commoditymonthly 031208 edited -...

TRANSCRIPT

Investment research

Commodity sales: Martin Vorgod,, Dealer, FX, MM and derivatives sales, +45 45 14 32 86, [email protected]

Editor in Chief: Steen Bocian, Chief Economist, + 45 45 12 85 31, [email protected]

Web: http://www.danskebank.com/danskeresearch

Commodity Monthly

December 3, 2008

Economic slowdown continues Commodity Research: Arne Lohmann Rasmussen, Senior Analyst, +45 45 12 85 32, [email protected]

Over the last couple of months it has become clear that the economic crisis had turned into a global recession. Furthermore, the crisis has spread to emerging markets with a vengeance, and commodity demand is not just slowing, but is currently falling compared to earlier this year. The short-term outlook for the global economy is very bleak. Over the last couple of days global PMIs have nose-dived: the indicators were a record low in November in countries such as UK, Germany, Japan and China. In the US the ISM has dropped to the weakest level since 1982. Overall, the data releases point to an unprecedented drop in manufacturing activity in Q4. In light of the weak outlook, we published our new global growth forecasts in Global Scenarios last week. Basically, we forecast that in the coming three to six months the major economies are expected to continue to contract as the negative impact from the credit crisis, a further deepening of the housing slowdown, a backlash in emerging markets, and the negative recession dynamics, already in train, dominate.

With the short-term outlook for commodities looking dire, we also revised down our oil price forecasts for Q1 and Q2 2009 to approximately USD 50 a barrel on average. However, in our view there is already a very negative growth trajectory priced into commodities. The market seems to have overlooked the fact that the next couple of quarters are going to see very accommodative economic policies on a global scale. The Federal Reserve is, for example, most likely going to introduce a Zero Interest Rate Policy, and new fiscal stimuli have or will be introduced in almost all countries. In that respect one should not forget the aggressive easing that China recently introduced with fiscal packages, rate cuts and the removal of credit quotas. All in all, we expect that by mid-2009 the major OECD economies should return to positive growth rates and that a subsequent slow recovery will materialize in H2 2009. Our forecast for commodity prices is closely connected to this growth outlook. Hence, we look for more or less stable prices in H1 2009 and rising prices in line with the improved growth outlook during H2 2009. We also argue that the supply side will gain growing attention going forward and eventually support prices. A consequence of the current collapse in commodity prices and the financial credit crisis is a significant slowdown in commodity production and commodity investments. The latter points to a renewed tightness in many commodity markets when the global economy eventually recovers.

But one should expect ongoing high volatility over the coming months. Trying to call a bottom in commodity markets is like catching a falling knife at the moment. Therefore, one should not, for example, be surprised to see oil below USD 40 for a shorter period of time, depending on e.g. OPEC action. On top of the weak growth we could add closure of long commodity positions both from speculators and investors, but also from businesses that choose to close down loss-incurring commodity hedges entered into in the summer when the outlook for commodities was very different from today. Just as speculative activity might have added to prices in the first half of 2008, it cannot be ruled out that the opposite is now happening. Speculators are entering short positions to bet on an even more severe �global recession�. Hence, just as commodity prices might have �overshot� earlier in the year, it certainly cannot be ruled out that we are now seeing some sort of �undershooting�.

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 2

Energy

OPEC showing signs of indecisiveness

OPEC did not cut production at the extraordinary OPEC meeting in Cairo November 29 despite clear evidence that the oil market is over supplied. OPEC deferred a decision to the ordinary OPEC meeting on December 17. The inaction of OPEC is probably a key reason why oil is once again trading below USD 50 a barrel.

But in reality, OPEC�s inaction at the meeting was not the only important news from the meeting. We find it quite surprising that Saudi Arabia attacked the hawks of OPEC, notably Iran and Venezuela, for not complying with quotas, considering that both countries claim compliance. Probably the first sign that the cartel is starting to crack, at a time when it is maybe facing the toughest demand contraction in the history of OPEC. Historically it has proved very difficult for OPEC to stabilise oil prices and adhere to quotas when the global economy is heading for a recession. Consider the development in oil prices after the Asian crisis in 1998 or after 9/11 in 2001.

Another explanation for OPEC�s inaction could be that the cartel, or rather the Saudis, are trying to convince its fellow members of OPEC and e.g. Russia that it is of utmost importance this time to comply with quotas (and words in the case of Russia). Maybe a very timely warning, as the latest Reuters survey indicated that OPEC might only have slashed production by 66% of the 1.5 mb/d pledged by November 1.

The obvious question is of course how much oil OPEC will actually take off the market over the coming months in order to stabilize it. Comments by Saudi Minister Ali al-Naimi indicate that he thinks that if OPEC complied to the current 2 mb/d production cuts, everything would be fine. However, we very much doubt this will be the case. If OPEC only cut production by this amount we would see a significant further rise in OECD stocks. End-September OECD crude oil stocks were standing at 55 days forward cover � up more than two days compared to the 2003-2007 average.

If production is not cut further we could see a counter-seasonal build up in stocks in Q4 and Q1 next year, and we are sure that OPEC President Khelil has made this clear to his members. Hence, we base our forecast on the presumption that OPEC adheres 80% to its quotas and slashes quotas by another 1.5 mb/d at the December 17 meeting and follows up with a final albeit smaller cut in Q1 next year. Remember that many OPEC countries including Iran, Iraq and Venezuela, will face budgetary problems if oil prices stay at current levels. A problem magnified by the fact that OPEC oils trade at a significant discount to Brent and WTI.

As mentioned on the front page, we have revised our 2009 average oil price forecast down from USD 80 a barrel to USD 60. In the first two quarters we forecast around USD 50. But in line with better global economic growth in H2 2009, we expect prices to approach USD 75 by end-2009.

Our forecast oil price rise in H2 2009 depends, of course, on the slow global recovery that we forecast actually materializing. But it also depends on the supply side. Not just OPEC slashing production, but also that the market turns its attention to the slowdown in non-OPEC supply growth that we anticipate going forward.

Our view is that the current price collapse and the very difficult funding/credit situation will be a severe impediment for non-OPEC oil supply growth in 2009, and not least in 2010. Many oil companies operate with a hurdle-rate of USD65/barrel. Marginal costs today might be as high as USD 80 a barrel. Even though marginal costs are also falling at the moment, it could, according to the IEA, take 12-18 months before overall costs start to decline.

Oil investment plans are being slashed dramatically at the moment. Remember, that the IEA warned in connection with the release of the new Global Energy Outlook that the oil market might tighten again in 2010�2012 due to lack of investment. Looking into 2010�2012, oil prices could very well again trade above USD100/barrel. The current investment slowdown combined with a global economic recovery points to a very tight oil market in just a few years. The IEA has repeatedly warned about this negative effect of the current price collapse and the financial crisis

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 3

Two regions especially are suffering: Canada and Russia. In Canada, Suncor has already announced that it will cut investment by 30-40% in 2009. Hence, the outlook for supply growth from Canadian oil sands looks less promising even though the effect will mostly be felt in 2010. Russia is definitely an area in which oil production could disappoint heavily in 2009. Russian oil companies are very dependent on debt to finance investments, and with the current state of the Russian banking sector and the bleak outlook for the Russian economy, it does not bode well for Russian oil production going forward. Heavy export taxes also work as an impediment for Russian oil production at the moment even though this issue is expected to be resolved eventually. There are also growing signs that Russia is approaching OPEC. We doubt that Russia will take any direct part in production cuts. But production is expected to fall anyway in 2009.

We also note that the oil majors are talking about revising their investments plans. There are now indications that the upstream companies are trying to pressure the oil service companies, which during the five-year oil-boom generated very high profits. We also expect smaller debt-burdened oil companies to be forced to slash investment programmes and cancel rig orders going forward. The bleaker outlook is already reflected in lower rig rates and not least in the stock market, where oil service companies have seen their market value eroded heavily during the bear market. The latest survey by the IEA also showed that the so-called decline rates are on the rise. Hence, the need for investment is even higher, merely to keep production afloat. We forecast that non-OPEC production will be close to flat again in 2009, if not falling.

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 4

Energy � charts

Crude oil prices WTI futures curve

.

jan06

maj sep jan07

maj sep jan08

maj sep

perc

ent

40

60

80

100

120

140

perc

ent

40

60

80

100

120

140USD/barrel USD/barrel

WTI 1-pos, NYMEX

Brent, 1-pos

.

1 4 7 10 13 16

perc

ent

40

50

60

70

80

90

100

40

50

60

70

80

90

100

One month ago

USD/barrel

Last valid

Source: ECOWIN Source: ECOWIN

Natural Gas, Henry Hub, 1-pos Bunker fuel oil, 380 cst Amsterdam

.

jan06

maj sep jan07

maj sep jan08

maj sep

perc

ent

4

6

8

10

12

14

perc

ent

4

6

8

10

12

14 USD/mmBtu USD/mmBtu

.

jan06

maj sep jan07

maj sep jan08

maj sep

perc

ent

100

200

300

400

500

600

700

800

perc

ent

100

200

300

400

500

600

700

800 USD/ton USD/ton

Source: ECOWIN Source: ECOWIN

Gasoline RBOB, 1-pos NYMEX RBOB gasoline futures curve

.

jan06

maj sep jan07

maj sep jan08

maj sep

perc

ent

100

150

200

250

300

350

400

perc

ent

100

150

200

250

300

350

400 c/gallon c/gallon

.

0 1 2 3 4 5 6 7 8 9 10

perc

ent

1,0

1,1

1,2

1,3

1,4

1,5

1,6

1,7

1,8

perc

ent

1,0

1,1

1,2

1,3

1,4

1,5

1,6

1,7

1,8

one month ago

Last valid

USD/gallon USD/gallon

Source: ECOWIN Source: ECOWIN

Heating oil, 1-pos NYMEX Coal, 1-pos, API2

.

jan06

maj sep jan07

maj sep jan08

maj sep

perc

ent

100

150

200

250

300

350

400

450

perc

ent

100

150

200

250

300

350

400

450 c/gallon c/gallon

.

03 04 05 06 07 08

perc

ent

25

50

75

100

125

150

175

200

225

perc

ent

25

50

75

100

125

150

175

200

225 USD/ton USD/ton

Coal API2 1.pos. future

Source: ECOWIN Source: ECOWIN

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

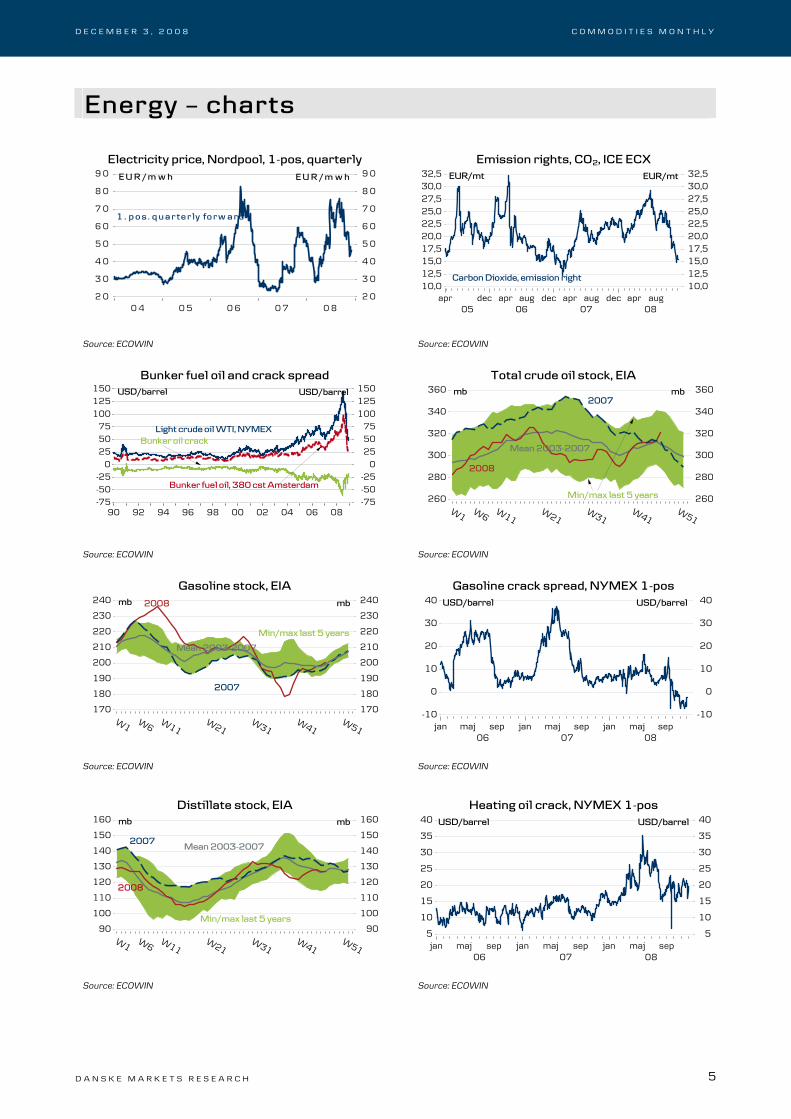

D A N S K E M A R K E T S R E S E A R C H 5

Energy � charts

Electricity price, Nordpool, 1-pos, quarterly Emission rights, CO2, ICE ECX

.

0 4 0 5 0 6 0 7 0 8

perc

ent

2 0

3 0

4 0

5 0

6 0

7 0

8 0

9 0

perc

ent

2 0

3 0

4 0

5 0

6 0

7 0

8 0

9 0

1 . p o s . q u a r t e r ly fo r w a r d

E U R / m w h E U R / m w h

.

apr05

dec06

apr aug dec07

apr aug dec08

apr aug

perc

ent

10,012,515,017,520,022,525,027,530,032,5

p

10,012,515,017,520,022,525,027,530,032,5

Carbon Dioxide, emission right

EUR/mt EUR/mt

Source: ECOWIN Source: ECOWIN

Bunker fuel oil and crack spread Total crude oil stock, EIA

.

90 92 94 96 98 00 02 04 06 08

perc

ent

-75-50-25

0255075

100125150

perc

ent

-75-50-25

0255075

100125150

Light crude oil WTI, NYMEX

USD/barrel USD/barrel

Bunker fuel oil, 380 cst Amsterdam

Bunker oil crack

W1 W6 W11W21

W31W41

W51

perc

ent(

milli

ons)

260

280

300

320

340

360

perc

ent (

milli

ons)

260

280

300

320

340

360

Mean 2003-2007

2007

2008

Min/max last 5 years

mb mb

Source: ECOWIN Source: ECOWIN

Gasoline stock, EIA Gasoline crack spread, NYMEX 1-pos

.

W1 W6 W11W21

W31W41

W51

perc

ent (

milli

ons)

170

180

190

200

210

220

230

240

perc

ent (

milli

ons)

170

180

190

200

210

220

230

240

Mean 2003-2007

2008

Min/max last 5 years

mb mb

2007

jan06

maj sep jan07

maj sep jan08

maj seppe

rcen

t-10

0

10

20

30

40

p

-10

0

10

20

30

40 USD/barrel USD/barrel

Source: ECOWIN Source: ECOWIN

Distillate stock, EIA Heating oil crack, NYMEX 1-pos

.

W1 W6 W11W21

W31W41

W51

perc

ent (

milli

ons)

90

100

110

120

130

140

150

160

perc

ent (

milli

ons)

90

100

110

120

130

140

150

160 mb

Mean 2003-2007

Min/max last 5 years

2008

mb

2007

jan06

maj sep jan07

maj sep jan08

maj sep

perc

ent

5

10

15

20

25

30

35

40

5

10

15

20

25

30

35

40 USD/barrel USD/barrel

Source: ECOWIN Source: ECOWIN

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 6

Base metals PMI �s plummet and push base metal even lower

The immense pressure on commodity prices, not least the cyclical sensitive base metals, continued in November. The fact that global manufacturing PMI�s plummeted in November does not bode well for demand in the current quarter for base metals. Global construction and other investments seem to have almost come to a halt at the moment and certainly adds to worries in the market.

The pressure on the base metal markets is evident in the stock build we are seeing across the board. Aluminium and copper LME stocks rose 19% and 23% in November. However, the rising stocks might also reflect both consumers and producers trying to create liquidity by delivering metal to warehouses. It is also said in the market that many companies need an exchange registered warrant to get finance for new raw material inventory. But even these anomalies cannot hide that the base metal market will remain soft for a prolonged period. There is simply an oversupply at the moment that has to be worked off.

We have earlier argued that many base metals are trading below marginal costs. Especially we have pointed to aluminium where the downside should be protected. But we have to admit that at the moment marginal costs are now falling very quickly. The combination of falling energy, alumina, shipping and even labour costs all work in favour of lower production costs. But even taking this into account, a significant fraction of e.g. aluminium production is now being produced at a loss.

However, as we wrote in the energy section, another side effect of the ongoing financial crisis and slide in commodity prices is emerging in the form of an increasingly serious negative impact on the supply of commodities and investment plans. Nickel producers are one area where the market has already begun to adapt to the new world order. The drop in global stainless steel production in the past couple of months will probably continue in the coming months, and production cuts of up to 8% for nickel and 5-6% for aluminium have already been announced. So far these production cuts have been ignored by the market, as there has also been a huge drop in demand and stock building. However, if demand starts to stabilise and then recover, a number of commodity markets could tighten again. But for now this is probably an H2 2009 story when it comes to the base metal complex.

In line with our new oil forecast we have also revised our base metal forecasts lower. Basically we think that the market is about to form a bottom. But again it is like catching a falling knife. But it seems that a very negative growth trajectory is priced into spot prices. If we are right that the growth outlook should improve somewhat during 2009, this should mean higher prices over the course of 2009. We expect aluminium and copper prices at USD 2,400 and USD 4,700 a tonne at end-2009. But we do not expect significantly higher prices for the next 3-6 months. Our average forecast prices for 2009 for aluminium and copper are USD 2,100 and USD 4,225 a tonne, respectively.

Global PMI�s in free fall

.

02 03 04 05 06 07 08

perc

ent

38

42

46

50

54

58

perc

ent

38

42

46

50

54

58 Net figure Net figure

G4 manufacturing PMI

Emerging Markets Manufacturing PMI

China PMI

Putting pressure on base metals

.../figurbibliotek/

90 92 94 96 98 00 02 04 06 08

perc

ent

37,5

42,5

47,5

52,5

57,5

62,5

perc

ent

-80

-60

-40

-20

0

20

40

60

80 Index<< Copper. LME

ISM >>

% y/y

<< Aluminium

Copper, LME

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 7

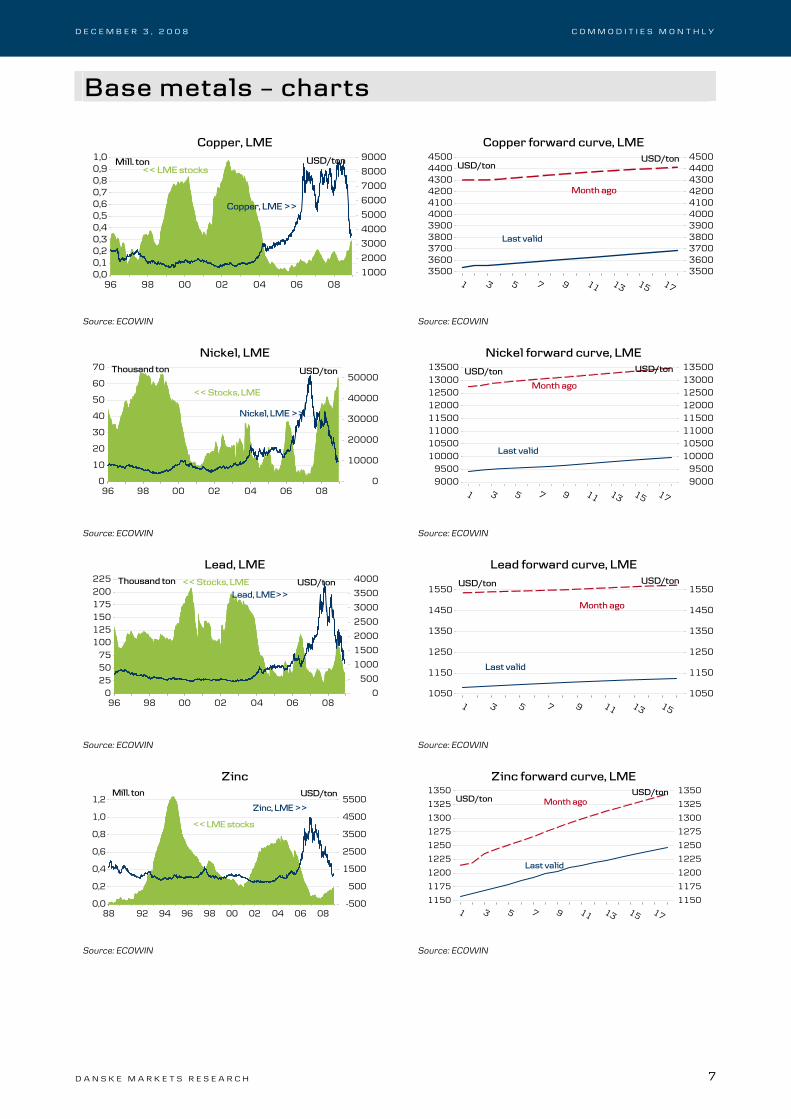

Base metals � charts

Copper, LME Copper forward curve, LME

.

96 98 00 02 04 06 08

perc

ent

1000

2000

3000

4000

5000

6000

7000

8000

9000

perc

ent (

milli

ons)

0,00,10,20,30,40,50,60,70,80,91,0

Copper, LME >>

<< LME stocksUSD/tonMill. ton

1 3 5 7 9 11 13 15 17

perc

ent

35003600370038003900400041004200430044004500

perc

ent

35003600370038003900400041004200430044004500

USD/tonUSD/ton

Last valid

Month ago

Source: ECOWIN Source: ECOWIN

Nickel, LME Nickel forward curve, LME

.

96 98 00 02 04 06 08

perc

ent

0

10000

20000

30000

40000

50000

perc

ent (

thou

sand

s)

0

10

20

30

40

50

60

70

Nickel, LME >>

<< Stocks, LME

USD/tonThousand ton

1 3 5 7 9 11 13 15 17

perc

ent

90009500

1000010500110001150012000125001300013500

perc

ent

90009500

1000010500110001150012000125001300013500 USD/ton USD/ton

Month ago

Last valid

Source: ECOWIN Source: ECOWIN

Lead, LME Lead forward curve, LME

.

96 98 00 02 04 06 08

perc

ent

0

500

1000

1500

2000

2500

3000

3500

4000

perc

ent (

thou

sand

s)

0255075

100125150175200225

Lead, LME>><< Stocks, LME USD/tonThousand ton

1 3 5 7 9 11 13 15pe

rcen

t

1050

1150

1250

1350

1450

1550

perc

ent

1050

1150

1250

1350

1450

1550USD/ton USD/ton

Last valid

Month ago

Source: ECOWIN Source: ECOWIN

Zinc Zinc forward curve, LME

.

88 92 94 96 98 00 02 04 06 08

perc

ent

-500

500

1500

2500

3500

4500

5500

perc

ent (

milli

ons)

0,0

0,2

0,4

0,6

0,8

1,0

1,2Zinc, LME >>

<< LME stocks

USD/tonMill. ton

.

1 3 5 7 9 11 13 15 17

perc

ent

1150

1175

1200

1225

1250

1275

1300

1325

1350

perc

ent

1150

1175

1200

1225

1250

1275

1300

1325

1350USD/ton

USD/ton

Last valid

Month ago

Source: ECOWIN Source: ECOWIN

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 8

Aluminium, LME Aluminium forward curve, LME

.

96 98 00 02 04 06 08

perc

ent

1000

1500

2000

2500

3000

3500

perc

ent (

milli

ons)

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

<< Stocks, LME

USD/tonMill. ton

Aluminium, LME >>

.

1 3 5 7 9 11 13 15 17

perc

ent

1600

1700

1800

1900

2000

2100

2200

2300

2400

perc

ent

1600

1700

1800

1900

2000

2100

2200

2300

2400 USD/ton USD/ton

Month ago

Last valid

Source: ECOWIN Source: ECOWIN

Tin, LME Tin forward curve, LME

.

96 98 00 02 04 06 08

perc

ent

2500

7500

12500

17500

22500

27500

perc

ent

-5000

5000

15000

25000

35000

45000

Tin, LME >><< Stocks, LME

USD/tonTon

.

1 3 5 7 9 11 13 15

perc

ent

11500

12000

12500

13000

13500

14000

14500

15000

15500

perc

ent

11500

12000

12500

13000

13500

14000

14500

15000

15500 USD/ton USD/ton

Last valid

Month ago

Source: ECOWIN Source: ECOWIN

Metal price index and ISM Metal price index and ifo

.../figurbibliotek/

90 92 94 96 98 00 02 04 06 08

perc

ent

37,5

42,5

47,5

52,5

57,5

62,5

perc

ent

-80

-60

-40

-20

0

20

40

60

80 Index<< Metal price index

ISM >>

% y/y

.../figurbibliotek/

94 96 98 00 02 04 06 08

perc

ent

-30

-20

-10

0

10

20

30

40

perc

ent

-60

-40

-20

0

20

40

60

80 Value y/y

<< Metal price index

% y/yifo business indicator, Germany >>

Source: ECOWIN Source: ECOWIN

Steel Billets, LME Stainless steel

.

jan08

mar maj jul sep nov

perc

ent

200

400

600

800

1000

1200

perc

ent

200

400

600

800

1000

1200USD/ton USD/ton

Steel Billet future, LME Mediterranean

Steel Billet future, LME Far East

.

01 02 03 04 05 06 07 08

perc

ent

1000

2000

3000

4000

5000

6000

perc

ent

1000

2000

3000

4000

5000

6000 USD/ton

Stainless steel, CR type 304

USD/ton

Source: ECOWIN Source: ECOWIN

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 9

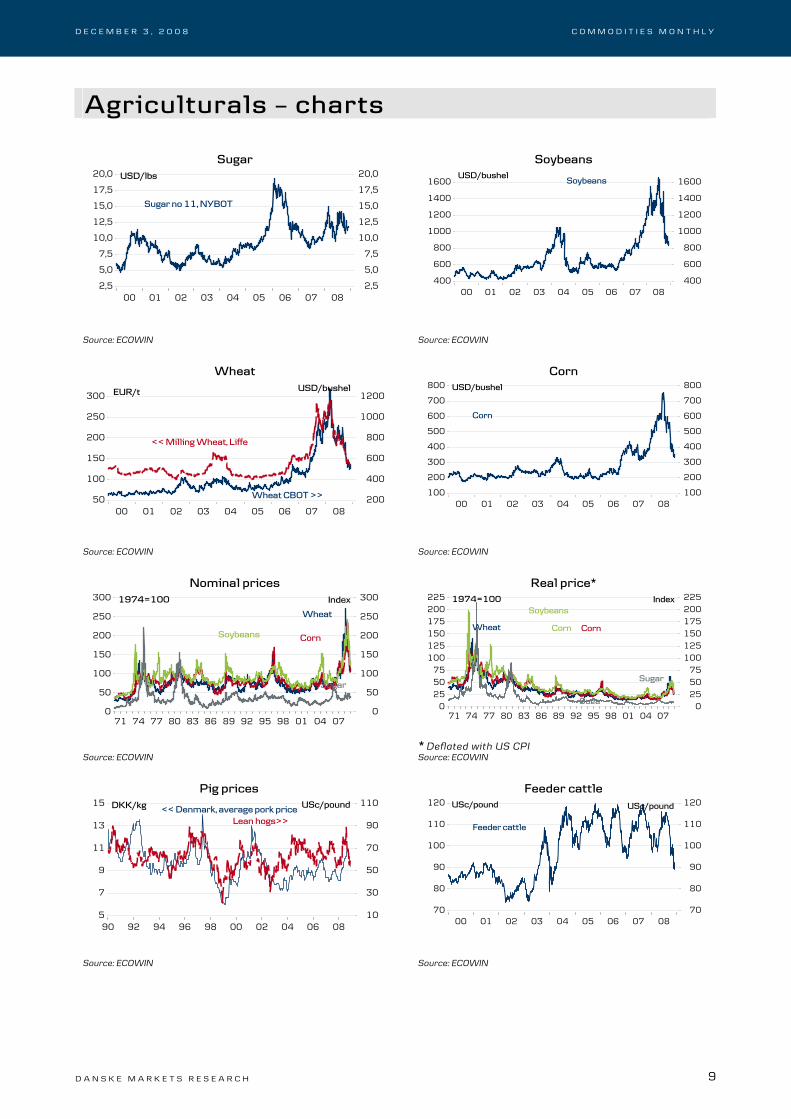

Agriculturals � charts

Sugar Soybeans

.

00 01 02 03 04 05 06 07 08

perc

ent

2,5

5,0

7,5

10,0

12,5

15,0

17,5

20,0

perc

ent

2,5

5,0

7,5

10,0

12,5

15,0

17,5

20,0

Sugar no 11, NYBOT

USD/lbs

.

00 01 02 03 04 05 06 07 08

perc

ent

400

600

800

1000

1200

1400

1600

perc

ent

400

600

800

1000

1200

1400

1600 SoybeansUSD/bushel

Source: ECOWIN Source: ECOWIN

Wheat Corn

00 01 02 03 04 05 06 07 08200

400

600

800

1000

1200

50

100

150

200

250

300

Wheat CBOT >>

EUR/t

<< Milling Wheat, Liffe

USD/bushel

.

00 01 02 03 04 05 06 07 08

perc

ent

100

200

300

400

500

600

700

800

perc

ent

100

200

300

400

500

600

700

800

Corn

USD/bushel

Source: ECOWIN Source: ECOWIN

Nominal prices Real price*

.

71 74 77 80 83 86 89 92 95 98 01 04 07

perc

ent

0

50

100

150

200

250

300

perc

ent

0

50

100

150

200

250

300

Sugar

Wheat

1974=100

CornSoybeans

Index

.

71 74 77 80 83 86 89 92 95 98 01 04 07pe

rcen

t0

255075

100125150175200225

perc

ent

0255075

100125150175200225

Sugar

Wheat

1974=100 Index

Suga

Corn

Soybeans

Corn

* Deflated with US CPI

Source: ECOWIN Source: ECOWIN

Pig prices Feeder cattle

.

90 92 94 96 98 00 02 04 06 08

perc

ent

10

30

50

70

90

110

perc

ent

5

7

9

11

13

15 DKK/kg << Denmark, average pork priceLean hogs>>

USc/pound

.

00 01 02 03 04 05 06 07 08

perc

ent

70

80

90

100

110

120

perc

ent

70

80

90

100

110

120 USc/pound USc/pound

Feeder cattle

Source: ECOWIN Source: ECOWIN

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 10

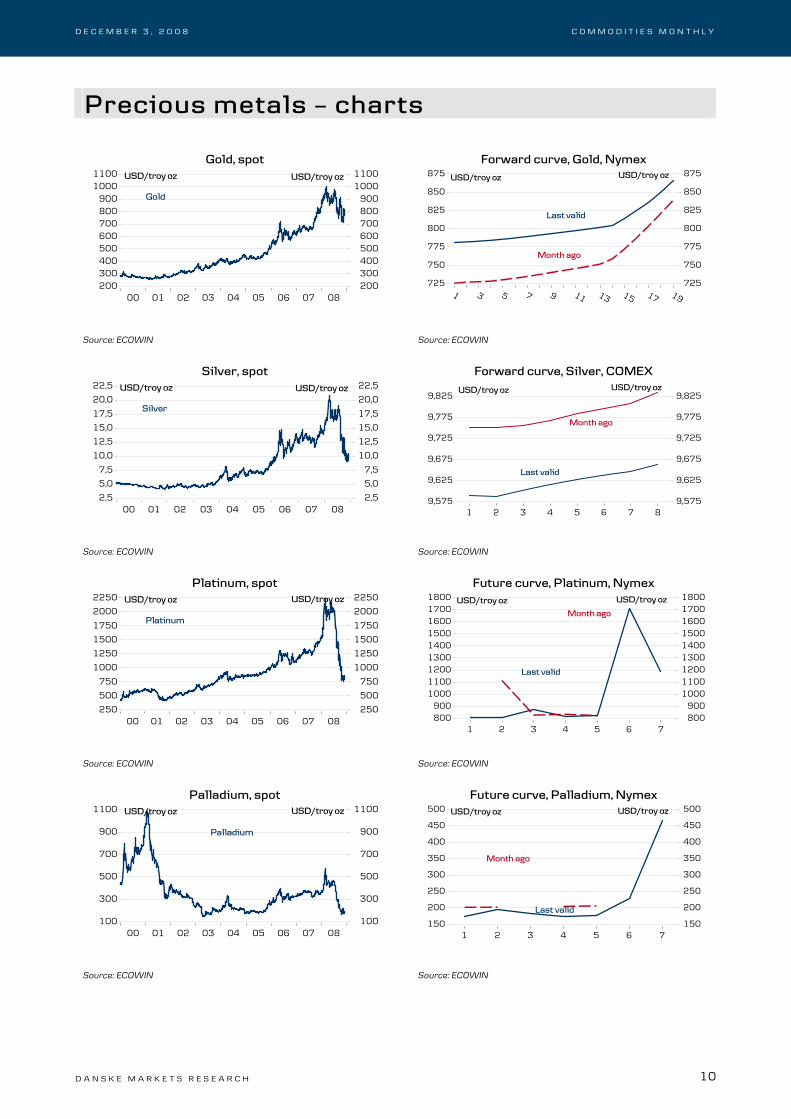

Precious metals � charts

Gold, spot Forward curve, Gold, Nymex

.

00 01 02 03 04 05 06 07 08

perc

ent

200300400500600700800900

10001100

perc

ent

200300400500600700800900

10001100 USD/troy oz USD/troy oz

Gold

.

1 3 5 7 9 11 13 15 17 19

perc

ent

725

750

775

800

825

850

875

perc

ent

725

750

775

800

825

850

875 USD/troy oz USD/troy oz

Last valid

Month ago

Source: ECOWIN Source: ECOWIN

Silver, spot Forward curve, Silver, COMEX

.

00 01 02 03 04 05 06 07 08

perc

ent

2,5

5,0

7,5

10,0

12,5

15,0

17,5

20,0

22,5

perc

ent

2,5

5,0

7,5

10,0

12,5

15,0

17,5

20,0

22,5 USD/troy oz USD/troy oz

Silver

.

1 2 3 4 5 6 7 8

perc

ent

9,575

9,625

9,675

9,725

9,775

9,825

perc

ent

9,575

9,625

9,675

9,725

9,775

9,825USD/troy oz USD/troy oz

Last valid

Month ago

Source: ECOWIN Source: ECOWIN

Platinum, spot Future curve, Platinum, Nymex

.

00 01 02 03 04 05 06 07 08

perc

ent

250

500

750

1000

1250

1500

1750

2000

2250

perc

ent

250

500

750

1000

1250

1500

1750

2000

2250 USD/troy oz USD/troy oz

Platinum

.

1 2 3 4 5 6 7

perc

ent

800900

100011001200130014001500160017001800

perc

ent

800900

100011001200130014001500160017001800 USD/troy oz USD/troy oz

Last valid

Month ago

Source: ECOWIN Source: ECOWIN

Palladium, spot Future curve, Palladium, Nymex

.

00 01 02 03 04 05 06 07 08

perc

ent

100

300

500

700

900

1100

perc

ent

100

300

500

700

900

1100 USD/troy oz USD/troy oz

Palladium

.

1 2 3 4 5 6 7

perc

ent

150

200

250

300

350

400

450

500

perc

ent

150

200

250

300

350

400

450

500 USD/troy oz USD/troy oz

Last valid

Month ago

Source: ECOWIN Source: ECOWIN

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 11

Technical outlook Technical Analyst Klaus Ikast, + 45 45128501, [email protected] / [email protected] Tehnical Analyst Kim Cramer Larsson, + 45 45128499, [email protected] / [email protected]

Recovery in Corn. Every month we take a closer technical look at a specific commodity. This time we take a look at Corn.

Corn has made a bearish move since its peak in June 2008 and is now testing the strong support area at around 322-355. The support is the TDST line at 335 which is just above the 76.4 retracement level at around 322 based on the bullish trend starting in 2005. A trough to 322 could be seen before a recovery. A recovery that could take Corn back to 495, which then would be the 38.2 retracement of the recent bearish move. Look out for strong resistance at around 431. A break below 308 could trigger a further sell-off.

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 12

Commodity prices

01-12-2008

Price Price %, m/m Price %, y/y Start level

EnergyNYMEX WTI - 1.pos. 52,0 67,8 -23,3 88,7 -41,4 96,0 -45,8

116,6 144,2 -19,2 226,0 -48,4 247,7 -52,9ICE Brent 1.pos. 51,5 65,4 -21,4 88,4 -41,8 94,0 -45,3ICE Carbon (�/tn), DEC-08 16,1 18,0 -10,4 22,4 -28,1 22,4 -28,2Electricity Nord Pool,�, 1.month 50,0 57,7 -13,3 - - - - -TTF Natural Gas,�, 1st. month 24,4 31,0 -21,5 - 14,1 24,6 -1,0Natural Gas, Nymex, 1.pos. 6,5 6,8 -4,0 7,3 -10,8 7,5 -13,0API2, steam coal, 1st month 89,7 100,7 -10,9 128,2 -30,0 125,0 -28,2

Aluminium 1.772 2.110 -16,02 2.510 -29,40 2.409 -26,44Copper 3.620 4.130 -12,35 6.715 -46,09 6.675 -45,77Lead 1.103 1.470 -24,97 3.030 -63,60 2.550 -56,75Nickel 10.200 11.970 -14,79 28.100 -63,70 26.300 -61,22Zinck 1.210 1.150 5,22 2.490 -51,41 2.370 -48,95

Gold 791,7 723,3 9,4 782,5 1,2 832,7 -4,9Silver 9,9 9,9 0,7 14,0 -29,2 14,8 -33,0

CBOT Wheat (US$/bushel) 547,3 557,0 -1,8 778,3 -29,7 795,3 -31,2Matif Mill Wheat (�/t) 132,3 144,0 -8,2 250,0 -47,1 251,0 -47,3CBOT Corn (US$/bushel) 361,0 402,0 -10,2 385,0 -6,2 456,0 -20,9CBOT Soybeans (US$/bushel) 867,0 925,8 -6,4 1.080,5 -19,8 1.199,5 -27,7NYBOT Sugar (US$/lb) 11,8 12,0 -2,0 9,7 20,8 10,8 8,9

Commodity indiciesReuters/CRB TR 242,2 268,4 -9,8 339,8 -28,7 358,7 -32,5S&P GSCI Energy TR 1.139,6 1.307,4 -12,8 1.828,0 -37,7 1.918,8 -40,6S&P GSCI Industrial Metals TR 1.051,6 1.225,8 -14,2 1.914,4 -45,1 1.835,6 -42,7S&P GSCI Agriculture TR 550,2 553,3 -0,6 786,6 -30,1 833,7 -34,0S&P GSCI Precious Metals TR 1.052,5 949,8 10,8 1.089,9 -3,4 1.133,1 -7,1AIG 122,8 132,0 -7,0 177,2 -30,7 185,0 -33,6Rogers commodity index TR 2.721,4 3.136,3 -13,2 4.208,5 -35,3 4.420,1 -38,4

Steel prices (EUR/t)EU domestic hot rolled coil 670,0 670,0 0,0 500,0 34,0 500,0 34,0EU domestic cold rolled coil 735,0 735,0 0,0 560,0 31,3 560,0 31,3EU domestic hotdip galv. Coil 837,5 837,5 0,0 610,0 37,3 610,0 37,3

Preciuos Metals: Spot Prices (US$/oz)

Agriculturals: Front Month Prices

Month ago Year ago This year

Base metals: LME 3M Prices (US$/t)

NYMEX Gasoline RBOB (Usc/gln) 1.pos.

YTD change, %

Source: ECOWIN

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 13

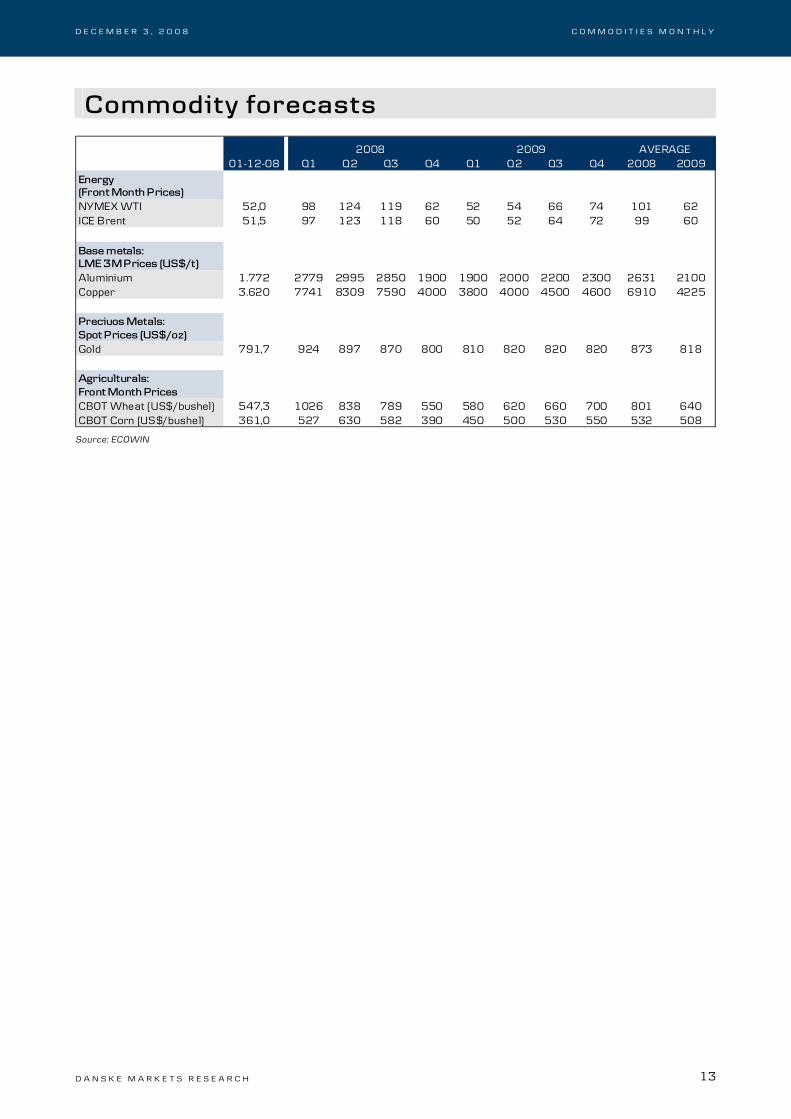

Commodity forecasts

2009 AVERAGE01-12-08 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2008 2009

NYMEX WTI 52,0 98 124 119 62 52 54 66 74 101 62ICE Brent 51,5 97 123 118 60 50 52 64 72 99 60

Aluminium 1.772 2779 2995 2850 1900 1900 2000 2200 2300 2631 2100Copper 3.620 7741 8309 7590 4000 3800 4000 4500 4600 6910 4225

Gold 791,7 924 897 870 800 810 820 820 820 873 818

CBOT Wheat (US$/bushel) 547,3 1026 838 789 550 580 620 660 700 801 640CBOT Corn (US$/bushel) 361,0 527 630 582 390 450 500 530 550 532 508

2008

Agriculturals: Front Month Prices

Preciuos Metals: Spot Prices (US$/oz)

Base metals: LME 3M Prices (US$/t)

Energy (Front Month Prices)

Source: ECOWIN

D E C E M B E R 3 , 2 0 0 8 C O M M O D I T I E S M O N T H L Y

D A N S K E M A R K E T S R E S E A R C H 14

This report has been prepared by Danske Research, which is part of Danske Markets, a division of Danske Bank. Danske Bank is under supervision by the Danish Financial Supervisory Authority. Danske Bank has established procedures to prevent conflicts of interest and to ensure the provision of high quality research based on research objectivity and independence. These procedures are documented in the Danske Bank Research Policy. Employees within the Danske Bank Research Departments have been instructed that any request that might impair the objectivity and independence of research shall be referred to Research Management and to the Compliance Officer. Danske Bank Research departments are organised independently from and do not report to other Danske Bank business areas. Research analysts are remunerated in part based on the over-all profitability of Danske Bank, which includes investment banking revenues, but do not receive bonuses or other remuneration linked to specific corporate finance or dept capital transactions. Danske Bank research reports are prepared in accordance with the Danish Society o f investment Professionals� Ethical rules and the Recommendations of the Danish and Norwegian Securities Dealers Associations. Financial models and/or methodology used in this report Calculations and presentations in this report are based on standard econometric tools and methodology as well as publicly available statistics for each individual country. Documentation can be obtained from the above named authors upon request. Risk warning Major risks connected with recommendations or opinions in this report, including as sensitivity analysis of relevant assumptions, are stated throughout the text. First date of publication Please see the front page of this research report. Disclaimer This publication has been prepared by Danske Markets for information purposes only. It is not an offer or solicitation of any offer to purchase or sell any financial instrument. Whilst reasonable care has been taken to ensure that its contents are not untrue or misleading, no representation is made as to its accuracy or completeness and no liability is accepted for any loss arising from reliance on it. Danske Bank, its affiliates or staff, may perform services for, solicit business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives), of any issuer mentioned herein. The Equity and Corporate Bonds analysts are not permitted to invest in securities under coverage in their research sector. This publication is not intended for retail customers in the UK or any person in the US. Danske Markets is a division of Danske Bank A/S. Danske Bank A/S is authorized by the Danish Financial Supervisory Authority and subject to limited regulation by the Financial Services Authority (UK). Details on the extent of our regulation by the Financial Services Authority are available from us on request. Copyright © Danske Bank A/S. All rights reserved. This publication is protected by copyright and may not be reproduced in whole or in part without permission