combined financial statements and other financial ... · loss of approximately $583,041 in our...

TRANSCRIPT

1

Dear Brothers and Sisters of the Diocese of Providence:

The past 16 months have been extremely difficult financial times for many of us and for the Diocese of Providence as well. With local unemployment above 12% for much of the past year and many of our cities and towns struggling to pay their bills, our state and nation have not seen times like these since the Great Depression. Yet with all of these financial struggles, we are called by our faith to bring the message of Christ to all. We do this in word as well as action whenever we try to meet the needs of our neighbors. God challenges us to be people of faith and hope trusting always in the providence of God.

At the end of the year it has been our practice to provide our diocesan community with the results of the annual audited financial report for the previous fiscal year. The timing of this publication coincides with the end of the calendar year and the beginning of this new decade that we hope will be one of promise.

Accordingly, I am pleased to present to you on the diocesan website (www.dioceseofprovidence.org) the completed Combined Financial Statements and other financial information for the Central Administration Funds and Diocesan Cemetery Operations within the Diocese of Providence for the fiscal year ended June 30, 2009 and 2008. As in the past, it has been prepared by Tofias P.C., whose shareholders became shareholders of the firm Mayer Hoffman McCann P.C. during this past fiscal year.

The report has been reviewed and approved by the Diocesan Audit Committee, a subcommittee of the Diocesan Finance Council, and accepted by the Diocesan Finance Council in accordance with the stated requirements of both Church law and responsible stewardship practices. It follows a national standard of accounting and reporting format. If you would like a printed copy of the report, please call Rev. Msgr. Raymond B. Bastia, Vicar for Planning and Financial Services or Michael F. Sabatino, CFO, at 278-4540. It will also be available in an easy-to-read format that will soon be published in the Rhode Island Catholic.

As you review this report, you will note that we had an overall decrease in net operations of ($22,154,386). This was mainly attributed to Realized Losses on Investments of ($9,245,709) and Unrealized Losses of ($9,375,133). The realized losses were attributed to a realignment of investments by the Diocesan Investment Advisory Committee to better reflect the changes in the investment market of the past two years. It was felt that these changes, although painful in the short term will bear much fruit in the foreseeable future. In addition, some investments were sold in order to generate cash flow to maintain and operate the many ministries of the Diocese.

We are happy to report the positive news that in the first quarter of Fiscal Year 2010 we have realized a 10.4% gain on our investment portfolio, gaining back some portion of the unrealized losses suffered last year. In another area we did realize a loss of approximately $583,041 in our Diocesan Insurance Fund as we incurred greater insurable losses than in past years and some parishes have struggled to keep current with their quarterly premiums.

Also on the positive side, the annual Catholic Charity Fund Appeal met its goal of $7.8 million thanks to the wonderful efforts of our pastors, volunteers and contributors who are so loyal to this diocesan appeal. I am particularly grateful for the work of the Diocesan Finance Council whose guidance and expertise continue to provide our diocese with direction for a responsible financial future, and to all the Diocesan committees who serve so selflessly to strengthen our Church.

If you have any questions about the report, please do not hesitate to contact Michael F. Sabatino, CFO at his email address: [email protected]. I again would like to extend my gratitude to the diocesan staff and to our clergy and faithful for their generosity and support. As we look ahead to the challenges of the future, I am confident that the Lord will continue to guide us through them. May the Lord bless us and continue to help us to be financial stewards of the church.

Sincerely yours,

Thomas J. TobinBishop of Providence

Combined Financial Statements and

Other Financial Information

Central Administration Funds and

Diocesan Cemetery Operations within the

Diocese of Providence

June 30, 2009 and 2008

DIOCESAN FINANCE COUNCIL MEMBERS

Most Rev. Thomas J. Tobin, D.D.Rev. Msgr. Raymond B. BastiaMr. Glenn CreamerThe Honorable Laureen A. D’AmbraMr. Almon HallVery Rev. William P. Marquis, OPRev. Robert P. PerronMrs. Virginia Roberts

Mrs. Margaret RuggieriSr. Dorothy Schwarz, SSDRev. Msgr. Richard D. SheahanMrs. Patricia SmolleyRev. Msgr. Paul D. TherouxMr. William K. WrayMr. Anthony T. Gwiazdowski (Staff)Mr. Michael F. Sabatino (Staff)

2

statements are free of material misstatement. An audit includes exam-

ining, on a test basis, evidence supporting the amounts and disclo-

sures in the financial statements. An audit also includes assessing the

accounting principles used and significant estimates made by manage-

ment, as well as evaluating the overall financial statement presentation.

We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements referred to above present fairly,

in all material respects, the combined financial position of the Central

Administration Funds and Diocesan Cemetery Operations within the

Diocese of Providence as of June 30, 2009 and the combined changes

in their net assets and their cash flows for the year then ended in con-

formity with U.S. generally accepted accounting principles.

January 6, 2010

Providence, Rhode Island

Independent Auditors’ Report

The Most Reverend Thomas J. Tobin

Bishop of Providence

We have audited the accompanying combined statement of financial

position of the Central Administration Funds and Diocesan Cemetery

Operations within the Diocese of Providence (the “Diocese”) as of

June 30, 2009 and the related combined statements of activities and

changes in net assets and cash flows for the year then ended. These

financial statements are the responsibility of Diocesan management.

Our responsibility is to express an opinion on these financial state-

ments based on our audit. The combined financial statements of the

Central Administration Funds and Diocesan Cemetary Operations

within the Diocese of Providence as of June 30, 2008 were audited by

other auditors, Tofias PC, whose shareholders became shareholders of

Mayer Hoffman McCann P.C. as of December 31, 2008, and whose

report dated November 21, 2008, expressed an unqualified opinion

on those combined statements.

We conducted our audit in accordance with U.S. generally accepted

auditing standards. Those standards require that we plan and perform

the audit to obtain reasonable assurance about whether the financial

June 30,

2009 2008

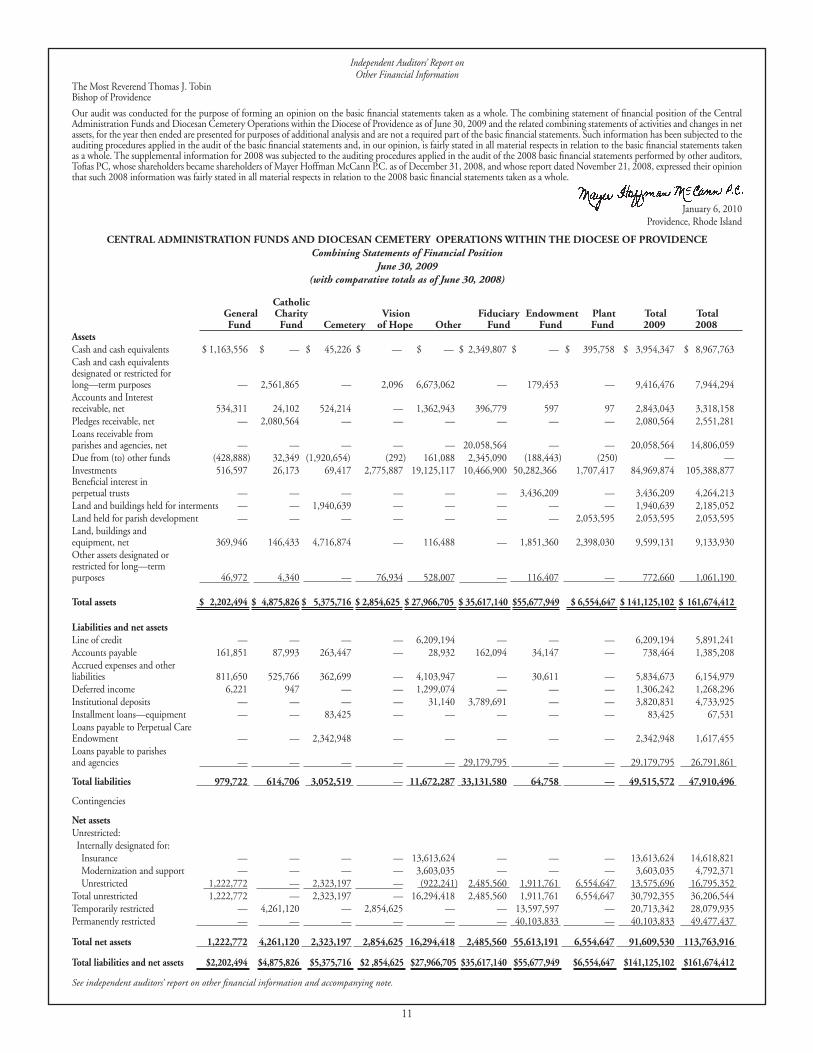

AssetsCash and cash equivalents $ 3,954,347 $ 8,967,763 Cash and cash equivalents designated or restricted for long-term purposes 9,416,476 7,944,294 Accounts and interest receivable, net of allowances of $2,657,176 and and $1,922,355 at 2009 and 2008 2,843,043 3,318,158 Pledges receivable, net of allowances of $411,602 and $468,740 at 2009 and 2008 2,080,564 2,551,281 Loans receivable from parishes and agencies, net of allowances of $1,600,000 and$1,100,000 at 2009 and 2008 20,058,564 14,806,059 Investments 84,969,874 105,388,877 Beneficial interest in perpetual trusts 3,436,209 4,264,213 Land and buildings held for interments 1,940,639 2,185,052 Land held for parish development 2,053,595 2,053,595 Land, buildings and equipment, net 9,599,131 9,133,930 Other assets designated or restricted for long-term purposes 772,660 1,061,190

Total assets $141,125,102 $ 161,674,412

CENTRAL ADMINISTRATION FUNDS AND DIOCESAN CEMETERY OPERATIONS WITHIN THE DIOCESE OF PROVIDENCE

Combined Statements of Financial Position

Liabilities and net assets Line of credit $ 6,209,194 $ 5,891,241 Accounts payable 738,464 1,385,208 Accrued expenses and other liabilities 5,834,673 6,154,979 Deferred income 1,306,242 1,268,296 Institutional deposits 3,820,831 4,733,925 Installment loans - equipment 83,425 67,531 Loans payable to perpetual care endowment 2,342,948 1,617,455 Loans payable to parishes and agencies 29,179,795 26,791,861

Total liabilities 49,515,572 47,910,496

Contingencies (Note 14)

Net assets Unrestricted: Internally designated for: Insurance 13,613,624 14,618,821 Modernization and support 3,603,035 4,792,371 Unrestricted 13,575,696 16,795,352 Total unrestricted 30,792,355 36,206,544 Temporarily restricted 20,713,342 28,079,935 Permanently restricted 40,103,833 49,477,437 Total net assets 91,609,530 113,763,916

Total liabilities and net assets $141,125,102 $161,674,412

June 30, 2009 2008

See accompanying notes to the financial statements.

3

CENTRAL ADMINISTRATION FUNDS AND DIOCESAN CEMETERY OPERATIONS WITHIN THE DIOCESE OF PROVIDENCE

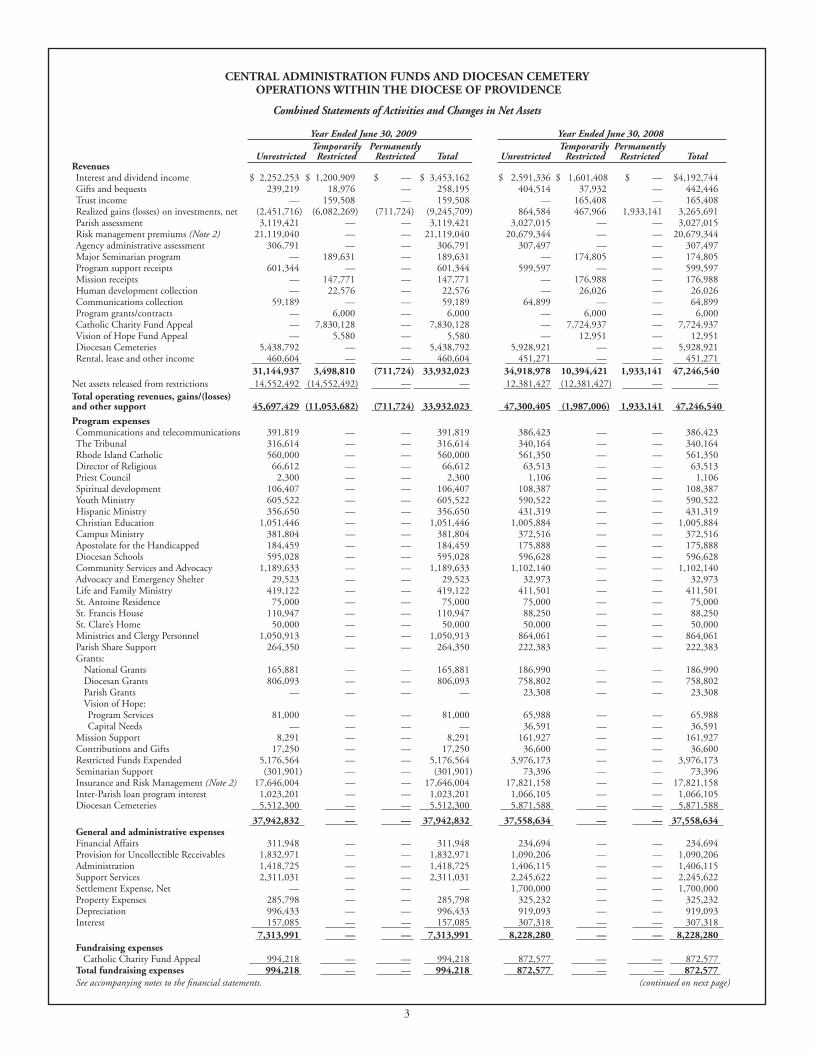

Combined Statements of Activities and Changes in Net Assets

Year Ended June 30, 2009 Year Ended June 30, 2008

Temporarily Permanently Temporarily Permanently Unrestricted Restricted Restricted Total Unrestricted Restricted Restricted TotalRevenues Interest and dividend income $ 2,252,253 $ 1,200,909 $ — $ 3,453,162 $ 2,591,336 $ 1,601,408 $ — $4,192,744 Gifts and bequests 239,219 18,976 — 258,195 404,514 37,932 — 442,446 Trust income — 159,508 — 159,508 — 165,408 — 165,408 Realized gains (losses) on investments, net (2,451,716) (6,082,269) (711,724) (9,245,709) 864,584 467,966 1,933,141 3,265,691 Parish assessment 3,119,421 — — 3,119,421 3,027,015 — — 3,027,015 Risk management premiums (Note 2) 21,119,040 — — 21,119,040 20,679,344 — — 20,679,344 Agency administrative assessment 306,791 — — 306,791 307,497 — — 307,497 Major Seminarian program — 189,631 — 189,631 — 174,805 — 174,805 Program support receipts 601,344 — — 601,344 599,597 — — 599,597 Mission receipts — 147,771 — 147,771 — 176,988 — 176,988 Human development collection — 22,576 — 22,576 — 26,026 — 26,026 Communications collection 59,189 — — 59,189 64,899 — — 64,899 Program grants/contracts — 6,000 — 6,000 — 6,000 — 6,000 Catholic Charity Fund Appeal — 7,830,128 — 7,830,128 — 7,724,937 — 7,724,937 Vision of Hope Fund Appeal — 5,580 — 5,580 — 12,951 — 12,951 Diocesan Cemeteries 5,438,792 — — 5,438,792 5,928,921 — — 5,928,921 Rental, lease and other income 460,604 — — 460,604 451,271 — — 451,271

31,144,937 3,498,810 (711,724) 33,932,023 34,918,978 10,394,421 1,933,141 47,246,540

Net assets released from restrictions 14,552,492 (14,552,492) — — 12,381,427 (12,381,427) — —

Total operating revenues, gains/(losses) and other support 45,697,429 (11,053,682) (711,724) 33,932,023 47,300,405 (1,987,006) 1,933,141 47,246,540

Program expenses Communications and telecommunications 391,819 — — 391,819 386,423 — — 386,423 The Tribunal 316,614 — — 316,614 340,164 — — 340,164 Rhode Island Catholic 560,000 — — 560,000 561,350 — — 561,350 Director of Religious 66,612 — — 66,612 63,513 — — 63,513 Priest Council 2,300 — — 2,300 1,106 — — 1,106 Spiritual development 106,407 — — 106,407 108,387 — — 108,387 Youth Ministry 605,522 — — 605,522 590,522 — — 590,522 Hispanic Ministry 356,650 — — 356,650 431,319 — — 431,319 Christian Education 1,051,446 — — 1,051,446 1,005,884 — — 1,005,884 Campus Ministry 381,804 — — 381,804 372,516 — — 372,516 Apostolate for the Handicapped 184,459 — — 184,459 175,888 — — 175,888 Diocesan Schools 595,028 — — 595,028 596,628 — — 596,628 Community Services and Advocacy 1,189,633 — — 1,189,633 1,102,140 — — 1,102,140 Advocacy and Emergency Shelter 29,523 — — 29,523 32,973 — — 32,973 Life and Family Ministry 419,122 — — 419,122 411,501 — — 411,501 St. Antoine Residence 75,000 — — 75,000 75,000 — — 75,000 St. Francis House 110,947 — — 110,947 88,250 — — 88,250 St. Clare’s Home 50,000 — — 50,000 50,000 — — 50,000 Ministries and Clergy Personnel 1,050,913 — — 1,050,913 864,061 — — 864,061 Parish Share Support 264,350 — — 264,350 222,383 — — 222,383 Grants: National Grants 165,881 — — 165,881 186,990 — — 186,990 Diocesan Grants 806,093 — — 806,093 758,802 — — 758,802 Parish Grants — — — — 23,308 — — 23,308 Vision of Hope: Program Services 81,000 — — 81,000 65,988 — — 65,988 Capital Needs — — — — 36,591 — — 36,591 Mission Support 8,291 — — 8,291 161,927 — — 161,927 Contributions and Gifts 17,250 — — 17,250 36,600 — — 36,600 Restricted Funds Expended 5,176,564 — — 5,176,564 3,976,173 — — 3,976,173 Seminarian Support (301,901) — — (301,901) 73,396 — — 73,396 Insurance and Risk Management (Note 2) 17,646,004 — — 17,646,004 17,821,158 — — 17,821,158 Inter-Parish loan program interest 1,023,201 — — 1,023,201 1,066,105 — — 1,066,105 Diocesan Cemeteries 5,512,300 — — 5,512,300 5,871,588 — — 5,871,588

37,942,832 — — 37,942,832 37,558,634 — — 37,558,634 General and administrative expenses Financial Affairs 311,948 — — 311,948 234,694 — — 234,694 Provision for Uncollectible Receivables 1,832,971 — — 1,832,971 1,090,206 — — 1,090,206 Administration 1,418,725 — — 1,418,725 1,406,115 — — 1,406,115 Support Services 2,311,031 — — 2,311,031 2,245,622 — — 2,245,622 Settlement Expense, Net — — — — 1,700,000 — — 1,700,000 Property Expenses 285,798 — — 285,798 325,232 — — 325,232 Depreciation 996,433 — — 996,433 919,093 — — 919,093 Interest 157,085 — — 157,085 307,318 — — 307,318

7,313,991 — — 7,313,991 8,228,280 — — 8,228,280

Fundraising expenses Catholic Charity Fund Appeal 994,218 — — 994,218 872,577 — — 872,577 Total fundraising expenses 994,218 — — 994,218 872,577 — — 872,577

(continued on next page)See accompanying notes to the financial statements.

4

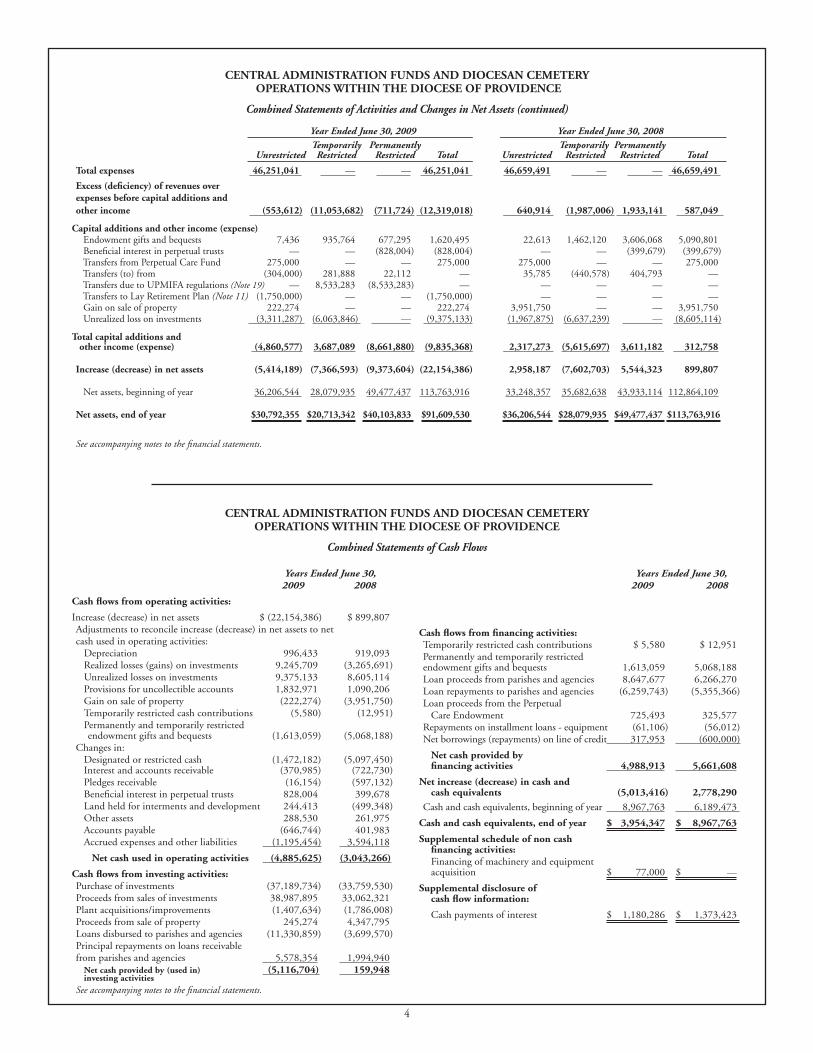

Years Ended June 30, 2009 2008

Cash flows from operating activities:

Increase (decrease) in net assets $ (22,154,386) $ 899,807 Adjustments to reconcile increase (decrease) in net assets to net cash used in operating activities: Depreciation 996,433 919,093 Realized losses (gains) on investments 9,245,709 (3,265,691) Unrealized losses on investments 9,375,133 8,605,114 Provisions for uncollectible accounts 1,832,971 1,090,206 Gain on sale of property (222,274) (3,951,750) Temporarily restricted cash contributions (5,580) (12,951) Permanently and temporarily restricted endowment gifts and bequests (1,613,059) (5,068,188)Changes in: Designated or restricted cash (1,472,182) (5,097,450) Interest and accounts receivable (370,985) (722,730) Pledges receivable (16,154) (597,132) Beneficial interest in perpetual trusts 828,004 399,678 Land held for interments and development 244,413 (499,348) Other assets 288,530 261,975 Accounts payable (646,744) 401,983 Accrued expenses and other liabilities (1,195,454) 3,594,118

Net cash used in operating activities (4,885,625) (3,043,266)

Cash flows from investing activities:Purchase of investments (37,189,734) (33,759,530)Proceeds from sales of investments 38,987,895 33,062,321 Plant acquisitions/improvements (1,407,634) (1,786,008)Proceeds from sale of property 245,274 4,347,795 Loans disbursed to parishes and agencies (11,330,859) (3,699,570)Principal repayments on loans receivable from parishes and agencies 5,578,354 1,994,940 Net cash provided by (used in) (5,116,704) 159,948 investing activities

Cash flows from financing activities:Temporarily restricted cash contributions $ 5,580 $ 12,951 Permanently and temporarily restricted endowment gifts and bequests 1,613,059 5,068,188 Loan proceeds from parishes and agencies 8,647,677 6,266,270 Loan repayments to parishes and agencies (6,259,743) (5,355,366)Loan proceeds from the Perpetual Care Endowment 725,493 325,577 Repayments on installment loans - equipment (61,106) (56,012)Net borrowings (repayments) on line of credit 317,953 (600,000)

Net cash provided by financing activities 4,988,913 5,661,608

Net increase (decrease) in cash and cash equivalents (5,013,416) 2,778,290

Cash and cash equivalents, beginning of year 8,967,763 6,189,473

Cash and cash equivalents, end of year $ 3,954,347 $ 8,967,763

Supplemental schedule of non cash financing activities: Financing of machinery and equipment acquisition $ 77,000 $ —

Supplemental disclosure of cash flow information:

Cash payments of interest $ 1,180,286 $ 1,373,423

CENTRAL ADMINISTRATION FUNDS AND DIOCESAN CEMETERYOPERATIONS WITHIN THE DIOCESE OF PROVIDENCE

Combined Statements of Cash Flows

CENTRAL ADMINISTRATION FUNDS AND DIOCESAN CEMETERY OPERATIONS WITHIN THE DIOCESE OF PROVIDENCE

Combined Statements of Activities and Changes in Net Assets (continued)

Year Ended June 30, 2009 Year Ended June 30, 2008

Temporarily Permanently Temporarily Permanently Unrestricted Restricted Restricted Total Unrestricted Restricted Restricted Total

Total expenses 46,251,041 — — 46,251,041 46,659,491 — — 46,659,491

Excess (deficiency) of revenues over expenses before capital additions and

other income (553,612) (11,053,682) (711,724) (12,319,018) 640,914 (1,987,006) 1,933,141 587,049

Capital additions and other income (expense) Endowment gifts and bequests 7,436 935,764 677,295 1,620,495 22,613 1,462,120 3,606,068 5,090,801 Beneficial interest in perpetual trusts — — (828,004) (828,004) — — (399,679) (399,679) Transfers from Perpetual Care Fund 275,000 — — 275,000 275,000 — — 275,000 Transfers (to) from (304,000) 281,888 22,112 — 35,785 (440,578) 404,793 — Transfers due to UPMIFA regulations (Note 19) — 8,533,283 (8,533,283) — — — — — Transfers to Lay Retirement Plan (Note 11) (1,750,000) — — (1,750,000) — — — — Gain on sale of property 222,274 — — 222,274 3,951,750 — — 3,951,750 Unrealized loss on investments (3,311,287) (6,063,846) — (9,375,133) (1,967,875) (6,637,239) — (8,605,114)

Total capital additions and other income (expense) (4,860,577) 3,687,089 (8,661,880) (9,835,368) 2,317,273 (5,615,697) 3,611,182 312,758 Increase (decrease) in net assets (5,414,189) (7,366,593) (9,373,604) (22,154,386) 2,958,187 (7,602,703) 5,544,323 899,807 Net assets, beginning of year 36,206,544 28,079,935 49,477,437 113,763,916 33,248,357 35,682,638 43,933,114 112,864,109 Net assets, end of year $30,792,355 $20,713,342 $40,103,833 $91,609,530 $36,206,544 $28,079,935 $49,477,437 $113,763,916

See accompanying notes to the financial statements.

Years Ended June 30, 2009 2008

See accompanying notes to the financial statements.

5

CENTRAL ADMINISTRATION FUNDS AND DIOCESAN CEMETERY OPERATIONS WITHIN THE DIOCESE OF PROVIDENCE

Notes to Financial Statements

Note 1 – Description and Basis of Financial Statements Presentation

The accompanying combined financial statements of the Central Administration Funds and Diocesan Cemetery Operations within the Diocese of Providence (the Funds) include the following corporations: Diocesan Administration Corporation (DAC) (General Fund); the Catholic Charity Fund (CCF); the Catholic Foundation of Rhode Island (the Foundation); the Catholic Cemeteries (the Cemeteries); the Seminary of Our Lady of Providence (Seminary); the Inter-Parish Loan Fund, Inc. (Deposit and Loan Fund); the Vision of Hope Fund, Inc. (VOH), Roman Catholic Bishop of Providence (RCB), a corporation sole; Parish Investment Group (Parish Investment); DiMed Corp.; Financial Aid for Catholic Education of RI (F.A.C.E. of Rhode Island), Diocesan Service Corporation (DSC) and begin-ning in fiscal year 2009, the Diocesan Plant Fund. All significant inter-fund balances and transactions have been eliminated in combination.

The Diocese of Providence (the Diocese) is a canonical organization and consists of over 250 separate corporations through which the Roman Catholic Church conducts a portion of its temporal affairs in Rhode Island. The corporations included in these financial statements are those organizations that, in addition to carrying out a portion of the mission of the Church in this Diocese, provide fundraising and general and administrative support to other organizations. The combined financial statements are not the general purpose financial statements of the 250 separate corporations of the Diocese of Providence and do not reflect nor include information relating to the other corporations included in the Diocese of Providence, such as parish corpora-tions, institutions, and entities through which various other agencies of the Roman Catholic Church carry on their temporal affairs.

Note 2 – Summary of Significant Accounting Policies

Financial Statement PresentationThe financial statements are presented on the basis of unrestricted, temporarily restricted and permanently restricted net assets, in accordance with Statement of Financial Accounting Standards (SFAS) No. 117, Financial Statements of Not-For-Profit Organizations. Accordingly, net assets of the Funds and changes therein are classified and reported as follows:

that stipulate the resources be maintained permanently, but permit the Funds to use, or expend, part or all of the income derived from the donated assets for either specified or unspecified purposes.

that permit the Funds to use, or expend, the assets as specified. The restrictions are satisfied either by the passage of time or by actions of the Funds.

imposed restrictions have expired. As reflected in the accompanying statements of financial position, the Funds’ Board of Directors has designated the unrestricted net assets of certain funds for insurance programs and for modernization and support. The Self Insurance and Workers’ Compensation Self Insurance Funds (the Insurance Funds) are designated for insurance deductibles and claims not covered by insurance policies. DiMed Corp. is designated and internally restricted for the operation of group healthcare programs for the various parishes and institutions. The Modernization and Support Fund has been designated for the purposes of supporting the capital and contingent needs of DAC.

Measure of OperationsThe Funds include, in their definition of operations, all revenues and expenses that are an integral part of their programs and supporting activities. Endowment gifts and bequests, unrealized gains and losses and certain other income and expense items are not included in operating income.

Revenue RecognitionUnconditional promises to give cash and other assets to the Funds are reported at fair value at the date the promise is verifiably committed. Conditional promises to give and indications of intentions to give are reported at fair value at the date the actual gift is received or the conditional promise becomes

unconditional. Gifts are reported as either temporarily or permanently restricted if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when a stipulated time restriction ends or purpose restriction is accomplished, temporarily restricted net assets are reclassified as unrestricted net assets and reported in the statements of activities and changes in net assets as net assets released from restrictions.

Contributions to be received after one year are discounted at a rate commen-surate with the time involved. Amortization of the discount is recorded as additional contribution revenue and used in accordance with donor-imposed restrictions, if any, on the contributions. Allowance is made for uncollect-ible contributions based upon management’s judgment and analysis of the creditworthiness of the donors, past collection experience and other relevant factors.

Medical premium fees received in advance are recorded as deferred revenue until it is earned.

Permanently Restricted Net AssetsRhode Island state law, with respect to endowment funds, has changed effec-tive June 30, 2009. The former requirement that the historical gift amount of endowment gifts plus an annual percentage increase measuring the consumer price index be recognized as permanently restricted has been eliminated ret-roactively (see Note 19).

Realized and unrealized appreciation, unless explicitly stated otherwise by the donor, is recognized as temporarily restricted unless the restriction is released in the same accounting period as the appreciation is earned. If the restriction is released in the same accounting period, the appreciation is recognized as unrestricted.

Investment IncomeThe Funds’ investments are pooled to facilitate their management. Investment income is allocated among unrestricted, temporarily restricted and perma-nently restricted net assets, based on donor restrictions or the absence thereof, using the market value unit method. Investment income, including net real-ized gains and losses, is recognized as operating revenue. Net unrealized gains and losses are recorded as other income.

Catholic Charity Fund AppealThe annual appeal of the CCF starts during the Lenten season and concludes at the end of the Fiscal Year. The appeal provides support for various pro-grams and agencies. Accordingly, the funds are accounted for in temporarily restricted given the time restriction. Certain of these gifts are further restricted by the donor. Pledges are recorded as revenue when the pledge is made, and allowances are provided for amounts estimated to be uncollectible. Funds from the prior year used in the current year are reflected as net assets released from restrictions in the statements of activities and changes in net assets.

Diocesan CemeteriesSales of graves and crypts are recorded when interment agreements are signed. The cost of graves and crypts is expensed when the sales are recognized.

Parish and Agency SupportThe DAC, CCF and VOH provide support to various Diocesan parishes, programs and agencies. The expenditures related to support are recognized at the time the subsidies are provided. To support such programs, the parishes and agencies of the Diocese are assessed annual fees and the parishes and agencies that participate in the insurance programs sponsored by the Funds are charged risk management premiums. The risk management premiums charged by the Funds to participating parishes and agencies are the result of the Funds implementing a self-funded medical program effective July 1, 2007, in an effort to control rising medical costs, whereby all premiums are earned by the Funds rather than earned by an outside insurer. Such amounts totaled approximately $16 million and $15 million in fiscal 2009 and 2008, respec-tively. The related expenses associated with running this self funded medical program were approximately $12.9 million and $12.4 million in Fiscal 2009 and 2008, respectively. These fees and premiums are recognized as revenue at the time they are billed. Program fees represent monies collected by the Funds for programs and seminars that they provide. Rental income represents charges to Diocesan parishes and agencies for the use of property and build-ings that are owned by the Funds.

6

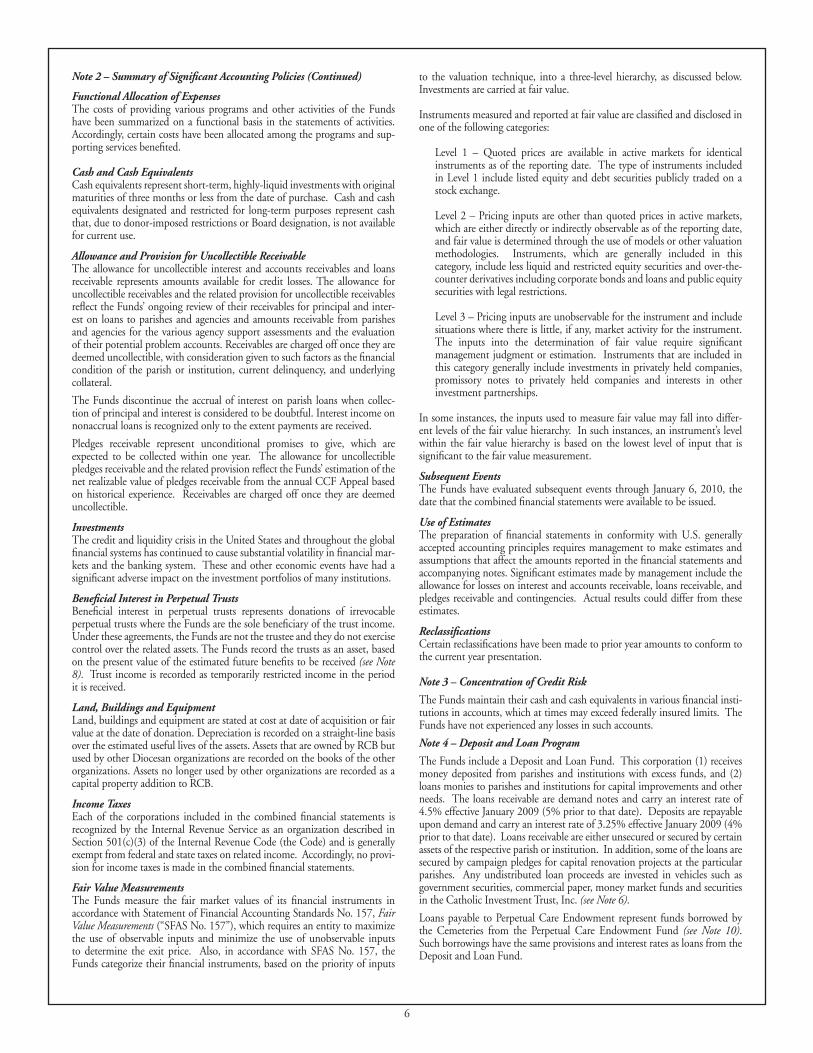

Functional Allocation of ExpensesThe costs of providing various programs and other activities of the Funds have been summarized on a functional basis in the statements of activities. Accordingly, certain costs have been allocated among the programs and sup-porting services benefited.

Cash and Cash EquivalentsCash equivalents represent short-term, highly-liquid investments with original maturities of three months or less from the date of purchase. Cash and cash equivalents designated and restricted for long-term purposes represent cash that, due to donor-imposed restrictions or Board designation, is not available for current use.

Allowance and Provision for Uncollectible ReceivableThe allowance for uncollectible interest and accounts receivables and loans receivable represents amounts available for credit losses. The allowance for uncollectible receivables and the related provision for uncollectible receivables reflect the Funds’ ongoing review of their receivables for principal and inter-est on loans to parishes and agencies and amounts receivable from parishes and agencies for the various agency support assessments and the evaluation of their potential problem accounts. Receivables are charged off once they are deemed uncollectible, with consideration given to such factors as the financial condition of the parish or institution, current delinquency, and underlying collateral.

The Funds discontinue the accrual of interest on parish loans when collec-tion of principal and interest is considered to be doubtful. Interest income on nonaccrual loans is recognized only to the extent payments are received.

Pledges receivable represent unconditional promises to give, which are expected to be collected within one year. The allowance for uncollectible pledges receivable and the related provision reflect the Funds’ estimation of the net realizable value of pledges receivable from the annual CCF Appeal based on historical experience. Receivables are charged off once they are deemed uncollectible.

InvestmentsThe credit and liquidity crisis in the United States and throughout the global financial systems has continued to cause substantial volatility in financial mar-kets and the banking system. These and other economic events have had a significant adverse impact on the investment portfolios of many institutions.

Beneficial Interest in Perpetual TrustsBeneficial interest in perpetual trusts represents donations of irrevocable perpetual trusts where the Funds are the sole beneficiary of the trust income. Under these agreements, the Funds are not the trustee and they do not exercise control over the related assets. The Funds record the trusts as an asset, based on the present value of the estimated future benefits to be received (see Note 8). Trust income is recorded as temporarily restricted income in the period it is received.

Land, Buildings and EquipmentLand, buildings and equipment are stated at cost at date of acquisition or fair value at the date of donation. Depreciation is recorded on a straight-line basis over the estimated useful lives of the assets. Assets that are owned by RCB but used by other Diocesan organizations are recorded on the books of the other organizations. Assets no longer used by other organizations are recorded as a capital property addition to RCB.

Income TaxesEach of the corporations included in the combined financial statements is recognized by the Internal Revenue Service as an organization described in Section 501(c)(3) of the Internal Revenue Code (the Code) and is generally exempt from federal and state taxes on related income. Accordingly, no provi-sion for income taxes is made in the combined financial statements.

Fair Value MeasurementsThe Funds measure the fair market values of its financial instruments in accordance with Statement of Financial Accounting Standards No. 157, Fair Value Measurements (“SFAS No. 157”), which requires an entity to maximize the use of observable inputs and minimize the use of unobservable inputs to determine the exit price. Also, in accordance with SFAS No. 157, the Funds categorize their financial instruments, based on the priority of inputs

to the valuation technique, into a three-level hierarchy, as discussed below. Investments are carried at fair value.

Instruments measured and reported at fair value are classified and disclosed in one of the following categories:

Level 1 – Quoted prices are available in active markets for identical instruments as of the reporting date. The type of instruments included in Level 1 include listed equity and debt securities publicly traded on a stock exchange. Level 2 – Pricing inputs are other than quoted prices in active markets, which are either directly or indirectly observable as of the reporting date, and fair value is determined through the use of models or other valuation methodologies. Instruments, which are generally included in this category, include less liquid and restricted equity securities and over-the-counter derivatives including corporate bonds and loans and public equity securities with legal restrictions.

Level 3 – Pricing inputs are unobservable for the instrument and include situations where there is little, if any, market activity for the instrument. The inputs into the determination of fair value require significant management judgment or estimation. Instruments that are included in this category generally include investments in privately held companies, promissory notes to privately held companies and interests in other investment partnerships.

In some instances, the inputs used to measure fair value may fall into differ-ent levels of the fair value hierarchy. In such instances, an instrument’s level within the fair value hierarchy is based on the lowest level of input that is significant to the fair value measurement.

Subsequent EventsThe Funds have evaluated subsequent events through January 6, 2010, the date that the combined financial statements were available to be issued.

Use of EstimatesThe preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Significant estimates made by management include the allowance for losses on interest and accounts receivable, loans receivable, and pledges receivable and contingencies. Actual results could differ from these estimates.

ReclassificationsCertain reclassifications have been made to prior year amounts to conform to the current year presentation.

Note 3 – Concentration of Credit Risk

The Funds maintain their cash and cash equivalents in various financial insti-tutions in accounts, which at times may exceed federally insured limits. The Funds have not experienced any losses in such accounts.

Note 4 – Deposit and Loan Program

The Funds include a Deposit and Loan Fund. This corporation (1) receives money deposited from parishes and institutions with excess funds, and (2) loans monies to parishes and institutions for capital improvements and other needs. The loans receivable are demand notes and carry an interest rate of 4.5% effective January 2009 (5% prior to that date). Deposits are repayable upon demand and carry an interest rate of 3.25% effective January 2009 (4% prior to that date). Loans receivable are either unsecured or secured by certain assets of the respective parish or institution. In addition, some of the loans are secured by campaign pledges for capital renovation projects at the particular parishes. Any undistributed loan proceeds are invested in vehicles such as government securities, commercial paper, money market funds and securities in the Catholic Investment Trust, Inc. (see Note 6).

Loans payable to Perpetual Care Endowment represent funds borrowed by the Cemeteries from the Perpetual Care Endowment Fund (see Note 10). Such borrowings have the same provisions and interest rates as loans from the Deposit and Loan Fund.

Note 2 – Summary of Significant Accounting Policies (Continued)

7

Note 5 – Allowance for Losses

An analysis of the allowance for losses is as follows: Accounts and Parish Interest Pledges Loans Receivable Receivable Receivable2009 Balance at beginning of year $ 1,922,355 $ 468,740 $ 1,100,000 Provision for losses 846,100 486,871 500,000 Charge-offs, net (111,279) (544,009) —

Balance at end of year $ 2,657,176 $ 411,602 $ 1,600,000

2008Balance at beginning of year $ 1,513,544 $ 440,018 $ 1,050,000 Provision for losses 668,455 371,751 50,000 Charge-offs, net (259,644) (343,029) — Balance at end of year $ 1,922,355 $ 468,740 $ 1,100,000

At June 30, 2009 and 2008, the Funds had parish (and institution) loans totaling $21,658,564 and $15,906,059, respectively, of which approximately $2,000,000 were considered impaired at June 30, 2009 and 2008, respec-tively, under SFAS No. 114, Accounting for Certain Investments in Debt and Equity Securities, as amended, and interest is not being accrued on such loans. The allowance for loan losses, related to impaired loans, was $1,600,000 and $1,100,000 for the years ended June 30, 2009 and 2008, respectively.

Note 6 – Investments

The majority of the Funds’ investments are maintained in the Catholic Investment Trust, Inc. (CIT) pool, a separate Diocesan corporation that pro-vides a centralized investment pool for the parishes, agencies and programs of the Diocese of Providence. Income, gains, and losses are allocated to partici-pating funds based upon their units. The participating funds purchase units based upon a per unit value at the time of purchase. The CIT tracks separate investment unit values based upon the type of investment (fixed or equity). The fixed and equity values per unit at June 30, 2009, were $9.71 and $8.90, respectively, and at June 30, 2008, were $11.32 and $9.05, respectively.

The Funds’ pro-rata shares (based on units held at June 30) of investments held by the CIT along with investments held directly by the Funds, are as follows: 2009 2008 Cost Fair Value Cost Fair ValueCash and cash equivalents $ 13,617,741 $ 13,617,741 $ 10,033,192 $ 10,033,192 Government obligations 4,142,969 4,082,560 4,910,694 4,850,808 Mutual funds 49,203,728 43,077,880 58,155,558 60,522,325 Corporate and foreign bonds 9,549,257 8,732,274 9,308,963 8,675,144 Common stock 2,632,255 2,046,763 10,115,726 8,560,976 Real estate investment trust 3,409,016 2,044,206 3,460,469 2,909,073 Limited partnership 11,595,214 11,368,450 9,209,448 9,837,359

$ 94,150,180 $ 84,969,874 $ 105,194,050 $ 105,388,877

Components of investment loss related to the above investments for the years ended June 30, are as follows: 2009 2008Interest and dividends (in operating income) $ 2,684,075 $ 3,416,157 Net realized gains (losses) (in operating income) (9,245,709) 3,265,691 Net unrealized losses (in other income/expense) (9,375,133) (8,605,114)

$ (15,936,767) $ (1,923,266)

Certain parishes and agencies participate in the CIT, whereby the related investments are included in the combined financial statements, but the applicable investment income is distributed to those parishes and agencies; accordingly, $371,160 and $210,485 of net realized gains and $326,862 and $406,489 of net unrealized gains are excluded from investment income in the combined financial statements for the years ended June 30, 2009 and June 30, 2008, respectively.

For the year ended June 30, 2009, custodian fees and investment advisor fees of $194,487 and $419,870 were netted against interest and dividend income and net realized gains, respectively. For the year ended June 30, 2008, such fees were $228,078 and $420,256, respectively.

Note 7 – Fair Value Measurements

The Funds adopted SFAS No. 157 as of July 1, 2008, which among other matters, requires enhanced disclosures about instruments that are measured and reported at fair value. SFAS No. 157 establishes a hierarchal disclosure framework which prioritizes and ranks the level of market price used in mea-suring instruments at fair value. Market price is affected by a number of factors, including the type of instrument and the characteristics specific to the instrument. Instruments with readily available quoted prices or for which fair value can be measured for actively quoted prices generally will have a higher degree of market price observability and a lesser degree of judgment used in measuring fair value. The implementation of SFAS No. 157 had no impact on reported amounts.

The Funds assume that for the following financial instruments, the carrying value reported in the balance sheets approximates fair value: cash and cash equivalents, accounts, interest, pledges, and loans receivable, payables and line of credit.

The valuation of the Funds instruments using the fair value hierarchy con-sisted of the following at June 30, 2009:

Quoted prices Significant Significant in active observable unobservable markets inputs inputs

Level 1 Level 2 Level 3 TotalCash and cash equivalents $ 13,617,741 $ - $ - $ 13,617,741 Government obligations 4,082,560 - - 4,082,560 Mutual funds 43,077,880 - - 43,077,880 Corporate and foreign bonds - 8,732,274 - 8,732,274 Common stock 2,046,763 - - 2,046,763 Real estate investment trust 2,044,206 - - 2,044,206 Limited partnership - - 11,368,450 11,368,450

$ 64,869,150 $ 8,732,274 $ 11,368,450 $ 84,969,874

The changes in instruments measured at fair value for which the Funds have used Level 3 inputs to determine fair value are as follows:

Level 3Balance, July 1, 2008 $ 9,837,359

Purchases, net 2,814,203

Realized and unrealized losses (1,283,112)

Balance, June 30, 2009 $ 11,368,450

Changes in unrealized losses included in

earnings related to Level 3 investments

still held at reporting time $ (769,859)

Note 8 – Beneficial Interest in Perpetual Trusts

The Funds are the sole beneficiaries of several longstanding perpetual trusts that are required to be recorded on the Funds’ financial statements in accor-dance with SFAS No. 136, Transfers of Assets to a Not-for-Profit Organization or Charitable Trust That Raises or Holds Contributions for Others. Accordingly, the fair value of these trusts, which consists principally of equities and fixed income securities, of $3,436,209 and $4,264,213, are recorded as an asset at June 30, 2009 and June 30, 2008, respectively, with related appreciation (depreciation) of the underlying assets recorded as a change in permanently restricted net assets.

8

Note 9 – Land, Buildings and Equipment

Land, buildings and equipment of the Funds are comprised of the following at June 30: 2009 2008Land and improvements $ 4,802,666 $ 4,801,946 Buildings and improvements 14,467,615 12,963,109 Construction in progress - 517,436 Furniture and fixtures 1,072,108 974,921 Equipment 6,515,500 6,169,118 26,857,889 25,426,530 Less accumulated depreciation (17,258,758) (16,292,600)

Land, buildings and equipment, net $ 9,599,131 $ 9,133,930

Included in equipment are assets under capital lease totaling $83,425 and $67,531 at June 30, 2009 and 2008, respectively.

During 2009, one property and vehicle was sold, resulting in a net gain of $222,274. During 2008, two properties were sold resulting in a net gain of $3,951,750.

Note 10 – Perpetual Care Endowment Fund

The Cemeteries maintain the Diocesan cemeteries in accordance with the State Cemetery Act. The Cemeteries collect and pay into a perpetual care fund (the Perpetual Care Endowment Fund, or PCF) twenty percent (20%) of the gross sales price of each plot and crypt. The PCF is held for the benefit of those interred and their families. As such, the PCF assets are not considered to be the property of the Funds, notwithstanding distributions made available by the Funds, and are not included in these financial statements. Distributions are made available from these funds and amounted to $275,000 for the years ended June 30, 2009 and 2008. At June 30, 2009 and 2008, borrowings by the Cemeteries from the Perpetual Care Endowment Fund totaled $2,342,948 and $1,617,455, respectively. The loan carries an interest rate of 2.25% effec-tive May 2009 (4.5% prior to that date). Loan repayments are to be made from all amounts received by St. Ann’s Cemetery on new section sales and garden mausoleum sales less the 20% paid into the perpetual care fund, until interest and principal are paid in full.

In fiscal 2000, an actuarial study was performed for the Perpetual Care Endowment Fund in order to better understand the potential financial needs for developed and undeveloped cemetery land. Although there is no direct obligation to do so, the Cemeteries intent was to fund this potential need over a thirty-year period beginning in 2000. Each year subsequent to the study, monies are being set aside through compounding of investment returns. At June 30, 2009, the estimated need is $37.6 million, while the PCF has total restricted assets of $15.3 million, resulting in an estimated net unfunded potential need of $22.3 million.

Note 11 – Lay Pension Plans

The Funds participate in the Diocesan noncontributory defined benefit pension program for lay employees (a multi-employer plan) and in a multi- employer plan for unionized cemetery workers. As of July 1, 2008, the date of the latest actuarial report, the defined benefit pension program for lay employees had assets of $78.5 million and an actuarial present value of accumulated benefits of $113.4 million, resulting in a net liability of $34.9 million. Lay employees working for the Funds account for 4% of the partici-pants in these plans. The obligation for the remaining participants under the multi-employer plan continues to be the proportionate responsibility of each Diocesan corporation.

The Funds made annual contributions of $277,856 and $274,670 to the lay employee plan and $189,205 and $198,703 to the cemetery union plan during 2009 and 2008, respectively. Also during 2009, the Funds made a $1.75 million discretionary supplemental contribution to the lay employee plan using proceeds from risk management premiums made by Diocesan parishes and agencies, in an effort to reduce the unfunded basis of the plan.

Note 12 – Priest Benefits Fund

The Funds participate in Our Lady Queen of the Clergy (OLQC), a separate corporation, which maintains both the Priest Retirement Plan and the Priest Medical Programs, (multi-employer plans), within the Priest Benefits Fund (formerly known as the Clergy Retirement Plan, Clergy Medical Programs and Clergy Benefits Fund, respectively). These plans are noncontributory defined pension and medical benefit plans for priests working at the administrative offices and throughout other Diocesan organizations. As of July 1, 2008, the

date of the latest Actuarial Report, the defined benefit pension plan had assets of $12.6 million and an actuarial present value of accumulated benefits of $22.9 million, resulting in a net liability of $10.3 million. Priests working for the Funds account for 16% of the participants in these plans. The obligation for the remaining participants under the multi-employer plan continues to be the proportionate responsibility of each Diocesan corporation.

The Funds made contributions of $380,000 to OLQC during both 2009 and 2008.

Note 13 – Other Assets

Other assets consist of the following at June 30: 2009 2008Equity investment in the Catholic Umbrella Pool $ 422,075 $ 715,006 Cash surrender value of donated life insurance policies 190,152 219,226 Other 160,433 126,958 Other assets designated or restricted for long-term purposes $ 772,660 $ 1,061,190

The DSC (Self Insurance Fund) participates in the Catholic Umbrella Pool (CUP), a self-insurance liability pool of thirty-seven Dioceses and Archdioceses throughout the United States (see Note 14). The following condensed infor-mation relating to the CUP was audited by an independent accounting firm (see discussion of their report below in Note 14): 2009 2008 (In Thousands)Assets: Investments $ 21,237 $ 26,968 Cash and cash equivalents 2,029 2,001 Other 957 908

$ 24,223 $ 29,877 Liabilities and equity: Estimated unpaid claims and expenses $ 3,233 $ 3,697 Other 4,630 1,186 Dividends payable to participants 984 2,918 Participants’ equity 15,376 22,076 $ 24,223 $ 29,877

Note 14 – Contingencies

Catholic Umbrella Pool

The Funds are a participant in the CUP. The CUP provides excess insurance liability coverage and morality coverage for its membership. This coverage is placed through the administrator, Catholic Mutual Relief Society of America. As a participant, the Funds obtain insurance for certain risk levels that are not provided by its other insurance programs, thus mitigating their overall risk. The Funds make annual premium contributions to the CUP for the insurance provided. The CUP is responsible for the following liability coverages:

July 1, 1987 to July 1, 1988 $3,700,000 in excess of $1,300,000 July 1, 1988 to July 1, 2002 $3,500,000 in excess of $1,500,000 July 1, 2002 to July 1, 2003 40.0% of $3,500,000 in excess of $1,500,000 July 1, 2003 to January 1, 2005 37.5% of $3,500,000 in excess of $1,500,000 January 1, 2005 to January 1, 2007 66.7% of $3,500,000 in excess of $1,500,000 January 1, 2007 to present 64.3% of $3,500,000 in excess of $1,500,000

The CUP provides insurance coverage of $150,000 for morality claims rang-ing from $100,000 to $850,000 for the period July 1, 1987 through June 30, 2002.

Additionally, for the period July 1, 2002 through June 30, 2009, the CUP provides limited excess insurance coverage of $1,500,000 up to $5,000,000 for morality claims and excess coverage of $1,500,000 to a limit of $20,500,000 for liability claims.

As a participant in the CUP, the Funds are liable for any losses beyond the Pool’s ability to fund such losses after total participants’ equity is liquidated ($15,376,000 and $22,076,000 as of June 30, 2009 and 2008, respectively).

The Pool’s auditors were unable to obtain sufficient evidential matter regarding the provision and reserve for unpaid claims and claim expenses due to the lack of historical loss experience given the limited number of claims. Accordingly, the ultimate settlement of the losses and related loss adjustment expenses of the Pool may vary significantly from the estimated amounts included in the Pool’s financial statements and the ultimate liability would require the Funds to participate in the funding of such additional amounts, if any.

9

minimum debt service coverage and a minimum liquidity ratio.

Note 16 – Temporarily Restricted Net Assets

Temporarily restricted net assets are available for the following purposes, based on passage of time, donor intent or the purpose of the restriction being met at June 30:

2009 2008Vision of Hope Fund $ 2,854,625 $ 4,277,766 Catholic Charity Fund 4,261,120 4,296,510 Catholic Foundation of Rhode Island 10,634,151 16,809,147 Cutting Trust 1,206,465 1,283,758 Davey Trust - 156,597 Seminary of Our Lady of Providence 1,508,897 1,256,157 Mission Fund 248,084 -Total $ 20,713,342 28,079,935

Note 17 – Permanently Restricted Net Assets

Permanently restricted net assets are restricted to investment in perpetuity. The income is expendable to support the following at June 30:

2009 2008Catholic Foundation of Rhode Island $ 38,704,825 $ 46,924,390 Cutting Trust 115,890 292,958 Seminary of Our Lady of Providence 783,118 1,502,130 Mission Fund 500,000 757,959

Total $ 40,103,833 $ 49,477,437

Note 18 – Net Assets Released From Restriction

Net assets were released from donor restrictions by incurring expenses satisfy-ing the following restricted purposes:

2009 2008Vision of Hope Fund Programs $ 804,781 $ 158,744 Catholic Charity Fund Programs 8,387,283 7,845,267 Catholic Foundation of Rhode Island 4,841,899 3,671,487 Cutting Trust 18,851 271,550 Davey Trust 159,067 7,807 Mission Fund 147,771 176,988 Major Seminarian Program 189,631 174,805 Seminary of Our Lady of Providence 3,209 74,779

Total $ 14,552,492 $ 12,381,427

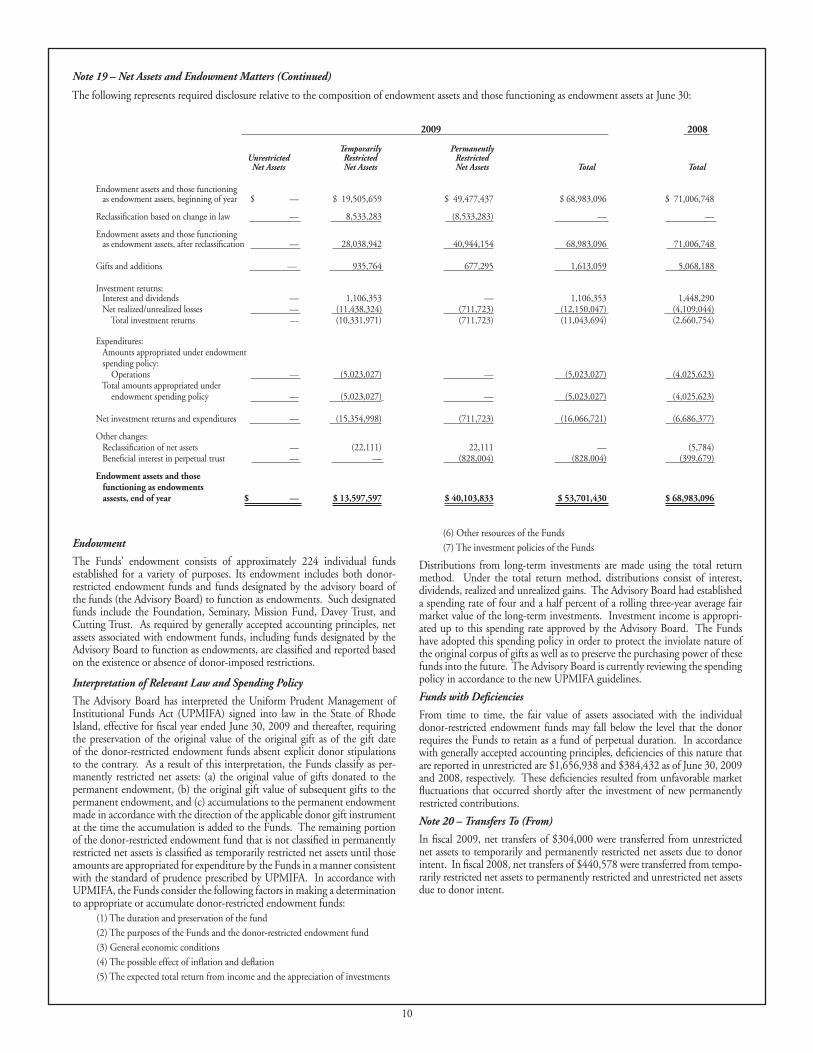

Note 19 – Net Assets and Endowment Matters

The Financial Accounting Standards Board (“FASB”) has issued FASB Staff Position 117-1 (“FSP 117-1”) effective for fiscal years ending after December 15, 2008. The Funds adopted FSP 117-1 as of July 1, 2008, which requires enhanced disclosures for each period for which the Funds present finan-cial statements. The adoption of FSP 117-1 had no impact on reported amounts.

The following is the composition of endowment assets and those functioning as endowment assets by net asset class as of June 30, 2009: Temporarily Permanently

Unrestricted Restricted Restricted Total Donor-restricted endowment funds $ - $ 13,597,597 $ 40,103,833 $ 53,701,430

Board-designated

endowment funds - - - -

$ - $ 13,597,597 $ 40,103,833 $ 53,701,430

The following is the composition of endowments assets and those functioning as endowment assets by net asset class as of June 30, 2008: Temporarily Permanently

Unrestricted Restricted Restricted Total Donor-restricted endowment funds $ - $ 19,505,659 $ 49,477,437 $ 68,983,096

Board-designated endowment funds - - - -

$ - $ 19,505,659 $ 49,477,437 $ 68,983,096

Note 14 – Contingencies (Continued)

Catholic Umbrella Pool (Continued)

The Funds do not believe there is significant exposure to losses beyond their equity in the CUP as of June 30, 2009 and 2008, respectively.

GuaranteesRCB is contingently liable as guarantor of two financing arrangements in order to facilitate needed construction by two related corporations. CIT is a guarantor of two construction loans for low income apartments/condos.

The guarantees are as follows at June 30: 2009 2008RCB Saint Antoine Residence $ 2,000,000 $ 2,000,000 The Frassati Residence - 379,145Cranston-Johnston Catholic Regional School 6,500,000 -

Total $ 8,500,000 $ 2,379,145

2009 2008Catholic Investment Trust, Inc. Pleasant View, LLC - Low Income Apartments/Condos $ 2,400,000 $ 2,400,000 St. Casimir Place, LLC - Low Income Apartments/Condos 2,064,478 -

Total $ 4,464,478 $ 2,400,000

The obligations of both RCB and CIT above are collateralized by the land and buildings at the residences/apartments/condos. In the event of default, these assets would be sold, with the net proceeds used to reduce the related obligations. If such proceeds were not sufficient to repay the entire obligation, RCB and CIT would be required to fulfill its guarantee.

Settlement Expense

RCB was named as the defendant in several matters relating to the alleged misconduct of priests along with other affiliated entities through which the Roman Catholic Church conducts its temporal affairs in Rhode Island. Although it is believed that these cases would result in a favorable judgment for RCB, from time to time, RCB has agreed to settle claims relating to such matters utilizing the assets of RCB.

During the year ended June 30, 2008, the funds incurred net charges of approximately $1,700,000 in order to increase the settlement reserve to $2,000,000. Payments of claims and related expenses totaled approximately $1,226,000 and $1,400,000 in 2009 and 2008, respectively.

As of June 30, 2009 and 2008, a remaining settlement reserve of approximately $774,000 and $2,000,000, respectively, was included in accrued expenses and other liabilities on the combined statements of financial position, representing the balance on claims due or expected to be settled and legal costs incurred or expected to be incurred. Management believes that the amount accrued is the best estimate of probable losses based upon the current facts and circum-stances. It is possible, however, that future results of RCB activities may be materially affected by changes in circumstances regarding these matters.

Note 15 – Line of Credit

On April 28, 2009, RCB refinanced the existing line of credit with a new twelve month open line of credit of $9,000,000 subject to annual review for renewal. The open line of credit expires on April 27, 2010. The balance due on the line of credit was $6,209,194 and $5,891,241 at June 30, 2009 and 2008, respectively. The Funds are in the process of extending this agreement and expect it to be renewed prior to its due date. Further, the Funds have cash and investments available to pay off the line of credit balance if necessary. At June 30, 2009, the Funds were not in compliance with a financial covenant under the agreement. On December 16, 2009, the financial covenant not in compliance was waived by the bank and prospectively modified effective June 30, 2010 and beyond.

The line of credit is secured by a first mortgage against a property located on Warwick Neck Avenue, Warwick, Rhode Island. Interest is charged at the London Inter-Bank Offer Rate (LIBOR) plus 175 basis points with a mini-mum rate of 2.20%. (2.20% as of June 30, 2009). Amounts borrowed under this agreement are guaranteed by real estate designated for sale by RCB. Interest on the loan is payable monthly in arrears on the first day of each month. The line of credit requires that RCB maintain certain financial ratios with regard to

10

Note 19 – Net Assets and Endowment Matters (Continued)

Endowment

The Funds’ endowment consists of approximately 224 individual funds established for a variety of purposes. Its endowment includes both donor-restricted endowment funds and funds designated by the advisory board of the funds (the Advisory Board) to function as endowments. Such designated funds include the Foundation, Seminary, Mission Fund, Davey Trust, and Cutting Trust. As required by generally accepted accounting principles, net assets associated with endowment funds, including funds designated by the Advisory Board to function as endowments, are classified and reported based on the existence or absence of donor-imposed restrictions.

Interpretation of Relevant Law and Spending Policy

The Advisory Board has interpreted the Uniform Prudent Management of Institutional Funds Act (UPMIFA) signed into law in the State of Rhode Island, effective for fiscal year ended June 30, 2009 and thereafter, requiring the preservation of the original value of the original gift as of the gift date of the donor-restricted endowment funds absent explicit donor stipulations to the contrary. As a result of this interpretation, the Funds classify as per-manently restricted net assets: (a) the original value of gifts donated to the permanent endowment, (b) the original gift value of subsequent gifts to the permanent endowment, and (c) accumulations to the permanent endowment made in accordance with the direction of the applicable donor gift instrument at the time the accumulation is added to the Funds. The remaining portion of the donor-restricted endowment fund that is not classified in permanently restricted net assets is classified as temporarily restricted net assets until those amounts are appropriated for expenditure by the Funds in a manner consistent with the standard of prudence prescribed by UPMIFA. In accordance with UPMIFA, the Funds consider the following factors in making a determination to appropriate or accumulate donor-restricted endowment funds: (1) The duration and preservation of the fund

(2) The purposes of the Funds and the donor-restricted endowment fund

(3) General economic conditions

(4) The possible effect of inflation and deflation

(5) The expected total return from income and the appreciation of investments

(6) Other resources of the Funds

(7) The investment policies of the Funds

Distributions from long-term investments are made using the total return method. Under the total return method, distributions consist of interest, dividends, realized and unrealized gains. The Advisory Board had established a spending rate of four and a half percent of a rolling three-year average fair market value of the long-term investments. Investment income is appropri-ated up to this spending rate approved by the Advisory Board. The Funds have adopted this spending policy in order to protect the inviolate nature of the original corpus of gifts as well as to preserve the purchasing power of these funds into the future. The Advisory Board is currently reviewing the spending policy in accordance to the new UPMIFA guidelines.

Funds with Deficiencies

From time to time, the fair value of assets associated with the individual donor-restricted endowment funds may fall below the level that the donor requires the Funds to retain as a fund of perpetual duration. In accordance with generally accepted accounting principles, deficiencies of this nature that are reported in unrestricted are $1,656,938 and $384,432 as of June 30, 2009 and 2008, respectively. These deficiencies resulted from unfavorable market fluctuations that occurred shortly after the investment of new permanently restricted contributions.

Note 20 – Transfers To (From)

In fiscal 2009, net transfers of $304,000 were transferred from unrestricted net assets to temporarily and permanently restricted net assets due to donor intent. In fiscal 2008, net transfers of $440,578 were transferred from tempo-rarily restricted net assets to permanently restricted and unrestricted net assets due to donor intent.

Temporarily Permanently Unrestricted Restricted Restricted Net Assets Net Assets Net Assets Total Total

Endowment assets and those functioning as endowment assets, beginning of year $ — $ 19,505,659 $ 49,477,437 $ 68,983,096 $ 71,006,748

Reclassification based on change in law — 8,533,283 (8,533,283) — —

Endowment assets and those functioning as endowment assets, after reclassification — 28,038,942 40,944,154 68,983,096 71,006,748

Gifts and additions — 935,764 677,295 1,613,059 5,068,188 Investment returns: Interest and dividends — 1,106,353 — 1,106,353 1,448,290 Net realized/unrealized losses — (11,438,324) (711,723) (12,150,047) (4,109,044) Total investment returns — (10,331,971) (711,723) (11,043,694) (2,660,754) Expenditures: Amounts appropriated under endowment spending policy: Operations — (5,023,027) — (5,023,027) (4,025,623) Total amounts appropriated under endowment spending policy — (5,023,027) — (5,023,027) (4,025,623) Net investment returns and expenditures — (15,354,998) (711,723) (16,066,721) (6,686,377) Other changes: Reclassification of net assets — (22,111) 22,111 — (5,784) Beneficial interest in perpetual trust — — (828,004) (828,004) (399,679)

Endowment assets and those functioning as endowments assests, end of year $ — $ 13,597,597 $ 40,103,833 $ 53,701,430 $ 68,983,096

2009 2008

The following represents required disclosure relative to the composition of endowment assets and those functioning as endowment assets at June 30:

11

CENTRAL ADMINISTRATION FUNDS AND DIOCESAN CEMETERY OPERATIONS WITHIN THE DIOCESE OF PROVIDENCE

Combining Statements of Financial PositionJune 30, 2009

(with comparative totals as of June 30, 2008)

Catholic General Charity Vision Fiduciary Endowment Plant Total Total Fund Fund Cemetery of Hope Other Fund Fund Fund 2009 2008AssetsCash and cash equivalents $ 1,163,556 $ — $ 45,226 $ — $ — $ 2,349,807 $ — $ 395,758 $ 3,954,347 $ 8,967,763 Cash and cash equivalents designated or restricted for long—term purposes — 2,561,865 — 2,096 6,673,062 — 179,453 — 9,416,476 7,944,294 Accounts and Interest receivable, net 534,311 24,102 524,214 — 1,362,943 396,779 597 97 2,843,043 3,318,158 Pledges receivable, net — 2,080,564 — — — — — — 2,080,564 2,551,281 Loans receivable from parishes and agencies, net — — — — — 20,058,564 — — 20,058,564 14,806,059 Due from (to) other funds (428,888) 32,349 (1,920,654) (292) 161,088 2,345,090 (188,443) (250) — —Investments 516,597 26,173 69,417 2,775,887 19,125,117 10,466,900 50,282,366 1,707,417 84,969,874 105,388,877 Beneficial interest in perpetual trusts — — — — — — 3,436,209 — 3,436,209 4,264,213 Land and buildings held for interments — — 1,940,639 — — — — — 1,940,639 2,185,052 Land held for parish development — — — — — — — 2,053,595 2,053,595 2,053,595 Land, buildings and equipment, net 369,946 146,433 4,716,874 — 116,488 — 1,851,360 2,398,030 9,599,131 9,133,930 Other assets designated or restricted for long—term purposes 46,972 4,340 — 76,934 528,007 — 116,407 — 772,660 1,061,190

Total assets $ 2,202,494 $ 4,875,826 $ 5,375,716 $ 2,854,625 $ 27,966,705 $ 35,617,140 $55,677,949 $ 6,554,647 $ 141,125,102 $ 161,674,412

Liabilities and net assetsLine of credit — — — — 6,209,194 — — — 6,209,194 5,891,241 Accounts payable 161,851 87,993 263,447 — 28,932 162,094 34,147 — 738,464 1,385,208 Accrued expenses and other liabilities 811,650 525,766 362,699 — 4,103,947 — 30,611 — 5,834,673 6,154,979 Deferred income 6,221 947 — — 1,299,074 — — — 1,306,242 1,268,296 Institutional deposits — — — — 31,140 3,789,691 — — 3,820,831 4,733,925 Installment loans—equipment — — 83,425 — — — — — 83,425 67,531 Loans payable to Perpetual Care Endowment — — 2,342,948 — — — — — 2,342,948 1,617,455 Loans payable to parishes and agencies — — — — — 29,179,795 — — 29,179,795 26,791,861

Total liabilities 979,722 614,706 3,052,519 — 11,672,287 33,131,580 64,758 — 49,515,572 47,910,496

Contingencies

Net assetsUnrestricted: Internally designated for: Insurance — — — — 13,613,624 — — — 13,613,624 14,618,821 Modernization and support — — — — 3,603,035 — — — 3,603,035 4,792,371 Unrestricted 1,222,772 — 2,323,197 — (922,241) 2,485,560 1,911,761 6,554,647 13,575,696 16,795,352 Total unrestricted 1,222,772 — 2,323,197 — 16,294,418 2,485,560 1,911,761 6,554,647 30,792,355 36,206,544 Temporarily restricted — 4,261,120 — 2,854,625 — — 13,597,597 — 20,713,342 28,079,935 Permanently restricted — — — — — — 40,103,833 — 40,103,833 49,477,437

Total net assets 1,222,772 4,261,120 2,323,197 2,854,625 16,294,418 2,485,560 55,613,191 6,554,647 91,609,530 113,763,916

Total liabilities and net assets $2,202,494 $4,875,826 $5,375,716 $2 ,854,625 $27,966,705 $35,617,140 $55,677,949 $6,554,647 $141,125,102 $161,674,412

See independent auditors’ report on other financial information and accompanying note.

Independent Auditors’ Report on Other Financial Information

The Most Reverend Thomas J. Tobin Bishop of Providence

Our audit was conducted for the purpose of forming an opinion on the basic financial statements taken as a whole. The combining statement of financial position of the Central Administration Funds and Diocesan Cemetery Operations within the Diocese of Providence as of June 30, 2009 and the related combining statements of activities and changes in net assets, for the year then ended are presented for purposes of additional analysis and are not a required part of the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and, in our opinion, is fairly stated in all material respects in relation to the basic financial statements taken as a whole. The supplemental information for 2008 was subjected to the auditing procedures applied in the audit of the 2008 basic financial statements performed by other auditors, Tofias PC, whose shareholders became shareholders of Mayer Hoffman McCann P.C. as of December 31, 2008, and whose report dated November 21, 2008, expressed their opinion that such 2008 information was fairly stated in all material respects in relation to the 2008 basic financial statements taken as a whole.

January 6, 2010 Providence, Rhode Island

12

Human devleopment collection — 22,576 — — — — — — 22,576 26,026 Communications collection 59,189 — — — — — — — 59,189 64,899 Program grants/contracts — 6,000 — — — — — — 6,000 6,000 Catholic Charity Fund Appeal — 7,830,128 — — — — — — 7,830,128 7,724,937 Vision of Hope Fund Appeal — — — 5,580 — — — — 5,580 12,951 Diocesan Cemeteries — — 5,438,792 — — — — — 5,438,792 5,928,921 Rental, lease and other income 428,745 5,156 — — 5,957 — 15,746 5,000 460,604 451,271

Total revenues 4,108,569 8,336,245 5,439,697 (186,206) 20,338,489 809,216 (4,948,046) 34,059 33,932,023 47,246,540

Program expensesCommunications andtelecommunications 391,819 — — — — — — — 391,819 386,423 The Tribunal 316,614 — — — — — — — 316,614 340,164 Rhode Island Catholic 560,000 — — — — — — — 560,000 561,350 Director of Religious — 66,612 — — — — — — 66,612 63,513 Priest Council 2,300 — — — — — — — 2,300 1,106 Spiritual Development 106,407 — — — — — — — 106,407 108,387 Youth Ministry — 605,522 — — — — — — 605,522 590,522 Hispanic Ministry — 356,650 — — — — — — 356,650 431,319 Christian Education — 1,051,446 — — — — — — 1,051,446 1,005,884 Campus Ministry — 381,804 — — — — — — 381,804 372,516 Apostolate for the Handicapped — 184,459 — — — — — — 184,459 175,888 Diocesan Schools — 595,028 — — — — — — 595,028 596,628 Community Services and Advocacy — 1,189,633 — — — — — — 1,189,633 1,102,140 Advocacy and Emergency Shelter — 29,523 — — — — — — 29,523 32,973 Life and Family Ministry — 419,122 — — — — — — 419,122 411,501 St. Antoine Residence — 75,000 — — — — — — 75,000 75,000 St. Francis House — 110,947 — — — — — — 110,947 88,250 St. Clare Home — 50,000 — — — — — — 50,000 50,000Ministries & Clergy personnel 429,078 621,835 — — — — — — 1,050,913 864,061 Parish share support — 264,350 — — — — — — 264,350 222,383 Grants: National grants 165,881 — — — — — — — 165,881 186,990 Diocesan grants 335,333 470,760 — — — — — — 806,093 758,802 Parish grants — — — — — — — — — 23,308 Vision of Hope Grants: Program and Services — — — 81,000 — — — — 81,000 65,988 Capital Needs — — — — — — — — — 36,591 Mission support — — — — — — 8,291 — 8,291 161,927 Contributions and gifts 17,250 — — — — — — — 17,250 36,600 Restricted Funds expended — — — — — — 5,176,564 — 5,176,564 3,976,173 Seminarian support 155,366 155,000 — — — — (612,267) — (301,901) 73,396 Insurance and risk management — — — 3,000 17,643,004 — — — 17,646,004 17,821,158 Inter-Parish loan program interest — — — — — 1,023,201 — — 1,023,201 1,066,105 Diocesan Cemeteries — — 5,512,300 — — — — — 5,512,300 5,871,588

Total program expenses $ 2,480,048 $ 6,627,691 $ 5,512,300 $ 84,000 $17,643,004 $ 1,023,201 $ 4,572,588 $ — $ 37,942,832 $ 37,558,634

(continued on next page)

Revenues

Interest and dividend income $ 15,787 $ 10,706 $ 905 $ 83,850 $ 656,489 $ 1,524,745 $ 1,131,621 $ 29,059 $ 3,453,162 $ 4,192,744 Gifts and bequests 3,310 18,976 — — 102,000 — 133,909 — 258,195 442,446Trust income — 159,508 — — — — — — 159,508 165,408 Realized gains (losses) on investments, net — — — (275,636) (1,610,782) (715,529) (6,643,762) — (9,245,709) 3,265,691 Parish assessment 3,119,421 — — — — — — — 3,119,421 3,027,015 Risk management premiums — — — — 21,119,040 — — — 21,119,040 20,679,344 Agency administrative assessment 306,791 — — — — — — — 306,791 307,497 Major Seminarian Program — — — — — — 189,631 — 189,631 174,805 Program support receipts 175,326 283,195 — — 65,785 — 77,038 — 601,344 599,597 Mission receipts — — — — — — 147,771 — 147,771 176,988

CENTRAL ADMINISTRATION FUNDS AND DIOCESAN CEMETERY OPERATIONS WITHIN THE DIOCESE OF PROVIDENCE

Combining Statements of Activities and Changes in Net Assets

Year ended June 30, 2009 (with comparative totals for the year ended June 30, 2008)

Catholic General Charity Vision Fiduciary Endowment Plant Total Total Fund Fund Cemetery of Hope Other Fund Fund Fund 2009 2008

See independent auditors’ report on other financial information and accompanying note.

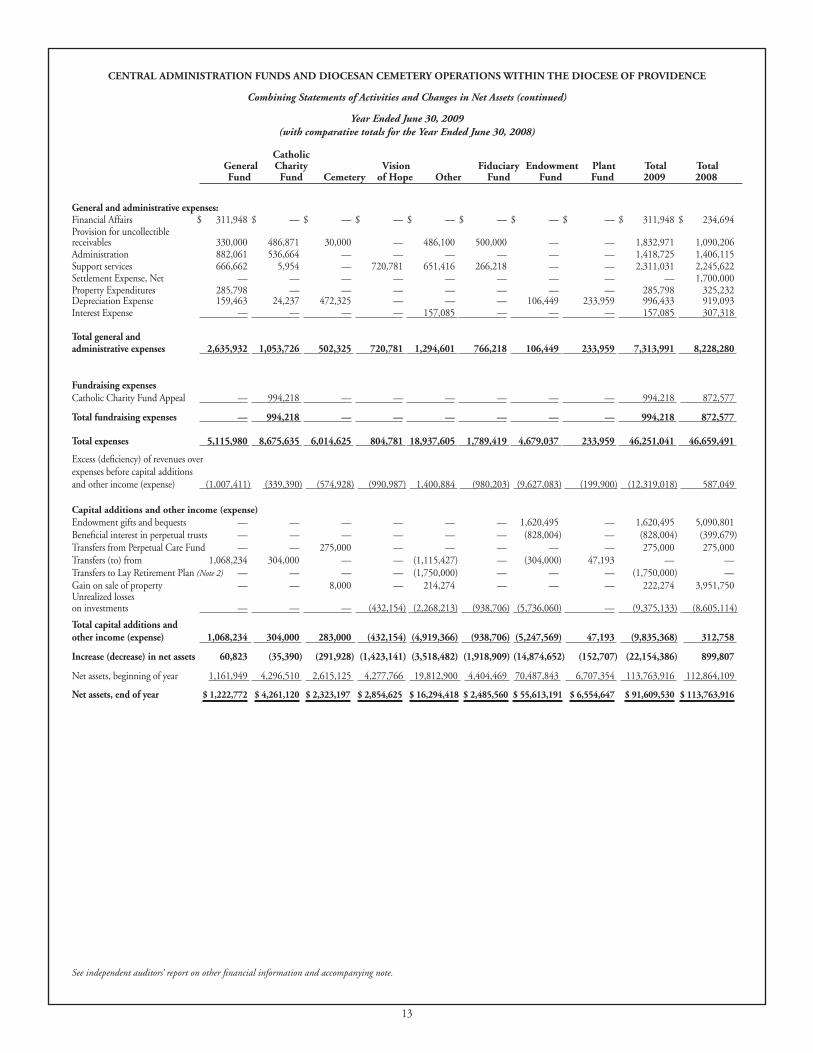

13

General and administrative expenses: Financial Affairs $ 311,948 $ — $ — $ — $ — $ — $ — $ — $ 311,948 $ 234,694 Provision for uncollectible receivables 330,000 486,871 30,000 — 486,100 500,000 — — 1,832,971 1,090,206 Administration 882,061 536,664 — — — — — — 1,418,725 1,406,115 Support services 666,662 5,954 — 720,781 651,416 266,218 — — 2,311,031 2,245,622 Settlement Expense, Net — — — — — — — — — 1,700,000 Property Expenditures 285,798 — — — — — — — 285,798 325,232 Depreciation Expense 159,463 24,237 472,325 — — — 106,449 233,959 996,433 919,093 Interest Expense — — — — 157,085 — — — 157,085 307,318

Total general andadministrative expenses 2,635,932 1,053,726 502,325 720,781 1,294,601 766,218 106,449 233,959 7,313,991 8,228,280

Fundraising expensesCatholic Charity Fund Appeal — 994,218 — — — — — — 994,218 872,577

Total fundraising expenses — 994,218 — — — — — — 994,218 872,577

Total expenses 5,115,980 8,675,635 6,014,625 804,781 18,937,605 1,789,419 4,679,037 233,959 46,251,041 46,659,491

Excess (deficiency) of revenues overexpenses before capital additions and other income (expense) (1,007,411) (339,390) (574,928) (990,987) 1,400,884 (980,203) (9,627,083) (199,900) (12,319,018) 587,049

Capital additions and other income (expense)

Endowment gifts and bequests — — — — — — 1,620,495 — 1,620,495 5,090,801 Beneficial interest in perpetual trusts — — — — — — (828,004) — (828,004) (399,679)Transfers from Perpetual Care Fund — — 275,000 — — — — — 275,000 275,000 Transfers (to) from 1,068,234 304,000 — — (1,115,427) — (304,000) 47,193 — —Transfers to Lay Retirement Plan (Note 2) — — — — (1,750,000) — — — (1,750,000) —Gain on sale of property — — 8,000 — 214,274 — — — 222,274 3,951,750 Unrealized losses on investments — — — (432,154) (2,268,213) (938,706) (5,736,060) — (9,375,133) (8,605,114)

Total capital additions andother income (expense) 1,068,234 304,000 283,000 (432,154) (4,919,366) (938,706) (5,247,569) 47,193 (9,835,368) 312,758

Increase (decrease) in net assets 60,823 (35,390) (291,928) (1,423,141) (3,518,482) (1,918,909) (14,874,652) (152,707) (22,154,386) 899,807

Net assets, beginning of year 1,161,949 4,296,510 2,615,125 4,277,766 19,812,900 4,404,469 70,487,843 6,707,354 113,763,916 112,864,109

Net assets, end of year $ 1,222,772 $ 4,261,120 $ 2,323,197 $ 2,854,625 $ 16,294,418 $ 2,485,560 $ 55,613,191 $ 6,554,647 $ 91,609,530 $ 113,763,916

CENTRAL ADMINISTRATION FUNDS AND DIOCESAN CEMETERY OPERATIONS WITHIN THE DIOCESE OF PROVIDENCE

Combining Statements of Activities and Changes in Net Assets (continued)

Year Ended June 30, 2009 (with comparative totals for the Year Ended June 30, 2008)

Catholic General Charity Vision Fiduciary Endowment Plant Total Total Fund Fund Cemetery of Hope Other Fund Fund Fund 2009 2008

See independent auditors’ report on other financial information and accompanying note.

14

The assets, liabilities, and net assets of the Central Administration Funds and Diocesan Cemetery Operations within the Diocese of Providence are reported in self-balancing fund groups as follows:

The General Fund records the daily unrestricted operating activities and its operations are part of the Diocesan Administration Corporation.

The Catholic Charity Fund raises funds that are used for the support of a broad range of community services and programs run by other organizations and entities.

The Cemetery Fund accounts for the operations of the Catholic Cemeteries.

The Vision of Hope Fund (VOH) records the donations received from and the support provided by a multi-year fund raising effort that was completed in 2003. The Capital Campaign will provide capital improvements for various parishes and institutions, establish endowments, and fund start-up costs for programs developed by the Diocesan Strategic Plan.

Other Funds: These Funds and a description of their operations follows:

The Insurance Funds are Board restricted for Diocesan insurance deductibles and for a partial self-insured workers’ compensation program for the parishes and various institutions, and for claims not covered by insurance policies.

The Diocesan Service Corporation, a separate legal entity, was established for the purposes of providing administrative, bookkeeping and other support services to various corporations organized to conduct temporal affairs for the Roman Catholic Church in the Diocese of Providence.

DiMed Corp. was established in fiscal year 2006 and is Board restricted for the operation of group healthcare programs for the various Parishes and Institutions.

Modernization and Support Fund and RCB are restricted by the Board to support the capital and contingent needs of DAC.

The Fiduciary Funds: These funds account for money received from other funds, parishes and institutions that are held in a Trustee capacity. These funds include:

The Loan Fund acts as a revolving loan fund for participating parishes and institutions. Loans are made for capital improvement needs and are funded by loans from parishes.

The Parish Investment Group represents assets of Parishes and Institutions which are in excess of short-term operating needs and are invested for the longer term in various managed equity and fixed income pools.

F.A.C.E. of Rhode Island established in fiscal year 2007, is the Diocesan Scholarship Granting Organization, which has been certified by the State Department of Taxation to receive from Rhode Island corpora-tions, tax credits which in turn will be used to support students who attend Catholic Schools.

The Endowment and Similar Funds: These represent funds that are subject to restrictions of gift instruments requiring that the principal be invested and the income only be used. They also include funds that are functioning as endowments and have been so designated by appropriate internal authority. These funds include:

Catholic Foundation, whose endowments are restricted to support specific parishes, Catholic education, certain agencies, programs, and services.

Seminary of Our Lady of Providence, whose endowment supports seminarians and vocation efforts.

The Mission Fund, whose endowment is used for the support of the missionary efforts of the Church of Providence.

Davey Trust holds a remainder trust, for which a final distribution was made in fiscal 2009.

The Cutting Trust holds an endowment for the Saint Clare Home, a separate corporation.

Effective June 2009, the Plant Fund now includes two funds, the RCB-Plant Fund and the Diocesan Plant Fund. The RCB-Plant Fund accounts for expenditures for land, buildings, furniture, and equipment used by the Central Administration Funds. The Diocesan Plant Fund is used to provide funding for future maintenance and repair of Diocesan Properties.

Prior to July 1, 1997, property, plant and equipment for the Funds, exclusive of Catholic Cemeteries, were accounted for in the Plant Fund. Subsequent to that date, all capital additions have been recorded in the specific funds that acquired them, along with the related depreciation expense for each period.

CENTRAL ADMINISTRATION FUNDS AND DIOCESAN CEMETERY OPERATIONS WITHIN THE DIOCESE OF PROVIDENCE

Note to Other Financial Information