commodities research · 2018-09-11 · energy market outlook: between scarcity and abundance march...

TRANSCRIPT

Energy Market Outlook: Between scarcity and abundance

March 2018

Commodities Research

PLEASE SEE ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES STARTING AFTER PAGE 37

Michael Cohen

+1 212 526-3606

BCI, US

Oil market short-term overview

3 December 2017

As inventories draw, geopolitical supply concerns emerge

1. Prices have experienced justified strength as stocks draw, but high prices will create a hangover effect

2. We remain bearish on prices at current levels due to expected shale growth, global supply builds in ‘18, and the

removal of temporary supply supports

3. OPEC strategy must balance short and long term revenue maximization: to that end it wants relatively high and

stable prices not price fluctuations in a lower range

Inventory drawdown continued through end of year. Market looking for clarity on situations in

Venezuela and Iran, and OPEC policy

0

20

40

60

80

100

120

140

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

98 00 02 04 06 08 10 12 14 16 18

bill. barrels

OECD industry petroleum stock levels vs 5-yr avg (Jan

1998-Dec 2018)

surplus to 5-yr Price Source s: IEA, Bloomberg, Barclays Research

4

Source for all charts: IEA, Bloomberg, Barclays Research

Solid outlook for global growth Global growth being driven by developed

economies and EM is catching up …

26 March 2018

Synchronicity: global economic recovery across all regions…

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16 Aug-17

Global industrial production, LHS

Global manufact. Conf. (Barclays), RHS

3m/3m change, saarnormalised

diffusion balance

-4

-2

0

2

07 08 09 10 11 12 13 14 15 16 17

normalised diffusion index

Manufacturing confidence

Advanced economies Emerging economies

… and some commodity intensive economies

still recovering

5 December 2017

…which is driving robust demand growth

Timeframes of synchronous global economic growth consistent with acceleration in demand

growth and rising oil prices (Jan 1998-Dec 2017)

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

0

20

40

60

80

100

120

140

160

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

Nom. oil price ($/b), LHS Oil Demand Growth (%, RHS)

syncrhonous global growth

Source: Haver Analytics, IEA, EIA (Imported nominal average acq. cost), Barclays Research

6

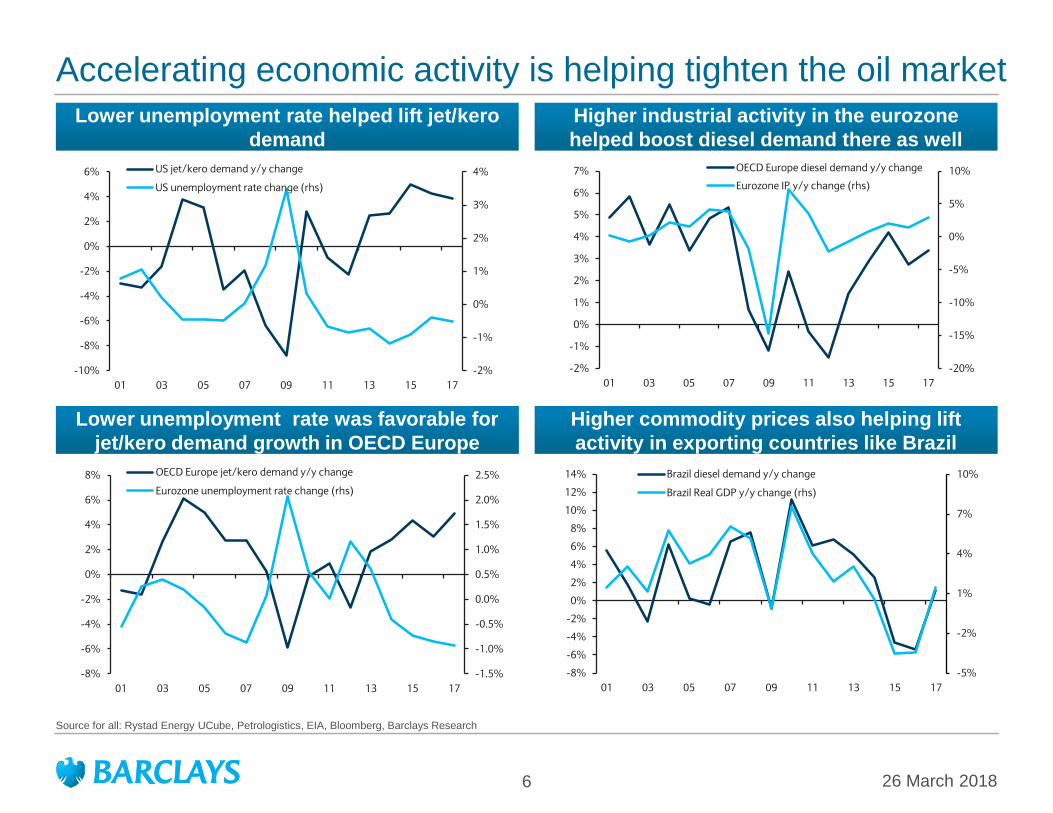

Accelerating economic activity is helping tighten the oil market

Source for all: Rystad Energy UCube, Petrologistics, EIA, Bloomberg, Barclays Research

Higher industrial activity in the eurozone

helped boost diesel demand there as well

Lower unemployment rate helped lift jet/kero

demand

Lower unemployment rate was favorable for

jet/kero demand growth in OECD Europe

Higher commodity prices also helping lift

activity in exporting countries like Brazil

26 March 2018

-2%

-1%

0%

1%

2%

3%

4%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

01 03 05 07 09 11 13 15 17

US jet/kero demand y/y change

US unemployment rate change (rhs)

-20%

-15%

-10%

-5%

0%

5%

10%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

01 03 05 07 09 11 13 15 17

OECD Europe diesel demand y/y change

Eurozone IP y/y change (rhs)

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01 03 05 07 09 11 13 15 17

OECD Europe jet/kero demand y/y change

Eurozone unemployment rate change (rhs)

-5%

-2%

1%

4%

7%

10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

01 03 05 07 09 11 13 15 17

Brazil diesel demand y/y change

Brazil Real GDP y/y change (rhs)

7 26 March 2018

But despite all this, surplus emerges later this year and next

Source: Bloomberg, Barclays Research

We assume robust demand growth and continued declines in Venezuela’s production, but strong

US supply growth this year and next will push the market into surplus

0

20

40

60

80

100

120

140

-1

0

1

2

3

4

1Q12 4Q12 3Q13 2Q14 1Q15 4Q15 3Q16 2Q17 1Q18 4Q18

$/bmb/d per

yearGlobal Supply and Demand Growth

Global Supply Growth (LHS)

Global Demand Growth (LHS)

Brent prices

62

5657 55

20

40

60

80

100

120

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

3Q13 2Q14 1Q15 4Q15 3Q16 2Q17 1Q18 4Q18 3Q19

Oil market balance and prices

Stock change + misc (LHS) Brent Price (RHS)

Oil outlook to 2019: Between scarcity and abundance

9

Source for all charts: IEA, EIA, Barclays Research

Non-OPEC supply growth centered entirely on

North America in 2018 and 2019

The Permian will drive production growth over

the coming years (mb/d)

26 March 2018

We forecast 1.9 & 1.2 mb/d of non-OPEC growth in 2018-19

0.4 0.10.1

1.2

0.0

0.5

1.6

2.4

1.5

-0.7

0.8

1.9

1.2

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2007 2009 2011 2013 2015 2017 2019

Non-OPEC Supply Growth

North America (NAM)

Non-OPEC ex-NAM

*Not including OPEC non-crude liquids

779624

127

95

50

75

75

92

204

78

307

248

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2018 2019

PermianWilliston Basin -NDEagle FordUS Gulf of MexicoOther CrudeNGLsAlaska

10

Source: Barclays Equity Research Global 2018 E&P Spending Outlook

US output to grow to 11.8 mb/d on rising upstream spend

Most of NAM upstream expects to spend 30%

more in 2018 y/y

0%

10%

20%

30%

40%

50%

60%

70%

80%

US IOCs* US Large-Cap E&Ps US Smid-Cap E&Ps NAM Small-

Cap/Privates

2017 Growth

2018 Growth

0% 1%

9%

72%

15%

3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Down over

20%

Down 10-20% Down 0-10% Up 0-10% Up 10-20% Up over 20%

0%

10%

20%

30%

40%

50%

60%

0-25% structural 25-50% structural 50-75% structural

Dec 2016 survey

Dec 2017 survey

In 2017, more NAM producers viewed cost

reductions as structural than in 2016…

…Yet 90% of producers expect some degree

of cost inflation this year Ultimately, activity will be driven by oil prices

-100%

-80%

-60%

-40%

-20%

0%

20%

1/24/2014 1/24/2015 1/24/2016 1/24/2017 1/24/2018

Prices

Rigs (4 month ahead)

Frac Spreads (3 month ahead)

Source: Primary Vision Market Intelligence and Consulting, Baker Hughes, Bloomberg, Barclays Research

Note: *Includes Chevron, Exxon Mobil, Hess, ConocoPhillips Source: Barclays Equity Research

Source: Barclays Equity Research Global 2018 E&P Spending Outlook

26 March 2018

11

Source: Company Reports, EIA, DrillingInfo, Barclays Research

26 March 2018

Leading to capacity constraints in strong growth areas

Canadian takeaway capacity looks

constrained until 2019

Tight takeaway capacity in the Permian should

cause Midland-USGC weakness in late 2018

Note: Assumes dilbit volumes (70/30) Source: Company reports, AER, Barclays Research

Enbridge

Express

Keystone

Rangeland

Line 3?

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Q1 2012 Q1 2014 Q1 2016 Q1 2018

Canadian Production vs Takeaway

AB and SK Heavy Oil

Trans Mountain

Refining

Pre-2017

Pipelines

0

1

2

3

4

5

6

Jan-16 Jan-17 Jan-18 Jan-19

mb/d Recent Announcements*

Midland-Sealy & PE 3

Permian Production

12

Saudi public expenditures have already been

sharply cut post-2014

December 2017

Pillars of OPEC strategy #1: Tradeoff between long/short term revenue maximization

Source: Haver Analytics, SAMA, Barclays Research

Focus on the flexible four: UAE, Kuwait, Saudi

Russia. Most others producing at status quo Saudi fiscal breakeven at around $74/b

Most MENA countries have fiscal BEs around

current price levels

-800

-400

0

400

800

1,200

Feb-16 Aug-16 Feb-17 Aug-17 Feb-18 Aug-18

OPEC/NOPEC Production Levels

(Jan 2016=0)

Flexible four: Russia, Saudi, UAE, Kuwait

Other participants

swing of 1.4 mb/d

0

20

40

60

80

100

120

1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Oil price fiscal breakeven, $bbl

Arab light

Fiscal

breakeven

Including

contractor

arrears

0

20

40

60

80

100

120

0

50

100

150

200

250

300

350

400

1969 1975 1981 1987 1993 1999 2005 2011 2017

Capital expenditure

Arab light

SAR Billion $bbl

Source: IMF, 2017, Barclays Research.

$63

$98

$59 $57 $50

$91$79

$55

$74$59

0

50

100

150

200

250

Algeria Bahrain Iran Iraq Kuwait Libya Oman Qatar Saudi

Arabia

UAE

2014 2015 2016 2017 2018

13 December 2017

Pillar #2: Fragile producers deliver high overall compliance

Source: EIA (map), IEA (production), Petrologistics (exports), Barclays Research

Trump’s Iran policy – death by a thousand cuts to the JCPOA. Working class protests pose a

more serious problem to the regime and some protests centered near energy infrastructure

6%

5% 5%

3%

3% 3%3%

4% 4%4%

5% 5%

2%

1% 1% 1%

3%4%

0%

1%

2%

3%

4%

5%

6%

7%

2009 2010 2011 2012 2013 2014 2015 2016 2017

Iran Market Share in Asia and Europe (2009-16)

Asia Europe

Top annual

exports2017 Ave Wiggle Room

China 602 584 18

France 127 127 -

Greece 86 86 -

India 467 446 22

Italy 196 196 -

Japan 348 119 229

Malaysia 17 1 15

Netherlands 117 31 86

Pakistan 35 0 35

South Africa 119 0 119

South Korea 237 104 133

Spain 110 93 17

Sri Lanka 39 0 39

Taiwan 65 39 25

Syria, Turkey, Phillippines 312 270 42

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

09 10 11 12 13 14 15 16 17 18

Iranian Crude Output and Exports

Energy security metric Unit Nov-02 Jun-17 Better/Worse*

Spare Capacity mb/d 3.68 2.01 Worse

Spare Capacity/Demand ratio 5% 2% Worse

OECD Inventory cover days 32.7 30.3 Worse

US crude throughput cover days 17.5 25.1 slightly better**

US crude and cond. output kb/d 7,975 13,294 Better

US Import share ratio 13% 8% Better

US oil imports from Venezuela kb/d 1,447 796 Better

Venezuela Production kb/d 2,745 2,000 Better

Venezuela output as share of global heavy output ratio 18% 14% Better

*in terms of being better/worse off in the case of a disruption. **though inventory levels are higher, some of

the increase is due to higher inventory needs for more pipeline and infrastructure capacity.

14 December 2017

Sanctions accelerating Venezuela’s production decline

Source: for all: Rystad Energy UCube, Petrologistics, EIA, Barclays Research,

Revenues remain depressed as production

declines have offset higher prices

Production is expected to decline 50-100 kb/d

m-o-m in 2018.

Markets likely better prepared for a Venezuela

disruption than it was in 2002

PDVSA controls the lion’s share of production

(kb/d)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2005 2007 2009 2011 2013 2015 2017

mb/d<20 20-30 >30 NGLs

0

5

10

15

20

25

30

35

0

500

1,000

1,500

2,000

2,500

3,000

3,500 Production (lhs, kb/d)

Consumption (lhs, kb/d)

Revenues (rhs, $bn)

Company 2010 2011 2012 2013 2014 2015 2016

Shell 10 20 20 20 20 20 20

Chevron 80 80 90 90 90 90 80

Repsol 20 30 30 30 20 30 30

CNPC 10 20 20 20 20 30 30

PetroChina 20 20 20 30 30 30 30

Total 40 40 40 40 40 40 30

Rosneft 40 40 50 60 60 60 70

Gazprom 100 90 90 80 90 60 50

Others 70 80 80 110 110 130 130

PDVSA 2,220 2,260 2,210 2,150 2,050 2,060 1,880

15

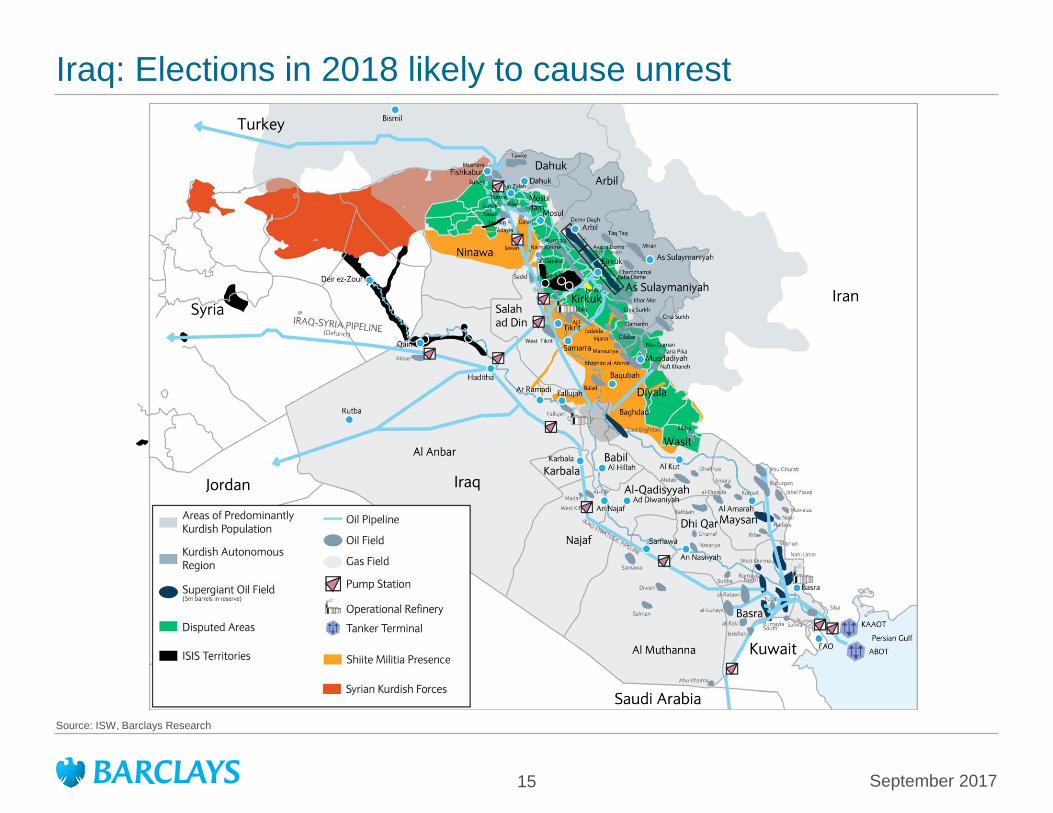

Source: ISW, Barclays Research

September 2017

Iraq: Elections in 2018 likely to cause unrest

16

Note: Military dispositions represent location of forces, not their relative strength which is variable. Source: Petroleum Economist, Barclays Research

Libya’s western exports are captive to the free flow of oil to Zawiyah, while the Sirte basin fields

have more alternatives

September 2017

Libya: Output likely to improve/decline in fits and starts

AG – Arabian Gulf Oil Co

Ak – Akakus Oil Co

AO – Agip Oil Co

HO – Harouge Oil

MO – Mabruk Oil

SO – Sirte Oil Co

WO – Waha Oil Co

Wi – Wintershall

ZO – Zueitina Oil

A – Amazigh

BDB – Benghazi Defence Brigades

LNA – Libya National Army

M – Misrata

SC – Shura council

SCM – Shura Council of Mujahideen (Allied to AQ)

T – Tebu Militia

Trp – Tripoli Militias

Za – Zawiyah

Zi – Zintan

Libya Dawn

Operation Dignity

Islamist

Petroleum

Facilities Guard

Libyan

National Guard

T

LNA

BDB PFG

LNA

PFG LNA

M

LNA

Zi

Zi

Zi

Za

A

Za Za

Trp LNG

PFG LNA

M

LNALNA LNA

LNA

SCM

LNA

LNA

LNA PFG

SC LNA ISIS

M

AO

Ak

ZO

HO

MO

ZOWO

WO

SO

SO

WO

HO

SOZO

WO

WOAG

Wi

MO

Ind

Zawara

Mellitah

Riyayna

Zintan

Zawiyah

Tripoli (Tarabulas)

Nalut

Ghadames

Ghat

Awbari

Murzuq

Sabha

Al Khums

Misrata

Sirte

Sidra

(Es-Sider)

Brak

Ras Lanuf

Marada

Ujala

Marsa el Brega

Ajdadiya

Zueitina

Benghazi

Al BaydaDerna

Tobruk

(Hariga)

What Jalu

Sarir RefineryGMMR Power

Station

Sharara

El Feel

(Elephant)

En Naga

Sabah

Zella

GhaniJofra

Al MabrukBahi

Dahra

Tibisti

Raguba

Nasser

SamahDefa

Waha S

Amal

Intisar

Gialo

Mesla

Sarir

Al Jurf

WafaWaddan

Libya

Tunisia

Murzuq Basin

Sirte Basin

Sarir/Mesla

Oilfield

Oil Pipeline

Oil Refinery

Oil Storage

Tanker Terminal

Active Front Line

Zawiyah

Max refining/export

capacity 200,000 b/d

NOC

Mellitah

Export capacity 30,000 b/d

NOC/ENI

Es-Sider

Export capacity 447,000 b/d

NOC

Ras Lanuf

Max refining/export

capacity 220,000 b/d

NOC

Zueitina

Export capacity 200,000 b/d

NOC/Occidental/OMV

Brega

Max refining/export

capacity 51,000 b/d

NOC

Hariga

Export capacity 120,000 b/d

AGOCO-NOC

17

Source for all charts: Bloomberg, CDU-TEK, IEA, CNH, ANP, WoodMackenzie, Barclays Research

December 2017

Pillar #3: Include as many non-OPEC countries as possible

Russia has substantial incremental output potential but subject to brownfield declines

Mexico’s production declining anyway

Field Operator 2017 2018 201918

Growth

19

Growth

Urengoy (Rospan), Cond. Rospan International 29 74 96 45 21

Novoportovskoye Gazpromneft-Yamal 90 120 128 30 8

Vladimir Filanovski LUKOIL Nizhnevolzhskneft 90 114 126 24 12

Odoptu-More (Sakhalin) ExxonMobil 43 66 71 22 5

East Urengoy Rospan International 4 26 38 22 12

Yurubcheno-Tokhomskoye Vostsibneftegaz 12 32 90 20 58

East Messoyakhskoye Messoyakhaneftegaz 40 60 85 20 25

Srednebotuobinskoye Cntl Taas-Yuryakh 27 47 78 20 31

Prirazlomnoye (TP) Gazprom neft shelf 50 65 75 15 10

Orenburg (East) Gazpromneft-Orenburg 37 52 67 15 15

Total* 423 657 853 233 196

-400

-300

-200

-100

0

100

200

300

400

500

9.8

10.0

10.2

10.4

10.6

10.8

11.0

11.2

11.4

Jan-14 Sep-14 May-15 Jan-16 Sep-16 May-17

Th

ou

san

ds

Russian Output

y/y growth (RHS, kb/d) Output C&C (mb/d), LHS

1800

2100

2400

2700

3000

3300

3600

0

20

40

60

80

100

120

140

160

05 06 07 08 09 10 11 12 13 14 15 16 17

New Dev. Drilling/m (LHS) Production

Canada and Brazil to pose challenges in 2018

1600

2000

2400

2800

3200

-400

-200

0

200

400

600

Jan-13 Oct-13 Jul-14 Apr-15 Jan-16 Oct-16 Jul-17 Apr-18

Brazil Production by Basin

Santos Campos Other Total (RHS)

18

Source : Bloomberg, EIA, Barclays Research

December 2017

2018 outlook: OPEC strategy for the shale age still evolving

Higher spare capacity in 2017. May decline in

2018 and induce contango

US supply is more elastic than assumed: 1+

mb/d of US tight liquids growth in 2018

1. Commentary should focus more on demand drivers

2. OPEC/Non-OPEC Dec. of Cooperation is signaling mechanism that won’t be scrapped

3. Just as during price decline, OPEC testing symmetry and degree of shale response.

4. OPEC strategy balancing short and long term revenue maximization, collectively.

Seeking relatively high and stable prices not price fluctuations.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

-3

-2

-1

0

1

2

3

4

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

Spare Capacity and Brent Time Structure

Brent M1-M3 (LHS) Spare Capacity/Demand

$63

$52 $55

$-

$10

$20

$30

$40

$50

$60

$70

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

Completions Y+1 Calendar Avg Price

With prices above $50 ...

...the rate of completions

picked up

19

Source: IEA (history), Barclays Research

Oil fields naturally decline, but new additions mitigate the field/basin/country-level declines

Production outside the US comes from multiple locations

26 March 2018

-400

-200

0

200

400

600

800

Ca

na

da

Bra

zil

Ka

zak

hsta

n

Oth

er F

SU

Au

stralia

UK

Oth

er N

on

-OE

CD

Am

eric

as

Ind

ia

Ind

on

esia

Vie

tna

m

Eg

yp

t

Co

lom

bia

Ch

ina

Me

xic

o

kb/d

Production Growth/Decline outside US (2018 and 2019)

18 v 17 19 v 18

US production not shown

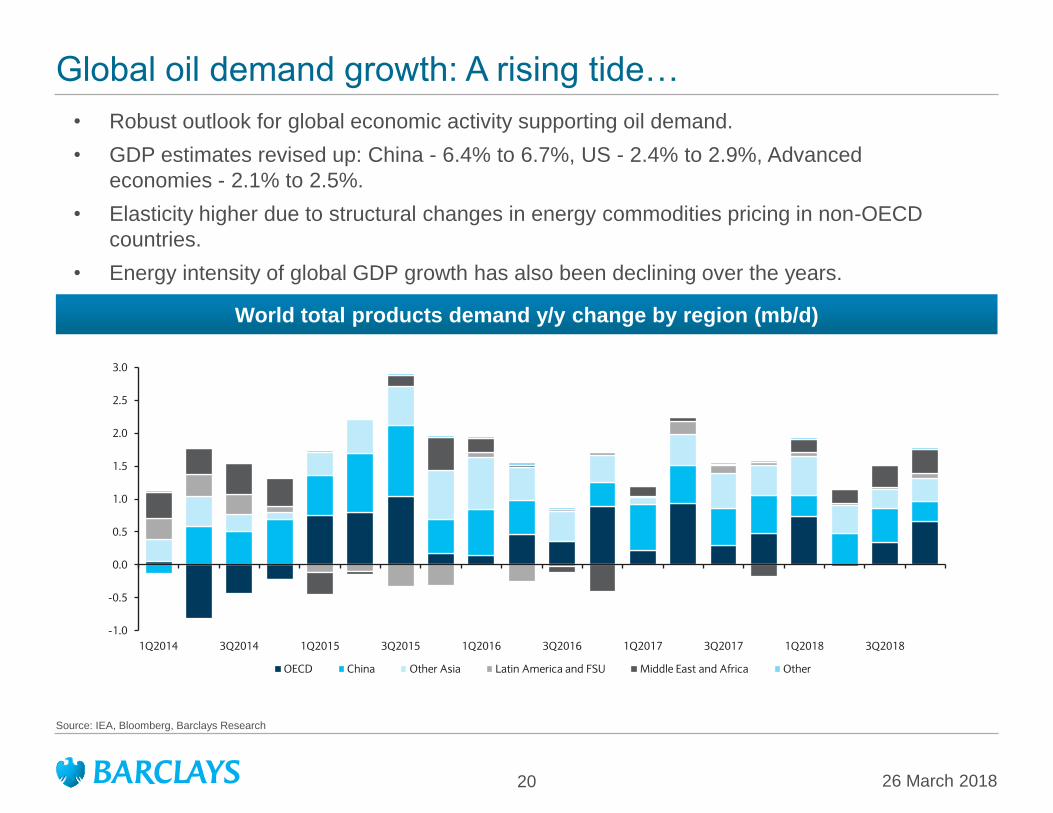

Global oil demand growth: A rising tide…

Source: IEA, Bloomberg, Barclays Research

World total products demand y/y change by region (mb/d)

20

• Robust outlook for global economic activity supporting oil demand.

• GDP estimates revised up: China - 6.4% to 6.7%, US - 2.4% to 2.9%, Advanced

economies - 2.1% to 2.5%.

• Elasticity higher due to structural changes in energy commodities pricing in non-OECD

countries.

• Energy intensity of global GDP growth has also been declining over the years.

26 March 2018

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1Q2014 3Q2014 1Q2015 3Q2015 1Q2016 3Q2016 1Q2017 3Q2017 1Q2018 3Q2018

OECD China Other Asia Latin America and FSU Middle East and Africa Other

21

Accelerating economic activity is helping tighten the oil market

Source for all: Rystad Energy UCube, Petrologistics, EIA, Bloomberg, Barclays Research

Higher industrial activity in the eurozone

helped boost diesel demand there as well

Lower unemployment rate helped lift jet/kero

demand

Lower unemployment rate was favorable for

jet/kero demand growth in OECD Europe

Higher commodity prices also helping lift

activity in exporting countries like Brazil

26 March 2018

-2%

-1%

0%

1%

2%

3%

4%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

01 03 05 07 09 11 13 15 17

US jet/kero demand y/y change

US unemployment rate change (rhs)

-20%

-15%

-10%

-5%

0%

5%

10%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

01 03 05 07 09 11 13 15 17

OECD Europe diesel demand y/y change

Eurozone IP y/y change (rhs)

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

01 03 05 07 09 11 13 15 17

OECD Europe jet/kero demand y/y change

Eurozone unemployment rate change (rhs)

-5%

-2%

1%

4%

7%

10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

01 03 05 07 09 11 13 15 17

Brazil diesel demand y/y change

Brazil Real GDP y/y change (rhs)

Natural Gas Outlook

23

Storage levels entered winter (end October) at 5%

above the five-year average and are now 16%

below the five-year average

Storage levels are on pace to end March at their lowest level since 2014

Source for both charts: EIA, Bloomberg, Barclays Research

Current March forecasts suggest a total winter

2017-18 that will come in 2% warmer than the 10-

year average but 12% colder than last winter

March 2018

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Winter '17-'18

forecast

Winter '16-'17 10-year

HDDs

Nov Dec Jan Feb Mar Total

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Jan

-17

Fe

b-1

7

Ma

r-1

7

Ap

r-1

7

Ma

y-1

7

Jun

-17

Jul-

17

Au

g-1

7

Se

p-1

7

Oct

-17

No

v-1

7

De

c-1

7

Jan

-18

Fe

b-1

8

Ma

r-1

8

24

…resulting in more gas in storage, which has, in

turn, weighed on prices

The eternal struggle for US gas: Too much gas not enough demand

Source for both charts: EIA, Bloomberg, Barclays Research

The shale revolution has increased the spread

between total supply and total demand…

March 2018

-50

-40

-30

-20

-10

0

10

20

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Jan

Ap

r

Jul

Oct

Bcf/d

2005-2009 2010-20140.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

3,200

3,300

3,400

3,500

3,600

3,700

3,800

3,900

4,000End Octobber storage (RHS)

Henry Hub Avg

$/MMBtu Bcf

'05-'09 '10-'14 '15-'17

27

The build out in the US will make it a top three

global LNG exporter by 2020

The global LNG industry is in the middle of one of the larger build outs ever

Source for both charts: GIIGNL, Barclays Research

We forecast global LNG supply to grow from

295MMt in 2017 to around 354 MMt in 2020

0

50

100

150

200

250

300

350

400

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

MMt/y Forecast

2000-04

CAGR 5%

2005-09

CAGR 5.2%

2010-14

CAGR 1.6%

2015-20

CAGR 7%

Qatari build out

Aussie/ US buildoutCountry

2015

market

share

Country2020

market

share (F)Qatar 32% Australia 22%

Australia 12% Qatar 21%

Malaysia 10% US 14%Nigeria 8% Malaysia 8%

Indonesia 7% Nigeria 6%

Algeria 5% Russia 4%

Trinidad 5% Indonesia 4%

Russia 4% Trinidad 4%

Oman 3% Algeria 3%

Papua NG 3% Oman 2%

March 2018

Australia

26

Incremental demand growth will slow in 2018

relative to 2017. Price rebound in 2020 is highly

dependent on LNG export levels

Exports to Mexico and power burn have also offered incremental demand for gas

Source for both charts: EIA, Bloomberg, Barclays Research

Exports to Mexico have increased steadily but are

limited by downstream pipes and CCGTs in

Mexico

March 2018

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

Bcf/d

0.9

0.40.5

0.3 0.3

0.7

1.6

1.3

2.2

2.7

0.00

0.50

1.00

1.50

2.00

2.50

3.00

2016 2017 2018 2019 2020

Bcf/d

Mexico P/L LNG

27

Gas and renewables have gained as coal

generation has moved lower

Overall, electricity demand in the US has been relatively static

Source for both charts: EIA, Bloomberg, Barclays Research

Total generation in the US has showed limited

growth

March 2018

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Jan

-08

Se

p-0

8

Ma

y-0

9

Jan

-10

Se

p-1

0

Ma

y-1

1

Jan

-12

Se

p-1

2

Ma

y-1

3

Jan

-14

Se

p-1

4

Ma

y-1

5

Jan

-16

Se

p-1

6

Ma

y-1

7

Gwh

0%

10%

20%

30%

40%

50%

60%

2008 2009 2010 2011 2012 2013 2014 2015 2016

Gas Coal Wind/Solar

28

Large y/y ramp up in pipeline capacity will

support higher production levels out of the

Northeast

Northeast production grows as increased levels of take away capacity come online

Source: Bloomberg, EIA, Platts, Barclays Research

After some 2017 delays, major northeast pipes

seem ready to ramp up in 2018

0

5

10

15

20

25

30

Jan-16 Jan-17 Jan-18

Bcf/d

-Rex Z3

-Tetco projects-Atlantic Sunrise 1-Leach Xpress- Rover phased in

-Atlantic Sunrise 2-Bayway Lateral-Nexus

-Mountaineer Xpress- WB Xpress

March 2018

2017 additionsCapacity

(MMcf/dStatus Date

Access South 320 Online

Adair Southwest 200 Online

Lebanon Extension 102 Online

Leach Xpress 1500 Online

Rover 1A & 1B 1625 Online

Total 3,747

2018

Rover 1625Full approvals for phase

two except TuscawarasQ2 '18

Nexus 1500 Under Construction 2H '18

Atlantic Sunrise 1700 Under Construction Summer '18

Bayway Lateral 300 Awaiting FERC 2H '18

Mountaineer

Xpress2700 Waiting on approvals Q4 '18

Mountain Valley 650Received FERC notice to

proceed in early JanQ4 '18

Total 8,475

29

Over 10 Bcf/d of takeaway capacity from the

Permian

Permian associated gas production continues to move higher as the oil directed rig count has grown

Source: Barclays Research

We expect that Permian production will cross

10 Bcf/d this year

Proposed PipelinesCapacity

(MMcf/d)Date Origin Destination

Pecos Trail 1850 2Q 19 Reeves County Agua Dulce

Gulf Coast Express 1700 2H19 Waha Agua Dulce

Enterprise Unnamed 1500 2H19 Waha Agua Dulce

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

MMcf/d

March 2018

North Outlet

Capacity

(MMcf/d

)

Utilization

NGPL 150

NNG 500

EPNG 300

Total North 950 ~30%

Mexico Outlet

Roadrunner 570

Comanche 1100

Trans-Pecos 1400

Total Mexico 3070 ~5%

West outlet

EPNG 2400

Transwester 500

Total West 2900 ~80%

East Outlet (Hou

ship/Katy)

Oasis 1200

KMTP 200

EDP/DCP 800

East-Dallas

Atmos-Texas 800

EDP Texas-ETP

Fuel800

Total East 3800 ~80%

30

We expect associated gas production growth

of almost 3.2 bcf/d this year

An average horizontal well in the Permian

yields about 140 kb of oil over 12 months…

March 2018

Associated gas production: How sensitive to oil?

…and about 300 MMcf of associated gas

production

Most of this growth will come from increased

activity in the Permian region

Source for all charts: DrillingInfo, EIA, Barclays Research

Pre-2013

20132014

20152016

2017

0

2

4

6

8

10

12

Q1 13 Q1 14 Q1 15 Q1 16 Q1 17 Q1 18

2018

0

50

100

150

200

250

300

2013 2014 2015 2016E 2017E

0

20

40

60

80

100

120

140

160

2013 2014 2015 2016 2017E

Region 2016 2017E 2018E 2017E 2018E

Permian 7.12 8.31 10.21 1.18 1.90

Rockies 8.12 7.96 8.29 (0.16) 0.33

Eagle Ford 7.01 6.15 6.39 (0.87) 0.24

Bakken 1.71 1.82 2.20 0.11 0.38

Scoop/Stack 2.78 3.05 3.36 0.27 0.31

Y/y changeAssociated gas production (bcf/d)

28

Lower oil prices have slowed LNG FIDs. Just one FID in 2017 (Coral LNG 3.4 MMt)

Source for both charts: GIIGNL, Barclays Research

Sabine Pass

Cove Point

Cameron

Corpus

0

20

40

60

80

100

120

140

160

2000–05 2006–10 2011–14 2015-16

MMt/y

Middle East Australia Other Pacific United States Other Atlantic Total

Brent $33.29 Brent $75.17 Brent $107.60 Brent $47.83

Qatari mega train build-out

March 2018

Natural gas balances

Source: Barclays Research

26 March 2018 37

2013 2014 2015 2016 2017 2018E 2013 2014 2015 2016 2017 2018E

Supply - total (Bcf/d) 69.0 73.2 75.8 73.8 72.3 76.7 0.1 4.2 2.6 (2.0) (1.5) 4.4

US L-48 production 65.4 70.0 73.2 71.9 72.6 79.1 0.7 4.6 3.2 (1.3) 0.7 6.4

Canadian Exports to US, net 5.1 5.1 5.3 5.9 5.6 5.6 (0.3) (0.0) 0.2 0.6 (0.3) (0.0)

US LNG imports, net 0.3 0.1 0.2 (0.3) (1.7) (3.2) (0.1) (0.1) 0.1 (0.4) (1.5) (1.5)

Exports to Mexico 1.8 (2.0) (2.9) (3.8) (4.2) (4.7) 0.1 (3.8) (0.9) (0.9) (0.5) (0.5)

Demand - total (Bcf/d) 71.7 73.0 74.8 75.1 74.2 76.6 4.6 1.2 1.8 0.3 (0.9) 2.4

Residential & Commercial 22.5 23.6 21.6 20.4 20.9 21.3 3.3 1.0 (2.0) (1.2) 0.5 0.4

Industrial 20.4 21.0 20.6 21.1 21.7 22.0 0.6 0.6 (0.3) 0.5 0.6 0.3

Power 22.4 22.3 26.3 27.3 25.3 26.3 (2.5) (0.1) 4.0 0.9 (2.0) 1.0

Other 6.4 6.2 6.3 6.4 6.4 7.0 0.5 (0.3) 0.1 0.1 0.0 0.6

Storage Inventories (Tcf)

End of March 1.7 0.9 1.5 2.5 2.1 1.4 (0.8) (0.9) 0.6 1.0 (0.4) (0.6)

End of October 3.8 3.6 3.9 4.0 3.8 3.9 (0.1) (0.2) 0.4 0.1 (0.2) 0.1

2013 2014 2015 2016 2017 2018E Q3 Q4 Q1 Q2 Q3 Q4

3.73 4.37 2.61 2.48 2.96 3.01 2.94 2.89 3.12 3.23 3.01 2.69

A nnual av erage y/y change

A nnual av erage

Natural gas price ($/MMBtu)

2017 2018E

Medium-term oil price outlook

34

Source: Barclays Research

Global supply is set to grow at an average pace of 1 mb/d through 2025

Most of the growth will come from US tight oil (+810 kb/d y/y); OPEC is expected to add 240 kb/d

y/y on average, while the rest of the supply stack is set to remain flat

26 March 2018

890

780

740

760

740840

$60

$57 $55

$70

$60

$73

$0

$10

$20

$30

$40

$50

$60

$70

$80

-1,000

-500

0

500

1,000

1,500

2,000

2,500

2018 2019 2020 2021 2022 2023 2024 2025

OPEC

US Tight Oil

Other Non-OPEC

Brent ($/bbl, rhs)

MEID

35

Source for all charts: IMF, IEA, Bloomberg, Barclays Research

Annual supply revisions continue to outpace

higher demand expectations

Non-OPEC supply (ex US tight oil and

Canadian Oil Sands) remains flat through 2021

Supply gap thesis is valid, but it is deferred and not as big

0.0

0.5

1.0

1.5

2.0

2.5

2015 2016 2017 2018 2019 2020

Revisions from July 2016 Medium Term

Global Supply Demand

~500 kb/d of the change

is due to change in

baseline expectations

~1 mb/d due to change

in near term forecast

expectations

26 March 2018

0

5

10

15

20

25

30

35

40

45

50

2010 2012 2014 2016 2018 2020 2022 2024

Non-OPEC non-tight oil or oil sands

production

by start time at $55 Brent

Pre-2010 2011-2017 2018-2021

mb/d

at $70/b

36

Note: WoodMackenzie assumes 15% cost of capital, WTI equivalent prices, half cycle breakeven. Source: WoodMackenzie, Barclays Research.

Nearly 85% of the cost base is below $60/bl at a 15% IRR; breakevens have fallen a further 15%

just in the last year

Woodmac resource base assessments keep growing y/y

$0

$20

$40

$60

$80

$100

$120

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000

Q3 2014

Q3 2015

Q3 2016

Q3 2016

Q3 2017

WTI Breakeven at 15% IRR ($/bbl)

Cumulative commercial liquids resource (mmboe)

26 March 2018

37

• Our estimates are based on higher world GDP growth, coupled with lower unemployment

rates in developed countries and rising per capita income levels in the developing world.

• Transport remains the key growth driver, contributing more than three-fourths to the net

consumption increase, as increasing private vehicles density, trucking and air miles

travelled more than offset the effect of growing electric vehicle sales and fuel efficiency.

In our base case, we expect global liquids demand to grow to about 106.2 mb/d by 2025

Source: IEA, WIND , Bloomberg, Barclays Research

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

U.S. Europe

China India

ROW World (Base Case)

World (Low GDP Growth) World (Mobility Revolution)

Liquids demand growth (mb/d)

26 March 2018

38

• Use of oil products to produce petrochemicals to grow at 2% CAGR over the medium

term

• Aviation: growing air passenger miles resulting from improved affordability around the

world due to declining unemployment in the developed world, rising per capita income

levels in developing countries and lower fuel costs

In our base case, we expect global liquids demand to grow to about 106.2 mb/d by 2025

Source: IEA, WIND , Bloomberg, Barclays Research

90

92

94

96

98

100

102

104

106

108

Cars

Other

Transport

Petchem

Power

Other

20

16

20

25

Process

Heating

Trucks

20

16

26 March 2018

39

Transport drives most of the demand growth in our base case, despite fuel efficiency gains and rapid growth in EVs

2016 Oil demand by end-use

Transport

56%

Petrochemical

12%

Power

5%

Process Heating

6%

Other

21%

Source for all charts: IMF, IEA, BP, Bloomberg, Barclays Research

Ownership increases as income rises

Higher ownership rates drive continued

increase in car stock

U.S.Germany

U.K.Russia

MexicoChina

BrazilSouth

Africa

Indonesia

India

6

8

10

12

3 4 5 6 7

Ln

(PP

P G

DP

pe

r c

ap

ita

-4

50

0 U

SD

)

Ln(Passenger cars per 1000 capita)

800

850

900

950

1,000

1,050

1,100

1,150

1,200

1,250

1,300

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Global car stock (millions)

26%

18%

6%5%

1%

7%

12%

8%

6%

12%Road Passenger Vehicles

Road Freight

Aviation

Maritime

Other Transport

Steam/Proc. Heat

Petchem Feeds.

Buildings

Power Gen

Other

26 March 2018

40

Electric vehicle summary

26 March 2018

• Road passenger transport and road freight account for roughly 45% of oil demand.

• Electric vehicles are making inroads into passenger and freight fleets but have too little market

share today to move the needle on oil demand.

• Fuel efficiency improvements will likely play a much larger role than EV penetration in demand

destruction over the next 5-10 years.

• We estimate that oil demand from passenger transport should increase 2.7 mb/d from 2016-25

after accounting for EV penetration (-1 mb/d) and fuel efficiency gains (-2.6 mb/d).

• EV penetration (% of car fleet) should increase twenty-fold from 2016-25 to 4.3% despite

declining subsidy programs (Barclays estimate). There are several factors that will drive this

trend

• Government policies discourage ICE vehicle usage through restrictions and bans

• Battery technology should continue to improve, helping lower EV costs to levels competitive

with ICE counterparts

• The number of EV models will likely expand rapidly in the coming years as auto

manufacturers dedicate more resources to this growing market

• Transport-as-a-service, pooling, and autonomous driving technology should lower the overall

cost of EV usage and could significantly alter the current individual vehicle ownership model.

The authoring analysts would like to thank Amarpreet Singh for his assistance with the preparation of this presentation.

41

EV car sales have gone parabolic…

Source for both charts: Based on IEA data from Global EV Outlook 2017 © OECD/IEA 2017, www.iea.org/statistics. License: www.iea.org/t&c; as modified by Barclays Research, EV-Volumes.com,

Barclays Research

26 March 2018

BEVs have been gaining market share versus

PHEVs in recent years

China accounted for roughly half

of EV sales in 2017

150%

70%

60%

70%

40%

60%

0

200

400

600

800

1,000

1,200

1,400

2011 2012 2013 2014 2015 2016 2017E

China

Japan

Europe

USA

Others

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

200

400

600

800

1,000

1,200

1,400

2011 2012 2013 2014 2015 2016 2017E

BEV

PHEV

% BEV (rhs)

42

… and the EV car fleet is expanding at a rapid pace…

26 March 2018

The global EV fleet more

than doubled since 2015

China’s EV fleet surpassed

the US and Europe in 2016

280% 180%110%

80%

80%

60%

60%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2010 2011 2012 2013 2014 2015 2016 2017E

China

Japan

Europe

USA

Others

Source for both charts: Based on IEA data from Global EV Outlook 2017 © OECD/IEA 2017, www.iea.org/statistics. License: www.iea.org/t&c; as modified by Barclays Research, EV-Volumes.com,

Barclays Research

0%

20%

40%

60%

80%

100%

120%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2010 2011 2012 2013 2014 2015 2016 2017E

BEV

PHEV

% BEV (rhs)

99%

EV % of sales

ICE & Others

43

… but perspective is needed

26 March 2018

EVs have gained sizable market share

in some countries (% of sales)…

… but EVs represented only 1%

of the total car sales in 2016…

0%

5%

10%

15%

20%

25%

30%

35%

2011 2012 2013 2014 2015 2016

Norway

Netherlands

Sweden

France

United Kingdom

China

Source for both charts: Based on IEA data from Global EV Outlook 2017 © OECD/IEA 2017, www.iea.org/statistics. License: www.iea.org/t&c; as modified by Barclays Research, EV-Volumes.com,

Barclays Research

99.8%

Evs % of fleet

ICE & Others

… and represent a small fraction of the total

car fleet

Country Purchase Incentives* Other incentives*

Canada Provincial incentives of $6-13k Various provincial exemptions from fees

including on toll roads, parking, etc.

China Tax exemptions of up to ~$8k, with local tax exemptions as well. Certain programs provide

free license plates to EV purchasers (normally $15,000, allotted by lottery system)

Increased road access and free parking

Denmark Registration tax reductions

France Bonus of up to $11k for BEVs when diesel car retired. Up to $4k for PHEV when diesel car

retired.

Germany Up to $4.4k for BEV and $3.3k for PHEV. Subsidy funding split between government and

automaker

Increased road access and free parking

India Rebates or exemptions from VAT and registration tax exist but vary by state level

Japan Up to $7.7k subsidy, dependent on battery size Increased road access and fee waivers

Netherlands BEVs exempt from registration tax and ownership tax, PHEVs receive 50% reduction in

ownership tax

Norway Exempt from purchase tax, and BEVs exempt from VAT Toll- and ferry-fee waivers and free parking

South Korea National subsidies of $12.3k for BEVs and $4.4k for PHEVs. Local subsidies ranging from

$2.7k to $10.6k. Tax reductions of $3.5k for BEVs and $2.4k for PHEVs.

Sweden Rebates of $4.5k for BEVs and $2.3k for PHEVs. Circulation tax exemptions for low

emissions EVs of up to $340 per year

United Kingdom Subsidies of $5.8k for BEVs and $3.3k for PHEVs. Excise tax exemption for BEVs and

reduction for PHEVs

Increased road access, exemption from

congestion fees, and free parking

United States National tax credits of $2.5-7.5k. State level rebates and tax exemptions also offered

44

EV uptake has relied on government incentive programs

26 March 2018

Note. *May not include all incentives or recent changes to subsidy programs. Source: Based on IEA data from Global EV Outlook 2017 © OECD/IEA 2017, www.iea.org/statistics. License:

www.iea.org/t&c; as modified by Barclays Research, Government websites, Barclays Research

Continued cost reductions and rising utility

Source: Bloomberg New Energy Finance, Boston Consulting Group, Tesla, Ford, Barclays Equity Research The Battery Revolution September 2015

26 March 2018 45

• EV battery costs expected to fall further

• ‘Transport as a Service’ to cut cost per mile traveled, challenge traditional vehicle

ownership model

• Autonomous technology to increase utility

Forecasts call for battery costs to decline ~40% by 2020 and ~55% by 2025

as scale of production increases and technology improves

156 140

130 10690

120 80 70$0

$200

$400

$600

$800

$1,000

$1,200

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Observed prices ($/kWh)

BNEF

Barclays

BCG Base

BCG Low

Falling battery costs and expanding charging infrastructure

Source: Bloomberg New Energy Finance, Barclays Research

26 March 2018 46

Battery costs have fallen by 2/3 since 2012 Charging capacity continues to expand

0

1

2

3

4

5

6

7

8

9

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014 2015 2016

Thousands

Fast Charge

Slow Charge

EVs:Public Chargers

(rhs)

Source: Based on IEA data from Global EV Outlook 2017 © OECD/IEA 2017, www.iea.org/statistics. License: www.iea.org/t&c; as modified by Barclays Research, Barclays Research

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

2012 2013 2014 2015 2016 2017

Battery prices ($/kWh)

Range Weighted Average

Fuel economy standards inflect post-2020

Note: China's target reflects gasoline fleet scenario. If including other fuel types, the target will be higher. Source: ICCT, Barclays Research

47

25

35

45

55

65

75

85

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

MP

G, n

orm

alis

ed

to

US

CA

FE

te

st c

yc

le

EU enacted EU proposed US enacted China enacted China proposed Japan enacted

EU 2021: 60.6

US 2025: 56.2

China 2020: 50.1

Japan 2020: 55.1

EU 2025: 72.5-82.3

26 March 2018

48

Electronic vehicles should make inroads into oil demand over the medium term

Source: Barclays Commodities Research Disruptive Stability Report (July 2017)

33% EV penetration by 2040 could affect oil

demand by ~ 9 mb/d

In our analysis, EV uptake and increased fleet fuel

efficiency could cut oil demand by ~ 3.5 mb/d in

2025 (mb/d)

Source: Bloomberg, Barclays Commodities Research

20

21

22

23

24

25

26

27

28

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Estimated global oil demand from cars (mb/d)

No Increase in FE or EV adoption

Only Fuel Efficiency Improvements

Only EV Benefits

Demand Inclusive of EV and FE Benefits

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2016 2019 2022 2025 2028 2031 2034 2037 2040

EVs (Bloomberg, LHS)

ICE Vehicles (Bloomberg, LHS)

EV Penetration (Bloomberg)

EV Penetration (Barclays)

26 March 2018

Appendix

50

Source: Based on IEA data from The Future of Trucks: Implications for energy and the environment © OECD/IEA 2017, www.iea.org/statistics. License: www.iea.org/t&c; as modified by Barclays Research.

December 2017

IMO 2020: Marine bunker fuel sulfur limits lowered to 0.5%

The maritime industry consumes ~5% of

global liquid fuels

The regulation has had a visible impact on fuel

oil cracks

26%

18%

6%5%

1%

7%

12%

8%

6%

12%Road Passenger Vehicles

Road Freight

Aviation

Maritime

Other Transport

Steam/Proc. Heat

Petchem Feeds.

Buildings

Power Gen

Other

The maritime industry has several options in order

to comply with this rule:

•Ultra low sulfur (.5%) fuel oil

•Ultra low sulfur (.5%) marine gasoil

•LNG conversion

•Scrubber installation

-25

-20

-15

-10

-5

0

0

2

4

6

8

10

12

14

16

18

Mar-18 Sep-18 Mar-19 Sep-19 Mar-20 Sep-20 Mar-21 Sep-21

Gasoil Crack Fuel Oil, 3.5% Rdam Crack (rhs)

IMO regulations reflected in the

HSFO crackcurve

Less so in gasoil cracks

This regulation will have several affects on the market:

•Wider light-heavy spreads (all else equal)

•Positive for ULSD/gasoil cracks

•Negative for HSFO cracks

•More expensive bunkers, and thus wider waterborne

crude and product differentials

•Positive for complex refiners that produce minimal HSFO

•Negative for coastal refineries producing HSFO

Source: Bloomberg, Barclays Research.

51

Offshore oil output accounts for one-third of global supplies; capex on the offshore cedes share to unconventionals

Capex on offshore exp & development to fall,

but then rebound with rising prices

Source for all charts: Rystad Energy Ucube, Barclays Research

Growth concentrated in certain countries

If prices stay close to $50/b, reduction in

offshore supplies by ~6 mb/d

0

100

200

300

400

500

600

700

800

0%

10%

20%

30%

40%

50%

60%

2000 2005 2010 2015 2020 2025 2030

Share of Capital Spending on Oil Assets

(by supply segment)

Offshore share

Unconv. Share

Other onshore share

Total ($B), RHS

-1,000 -500 0 500 1,000 1,500 2,000

Brazil

Iran

United States

Kazakhstan

Saudi Arabia

Russia

Australia

Guyana

Qatar

Senegal

Canada

United Kingdom

Venezuela

Malaysia

China

Angola

Selected sources of growth/decline in

offshore oil output from 2017-2030 (kb/d)

0

5,000

10,000

15,000

20,000

25,000

30,000

2013 2016 2019 2022 2025

Production forecast by status (kb/d)

Producing Under developmentPre-FID At $50/b

*Rystad assumes prices rise to $90/b by 2025

but if prices stay at $50 offshore oil production

would be roughly 6.5 mb/d lower

20%

2%

3%

53%

14%

Proven (P90) offshore oil reserves

Major Integrated Independent NOC INOC

26 March 2018

And the majority of the proven reserves

controlled by NOCs

52

Auto manufacturers planning big expansions to EV offerings

Note: List not all inclusive. Source: Company reports, BBC, Reuters, Bloomberg, Barclays Research

Company Electric vehicle sales targets

BMW 100,000 electric car sales in 2017 and 15-25% of BMW group sales by 2025

GM 30,000 annual electric car sales by 2017

Chinese OEMs 4.52 million electric car sales by 2020

Daimler 0.1 million annual electric car sales by 2020

Renault-Nissan 1.5 million cumulative sales of electric cars by 2020

Tesla 500,000 annual electric car sales by 2018. 1 million annual electric care sales by 2020

Volkswagen 2-3 million annual electric car sales by 2025

Volvo 1 million cumulative electric car sales by 2025

Company Planned electric vehicle offerings

BMW Provide 12 BEVs and 13 hybrids by 2025

GM Offer at least 20 electric vehicles by 2023

Daimler Offer 10 BEVs by 2022

Fiat Chrysler Incorporate electrification into half of its fleet by 2022

Ford Launch 13 new electrified vehicles over the next five years

Honda Launch two fully electric vehicles in 2018 and electrify two-thirds of its offerings by 2030

Jaguar Land Rover Every new Jaguar or Land Rover launched from 2020 will be electrified

Renault-Nissan Launch 12 new ZEVs by 2022

Toyota Provide solid state battery electric cars by 2022

Volkswagen Eighty new electric vehicles by 2025

Volvo Every model launched from 2019 onward will be electrified

Expect the electric vehicle offering to expand

significantly in the coming years

Sales targets are still a drop in the bucket

(IEA data)

Note: List not all inclusive. Source: IEA Global EV Outlook 2017

26 March 2018

53

Analyst Certifications and Important Disclosures Analyst Certification(s)

I, Michael Cohen hereby certify (1) that the views expressed in this research report accurately reflect my personal view about any or all of the subject securities or issuers referred to in this research report and (2) no part of our compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this research report.

Important Disclosures:

Barclays Research is produced by the Investment Bank of Barclays Bank PLC and its affiliates (collectively and each individually, "Barclays")

All authors contributing to this research report are Research Analysts unless otherwise indicated. The publication date at the top of the report reflects the local time where the report was produced and

may differ from the release date provided in GMT.

Availability of Disclosures:

For current important disclosures regarding any issuers which are the subject of this research report please refer to https://publicresearch.barclays.com or alternatively send a written request to:

Barclays Research Compliance, 745 Seventh Avenue, 13th Floor, New York, NY 10019 or call +1-212-526-1072.

Barclays Capital Inc. and/or one of its affiliates does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Barclays may have a conflict

of interest that could affect the objectivity of this report. Barclays Capital Inc. and/or one of its affiliates regularly trades, generally deals as principal and generally provides liquidity (as market maker or

otherwise) in the debt securities that are the subject of this research report (and related derivatives thereof). Barclays trading desks may have either a long and / or short position in such securities,

other financial instruments and / or derivatives, which may pose a conflict with the interests of investing customers. Where permitted and subject to appropriate information barrier restrictions, Barclays

fixed income research analysts regularly interact with its trading desk personnel regarding current market conditions and prices. Barclays fixed income research analysts receive compensation based

on various factors including, but not limited to, the quality of their work, the overall performance of the firm (including the profitability of the Investment Banking Department), the profitability and

revenues of the Markets business and the potential interest of the firm's investing clients in research with respect to the asset class covered by the analyst. To the extent that any historical pricing

information was obtained from Barclays trading desks, the firm makes no representation that it is accurate or complete. All levels, prices and spreads are historical and do not represent current market

levels, prices or spreads, some or all of which may have changed since the publication of this document. Barclays Research Department produces various types of research including, but not limited to,

fundamental analysis, equity-linked analysis, quantitative analysis, and trade ideas. Recommendations and trade ideas contained in one type of Barclays Research may differ from those contained in

other types of Barclays Research, whether as a result of differing time horizons, methodologies, or otherwise.

The Barclays Research Department operates independently from the Absa Research Department. Absa Research is produced by Absa Bank Limited acting through its Corporate and Investment Bank

division, which is a part of Barclays Africa Group Limited and affiliated with the Investment Bank of Barclays Bank PLC. Eligible clients may receive research reports from both research departments,

which may reach different conclusions and may contain different and conflicting forecasts, recommendations, or trade ideas. In order to access Barclays Statement regarding Research Dissemination

Policies and Procedures, please refer to https://publicresearch.barcap.com/S/RD.htm. In order to access Barclays Research Conflict Management Policy Statement, please refer to:

https://publicresearch.barcap.com/S/CM.htm.

All pricing information is indicative only. Prices are sourced from Thomson Reuters as of the last available closing price at the time of production of the research report, unless another time and source

is indicated.

Explanation of other types of investment recommendations produced by Barclays FICC Research:

Trade ideas contained herein that have been produced by the Credit teams within Barclays Research are valid at current market conditions and may not be otherwise relied upon.

Trade ideas contained herein that have been produced by other research teams within Barclays FICC Research shall remain open until they are subsequently amended or closed in a future research

report.

Disclosure of previous investment recommendations produced by Barclays FICC Research:

Barclays FICC Research may have published other investment recommendations in respect of the same securities/instruments recommended in this research report during the preceding 12 months.

To view previous investment recommendations published by Barclays FICC Research in the preceding 12 months please refer to

https://live.barcap.com/go/research/ResearchInvestmentRecommendations.

Legal entities involved in producing Barclays Research:

Barclays Bank PLC (Barclays, UK)

Barclays Capital Inc. (BCI, US)

Barclays Securities Japan Limited (BSJL, Japan)

Barclays Bank PLC, Hong Kong branch (Barclays Bank, Hong Kong)

Barclays Capital Canada Inc. (BCCI, Canada)

Barclays Bank Mexico, S.A. (BBMX, Mexico)

Barclays Securities (India) Private Limited (BSIPL, India)

Barclays Bank PLC, India branch (Barclays Bank, India)

Barclays Bank PLC, Singapore branch (Barclays Bank, Singapore)

26 March 2018

54

Disclaimer This publication has been produced by Barclays Research Department in the Investment Bank of Barclays Bank PLC and/or one or more of its affiliates (collectively and each individually, "Barclays").

It has been distributed by one or more Barclays affiliated legal entities listed below. It is provided to our clients for information purposes only, and Barclays makes no express or implied warranties,

and expressly disclaims all warranties of merchantability or fitness for a particular purpose or use with respect to any data included in this publication. To the extent that this publication states on the

front page that it is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors under U.S.

FINRA Rule 2242, it is an “institutional debt research report” and distribution to retail investors is strictly prohibited. Barclays also distributes such institutional debt research reports to various issuers,

regulatory and academic organisations for informational purposes and not for the purpose of making investment decisions regarding any debt securities. Any such recipients that do not want to

continue receiving Barclays institutional debt research reports should contact [email protected]. Barclays will not treat unauthorized recipients of this report as its clients and accepts no

liability for use by them of the contents which may not be suitable for their personal use. Prices shown are indicative and Barclays is not offering to buy or sell or soliciting offers to buy or sell any

financial instrument.

Without limiting any of the foregoing and to the extent permitted by law, in no event shall Barclays, nor any affiliate, nor any of their respective officers, directors, partners, or employees have any

liability for (a) any special, punitive, indirect, or consequential damages; or (b) any lost profits, lost revenue, loss of anticipated savings or loss of opportunity or other financial loss, even if notified of

the possibility of such damages, arising from any use of this publication or its contents.

Other than disclosures relating to Barclays, the information contained in this publication has been obtained from sources that Barclays Research believes to be reliable, but Barclays does not

represent or warrant that it is accurate or complete. Barclays is not responsible for, and makes no warranties whatsoever as to, the information or opinions contained in any written, electronic, audio or

video presentations of third parties that are accessible via a direct hyperlink in this publication or via a hyperlink to a third-party web site (‘Third-Party Content’). Any such Third-Party Content has not

been adopted or endorsed by Barclays, does not represent the views or opinions of Barclays, and is not incorporated by reference into this publication. Third-Party Content is provided for information

purposes only and Barclays has not independently verified its accuracy or completeness.

The views in this publication are solely and exclusively those of the authoring analyst(s) and are subject to change, and Barclays Research has no obligation to update its opinions or the information

in this publication. Unless otherwise disclosed herein, the analysts who authored this report have not received any compensation from the subject companies in the past 12 months. If this publication

contains recommendations, they are general recommendations that were prepared independently of any other interests, including those of Barclays and/or its affiliates, and/or the subject companies.

This publication does not contain personal investment recommendations or investment advice or take into account the individual financial circumstances or investment objectives of the clients who

receive it. The securities and other investments discussed herein may not be suitable for all investors. Barclays is not a fiduciary to any recipient of this publication. Investors must independently

evaluate the merits and risks of the investments discussed herein, consult any independent advisors they believe necessary, and exercise independent judgment with regard to any investment

decision. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information

herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results.

This document is being distributed (1) only by or with the approval of an authorised person (Barclays Bank PLC) or (2) to, and is directed at (a) persons in the United Kingdom having professional

experience in matters relating to investments and who fall within the definition of "investment professionals" in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order

2005 (the "Order"); or (b) high net worth companies, unincorporated associations and partnerships and trustees of high value trusts as described in Article 49(2) of the Order; or (c) other persons to

whom it may otherwise lawfully be communicated (all such persons being "Relevant Persons"). Any investment or investment activity to which this communication relates is only available to and will

only be engaged in with Relevant Persons. Any other persons who receive this communication should not rely on or act upon it. Barclays Bank PLC is authorised by the Prudential Regulation

Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority and is a member of the London Stock Exchange.

The Investment Bank of Barclays Bank PLC undertakes U.S. securities business in the name of its wholly owned subsidiary Barclays Capital Inc., a FINRA and SIPC member. Barclays Capital Inc., a

U.S. registered broker/dealer, is distributing this material in the United States and, in connection therewith accepts responsibility for its contents. Any U.S. person wishing to effect a transaction in any

security discussed herein should do so only by contacting a representative of Barclays Capital Inc. in the U.S. at 745 Seventh Avenue, New York, New York 10019.

Non-U.S. persons should contact and execute transactions through a Barclays Bank PLC branch or affiliate in their home jurisdiction unless local regulations permit otherwise.

Barclays Bank PLC, Paris Branch (registered in France under Paris RCS number 381 066 281) is regulated by the Autorité des marchés financiers and the Autorité de contrôle prudentiel. Registered

office 34/36 Avenue de Friedland 75008 Paris.

This material is distributed in Canada by Barclays Capital Canada Inc., a registered investment dealer, a Dealer Member of IIROC (www.iiroc.ca), and a Member of the Canadian Investor Protection

Fund (CIPF).

Subject to the conditions of this publication as set out above, Absa Bank Limited, acting through its Corporate and Investment Bank division, which is a part of Barclays Africa Group Limited and

affiliated with the Investment Bank of Barclays Bank PLC, an authorised financial services provider (Registration No.: 1986/004794/06. Registered Credit Provider Reg No NCRCP7), is distributing

this material in South Africa. Absa Bank Limited is regulated by the South African Reserve Bank. This publication is not, nor is it intended to be, advice as defined and/or contemplated in the (South

African) Financial Advisory and Intermediary Services Act, 37 of 2002, or any other financial, investment, trading, tax, legal, accounting, retirement, actuarial or other professional advice or service

whatsoever. Any South African person or entity wishing to effect a transaction in any security discussed herein should do so only by contacting a representative of Absa Bank Limited acting through

its Corporate and Investment Bank division in South Africa, 7th Floor, Barclays Towers West, 15 Troye Street, Johannesburg. Absa Bank Limited is an affiliate of the Barclays group.

.

26 March 2018

55

Disclaimer (continued) All Barclays research reports are distributed to institutional investors in Japan by Barclays Securities Japan Limited. Barclays Securities Japan Limited is a joint-stock company incorporated in Japan

with registered office of 6-10-1 Roppongi, Minato-ku, Tokyo 106-6131, Japan. It is a subsidiary of Barclays Bank PLC and a registered financial instruments firm regulated by the Financial Services

Agency of Japan. Registered Number: Kanto Zaimukyokucho (kinsho) No. 143.

Barclays Bank PLC, Hong Kong Branch is distributing this material in Hong Kong as an authorised institution regulated by the Hong Kong Monetary Authority. Registered Office: 41/F, Cheung Kong

Center, 2 Queen's Road Central, Hong Kong.

All Indian securities-related research and other equity research produced by Barclays’ Investment Bank are distributed in India by Barclays Securities (India) Private Limited (BSIPL). BSIPL is a

company incorporated under the Companies Act, 1956 having CIN U67120MH2006PTC161063. BSIPL is registered and regulated by the Securities and Exchange Board of India (SEBI) as a

Research Analyst: INH000001519; Portfolio Manager INP000002585; Stock Broker/Trading and Clearing Member: National Stock Exchange of India Limited (NSE) Capital Market INB231292732,

NSE Futures & Options INF231292732, NSE Currency derivatives INE231450334, Bombay Stock Exchange Limited (BSE) Capital Market INB011292738, BSE Futures & Options INF011292738;

Depository Participant (DP) with the National Securities & Depositories Limited (NSDL): DP ID: IN-DP-NSDL-299-2008; Investment Adviser: INA000000391. The registered office of BSIPL is at 208,

Ceejay House, Shivsagar Estate, Dr. A. Besant Road, Worli, Mumbai – 400 018, India. Telephone No: +91 2267196000. Fax number: +91 22 67196100. Any other reports produced by Barclays’

Investment Bank are distributed in India by Barclays Bank PLC, India Branch, an associate of BSIPL in India that is registered with Reserve Bank of India (RBI) as a Banking Company under the

provisions of The Banking Regulation Act, 1949 (Regn No BOM43) and registered with SEBI as Merchant Banker (Regn No INM000002129) and also as Banker to the Issue (Regn No

INBI00000950). Barclays Investments and Loans (India) Limited, registered with RBI as Non Banking Financial Company (Regn No RBI CoR-07-00258), and Barclays Wealth Trustees (India) Private

Limited, registered with Registrar of Companies (CIN U93000MH2008PTC188438), are associates of BSIPL in India that are not authorised to distribute any reports produced by Barclays’ Investment

Bank.

Barclays Bank PLC Frankfurt Branch distributes this material in Germany under the supervision of Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin).

This material is distributed in Mexico by Barclays Bank Mexico, S.A.

Nothing herein should be considered investment advice as defined in the Israeli Regulation of Investment Advisory, Investment Marketing and Portfolio Management Law, 1995 (“Advisory Law”). This

document is being made to eligible clients (as defined under the Advisory Law) only. Barclays Israeli branch previously held an investment marketing license with the Israel Securities Authority but it

cancelled such license on 30/11/2014 as it solely provides its services to eligible clients pursuant to available exemptions under the Advisory Law, therefore a license with the Israel Securities

Authority is not required. Accordingly, Barclays does not maintain an insurance coverage pursuant to the Advisory Law.

Barclays Bank PLC in the Dubai International Financial Centre (Registered No. 0060) is regulated by the Dubai Financial Services Authority (DFSA). Principal place of business in the Dubai

International Financial Centre: The Gate Village, Building 4, Level 4, PO Box 506504, Dubai, United Arab Emirates. Barclays Bank PLC-DIFC Branch, may only undertake the financial services

activities that fall within the scope of its existing DFSA licence. Related financial products or services are only available to Professional Clients, as defined by the Dubai Financial Services Authority.

Barclays Bank PLC in the UAE is regulated by the Central Bank of the UAE and is licensed to conduct business activities as a branch of a commercial bank incorporated outside the UAE in Dubai

(Licence No.: 13/1844/2008, Registered Office: Building No. 6, Burj Dubai Business Hub, Sheikh Zayed Road, Dubai City) and Abu Dhabi (Licence No.: 13/952/2008, Registered Office: Al Jazira

Towers, Hamdan Street, PO Box 2734, Abu Dhabi).

Barclays Bank PLC in the Qatar Financial Centre (Registered No. 00018) is authorised by the Qatar Financial Centre Regulatory Authority (QFCRA). Barclays Bank PLC-QFC Branch may only

undertake the regulated activities that fall within the scope of its existing QFCRA licence. Principal place of business in Qatar: Qatar Financial Centre, Office 1002, 10th Floor, QFC Tower, Diplomatic

Area, West Bay, PO Box 15891, Doha, Qatar. Related financial products or services are only available to Business Customers as defined by the Qatar Financial Centre Regulatory Authority.

This material is distributed in the UAE (including the Dubai International Financial Centre) and Qatar by Barclays Bank PLC.

This material is not intended for investors who are not Qualified Investors according to the laws of the Russian Federation as it might contain information about or description of the features of

financial instruments not admitted for public offering and/or circulation in the Russian Federation and thus not eligible for non-Qualified Investors. If you are not a Qualified Investor according to the

laws of the Russian Federation, please dispose of any copy of this material in your possession.

This material is distributed in Singapore by the Singapore branch of Barclays Bank PLC, a bank licensed in Singapore by the Monetary Authority of Singapore. For matters in connection with this

report, recipients in Singapore may contact the Singapore branch of Barclays Bank PLC, whose registered address is 10 Marina Boulevard, #23-01 Marina Bay Financial Centre Tower 2, Singapore

018983.

This material is distributed to persons in Australia by either Barclays Bank plc, Barclays Capital Inc., Barclays Capital Securities Limited or Barclays Capital Asia Limited. None of Barclays Bank plc,

nor any of the other referenced Barclays group entities, hold an Australian financial services licence and instead they each rely on an exemption from the requirement to hold such a licence. This

material is intended to only be distributed to “wholesale clients” as defined by the Australian Corporations Act 2001.

IRS Circular 230 Prepared Materials Disclaimer: Barclays does not provide tax advice and nothing contained herein should be construed to be tax advice. Please be advised that any discussion of

U.S. tax matters contained herein (including any attachments) (i) is not intended or written to be used, and cannot be used, by you for the purpose of avoiding U.S. tax-related penalties; and (ii) was

written to support the promotion or marketing of the transactions or other matters addressed herein. Accordingly, you should seek advice based on your particular circumstances from an independent

tax advisor.

© Copyright Barclays Bank PLC (2018). All rights reserved. No part of this publication may be reproduced or redistributed in any manner without the prior written permission of Barclays. Barclays

Bank PLC is registered in England No. 1026167. Registered office 1 Churchill Place, London, E14 5HP. Additional information regarding this publication will be furnished upon request. US33896

26 March 2018