companies act today - ca 2013 todays’ topic at west study circle anniversary of wsc of sirc icsi a...

TRANSCRIPT

BOARDS’ REPORTFOR

LISTED COMPANIES

Companies Act Today - CA 2013

TODAYS’ TOPIC AT WEST STUDY CIRCLE

Anniversary of WSC of SIRC ICSI A Workshop on Disclosures of Boards’ Report of Listed Companies is organied by the WSC of SIRC, ICSI. The Presentation is more specific to Listed Companies, the main difference between the CA, 2013 and the Listing Agreement requirements, how there is an overlap of information required, details of policies, disclosures of the Internal audit control, Related Party Transaction , Directors, their appointment, remuneration etc., Duties of Auditors, Secretarial Auditors etc….

The Topic is addressed by Mr. P.Sriram and Mr. Eswar, Practicing Company Secretaries, Chennai. Today being the 3rd Anniversary of West Study Circle, lot and lot more of interesting events are also organized by the members of WSC.

It is to be noted that Mr. Mohan, Convener has recently contested and won the election of the SIRC, ICSI and his contributions to the CS Circle is continuing and remarkable. Sources report that Mr, Palaniappan, Deputy Convener will be designated as the Convener of WSC.

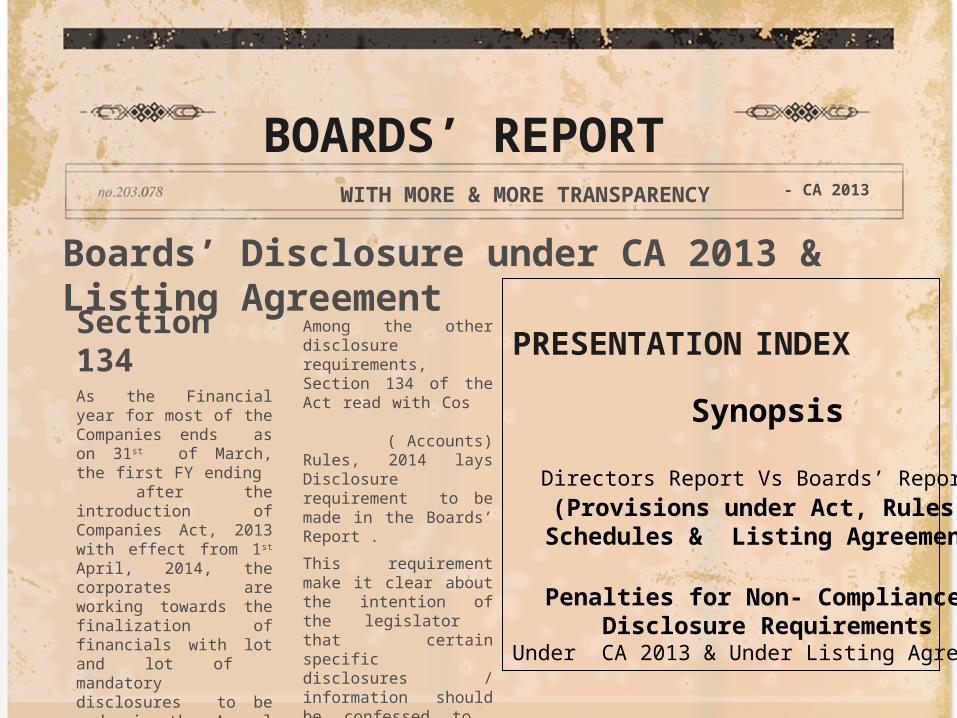

BOARDS’ REPORT WITH MORE & MORE TRANSPARENCY - CA 2013

Boards’ Disclosure under CA 2013 & Listing Agreement

PRESENTATION INDEX

Synopsis

Directors Report Vs Boards’ Report (Provisions under Act, Rules,

Schedules & Listing Agreement)

Penalties for Non- Compliances Disclosure Requirements

Under CA 2013 & Under Listing Agreement

Section 134As the Financial year for most of the Companies ends as on 31st of March, the first FY ending after the introduction of Companies Act, 2013 with effect from 1st April, 2014, the corporates are working towards the finalization of financials with lot and lot of mandatory disclosures to be made in the Annual Report.

With the increased level of compliances and higher transparency, the CA 2013 mandates certain disclosures to be made in the Annual Report .

Among the other disclosure requirements, Section 134 of the Act read with Cos ( Accounts) Rules, 2014 lays Disclosure requirement to be made in the Boards’ Report .

This requirement make it clear about the intention of the legislator that certain specific disclosures / information should be confessed to the stakeholders/ authorities from the Horse mouth , the Board of Directors of the Company. (To read the full coverage .. Lets’ go to the the presentation)

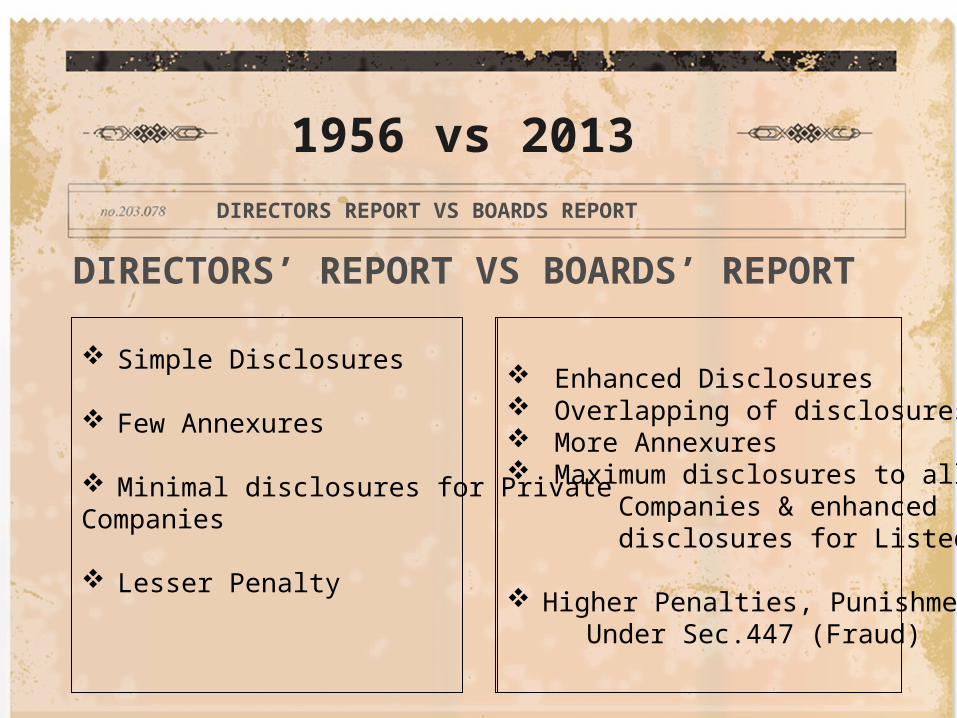

DIRECTORS’ REPORT VS BOARDS’ REPORT

Simple Disclosures

Few Annexures

Minimal disclosures for PrivateCompanies

Lesser Penalty

1956 vs 2013DIRECTORS REPORT VS BOARDS REPORT

Enhanced Disclosures Overlapping of disclosures More Annexures Maximum disclosures to all Companies & enhanced disclosures for Listed Companies.

Higher Penalties, Punishment Under Sec.447 (Fraud)

5

DISCLOSURE BOARDS' REPORT

SECTION 134 & COMPANIES (ACCOUNTS) RULES, 2014

VARIOUS OTHER

SECTIONS OF CA 2013

DISCLOSURES UNDER OTHER

STATUTES

LISTING AGREEMENT

SECRETARIAL STANDARDS

SCHEDULES UNDER CA

2013

VARIOUS OTHER RULES

UNDER CA 2013

6

Boards Report - New Avatar

More Disclosures

& Annexures

Internal Financial Controls /

compliance of all laws

RPT/ Details of contracts

Details about the Policies

Reply to Qualification of Secretarial

Auditor

Details about Directors, their Remuneration, Performance Evaluation

7

SIGNATORIES TO BOARDS’ REPORT

SIGNATORIES TO BOARDS

REPORT

• CHAIRMAN OF THE COMPANY AND

• MANAGING DIRECTOR, (if any ) OR

• TWO DIRECTORS

8

PENALTY FOR NON COMPLIANCE

9

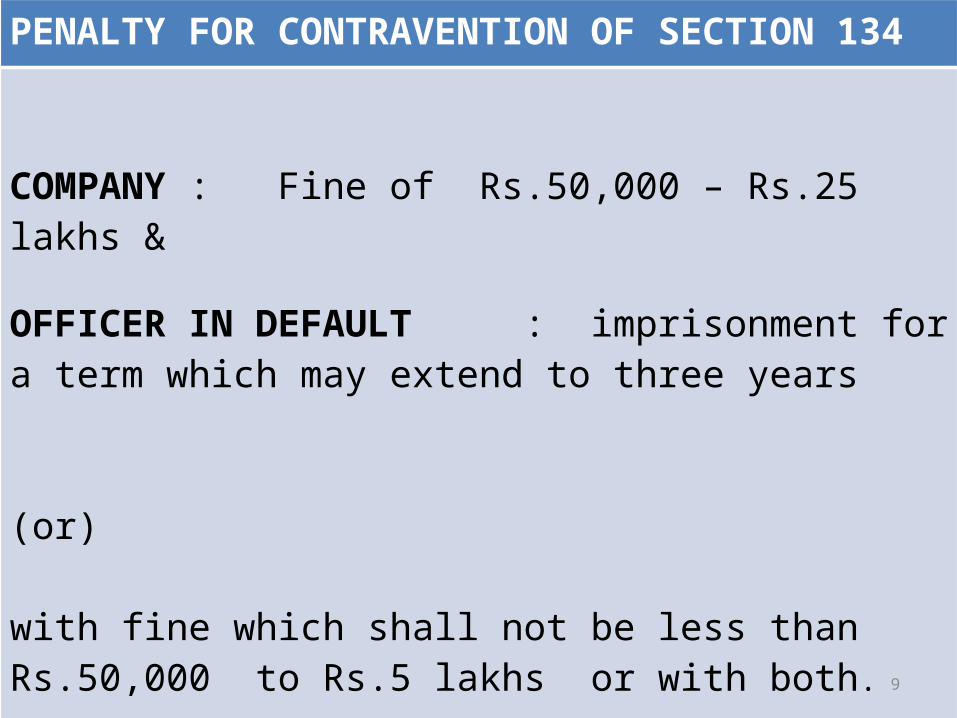

PENALTY FOR CONTRAVENTION OF SECTION 134

COMPANY : Fine of Rs.50,000 – Rs.25 lakhs & OFFICER IN DEFAULT : imprisonment for a term which may extend to three years

(or)

with fine which shall not be less than Rs.50,000 to Rs.5 lakhs or with both.

10

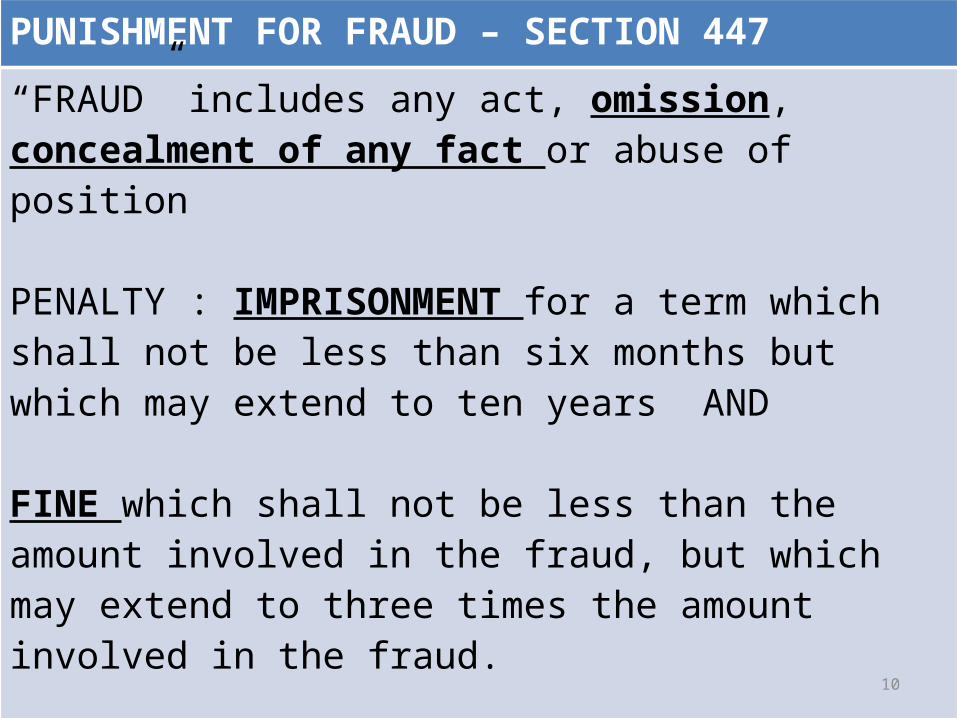

PUNISHMENT FOR FRAUD – SECTION 447

“FRAUD” includes any act, omission, concealment of any fact or abuse of position

PENALTY : IMPRISONMENT for a term which shall not be less than six months but which may extend to ten years AND

FINE which shall not be less than the amount involved in the fraud, but which may extend to three times the amount involved in the fraud.

CLASS ACTION SUIT ????

11

PENALTY UNDER LISTING AGREEMENT

SECTION 21 READ WITH 23A OF SECUTIRIES CONTRACT (REGULATION) ACT, 1956 (SCRA)

PENALTY FOR NON –COMPLIANCE/ NON FURNISHING/ NON MAINTAINING OF RECORDS – FINE OF RS. 1 LAKH FOR EACH DAY TILL SUCH FAILURE OR RS. 1 CRORE WHICH EVER IS LESS

12

VARIOUS (NUMEROUS) DISCLOSURE

IN BOARDS’ REPORT

13

DISCLOSURES PURSUANT TO SECTION 134 (3) (a) – Extract of Annual Return

Registered office address/Principal business activities along with % to total turnover of the CompanyParticulars of its holding, subsidiary and associate companies.Details of issued , subscribed and paid up share capital along with changes therein since the close of the previous financial year)

Details of non-convertible , partly convertible, fully convertible debentures

Details of premium of equity shares and other securities along with changes

Total turnover and net worth Shareholding pattern.

Category wise shareholding with details of holding in physical and de-mat

14

DISCLOSURES PURSUANT TO SECTION 134 (3) (A) – EXTRACT OF ANNUAL RETURN

Shareholding of promoters with details of shares pledged

Change in promoters shareholding

Shareholding pattern of top 10 shareholders along with change

Shareholding of directors and key managerial personnelIndebtedness along with changes if any and interest details

Details of members, debenture and other security holders along with changes therein since the close of the previous financial year……..

15

DISCLOSURES PURSUANT TO SECTION 134 (3) (A) – EXTRACT OF ANNUAL RETURN

Details of attendance of all directors in board and committee meetings

Details of remuneration of whole-time & managing directors, manager and key managerial personnel in terms of Salary & perquisites/ Commission

Stock option and sweat equity

Details of remuneration of other directors in terms of Sitting fees commission

Details of penalty or punishment imposed on the company, its directors or officers and details of compounding of offences and appeals made against such penalty or punishment under Companies Act;

16

DISCLOSURES PURSUANT TO SECTION 134 (3) (A) – EXTRACT OF ANNUAL RETURN

Details of events in respect of which company was liable to file return or comply with requisite provisions of the Act

Disclosures in respect of following:

Closure of registers

Declaration of dividend

Delisting of shares/securities

Particulars of inter-corporate loans and investment

17

DISCLOSURES PURSUANT TO SECTION 134 (3) (A) – EXTRACT OF ANNUAL RETURN

Related party transactions in AOC-2

Resolutions passed by postal ballot

Furnishing of necessary information and declaration by the directors

Details in respect of shares held by or on behalf of the Foreign Institutional Investors

Amount spent on Corporate Social Responsibility

Limits under sections 186 i.e. Loan and investment by company and section 180 (1)(c) i.e. Restrictions on powers of board

18

DIRECTORS RESPONSIBILITY STATEMENT !!!!!SECTION 134 (3) (c) & 134 (5) (e)

19

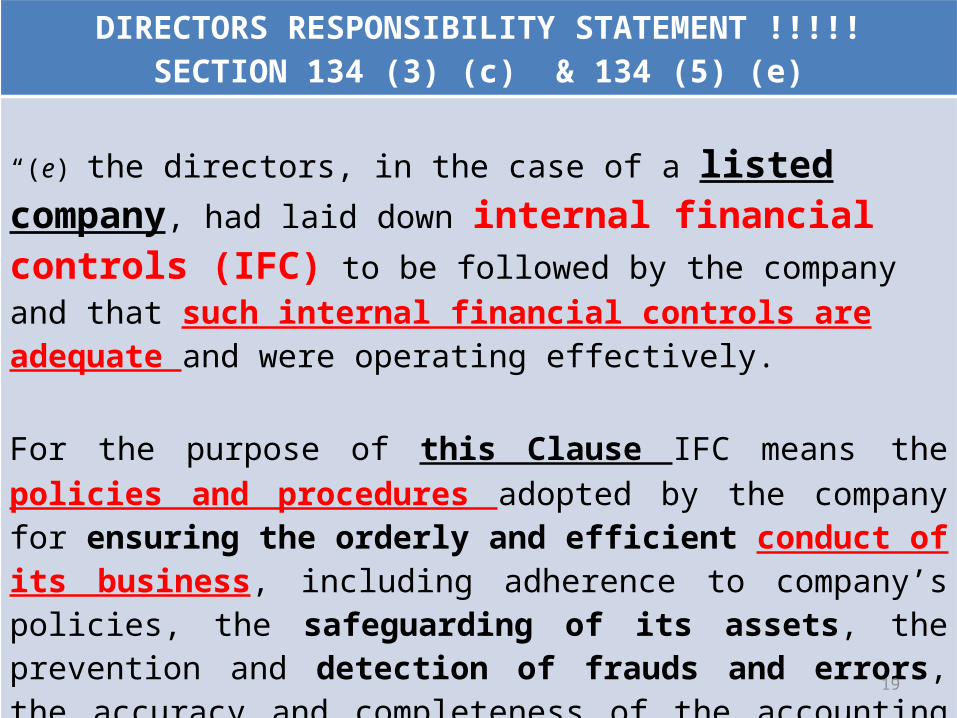

DIRECTORS RESPONSIBILITY STATEMENT !!!!!SECTION 134 (3) (c) & 134 (5) (e)

“(e) the directors, in the case of a listed company, had laid down internal financial controls (IFC) to be followed by the company and that such internal financial controls are adequate and were operating effectively.

For the purpose of this Clause IFC means the policies and procedures adopted by the company for ensuring the orderly and efficient conduct of its business, including adherence to company’s policies, the safeguarding of its assets, the prevention and detection of frauds and errors, the accuracy and completeness of the accounting records, and the timely preparation of reliable financial information. RULE 8(viii) OF THE COMPANIES (ACCOUNTS) RULES 2014 - the details in respect of adequacy of internal financial controls with reference to the Financial Statements.

20

About INTERNAL FINANCIAL CONTROLOn Companies Act 2013

SECTION 143 (3) (i) – Auditor to report on adequacy of Internal financial control system are in place and operating effectiveness of such control .

SECTION 143(12) - The provisions of this section shall mutatis mutandis apply to PCS while conducting Secretarial Audit under Section 204

LISTING AGREEMENT : Clause 49 – Role of Audit Committee to evaluate internal financial controls and risk management systems .

Clause 49 (VIII) (D) – MD & A requires discussion on internal financial controls.

21

DIRECTORS RESPONSIBILITY STATEMENT – SECTION 134 (3) (c) & 134 (5) (f)(f) the directors had devised proper systems to ensure compliance with the provisions of all applicable laws and that such systems were adequate and operating effectively.

LISTING AGREEMENT – CLAUSE 49 (I) The Board shall periodically review compliance reports of all laws applicable to the company, prepared by the company as well as steps taken by the company to rectify instances of non-compliances.

SECTION 205 - CS to report to the Board about the compliance with the provisions of all other laws applicable to the Company.

SECTION 204 / Form MR-3 “ I Further report that there are adequate systems and processes in the Co, commensurate with the size and operations of the Co., to monitor and ensure compliance with applicable laws , rules, regulations, guidelines.

22

23

POLICIES

24

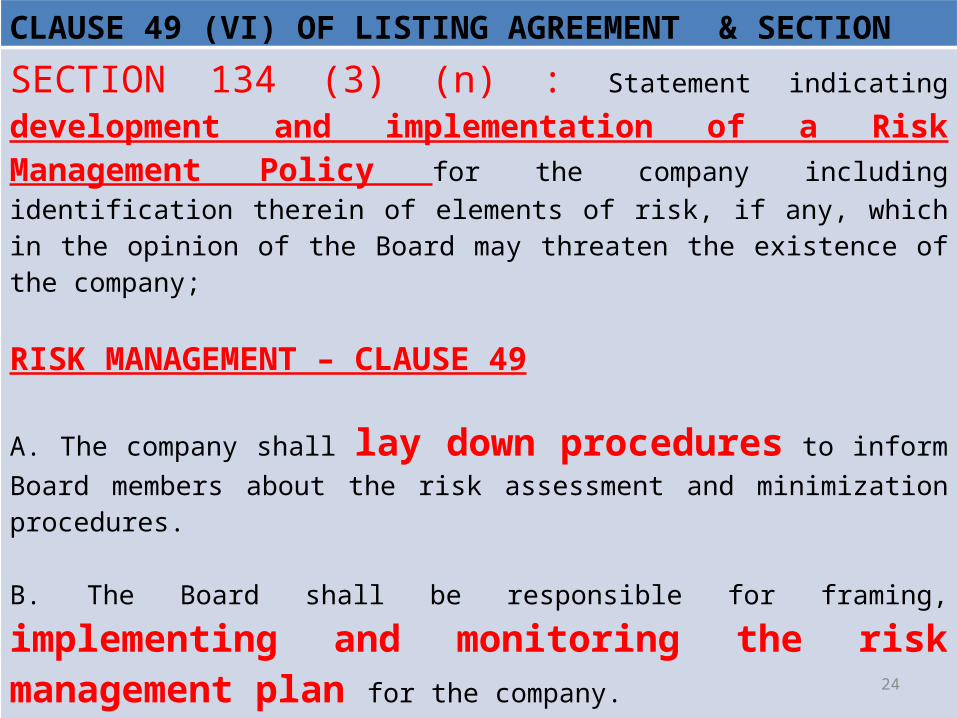

CLAUSE 49 (VI) OF LISTING AGREEMENT & SECTION 134 (3) (n)

SECTION 134 (3) (n) : Statement indicating development and implementation of a Risk Management Policy for the company including identification therein of elements of risk, if any, which in the opinion of the Board may threaten the existence of the company;

RISK MANAGEMENT – CLAUSE 49

A. The company shall lay down procedures to inform Board members about the risk assessment and minimization procedures.

B. The Board shall be responsible for framing, implementing and monitoring the risk management plan for the company.

## C. The company shall also constitute a Risk Management Committee. The Board shall define the roles and responsibilities of the Risk Management Committee and may delegate monitoring and reviewing of the risk management plan to the committee and such other functions as it may deem fit.

## Applicability :

applicable with effect from October 01, 2014 for top 100 listed companies by market capitalisation as at the end of the immediate previous financial year.

25

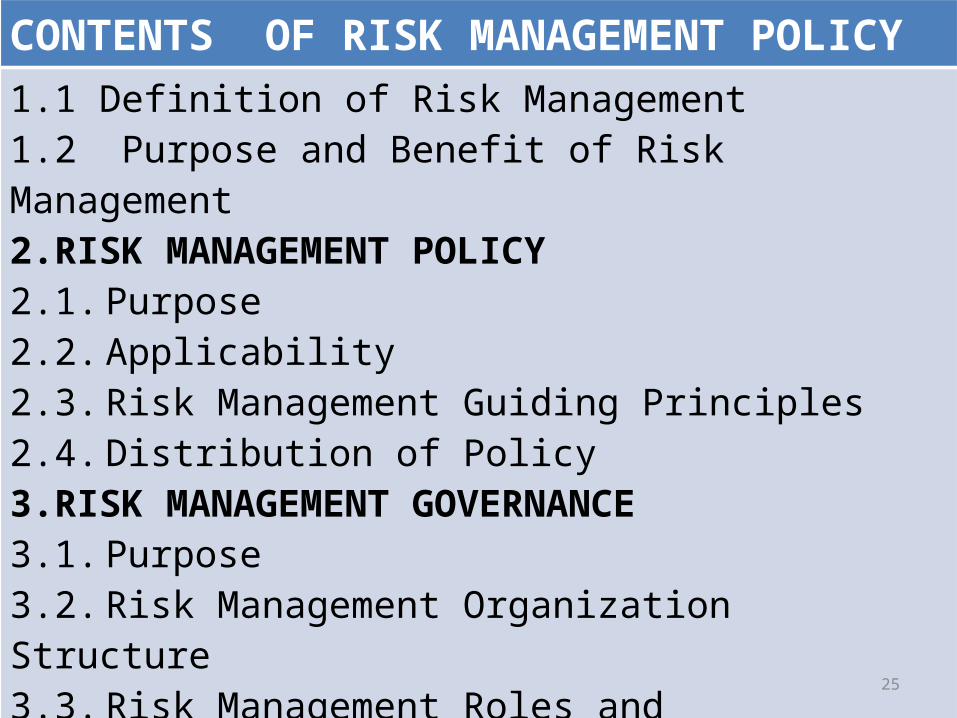

CONTENTS OF RISK MANAGEMENT POLICY 1.1 Definition of Risk Management1.2 Purpose and Benefit of Risk Management2. RISK MANAGEMENT POLICY2.1. Purpose2.2. Applicability2.3. Risk Management Guiding Principles2.4. Distribution of Policy3. RISK MANAGEMENT GOVERNANCE3.1. Purpose3.2. Risk Management Organization Structure3.3. Risk Management Roles and Responsibilities3.4. Risk Management Committee4. RISK MANAGEMENT PROCEDURES4.2. Risk Identification4.3. Risk Assessment4.4. Risk Treatment

26

NOMINATION AND REMUNERATION POLICY – SECTION 134 3(e) & Sec. 178 & CLAUSE 49 (IV)

(e)…….. company’s policy on directors’ appointment and remuneration criteria for determining qualifications, independence of a director etc., (APPLICABLE TO CO’S THAT REQUIRED TO HAVE NOMINATION & REMUNERATION COMMITTEE)

COMMENT :

Though Listing Agreement mentions about the role of Nomination and Remuneration Committee , it does not provides about the contents of Remuneration Policy. However, Section 178 provides for inclusion of certain details in the policy.

27

REMUNERATION POLICY :SECTION 178 (4) : The Nomination and Remuneration Committee shall, while formulating the policy ensure that—

(a)the level and composition of remuneration is reasonable and sufficient to attract, retain and motivate directors of the quality required to run the company successfully;

(b) relationship of remuneration to performance is clear and meets appropriate performance benchmarks; and

(c) remuneration to directors, key managerial personnel and senior management involves a balance between fixed and incentive pay reflecting short and long-term performance objectives appropriate to the working of the company and its goals: Provided that such policy shall be disclosed in the Board's report.

28

CONTENTS OF NOMINATION CUM REMUNERATION POLICY-

I . Introduction: II. Objective of this policy III. Nomination and Appointment:IV. Criteria & Process Of Appointment Of Executive Directors & Non-Executive Directors: Independent Directors Key Managerial PersonnelEvaluation & Appraisal V. Remuneration:Executive Directors & Non-Executive Directors: Independent Directors Key Managerial PersonnelEmployees VI. Other General terms :

29

VIGIL MECHANISM / WHISTLE BLOWER POLICY :

SECTION 177(9) & (10) read with Rule (7) of Cos (Meeting of its Board & its Directors) Rules, 2014 :

- Establishment of Vigil Mechanism - Disclosure in Boards’ Report - Audit Committee to oversee

CLAUSE 49 (II)(F)

WHISTLE BLOWER POLICY :

Listed Company to formulate a policy for Vigil Mechanism and to establish a mechanism that any personnel may raise Reportable Matters within 60 days after becoming aware of the same to the Audit Committee.

30

CONTENTS OF WHISTLE BLOWER POLICYPurpose of the Policy

Applicability

Coverage of Policy

Definitions

Scope

Reporting Responsibility

False Complaints

Reporting Mechanism

Process of Enquiry/Investigation

Investigations

Non-Retaliation

31

CONTENTS OF CSR POLICY - SECTION 135 Read with Rule 6

1. INTRODUCTION:2. AIMS & OBJECTIVES:3. COMMITTEE COMPOSITION:4. COMMITTEE MEETINGS:5. DUTIES & RESPONSIBILITIES OF CSR COMMITTEE:6. RESPONSIBILITY OF THE BOARD:7. CSR EXPENDITURE:8. CSR ACTIVITIES – PROJECTS:9. IMPLEMENTING CSR ACTIVITIES10. CSR TEAM CAPABILITIES11. CSR MONITORING 12.CSR REPORTING:13. WEBSITE DISPLAY:14. REVIEW AND AUDIT:

32

OTHER POLICIES UNDER LISTING AGREEMENTPOLICY FOR DETERMINING THE MATERIAL SUBSIDIARY :

Listed Company to formulate a policy for determining the Material Subsidiary and the details of such policies are disseminated in the website of the Company

Material Non Listed Indian Subsidiary: Income/Net worth exceeds 20% of the consolidated income or ne tworth of Listed holding co., & its subsidiaries.

RELATED PARTY TRANSACTION POLICY :

Listed Company to formulate a policy on dealing with RPT and disclose the by way of providing web link in the Boards Report.

No requirement under CA 2013.

33

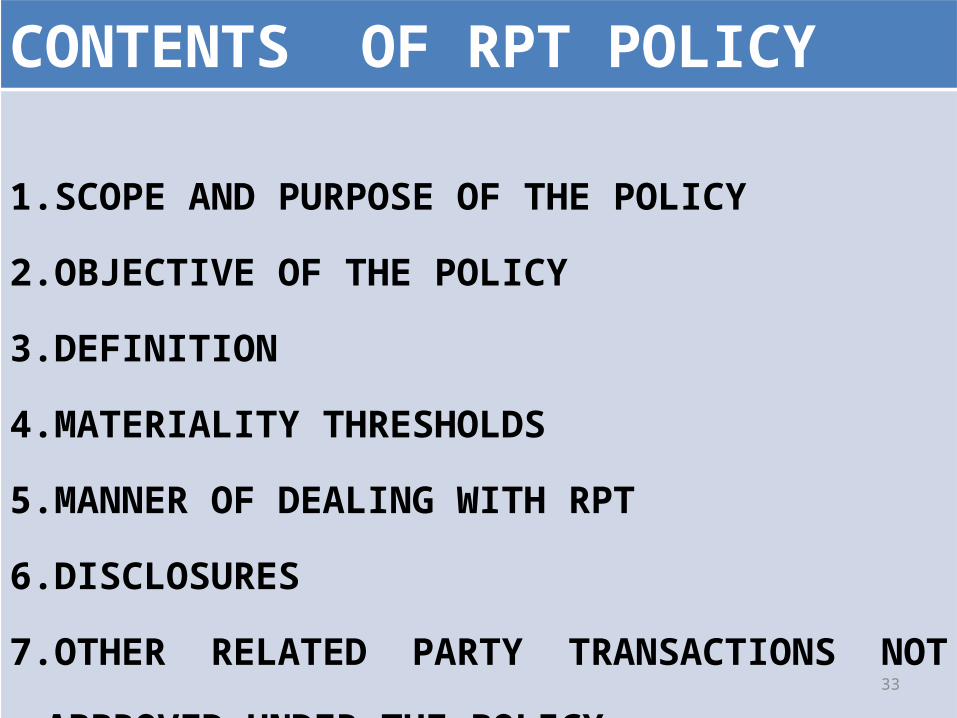

CONTENTS OF RPT POLICY

1. SCOPE AND PURPOSE OF THE POLICY2. OBJECTIVE OF THE POLICY3. DEFINITION4. MATERIALITY THRESHOLDS5. MANNER OF DEALING WITH RPT6. DISCLOSURES7. OTHER RELATED PARTY TRANSACTIONS NOT APPROVED

UNDER THE POLICY

34

35

ABOUT THE BOARD Board of Directors

Executive Directors Non Executive Directors

Non Executive Independent Directors

36

DISCLOSURE ABOUT THE BOARD

Clause 49 applicability Vis-a- Vis Companies Act Applicability on Board

Board Composition to be in accordance with Listing Agreement. Woman Director

Independent Director not less than 21 years of age.

Independent Director cannot be ID in more than 7 companies and a WTD cannot be ID in more than 3 Companies.

a statement on declaration given by independent directors MEETING THE CRITERIA

Formal Letter of Appointment of ID to be disclosed along with Profile in Website of Company

Separate Meeting of ID atleast once in a year. (Clause 49 & Sch IV )

Familiarization programme for ID. Details to be provided in Website of the company

37

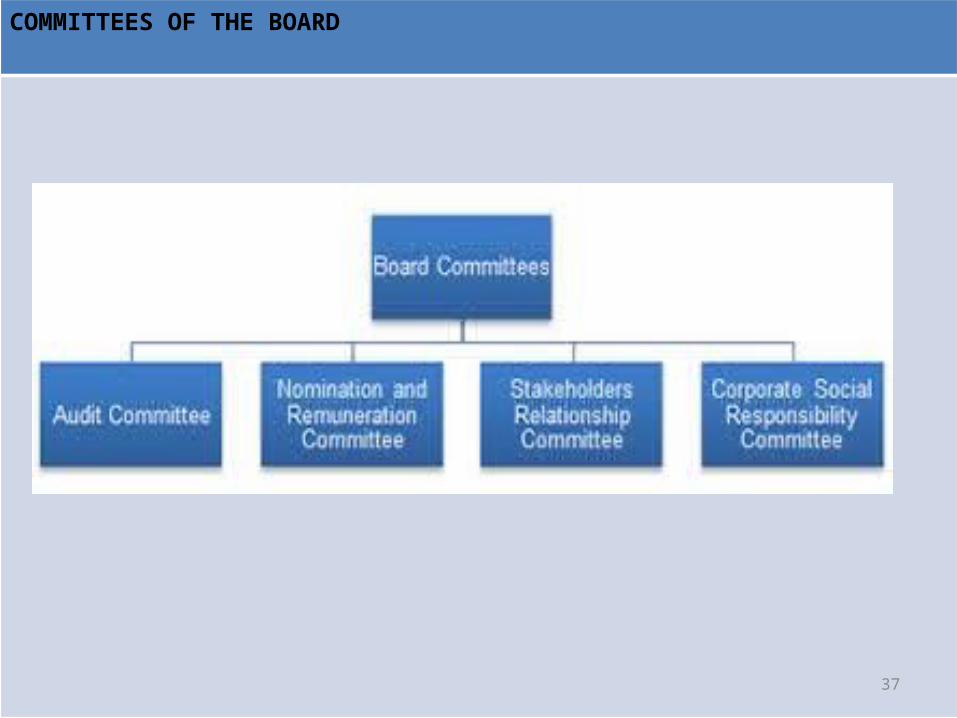

COMMITTEES OF THE BOARD

38

AUDIT COMMITTEE - SECTION 149 & CLAUSE 49

PARTICULARS COMPANIES ACT LISTING AGREEMENT

CHAIRMAN NOT SPECIFIC ONLY ID

COMPOSITION MINIMUM 3 WITH MAJORITY OF ID

MINIMUM 3 WITH 2/3RD ID

QUALIFICATION ABILITY TO READ & UNDERSTAND FS

ALL MEMBERS TO BE FINANCIALLY LITERATE WITH ONE MEMBER HAVING ACCOUNTING OR RELATED FINANCIAL MANAGEMENT EXPERTISE

ATTENDANCE AT AGM NOT SPECIFIC ID TO BE PRESENT

39

AUDIT COMMITTEE DISCLOSURES - SECTION 149 (10) & CLAUSE 49

1. If an independent director is re-appointed after holding office for a consecutive period of 5 years, then such a fact has to be disclosed.

2. To disclose the composition of Audit Committee

3. Disclosure of reasons for not accepting the recommendation of the Audit Committee.

4. Company which is required to establish a vigil mechanism shall disclose the details of establishment of such mechanism.

40

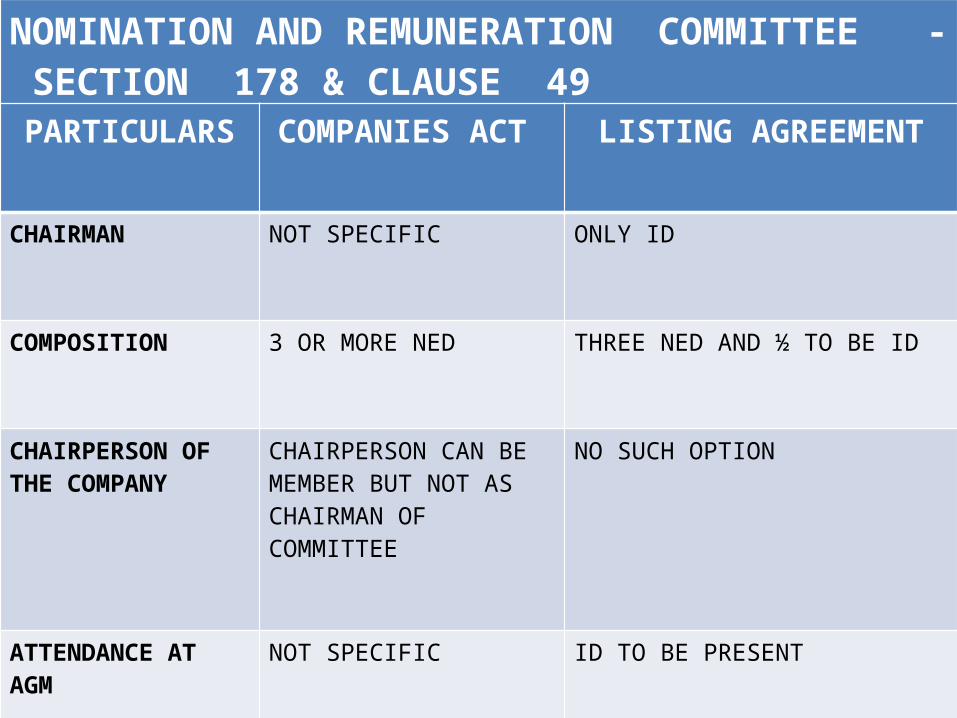

NOMINATION AND REMUNERATION COMMITTEE - SECTION 178 & CLAUSE 49

PARTICULARS COMPANIES ACT LISTING AGREEMENT

CHAIRMAN NOT SPECIFIC ONLY ID

COMPOSITION 3 OR MORE NED THREE NED AND ½ TO BE ID

CHAIRPERSON OF THE COMPANY

CHAIRPERSON CAN BE MEMBER BUT NOT AS CHAIRMAN OF COMMITTEE

NO SUCH OPTION

ATTENDANCE AT AGM NOT SPECIFIC ID TO BE PRESENT

41

DISCLOSURES WITH RESPECT TO REMUNERATION TO DIRECTORS/ KMP ( LISTED CO)

Disclosure in respect of the following : Section 197 (12) read Rule 5 with Cos.(Apptn & Remn) Rules, 2014.

Ratio of the remuneration of each director to the median remuneration of the employees of the company for the financial year ;

Percentage increase in remuneration of each director, CFO, CS, or Manager with Percentage increase in the median remuneration of employees if any in the financial year;

(“Median” means the numerical value separating the higher half of a population from the lower half and the median of a finite list of numbers may be found by arranging all the observations from lowest value to highest value and picking the middle one; (ii) if there is an even number of observations, the median shall be the average of the two middle values.)

42

DISCLOSURES WITH RESPECT TO REMUNERATION TO DIRECTORS/ KMP ( LISTED CO)

Number of permanent employees on the rolls of company;

Explanation on the relationship between average increase in remuneration and company performance;

• Comparison of the remuneration of the KMP with performance of the company;

• Variations in the market capitalization of the company, price earning ratio & percentage increase over decrease in the market quotations of the shares of the company in comparison to the rate at which the company came out with the last public offer in case of listed companies.

43

DISCLOSURES (IF LISTED )

• The ratio of the remuneration of the highest paid director to that of the employees who are not directors but receive remuneration in excess of the highest paid director during the year.

• A affirmation that the remuneration is as per the remuneration policy of the company

44

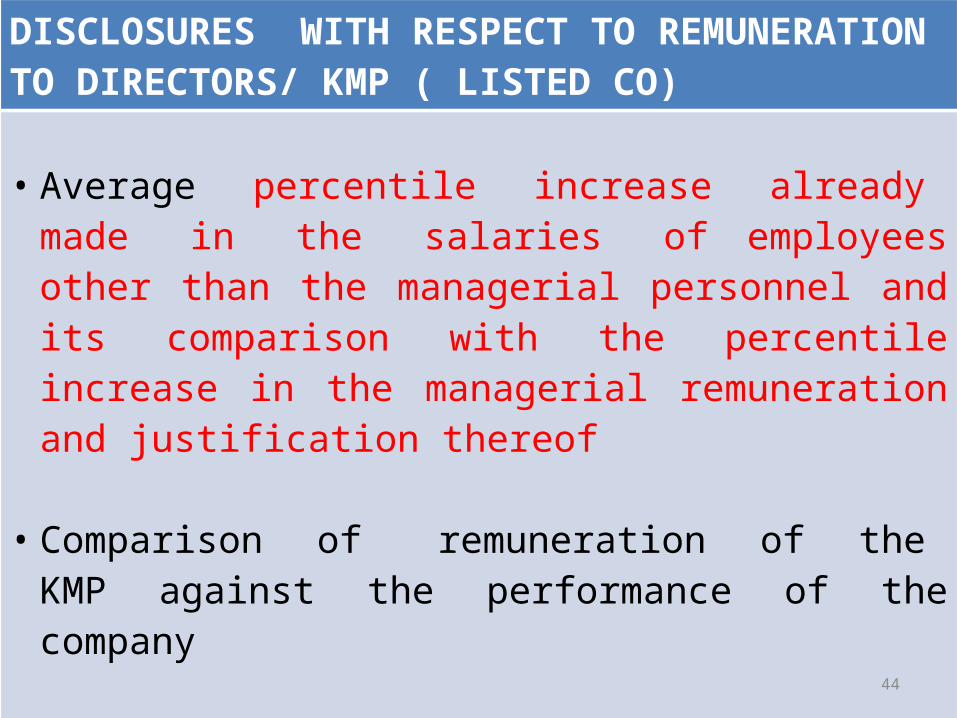

DISCLOSURES WITH RESPECT TO REMUNERATION TO DIRECTORS/ KMP ( LISTED CO)

• Average percentile increase already made in the salaries of employees other than the managerial personnel and its comparison with the percentile increase in the managerial remuneration and justification thereof

• Comparison of remuneration of the KMP against the performance of the company

• The key parameters for any variable component of remuneration availed by the directors;

45

DISCLOSURES (ALL Companies)

- Who is in receipt of remuneration for FY, in the aggregate, was not less than Rs 60 lakh or in receipt of remuneration for any part of that year, at a rate which, in the aggregate, was not less than Rs 5 lakh per month;

- Employed throughout the financial year or part thereof, was in receipt of remuneration which, in the aggregate, is in excess of that drawn by the managing director or whole-time director or manager and holds by himself or along with his spouse and dependent children, not less than 2% of the equity shares of the company.

Exceptions to such Disclosure: Employees posted outside India (No relative/directors)

Though need not be circulated, need to be filed with ROC along with FS & Boards’ report. To be available to share holder on request

46

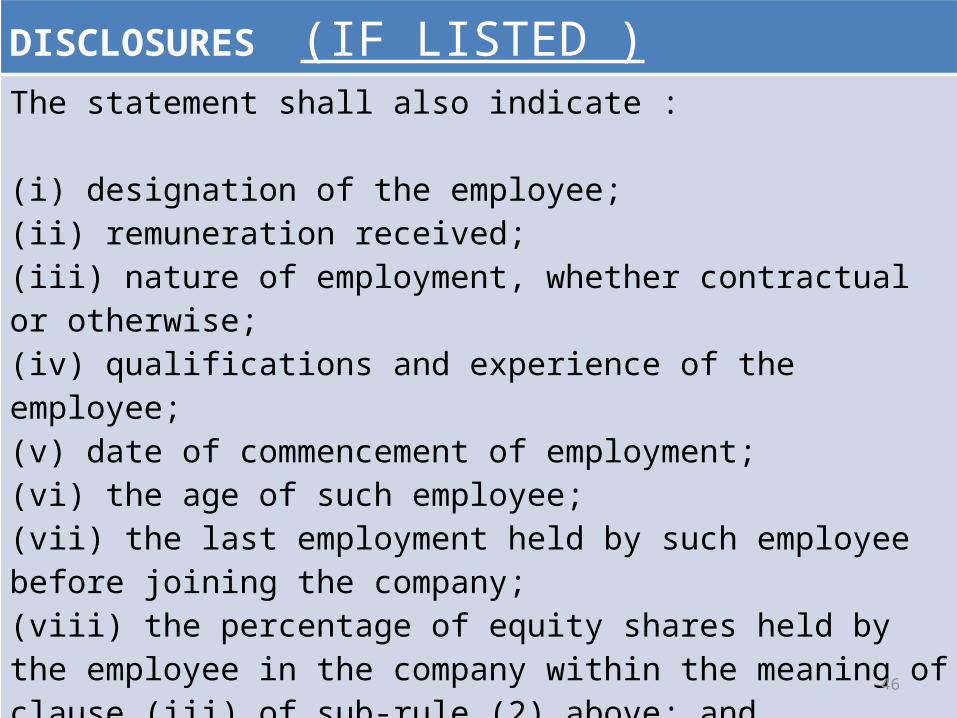

DISCLOSURES (IF LISTED )The statement shall also indicate :

(i) designation of the employee; (ii) remuneration received; (iii) nature of employment, whether contractual or otherwise; (iv) qualifications and experience of the employee; (v) date of commencement of employment; (vi) the age of such employee; (vii) the last employment held by such employee before joining the company; (viii) the percentage of equity shares held by the employee in the company within the meaning of clause (iii) of sub-rule (2) above; and (ix) whether any such employee is a relative of any director or manager of the company and if so, name of such director or manager:

47

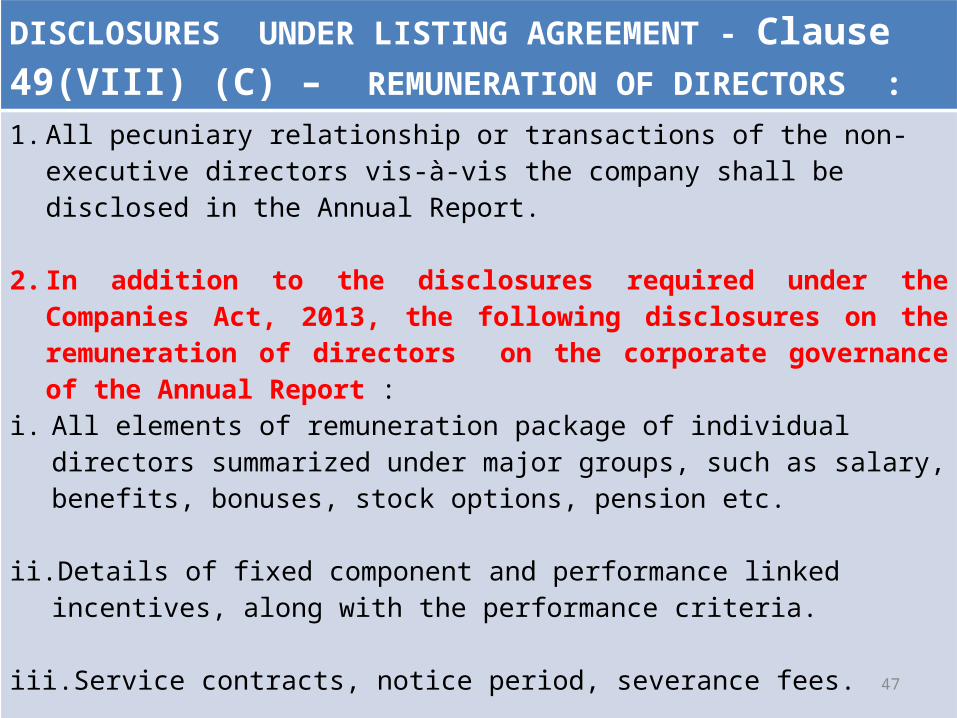

DISCLOSURES UNDER LISTING AGREEMENT - Clause 49(VIII) (C) – REMUNERATION OF DIRECTORS :

1. All pecuniary relationship or transactions of the non-executive directors vis-à-vis the company shall be disclosed in the Annual Report.

2. In addition to the disclosures required under the Companies Act, 2013, the following disclosures on the remuneration of directors on the corporate governance of the Annual Report :

i. All elements of remuneration package of individual directors summarized under major groups, such as salary, benefits, bonuses, stock options, pension etc.

ii. Details of fixed component and performance linked incentives, along with the performance criteria.

iii. Service contracts, notice period, severance fees.

iv. Stock option details, if any - and whether issued at a discount as well as the period over which accrued and over which exercisable.

* Same disclosures (I to iv) is required to be provided in Schedule V of CA 2013 but only in case of No/ Inadequate profits .

48

FORMAL ANNUAL EVALUATION- SECTION 134 ( 3) (P) RULE NO. 8(4) OF THE COMPANIES (ACCOUNTS) RULES 2014

In case of a listed company and every other public company having such paid-up share capital of Rs. 25 Crores , a statement indicating the manner in which formal annual evaluation has been made by the Board of its own performance and that of its committees and individual directors;

Clause 49 II (B) (5) - PERFORMANCE EVALUATION OF INDEPENDENT DIRECTORS

a. The Nomination Committee shall lay down the evaluation criteria for performance evaluation of independent directors.

b. The company shall disclose the criteria for performance evaluation, as laid down by the Nomination Committee, in its Annual Report.

c. The performance evaluation of independent directors shall be done by the entire Board of Directors (excluding the director being evaluated).

d. On the basis of the report of performance evaluation, it shall be determined whether to extend or continue the term of appointment of the independent director.

49

OTHER DISCLOSURES

(i) the change in the nature of business, if any;

(ii) Details of subsidiaries/ joint ventures or associate companies LISTING AGREEMENT – CLAUSE 49 (V) recognise Subsidiary Companies and Material Non- Listed Indian Subsidiary

(ID , review of FS of subsidiary, BM Minutes )

RULE 8(1) - A report, on the performance and financial position of each of the subsidiaries, associates and joint venture companies included in the consolidated financial statement is presented

50

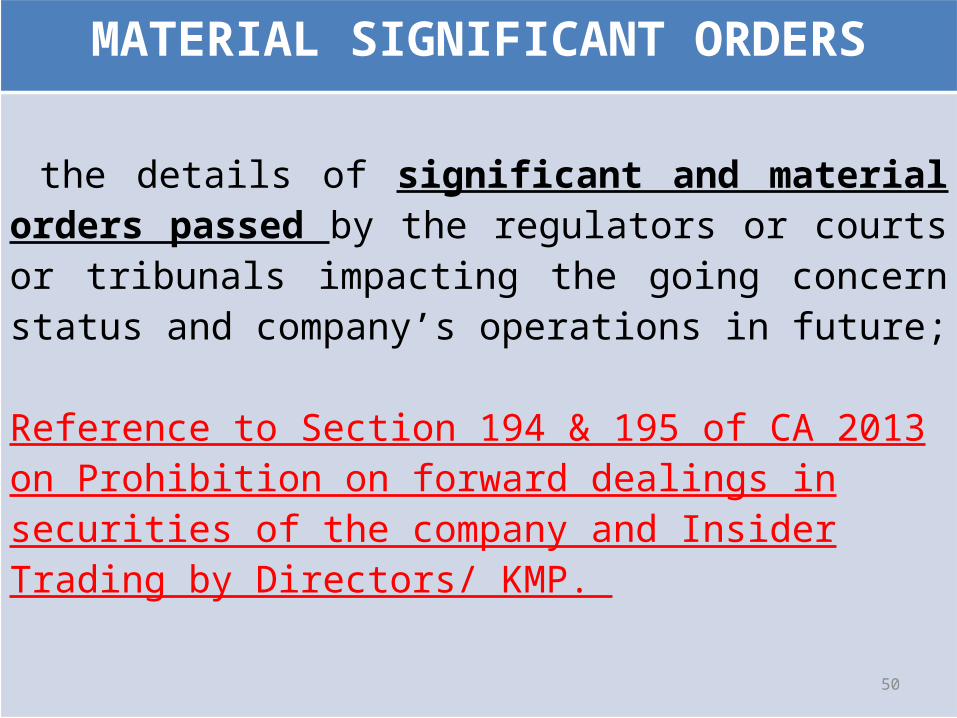

MATERIAL SIGNIFICANT ORDERS

the details of significant and material orders passed by the regulators or courts or tribunals impacting the going concern status and company’s operations in future;

Reference to Section 194 & 195 of CA 2013 on Prohibition on forward dealings in securities of the company and Insider Trading by Directors/ KMP.

51

MANAGEMENT DISCUSSION & ANALYSIS REPORT

CLAUSE 49 (VIII) (D) – MANAGEMENT :

As a part of Directors’ Report or as addition thereto MD&A should form part as Annual Report and shall include discussions on a. Industry structure and developments. b. Opportunities and Threats. c. Segment–wise or product-wise performance. d. Outlook e. Risks and concerns. f. Internal control systems and their adequacy. g. Discussion on financial performance with respect to operational performance. h. Material developments in Human Resources / Industrial Relations front, including number of people employed.

52

BUSINESS RESPONSIBILITY REPORT CLAUSE 55 OF LISTING AGREEMENT:

The requirement to include Business Responsibility Reports, describing the initiatives taken by them from an environmental, social and governance perspective, in the format suggested as part of the Annual Reports which shall be mandatory for top 100 listed entities based on market capitalisation at BSE and NSE as on March 31, 2012

CONTENTS OF BR REPORT :Section A: General Information about the CompanySection B: Financial Details of the CompanySection C: Other Details ( Subsidiary companies/ other related companies)Section D: BR InformationSection E: Principle-wise performance

53

RELATED PARTIES & TRANSACTIONS

54

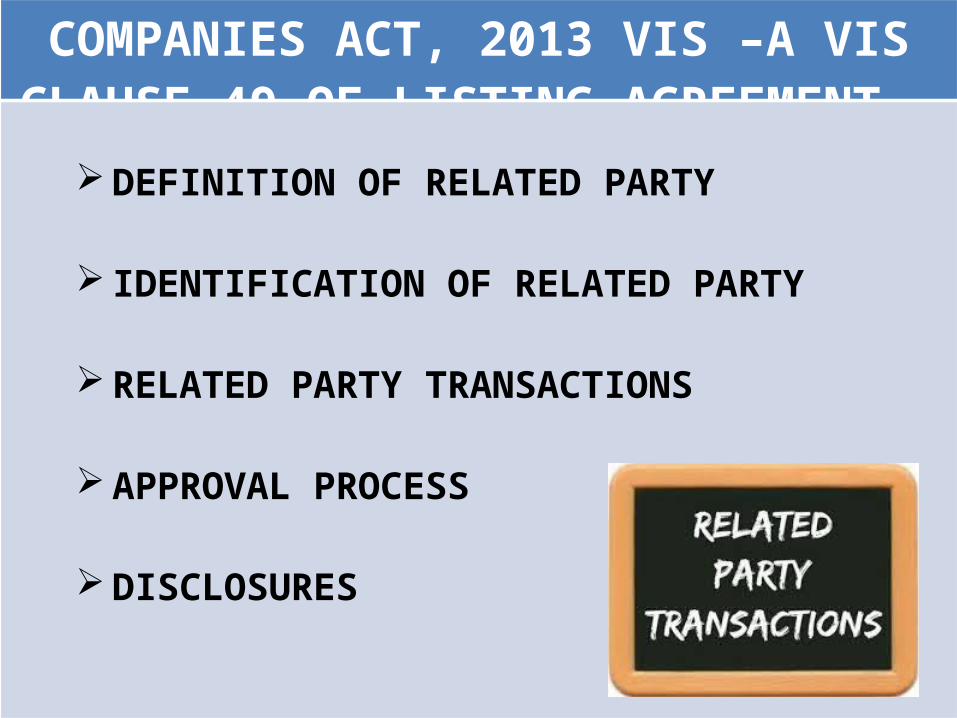

COMPANIES ACT, 2013 VIS –A VIS CLAUSE 49 OF LISTING AGREEMENT

DEFINITION OF RELATED PARTY

IDENTIFICATION OF RELATED PARTY

RELATED PARTY TRANSACTIONS

APPROVAL PROCESS

DISCLOSURES

55

DEFINITION OF RELATED PARTY- S. 2(76) Vs. Cl. 49(VII) Vs. AS24

CA 2013 : - Section (76)“related party”, with reference to a company, means—(i) a director or his relative(ii) a key managerial personnel or his relative;(iii) a firm, in which a director, manager or his relative is a partner;(iv) a private company in which a director or manager is a member or director;(v) a public company in which a director or manager is a director or holds along with his relatives, more than two per cent. of its paid-up share capital;(vi) any body corporate whose Board of Directors, managing director or manager is accustomed to act in accordance with the advice, directions or instructions of a director or Manager;(vii) any person on whose advice, directions or instructions a director or manager is accustomed to act:Provided that nothing in sub-clauses (vi) and (vii) shall apply to the advice, directions or instructions given in a professional capacity;(viii) any company which is—(A) a holding, subsidiary or an associate company of such company; or(B) a subsidiary of a holding company to which it is also a subsidiary;(ix) such other person as may be prescribed;

56

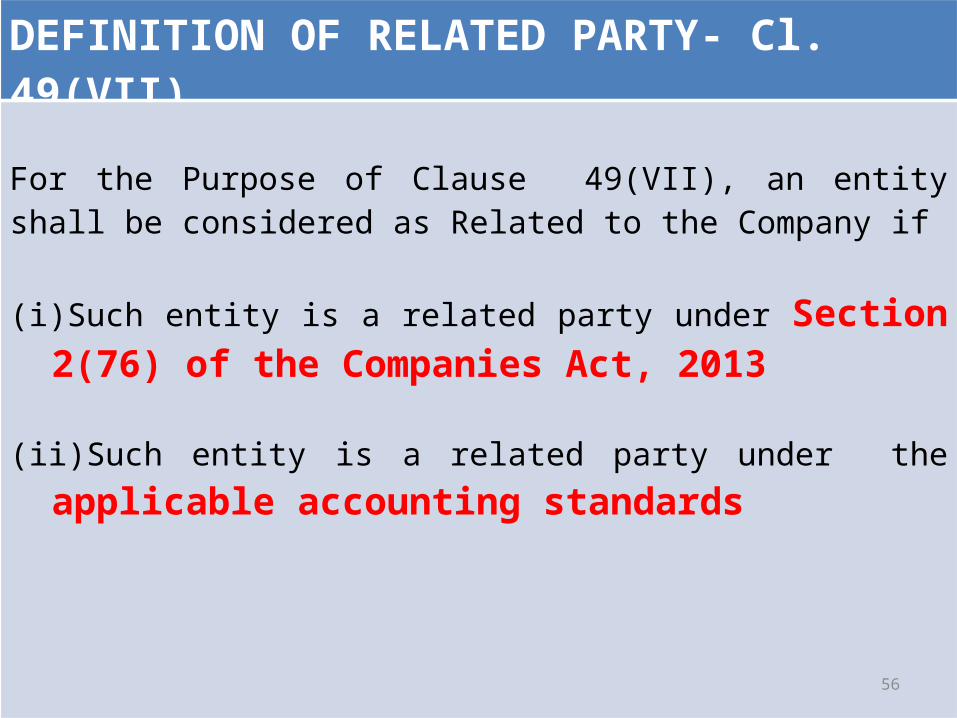

DEFINITION OF RELATED PARTY- Cl. 49(VII)

For the Purpose of Clause 49(VII), an entity shall be considered as Related to the Company if

(i) Such entity is a related party under Section 2(76) of the Companies Act, 2013

(ii) Such entity is a related party under the applicable accounting standards

57

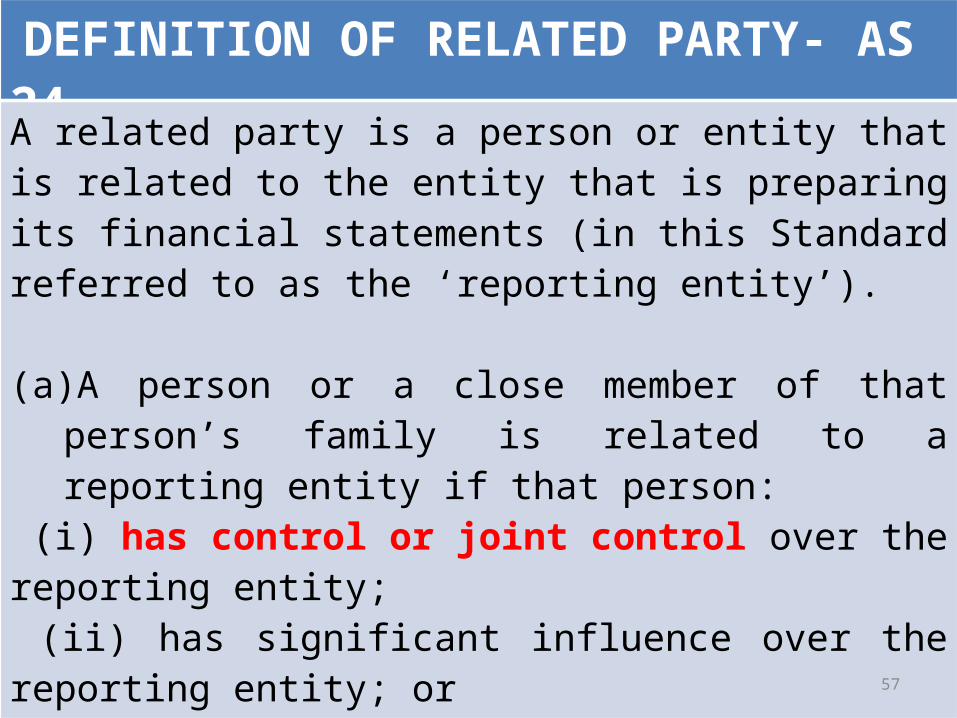

DEFINITION OF RELATED PARTY- AS 24

A related party is a person or entity that is related to the entity that is preparing its financial statements (in this Standard referred to as the ‘reporting entity’).

(a) A person or a close member of that person’s family is related to a reporting entity if that person:

(i) has control or joint control over the reporting entity; (ii) has significant influence over the reporting entity; or (iii) is a member of the key management personnel of the reporting entity or of a parent of the reporting entity.

58

DEFINITION OF RELATED PARTY- AS 24

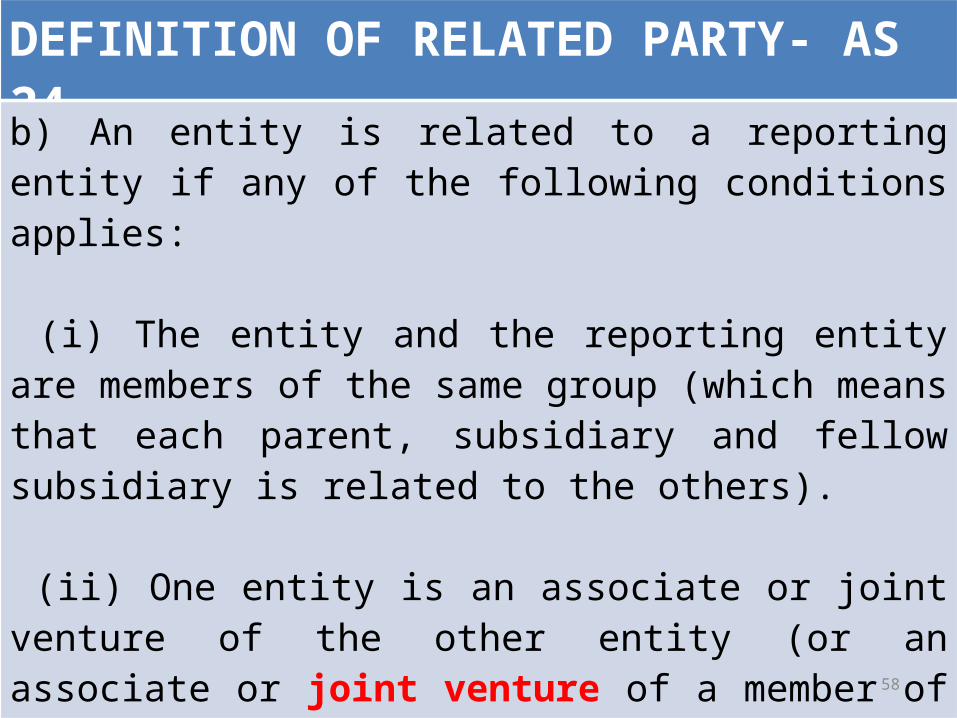

b) An entity is related to a reporting entity if any of the following conditions applies:

(i) The entity and the reporting entity are members of the same group (which means that each parent, subsidiary and fellow subsidiary is related to the others).

(ii) One entity is an associate or joint venture of the other entity (or an associate or joint venture of a member of a group of which the other entity is a member).

(iii) Both entities are joint ventures of the same third party.

59

DEFINITION OF RELATED PARTY- AS 24

(iv) One entity is a joint venture of a third entity and the other entity is an associate of the third entity.

(v) The entity is a post-employment benefit plan for the benefit of employees of either the reporting entity or an entity related to the reporting entity. If the reporting entity is itself such a plan, the sponsoring employers are also related to the reporting entity.

(vi) The entity is controlled or jointly controlled by a person identified in (a). vii) A person identified in (a)(i) has significant influence over the entity or is a member of the entity

60

IDENTIFICATION OF RELATED PARTY

Sec. 188 of CA 2013 Clause 49 (VII) & AS 24

Sale, Purchase of goods , services, Property Leasing of Property , Office of Place of Profit et

transfer of resources, services or obligations between a reporting entity and a related party, regardless of whether a price is charged

61

APPROVAL PROCESS

Sec. 188 of CA 2013 Clause 49 (VII) & AS 24

A. Audit Committee – Section 177 ( prior/ Post facto ?)

B. Transactions with RPT that are not in ordinary course of business and are not at arms’ length price.

C. Ratification of RPTD. Omnibus not possible

A. Prior approval of Audit Committee

B. No such exemption provided.

C. Ratification not possibleD. Audit Committee may

grant Omnibus approval for RPT.

62

APPROVAL PROCESS

Sec. 188 of CA 2013 Clause 49 (VII) & AS 24

E. Board of Directors F. Shareholders (Special Resolution) only for certain cases where the value exceeds the limits under Sec.188(1) read with rule 15 of Cos(Meeting of Board and its Powers) Rules, 2014

E. Board of DirectorsF. Shareholders (Special Resolution based on materiality which is 10% of the annual consolidated turnover of the company for transactions entered / to be entered individually or taken together with previous transactions during a FY.

63

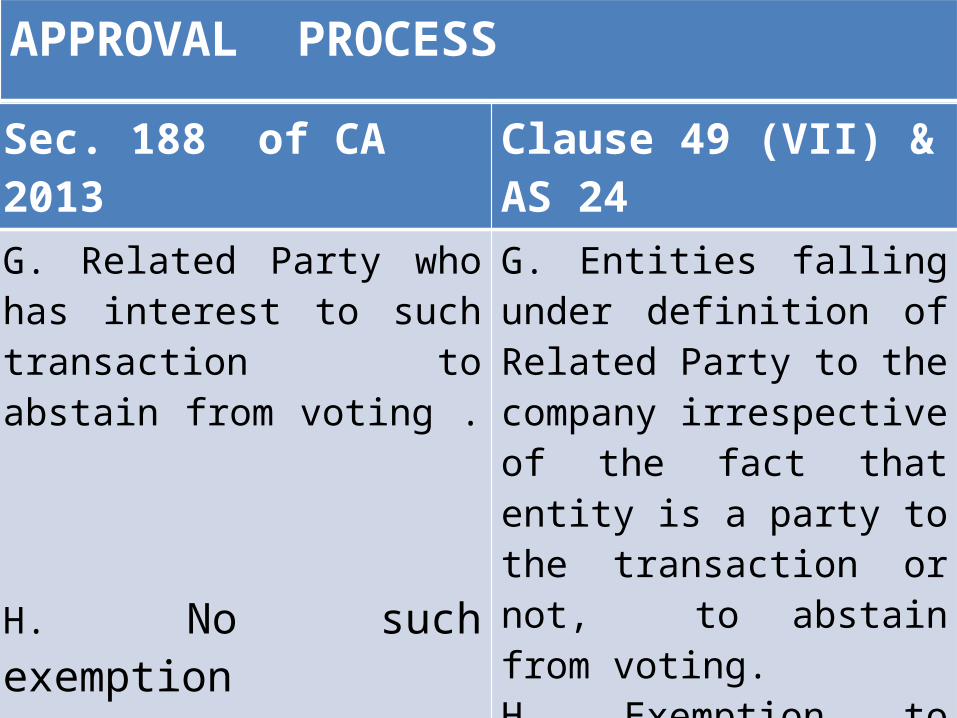

APPROVAL PROCESS

Sec. 188 of CA 2013 Clause 49 (VII) & AS 24

G. Related Party who has interest to such transaction to abstain from voting .

H. No such exemption

G. Entities falling under definition of Related Party to the company irrespective of the fact that entity is a party to the transaction or not, to abstain from voting.H. Exemption to certain cos. ( viz. Govt. co, Holding Co., & WOS whose accounts are consolidated with Holding Co)

64

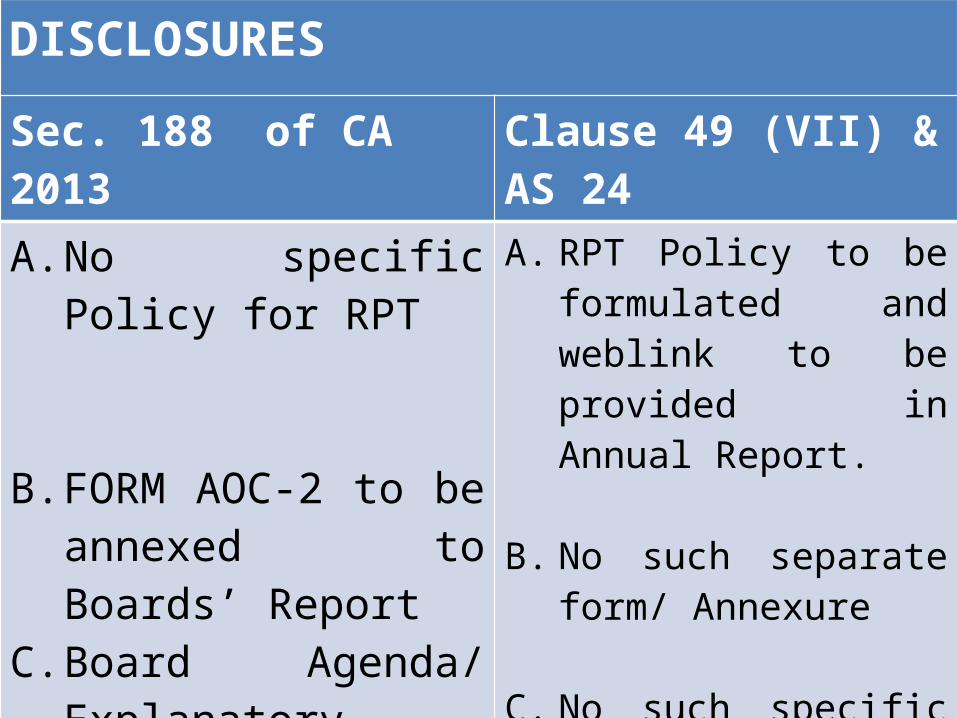

DISCLOSURES

Sec. 188 of CA 2013 Clause 49 (VII) & AS 24

A. No specific Policy for RPT

B. FORM AOC-2 to be annexed to Boards’ Report

C. Board Agenda/ Explanatory Statement to include certain specific details about RPT

A. RPT Policy to be formulated and weblink to be provided in Annual Report.

B. No such separate form/ Annexure

C. No such specific details sought.

65

DISCLOSURES

Sec. 188 of CA 2013 Clause 49 (VII) & AS 24

D. No quarterly reportings.

E. No disclosure by Senior Management.

F. Earlier Approval valid till the period of approval granted.

D. Details about RPT to be mentioned in Corporate Governance report every quarter.

E. Disclosure by Senior Management about material / commercial transactions where they have interest.

F. RPT beyond 31st Mar,2015 require approval in first GM.

66

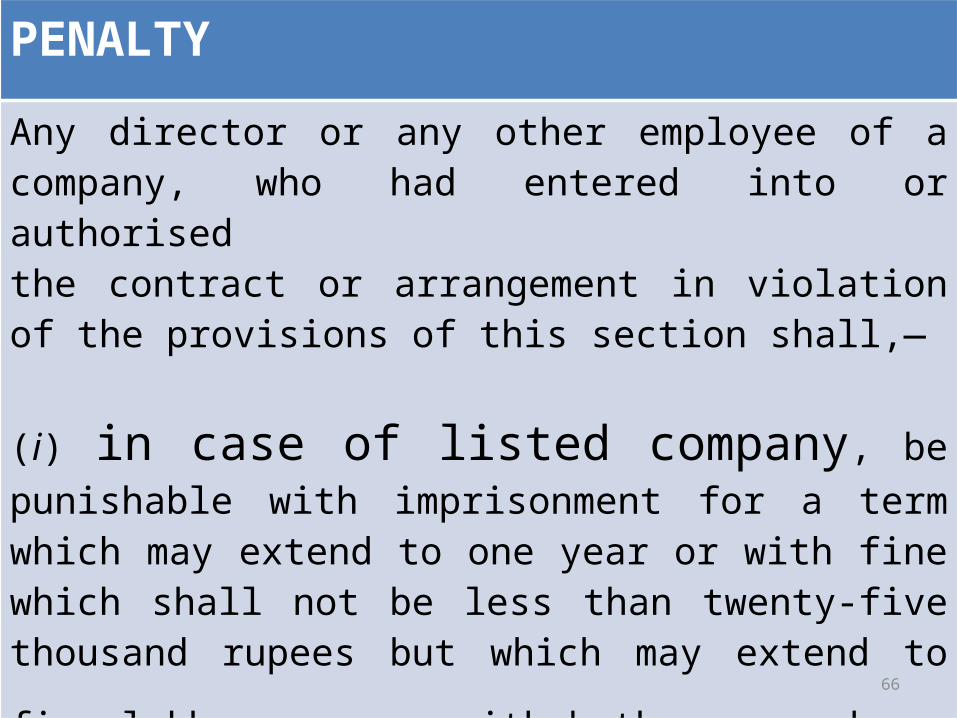

PENALTY

Any director or any other employee of a company, who had entered into or authorisedthe contract or arrangement in violation of the provisions of this section shall,—

(i) in case of listed company, be punishable with imprisonment for a term which may extend to one year or with fine which shall not be less than twenty-five thousand rupees but which may extend to five lakh rupees or with both; and (ii) in case of any other company, be punishable with fine which shall not be less than twenty-five thousand rupees but which may extend to five lakh rupees.

67

APPROVAL PROCESS UNDER CA 2013 & CLAUSE 49

ACT 2013 AUDIT COMMITTEE (ALL COMPANIES , ALL

TRANSACTIONS)

TRANSACTIONS UNDER S.188 NOT IN ORDINARY COURSE OF BUSINESS/

ARMS LENGHTH

BOARD APPROVAL

OTHER CASES IF CERTAIN

THRESHOLD MET

SPECIAL RESOLUTION AT GM - VOTING BY

PARTIES NOT INTERESTED

TRANSACTIONS UNDER S.188 IN ORDINARY

COURSE OF BUSINESS/ ARMS LENGHTH

NO FURTHER

APPROVAL

CLAUSE 49PRIOR APVL

AUDIT COMMITTEE (EVEN NO PRICE) ALL TRANSACTIONS)

MATERIAL TRANSACTIONS(10% OF ANNUAL CONSOLIDATED

TURNOVER)

SPECIAL RESOLUTION-

VOTING BY UNRELATED

PARTIES

NO MATERIAL TRANSACTIONS

NO FURTHER

APPROVAL

68

OTHER DISCLOSURES AS PER LA &ON EVENTS

69

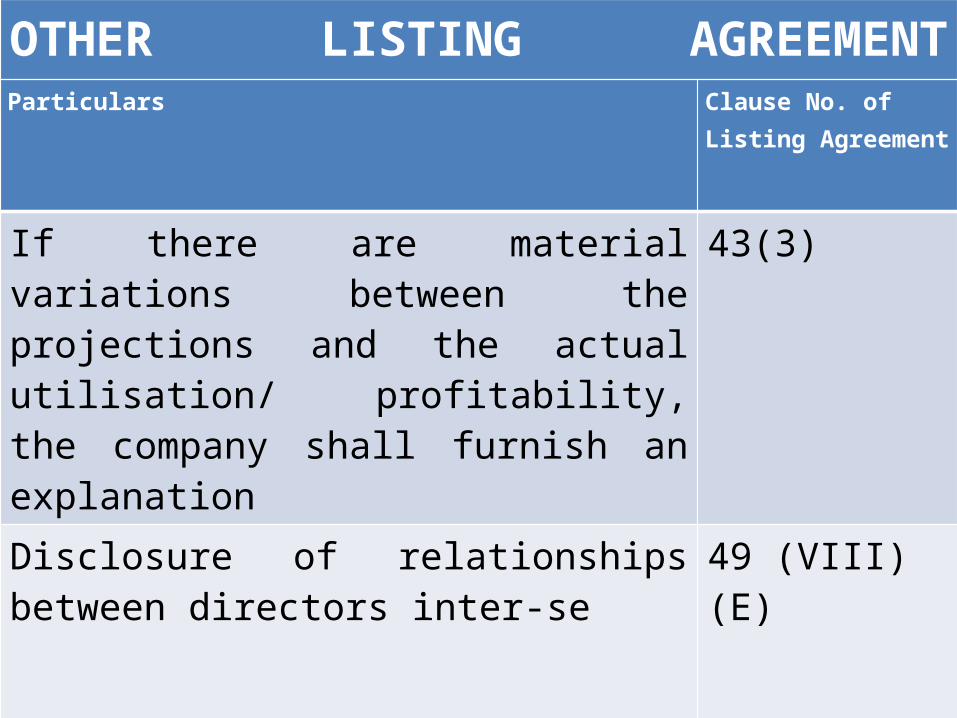

OTHER LISTING AGREEMENT DISCLOSURESParticulars Clause No. of

Listing Agreement

Details of shares lying in the suspense account 5.A.(I).g/ (II).h

i. In case the shares are delisted /suspended from trading, explain the reason thereof

ii. The name and address of each stock exchange at which the issuer’s securities are listed

iii. confirmation that Annual Listing Fee has been paid to each of the exchange.

32 (iii)b.i to iii

70

OTHER LISTING AGREEMENT DISCLOSURESParticulars Clause No. of

Listing Agreement

If there are material variations between the projections and the actual utilisation/ profitability, the company shall furnish an explanation

43(3)

Disclosure of relationships between directors inter-se

49 (VIII) (E)

71

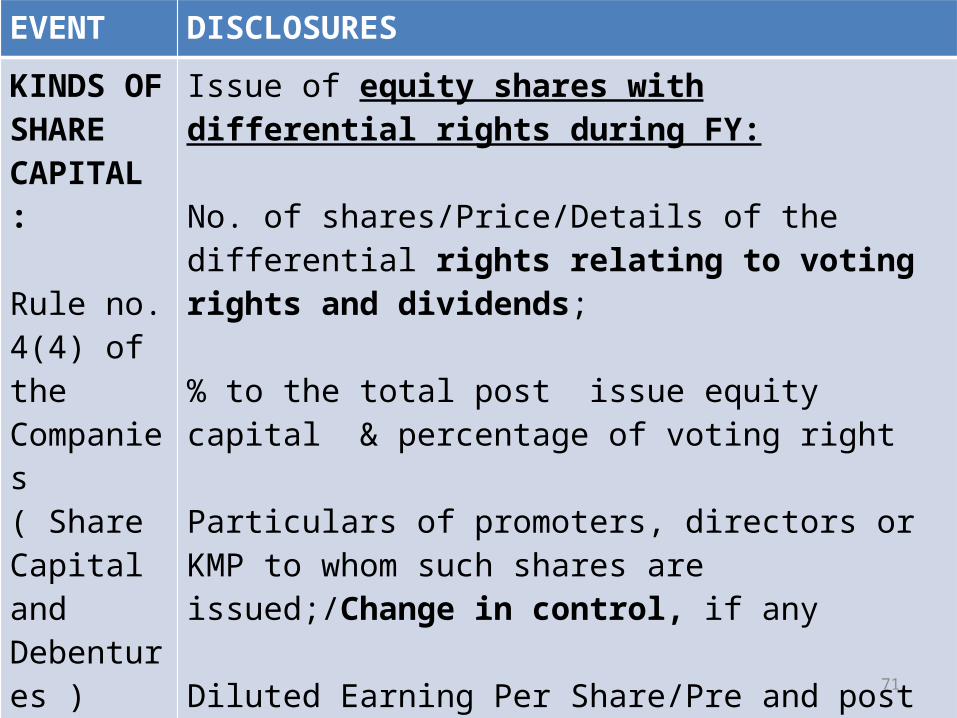

EVENT DISCLOSURES

KINDS OF SHARE CAPITAL : Rule no. 4(4) of the Companies ( Share Capital and Debentures ) Rules, 2014

Issue of equity shares with differential rights during FY:

No. of shares/Price/Details of the differential rights relating to voting rights and dividends;

% to the total post issue equity capital & percentage of voting right

Particulars of promoters, directors or KMP to whom such shares are issued;/Change in control, if any

Diluted Earning Per Share/Pre and post issue shareholding pattern along with voting rights

Other disclosure as per SEBI Guidelines

72

EVENT DISCLOSURES

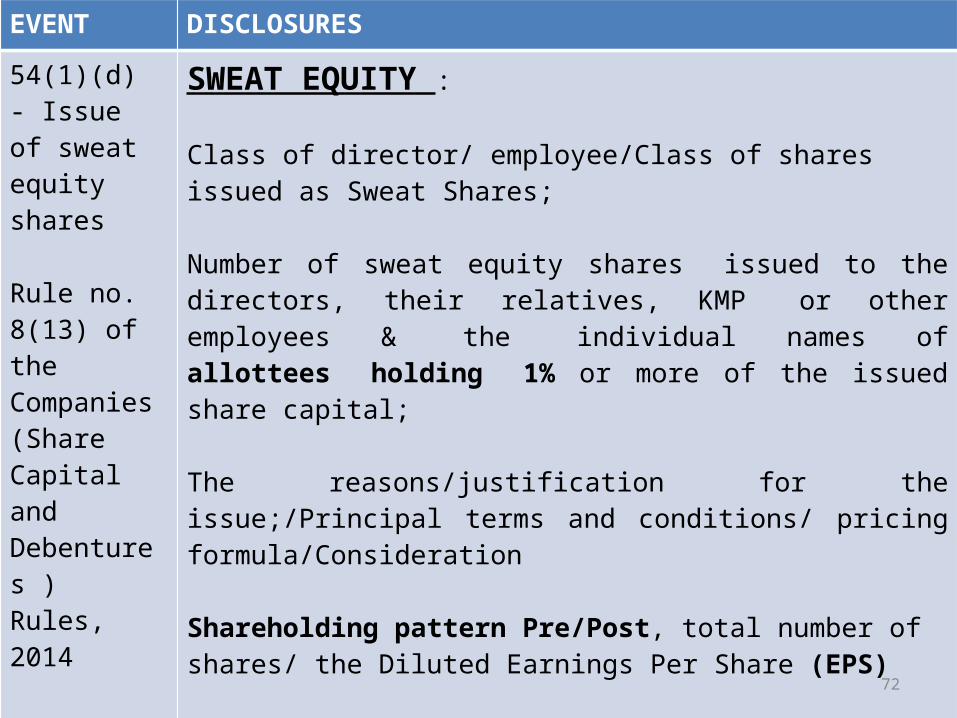

54(1)(d) - Issue of sweat equity shares Rule no. 8(13) of the Companies (Share Capital and Debentures ) Rules, 2014

SWEAT EQUITY :

Class of director/ employee/Class of shares issued as Sweat Shares;

Number of sweat equity shares issued to the directors, their relatives, KMP or other employees & the individual names of allottees holding 1% or more of the issued share capital;

The reasons/justification for the issue;/Principal terms and conditions/ pricing formula/Consideration

Shareholding pattern Pre/Post, total number of shares/ the Diluted Earnings Per Share (EPS)

Other disclosure as per SEBI Guidelines

73

EVENT DISCLOSURES

62(1)(b) - Further issue of share capital Rule no. 12(2) of the Companies ( Share Capital and Debentures ) Rules, 2014

EMPLOYEES STOCK OPTION SCHEME:

Options granted/vested/exercised/lapsed

The total number of shares arising as a result of exercise of option;

The exercise price;/ Variation of terms of options & Total number of options in force;

Employee wise details of options granted to KMP, Other employees who receives a grant in any one year of option amounting to 5% or more of./Identified employees who were granted option exceeding 1%

Other disclosure as per SEBI Guidelines

74

TAKE AWAYS FOR TODAY’S WORKSHOP

75

TAKEAWAYS FOR TODAY’S SESSION

1. DIRECTORS’ RESPONSIBILITY STATEMENT ON A. Internal financial control B. COMPLIANCE OF ALL APPLICABLE LAWS

2. FORMULATION OF POLICIES

3. REMUNERATION COMMITTEE & OTHER COMMITTEES, ITS POLICY AND DISCLOSURES

4. RELATED PARTY TRANSACTIONS

5. STRUCTURING OF BOARDS’ REPORT & CORPORATE GOVERNANCE TO MINIMIZE DUPICATION AND GIVE MEANINGFUL REPORT.