commodity futures trading commission ule … · rbccm’s business activities and financial data...

TRANSCRIPT

COMMODITY FUTURES TRADING COMMISSION RULE 1.55(k):

FCM-SPECIFIC DISCLOSURE DOCUMENT

The Commodity Futures Trading Commission (“Commission” or the “CFTC”) requires each

futures commission merchant (FCM), including RBC Capital Markets, LLC (“RBCCM” or

“the Firm”), to provide the following information to a customer prior to the time the customer

first enters into an account agreement with the FCM or deposits money or securities (funds)

with the FCM.1 Except as otherwise noted below, the information contained herein is as of

July 11, 2017.

RBCCM will update this information annually, and as necessary, to account for any material

change to its business operations, financial condition or other factors that RBCCM believes

may be material to a customer’s decision to do business with the Firm. Nonetheless,

RBCCM’s business activities and financial data are not static and will change in non-material

ways frequently throughout any 12-month period.

Information that may be material with respect to RBCCM for purposes of the Commission’s

disclosure requirements may not be material to RBC USA Holdco Corporation for purposes of

applicable securities laws. RBCCM is a wholly-owned subsidiary of RBC USA Holdco

Corporation (the “Parent”), which is a wholly-owned subsidiary of Royal Bank of Canada

(“RBC”). The Parent is the Intermediate Holding Company (IHC) consolidating US operations

as mandated by the Enhanced Prudential Standards of Dodd-Frank Act. The consolidated

statement of financial condition includes wholly-owned subsidiaries, and is available at

www.rbccm.com. RBCCM’s Designated Self-Regulatory Organization is the CME Group,

www.cmegroup.com. RBCCM’s financial information reports can also be found by conducting

a search for RBCCM in National Futures Association’s (“NFA”) BASIC system

(http://www.nfa.futures.org/basicnet/) and then clicking on “View Financial Information” on the

RBCCM’s BASIC Details page.

Pursuant to CFTC Rule Sections 1.55(k)(1) and (k)(2), the following is relevant information

about RBCCM, including, name, title, business address, business background, areas of

responsibility and the nature of the duties of each principal as defined in § 3.1(a) (Individuals

listed as Principals with the National Futures Association (“NFA”)). This information is up to

date as of April 2018.

Firm and its Principals

RBC Capital Markets, LLC

Three World Financial Center

200 Vesey Street, 8th fl.

New York, NY 10281

1 The objective of the disclosures is to provide prospective and existing customers of RBCCM with material

information in determining whether to engage in a relationship with the Firm.

2

Phone: 212-858-7000

Fax number: 212-428-2370

Email: [email protected]

The following individuals are located at 200 Vesey Street, New York, NY, 10281:

Fleming, Blair, Managing Director (“MD”), Chief Executive Officer & Chairman of the Board

Downie, David, MD & Chief Risk Officer

Kachenoura, Ahmed, MD, Head of Global Equity-Linked Products & Board Member

The following individuals are located at 30 Hudson Street, Jersey City, NJ, 07302

Chiulli, Eugene, MD, Chief Financial Officer

Bailey, Elizabeth, MD, Chief Compliance Officer

Thurlow, John J., MD, Chief Operating Officer & Board Member

Murphy, Thomas, MD, Head, US CM Operations

The following individuals are located at 60 S 6th Street, Minneapolis, MN, 55402:

Armstrong, Robert Michael, CEO, US Wealth Management

Sagissor, Thomas, SR. VP, President, RBC Wealth Management & Board Member

Thorne, Brett, VP, Head Correspondent & Advisor Services & Board Member

The following individuals are located at 200 Bay Street – South Tower, Toronto, ON, M5J

2J5, Canada:

Maxwell, V. Troy, Chief Operating Officer

Ahn, Nadine, SVP, CFO Capital Markets Finance, Board Member

Neldner, Derek, Head of Canadian Investment Banking, Board Member

The following individual is located at 1918 8th Ave, Suite 3600, Seattle, WA, 98101:

Rasmusson, Karen, VP, Manager, Risk

The following individual is located at 1801 California Street, Suite 3900, Denver, CO, 80202:

Traweek, Darryl, Sr. VP, Divisional Director, West

The following parents are registered at Corporation Service Company, 2711 Centerville

Road, Suite 400, Wilmington, DE, 19808:

RBC USA Holdco Corporation, Direct Parent (99% ownership)

RBC CM Member Corp., Direct Parent (1% ownership)

Firm’s Business

CFTC Rule Section 1.55(k)(3) requires disclosure by an FCM of significant types of activities

and product lines that the FCM engages in and the approximate percentage of assets and capital

that are contributed to each type of business activity or product line. Further, the regulation is

intended to provide the public with information concerning the major business activities

engaged in by RBCCM as a registered FCM, so that a customer may be informed with regard

to applicable benefits and risks when conducting transactions in commodity interests. This

includes material business activities by RBCCM as the FCM.

3

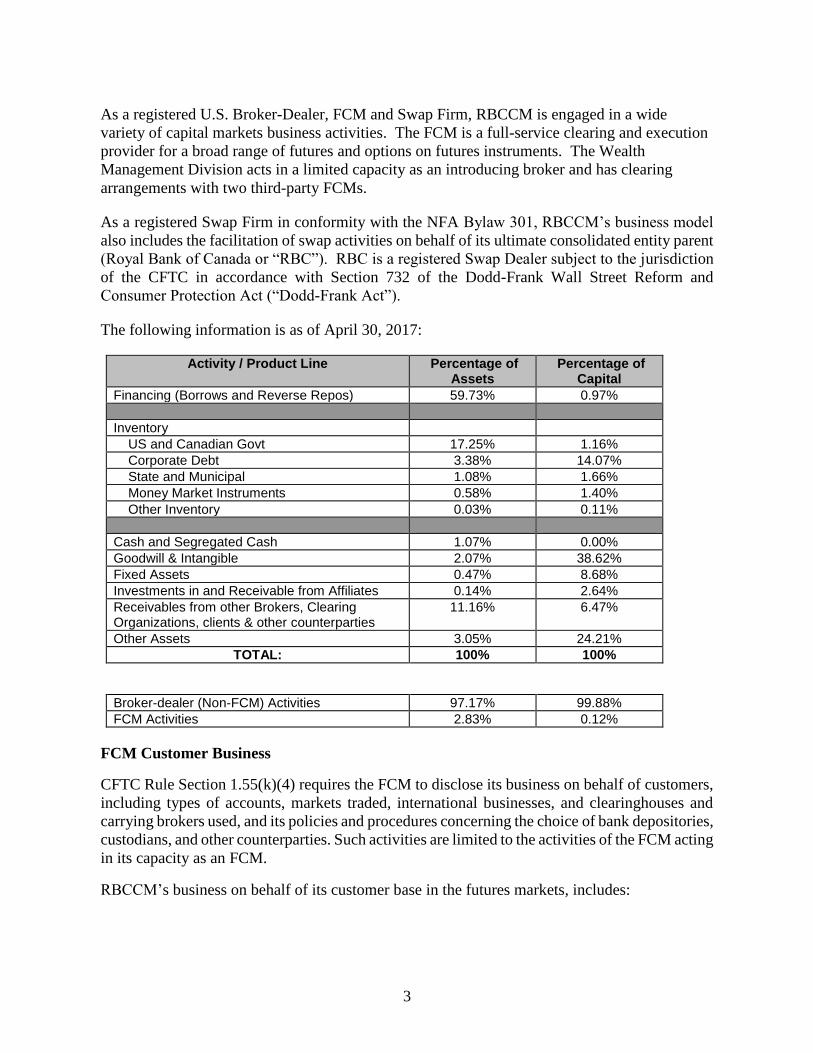

As a registered U.S. Broker-Dealer, FCM and Swap Firm, RBCCM is engaged in a wide

variety of capital markets business activities. The FCM is a full-service clearing and execution

provider for a broad range of futures and options on futures instruments. The Wealth

Management Division acts in a limited capacity as an introducing broker and has clearing

arrangements with two third-party FCMs.

As a registered Swap Firm in conformity with the NFA Bylaw 301, RBCCM’s business model

also includes the facilitation of swap activities on behalf of its ultimate consolidated entity parent

(Royal Bank of Canada or “RBC”). RBC is a registered Swap Dealer subject to the jurisdiction

of the CFTC in accordance with Section 732 of the Dodd-Frank Wall Street Reform and

Consumer Protection Act (“Dodd-Frank Act”).

The following information is as of April 30, 2017:

Activity / Product Line Percentage of Assets

Percentage of Capital

Financing (Borrows and Reverse Repos) 59.73% 0.97%

Inventory

US and Canadian Govt 17.25% 1.16%

Corporate Debt 3.38% 14.07%

State and Municipal 1.08% 1.66%

Money Market Instruments 0.58% 1.40%

Other Inventory 0.03% 0.11%

Cash and Segregated Cash 1.07% 0.00%

Goodwill & Intangible 2.07% 38.62%

Fixed Assets 0.47% 8.68%

Investments in and Receivable from Affiliates 0.14% 2.64%

Receivables from other Brokers, Clearing Organizations, clients & other counterparties

11.16%

6.47%

Other Assets 3.05% 24.21%

TOTAL: 100% 100%

Broker-dealer (Non-FCM) Activities 97.17% 99.88%

FCM Activities 2.83% 0.12%

FCM Customer Business

CFTC Rule Section 1.55(k)(4) requires the FCM to disclose its business on behalf of customers,

including types of accounts, markets traded, international businesses, and clearinghouses and

carrying brokers used, and its policies and procedures concerning the choice of bank depositories,

custodians, and other counterparties. Such activities are limited to the activities of the FCM acting

in its capacity as an FCM.

RBCCM’s business on behalf of its customer base in the futures markets, includes:

4

Types of customers: Institutional (Corporations, Commodity Pools, Hedge Funds,

Asset Managers, Pension Funds, Banks, Trusts, Insurance Companies); Commercial

(Agricultural, Energy) and Affiliates;

Markets traded: Equity Index, Interest Rates, FX, Agricultural, Energy and Metals

International businesses: Canada, Europe, Asia, Australia

Exchange Memberships:

Clearinghouses used (as of April 2018): member, non-member

Clearing Organization RBCCM is

the Member

RBCCM

Affiliate is the

Member

Non Affiliate

Clearing

Broker

Asigna Compensacion y

Liquidacion (Mexico) X

ASX Clear (Australia) X

ATHEXClear (Greece) X

BM&F (Brazil) X

BME Clearing (Spain) X

Bursa Malaysia Derivatives

Clearing Bhd X

Canadian Derivatives

Clearing Corporation

(Canada) X

Cassa di Compensazione e

Garanzia S.p.A. (CC&G)

(Italy) X

Exchange Memberships

CBOE Futures Exchange Nodal Exchange LLC

Chicago Board of Trade ICE Futures Europe

Chicago Mercantile Exchange, Inc. Eurex Exchange (NCM)

Commodity Exchange Inc. Euronext Paris (NCM)

ICE Futures US, Inc.

Nasdaq Futures Exchange

New York Mercantile Exchange, Inc.

5

Central Clearing House &

Depository Ltd (Hungary) X

CME Clear - Futures and

OTC Interest Rates X

DCCC (Dubai) X

Eurex Clearing X

HKFE Clearing X

ICE Clear Canada X

ICE Clear Europe X X

ICE Clear Singapore X

ICE Clear US X

Japan Commodity Clearing

House Co Ltd (JCCH) X

Japanese Securities

Clearing Corporation X

KDPW (Poland) X

KRX (Korea) X

LCH Clearnet LLC X

LCH Clearnet Limited X

LCH Clearnet SA X

LME Clear X

Minneapolis Grain

Exchange Clearing House X

Nasdaq Clearing AB (OMX

- Sweden) X

Nodal Clear X

NSCCL (India) X

Options Clearing

Corporation (OCC) X

JSE Clear (South Africa) X

Singapore Exchange

Derivatives Clearing X

TAIFEX Clearing (Taiwan) X

Takasbank (Turkey) X

Tel Aviv Stock Exchange

Clearing House X

6

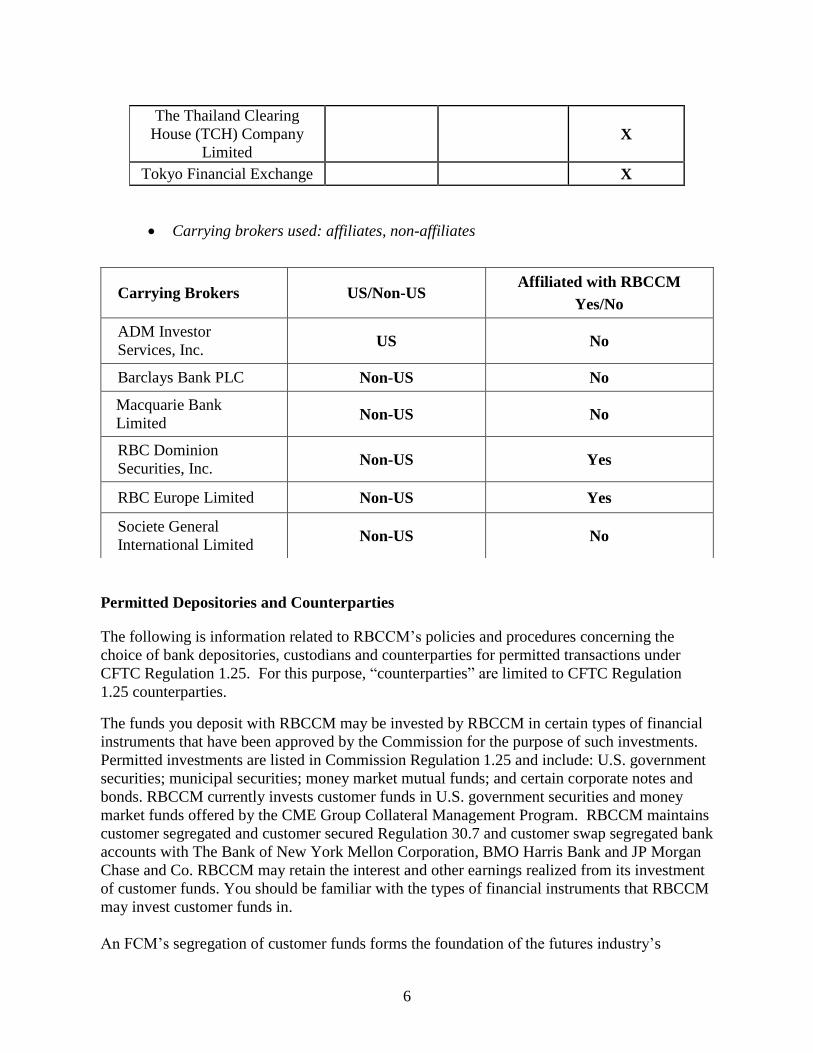

The Thailand Clearing

House (TCH) Company

Limited X

Tokyo Financial Exchange X

Carrying brokers used: affiliates, non-affiliates

Permitted Depositories and Counterparties

The following is information related to RBCCM’s policies and procedures concerning the

choice of bank depositories, custodians and counterparties for permitted transactions under

CFTC Regulation 1.25. For this purpose, “counterparties” are limited to CFTC Regulation

1.25 counterparties.

The funds you deposit with RBCCM may be invested by RBCCM in certain types of financial

instruments that have been approved by the Commission for the purpose of such investments.

Permitted investments are listed in Commission Regulation 1.25 and include: U.S. government

securities; municipal securities; money market mutual funds; and certain corporate notes and

bonds. RBCCM currently invests customer funds in U.S. government securities and money

market funds offered by the CME Group Collateral Management Program. RBCCM maintains

customer segregated and customer secured Regulation 30.7 and customer swap segregated bank

accounts with The Bank of New York Mellon Corporation, BMO Harris Bank and JP Morgan

Chase and Co. RBCCM may retain the interest and other earnings realized from its investment

of customer funds. You should be familiar with the types of financial instruments that RBCCM

may invest customer funds in.

An FCM’s segregation of customer funds forms the foundation of the futures industry’s

Carrying Brokers US/Non-US Affiliated with RBCCM

Yes/No

ADM Investor

Services, Inc. US No

Barclays Bank PLC Non-US No

Macquarie Bank

Limited Non-US No

RBC Dominion

Securities, Inc. Non-US Yes

RBC Europe Limited Non-US Yes

Societe General

International Limited Non-US No

7

customer protection regime. Funds that customers deposit with RBCCM, or that are otherwise

required to be held for the benefit of customers, to margin futures and options on futures

contracts traded on futures markets located in the United States, must be held in a customer

segregated funds account pursuant to Section 4d(a)(2) of the Commodity Exchange Act and

CFTC Regulation 1.20. Funds that customers deposit with RBCCM, or that are otherwise

required to be held for the benefit of customers, to margin futures and options on futures

contracts traded on foreign boards of trade, may be held in a foreign futures and foreign options

secured amount account in accordance with CFTC Regulation 30.7. Funds that customers

deposit with an FCM, or that are otherwise required to be held for the benefit of customers, to

margin, guarantee or secure a cleared swap, must be segregated and held in accordance with

CFTC Regulation 22.2.

CFTC Regulation 1.22 prohibits an FCM from using one customer's funds to meet the

obligations of another customer. Similarly, CFTC Regulation 22.2(d) prohibits an FCM from

using one cleared swaps customer’s collateral to meet the obligations of any other person.

Therefore, if a customer fails to have sufficient funds on deposit with an FCM to meet the

customer’s obligation, the FCM must use its own funds (excess funds) to make up any

deficiency in a customer's account.

CFTC Regulation 1.11(e)(3)(i)(D), CFTC Regulation 1.23(c) and NFA Financial Requirements

Section 16 requires RBCCM to maintain written policies and procedures regarding the

maintenance of its excess customer segregated, secured 30.7 funds and customer segregated

swaps to ensure RBCCM remains in compliance with segregation, secured 30.7 requirements

and cleared swap segregation.

In establishing targeted excess segregated, secured 30.7 and cleared swap amounts, RBCCM

performs due diligence inquiries relating to the nature of its business, along with the factors

outlined below:

the firm’s type of customers and their general creditworthiness;

trading activity;

type of markets and products traded by the firm’s customers and the firm itself;

general volatility and liquidity of those markets and products;

the firm’s own liquidity and capital needs;

historical trends in customer segregated/secured requirements and customer

debit/deficits; and

observed market conditions

Based upon these considerations, RBCCM has established a target dollar “range” for such

purposes as of April 2018:

The targeted range for customer segregated and secured §30.7 is as follows:

Customer Funds Required ≤ $500 million

o Target Minimum - $35 million excess

Customer Funds Required > $500 million ≤ $1 billion

8

o Target Minimum - $100 million excess

Customer Funds Required > $1 billion ≤ $1.5 billion

o Target Minimum - $160 million excess

Customer Funds Required > $1.5 billion ≤ $2.0 billion

o Target Minimum - $225 million excess

Customer Funds Required > $2.0 billion ≤ $2.5 billion

o Target Minimum - $300 million excess

Customer Funds Required > $2.5 billion ≤ $3.0 billion

o Target Minimum - $350 million excess

Customer Funds Required > $3.0 billion ≤ $3.5 billion

o Target Minimum - $425 million excess

Customer Funds Required > $3.5 billion ≤ $4.0 billion

o Target Minimum - $475 million excess

The targeted range for Cleared Swaps is as follows:

Customer Funds Required ≤ $500 million

o Target Minimum - $40 million excess

Customer Funds Required > $500 million ≤ $1 billion

o Target Minimum - $80 million excess

Customer Funds Required > $1 billion ≤ $1.5 billion

o Target Minimum - $120 million excess

Customer Funds Required > $1.5 billion ≤ $2.0 billion

o Target Minimum - $160 million excess

Customer Funds Required > $2.0 billion ≤ $2.5 billion

o Target Minimum - $200 million excess

These target percentage ranges are sufficient to meet customer obligations while concurrently

complying with segregated/secured §30.7/cleared segregated swap requirements. However, it is

important to note that falling below these targeted ranges will not necessarily result in a

violation of segregated/secured §30.7/cleared segregated swap amounts. If a withdrawal of

excess funds causes the Firm to fall below the targeted amount, RBCCM will comply with the

following:

By the close of business the following day, RBCCM must restore the excess funds to

the target amount;

Or if RBCCM chooses not to restore the targeted amount, a revised target amount must

be documented and approved by the Board of Directors.

Although RBCCM does not anticipate material changes to its written policies and targeted

range amounts, in the event such changes are necessary, appropriate internal approvals, record-

keeping and updates to Firm disclosures documentation will be performed accordingly.

9

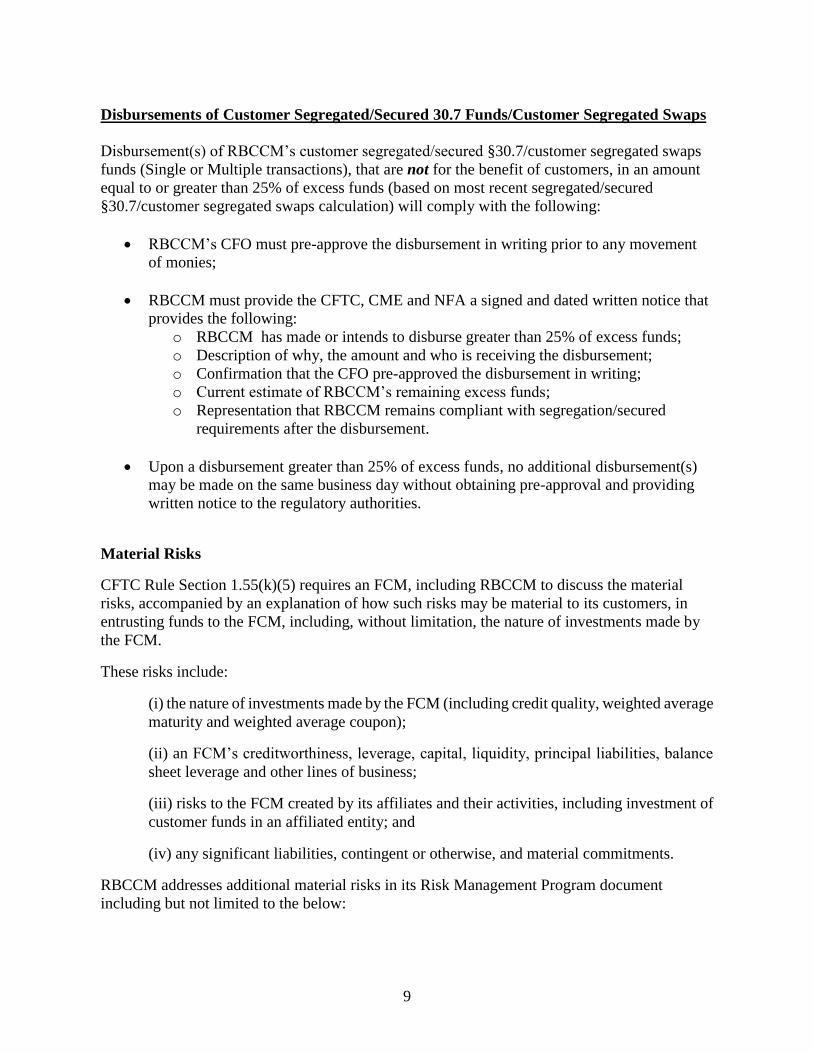

Disbursements of Customer Segregated/Secured 30.7 Funds/Customer Segregated Swaps

Disbursement(s) of RBCCM’s customer segregated/secured §30.7/customer segregated swaps

funds (Single or Multiple transactions), that are not for the benefit of customers, in an amount

equal to or greater than 25% of excess funds (based on most recent segregated/secured

§30.7/customer segregated swaps calculation) will comply with the following:

RBCCM’s CFO must pre-approve the disbursement in writing prior to any movement

of monies;

RBCCM must provide the CFTC, CME and NFA a signed and dated written notice that

provides the following:

o RBCCM has made or intends to disburse greater than 25% of excess funds;

o Description of why, the amount and who is receiving the disbursement;

o Confirmation that the CFO pre-approved the disbursement in writing;

o Current estimate of RBCCM’s remaining excess funds;

o Representation that RBCCM remains compliant with segregation/secured

requirements after the disbursement.

Upon a disbursement greater than 25% of excess funds, no additional disbursement(s)

may be made on the same business day without obtaining pre-approval and providing

written notice to the regulatory authorities.

Material Risks

CFTC Rule Section 1.55(k)(5) requires an FCM, including RBCCM to discuss the material

risks, accompanied by an explanation of how such risks may be material to its customers, in

entrusting funds to the FCM, including, without limitation, the nature of investments made by

the FCM.

These risks include:

(i) the nature of investments made by the FCM (including credit quality, weighted average

maturity and weighted average coupon);

(ii) an FCM’s creditworthiness, leverage, capital, liquidity, principal liabilities, balance

sheet leverage and other lines of business;

(iii) risks to the FCM created by its affiliates and their activities, including investment of

customer funds in an affiliated entity; and

(iv) any significant liabilities, contingent or otherwise, and material commitments.

RBCCM addresses additional material risks in its Risk Management Program document

including but not limited to the below:

10

Trading Credit Risk - the risk of potential financial loss arising from the failure of a

counterparty or client with whom the Firm has entered into derivatives transactions,

interbank (cash) placements, securities finance, cash securities or spot foreign

exchange/precious metals transactions.

Operational Risk - the risk of loss or harm resulting from people, inadequate or failed

internal processes and systems, or from external events.

Settlement Risk – the risk created when the Firm pays away value to a counterparty in

anticipation of the concurrent receipt of an equivalent value from the counterparty in

satisfaction of a mutually agreed contract. It begins when the delivery instructions

become irrevocable and continues until such time when the counterparty’s delivery

obligations have been satisfied.

Legal Risk - the FCM manages its legal risk as part of an enterprise-wide approach. As

an FCM registered with the CFTC, the Firm is subject to numerous legal and regulatory

risks, including maintaining its compliance with obligations under the Commodity

Exchange Act, CFTC rules, rules of the NFA, and rules of designated contract markets

and derivatives clearing organizations of which it may be a member.

Nature of Investments

RBCCM holds a variety of instruments to support the wholesale broker dealer and wealth

management businesses, the majority of which are US Treasury securities, followed by other

highly rated government and/or government sponsored entity (“GSE”) securities, and other

investment grade securities, such as corporate bonds and municipal securities. Additionally,

RBCCM also holds non-investment grade corporate bonds, mortgage backed securities,

convertible bonds and certain equities and equity options. Although the weighted average

maturity and coupon for such holdings will vary, the Firm maintains robust risk management

practices which address the inherent risks with longer maturity or duration securities, including

interest rate sensitivity risk. RBCCM also performs repurchase agreements and reverse

repurchase agreements transacted through RBCCM, most of which are on an overnight basis.

The business activities performed and inventories held within RBCCM may lead to the

exposure to a variety of risks. Our ability to manage these risks is a key competency within

RBCCM, and is supported by a strong risk culture and risk management approach. As

mentioned above, these risks include credit, operational, settlement and legal risk. Risks

created by affiliates are limited to RBCCM’s ultimate consolidated entity parent, RBC. Other

affiliates of RBC do not create material risks to RBCCM unless they have a material impact or

exposure to the parent.

Credit, Leverage Net Capital & Liquidity

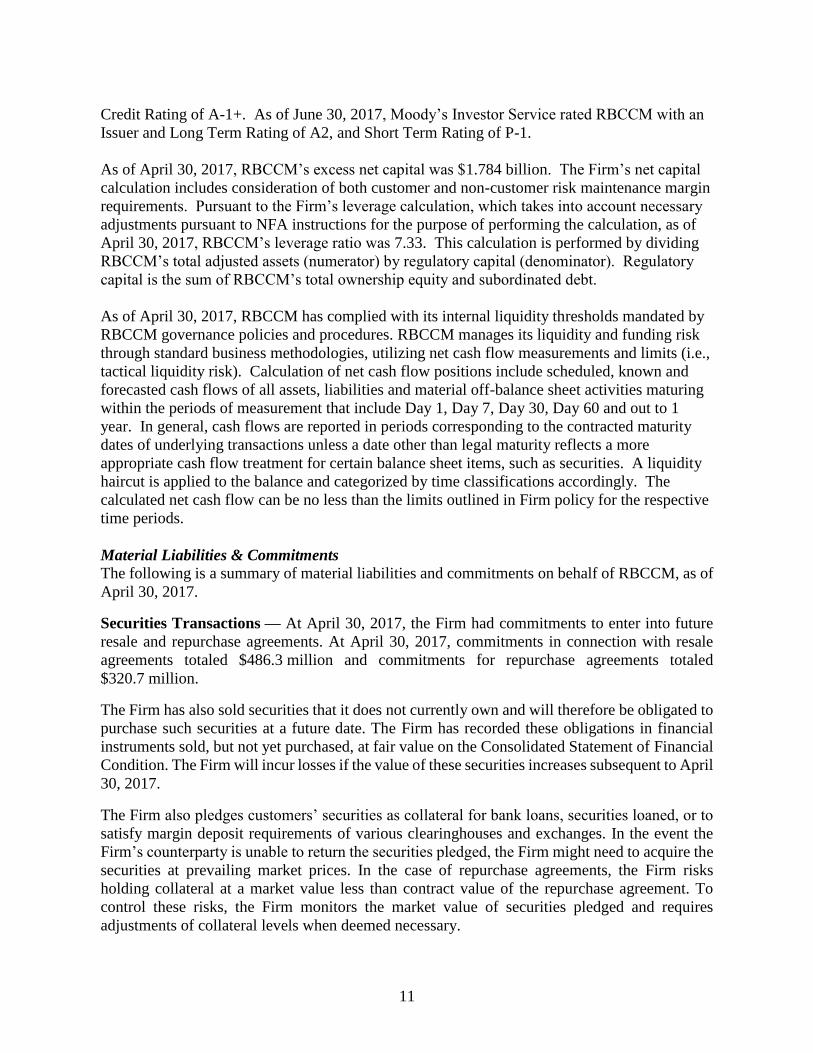

As of June 30, 2017, RBCCM was independently rated by Standard and Poor’s, with a Long

Term Foreign and Local Issuer Credit rating of AA- and Short Term Foreign and Local Issuer

11

Credit Rating of A-1+. As of June 30, 2017, Moody’s Investor Service rated RBCCM with an

Issuer and Long Term Rating of A2, and Short Term Rating of P-1.

As of April 30, 2017, RBCCM’s excess net capital was $1.784 billion. The Firm’s net capital

calculation includes consideration of both customer and non-customer risk maintenance margin

requirements. Pursuant to the Firm’s leverage calculation, which takes into account necessary

adjustments pursuant to NFA instructions for the purpose of performing the calculation, as of

April 30, 2017, RBCCM’s leverage ratio was 7.33. This calculation is performed by dividing

RBCCM’s total adjusted assets (numerator) by regulatory capital (denominator). Regulatory

capital is the sum of RBCCM’s total ownership equity and subordinated debt.

As of April 30, 2017, RBCCM has complied with its internal liquidity thresholds mandated by

RBCCM governance policies and procedures. RBCCM manages its liquidity and funding risk

through standard business methodologies, utilizing net cash flow measurements and limits (i.e.,

tactical liquidity risk). Calculation of net cash flow positions include scheduled, known and

forecasted cash flows of all assets, liabilities and material off-balance sheet activities maturing

within the periods of measurement that include Day 1, Day 7, Day 30, Day 60 and out to 1

year. In general, cash flows are reported in periods corresponding to the contracted maturity

dates of underlying transactions unless a date other than legal maturity reflects a more

appropriate cash flow treatment for certain balance sheet items, such as securities. A liquidity

haircut is applied to the balance and categorized by time classifications accordingly. The

calculated net cash flow can be no less than the limits outlined in Firm policy for the respective

time periods.

Material Liabilities & Commitments

The following is a summary of material liabilities and commitments on behalf of RBCCM, as of

April 30, 2017.

Securities Transactions — At April 30, 2017, the Firm had commitments to enter into future

resale and repurchase agreements. At April 30, 2017, commitments in connection with resale

agreements totaled $486.3 million and commitments for repurchase agreements totaled

$320.7 million.

The Firm has also sold securities that it does not currently own and will therefore be obligated to

purchase such securities at a future date. The Firm has recorded these obligations in financial

instruments sold, but not yet purchased, at fair value on the Consolidated Statement of Financial

Condition. The Firm will incur losses if the value of these securities increases subsequent to April

30, 2017.

The Firm also pledges customers’ securities as collateral for bank loans, securities loaned, or to

satisfy margin deposit requirements of various clearinghouses and exchanges. In the event the

Firm’s counterparty is unable to return the securities pledged, the Firm might need to acquire the

securities at prevailing market prices. In the case of repurchase agreements, the Firm risks

holding collateral at a market value less than contract value of the repurchase agreement. To

control these risks, the Firm monitors the market value of securities pledged and requires

adjustments of collateral levels when deemed necessary.

12

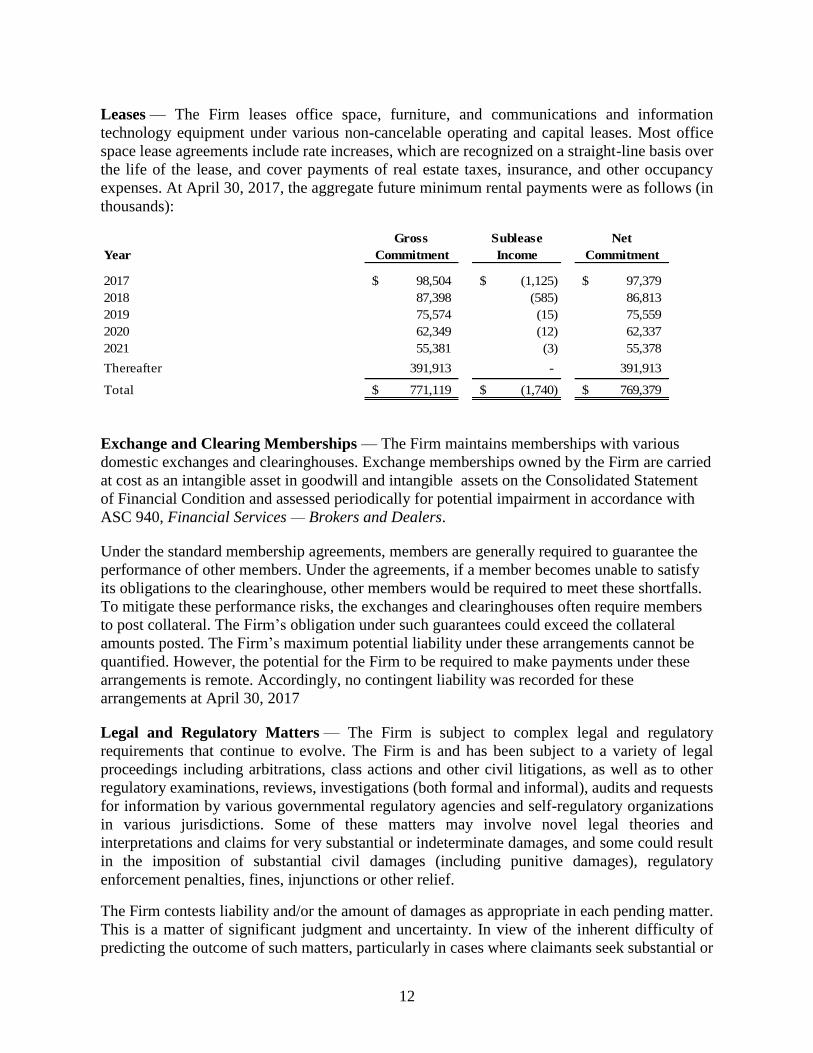

Leases — The Firm leases office space, furniture, and communications and information

technology equipment under various non-cancelable operating and capital leases. Most office

space lease agreements include rate increases, which are recognized on a straight-line basis over

the life of the lease, and cover payments of real estate taxes, insurance, and other occupancy

expenses. At April 30, 2017, the aggregate future minimum rental payments were as follows (in

thousands):

Exchange and Clearing Memberships — The Firm maintains memberships with various

domestic exchanges and clearinghouses. Exchange memberships owned by the Firm are carried

at cost as an intangible asset in goodwill and intangible assets on the Consolidated Statement

of Financial Condition and assessed periodically for potential impairment in accordance with

ASC 940, Financial Services — Brokers and Dealers.

Under the standard membership agreements, members are generally required to guarantee the

performance of other members. Under the agreements, if a member becomes unable to satisfy

its obligations to the clearinghouse, other members would be required to meet these shortfalls.

To mitigate these performance risks, the exchanges and clearinghouses often require members

to post collateral. The Firm’s obligation under such guarantees could exceed the collateral

amounts posted. The Firm’s maximum potential liability under these arrangements cannot be

quantified. However, the potential for the Firm to be required to make payments under these

arrangements is remote. Accordingly, no contingent liability was recorded for these

arrangements at April 30, 2017

Legal and Regulatory Matters — The Firm is subject to complex legal and regulatory

requirements that continue to evolve. The Firm is and has been subject to a variety of legal

proceedings including arbitrations, class actions and other civil litigations, as well as to other

regulatory examinations, reviews, investigations (both formal and informal), audits and requests

for information by various governmental regulatory agencies and self-regulatory organizations

in various jurisdictions. Some of these matters may involve novel legal theories and

interpretations and claims for very substantial or indeterminate damages, and some could result

in the imposition of substantial civil damages (including punitive damages), regulatory

enforcement penalties, fines, injunctions or other relief.

The Firm contests liability and/or the amount of damages as appropriate in each pending matter.

This is a matter of significant judgment and uncertainty. In view of the inherent difficulty of

predicting the outcome of such matters, particularly in cases where claimants seek substantial or

Gross Sublease Net

Year Commitment Income Commitment

2017 98,504$ (1,125)$ 97,379$

2018 87,398 (585) 86,813

2019 75,574 (15) 75,559

2020 62,349 (12) 62,337

2021 55,381 (3) 55,378

Thereafter 391,913 - 391,913

Total 771,119$ (1,740)$ 769,379$

13

indeterminate damages or where investigations and proceedings are in the early stages, the Firm

cannot predict the loss or range of loss, if any, related to such matters; how or if such matters will

be resolved; when they will ultimately be resolved; or what the eventual settlement, fine, penalty

or other relief, if any, might be. Subject to the foregoing, the Firm believes, based on current

knowledge and after consultation with counsel, that the outcome of such pending matters will

not have a material adverse effect on the Consolidated Statement of Financial Condition,

although the outcome of such matters could be material to the Firm’s operating results and cash

flows for a particular future period, depending on, among other things, the level of the Firm’s

revenues, income or cash flows for such period.

Material Complaints or Actions

CFTC Rule Section 1.55(k)(7) requires RBCCM to disclose any material administrative, civil,

enforcement or criminal complaints or actions filed against the FCM where such complaints or

actions have not concluded, and any enforcement complaints or actions filed against the FCM

during the last three years.

Based upon a review of relevant open and/or closed actions, RBCCM in its capacity as the

registered FCM has no current reportable material complaints or actions.

Customer Funds Segregation

CFTC Rule Section 1.55(k)(8) requires a basic overview of customer fund segregation, FCM

management and investments, FCMs and joint FCM/broker dealers. RBCCM maintains three

different types of accounts for customers, depending on the products a customer trades:

(i) a Customer Segregated Account for customers that trade futures and options on

futures listed on US futures exchanges;

(ii) a Secured 30.7 Account for customers that trade futures and options on futures

listed on foreign boards of trade; and

(iii) a Cleared Swaps Customer Account for customers trading swaps that are cleared

on a derivatives clearing organization (DCO) registered with the Commission.

The requirement to maintain these separate accounts reflects the different risks posed by the

different products. Cash, securities and other collateral (collectively, “Customer Funds”)

required to be held in one type of account, e.g., the Customer Segregated Account, may not be

commingled with funds required to be held in another type of account, such as the Secured 30.7

Account, except as the Commission may permit by order.

Customer Segregated Account. Funds that customers deposit with RBCCM, or that are

otherwise required to be held for the benefit of customers, to margin futures and options on

futures contracts traded on futures exchanges located in the US, (i.e., designated contract

markets) are held in a Customer Segregated Account in accordance with section 4d(a)(2) of the

Commodity Exchange Act (Act) and Commission Rule 1.20. Customer Segregated Funds held

in the Customer Segregated Account may not be used to meet the obligations of RBCCM or

any other person, including another customer.

14

All Customer Segregated Funds may be commingled in a single account, (i.e., a customer

omnibus account) and held with: (i) a bank or trust company located in the US; (ii) a bank or

trust company located outside of the US that has in excess of $1 billion of regulatory capital;

(iii) an FCM; or (iv) a DCO. Such commingled account is properly titled to make clear that the

funds belong to, and are being held for the benefit of, RBCCM’s customers.

RBCCM will hold sufficient US dollars in the US to meet all US dollar obligations. Unless a

customer provides instructions to the contrary, RBCCM may hold Customer Segregated Funds

only: (i) in the US; (ii) in a money center country; or (iii) in the country of origin of the

currency.

Secured 30.7 Account. Funds that customers deposit with RBCCM, or that are otherwise

required to be held for the benefit of customers, to margin futures and options on futures

contracts traded on foreign boards of trade, (i.e., Secured 30.7 Customer Funds), and

sometimes referred to as the foreign futures and foreign options secured amount, are held in a

Secured 30.7 Account in accordance with Commission Rule 30.7.

Funds required to be held in the Secured 30.7 Account for or on behalf of customers may be

commingled in a Secured 30.7 customer omnibus account and held with: (i) a bank or trust

company located in the US; (ii) a bank or trust company located outside the US that has in

excess of $1 billion in regulatory capital; (iii) an FCM; (iv) a DCO; (v) the clearing

organization of any foreign board of trade; (vi) a foreign broker; or (vii) such clearing

organization’s or foreign broker’s designated depositories. Such commingled account must be

properly titled to make clear that the funds belong to, and are being held for the benefit of, the

RBCCM’s customers.

Customers trading on foreign markets assume additional risks. Laws or regulations will vary

depending on the foreign jurisdiction in which the transaction occurs, and funds held in a

Secured 30.7 Account outside of the US may not receive the same level of protection as

customer segregated funds. If the foreign broker carrying Secured 30.7 customer positions

fails, the broker will be liquidated in accordance with the laws of the jurisdiction in which it is

organized, which laws may differ significantly from the US Bankruptcy Code. Return of

Secured 30.7 customer funds to the US will be delayed and likely will be subject to the costs of

administration of the failed foreign broker in accordance with the law of the applicable

jurisdiction, as well as possible other intervening foreign brokers, if multiple foreign brokers

were used to process the US customers’ transactions on foreign markets.

If the foreign broker does not fail but the Secured 30.7 Customers’ US FCM fails, the foreign

broker may want to assure that appropriate authorization has been obtained before returning the

funds to the FCM’s trustee, which may delay their return. If both the foreign broker and the US

FCM were to fail, disputes between the trustee for the US FCM and the administrator for the

foreign broker may result in significant delays and additional administrative expenses. Use of

other intervening foreign brokers by the US FCM to process the trades of Secured 30.7

customers on foreign markets may cause additional delays and administrative expenses.

To reduce the potential risk to Secured 30.7 customer funds held outside of the US,

Commission Rule 30.7 generally provides that an FCM may not deposit or hold Secured 30.7

customer funds in permitted accounts outside of the US except as necessary to meet margin

15

requirements, including prefunding margin requirements, established by rule, regulation, or

order of the relevant foreign boards of trade or foreign clearing organizations, or to meet

margin calls issued by foreign brokers carrying the Secured 30.7 customers’ positions. The

rule further provides, however, that, in order to avoid the daily transfer of funds from accounts

in the US, an FCM may maintain in accounts located outside of the US an additional amount of

up to 20 percent of the total amount of funds necessary to meet margin and prefunding margin

requirements to avoid daily transfers of funds.

Cleared Swaps Customer Account. Funds deposited with RBCCM, or otherwise required to

be held for the benefit of customers, to margin swaps cleared through a registered DCO, (i.e.,

Cleared Swaps Customer Collateral), are held in a Cleared Swaps Customer Account in

accordance with the provisions of section 4d(f) of the Act and Part 22 of the Commission’s

rules. Funds required to be held in a Cleared Swaps Customer Account may be commingled in

an omnibus account and held with: (i) at a bank or trust company located in the US; (ii) a bank

or trust company located outside of the US that has in excess of $1 billion of regulatory capital;

(iii) a DCO; or (iv) another FCM. Such commingled account is properly titled to make clear

that the funds belong to, and are being held for the benefit of, RBCCM’s Cleared Swaps

Customers.

No SIPC Protection. Although RBCCM is a registered broker-dealer, it is important to

understand that the funds you deposit with RBCCM for trading futures and options on futures

contracts on either US or foreign markets or cleared swaps are not protected by the Securities

Investor Protection Corporation.

Further, Commission rules require RBCCM to hold funds deposited to margin futures and

options on futures contracts traded on US designated contract markets in Customer Segregated

Accounts. Similarly, RBCCM must hold funds deposited to margin cleared swaps and futures

and options on futures contracts traded on foreign boards of trade in a Cleared Swaps Customer

Account or a Secured 30.7 Account, respectively. In computing its Customer Funds

requirements under relevant Commission rules, RBCCM may only consider those Customer

Funds actually held in the applicable Customer Accounts and may not apply free funds in an

account under identical ownership but of a different classification or account type (e.g.,

securities, Customer Segregated, Secured 30.7) to an account’s margin deficiency. In order to

be used for margin purposes, the funds must actually transfer to the identically-owned

undermargined account.

For additional information on the protection of customer funds, please see the Futures Industry

Association’s “Protection of Customer Funds Frequently Asked Questions” located at

www.futuresindustry.org/downloads/PCF_questions.pdf

Filing a Complaint

CFTC Rule Section 1.55(k)(9) requires RBCCM to describe how a customer may obtain

information regarding filing a complaint about RBCCM with the Commission or with

RBCCM’s DSRO.

A customer that wishes to file a complaint about RBCCM or one of its employees with the

Commission can contact the Division of Enforcement either electronically at

16

https://forms.cftc.gov/fp/complaintform.aspx or by calling the Division of Enforcement toll-

free at 866-FON-CFTC (866)-366-2382.

A customer that may file a complaint about the RBCCM or one of its employees with the

National Futures Association electronically at http://www.nfa.futures.org/basicnet/

Complaint.aspx or by calling the NFA directly at (800)-621-3570.

A customer that wishes to file a complaint about RBCCM or one of its employees with the

CME Group, RBCCM’s DSRO, can do so electronically at www.cmegroup.com/market-

regulation/dispute-resolution or by calling the CME Group’s Division of Market Regulation at

(312)-930-1000.

Relevant Financial Data

CFTC Rule Section 1.55(k)(10) requires RBCCM to include the following financial information

as of the most recent month-end that such information is available with respect to this Disclosure

Document. This financial information includes the following as of April 30, 2017, unless stated

otherwise:

(i) RBCCM’s total equity, regulatory capital, and net worth, all computed in accordance

with U.S. Generally Accepted Accounting Principles and Rule 1.17, as applicable;

(ii) the dollar value of RBCCM’s proprietary margin requirements as a percentage of

the aggregate margin requirement for futures customers, cleared swaps customers, and

30.7 customers;

(iii) the number of futures customers, cleared swaps customers, and 30.7 customers that

comprise 50 percent of RBCCM’s total funds held for futures customers, cleared swaps

customers, and 30.7 customers, respectively;

(iv) the aggregate notional value, by asset class, of all non-hedged, principal over-the

counter transactions into which RBCCM has entered;

(v) the amount, generic source and purpose of any unsecured lines of credit (or similar

short-term funding) the RBCCM has obtained but not yet drawn upon.

(vi) the aggregate amount of financing the FCM provides for customer transactions

involving illiquid financial products for which it is difficult to obtain timely and

accurate prices;

(vii) the percentage of futures customers, cleared swaps customers, and 30.7 customer

receivable balances that RBCCM was required to write-off as uncollectable during the

past 12-month period, as compared to the current balance of funds held for futures

customers, cleared swaps customers, and 30.7 customers.

Financial Data

17

RBCCM’s Ownership Equity is $5,169,521,814, Regulatory Capital (Ownership Equity

plus Subordinated Debt) is $6,569,521,814 and Net Worth (Net Capital) is

$2,034,366,274, all which were computed in accordance with U.S. Generally Accepted

Accounting Principles and Rule 1.17, as applicable;

RBCCM’s proprietary margin requirement was less than 1% of the aggregate margin

requirement for all customers;

Ten (10) Futures customers comprised 50 percent of RBCCM’s funds held in

Segregation accounts, two (2) Cleared Swaps customers comprised 50 percent of

RBCCM’s funds held in cleared swaps accounts, and eight (8) Foreign Futures/Options

customers comprised 50 percent of RBCCM’s funds held in 30.7 Secured accounts;

RBCCM was not required to write-off any customer balances as uncollectable during

the past 12-month period;

RBCCM does not currently provide financing to customers within its FCM, and

therefore would not be subject to risk regarding customer financing involving illiquid

financial products.

Lines of Credit & Funding

18

The Firm entered into various borrowing arrangements to meet short-term financing needs.

At April 30, 2017, short-term borrowings consist of the following arrangements (in

thousands):

Total

Facility Borrowings

Secured revolving loan agreement entered into with an affiliate that allows the Company to borrow

cash under a series of arrangements with maturity 90 days or less. Facility expires December 2018.

10,000,000$ 3,628,521$

Unsecured revolving credit agreement entered into with RBC to manage short-term liquidity needs.

Agreement matures August 2017.

3,000,000 1,000,000

Uncommitted overnight credit facility entered into with RBC to manage short-term liquidity needs.

Facility matures July 2017. Facility was not used.

850,000 -

Unsecured uncommitted facilities entered into with an affiliate to manage short-term liquidity needs.

The facility provides for funding in various currencies up to the equivalent of €505 million ($550

million as at April 30, 2017).

550,000 17,288

Uncommitted overdraft credit facility entered into with an affiliate to facilitate the settlement of

foreign exchange transactions. Facility has an open maturity date.

35,000 16,593

Floaters issued by consolidated VIEs in the TOB program. Floaters, which are issued to third-party

investors, are secured.

- 1,951,330

Overdraft balances in various non-affiliated bank accounts. - 511

Total 14,435,000$ 6,614,243$

The Company also maintains certain uncommitted overnight credit facilities with various non-affiliated banks to

clear securities transactions. As at April 30, 2017, there were no outstanding borrowings from these facilities.

Customers should be aware that the NFA publishes on its website certain financial information

with respect to each FCM. The FCM Capital Report provides each FCM’s most recent month-

end adjusted net capital, required net capital, and excess net capital. (Information for a twelve-

month period is available.) In addition, the NFA publishes twice-monthly a Customer

Segregated Funds report, which shows for each FCM: (i) total funds held in Customer

Segregated Accounts; (ii) total funds required to be held in Customer Segregated Accounts; and

(iii) excess segregated funds, (i.e., the FCM’s Residual Interest). This report also shows the

percentage of Customer Segregated Funds that are held in cash and each of the permitted

investments under Commission Rule 1.25. Finally, the report indicates whether an FCM held

any Customer Segregated Funds during that month at a depository that is an affiliate.

The report shows the most recent semi-monthly information, but the public will also have the

ability to see information for the most recent twelve-month period. A 30.7 Customer Funds

report and a Customer Cleared Swaps Collateral report provides the same information with

respect to the 30.7 Account and the Cleared Swaps Customer Account.

The above financial information reports can be found by conducting a search for a specific FCM

in NFA’s BASIC system (http://www.nfa.futures.org/basicnet/) and then clicking on “View

Financial Information” on the FCM’s BASIC Details page.

19

Current Risk Practices, Controls and Procedures

CFTC Rule Section 1.55(k)(11) requires a summary of RBCCM’s current risk practices,

controls and procedures. RBCCM is both a registered FCM with the NFA and the CFTC, and

is a registered broker dealer with the SEC and FINRA in the United States. Pursuant to these

registrations, RBCCM is subject to ongoing rigorous regulatory obligations, including, but not

limited to, maintaining satisfactory risk controls, policies and procedures. Further, RBCCM is

subject to periodic review by these aforementioned regulatory bodies, and performs its own

internal controls testing reviews. This is further supported by independent reviews performed

by the Firm’s Internal Audit function and external third-party auditors more broadly.

Governance Functions and Risk Controls

RBCCM maintains a robust risk and controls governance framework supported by policies and

procedures pertaining to the oversight of the Firm both within the U.S. and globally. Relevant

RBCCM control areas include, but are not limited to, Market Risk, Credit Risk, Liquidity Risk,

Operational Risk, Compliance and Audit. Each functional risk and/or control area maintains

policies, procedures and governance tools (e.g., surveillance reports, risk limit thresholds and

metrics, front-office systemic controls) for purposes of maintaining the Firm’s overall

governance and risk management structure.

These risk and control functions also maintain dedicated staffing specifically for the sales and

trading activity within the FCM platform. Among other duties, the FCM Risk function measures

overnight and intraday risks of all client positions using methods consistent with the Firm’s Risk

Management policies and procedures. These measures are also compared to Exchange margin

requirements for validating appropriate margin. Additional monitoring includes a review of

profit/loss, concentration risks and liquidity risks. These and other reviews of client positions

enhance the existing controls that already exist with RBCCM.

Polices & Procedures

RBCCM maintains a wide array of policies and procedures utilized by both front-office and

functional support areas of the FCM. Many of these policies and procedures are required as

part of the obligations associated with being a registered FCM. The aforementioned Risk

Management Program, pursuant to CFTC Rule 1.11, sets forth the established policies and

procedures (the “Risk Program”) designed to monitor and manage the comprehensive set of

risks associated with the activities of the FCM. The Firm also maintains and follows Firm

specific policies and procedures which are adhered to at a global organization level.

This Disclosure Document was first used on April 4, 2018.