commodities – how to leverage...

TRANSCRIPT

Commodities –How to Leverage OpportunityInvestment Conference, Boston, March 2010

Peter Königbauer | Senior Portfolio Manager

For Broker/Dealer Use Only and Not to be Distributed to the Public

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 2

Commodity Market Update

Investment Philosophy

Strategy Profile

Active Allocation

Alpha Generation

Agenda

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 3

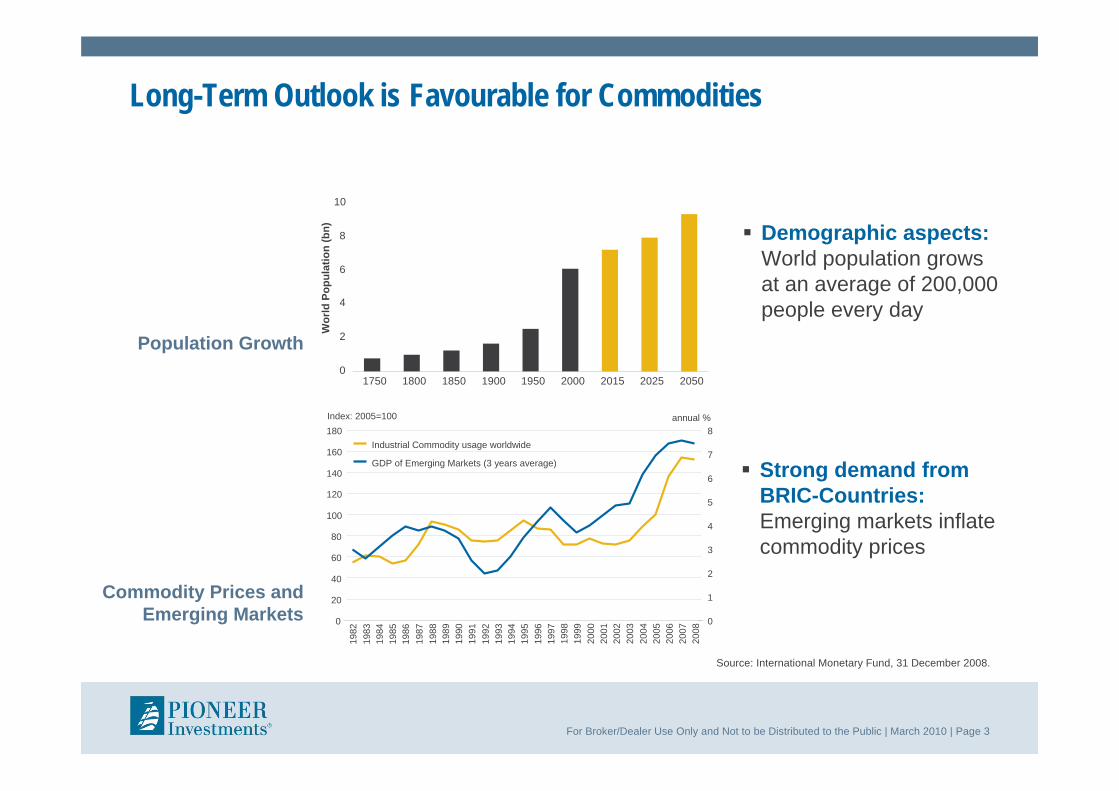

Long-Term Outlook is Favourable for Commodities

Demographic aspects:World population grows at an average of 200,000 people every day

Source: International Monetary Fund, 31 December 2008.

0

2

4

6

8

10

1750 1800 1850 1900 1950 2000 2015 2025 2050

Wor

ld P

opul

atio

n (b

n)

0

20

40

60

80

100

120

140

160

180

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

0

1

2

3

4

5

6

7

8Industrial Commodity usage worldwide

GDP of Emerging Markets (3 years average)

annual %Index: 2005=100

Population Growth

Strong demand from BRIC-Countries:Emerging markets inflate commodity prices

Commodity Prices andEmerging Markets

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 4

Source: International Monetary Fund, World Bank, Keybridge Research LLC

Emerging Markets – ChinaShare of Global Consumption (2008) & Commodity Price Increases (Feb - Nov 2009)

China’s growth may have driven commodity prices up, but its oil demand is still not as strong as expected.

46%

101%

62%

86%

0%

20%

40%

60%

80%

100%

120%

Aluminium Copper Nickel Petroleum

33%

28%

24%

9%

ChinaWorld

Com

mod

ity P

rice

Incr

ease

s (F

eb-N

ov 2

009)

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 5

Inventories: OilWithout Increasing Demand, Oil Prices Will Barely Rise

B A

R R

E L

Source: Pioneer Investments, Bloomberg as at 5 February 2010

US Inventory: Oil

US Inventory: Gasoline

Min / Max 5 Years(2003-2008)

Average 5 Years(2003-2008)

Inventories 2009B

A R

R E

L

B A

R R

E L

170,000

180,000

190,000

200,000

210,000

220,000

230,000

240,000

Jan

Feb

Mar

Apr May

Jun

Jul

Aug Sep Oct

Nov

Dec

90,000

100,000

110,000

120,000

130,000

140,000

150,000

160,000

170,000

180,000

Jan

Feb

Mar

Apr May

Jun

Jul

Aug Sep Oct

Nov

Dec

2000

2200

2400

2600

2800

3000

3200

3400

3600

3800

4000

Jan

Feb

Mar

Apr May

Jun Jul

Aug Sep Oct

Nov

Dec

US Inventory: Heating Oil/Diesel

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 6

Inventories: CopperRising Prices Depend on Europe and the US

Inventories LMI(London Metal Exchange)

Price US Industry Inventories

US Industry Production

Inventory: Copper (World) US Industry Inventory: Copper

Source: Pioneer Investments, Bloomberg as at 31 January 2010

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

28.0

3.20

00

28.0

3.20

01

28.0

3.20

02

28.0

3.20

03

28.0

3.20

04

28.0

3.20

05

28.0

3.20

06

28.0

3.20

07

28.0

3.20

08

28.0

3.20

090

50

100

150

200

250

300

350

400

450

500

85

90

95

100

105

110

115

Jan 00 Jan 02 Jan 04 Jan 06 Jan 08 Jan 10-8.00%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 7

Inventories: Soybeans Inventories Remain Tight Despite Increased Production

Source: Pioneer Investments, Bloomberg as at 31 January 2010

Stock/Use Ratio US Soybeans Production

Soybean Import China US Soybean Production

0

1

2

3

4

5

6

Mill

ion

Tons

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Dec

90

Dec

91

Dec

92

Dec

93

Dec

94

Dec

95

Dec

96

Dec

97

Dec

98

Dec

99

Dec

00

Dec

01

Dec

02

Dec

03

Dec

04

Dec

05

Dec

06

Dec

07

Dec

08

1500

1700

1900

2100

2300

2500

2700

2900

3100

3300

3500

Mill

ion

Met

ric T

ons

2001 2002 2003 2004 2005 2006 2007 2008 2009

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 8

Commodity Market Update

Investment Philosophy

Strategy Profile

Active Allocation

Alpha Generation

Agenda

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 9

Pioneer Funds – Commodity AlphaPortfolio Overview

Active, quantitatively-managed commodity Portfolio

Four alpha sources enhance performance potential: Source 1: Changes in inventory levels can identify attractive opportunities

Source 2: Long/Short positions efficiently exploit investment philosophy

Source 3: Exposure to small commodities increases the opportunity for alpha

Source 4: Active allocation between the five different strategies optimises the performance potential

Broad investment universe (consisting of 31 commodities)

Objective: Generate outperformance versus its reference index, Dow Jones-UBS Commodity Total Return Index (DJ-UBS)

This sub-fund does not invest directly in commodities, but it gains exposure via derivatives linked to the performance of five commodity future indices and sub-indices.

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 10

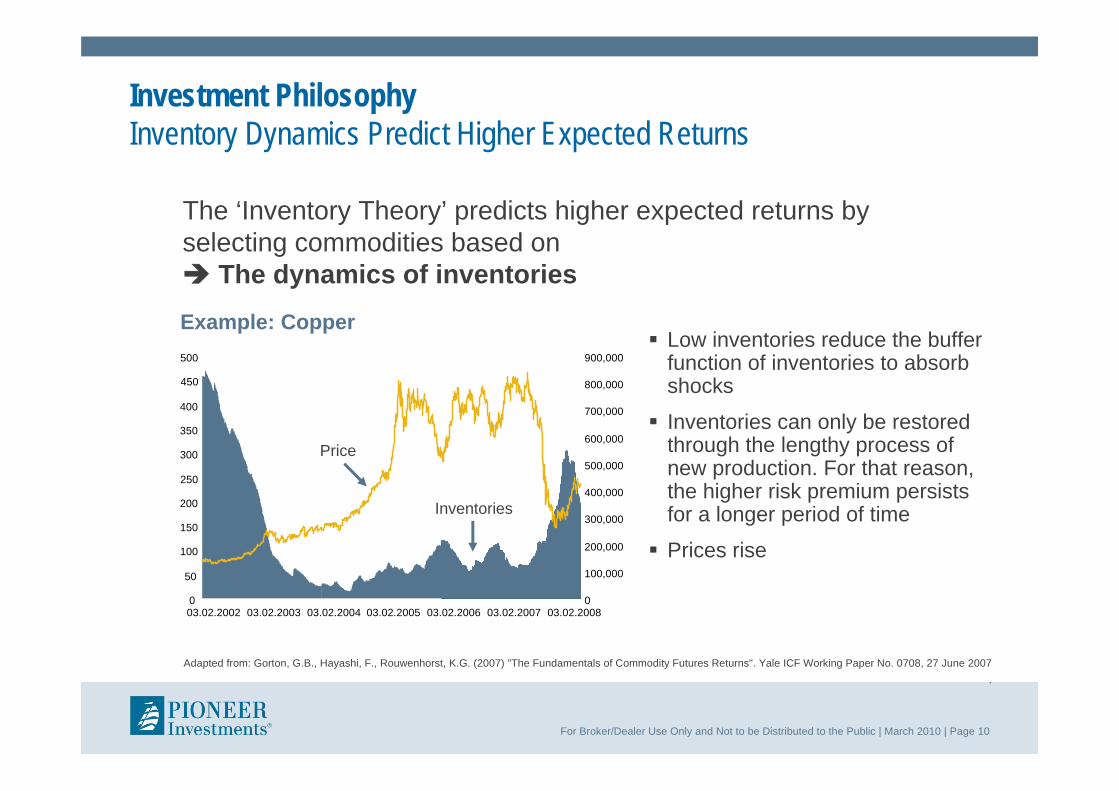

Low inventories reduce the buffer function of inventories to absorb shocks

Inventories can only be restored through the lengthy process of new production. For that reason, the higher risk premium persists for a longer period of time

Prices rise

Adapted from: Gorton, G.B., Hayashi, F., Rouwenhorst, K.G. (2007) "The Fundamentals of Commodity Futures Returns". Yale ICF Working Paper No. 0708, 27 June 2007.

Inventories

Investment PhilosophyInventory Dynamics Predict Higher Expected Returns

The ‘Inventory Theory’ predicts higher expected returns by selecting commodities based on The dynamics of inventories

0

50

100

150

200

250

300

350

400

450

500

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

03.02.2002 03.02.2003 03.02.2004 03.02.2005 03.02.2006 03.02.2007 03.02.2008

Price

Example: Copper

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 11

Commoditieswith lowinventories

Commoditieswith highinventories

Source: Gorton, Gary B., Fumio Hayashi, and K. Geert Rouwenhorst (2006)*A normal inventory level for each commodity is calculated using a Hodrick-Prescott filter on historical inventory data. The Hodrick-Prescott filter is an algorithm, used widely in economics, for extracting a smooth, but possibly non-linear, trend from an economic time series. High inventory is defined as when inventories are above normal, while low inventory is defined as the opposite case. High inventory commodities are selected on a monthly basis and included in the High Inventory index, while low inventory commodities are included in the Low Inventory index. Inventories reflect any revisions which may have been released after initial publication.Source: Inventory data compiled by UBS-FP based on public and private sources.

Investment PhilosophySuccessful Commodity Selection Using Inventory Data*

0.0

100.0

200.0

300.0

400.0

500.0

600.0

1990 1992 1993 1995 1996 1998 1999 2001 2002 2004

DJ-UBS CI TRHigh Inventories TRLow Inventories TR

DJ-UBS CI TR High Inventories TR Low Inventories TRAnn. Return 7.09% 6.72% 11.19%Volatility 11.83% 11.56% 10.76%Sharpe Ratio 0.26 0.23 0.66

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 12

Investment Philosophy: Futures Basis Reflects Inventory LevelsThe Basis is High when Inventories are LowAverage Futures Basis Relative to Normalised Inventories*

-20%

-10%

0%

10%

20%

Aluminium

CocoaCopper

Crude OilHeating

Oil

Lean Hogs

Live Cattle

Natural Gas

Nickel

SoybeanOil

SoybeansUnleaded

GasWheat

Zinc

Bas

is R

elat

ive

to A

vera

ge

High InventoryLow Inventory

Source: Gorton, Gary B., Fumio Hayashi, and K. Geert Rouwenhorst (2006)*A normal inventory level for each commodity is calculated using a Hodrick-Prescott filter on historical inventory data. The Hodrick-Prescott filter is an algorithm, used widely in economics, for extracting a smooth, but possibly non-linear, trend from an economic time series. High inventory is defined as when inventories are above normal, while low inventory is defined as the opposite case. High inventory commodities are selected on a monthly basis and included in the High Inventory index, while low inventory commodities are included in the Low Inventory index. Inventories reflect any revisions which may have been released after initial publication.Source: Inventory data compiled by UBS-FP based on public and private sources.

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 13

Investment Philosophy: Price Performance Reflects Inventory LevelsReturns are High when Inventories are LowReturns Relative to Normalised Inventories*

Source: Gorton, Gary B., Fumio Hayashi, and K. Geert Rouwenhorst (2006)*A normal inventory level for each commodity is calculated using a Hodrick-Prescott filter on historical inventory data. The Hodrick-Prescott filter is an algorithm, used widely in economics, for extracting a smooth, but possibly non-linear, trend from an economic time series. High inventory is defined as when inventories are above normal, while low inventory is defined as the opposite case. High inventory commodities are selected on a monthly basis and included in the High Inventory index, while low inventory commodities are included in the Low Inventory index. Inventories reflect any revisions which may have been released after initial publication.Source: Inventory data compiled by UBS-FP based on public and private sources.

-30%

-20%

-10%

0%

10%

20%

30%

Prio

r 12-

Mon

th R

etur

n R

elat

ive

to A

vera

ge

Aluminium

Cocoa

Copper

Crude OilHeating

Oil

Lean Hogs

Live Cattle

Natural Gas

NickelSoybean

Oil

Soybeans

UnleadedGas

WheatZinc

High InventoryLow Inventory

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 14

Commodity Market Update

Investment Philosophy

Strategy Profile

Active Allocation

Alpha Generation

Agenda

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 15

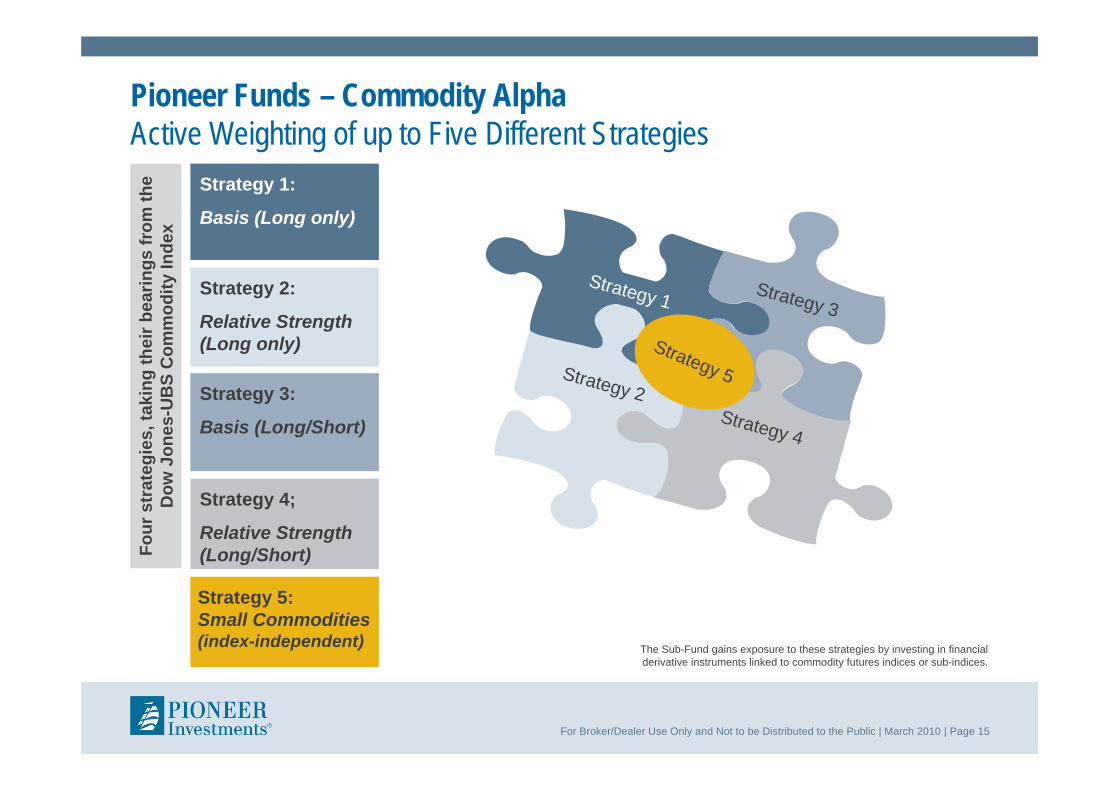

Pioneer Funds – Commodity AlphaActive Weighting of up to Five Different Strategies

Strategy 1 Strategy 3

Strategy 2Strategy 4

Strategy 5

Strategy 1:

Basis (Long only)

Strategy 2:

Relative Strength (Long only)

Strategy 3:

Basis (Long/Short)

Strategy 4;

Relative Strength (Long/Short)

Strategy 5:Small Commodities(index-independent)

Four

str

ateg

ies,

taki

ng th

eir b

earin

gs fr

om th

e D

ow J

ones

-UB

S C

omm

odity

Inde

x

The Sub-Fund gains exposure to these strategies by investing in financial derivative instruments linked to commodity futures indices or sub-indices.

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 16

Sources of Performance: Implementing the Investment PhilosophyAlpha Opportunity 1: Commodity Basis and Relative Strength Strategies

Strategy 1:

Basis (Long)

Strategy 2:

Relative Strength (Long)A

lpha

Opp

ortu

nity

1 Long only – Basis Monthly, rank the commodities in the DJ-UBS excluding Gold

and Silver in order of “backwardation“ or basis*

Go long in the 8 commodities with the highest basis, with the same relative weights as in the DJ-UBS (subject to constraints)

Take no position in the remaining commodities

Long only – Relative Strength

Monthly, rank the commodities in the DJ-UBS in order of momentum as measured by the previous 12 months return**

Go long the 9 commodities with the highest momentum, with the same relative weights as in the DJ-UBS (subject to constraints)

Take no position in the remaining commodities

Strategy 3:

Basis (Long/Short)

Strategy 4;

Relative Strength (Long/Short)

Strategy 5:Small Commodities(index-independent) * Basis is calculated for each commodity as (F1/F2-1)*365/(D2-D1),

where F1 is the nearest futures contract. D1 and D2 are the number of days until expiration of the respective contracts **Momentum is calculated for each commodity using the cumulative return for the immediately preceding 12 months.

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 17

Sources of Performance: Extending the Investment Philosophy Alpha Opportunity 2: Long/Short Strategies

Strategy 3:

Basis (Long/Short)

Strategy 4;

Relative Strength (Long/Short)A

lpha

Opp

ortu

nity

2

Long/Short – Basis Monthly, rank the commodities in the DJ-UBS excluding

Gold and Silver in order of “backwardation“ or basis*

Go long in the 8 commodities with the highest basis, with the same relative weights as in the DJ-UBS (subject to constraints)

Take a short position in the 8 Commodities with the lowest basis*

Long/Short – Relative Strength

Monthly, rank the commodities in the DJ-UBS in order of momentum as measured by the previous 12 months return**

Go long the 9 commodities with the highest momentum, with the same relative weights as in the DJ-UBS (subject to constraints)

Take a short position in the 9 commodities with the lowest momentum

Strategy 1:

Basis (Long only)

Strategy 2:

Relative Strength (Long only)

Strategy 5:Small Commodities(index-independent) *Basis is calculated for each commodity as (F1/F2-1)*365/(D2-D1),

where F1 is the nearest futures contract. D1 and D2 are the number of days until expiration of the respective contracts**Momentum is calculated for each commodity using the cumulative return for the immediately preceding 12 months.

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 18

Sources of Performance: Broadening the Investment UniverseAlpha Opportunity 3: Source of Return Outside the Traditional UniverseA

lpha

Opp

ortu

nity

3

Strategy 5:Small Commodities(index-independent)

Long only Strategy

12 commodities outside the DJ-UBS Index universe

Sector weights: Energy 30%, Metals 16% and Agriculture 54%

Using 2006 liquidity levels (open interests and turnover) to determine weightings

Single commodity weight capped at max.15%, min. 2%

Annual review and rebalancing

Commodities Weights Commodities WeightsCrude oil 15% Tin 2%Gas oil 15% Platinum 2%Soybean meal 15% Palladium 2%Kansas wheat 15% Range cattle 10%Minneapolis wheat 2% Cocoa 10%Lead 10% Orange juice 2%

Strategies for Small CommoditiesStrategy 1:

Basis (Long only)

Strategy 2:

Relative Strength (Long only)

Strategy 3:

Basis (Long/Short)

Strategy 4;

Relative Strength (Long/Short)

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 19

Commodity Market Update

Investment Philosophy

Strategy Profile

Active Allocation

Alpha Generation

Agenda

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 20

Strategy CompositionGood Historical Performance in all Strategies

Long-only Strategies and Small Commodities have shown a long-term outperformance and generally followed market development

Long/Short-Strategies have offered further Alpha and hedging in weak commodity markets

Back-testing of all different strategies* vs. Dow Jones-UBS Commodity Index

Source: Pioneer Investments, *DJ-UBS strategies 29 January 2010

100

300

500

700

900

1100

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

DJ UBSCI Total Return UBS BASIS Long Total ReturnUBS R&S Long Total Return UBS BASIS L&S Total ReturnUBS RS L&S Total Return Smaller Commodities Total Return

Perf

orm

ance

, reb

ased

to 1

00

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 21

Strategy CompositionAlpha Opportunity 4: Optimise Allocation in Line with Identified Scenarios

Strategy selection and implementation

– Identification of different scenariosusing historical data

– Optimisation across the scenariosbased on best risk/return profile

– Evaluation of current scenarioat monthly intervals

Position limits*

– No strategy has a weight of more than 50%

– Long/Short strategies limited to a combined weight of 30%

Position Limits*“Basis” Long 0%-50%

“Basis” Long/Short 0%-20%

“Relative Strength” Long 0%-50%

“Relative Strength” Long/Short 0%-20%

Small Commodities Long 5%-15%

The Portfolio always combines two or more strategies,depending on the market phase

Implementing the Investment Philosophy

*Note: these are internal guidelines and not prospectus limits and may be subject to change over time.

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 22

Identification of different market phases based on historical data of the last 15 years

Optimisation across the scenarios based on best risk/return profile

Evaluation of current scenario at monthly intervals

Strategy CompositionAlpha Opportunity 4: Optimise Allocation in Line with Identified Scenarios

Active allocation between different DJ-UBS strategies

Source: DJ-UBS, Pioneer Investments. Back-testing from December 1992 to December 2008. Back test return figures have been adjusted to take into account trading costs, management fees, slippage (difference between real and prices used in back test). In total back test return figures have been adjusted by 300 basis points. Simulated past performance is not a reliable indicator of future performance. Performance of Pioneer Funds – Commodity Alpha, Class A EUR ND units net of fees from March 2008 to December 2009. Returns have been converted to US dollar.

100

300

500

700

900

1100

1300

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

DJ UBSCI Total Return UBS BASIS Long Total Return UBS R&S Long Total Return

UBS BASIS L&S Total Return UBS RS L&S Total Return Smaller Commodities Total Return

Commodities A L P H A Total ReturnPioneer Funds – Commodity Alpha

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 23

Commodity Market Update

Investment Philosophy

Strategy Profile

Active Allocation

Alpha Generation

Agenda

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 24

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

1 year 3 years ann. 5 years ann. since 1992 ann.

Pioneer Funds – Commodity Alpha DJ-UBS TR Relative performance

Alpha GenerationStrong Outperformance PotentialObjective: Outperforming the DJ-UBS Commodity Index in different periods(figures include back-testing)

Source: DJ-UBS, Pioneer Investments as at 31 January 2010. Back test returns adjusted to trading costs, administrative fees and Slippage (Difference between real prices and prices used in back test). The back test return quote has been adapted overall to 300 bps. Simulated past performance is not a reliable indicator of future performance.

Performance of Pioneer Funds – Commodity Alpha, Class A EUR ND net of fees from March 2008 to January 2010. Returns have been converted to USD.

Characteristics

Tracking error 9.03%

Volatility 13.92%

Volatility Benchmark 15.19%

Correlation 0.81

Dec 1992 – Jan 2010Portfolio

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 25

Alpha GenerationStrong Outperformance PotentialCumulative Monthly ReturnPerformance in USD: Pioneer Funds – Commodity Alpha

45

55

65

75

85

95

105

Feb08

Mar08

Apr08

May08

Jun08

Jul08

Aug08

Sep08

Oct08

Nov08

Dec08

Jan09

Feb09

Mar09

Apr09

May09

Jun09

Jul09

Aug09

Sep09

Oct09

Nov09

Dec09

Jan10

Feb10

Ret

urns

reba

sed

to 1

00

-1%

4%

9%

14%

19%

24%

29%

34%

Exce

ss R

etur

ns in

%

Excess returns Pioneer Funds – Commodity Alpha DJ-UBS TR Index

Source: Pioneer Investments, DJ-UBS, Bloomberg (as at 25 February 2010). Performance data provided refers to Class A (USD) units only net of fees. Returns of DJ-UBS and DJ-UBS TR Index on basis of USD. The benchmark performance is adjusted to the previous day for the fund pricing adjustment. Before the fund inception

date of class A in USD on 3 April 2008, the performance of Pioneer Funds – Commodity Alpha, Class A EUR ND net of fees have been converted to USD

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 26

Source: Pioneer Investments, as at 25 Febuary 2010

Alpha Generation: Portfolio PerformanceCurrent Weights of Sub-Sectors

32.5%

22.1%18.8%

7.5%3.1%

6.4%

19.4%

0.5%

10.9%

-1.2% -0.8%

19.4%

12.4%

42.8%

7.9% 8.4%

-10%

0%

10%

20%

30%

40%

50%

Energy Petroleum Base Metals Precious Metals Grains Softs Vegetable Oil Live Stock

DJ-UBS Pioneer Funds – Commodity Alpha

Highest overweighting Highest underweightingCOPPER 9.13% CRUDE OIL -18.58%ALUMINIUM 6.65% NATURAL GAS -10.85%GOLD 4.01% CORN -9.36%SUGAR 3.38% SOYBEANS -7.61%NICKEL 3.29% WHEAT -6.21%

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 27

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Feb. 08 May. 08 Aug. 08 Nov. 08 Feb. 09 May. 09 Aug. 09 Nov. 09 Feb. 10

Energy Metals Agriculture

Active Allocation Offers Flexibility and OpportunitiesSector Weightings are Adjusted According to Trends

Fund inception date: 21 February 2008. Source: Pioneer Investments, in-house calculations (based on the following basic assumptions: target weightings for each strategy are assumed to remain unchanged throughout the entire month; transaction costs are not taken into account; figures are calculated on a same-day basis; NAV calculations for the portfolio are preformed with a one-day time delay (T-1), so performance may deviate; liquidity resulting from sizeable inflows and outflows changes the Portfolio's real performance;back-testing figures have been reduced by 25 bps per month in order to obtain a more realistic picture of expected results). As at 25 February 2010.

Weightings follow wave patterns. Trends are pursued.

March 2009Energy 5%

Metals 19%

Agriculture 53%

December 2009Energy 8%

Metals 57%

Agriculture 35%

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 28

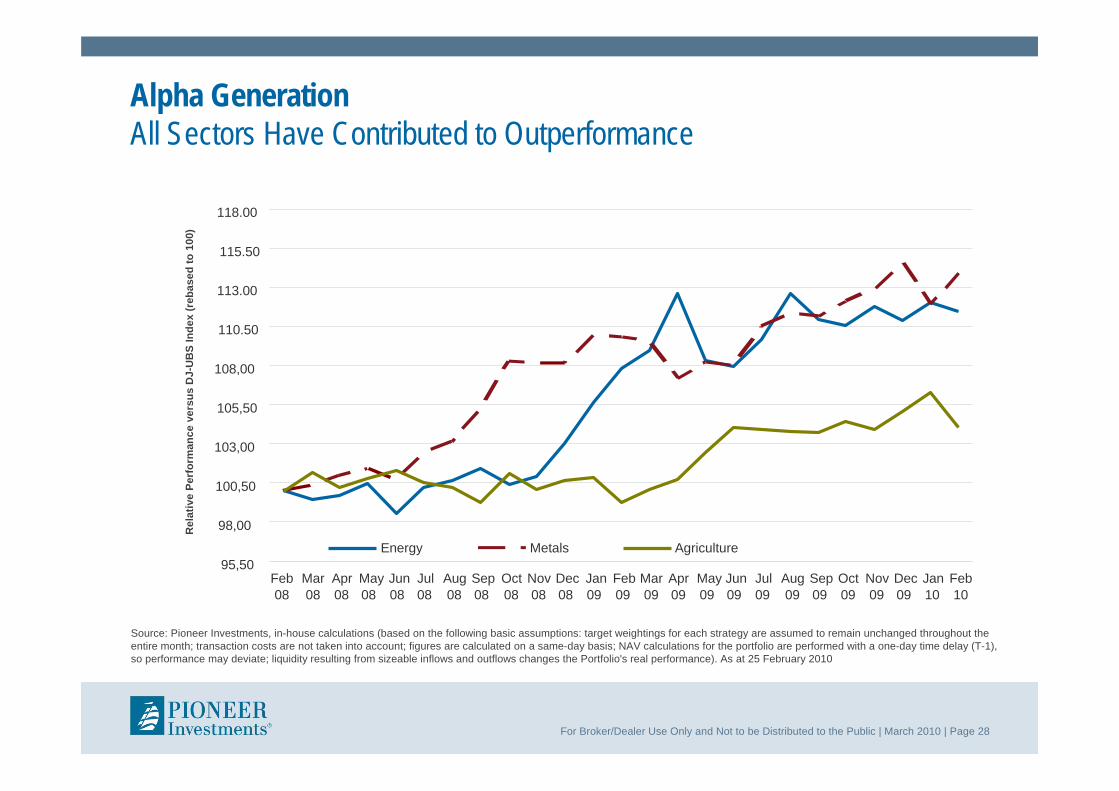

Alpha GenerationAll Sectors Have Contributed to Outperformance

Rel

ativ

e Pe

rfor

man

ce v

ersu

s D

J-U

BS

Inde

x (r

ebas

ed to

100

)

95,50

98,00

100,50

103,00

105,50

108,00

110.50

113.00

115.50

118.00

Feb08

Mar08

Apr08

May08

Jun08

Jul08

Aug08

Sep08

Oct08

Nov08

Dec08

Jan09

Feb09

Mar09

Apr09

May09

Jun09

Jul09

Aug09

Sep09

Oct09

Nov09

Dec09

Jan10

Feb10

Energy Metals Agriculture

Source: Pioneer Investments, in-house calculations (based on the following basic assumptions: target weightings for each strategy are assumed to remain unchanged throughout the entire month; transaction costs are not taken into account; figures are calculated on a same-day basis; NAV calculations for the portfolio are performed with a one-day time delay (T-1), so performance may deviate; liquidity resulting from sizeable inflows and outflows changes the Portfolio's real performance). As at 25 February 2010

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 29

Important InformationUnless otherwise stated all information contained in this document is from Pioneer Investments and is as at 23 February 2010.

Pioneer Funds – Commodity Alpha is a sub-fund (the “Sub-Fund”) of Pioneer Funds (the “Fund”), a fonds commun de placement with several separate sub-funds established under the laws of the Grand Duchy of Luxembourg.

Past performance does not guarantee and is not indicative of future results. Unless otherwise stated, all views expressed are those of Pioneer Investments. These views are subject to change at any time based on market and other conditions and there can be no assurances that countries, markets or sectors will perform as expected. Investments involve certain risks, including political and currency risks. Investment return and principal value may go down as well as up and could result in the loss of all capital invested. More recent returns may be different than those shown. Please contact your local sales representative for more current performance results.

This material is not a prospectus and does not constitute an offer to buy or a solicitation to sell any units of the Fund or any services, by or to anyone in any jurisdiction in which such offer or solicitation would be unlawful or in which the person making such offer or solicitation is not qualified to do so or to anyone to whom it is unlawful to make such offer or solicitation. For additional information on the Fund, a free prospectus should be requested from Pioneer Global Investments Limited (“PGIL”), 1 George’s Quay Plaza, George’s Quay, Dublin 2, Ireland. Call +353 1 480 2000 Fax +353 1 449 5000. This information is not for distribution and does not constitute an offer to sell or the solicitation of any offer to buy any securities or services in the United States or in any of its territories or possessions subject to its jurisdiction to or for the benefit of any United States person (being residents and citizens of the United States or partnerships or corporations organized under United States laws). The Fund has not been registered in the United States under the Investment Company Act of 1940 and units of the Fund are not registered in the United States under the Securities Act of 1933.

This document is not intended for and no reliance can be placed on this document by retail clients, to whom the document should not be provided. The content of this document is approved by PGIL. In the UK, it is directed at professional clients and not at retail clients and it is approved for distribution by Pioneer Global Investments Limited (London Branch), 123 Buckingham Palace Road, London SW1W 9SL, authorised by the Financial Regulator in Ireland and regulated by the Financial Services Authority for the conduct of UK business. The Fund is an unregulated collective investment scheme under the UK Financial Services and Markets Act 2000 and therefore does not carry the protection provided by the UK regulatory system.

Pioneer Funds Distributor, Inc., 60 State Street, Boston, MA 02109 (“PFD”), a U.S.-registered broker-dealer, provides marketing services in connection with the distribution of Pioneer Investments’ products. PFD markets these products to financial intermediaries, both within and outside of the U.S. (in jurisdictions where permitted to do so) for sale to clients who are not United States persons.

“UBS®”, [“UBS Commodity Basis P Strategy”], [“UBS Commodity Relative Strength P Strategy”], [“UBS Commodity Small Caps P Strategy”], [“UBS Commodity Long-Short Basis P Strategy”], [“UBS Commodity Long-Short Relative Strength P Strategy”], [“UBSIBAPE”], [“UBSIRSPE”], [“UBSISCIE”], [“UBSIBLPE”] and [“UBSIRLPE”] are trademarks or service marks of UBS Securities LLC (“UBS”), and have been licensed for use for certain purposes by Pioneer Asset Management S.A. Luxemburg. Pioneer Asset Management S.A.’s “Pioneer Funds – Commodity Alpha”, based on the [“UBS Commodity Basis P Strategy”], [“UBS Commodity Relative Strength P Strategy”], [“UBS Commodity Small Caps P Strategy”], [“UBS Commodity Long-Short Basis P Strategy”] and [“UBS Commodity Long-Short Relative Strength P Strategy”], are not sponsored, endorsed, sold or promoted by UBS Securities LLC, UBS AG or any of their respective subsidiaries or affiliates, and none of UBS, UBS AG or any of their respective subsidiaries or affiliates, makes any representation regarding the advisability of investing in such products.

Pioneer Investments is a trading name of the Pioneer Global Asset Management S.p.A. group of companies. Date of First Use 11 March 2010

Pioneer Funds – Commodity Alpha

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 30

Conclusion II

Positioning:

– High breakeven spreads in the short end of the curve, but higherimplied default rate protection in the medium-long end of the curve

– Overweight issuers with stable cash flow characteristics and little probability of downgrade to sub-IG

– Underweight deeply subordinated bank debt from issuers with highstate involvement or risk of nationalisation

The key risks to our strategy are:

– Early and accelerated exit from expansive monetary policy

– Increased risk aversion through unexpected sovereign defaults, systemically important bank failures and related spill-over

– Double dip of economic growth in Europe

For Broker/Dealer Use Only and Not to be Distributed to the Public | March 2010 | Page 31

Important Information

Unless otherwise stated all information contained in this document is from Pioneer Investments and is as at 29 January 2010Past performance does not guarantee and is not indicative of future results. Unless otherwise stated, all views expressed are those of Pioneer Investments. These views are subject to change at any time based on market and other conditions and there can be no assurances that countries, markets or sectors will perform as expected. Investments involve certain risks, including political and currency risks. Investment return and principal value may go down as well as up and could result in the loss of all capital invested. More recent returns may be different than those shown. Please contact your local sales representative for more current performance results.This material is not a prospectus and does not constitute an offer to buy or a solicitation to sell any units of the Pioneer Invesetments range of mutual funds or any services, by or to anyone in any jurisdiction in which such offer or solicitation would be unlawful or in which the person making such offer or solicitation is not qualified to do so or to anyone to whom it is unlawful to make such offer or solicitation. For additional information on the Fund, a free prospectus should be requested from Pioneer Global Investments Limited (“PGIL”), 1 George’s Quay Plaza, George’s Quay, Dublin 2, Ireland. Call +353 1 480 2000 Fax +353 1 449 5000. This information is not for distribution and does not constitute an offer to sell or the solicitation of any offer to buy any securities or services in the United States or in any of its territories or possessions subject to its jurisdiction to or for the benefit of any United States person (being residents and citizens of the United States or partnerships or corporations organized under United States laws). The non-US Pioneer Investments mutual funds have not been registered in the United States under the Investment Company Act of 1940 and units of these funds are not registered in the United States under the Securities Act of 1933.This document is not intended for and no reliance can be placed on this document by retail clients, to whom the document should not be provided.The content of this document is approved by PGIL. In the UK, it is directed at professional clients and not at retail clients and it is approved for distribution by Pioneer Global Investments Limited (London Branch), 123 Buckingham Palace Road, London SW1W 9SL, authorised by the Financial Regulator in Ireland and regulated by the Financial Services Authority for the conduct of UK business. The Pioneer Investments funds are unregulated collective investment scheme under the UK Financial Services and Markets Act 2000 and therefore do not carry the protection provided by the UK regulatory system.Pioneer Funds Distributor, Inc., 60 State Street, Boston, MA 02109 (“PFD”), a U.S.-registered broker-dealer, provides marketing services in connection with the distribution of Pioneer Investments’ products. PFD markets these products to financial intermediaries, both within and outside of the U.S. (in jurisdictions where permitted to do so) for sale to clients who are not United States persons.Pioneer Investments is a trading name of the Pioneer Global Asset Management S.p.A. group of companies.For Broker/Dealer use only and not for distribution to the publicDate of First Use: 10 March 2010