commercial vehicle group, inc. 2011 annual meeting · daimler trucks north america (“dtna”) –...

TRANSCRIPT

Commercial Vehicle Group, Inc.

2011 Annual Meeting

This presentation contains forward-looking statements that are subject to risks and uncertainties. These statements

often include words such as “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” or similar expressions. In

particular, this presentation contains forward-looking statements about Company estimates for future periods with

respect to cost savings, restructuring charges, revenues or other financial information. These statements are based

on certain assumptions that the Company has made in light of its experience in the industry as well as its perspective

on historical trends, current conditions, expected future developments and other factors it believes are appropriate

under the circumstances. Actual results may differ materially from the anticipated results because of certain risks

and uncertainties, including but not limited to: (i) general economic or business conditions affecting the markets in

which the Company serves; (ii) the Company's ability to develop or successfully introduce new products; (iii) risks

associated with conducting business in foreign countries and currencies; (iv) increased competition in the heavy-duty

truck market and other key end markets; (v) our failure to complete or successfully integrate additional strategic

acquisitions; (vi) the impact of changes in governmental regulations on the Company's customers or on its business;

(vii) the loss of business from a major customer or the discontinuation of particular commercial vehicle platforms;

(viii) the Company’s ability to obtain future financing due to changes in the lending markets or its financial position;

(ix) our ability to comply with the financial covenants in our revolving credit facility; and (x) various other risks as

outlined in CVG’s SEC filings. There can be no assurance that statements made in this presentation relating to future

events will be achieved. CVG undertakes no obligation to update or revise forward-looking statements to reflect

changed assumptions, the occurrence of unanticipated events or changes to future operating results over time. All

subsequent written and oral forward-looking statements attributable to CVG or persons acting on behalf of CVG are

expressly qualified in their entirety by such cautionary statements.

For a complete description of risks, please refer to our 2010 Annual Report on Form 10-K and current SEC reports on

file. 2

Forward-Looking Statement

3

Good Afternoon and Welcome to the

Commercial Vehicle Group, Inc.

2011 Annual Meeting of Stockholders

Welcome

The Year in Review / Moving Ahead

Managing for the Future

Financial Review

Closing

Questions

4

Agenda

Over the past year, and in preparation for continued growth and

success, we focused on:

Continuing to diversify our products, end markets and customers

Improving our capital structure

− $25 million equity offering in Q1 2010

− $250 million bond offering in April 2011

Investing in global expansion

− Saltillo, Mexico

− Beijing, China

Realigning our manufacturing footprint through facility consolidations

Achieving new business awards

Capitalizing on our variable cost structure and improving our bottom line

Strategic acquisitions and new market opportunities

− Bostrom Seating

− Exploring India Opportunities

− Exploring Brazil Opportunities

The Year in Review

CVG continued to be a diversified global leader, with a balanced

product, market and customer portfolio:

The Year in Review

2010

CVG has a well positioned capital structure for the future:

First Quarter 2010: public offering of common stock

− 4.37 million shares

− Priced at $6.25 per share

− CVG received approximately $25.4 million of net proceeds from

the offering

$21.4 million cash tax refund during the second quarter of 2010

$250 million bond offering in April 2011 at 7.875% (due in 2019)

Stock Offering + Tax Refund + Revolver Capacity + Bond Offering

= Strong Balance Sheet / Liquidity

Year in Review and Moving Ahead

Moving Ahead - Global Expansion – Saltillo, Mexico

Moving Ahead - Global Expansion – Beijing, China

Daimler Trucks North America

(“DTNA”) – Seats, Flooring, Interior

Components

Beiqi Foton Motor Co

Truck Seats ($30m sales at full

production)

XCMG

Seat Supplier ($4-6m sales)

John Deere

Wire Harnesses for Excavators

Manufactured in China ($4-4.5m

sales)

Hino

Seat Supplier for Medium-duty Trucks

Manufactured in North America ($2-

3m sales)

Skoda Auto

Wire Harnesses ($14-17m sales)

Moving Ahead - New Business Success

Strong Pipeline of New Business Achievements

Managing for the Future - Continuous Improvement and Growth

Moving forward, our focus will remain on:

Capitalizing on Strong End Market Recovery and Growth – Truck/Construction

Geographic Diversification – organic & acquisition

– Mexico Opportunities

– China Opportunities

– India Opportunities

– Brazil Opportunities

– U.S. Opportunities

End Market Diversification - organic & acquisition

Investment in Technology

12

Indicators Support Ongoing Recovery Significant Opportunity For Global Growth

Early stages of penetration into large Asian

commercial vehicle market

Growth opportunities in Asia with strong

production volumes

Continued growth in China

Opportunity in other emerging markets (India,

Russia, South America, etc.)

New business wins with new and existing

customers

Managing for the Future – End Market Growth Opportunity

ROW

12%

NA

12%

Europe

15%

Asia

61%

Managing for the Future - End Market Growth Opportunity

13

2009 2010 2011 2012 2013 2014 2015

North America Europe Asia South America

837 860

937

1,038

1,144

1,247

1,326

Medium / Heavy Duty Equipment Sales

(Represents cranes & movers and earthmoving equipment in thousands of units)

’09-’15

CAGR

12.3%

8.4%

6.6%

6.6%

8.0%

CVG Construction End Market Sales

Heavy truck

40%

Construction

23%

Aftermarket

14%

Military

9%

Other

10%

Agriculture 1%

Bus 3%

Favorable End Market Trends

Improving tone in key U.S. and European construction

markets supported by strong order rates

Exceptional growth in emerging markets, particularly

China, Brazil, Middle East and India

Significant equipment requirements to improve / replace

aging infrastructure globally

Broader equipment usage / recovery across end markets

(e.g., industrial, oil and gas, power and mining) Source: Millmark Associates (January 2011)

Note: Revenue breakdown based on 2010 results.

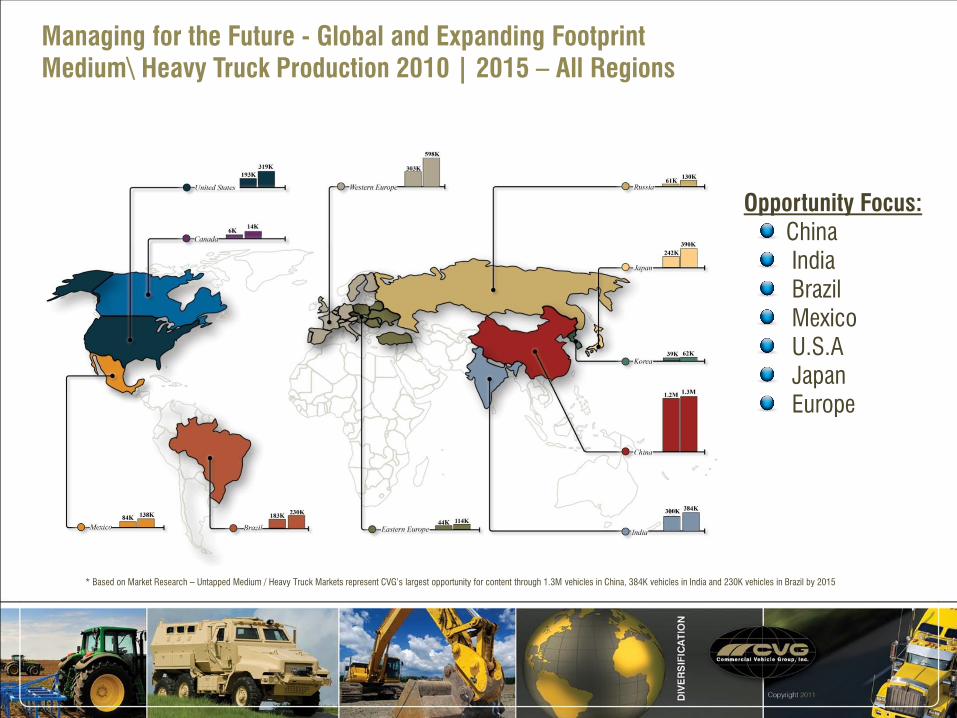

Managing for the Future - Global and Expanding Footprint

Medium\ Heavy Truck Production 2010 | 2015 – All Regions

Opportunity Focus:

China

India

Brazil

Mexico

U.S.A

Japan

Europe

* Based on Market Research – Untapped Medium / Heavy Truck Markets represent CVG’s largest opportunity for content through 1.3M vehicles in China, 384K vehicles in India and 230K vehicles in Brazil by 2015

Managing for the Future - Global and Expanding Footprint

Medium\ Heavy Construction Production 2010 | 2014 – All Regions

Opportunity Focus:

China

India

Brazil

U.S.A

Japan

Europe

* Based on Market Research – Construction market growth from 2010 to 2014 shows China and India as CVG’s largest opportunity to increase content along with continued focus on North American increased content and Western Europe and Japan

Opportunity Focus:

China

India

Brazil

U.S.A

Japan

Europe

* Based on Market Research – Agriculture market growth from 2010 to 2014 represent CVG’s largest opportunity for content through 762K vehicles in China and 640K vehicles in India, along with continued focus on

increasing North American content and growth in Brazil, Europe and Japan

Managing for the Future - Global and Expanding Footprint

Agriculture Equipment Production 2010 | 2014 - All Regions

Managing for the Future - Becoming A Technology Leader

17

Global Engineering Support

Acoustics and Thermal Systems Development

Material and Process Development

Advanced Testing Services

Dedicated 37,500 sq.ft. facility

Design and Visualization Studio

Three Secure Customer Project Bays

Concept Development and Realization

Physical and Rapid Prototyping

Benchmarking and Reverse

Engineering

Innovative, Industry Leading Products

Arm Rest

Extended Position

Advanced Seating

Innovative Design and R&D Capabilities

Financial Overview

Historical Financial Overview

Financial Review

20

Global industry recession continued to

challenged the business through 2009 with

signs of recovery in 2010 and in early 2011

Continued improvement in financial results on

a sequential quarter-over-quarter basis – last

eight quarters

Continue to drive culture of entrepreneurship,

innovation and employee engagement to

improve our bottom line

Focus on strategic efforts during downturn:

− Diversification

− Profit improvement goals across organization

Actions during 2009 and 2010 demonstrate

significant progress towards CVG’s long-term

financial goals

Financial Review - Strong Liquidity and Maturity Profile

21

Strong Balance Sheet & Liquidity

Q1 2010 Equity Offering

Q2 2010 Tax Refund

April 2011 $250 million bond offering:

− Reduced overall cost of debt to 7.875%

− Simplified capital structure

− Maintains modest leverage level, positioned to improve with cycle rebound

− 3/31/2011 Pro forma available liquidity of approximately $130 million

• Amended and upsized ABL to $40M with no availability block

− Significantly extends maturity profile

Positioned well to capitalize on growth plans and strategic initiatives

Acquisition of

Bostrom Seating

Saltillo, Mexico

expansion

Beijing, China

expansion

22

Pursue additional new business and “conquest” business wins

− Continue to monitor competitors operating in a distressed state for additional opportunities

− Invest in new processes or capabilities

Pursue strategic, add-on acquisitions to augment strategic initiatives

− Capitalize on track record integration and performance

Sale of Monona Medical Harness

Acquisition of CIEB

Groundbreaking of CVG Corporate Headquarters

Acquisition of National

Seating

Acquisition of Sprague

Device (Prutsman /

Motomirror)

Acquisition of KAB Seating

Acquisition of

R-Squared

Acquisition of Tempress,

Inc.

CVG Initial Public

Offering

Opening of CVG

Shanghai

Acquisition of Short Bark

Industries

Acquisition of Gage

Acquisition of PEKM

Acquisition of ASC, Inc.

Acquisition of Landmark Industries

Formation of Trim Systems

Acquisition of

Mayflower

Acquisition of Monona

Acquisition of Cabarrus

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Financial Review

Track Record of Disciplined, Successful Investment & Growth Strategy

Appendix

23

Historical Non-GAAP Measures

Adjusted EBITDA and Adjusted Operating Income

24

Non-GAAP Measures

Reconciliation to Adjusted Operating Income

2005 2006 2007 2008 2009 2010 3/31/09 6/30/09 9/30/09 12/31/09 3/31/10 6/30/10 9/30/10 12/31/10 3/31/11

Operating Income 89.5$ 97.5$ 18.8$ (191.4)$ (89.7)$ 16.7$ (18.4)$ (22.2)$ (7.8)$ (41.2)$ 3.6$ 2.6$ 5.1$ 5.4$ 8.1$

Long-lived asset impairment - - - - 17.3 - - 3.4 - 13.8 - - - - -

Goodwill and intangible asset impairment - - - 207.5 30.1 - - 7.0 - 23.1 - - - - -

Restructuring Charges - - 1.4 - 3.7 1.7 1.7 0.2 - 1.7 - 1.4 0.2 0.2 0.3

Adjusted Operating Income 89.5$ 97.5$ 20.3$ 16.1$ (38.6)$ 18.4$ (16.7)$ (11.6)$ (7.8)$ (2.6)$ 3.6$ 4.0$ 5.3$ 5.5$ 8.4$

Source: Company filings

Fiscal Year Ending December 31 Fiscal Quarter Ending