX

Going Forward

1.06

1.25

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Interest Bearing Debt to Equity

Net Interest Bearing Debt to Equity

Internal Policy

X

Interest Bearing Debt to Net Replacement Value

* Incremental capital increase from MINT W-4 exercise, assuming 100% MINT-W4 Conversion

THB million

Back-up Financing

0

10,000

20,000

30,000

40,000

50,000

Outstanding Borrowing &Equity

Un-Utilized Facility

Debt Debt

Shareholders’ Equity

Equity*

FIVE-YEAR ASPIRATIONS

29

22 hotels

676 restaurants

316 retail shops & POS

(14,524 Sqm)

2007

82 hotels

67 residences built to date

46 timeshare units

1,381 restaurants

235 retail shops & POS

(20,062 Sqm)

2012

> 140 hotels

> 200 residences built to date

> 400 timeshare units

> 2,700 restaurants

> 260 retail shops & POS

(>23,000 Sqm)

2017F

NPAT (THB) 1.6bn

1.6bn 3.4bn

Going Forward

MINT’S FIVE-YEAR STRATEGY 2013-2017

MINT’S FIVE-YEAR STRATEGY WAS FORMULATED MAINLY BASED ON THE FOLLOWING THREE KEY PILLARS, WITH CLEAR GOALS AS WELL AS MEASUREMENTS.

30

Going Forward

NPAT growth of ~15-20% CAGR ROIC of >15%

Growth Pillars

Measure-ments

Drive Profitable Portfolio of Own Brands

Continually Enhance Asset Productivity

Expand Internationally Through Strategic

Investments & Acquisitions

Asset-light

Model

Mixed-use

Initiatives

Total-system-sales growth of over 15%

Revenues growth

of over 10%

Improvement of margins

Revenues from overseas of over 40%

Net profit from overseas

of 50%

2017 Goals

Appendix

Anantara Sanya Resort And Spa, China

-

2,000

4,000

6,000

8,000

10,000

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Restaurant Hotel & Mixed-Use

Retail Trading Gain on Reclassification

32

4Q12 & 2012 Results 2012 REVENUE INCREASE OF 21%

THB million +21% YoY (Excl S&P Gain)

6,679

MINT REPORTED 2012 REVENUE INCREASE OF 21% YoY (EXCLUDING ONE-TIME GAIN), ATTRIBUTABLE TO STRONG PERFORMANCE OF HOTEL & MIXED-USE AND RESTAURANT BUSINESSES, FULL OPERATIONS OF ANANTARA KIHAVAH IN THE MALDIVES AND ST. REGIS HOTEL BANGKOK, INCREASED POPULARITY OF ANANTARA VACATION CLUB, TOGETHER WITH FULL YEAR CONSOLIDATION OF OAKS.

6,278

8,030

of Investment in S&P

7,345

8,768*

Restaurant 40%

Hotel & Mixed-Use

50%

Retail Trading

10%

7,524

* Note: Revenue of Anantara Vacation Club associated with the inventory unit transfer in 1Q12 of THB 80 million has been adjusted to conform with the figures in this period

-

10,000

20,000

30,000

40,000

2011 2012

32,993

+21% YoY (Excl S&P Gain)

28,332

THB million

Restaurant

Hotel & Mixed-Use

Retail Trading 7,842

6,976

Gain on reclassification of Investment in S&P

27,278

8,859

-400

-

400

800

1,200

1,600

2,000

2,400

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Restaurant Hotel & Mixed-Use

Retail Trading Gain on Reclassification

33

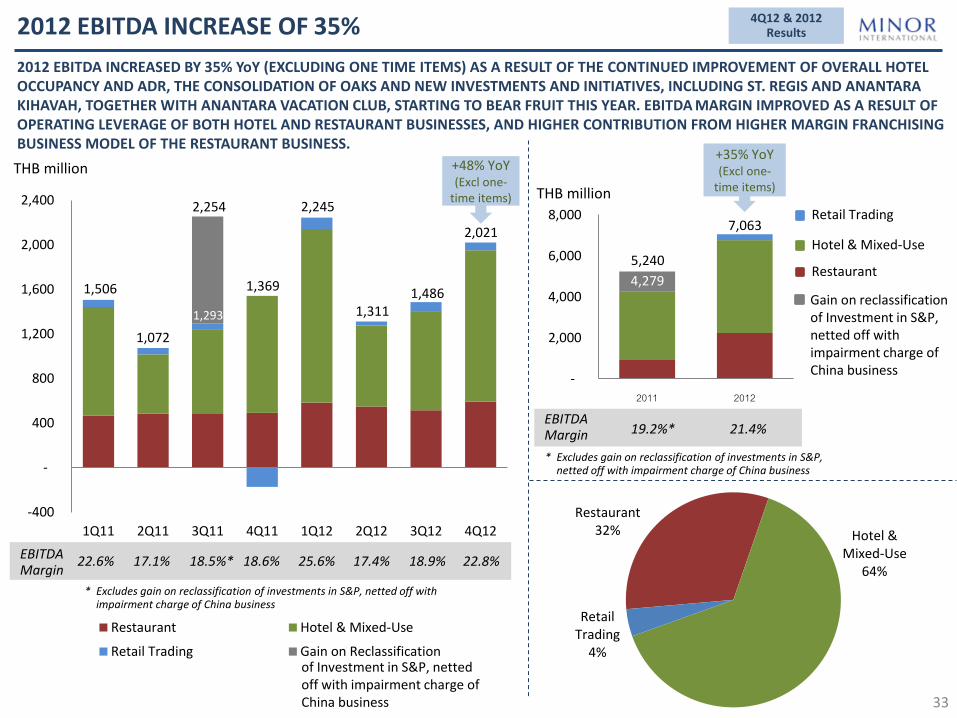

2012 EBITDA INCREASE OF 35%

2012 EBITDA INCREASED BY 35% YoY (EXCLUDING ONE TIME ITEMS) AS A RESULT OF THE CONTINUED IMPROVEMENT OF OVERALL HOTEL OCCUPANCY AND ADR, THE CONSOLIDATION OF OAKS AND NEW INVESTMENTS AND INITIATIVES, INCLUDING ST. REGIS AND ANANTARA KIHAVAH, TOGETHER WITH ANANTARA VACATION CLUB, STARTING TO BEAR FRUIT THIS YEAR. EBITDA MARGIN IMPROVED AS A RESULT OF OPERATING LEVERAGE OF BOTH HOTEL AND RESTAURANT BUSINESSES, AND HIGHER CONTRIBUTION FROM HIGHER MARGIN FRANCHISING BUSINESS MODEL OF THE RESTAURANT BUSINESS.

THB million

22.6% EBITDA Margin

1,506

1,072

+48% YoY (Excl one-

time items)

17.1% 18.5%*

* Excludes gain on reclassification of investments in S&P, netted off with impairment charge of China business

2,254

of Investment in S&P, netted off with impairment charge of China business

1,369

18.6%

2,245

25.6%

Restaurant 32% Hotel &

Mixed-Use 64%

Retail Trading

4%

4Q12 & 2012 Results

1,311

17.4%

-

2,000

4,000

6,000

8,000

2011 2012

7,063

5,240

+35% YoY (Excl one-

time items)

EBITDA Margin

THB million

19.2%* 21.4%

Restaurant

Hotel & Mixed-Use

Retail Trading

1,486

1,293

18.9%

4,279

* Excludes gain on reclassification of investments in S&P, netted off with impairment charge of China business

Gain on reclassification of Investment in S&P, netted off with impairment charge of China business

2,021

22.8%

-200

-

200

400

600

800

1,000

1,200

1,400

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Restaurant Hotel & Mixed-Use

Retail Trading Gain on Reclassification

34

2012 NET PROFIT INCREASE OF 78%

THB million

2012 NET PROFIT ROSE 78% YoY (EXCLUDING ONE TIME ITEMS) AS A RESULT OF IMPROVED PERFORMANCE OF ALL THREE BUSINESSES, TOGETHER WITH THE CONSOLIDATION OF OAKS. THE GROWTH RATE OF NET PROFIT EXCEEDED THAT OF REVENUE DUE TO THE IMPROVED PROFITABILITY OF HOTEL& MIXED-USE AND RESTAURANT BUSINESSES, WITH NET MARGIN EXPANDING TO 10.3% IN 2012.

823

12.3% Net Margin

280

4.5% 4.9%*

1,306

+151% YoY (Excl one-

time items)

472

6.4% 14.5%

1,276

Restaurant 35%

Hotel & Mixed-Use

61%

Retail Trading

4%

4Q12 & 2012 Results

364

4.8%

-1,000

-

1,000

2,000

3,000

4,000

2011 2012

Net Margin 10.3% 7.0%*

THB million

+78% YoY (Excl one-time items

2,880 3,409

345

585

7.5%

* Excludes gain on reclassification of investments in S&P, netted off with impairment charge of China business

of Investment in S&P, netted off with impairment charge of China business

1,919

Restaurant

Hotel & Mixed-Use

Retail Trading

Gain on reclassification of Investment in S&P, netted off with impairment charge of China business

* Excludes gain on reclassification of investments in S&P, netted off with impairment charge of China business

1,184

13.4%

35

FINANCIAL PERFORMANCE – HOTEL & MIXED-USE Hotel Updates

Revenue

EBITDA

NPAT

EBITDA Margin

Net Margin

1Q11

THB million

2,876 2,598

3,308 3,875

4,527

3,480 3,834

4,549

975

533 755

1,050

1,559

726 890

1,360

33.9%

586

38 101

433

881

90 273

841

20.4%

2012 REVENUE AND PROFIT FROM HOTEL & MIXED-USE BUSINESS CONTINUED TO SEE IMPRESSIVE GROWTH YoY WITH IMPROVED MARGINS.

20.5%

1.5%

2Q11

2012 overall occupancy & ADR of MINT’s hotel portfolio improved YoY, due to the uninterrupted favorable climate, together with MINT’s continued marketing effort, throughout the year;

The new Anantara Kihavah and St. Regis Bangkok, which reported losses during start-up stage, saw considerable increase in occupancy, helping both top line and the profitability of the hotel portfolio;

Consolidation of Oaks’ performance since June 2011 was another main contribution, while post-acquisition plan is on track;

Sales of Anantara Vacation Club is becoming a meaningful contribution to MINT’s real estates business, with the business becoming profitable in 2012;

Even excluding Oaks, performance of MINT’s hotel & mixed use business continued to improve, with 2012 revenue increase of 16% and EBITDA increase of 27% YoY.

Key Highlights

22.8%

3.0%

3Q11 4Q11

27.1%

11.2%

1Q12

+17% YoY

34.4%

19.5%

16,390

12,657

3,313

4,535

1,157

2,085

2011 2012

20.9%

9.1% 17.6%

+30% YoY

+94% YoY

2.6%

2Q12

+29% YoY

+37% YoY

+80% YoY

26.2% 28.3%

4Q12

23.2%

18.5%

29.9%

7.1%

3Q12

36

HOTEL PERFORMANCE – 4Q12

Systemwide

Organic

Hotel ARR (Bt/night)

4Q12 4Q11 Chg 4Q12 4Q11 %Chg 4Q12 4Q11 Chg

Anantara 60% 58% 3% 6,906 7,239 -5% 4,167 4,178 0%

Marriott 83% 65% 18% 4,359 4,029 8% 3,607 2,614 38%

Four Seasons 71% 42% 29% 9,068 9,970 -9% 6,426 4,197 53%

Oaks 77% 79% -2% 5,071 4,880 4% 3,917 3,856 2%

Others 58% 44% 14% 5,983 5,302 13% 3,449 2,335 48%

Average

(incl. Oaks) 71% 68% 3% 5,740 5,483 5% 4,075 3,737 9%

Average

(excl. Oaks) 64% 56% 9% 6,476 6,456 0% 4,171 3,602 16%

Avg - Thailand 70% 54% 16% 5,029 4,808 5% 3,517 2,595 36%

Avg - Overseas

(incl. Oaks) 72% 76% -5% 6,083 5,754 6% 4,350 4,384 -1%

Avg - Overseas

(excl. Oaks) 53% 62% -9% 10,470 11,366 -8% 5,539 7,044 -21%

Occupancy (%) RevPar (Bt/night)

Hotel ARR (Bt/night)

4Q12 4Q11 Chg 4Q12 4Q11 %Chg 4Q12 4Q11 Chg

Anantara 64% 58% 6% 6,926 7,239 -4% 4,427 4,178 6%

Marriott 83% 65% 18% 4,359 4,029 8% 3,607 2,614 38%

Four Seasons 71% 42% 29% 9,068 9,970 -9% 6,426 4,197 53%

Oaks 77% 79% -2% 5,071 4,880 4% 3,917 3,856 2%

Others 57% 44% 13% 6,253 5,302 18% 3,553 2,335 52%

Average

(incl. Oaks) 73% 68% 4% 5,726 5,483 4% 4,160 3,737 11%

Average

(excl. Oaks) 67% 56% 11% 6,514 6,456 1% 4,372 3,602 21%

Avg - Thailand 70% 54% 16% 5,029 4,808 5% 3,517 2,595 36%

Avg - Overseas

(incl. Oaks) 74% 76% -2% 6,083 5,754 6% 4,508 4,384 3%

Avg - Overseas

(excl. Oaks) 58% 62% -4% 12,654 11,366 11% 7,283 7,044 3%

Occupancy (%) RevPar (Bt/night)

Hotel Updates

37

HOTEL PERFORMANCE – 2012

Systemwide

Organic

Hotel ARR (Bt/night)

2012 2011 Chg 2012 2011 %Chg 2012 2011 Chg

Anantara 57% 52% 6% 6,554 6,829 -4% 3,752 3,526 6%

Marriott 75% 67% 8% 4,047 3,643 11% 3,050 2,450 25%

Four Seasons 64% 50% 14% 8,455 8,660 -2% 5,374 4,325 24%

Oaks 77% 79% -2% 5,138 4,977 3% 3,945 3,917 1%

Others 55% 45% 10% 6,075 4,925 23% 3,315 2,193 51%

Average

(incl. Oaks) 69% 65% 5% 5,589 5,385 4% 3,871 3,479 11%

Average

(excl. Oaks) 61% 55% 6% 6,196 5,772 7% 3,769 3,186 18%

Avg - Thailand 65% 56% 9% 4,819 4,640 4% 3,126 2,575 21%

Avg - Overseas

(incl. Oaks) 72% 73% -1% 5,960 5,882 1% 4,268 4,267 0%

Avg - Overseas

(excl. Oaks) 49% 54% -5% 11,265 9,809 15% 5,574 5,311 5%

Occupancy (%) RevPar (Bt/night)

Hotel ARR (Bt/night)

2012 2011 Chg 2012 2011 %Chg 2012 2011 Chg

Marriott 60% 52% 8% 6,564 6,829 -4% 3,908 3,526 11%

Anantara 75% 67% 8% 4,047 3,643 11% 3,050 2,450 25%

Four Seasons 64% 50% 14% 8,455 8,660 -2% 5,374 4,325 24%

Oaks 77% 79% -2% 5,138 4,977 3% 3,945 3,917 1%

Other 54% 45% 9% 6,164 4,925 25% 3,327 2,193 52%

Average

(incl. Oaks) 70% 65% 6% 5,584 5,385 4% 3,919 3,479 13%

Average

(excl. Oaks) 62% 55% 7% 6,204 5,772 7% 3,867 3,186 21%62% 55%

Avg - Thailand 65% 56% 9% 4,819 4,640 4% 3,126 2,575 21%

Avg - Overseas

(incl. Oaks) 73% 73% 1% 5,960 5,882 1% 4,358 4,267 2%

Avg - Overseas

(excl. Oaks) 53% 54% -1% 12,162 9,809 24% 6,487 5,311 22%

Occupancy (%) RevPar (Bt/night)

Hotel Updates

MINT’S COMPOSITION OF HOTEL ROOMS ARE EXPECTED TO CHANGE OVER THE NEXT FIVE YEARS. MINT WILL FOCUS ON THE EXPANSION OF OUR OWN BRANDS, ANANTARA AND OAKS, MORE EXPONENTIALLY THROUGH ASSET LIGHT MODEL (MANAGEMENT CONTRACTS), WITH GEOGRAPHICAL FOCUS OUTSIDE OF THAILAND.

MINT’S HOTEL PORTFOLIO

No of rooms

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2005 2012 2017F

Others Oaks

Avani Anantara

Four Seasons Marriott

2,169

14,573

55% 5% 4%

20%

26%

3%

19%

51%

35%

6%

8% 45%

6%

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2005 2012 2017F

Managed

Joint Venture

Own Equity

92% 23% 22% 8%

7% 5%

70%

73%

2,169

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2005 2012 2017F

International

Outside Bangkok

Bangkok

36% 15% 12% 56%

15% 11%

8%

70% 76%

2,169

By Location By Ownership By Brand

38

5%

10,348

7%

5%

14,573

10,348

14,573

10,348

Hotel Updates

No of rooms No of rooms

-10%

0%

10%

20%

30%

0

5

10

15

20

25

30

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013F

Tourist Arrival % Change

HOTEL INDUSTRY OUTLOOK IS EXPECTED TO REMAIN STRONG ON THE BACK OF INCREASING TOURIST ARRIVAL.

Million Tourists Arrival to Thailand – Yearly Trend

Source: Tourism Authority of Thailand and Bank of Thailand

TOURIST ARRIVAL TO THAILAND

Million Tourist Arrival to Thailand – Monthly Trend

39

-40%

-20%

0%

20%

40%

60%

80%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12

Hotel Updates

0

1,000,000

2,000,000

3,000,000

China Japan Russia Korea India

2011 2012

0

100,000

200,000

300,000

400,000

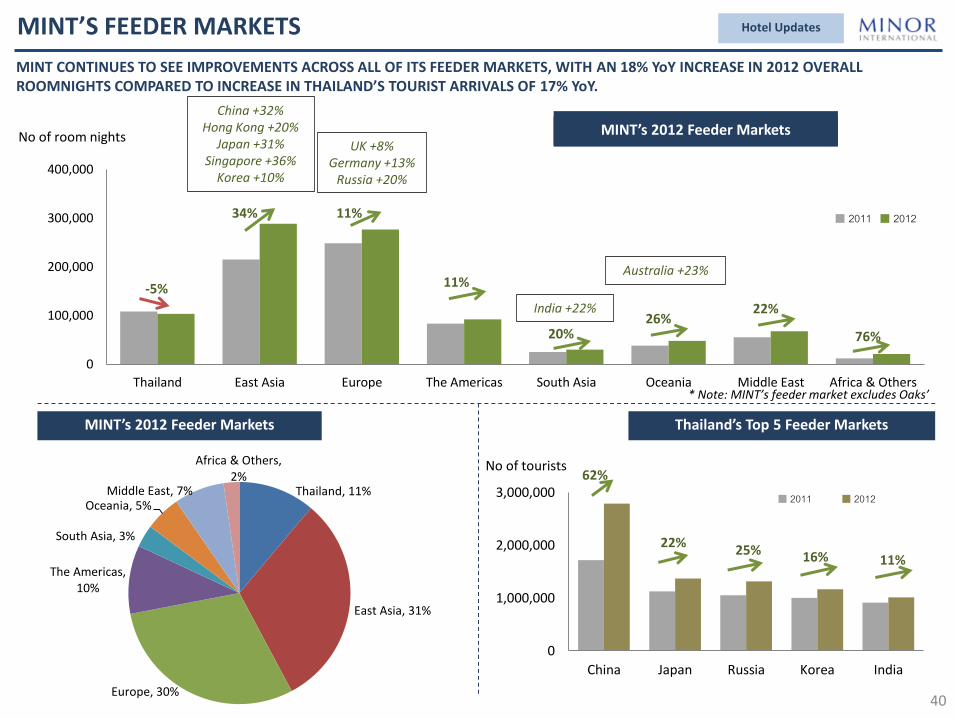

Thailand East Asia Europe The Americas South Asia Oceania Middle East Africa & Others

2011 2012

MINT’S FEEDER MARKETS

No of room nights

MINT’s 2012 Feeder Markets Thailand’s Top 5 Feeder Markets

No of tourists

MINT’s 1H12 Feeder Markets

* Note: MINT’s feeder market excludes Oaks’

40

Hotel Updates

-5%

34% 11%

11%

20% 26%

MINT’s 2012 Feeder Markets

76%

22%

MINT CONTINUES TO SEE IMPROVEMENTS ACROSS ALL OF ITS FEEDER MARKETS, WITH AN 18% YoY INCREASE IN 2012 OVERALL ROOMNIGHTS COMPARED TO INCREASE IN THAILAND’S TOURIST ARRIVALS OF 17% YoY.

China +32% Hong Kong +20%

Japan +31% Singapore +36%

Korea +10%

UK +8% Germany +13%

Russia +20%

Australia +23%

India +22%

62%

22% 25% 16% 11%

Thailand, 11%

East Asia, 31%

Europe, 30%

The Americas, 10%

South Asia, 3%

Oceania, 5% Middle East, 7%

Africa & Others, 2%

Hotel Updates

BANGKOK HAS SEEN AGGRESSIVE INCREASE IN NEW SUPPLY DURING 2010 – 2012, BUT THE RATE IS EXPECTED TO SLOW DOWN IN THE NEXT FEW YEARS.

0

5,000

10,000

15,000

20,000

2000 2001 2002 200 200 200 200 200 2008 2009 2010 2011 2012 201 201

No of rooms

Source: HVS Reseach

2012 No. of Rooms

Sofitel Bangkok, Sukhumvit 13

W Hotel Bangkok

Hotel Okura Bangkok

Hansar Bangkok

Hotel Sofitel So Bangkok

The Siam, Bangkok

Surya by Supatra

344

403

240

94

238

39

68

2013F

The Langham Sukhumvit Bangkok

Langham Place, Phayathai, Bangkok

230

400

No. of Rooms

LUXURY HOTEL SUPPLY IN BANGKOK

2014F

41

Jumeirah Bangkok

Park Hyatt Bangkok

305

222

DIVERSIFICATION OUTSIDE BANGKOK

WITH ITS EXPANSION OUTSIDE OF THAILAND AS WELL AS INCREASING CONTRIBUTION FROM MIXED USE BUSINESSES, MINT IS LESS DEPENDENT ON ITS BANGKOK HOTEL PORTFOLIO. NEVERTHELESS, DESPITE THE OVERSUPPLY OF HOTELS IN BANGKOK, MINT’S BANGKOK HOTEL PORTFOLIO IS STILL SEEING SIGNIFICANT IMPROVEMENT IN REVPAR OF 40% YoY.

42

Hotel Updates

25% 24% 32% 16% 15%

75% 76% 68% 84% 85%

0%

25%

50%

75%

100%

2008 2009 2010 2011 2012

Outside Bangkok

Bangkok

Number of hotel rooms in Bangkok doubled over the past 5 years

26% 28% 25% 14% 14%

74% 72% 75% 86% 86%

0%

25%

50%

75%

100%

2008 2009 2010 2011 2012

Other Hotel &Mixed Use

Bangkok

5,097

4,255 3,951

3,542 3,857

3,389

2,394 2,025 1,788

2,499

66%

56%

51% 51%

65%

0%

20%

40%

60%

80%

0

2,000

4,000

6,000

8,000

2008 2009 2010 2011 2012

0

300

600

900

1,200

1,500

2008 2009 2010 2011 2012

Managed

Owned

No of rooms

Revpar ADR % Occupancy

769 864

1,300

1,518 1,518

However, the contribution in terms of number of rooms in Bangkok significantly declined as the expansion is faster outside of Bangkok

Despite the oversupply of hotels in Bangkok, MINT’s Bangkok hotel portfolio improves significantly, with 2012 revpar increase of 40% YoY

The revenue contribution also significantly declined over the five years, in line with the contribution from number of rooms

THB Occupancy

872

1,173

1,923 2,238

43

2012 PERFORMANCE OF THE RESTAURANT BUSINESS CONTINUED TO EXHIBIT STRONG AND STABLE GROWTH, WITH REVENUE GROWTH OF 13% AND NET PROFIT GROWTH OF 35% YoY

FINANCIAL PERFORMANCE - RESTAURANT

Revenue

EBITDA

NPAT

EBITDA Margin

Net Margin

1Q11

THB million

2,963 2,901 2,880 2,954

3,451

3,237 3,097

3,406

467 483 481 492 583

549 515 592

15.8%

205 218 224 225

319 273 276 306

6.9%

Key Highlights

Most brands continued to exhibit strong and positive same store sales growth in 2012, from increases in both revenue per customer and customer count. The increase were mainly due to a combination of robust domestic consumption and successful marketing strategies;

Same store sales growth, together with outlet expansion, translated into strong total system sales growth of 15.1% in 2012;

The full consolidation of Thai Express’ performance, the 31% share of profit in S&P Syndicate and higher franchise fees, helped improve the restaurant business’s margin;

EBITDA & net profit margin expanded despite the minimum wage increase which was implemented since October 2011, attributable to improved cost structure, operating leverage and increasing franchise fees.

Restaurant Update

16.6%

2Q11

7.5%

16.7%

3Q11*

7.8%

4Q11

16.6%

7.6%

1Q12

9.2%

+13% YoY

+16% YoY

+35% YoY

16.9%

+15% YoY

+20% YoY

+20% YoY

17.0%

2Q12

8.4%

16.4% 17.0%

2011*

7.0%

2012

10.3%

16.6%

3Q12

8.9%

*Note: Excluding gain on reclassification of Investment in S&P, netted off with impairment charge of China business

9.0%

4Q12

17.4%

11,697 13,192

44

FOOD AND PAPER COSTS AS A PERCENTAGE OF SALES HAS COME DOWN OVER THE PAST FIVE YEARS AS A RESULT OF CONTINUED EFFECTIVE COST MANAGEMENT PROGRAM.

EFFECTIVE MANAGEMENT OF FOOD COSTS

35.9%

34.1%

34.9% 35.2% 35.2%

33.3%

33.0%

33.9%

34.5%

33.2% 33.2% 33.0%

34.0%

32.7%

31.8% 31.7%

32.0%

31.5%

31.7%

31.5% 31%

32%

33%

34%

35%

36%

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

% of Food & Paper Costs to Sales

Fixed Long-Term Contract

Prices

Menu-Mix Re-Engineering

Supply Chain Management

Maximization of FTA Benefit

Pro-Active Inventory

Management

Strategy

Note: Food and paper costs as a percentage of sales rose in first quarter of every year as a result of “Buy-one-get-one-free” promotional campaign launched in March of every year to celebrate the anniversary of The Pizza Company

Restaurant Update

45

RESTAURANT PERFORMANCE

Brand SSS (%) TSS (%)

4Q12 4Q11 2012 2011 4Q12 4Q11 2012 2011

The Pizza Company -0.8% 11.3% 5.9% 11.7% 4.2% 18.2% 14.6% 15.6%

Swensen’s 14.2% -0.3% 10.7% 3.6% 22.2% 8.6% 18.9% 11.8%

Sizzler 14.6% 5.0% 6.1% 11.8% 12.6% 8.3% 7.0% 14.5%

Dairy Queen 9.1% 20.7% 17.5% 16.7% 27.5% 30.8% 30.2% 23.8%

Burger King 18.2% 16.9% 10.2% 21.8% 19.5% 6.9% 10.8% 17.1%

The Coffee Club 2.3% 5.5% 3.1% 8.8% 8.7% 13.7% 10.3% 15.8%

Ribs & Rumps -0.8% N/A -0.5% N/A 46.5% N/A 270.7% N/A

Thai Express 1.8% -3.7% -0.4% -1.6% 4.2% -0.3% 5.2% 0.9%

Average 4.6% 6.5% 5.5% 9.0% 11.4% 12.7% 15.1% 14.1%

Average Thailand 7.5% 9.3% 8.6% 11.8% 13.8% 15.3% 15.9% 16.9%

Restaurant Update

RESTAURANT OUTLETS – 2012

Brand No. of outlets No. of outlets

Total Equity Franchise Thailand International

The Pizza Company 198 94 255 37 292

Swensen’s 124 157 259 22 281

Sizzler 45 - 39 6 45

Dairy Queen 237 72 309 - 309

Burger King 29 - 29 - 29

The Coffee Club 26 287 8 305 313

Ribs & Rumbs 9 3 - 12 12

Thai Express 56 8 - 64 64

Riverside 21 - - 21 21

Others 15 - 15 - 15

Total 760 621 914 467 1,381

46

Restaurant Update

267 562 487

683 751 1,097

1,097

46

55

(131)

61

1,054

1,054 1,054

4.8%

19.0% 20.8% 22.9%

26.3%

31.3% 31.3%

-10%

0%

10%

20%

30%

40%

-500

0

500

1,000

1,500

2,000

2,500

3,000

2006 2007 2008 2009 2010 2011 2012

Gain from investment reclassification

Unrealized gain (loss)

Investment Cost

% shareholding

47

S&P OPERATES A CHAIN OF RESTAURANTS AND BAKERY SHOPS WITH OVER 400 OUTLETS IN 7 COUNTRIES PRODUCING AND DISTRIBUTING FOOD AND BAKERY PRODUCTS UNDER THE S&P BRAND. SINCE 3Q11, S&P’S PERFORMANCE HAS BEEN RECOGNIZED THROUGH EQUITY ACCOUNTING METHOD. 2012 REVENUES INCREASED AS A RESULT OF BOTH DOMESTIC AND INTERNATIONAL EXPANSION, WHILE MARGINS IMPROVED BECAUSE OF INCREASE IN RETAIL PRICE, EFFICIENT PROCUREMENT AND LOWER MARKETING EXPENSES.

CONTINUED & STRENGTHENING PARTNERSHIP WITH S&P

Shareholding Structure

MINT’s Investment in S&P

THB million

313

617 744

1,805

Revenue

EBITDA

NPAT

EBITDA Margin

Net Margin

THB million

2,151

356 617

2010 2008 2009

4,437 4,761 5,340

5,941 6,653

583 674 817

962

1,216

13.1% 14.2% 15.3%

225 293 383 454

708

5.1% 6.2% 7.2%

16.2%

7.6%

2011

39% 39%

26% 31%

35% 30%

0%

20%

40%

60%

80%

100%

Pre-Tender Offer Post-Tender Offer

Others

MINT

Sila-on & Riva Families

5%

+12% YoY

+26% YoY

+56% YoY 2,151

Restaurant Update

18.3%

10.6%

2012

4

289

2,923

3,412

48

Retail Trading Update

2012 REVENUE OF RETAIL TRADING & CONTRACT MANUFACTURING INCREASED BY 17% PRIMARILY AS A RESULT OF EXPANSION OF KEY FASHION BRANDS ESPECIALLY IN 4Q12, INCREASE IN ORDERS OF CONTRACT MANUFACTURING, TOGETHER WITH INSURANCE CLAIMS FROM FLOOD RECEIVED IN 1Q12 AND 3Q12. AS A RESULT, EBITDA AND NET PROFIT INCREASED SIGNIFICANTLY IN 2012.

FINANCIAL PERFORMANCE – RETAIL TRADING & CONTRACT MANUFACTURING

Revenue

EBITDA

NPAT

EBITDA Margin

Net Margin

1Q11

THB million 840

779 789

516

789 807 911 905

64 57 56

-173

103

36 81 69

7.6%

32 23 21

-186

76

1 36 37

3.8%

Key Highlights

7.3%

2Q11

3.0%

13.1%

9.6%

7.2%

2.6%

3Q11

2012 revenue from retail trading increased by 16% YoY, primarily from the expansion of points of sale of the key fashion brands, despite the decline in number of cosmetic points of sale. Retail trading is seeing a turn around with same store sales growth turning positive in 4Q12;

2012 revenue from contract manufacturing increased by 18% YoY, from partial recovery of insurance claim in 1Q12 and 3Q12, together with increased order since its full operation in mid-2012;

As a result, EBITDA and net profit margins of retail trading & contract manufacturing business increased significantly in 2012;

-33.5%

4Q11

-36.2%

1Q12

+17% YoY

N/A

+75% YoY

4.5%

0.2%

2Q12

0.1% 8.5%

-3.8%

2011

4.4%

2012

8.9%

3.9%

3Q12

7.6%

4.1%

4Q12

-110

N/A

N/A

N/A 150