colombia: fundamental tax reform · colombia: fundamental tax reform for companies with interests...

TRANSCRIPT

COLOMBIA: FUNDAMENTAL TAX REFORM

FOR COMPANIES WITH INTERESTS IN COLOMBIA

INDEX

Book-tax conformity for income tax purposes using IFRS as a starting point 3

New corporate income tax rate applies since January 1st 2017 4

Distribution of dividends is taxed in all cases 4

New regime for the tax depreciation and amortization of assets 5

Transitional regime for the depreciation and amortization of assets 6

New income tax rate for free trade zone (FTZ) users 7

Changes in the rules for the carry forward of net operating losses (NOL’s) 7

New nominal income tax rates for individuals 7

The general rate of VAT increases to 19% 8

Sale of intangible assets in connection with intellectual property is subject to

VAT 9

Vat withholding on e-commerce services rendered from abroad 9

Sale of new residential real estate is subject to VAT 10

Changes in the taxable period of VAT 10

Changes in withholding tax schedules for outbound payments 11

NEWSLETTER I JANUARY 2017

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 2/23

Colombia implements controlled foreign corporation rules taxing passive

income 12

Dian is authorized to issue a Special Notice of Deficiency to assess and settle

taxes and penalties 12

Changes in the statute of limitations for assessment and collection of tax

returns 13

A new method for computing interests on late payments was introduced with

the new regulation 14

Dian is now able to reach court settlements with taxpayers 14

Dian is now able to terminate administrative proceedings against taxpayers 15

The employment and Pay-Roll Tax Administration (UGPP) will be able to make

court settlements with the payers of mandatory contributions to the system 16

The employment and Pay-Roll Tax Administration (UGPP) is now able to

terminate administrative proceedings 16

The employment and Pay-Roll Tax Administration (UGPP) is now able to

terminate administrative proceedings 17

A new tax amnesty program was introduced regarding invalid Value Added Tax

(VAT) and withholding returns 17

Tax benefits for taxpayers that increase their investments on hydrocarbons

and mining exploration 18

Two new criminal offenses were introduced in connection with tax evasion 18

A new national registry will be created for entities wishing to access to the

special tax regime of non-for-profit organizations 19

Alternative method to determine unjustified equity increases of qualified

entities belonging to the special tax regime 19

Contracts with individuals related directly or indirectly to the non-for-profit

entity shall be registered before DIAN 20

New activities will be established for belonging to the special tax regime of

non-for-profit entities 20

Time limit for the investment in permanent assignments of non-for-profit

entities 20

Creation of the single tax for small retail business 21

New taxation for the consumption of plastic bags 21

New carbon tax 22

Arbitration awards and court rulings will be taxed if they have an economic

content 22

Changes to the industry and commerce tax (ICA) 23

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 3/23

BOOK-TAX CONFORMITY FOR INCOME TAX PURPOSES USING IFRS AS A STARTING

POINT

The recognition of income, costs and expenses as well as the determination of the value of

assets and liabilities shall be made under IFRS

As of January 1st 2017, assets, liabilities, income, costs and expenses of corporate

taxpayers and of individuals that are required to keep accounting records, will be

recognized in accordance with IFRS.

The new law includes some exceptions to the general rule of realization under IFRS for the

tax recognition of income, costs and expenses.

Such exceptions would generate temporary differences in tax accounting since their tax

recognition would be made in accordance with the specific rules indicated by the new

regulation, and not according to financial accounting.

In terms of income, the realization principle under IFRS will be subject to exceptions on

such topics as: income accrued from dividends, sale of real estate, financial transactions

that generate income from implicit interests, application of the equity method accounting

technique, measurement at fair value with changes in net income, reversals of provisions

associated with non-tax deductible liabilities, reversals of the accumulated impairment of

assets, and income that, in accordance with IFRS, shall be recorded in the other

comprehensive income (OCI).

Income, costs and expenses included in the OCI account shall be recognized for income

tax purposes if an item listed in OCI becomes a realized gain or loss, being shifted out of

OCI and into net income or loss, and when they are reclassified in the OCI against an

element of equity.

In terms of costs, the realization principle under IFRS will be subject to exceptions on such

topics as: costs generated by losses due to impairment of the partial value of the

inventory due to adjustments to net realizable value, acquisitions that generate implicit

interests, fair value measurements with changes in net income, provisions associated with

obligations of uncertain amount or date, labor liabilities where the labor obligation is not

yet consolidated, update of estimated liabilities or provisions, impairment of assets,

among others.

In terms of deductions, the realization principle under IFRS will be subject to exceptions

on such topics as: expenses arising from transactions that generate implicit interests, fair

value measurements with changes in net income, provisions associated with uncertain

amounts or date obligations, labor liabilities where the labor obligation is not consolidated

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 4/23

and liabilities, which, in accordance with the regulatory frameworks, must be recorded in

the OCI, among others.

Expenses that do not meet the requirements established in the tax regulations for being

tax deductible, would generate permanent differences between financial and tax

accounting. These expenses include deductions resulting from the application of the equity

method, taxes whose deductibility is not expressly authorized and taxes assumed by third

parties.

This new regulation was included in Articles 21-1, 59, 61, and 772-1 of Law 1819 of 2016.

NEW CORPORATE INCOME TAX RATE APPLIES SINCE JANUARY 1ST 2017

A surcharge to the income tax rate will apply for years 2017 and 2018. As from 2018 the

corporate income tax rate would be 33%

According to new Law 1819 of 2016, a transitional rate of 34% was established for the

corporate income tax for 2017. The general rate of 33% will apply from 2018 onwards. A

tax surcharge of 6% and 4% was implemented for those corporate taxpayers that receive

income exceeding COP $800.000.000 in 2017 and 2018, respectively.

This new regulation was included in Article 100 of Law 1819 of 2016.

DISTRIBUTION OF DIVIDENDS IS TAXED IN ALL CASES

The dividends tax rate is lower for foreign investors

From January 1st 2017, dividends distributed to Colombian individual tax residents will be

subject to taxation when they exceed approximately USD 6.000, at a progressive rate that

varies from 5% to 10%, if those dividends come from profits that were taxed at the

corporate level.

When dividends out of profits that were taxed at the corporate level are distributed to both

non-resident individuals and corporate entities, they will be subject to dividends tax

withholding at a rate of 5%.

The dividends distributed out of profits that were not taxed at the corporate level and that

are distributed to individuals tax residents in Colombia, will be subject to a progressive

income tax rate from 35% to 41.5%, depending on the value of the dividends. When

distributed to Colombian companies, these dividends will be subject to the general

corporate income tax.

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 5/23

Finally, the distribution of dividends to foreign entities and individuals, out of profits that

were not taxed at the corporate level, will be subject to an income tax rate of 38.25%

from January 1st 2017.

These changes were included in Article 7 of Law 1819 of 2016.

NEW REGIME FOR THE TAX DEPRECIATION AND AMORTIZATION OF ASSETS

The procedure for computing the depreciation and amortization of assets was modified

In order to update the tax regime to comply with the International Financial Reporting

Standards ("IFRS"), it was determined that depreciable and amortizable assets include the

following: (i) property, plant and equipment (PP&E); (ii) investment properties and (iii)

the intangible assets in the exploration and evaluation of non-renewable natural resources.

Terrains, movable assets and transferable securities will continue as non-depreciable

assets.

The depreciation methods are those established in the accounting technique, since a

reference is made to the IFRS for this purpose.

The depreciation rate to be used annually will be established according to the accounting

technique, but limits will be established by the Government. The maximum depreciation

rates will range from 2.22% to 33%.

An accelerated depreciation will be allowed, increasing the depreciation rate by 25% if the

depreciable asset is used daily for 16 hours and proportionally in higher fractions, provided

that this can be proved. This treatment does not apply to real estate.

The depreciation basis does not include the VAT paid in the acquisition or nationalization of

the asset, when it should have been treated as a discount or deduction in the income tax,

in VAT or when other tax deduction was granted.

In relation with the useful life, it was established that this will be the period during which

the asset is expected to grant future benefits to the taxpayer. Therefore, the depreciation

rate will not necessarily match with the financial depreciation rate. In any case, the useful

life chosen must be supported in technical studies, user guides or reports.

In relation with the amortization of intangibles, the deduction for amortization applies to

intangible assets subject to demerit, which, according to the accounting technique, should

be recognized as assets for their amortization. As a general rule, the depreciation method

will be determined in accordance with the accounting technique, but in any case the

annual aliquot cannot exceed 20% of the tax basis of the asset. In the event that the

intangible is acquired under a contract, the amortization will be made using the straight

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 6/23

line method for the duration of the contract, but in any case the annual rate cannot

exceed 20% of the tax basis of the asset.

Intangibles acquired separately or as part of a business acquisition, will only be amortized

if: (i) they have a defined useful life; (ii) can be reliably identified and measured in

accordance with the accounting technique; and (iii) its acquisition generated at the level of

the Colombian tax resident an income taxed in Colombia, or when the asset had been

acquired from an independent third party from abroad.

It is important to take into consideration that intangible assets acquired from related

parties, whether domestic or foreign, will not be amortized.

Finally, it was established that capital gains from goodwill will not be amortized.

TRANSITIONAL REGIME FOR THE DEPRECIATION AND AMORTIZATION OF ASSETS

A transitional regime was established in connection with the outstanding depreciation

balances

As a general rule, outstanding balances to be amortized will continue to be amortized using

the straight line method for a term of not less than 5 years, unless it is determined that due to

the nature or duration of the business, the amortization shall be made during a shorter period.

In relation with the depreciation, it was established that outstanding balances to be

depreciated until December 31, 2016, will be depreciated during the remaining fiscal useful life

of the asset, taking into account the applicable statutory useful life (20 years for real estate,

10 years for movable assets and other equipment and 5 years for motor vehicles and

computers). This can be used for straight-line systems, declining balances or other

depreciation methods of recognized technical value and duly authorized.

Finally, transitional regimes were established for the amortization of goodwill and intangibles

associated with concession contracts.

This treatment was regulated in Article 290 of Law 1819 of 2016.

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 7/23

NEW INCOME TAX RATE FOR FREE TRADE ZONE (FTZ) USERS

The income tax rate applicable in FTZ increases from January 1st 2017

The income tax rate for FTZ increases from January 1st to a flat rate of 20% for industrial

users and a transitional rate of 34% in 2017 and 33% in the following years for

commercial users.

Finally, users located in the new FTZ’s in Cucuta city, created between 2017 and 2019, are

exempted from the general rate of 20%, and subject of a 15% rate.

This regulation is included in Article 101 of Law 1819 of 2016.

CHANGES IN THE RULES FOR THE CARRY FORWARD OF NET OPERATING LOSSES

(NOL’S)

A transitional regime was included in Law 1819 allowing the carry forward of NOL’s

accrued before December 31 of 2016 without temporary or percentage limitations

A general limitation to carry forward NOL’s within the next twelve (12) taxable periods was

established. However, the carry forward of NOL’s accrued before December 31 2016 is

allowed without any temporary or percentage limitations.

This regulation is established in Articles 8 and 290 of Law 1819 of 2016.

NEW NOMINAL INCOME TAX RATES FOR INDIVIDUALS

New income tax rates for individuals depend on the category of income they receive: labor

and pension income, non-labor income and income from dividends and shares

For the category of labor and pensions income, 4 progressive rates were implemented

which range from 0% to 33%, as well as 4 withholding tax rates, from 0% to 33%.

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 8/23

Rates for individuals in the labor and pension income category:

Rates

Ranges on Tax Units Marginal Rate

From Until

>0 1.090 0%

>1.090 1.700 19%

>1.700 4.100 28%

>4.100 Hereafter 33%

Withholding tax rates for the labor and pension income category:

Rates

Ranges on Tax Units Marginal Rate

From Until

>0 95 0%

>95 150 19%

>150 360 28%

>360 Hereafter 33%

It should be mentioned that the non-labor income category is taxed with a progressive

rate that goes up to 35%.

In the category of dividends, when dividends are distributed out of profits that were not

taxed at the corporate level, they will be subject to withholding at a rate of 35%. The net

dividend after subtracting this tax will be taxed again at a progressive rate from 0% to

10%.

Dividends out of profit that were taxed at a corporate level received by individuals’ tax

residents in Colombia will be subject to withholding at a rate of up to 10%.

This regime is regulated in articles 5, 6 and 7 of Law 1819 of 2016.

THE GENERAL RATE OF VAT INCREASES TO 19%

From January 1st 2017 the general rate of VAT will increase to 19%, partly destined for

the financing of health and education programs. A transitional regime for the sale of goods

and services to the public is established

Regarding 1% of the increase in the VAT rate, 0.5 points will be destined to the financing

of the insurance under the General System of Health Social Security. The remaining 0.5

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 9/23

points are destined for the education budget. 40% of these revenues are to be assigned to

the financing of public higher education.

Law 1819 established a transitional regime for the application of the increase in the VAT

rate. This regime applies only to businesses that sell pre-marked merchandise. This

merchandise can be sold with the pre-marked price, while supplies last. In any case, from

February 1st of 2017, business shall use the new VAT rate.

The new VAT rate can be found in Article 184, and the transitional regime in article 198, of

Law 1819 of 2017.

SALE OF INTANGIBLE ASSETS IN CONNECTION WITH INTELLECTUAL PROPERTY IS

SUBJECT TO VAT

The sale of intangible assets associated with industrial property will be taxed at a rate of

19%

Previously, the applicable law determined that transactions with intangible assets (patents,

trademarks, software etc.) were not subject to VAT if the operation was made within

Colombia.

Law 1819 included within the goods subject to a 19% VAT, the sale or transfer of

intangible assets associated with industrial property.

Intangibles acquired or licensed from foreign entities, shall be deemed as acquired or

licensed in Colombia, as long as their user or recipient is a tax resident in Colombia. This

same rule applies for the services provided from abroad for users or recipients that are tax

residents in Colombia.

The foregoing is regulated in Article 173 of Law 1819 of 2016.

VAT WITHHOLDING ON E-COMMERCE SERVICES RENDERED FROM ABROAD

A VAT withholding system for electronic or digital services rendered from abroad was

implemented

Credit and debit card issuers, prepaid card vendors, third party cash collectors, and

others, at the time of payment to suppliers from abroad, must withhold VAT, for the

following electronic or digital services:

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 10/23

Provision of audiovisual services (among others, music, videos, movies and games

of any kind, as well as broadcasting of any event);

Service of platform distribution of mobile applications;

Provision of advertising services online;

Supply of distance education or training

Law 1819 provides that this withholding system will enter into effect within 18 months

after the law enters into force. DIAN will indicate through a Resolution, the list of foreign

providers that will be subject to the VAT withholding.

The VAT withholding is contemplated in Article 180 of Law 1819 of 2016.

SALE OF NEW RESIDENTIAL REAL ESTATE IS SUBJECT TO VAT

The first sale of new residential real estate will be subject to 5% VAT

Law 1819 determined that the sale of new residential real estate worth more than 26.800

UVT (COP$ 797.380.400) would be subject to a 5% VAT. The sale of real estate through

the assignment of trust rights will also be taxed accordingly.

The sale of residential real estate by means of a pre-sale contract, purchase deed or

similar document signed before December 31 of 2017, certified by a public notary, is

excluded from this tax.

This change is included in Article 185 of Law 1819 of 2016.

CHANGES IN THE TAXABLE PERIOD OF VAT

The reform reduces the different VAT taxable periods to two: bi-monthly and quarterly

VAT returns used to have a bi-monthly, quarterly or annual periodicity.

Trying to decrease the problems in relation with the multiplicity of taxable periods of VAT,

the tax reform reduced these taxable periods into the following two:

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 11/23

Bi-monthly returns, for taxpayers whose income exceeds 92.000 UVT (COP

$2.737.276.000).

Quarterly returns, for taxpayers whose incomes the previous year, did not exceed

92.000 UVT (COP $2.737.276.000).

This change is regulated in Article 196 of Law 1819 of 2016.

CHANGES IN WITHHOLDING TAX SCHEDULES FOR OUTBOUND PAYMENTS

The approved tax reform unifies withholding tax rates, creates a new withholding tax rate

for capital gains, and subjects new outbound payments to taxation

In general, the outbound payment of fees, royalties, personal service payments, is to be

subject to a 15% withholding tax. This results in a reduction from the 33% rate that applied

until December 31st 2016.

With regards to interest payments, the 15% withholding tax will apply regardless of the

maturity period of the loan. Under the amended provision, withholding on outbound interests

payments depended on the maturity of the loan, i.e. short-term (less than a year) was

subject to 33% and long-term (more than a year) was subject to 14%.

The withholding tax rate applicable to consulting, technical services and technical assistance

services rendered from abroad to a Colombian resident was increased from 10% to 15%.

A 15% withholding tax rate is established for payments made to foreign parent companies

for administrative or direction services, regardless of whether the income derived is

domestic or foreign-sourced income. Previously, these payments were not subject to

withholding tax when they were rendered in or from abroad.

The withholding tax for payments related to cinema exploitation was reduced to 15%.

The withholding tax for payments related to the exploitation of computer programs was

maintained at 26.4%.

The withholding on items of income subject to long term capital gains treatment was lowered

from 14% to 10%.

Lastly, the default rate for outbound payments was amended from 14% to 15%.

These changes were included in Articles 126, 127, 128 and 129 of Law 1819 of 2016.

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 12/23

COLOMBIA IMPLEMENTS CONTROLLED FOREIGN CORPORATION RULES TAXING

PASSIVE INCOME

Passive income obtained through foreign investment vehicles is now subject to taxation in

Colombia in head of the Colombian controller

The approved law includes an anti-deferral regime for the Controlled Foreign Corporations

(“CFC”), which establishes that domestic corporations and Colombian tax residents that

hold, directly or indirectly, a share percentage equal or greater to 10% of the total equity

of the CFC, shall compute in their income tax return the passive income obtained by such

CFC. The passive income assigned to the Colombian taxpayer is the amount resulting from

deducting out of the passive income the total costs and deductions associated with such

income.

CFC’s are those entities that:

1. Are controlled by one or more Colombian tax residents, according to the terms in

the new legislation,

2. Do not have their tax residency in Colombia.

CFC’s include investment vehicles such as corporations, trusts, collective investment

funds, other fiduciary businesses and private interest foundations, incorporated with

operation or domiciled abroad, regardless if they are considered to be legal entities or not,

or if they are disregarded for tax purposes or not.

If the passive income of the CFC represents 80% or more of the total income, it will be

legally presumed that its total income, costs and deductions will generate passive income

subject to taxation for the controllers.

A list of items of income that are considered passive income is included, including

dividends, interests, income derived from intangibles assets, income derived from the sale

of assets that generate passive income, real estate lease income, amongst others.

This new regime is established in article 139 of law 1819 of 2016.

DIAN IS AUTHORIZED TO ISSUE A SPECIAL NOTICE OF DEFICIENCY TO ASSESS AND

SETTLE TAXES AND PENALTIES

Introduction of a new Special Notice of Deficiency

A new procedure to settle tax obligations called the Special Notice of Deficiency, by which

DIAN may determine and settle taxes, levies, surcharges, advance payments and

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 13/23

withholdings that are delinquent or were filed after their due date, as well as unpaid

penalties, was introduced in the new regulation.

The Special Notice of Deficiency may only be issued by the Administration, over the same

tax return, before the statute of limitation elapses or within five (5) years from the due date

of the a delinquent return.

Such Special Notice of Deficiency would replace the Official Assessment, Statement of

Objections, or the previous notification, as long as the Administration ratifies it.

Regarding the statute of limitations of the tax returns filed as a consequence of accepting

the Special Notice of Deficiency, the term will be six (6) moths after their filing. For these

returns to be valid, they will have to be in compliance with all the forms and conditions

stated in the Tax Code.

At the same time, the new regulation states that Tax Authority will consider that the

taxpayer accepted the Special Notice of Deficiency if they do not file an objection in the term

provided.

CHANGES IN THE STATUTE OF LIMITATIONS FOR ASSESSMENT AND COLLECTION OF

TAX RETURNS

The Tax Administration now has broader terms to exercise its audit powers over taxpayers

The new regulation extended the statute of limitation from two (2) years to three (3) years, computed since:

The due date to file the tax return;

The filing date of the tax return, when it was filed extemporaneously;

The date of the request for a balance in favor; and

The use of the balance in favor in subsequent tax periods.

In the same way, the new tax regulation extended the statute of limitation of the tax returns that report NOL’s from five (5) years to six (6) years since the submission date. For taxpayers obliged to file transfer pricing returns, the statute of limitation will be six (6)

years since the due date, or the submission date, in the cases in which it was submitted extemporaneously.

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 14/23

A NEW METHOD FOR COMPUTING INTERESTS ON LATE PAYMENTS WAS

INTRODUCED WITH THE NEW REGULATION

The new method to calculate the interest in arrears will depend on the rate certified by the

Financial Superintendence for consumer credit

Previously, the interest rate for late payments was determined according to the

benchmark nominal interest rate defined by the Financial Superintendence of Colombia.

Now the interest rate on late payments will be the interest rate determined by the

Financial Superintendence of Colombia for consumer credit, subtracting 2 points from it.

DIAN IS NOW ABLE TO REACH COURT SETTLEMENTS WITH TAXPAYERS

The preferential treatment will apply until the 30th of September of 2017

Taxpayers, withholding agents, customs users and persons subject to foreign exchange

penalties are now able to make court settlements with the Colombian Tax Authority

according to the following criteria:

Lower Court Instances: If the judicial process is being reviewed by a Lower Court

Instance, the Tax Administration can negotiate a settlement with the taxpayer, by lowering

80% of the penalties, interests on late payments, and price-level restatements. This

settlement will be valid only if the taxpayer pays in full all the taxes, duties or levies being

discussed in Court, and 20% of the penalties, interests on late payments, and price-level

restatements determined by the Tax Authority.

Higher Court Instances: If the judicial process is being reviewed by a Higher Court

Instance, the Tax Administration can settle with the taxpayer, by lowering 70% of the

penalties, interests on late payments, and price-level restatements. This settlement will be

valid only if the taxpayer pays in full all the taxes, duties or levies being discussed in Court,

and 30% of the penalties, interests on late payments, and price-level restatements

determined by the Tax Authority.

No taxes, duties or regional levies: When the trial is determining the validity of a penalty

imposed by the Tax Authority to the taxpayer, but no taxes, duties or levies are being

discussed, the settlement made with the taxpayer can reduce up to 50% the penalties

imposed to the taxpayer. For that, the taxpayer will have to pay 50% of the penalties

determined by the Tax Authority prior to the Court trial.

Tax refunds and tax credits: When tax refunds and tax credits are being discussed in

trial, the Tax Authority will be able to settle for the 50% of the penalties imposed to the

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 15/23

taxpayer, only if the last one reimburses 100% of the taxes that were refunded or credited

prior to the Court trial.

The settlement request should be submitted to the Tax Authority before the 30 th of

September of 2017 and the Tax Authority will only be able to settle court trials in which

the lawsuit was submitted by the taxpayer before entrance into force of this regulation.

DIAN IS NOW ABLE TO TERMINATE ADMINISTRATIVE PROCEEDINGS AGAINST

TAXPAYERS

The preferential treatment will apply until the 30th of September of 2017

The Tax Authority is able to terminate administrative proceedings that were notified to the

taxpayers, customs users, or persons subject to foreign exchange penalties (“taxpayers”).

The termination will proceed only if the taxpayer complies with the following conditions:

If the taxpayer pays in full all the taxes, duties or levies and 70% of the penalties

and of the interest on late payments that are being assessed in the administrative

procedure, the Tax Authority will have to terminate it.

If the administrative procedure is not assessing taxes, duties or levies, the Tax

Authority will have to terminate the procedure once the taxpayer pays 50% of the

penalty imposed.

If the administrative procedure is assessing a non-filling penalty, the Tax Authority

will have to terminate it once the taxpayer pays 30% of the penalties and of the

interest on late payments and 100% of the assessed taxes, duties or levies.

When tax refunds or tax credits are being discussed in the administrative

proceeding, the tax Authority will have to terminate it once the taxpayer

reimburses 100% of the taxes that were refunded or credited and pays 50% of the

penalties imposed within the proceeding.

The request to terminate the administrative procedure should be submitted to the Tax

Authority by the taxpayer, before the 30th of October of 2017.

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 16/23

THE EMPLOYMENT AND PAY-ROLL TAX ADMINISTRATION (UGPP) WILL BE ABLE TO

MAKE COURT SETTLEMENTS WITH THE PAYERS OF MANDATORY CONTRIBUTIONS TO

THE SYSTEM

The payroll taxpayers will be able to make court settlements to terminate judicial

processes

The new Law 1819 established the following criteria:

Lower Court Instances: If the judicial process is being reviewed by a Lower Court

Instance, the UGPP can settle with the payer, by lowering 30% of the penalties, interests

on late payments, and price-level restatements. This settlement will be valid only if the

payer pays in full all the mandatory contributions being disputed, 100% of the interests on

late payments and 70% penalties, interests on late payments, and price-level restatements

regarding the rest of the contributions.

Higher Court Instances: If the judicial process is being reviewed by a Higher Court

Instance, the UGPP can settle with the payer, by lowering 20% of the penalties, interests

on late payments, and price-level restatements. This settlement will be valid only if the

payer pays in full all the mandatory contributions being disputed, 100% of the interests on

late payments regarding retirement contributions and 80% penalties, interests on late

payments, and price-level restatements regarding the rest of the contributions.

Penalties: When the procedure is determining the validity of a penalty imposed by the

UGPP, but no mandatory contributions are being discussed, the settlement made with the

payer can reduce up to 50% the penalties imposed to the taxpayer. For that, the payer will

have to pay 50% of the penalties determined by the UGPP prior to the Court trial.

THE EMPLOYMENT AND PAY-ROLL TAX ADMINISTRATION (UGPP) IS NOW ABLE TO

TERMINATE ADMINISTRATIVE PROCEEDINGS

The UGPP will be able to terminate administrative proceedings that are currently in

progress regarding contributions, penalties, interests on late payments, and price-level

restatements

The taxpayer will be subject to the termination if it complies with the following

requirements:

In the proceedings regarding the determination of mandatory contributions, the UGPP will

terminate them once the taxpayer pays in full the mandatory contribution that was

determined, 100% of the interests on late payments regarding retirement contributions,

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 17/23

20% of the interests on late payments regarding the other mandatory contributions and

80% of the penalties.

If the administrative proceeding is determining a non-filling penalty, and the taxpayer pays

10% of the penalty, the UGPP will wave 90% of the total penalty amount.

THE EMPLOYMENT AND PAY-ROLL TAX ADMINISTRATION (UGPP) IS NOW ABLE TO

TERMINATE ADMINISTRATIVE PROCEEDINGS

The UGPP will be able to terminate administrative proceedings that are currently in

progress regarding contributions, penalties, interests on late payments, and price-level

restatements

The taxpayer will be subject to the termination if it complies with the following

requirements:

In the proceedings regarding the determination of mandatory contributions, the UGPP will

terminate them once the taxpayer pays in full the mandatory contribution that was

determined, 100% of the interests on late payments regarding retirement contributions,

20% of the interests on late payments regarding the other mandatory contributions and

80% of the penalties.

If the administrative proceeding is determining a non-filling penalty, and the taxpayer pays

10% of the penalty, the UGPP will wave 90% of the total penalty amount.

A NEW TAX AMNESTY PROGRAM WAS INTRODUCED REGARDING INVALID VALUE

ADDED TAX (VAT) AND WITHHOLDING RETURNS

This benefit applies until the 30th of November of 2016

Taxpayers will be able to file again invalid VAT returns until the 30 th of November of 2016

without having to compute penalties or late payment interests.

This benefit is also applicable to withholding tax returns.

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 18/23

TAX BENEFITS FOR TAXPAYERS THAT INCREASE THEIR INVESTMENTS ON

HYDROCARBONS AND MINING EXPLORATION

A Tax Reimbursement Certificate (CERT) will be granted to these taxpayers

This benefit will only be granted if the increase in the investment is directed to:

Discovering new hydrocarbons reservoirs, adding confirmed oil reserves or incorporating

new recoverable reserves.

Maintaining or increasing the mining production of the current mining projects and

accelerating projects that not being currently exploited (making the step from the

construction or assembly phase to mining).

TWO NEW CRIMINAL OFFENSES WERE INTRODUCED IN CONNECTION WITH TAX

EVASION

The criminal offenses are related with the failure to report assets or the inclusion of non-

existent liabilities and the failure to pay withheld taxes

The Tax Reform creates the so-called "Criminal Offenses Against the Tax Administration".

The criminal offense related with the failure to report assets or the inclusion of non-

existent liabilities punishes those taxpayers which intentionally omit assets or report

inaccurate information in relation to the assets, or who report non-existent liabilities, for a

value equal to or greater than seven thousand two hundred and fifty (7,250) minimum

legal monthly wages. This behavior will be subject to incarceration for a term of forty-

eight (48) up to one hundred and eight (108) months and a fine of twenty percent (20%)

of the value of the unreported assets, the value of the asset inaccurately reported or of

the value of the non-existent liability.

The criminal offense regarding the omission of duties as withholding agent punishes those

withholding agents or self-withholding taxpayers that do not pay before the Tax

Administration the withheld taxes within 2 months following the date set by the National

Government. The penalty established is incarceration from forty-eight (48) to one hundred

and eight (108) months and a fine equal to twice the un-paid amount without exceeding

the equivalent of one million twenty thousand (1,020,000) Tax Value Units. This same

sanction will be applied to those VAT or National Consumption Taxpayers that, having a

legal obligation to do so, do not pay the amounts collected in connection with those taxes

within two (2) months following the date set by the National Government.

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 19/23

With regards to both criminal offenses, there is a possibility of extinguishing the criminal

action if the taxpayer files or amends the corresponding tax return and makes the

applicable payments.

These changes were included in Articles 338 and 339 of Law 1819 of 2016.

A NEW NATIONAL REGISTRY WILL BE CREATED FOR ENTITIES WISHING TO ACCESS

TO THE SPECIAL TAX REGIME OF NON-FOR-PROFIT ORGANIZATIONS

Entities should seek to qualify before DIAN in order to apply the special tax regime, and

also must fulfill new reporting obligations online and before the Chamber of Commerce

All entities that wish to belong to the special tax regime, must file an application so as to

be qualified by DIAN. If such authorization is denied, the entity will be deemed as a

corporation for tax purposes.

The entities that at December 31st of 2016 were part of the special tax regime will remain

as such if they comply with the requirements for doing so.

Those legally incorporated non-for-profit organizations that as of January 1, 2017 were

considered as taxpayers of the ordinary income tax regime that were eligible for filing

their application to the special tax regime, are automatically admitted and qualified in it.

In those cases in which it is decided to modify the quality of the entity, an administrative

act shall be issued no later than October 31, 2018.

These regulations are included in Article 140 and 148 of Law 1819 of 2016.

ALTERNATIVE METHOD TO DETERMINE UNJUSTIFIED EQUITY INCREASES OF

QUALIFIED ENTITIES BELONGING TO THE SPECIAL TAX REGIME

Entities that are part of the special tax regime will be subject of the income tax

determination mechanism by equity comparison

The income mechanism by equity comparison will be applied to quantify differences in the

behavior of the surplus net benefits between taxable periods. In case that the difference is

unjustified, a taxable income will be triggered for the qualified entity.

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 20/23

CONTRACTS WITH INDIVIDUALS RELATED DIRECTLY OR INDIRECTLY TO THE NON-

FOR-PROFIT ENTITY SHALL BE REGISTERED BEFORE DIAN

Contracts with founders, managers, donors, family members among others, which own

more than 30% of the entity, shall be registered

All payments or execution of contracts, whether free of charge or not, made in favor of

founders, managers, donors, family members among others, which own more than 30% of

the entity, will be considered as an indirect distribution of profits and will have as

consequence the exclusion of the entity from the special tax regime.

All contracts or legal acts entered into with the founders, donors, managers or their relatives

who own more than 30% of the entity must be registered with DIAN. The Tax Administration

will determine if the contract constitutes an indirect distribution of profits, and if so, the

entity will be excluded from the special tax regime.

The indirect distribution of profits and remuneration of the management positions of

taxpayers to the special tax regime is contemplated in Article 147 of Law 1819 of 2016.

NEW ACTIVITIES WILL BE ESTABLISHED FOR BELONGING TO THE SPECIAL TAX

REGIME OF NON-FOR-PROFIT ENTITIES

The list of activities subject to the special tax regime is extended to new activities

The new activities covered by the special tax regime include the protection of the

environment, the prevention on the consumption of psychoactive substances, the

promotion of sport activities, the religious freedom, the economy development, the

promotion of the improvement of the justice administration and the execution of funds

deriving from international cooperation of foreign non-profit entities.

TIME LIMIT FOR THE INVESTMENT IN PERMANENT ASSIGNMENTS OF NON-FOR-

PROFIT ENTITIES

A limit of 5 years applies. New assets can be acquired with these assignments, as long as

they are destined to the development of the meritorious activity

When an investment program is being implemented whose execution requires additional

terms or new permanent allocations, an authorization by the General Assembly or

governing body of the entity will be required. However, permanent assignments may not

have a term of more than five (5) years.

With permanent assignments, new assets can be acquired, as long as they are destined to

the development of meritorious activity. However, the profits acquired with the permanent

assignments must be destined to the development of the social object of the entities.

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 21/23

This treatment is regulated in Article 153 of Law 1819 of 2016.

CREATION OF THE SINGLE TAX FOR SMALL RETAIL BUSINESS

The single tax for small retail business was created in order to promote formal business

and facilitate the compliance with the tax obligations

The single tax seeks to replace the income tax for individuals who obtain their income

from informal activities (retail or hairdressing) and who voluntarily subject themselves to

the regime of this new tax. The objective of this tax is to establish more beneficial rates

and a simpler system for taxpayers.

The taxpayers of the single tax are individuals who meet the following conditions:

Have gross income, in the taxable year, equal or above 1400 UVT (COP$

44,604,000) and less than 3500 UVT (COP$ 111,510,000)

To carry out their economic activity in an establishment with an area of less than

50 square meters.

Be eligible to receive the Social Service of Supplemental Periodic Economic Benefits

-BEPS.

Carry out as an economic activity in the field of retail or hairdressing as well as

other beauty treatments.

The amount to be paid will depend on the gross income of the taxpayer, according to the

categories defined in the law.

The single tax is included in Article 165 of Law 1819 of 2016.

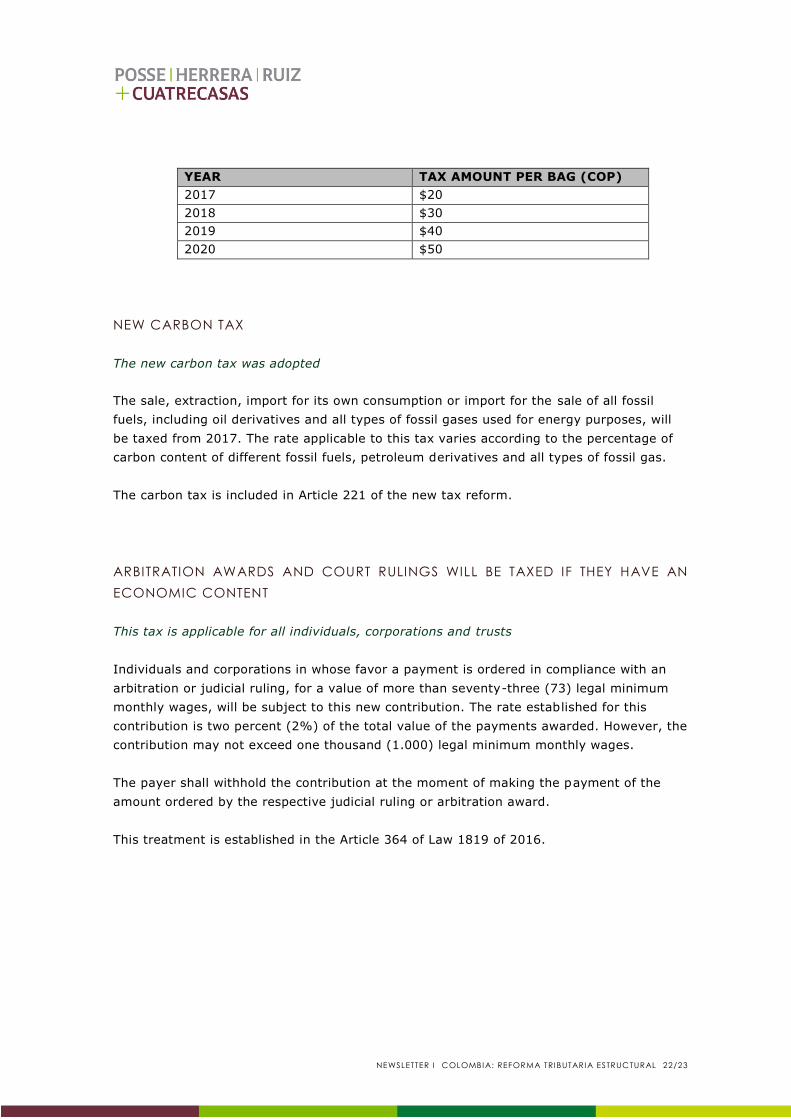

NEW TAXATION FOR THE CONSUMPTION OF PLASTIC BAGS

From the 1st of July of 2017, the use of plastic bags to carry items that were purchased in

stores or other retail business will be subject to this new tax.

Persons that use plastic bags to carry products purchased in any kind of businesses,

including the bags used for their delivery, will be charged with this new tax according to

the following chart:

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 22/23

YEAR TAX AMOUNT PER BAG (COP)

2017 $20

2018 $30

2019 $40

2020 $50

NEW CARBON TAX

The new carbon tax was adopted

The sale, extraction, import for its own consumption or import for the sale of all fossil

fuels, including oil derivatives and all types of fossil gases used for energy purposes, will

be taxed from 2017. The rate applicable to this tax varies according to the percentage of

carbon content of different fossil fuels, petroleum derivatives and all types of fossil gas.

The carbon tax is included in Article 221 of the new tax reform.

ARBITRATION AWARDS AND COURT RULINGS WILL BE TAXED IF THEY HAVE AN

ECONOMIC CONTENT

This tax is applicable for all individuals, corporations and trusts

Individuals and corporations in whose favor a payment is ordered in compliance with an

arbitration or judicial ruling, for a value of more than seventy-three (73) legal minimum

monthly wages, will be subject to this new contribution. The rate established for this

contribution is two percent (2%) of the total value of the payments awarded. However, the

contribution may not exceed one thousand (1.000) legal minimum monthly wages.

The payer shall withhold the contribution at the moment of making the payment of the

amount ordered by the respective judicial ruling or arbitration award.

This treatment is established in the Article 364 of Law 1819 of 2016.

NEWSLETTER I COLOMBIA: REFORMA TRIBUTARIA ESTRUCTURAL 23/23

CHANGES TO THE INDUSTRY AND COMMERCE TAX (ICA)

The new regulation included a description of the service activities subject to the tax

These activities should include all the services, activities, or labors executed by an

individual or a corporation, outside of a labor relationship or contract between the parties,

regardless of the predominance of the material or intellectual content of the activity.

The new regulation also included a new criterion for determining the territoriality for

“investment” activities. All income perceived from businesses wi ll be taxed by the city

where the business or corporation is located. This means that the dividends perceived by

Colombian holding entities will be subject to ICA tax.

This treatment is established in Article 343 of Law 1819 of 2016.

© 2017 CUATRECASAS. All rights reserved.

This document contains legal information prepared by Cuatrecasas. This information does not constitute legal advice.

Cuatrecasas owns the intellectual property rights to this document. Any reproduction, distribution, transfer or use of

this document, whether fully or partially, will require the prior consent of Cuatrecasas.