cognitive moral development and auditor independence 1997 accounting, organizations and society

TRANSCRIPT

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 1/16

ergamon

ACCWn ing Oganza ions

nd

Soce y

Vol. 22. No. 3/4, pp 337-352, 1997

\C 1997 Elsevier Science Ltd

All rights reserved. Printed in Great Britain

0361.3682/97 17.00+0.00

PII: SO361-3682(96)00025-6

COGNITIVE MORAL DEVELOPMENT AND AUDITOR INDEPENDENCE

JOHN T. SWEENEY

Un ive rsi t y o f M i ssou r i -Colu mb i a

and

ROBIN W. ROBERTS

I ow a S ta t e Un i ver si t y

bstract

This paper examines the influence of cognitive moral development on an auditor’s independence judg-

ments. Over three-hundred audit professionals participated in a field experiment in which they completed

a measure of mom1 development and responded to an ethical dilemma involving auditor independence.

The most significant findings are that an auditor’s level of moral development affected his or her sensitivity

to ethical issues and independence judgments. Additionally, the influence of the audit firm, partitioned by

size, moderated the moral development-independence relationship. U; 1997 Elsevier Science Ltd

The independence of financial statement audi-

tors has been the focus of recent investigations

by the Securities and Exchange Commission

(1994) and the Public Oversight Board of the

American Institute of Certified Public Accoun-

tants (POB, 1993, 1994). Recognizing that many

observers of the accounting profession view

the auditor as less than objective and indepen-

dent, the POB (1994, p. 4) concluded that the

“profession is at a critical juncture” in main-

taining the public trust.

The primary objective of this study is

to examine the influence of cognitive moral

development on

auditor

independence

judgments within the framework of a widely

accepted psychological model of ethical

behavior. We hypothesize that an auditor’s

level of moral development affects both

sensitivity to ethical issues in work-related

dilemmas and independence judgments. We

also hypothesize that the effectiveness of

potential penalties imposed for nonindependent

behavior are dependent upon an individual’s

level of moral development. Furthermore, we

investigate the effect of firm size on auditor

independence judgments.

Prior research on auditor independence has

generally focused on the audit firm as the level

of analysis (DeAngelo, 1981a,b) or developed

formal analytical models of auditor indepen-

dence (Antle, 1984; Magee & Tseng, 1990).

Underlying both streams of research is the stated

assumption that auditors always act as rational,

economic agents. Accountants, however, often

find themselves in situations where conflict

exists between their economic self-interest and

what moral principles indicate ought to be

done (Gas, 1992, 1994). In fact, the definition

of independence embodied in the

Code of

P ro f e ss iona l Conduc t

(American Institute of

Certified Public Accountants, 1988, sec. 101,102)

requires auditors “to act against self-interest

The authors gratefully acknowledge the helpful comments of the research workshop participants at the University of

Missouri, Iowa State University, and the University of Kansas and also the contributions ofJere Francis, Larry Ponemon, Earl

Wilson, and two anonymous reviewers.

337

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 2/16

33x

J. T. SWEENEY and R. W ROBERTS

and ignore the various economic and social

incentives affecting them” (Ponemon & Gab-

hart, 1990, p. 221). More recently, accounting

researchers have begun to study whether or not

economic self-interest is a sufficient basis for

analyzing independence (Farmer

et a l .

1987;

Ponemon & Gabhart, 1990).

Ponemon & Gabhart (1990) examined the

relationship between moral development and

ethical decision making in the context of an

auditor independence dilemma. Their results

indicated that auditors with a relatively low

level of moral development were more likely to

believe a hypothetical auditor’s action was in

compliance with independence rulings and

were influenced to a greater extent by the

existence of a potential penalty than auditors

with a

relatively high level of moral

development. Windsor and Ashkanasy (1995)

found that when faced with strong economic

pressure from client management, an auditor’s

moral development may interact with personal

beliefs in affecting independence. Tsui & Gul

(1996) found that moral development moder-

ated the relationship between locus of control

and the auditor’s acquiescence

to client

management.

We extend the prior research on moral

development and auditor independence in sev-

eral ways. First, we examine the relationship

between an auditor’s level of moral devel-

opment and sensitivity to contextual ethical

factors when formulating an independence

judgment. Second, the relationship between

auditor independence and moral development

is explored in a richer context devoid of any

manifest economic incentives to violate profes-

sional rules. Third, we examine the influence of

the audit firm in moderating the relationship

between an auditor’s level of moral devel-

opment and independence judgment.

Utilizing a field experiment, we tested the

hypotheses with a sample of 312 auditors, from

staff through partner levels, at eight different

public accounting firms representing three

distinct size classifications. Our results indicate

that an auditor’s level of moral development

affects (1) sensitivity to ethical issues in an

audit context, (2) independence judgments,

and (3) the effectiveness of potential penalties

for violating independence standards. Further-

more, we find that auditors incorporate

contextual information when processing ethical

judgments and that auditors from different

sized public accounting firms in the United

States may hold differing beliefs or perceptions

regarding their independence with respect to

client management.

The remainder of the paper is organized as

follows. The second section provides a brief

background for the study and a description of

cognitive moral development theory. The

research hypotheses are presented in section

three and our methodology is explained in

section four. Data analysis and results are

discussed in section five, followed by our con-

clusions in section six.

MORAL DEVELOPMENT AND AUDITORS’

INDEPENDENCE JUDGMENTS

Moral development theory (Kohlberg, 1969;

Rest, 1979) attempts to explain the cognitive

framework underlying individual decision

making in the context of an ethical dilemma.

The objective of moral development theory is

not to classify a behavior as inherently right or

wrong, but rather to understand the cognitive

reasoning processes an individual follows

in resolving an ethical dilemma. Kohlberg’s

stage-sequence model (Kohlberg, 1969) identi-

fies a series of three qualitatively different levels

of individual cognitive moral development:

preconventional, conventional, and principled

or postconventional. Each level is composed of

two stages, with the second stage a more

advanced form of the general perspective. Indi-

viduals progress through these hierarchically

arranged levels in a sequential, irreversible pro

gression. An individual’s moral growth results

from exposure to more advanced forms of

moral judgment. The ensuing cognitive conflict

or disequilibrium produces tension, which

results in the individual attempting to reconcile

the contradiction.

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 3/16

COGNITIVE MORAL DEVELOPMENT AND AUDITOR INDEPENDENCE

339

The conventional level of moral development

is the level attained by the majority of public

accountants (Gaa, 1992; Ponemon & Gabhart,

1993; Sweeney, 1995) and adults in the general

population of the United States and most other

societies (Colby & Kohlberg, 1987; Rest, 1979).

The moral development of public accountants

has been associated with underreporting beha-

vior (Ponemon, 1992a), hiring and promotion

decisions in public accounting firms (Ponemon,

19926), selection of recognized alternative

actions when making ethical judgments (Lampe

& Finn, 1992), perceptions of client integrity

(Ponemon, 1993; Bernardi, 1994) and bias in

litigation support judgments (Ponemon, 1995).

An auditor whose moral development is

primarily at the preconventional level will

follow independence standards only when it is

in his or her immediate interest. An auditor

whose moral development is primarily at the

conventional level has a desire to maintain rules

and authority and will always be independent if’

such behavior is consistent with referent group

norms. The behavior of auditors who reason

primarily at the postconventional level will

conform with organizational and/or indep-

endence standards when such standards are

consistent with internally held beliefs @one-

mon & Gabhart, 1990, 1993, 1994). Gaa states

that postconventional reasoning “implies the

ability to move beyond the rules to decide

when rules ought to be broken, e.g., for the

welfare of society or because justice demands

it.“(Gaa, 1992, p. 35)

Under the Kohlbergian paradigm, moral

action is not defined simply by the conduct

exhibited; rather, moral actions involve an

internal or cognitive component. Consistent

with moral development theory, the motivation

leading to an auditor’s ethical behavior will be

dependent upon the individual’s level of moral

development (Ponemon, 1994).

HYPOTHESES

E t h i c a l sen s i t i v i t y a nd mo ra l j u d gmen t

Rest (1986) contends that in order for moral

behavior to occur, an individual must perform

at least four basic processes, which he refers to as

the “Four-Component Model.” In Component 1

an individual becomes aware of the existence

of an ethical issue and the possible alternative

courses of action. Component 2 occurs when

the individual then makes a judgment as to

what course of action is morally right. The next

step, Component 3, is the process whereby the

individual decides what he or she actually

intends to do by selecting among competing

values or goals. Component 4 involves imple-

menting and executing a plan of action.

Before an individual can behave morally, the

person must realize that an ethical problem

exists. Ethical sensitivity, or the awareness of an

individual to the ethical issues present in a

social context, is a prerequisite for assessing the

relationship between moral development and

action (Rest, 1986). Some research has indi-

cated that individuals with more advanced

moral development [Component

21

are more

sensitive to ethical issues [Component 11

(Bebeau

et a l .

1985; Ponemon & Gabhart,

1990; Ponemon, 1993; Bernardi,

1994X

although Shaub (1989) did not find a correla-

tion between auditors’ moral development and

their sensitivity to ethical issues.

Rest (1986) indicates that each type of situa-

tion contributes a specific variability in ethical

sensitivity, and that professional dilemmas are

usually a combination of technical and moral

issues. Investments by the accounting profes-

sion and by individual accounting firms in

socializing auditors to behave in accordance

with professional standards (Fogarty, 1992;

Lampe & Finn, 1992) may desensitize some

auditors to ethical issues beyond the scope of

technical rules. Ponemon contends that

“progression to higher stages of ethical reason-

ing fosters an individual’s sensitivity to critical

events, issues, and conflicts” (1993, p. 7) and

that auditors

“with higher ethical reasoning

capacities would have greater ethical sensitivity

to ethical conflict not well defined by the firm

or profession” (1992, p. 254). Auditors who

have developed the ability to reason at the

postconventional level will be less responsive

to referent group norms and more sensitive to

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 4/16

340

J. T. SWEENEY and R. W. ROBERTS

imbedded ethical issues when judging an ethi-

cal dilemma. The first hypothesis predicts a

positive relationship between an auditor’s

moral development and his or her sensitivity to

ethical issues.

Hl: Auditors at higher levels of moral development will

be more sensitive to ethical issues.

Before the relationship between moral devel-

opment and independence judgments can be

assessed, the auditor must be aware that ethical

issues are present <Ponemon, 1994). Hypo-

thesis Hl effectively acts as a control to ensure

that subjects are sensitive to imbedded ethical

issues. Rest maintains that professional educa-

tion conditions the individual “not to recognize

and deal with the moral aspects of the job”

(Rest, 1986, p. 23). Auditors who respond to

only the technical issues in a dilemma, without

recognizing imbedded ethical issues, are relying

solely upon their knowledge of professional

standards in resolving the dilemma and not

upon their moral judgment. Individuals demon-

strating evidence of ethical sensitivity are utilized

in testing the relationship between moral

development and independence judgments.

moral judgment (Ponemon & Gabhart, 1990;

Arnold & Ponemon, 1991). Moral development

theory predicts that auditors at the preconven-

tional level will be independent if the perceived

potential sanctions for

nonindependent

behavior exceed the potential benefits. Con-

ventional level auditors are expected to be less

responsive to potential penalties and more sen-

sitive to reference group norms and to uphold-

ing the independence standards of the firm

or profession. The independence judgment of

postconventional auditors is affected by con-

cerns relating to social welfare or principles of

justice and is uninfluenced by potential sanc-

tions. This leads to the following hypothesis:

H3: The independence judgments of auditors whose

moral development is primarily at the preconventional

level will be affected by the presence of potential

sanctions.

The influence of audit firm size on indepen

dence

After testing hypothesis Hl and determining

which subjects are sensitive to ethical issues,

the relationship between moral development

and independence judgments is evaluated in

the context of an independence dilemma.

Based on the prior discussions of cognitive

moral development theory and auditor inde-

pendence, the following hypothesis is posited

regarding the influence of moral development

on auditor independence:

HZ: An auditor’s Ievel of moral development affects his

or her independence judgments.

Effect of sanctions

DeAngelo (1981a) maintains that larger audit

firms will be more independent than smaller

firms because they have greater potential future

client revenues to lose from nonindependent

action. A large audit firm provides a larger bond

for its audit than a smaller firm (Watts &

Zimmerman, 1986) and would therefore have

greater incentives for ensuring a strong nor-

mative structure promoting independence.

Trevino (1986) maintains that in an organiza-

tional culture which has a strong normative

structure, there will be more agreement among

members about what is appropriate ethical

behavior. Loeb (1971) found a lower incidence

of unethical behavior in large audit firms, and

Palmrose (1988) reported that Big Eight firms,

as a group, engage in less audit litigation than

non-Big Eight firms.

The effectiveness of rules and punishments

DeAngelo’s “collateral bond” argument

promoting desirable independence behavior

(DeAngelo, 1981~) predicts a positive relation-

will depend upon the moral judgment pro- ship between audit firm size and independent

cesses of auditors (Ponemon & Gabhart, 1993,

auditor behavior. Support for her theory would

1994). The presence of a potential penalty for

be generated if audit firm size corresponds to

nonindependent behavior is more likely to

increased auditor independence. The following

influence auditors with relatively less developed hypothesis tests whether auditors from larger

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 5/16

COGNITIVE MORAL DEVELOPMENT AND AUDITOR INDEPENDENCE

341

firms are more independent, for a given client,

than auditors from smaller firms.

H4: Auditor independence is positively related to firm

size.

METHOD

Sub j ec ts an d procedu r es

As a prelude to the selection of auditing sub

jects, public accounting firms were partitioned

into three size categories: Big Six international

firms (“large”), national firms (“midsize”), and

local and regional firms (“small”). Three large

firms, two midsize firms, and three small firms

were contacted and agreed to provide auditor

subjects. The large and midsize firms each

provided subjects from two different office

locations.

Firms participating in the study provided a

representative responsible for the coordination

and administration of the study in each office

location. Office representatives estimated the

number of available participants at each posi-

tional level. As a result, a total of

490

research

instruments were delivered to office repre-

sentatives with instructions for administration.

Shortly after delivery of the research instru-

ments, office representatives were instructed to

prompt subjects to complete and return the

materials. The completed research instruments

were returned by the subjects, intact in a sealed

envelope, to the office representative who then

returned the envelopes to the researchers.

Each research instrument contained a hypo-

thetical case (appendix A), a questionnaire

attached to the case instrument, and the six-

story “Defining Issues Test” (DIT). All partici-

pants were provided with written instructions

and asked not to discuss the materials with co

workers. The research instruments were equally

partitioned prior to distribution by treatment

condition. Before delivering the research instru-

ments to each office representative, the cases

(enclosed in envelopes) were randomly inter-

spersed to provide assurance that assignment of

the experimental treatment was unbiased.

A total of 34 1 envelopes (approximately 70%)

containing the research instruments were

returned by the eight firms participating in the

study. Two subjects did not indicate a response

to the case, leaving 339 completed cases and

341 completed questionnaires. One subject

failed to include the DIT. From the group of

340 subjects returning the DIT, twenty-six

subjects were purged from the sample for

failure to pass the internal reliability checks,

leaving a sample 314 usable DITs.’ After dele-

tion of the two subjects who did not indicate a

response to the case, the sample of participants

who submitted a completed case and ques-

tionnaire along with a valid DIT was 312.

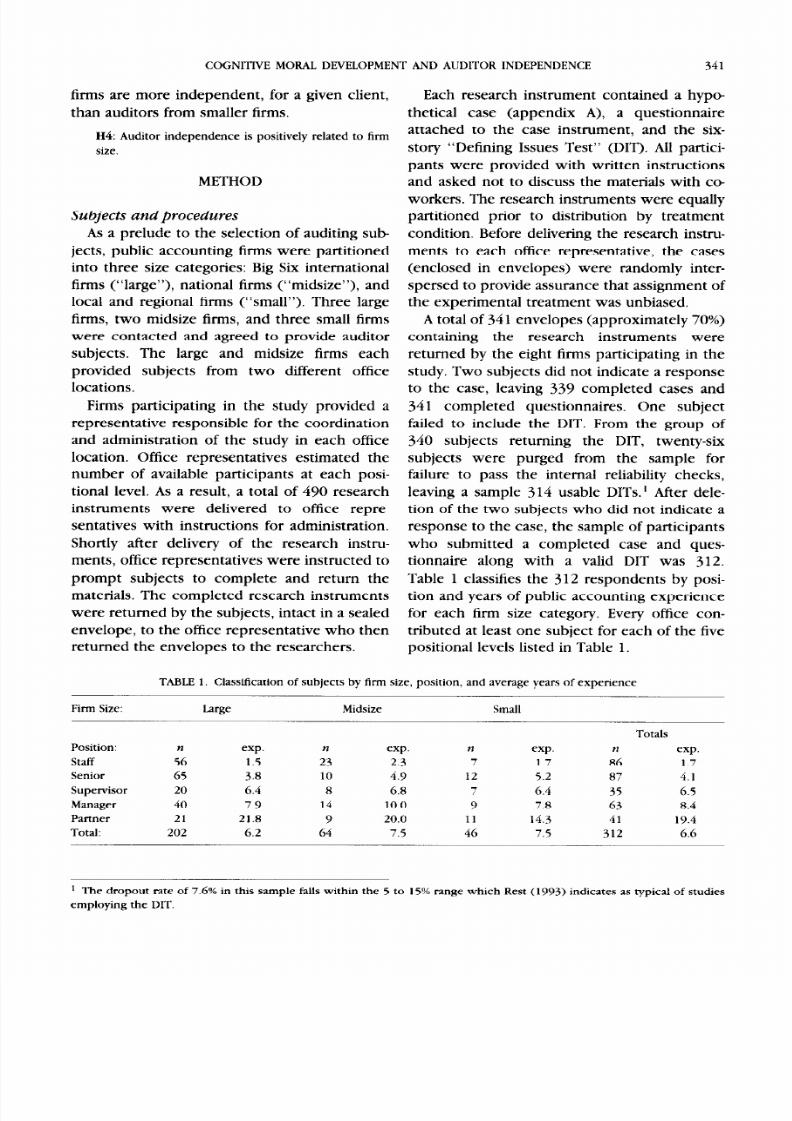

Table 1 classifies the 312 respondents by posi-

tion and years of public accounting experience

for each firm size category. Every office con-

tributed at least one subject for each of the five

positional levels listed in Table 1.

TABLE 1. Classification of subjects by firm size, position, and average years of experience

Firm Size: Large

Midsize Small

Position: n exp.

n exp. n exp.

staff 56 1.5 23 2.3

7 1.7

Senior 65 3.8 10 4.9

12 5.2

Supervisor 20 6.4 8 6.8

7 6.4

Manager 40 7.9 14 10.0

9 7.8

Partner 21 21.8 9 20.0

11 14.3

Total: 202 6.2 64 7.5

46 7.5

Totals

n exp.

86 1.7

87 4.1

35 6.5

63 8.4

41 19.4

312 6.6

’ The dropout rate of 7.6 in this sample falls within the 5 to 15 range which Rest (1993) indicates as typical of studies

employing the DIT.

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 6/16

342

J. T. SWEENEY and R. W. ROBERTS

Design and measurement of var i abl es

The design of this study is a 2 x3 x3, repre-

senting two levels of a sanction manipulation,

three levels of moral development, and three

levels of audit firm size as the independent

variables. Auditors’ independence judgments

served as the dependent variable. Auditors were

randomly assigned to one of the sanction con-

ditions, while the other independent variables

were measured. The moral development mea-

sure, auditor independence measure and sanc-

tion manipulation variable are discussed below.

Moral development was measured by the P

score value of the six-story version of Rest’s

Defining Issues Test (Rest, 1979, 1986). The

DIT is a structured, self-administered, objec-

tively scored instrument, which assesses a

person’s

moral development from forced-

choice responses to ethical dilemmas. The most

frequently used score from the DIT is the P

index (“P” for “principled”), which is inter-

preted as the relative importance that respon-

dents attributed to Stage 5 and 6 items. The

score is expressed in terms of a percentage and

can range from 0 to 95.’ While the P score is

based upon Stage 5 and 6 responses, Rest

(1979, p. 101) contends that the

P

score is the

appropriate indicator “for locating a subject

along the underlying developmental con-

tinuum.”

Rest (1986) reports an average P

score of 40.0 for American adults.

The DIT has been subject to extensive relia-

bility and validity studies (Rest, 1979, 1986, 1994;

Ponemon and Gabhart 1993). The P score of

the DIT (Rest, 1979, 1986) correlates only

weakly with gender, ethnic background, IQ,

and vocation variables. The strongest corre-

lation with moral judgments is years of formal

education, particularly with adult subjects (Rest

& Thoma, 1985).

Subjects were classified by

P

score into three

categories P Groups: (1) Low=under 27.6, (2)

Medium=27.6 to 41.5, and (3) High=41.6 and

above) for hypothesis testing. These partitions

are based on the theoretical P score ranges as

suggested by Rest (1993). The

P

groups are used

to proxy for the subjects’ predominant level

of moral development: Low=preconventional,

Medium=conventional, and High=postconven-

tional. Of the 312 respondents completing both

the case and the DIT, 175 were classified into

the High group, 107 into the Medium group,

and 30 into the Low group.

A case instrument (appendix A) was utilized in

conjunction with the DIT results to develop the

measures for testing hypotheses Hl through

H4. Some accounting researchers (DeAngelo,

198la; Antle, 1984; Magee & Tseng, 1990)

characterize independence behavior as moti-

vated by economic self-interest. Cushing, for

example, insists that

“auditor independence

cannot be fully understood except in an eco-

nomic context” (Cushing, 1990, p. 259). Thus,

in the absence of an economic motive for non-

independent behavior, auditors are always

expected to act independently. As noted

previously, this research effort takes the posi-

tion that independence is an ethical, as

opposed to an economic, concept (Gas, 1992,

p. 9; Ponemon & Gabhart, 1990, 1993). The

case, therefore, was crafted to insure that the

hypothetical auditor had no overt economic

incentives for violating professional indepen-

dence standards.

The vignette involves an independence

dilemma (acquiescence to the controller’s

request to conceal an irregularity)” and incor-

porates issues designed to appeal to the

perspectives of different levels of moral develop-

ment. For example: the sanction manipulation in

’ The P score is converted to a percentage by dividing the sum of the number of Stage 5 and 6 items by 60, the total ranking

that would occur if a subject selected only Stage 5 and 6 items for each dilemma. Because only three, not four, principled

items are present on three of the vignettes, the P percent has a maximum value of 95.

3 Independence “concerns an individual’s ability to act with integrity and objectivity” (AICPA, 1988). Rule 102 defines

integrity and objectivity, and requires that a member shall “be free of conflicts of interest, and shall not knowingly mis-

represent facts or subordinate his or her judgment to others.” Furthermore, SAS 60 requires an auditor to notify higher

levels of management if an irregularity is discovered, regardless of materiality

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 7/16

COGNITIVE MORAL DEVELOPMENT AND AUDITOR INDEPENDENCE

343

the case (the likelihood that the auditor’s lack

of independence will be discovered) is expec-

ted to affect the independence response of

preconventional auditors. Conventional level

auditors are expected to base their indepen-

dence response primarily in reaction to the

hypothetical auditor’s violation of professional

norms for independence. Postconventional

auditors are expected to consider the following

issues related to justice concerns: the company

suffered no financial harm, the controller saved

his son from serious physical injury, and

revealing the controller’s breach of company

policy will cause the controller to lose his job.

Consistent with the case construction strat-

egy emphasized by Rest (1979), the dilemma

depicts a hypothetical auditor’s actions. Rest

stresses that evaluation of moral judgments must

be in reference to a third person to mitigate

the potential social desirability response bias

present in self-reports concerning sensitive

issues (Randall & Fernandes,

1991). The

response scales require the subject to make a

judgment regarding what the hypothetical audi-

tor

shou l d

have done, as opposed to asking the

subject what action he or she would have taken

in the scenario (Ponemon SZGabhart, 1990).

The case required subjects to allocate 1000

points between an “approval” versus a

“disapproval”

response to the hypothetical

independence behavior of the auditor in the

case. Both statements are equivalent measures

of independence, and subjects’ point allocation

to category A (“Chris should not have disclosed

the disbursement”) served as the dependent

variable (POINTS) in testing hypotheses H2

through H4. The potential number of POINTS

allocated to category A ranged from zero

(absolute independence) to 1000 (absolute

nonindependence).

Requiring subjects to assign a fixed number

of points to mutually exclusive categories is

consistent with prior research in ethics (Arnold

& Ponemon, 1991; Ponemon 8z Gabhart, 1990;

Ponemon, 1993). The advantage of this scale

over a conventional likert-type scale is that

subjects can assign zero points to the dilemma,

signifying absolute compliance with indepen-

dence standards, or a positive number of points

over the range, indicating their relative

empathy or sensitivity to factors which may

have affected the hypothetical auditor acquies-

cence to management. Assigning zero points is

indicative that the subjects were not sensitive

to the contextual factors of the case and saw

the issue in strictly black-and-white terms as an

independence violation. The assignment of ZERO

points (ZERO point group) or a positive number

of points (NONZERO point group) is used as a

dichotomous variable in testing hypothesis H 1.

A treatment manipulation was incorporated

in the case for testing hypothesis H3 and

auditors were randomly assigned to one of two

conditions. The manipulation varied the prob-

ability of detection of the hypothetical auditor’s

acquiescence to the client by stating either (a)

“.

. .Cb r i s i s cer t a i n t h a t t he d i sbu r semen t w i l l

no t be subsequen t l y exam i ned ’

(NOSANCTION

case) or (b) “.

.Cb r i s i s aw a r e t ha t t he

d i sbu r semen t ma y be subsequ en t ly exam -

ined ’

(SANCTION case).4

DATA ANALYSIS

Of the 312 subjects available for testing

hypotheses Hl through H4, 113 (36%) assigned

a value of zero points (ZERO point group) to

category A of the case, indicating complete

adherence to technical independence stan-

dards. The remaining 199 participants (64%)

assigned one or more points (NONZERO point

group) to category A, suggesting at least some

degree of nonindependence. The mean number

of points assigned by the 199 NONZERO auditors

was 319 (s.d.=265), with a range of 1 to 1000.

4 Given the inability of the researchers to prevent subjects from altering their original responses, a manipulation check was

not incorporated into the research instrument and this represents a limitation of the study. However, auditing students

involved in a post-test assigned different probabilities to the likelihood of subsequent discovery of the hypothetical auditor’s

action based upon the manipulation.

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 8/16

344

J. T. SWEENEY and R. W. ROBERTS

The DIT

P

scores of the 312 participants

ranged from 8.3 to 70 with a mean of 42.8 and a

standard deviation of 11.4. The

P

scores of the

subjects in this study are consistent with those

reported in prior research of public accoun-

tants in the United States (Gas, 1992; Ponemon

& Gabhart, 1993).5

Hy pothesis HI : ethi cal sensit iv it y

While

participants were not necessarily

expected to agree with the hypothetical audi-

tor’s decision (pOINTS>SOO), an ethically sen-

sitive auditor would have evaluated the

decision in contemplation of all the issues

present in the case, incorporating both the

technical and ethical components. As Rest

notes, professional dilemmas are usually a

mix of technical and moral issues (Rest, 1986,

p. 23) but professional training may so strongly

highlight the technical aspects of the job that

the individual is blinded to ethical concerns

exogenous to formal rules.

Assigning at least one point is prima facie

evidence that the subject recognized the exis-

tence of one or more ethical issues which

influenced the hypothetical auditor’s decision

to violate the principle of independence

(acquiescence to management’s request to not

report a defalcation incident). Auditors who

assigned zero points to category A responded in

strict accordance with professional indepen-

dence standards; however, their response may

indicate that they lacked sensitivity to the ethi-

cal issues present in the dilemma, a prerequisite

in the Four-Component Model (Rest, 1986) for

testing the relationships hypothesized in H2,

H3 and H4.

A comparison of the

P

scores of subjects who

assigned zero points (ZERO) to category A,

indicating absolute compliance with indepen-

dence standards, to those subjects who

assigned at least one point (NONZERO) pro-

vides evidence in support of hypothesis Hl. A

t-test indicated that the mean

P

score of 40.2

for the auditors in the ZERO group was signiti-

candy lower (p ~0.002) than the mean

P

score

of 44.3 for auditors in the NONZERO group.

Table 2 classifies the ZERO and NONZERO

auditors by

P

Group. A chi-square test indicated

that the ZERO and NONZERO groups syste-

matically differ @<O.OOl) on the proportions

classified into High, Medium, and Low

P

groups. High

P

group and Low

P

group auditors

were more likely to be members of the NON-

ZERO point group (73% and 60%, respectively).

Auditors comprising the Medium

P

group,

however, were more likely to comply abso-

lutely with independence standards (5 1%

assigned ZERO points). Auditors who reason

predominately at a conventional level (Medium

P

group) are expected to take a strong position

on independence (Ponemon & Gabhart, 1990).6

TABLE 2. Classification of ZERO

and

NONZERO auditors by

P group

Point Group:

ZERO NONZERO Totals

n n n

P

Group:

High

47 (27 )

128

(73 ) 175

Medium

54

(51 )

53

(49 )

107

Low

12 (40 ) 18 (60 ) 30

Totals

113

(36%)

199

(64%) 12

Chi-square value 16.23; p <O.OOl

s In contrast to prior research which found relatively minor differences in moral development between males and females

in the general population (Thorna, 1986) gender was highly correlated (p <O.OOl) with P scores for the sample of auditor

subjects. The mean

P score

of 45.8 for the group of female auditors (n=llO) in the sample was significantly higher

(p <0.0007) than the mean

P score

of 41.2 for the male auditors (n=202). Shaub (1994) found similar gender differences in

P scores with auditing subjects.

’ The case manipulation had no effect on the classification of subjects into the ZERO and NONZERO point groups

(p ~0.36). Auditors who could act without threat of discovery (NOSANCTION) were as likely to assign zero points as

auditors who were acting under a high likelihood of discovery (SANCTION). This analysis is necessary only for ruling out an

alternative explanation for the results.

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 9/16

COGNITlVE MORAL DEVELOPMENT AND AUDITOR INDEPENDENCE

345

The lower P scores and P group classi-

fications of the auditors in the ZERO group are

consistent with the proposition that they are

more readily socialized to strictly adhere to

independence standards and less likely to attend

to ethical issues not addressed by professional

standards than auditors from the NONZERO

group.’ By relying solely upon professional

rules in resolving dilemmas, the ZERO group

auditors may lack the sensitivity to adequately

identify the ethical issues and the possible con-

sequences of alternative actions. A limitation

of this research design is that the assignment of

zero points by a subject only infers a lack of

sensitivity to ethical issues, and is not a direct

measure of ethical sensitivity.’

Hypothesis H2: Moral Development and

Auditor I ndependence

The basic premise of this study is that varia-

tions in individual moral development will

result in differences in independence judg-

ments when confronted with an ethical

dilemma (Ponemon & Gabhart, 1990, 1993).

Our position is that auditor independence is

not linearly related to moral development or

that individuals with higher

P

scores will

be more or less independent. Rather, assuming

the referent group maintains expectations

for independent behavior, conventional level

auditors will always be independent. Pre- and

postconventional level auditors may deviate

from independence, but for different reasons.

Relatively minor differences in

P

scores may not

result in significant variations in independence

judgments; however, it is expected that over

certain thresholds or ranges of moral develop-

ment, variations in judgment can be observed.

As indicated in the tests of hypothesis H 1, the

ZERO point group auditors, who responded in

strict accordance with technical rules, may

have lacked sensitivity to the imbedded ethical

issues in the case as required for testing the

relationship between moral development and

independence judgments. Therefore, only

those auditors who indicated sensitivity to the

ethical issues (NONZERO point group) will be

included in the ANOVA model for testing

hypotheses H2, H3, and H4. The ANOVA model

for the NONZERO point group is presented in

Table 3.

The results of the ANOVA model provide

support for the hypothesized relationship

between moral development and auditor inde-

pendence judgments. The significance of the P

Group variable indicates that level of moral

development is an important factor affecting

the independence judgment of the NONZERO

point group. Furthermore, the results of

hypothesis Hl could also be interpreted as

providing support for the moral development-

auditor independence relationship in that

conventional level auditors were more likely to

be absolutely independent (ZERO point group).

A discussion of the interaction of the moral

development variable P Group) with audit firm

size (SIZE) is undertaken in the discussion of

hypothesis H4.

Hypothesis H3: eff ect of sanction

Hypotheses H3 posits that the independence

judgments of auditors whose level of moral

development is predominately preconventional

(Low P Group) will be affected by the presence

of potential sanctions, because their judgments

are conditional upon perceived penalties

resulting from misconduct (Ponemon & Gab

hart, 1990). Table 4 presents mean Points

assigned for the NONZERO subjects by case

manipulation for each P Group.”

_ Auditors at higher positional levels are signilicantly more likely to have lower DIT P scores and to be members of the

ZERO point group (p <tl.OOl). However, position is not significantly related to the Points assigned by the NONZERO auditors

(p <0.573), indicating that point group membership is driven by an auditor’s moral development, and not position.

‘It is possible that some ZERO point group auditors may have been sensitive to the nonprofessional ethical issues in the

case vignette. However, it is not possible due to data limitations to differentiate between those ZERO group subjects who

were sensitive to both professional and nonprofessional ethical issues from those who were affectively socialized to recog-

nize only technical issues.

“A chi-square test indicated that auditors who received a SANCTION case were no more likely to be members of the ZERO

point group than auditors who received a NOSANCTION case.

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 10/16

346

J. T. SWEENEY and R. W. ROBERTS

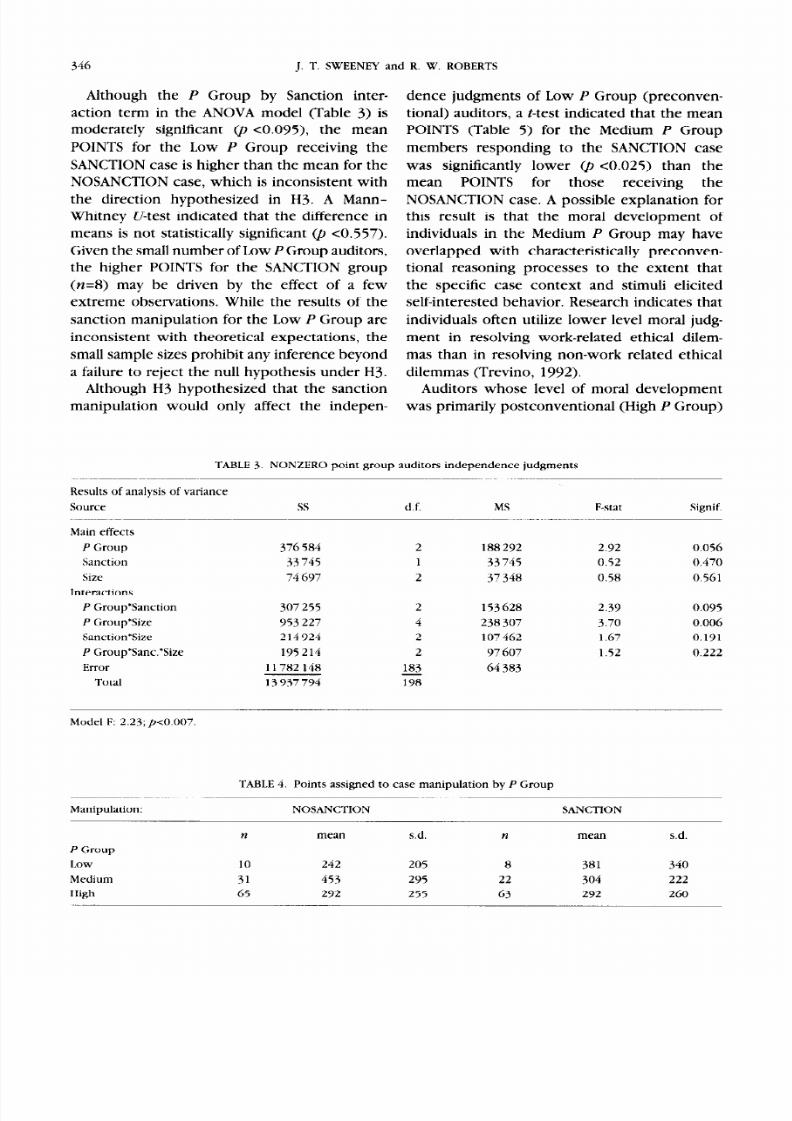

Although the P Group by Sanction inter-

dence judgments of Low

P

Group (preconven-

action term in the ANOVA model (Table 3) is

tional) auditors, a t-test indicated that the mean

moderately significant @ <0.095), the mean

POINTS (Table 5) for the Medium

P

Group

POINTS for the Low

P

Group receiving the

members responding to the SANCTION case

SANCTION case is higher than the mean for the

was significantly lower (p ~0.025) than the

NOSANCTION case, which is inconsistent with mean POINTS for those receiving the

the direction hypothesized in H3. A Mann-

NOSANCTION case. A possible explanation for

Whitney U-test indicated that the difference in

this result is that the moral development of

means is not statistically significant (p cO.557).

individuals in the Medium

P

Group may have

Given the small number of Low

P

Group auditors,

overlapped with characteristically preconven-

the higher POINTS for the SANCTION group

tional reasoning processes to the extent that

(n=g> may be driven by the effect of a few

the specific case context and stimuli elicited

extreme observations. While the results of the

self-interested behavior. Research indicates that

sanction manipulation for the Low P Group are

individuals often utilize lower level moral judg-

inconsistent with theoretical expectations, the

ment in resolving work-related ethical dilem-

small sample sizes prohibit any inference beyond mas than in resolving non-work related ethical

a failure to reject the null hypothesis under H3.

dilemmas (Trevino, 1992).

Although H3 hypothesized that the sanction

manipulation would only affect the indepen-

Auditors whose level of moral development

was primarily postconventional (High

P

Group)

TABLE 3. NONZERO point group auditors independence judgments

Results of analysis of variance

Source

Main effects

P

Group

Sanction

Size

Interactions

P

Group’Sanction

P Group’Size

Sanction’Stie

P

Group*Sanc.*Size

ElKX

Total

ss d.f.

376 584 2

33 745 1

74 697 2

307 255 2

953 227 4

214924 2

195 214 2

11782148 183

13 937 794 iG

MS

188 292

33 745

37 348

153628

238 307

107462

97 607

64 383

F-stat Signif

2.92 0.056

0.52 0.470

0.58 0 561

2.39 0.095

3.70 0.006

1.67 0.191

1.52 0.222

Model F: 2.23; p&007.

TABLE 4. Points assigned to case manipulation by

P

Group

Manipulation:

NOSANCTION

SANCTION

P

Group

Low

Medium

High

n

mean s.d. n mean s.d.

10 242 205 8 381 340

31 453 295 22 304 222

65 292 255 63 292 260

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 11/16

COGNITIVE MORAL DEVELOPMENT AND AUDITOR INDEPENDENCE 347

were unaffected by the potential penalty.

Consistent with theoretical expectations, the

mean POINTS of the NOSANCTION and SANC-

TION groups were equal for the High

P

Group

members, indicating that the presence or

absence of adverse personal consequences in

the case dilemma did not affect their indepen-

dence judgments. This result is consistent with

Windsor and Ashkanasy (1995), who found that

postconventional auditors were indifferent

to client economic pressure when forming

independence judgments.

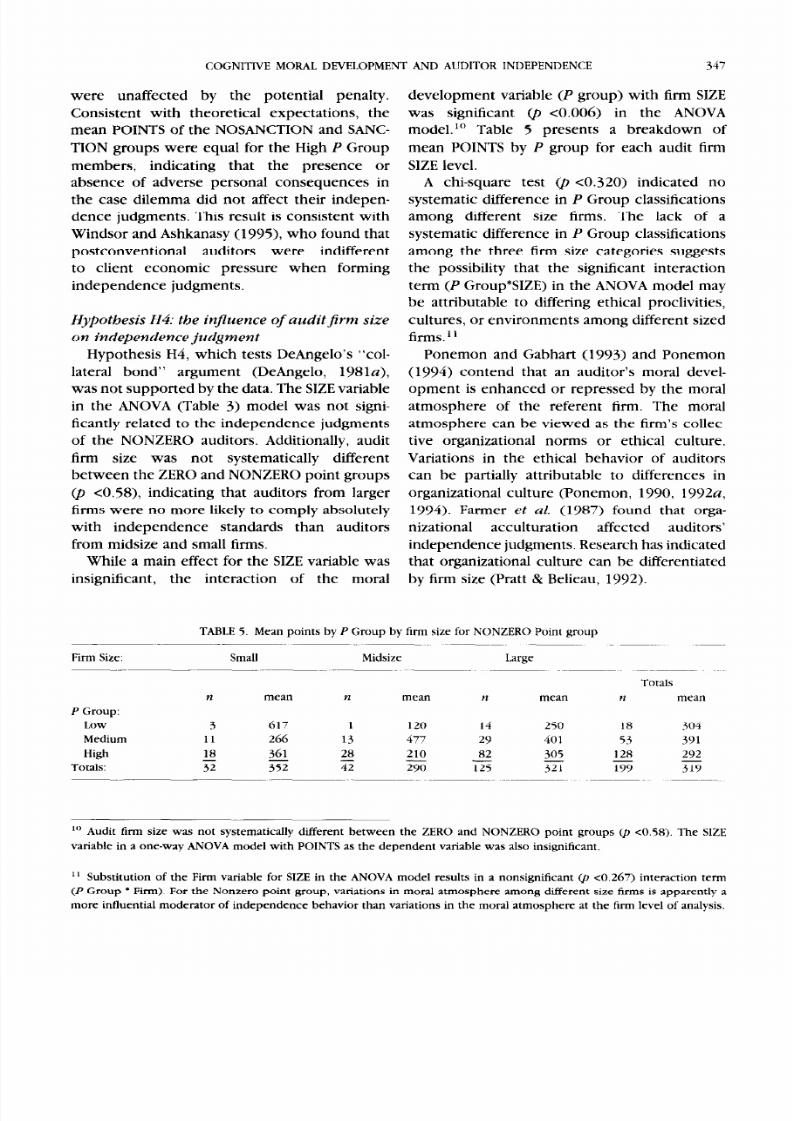

Hypothesis H4: the in .uence of auditJi rm size

on independence judgment

Hypothesis H4, which tests DeAngelo’s “col-

lateral bond” argument (DeAngelo, 1981a),

was not supported by the data. The SIZE variable

in the ANOVA (Table 3) model was not signi-

ficantly related to the independence judgments

of the NONZERO auditors. Additionally, audit

firm size was not systematically different

between the ZERO and NONZERO point groups

Cp <0.58), indicating that auditors from larger

firms were no more likely to comply absolutely

with independence standards than auditors

from midsize and small firms.

While a main effect for the SIZE variable was

insignificant,

the interaction of the moral

development variable P group) with firm SIZE

was significant (p <0.006) in the ANOVA

model.“’ Table 5 presents a breakdown of

mean POINTS by

P

group for each audit firm

SIZE level.

A chi-square test (p <0.320) indicated no

systematic difference in P Group classifications

among different size firms. The lack of a

systematic difference in

P

Group classifications

among the three firm size categories suggests

the possibility that the significant interaction

term P Group*SIZE) in the ANOVA model may

be attributable to differing ethical proclivities,

cultures, or environments among different sized

firms.

1’

Ponemon and Gabhart (1993) and Ponemon

(1994) contend that an auditor’s moral devel-

opment is enhanced or repressed by the moral

atmosphere of the referent firm. The moral

atmosphere can be viewed as the firm’s collec-

tive organizational norms or ethical culture.

Variations in the ethical behavior of auditors

can be partially attributable to differences in

organizational culture (Ponemon, 1990, 1992a,

1994). Farmer

et al.

(1987) found that orga-

nizational

acculturation affected auditors’

independence judgments. Research has indicated

that organizational culture can be differentiated

by firm size (Pratt & Belieau, 1992).

TABLE 5. Mean points by

P

Group by firm size for NONZERO Point group

Firm Size:

P

Group:

Low

Medium

Small Midsize Large

Totals

n mean n

mean

n mean n mean

3 617 I 120 14 250 18 304

11 266 13 477 29 401 53 391

High 18 361 28 210 82 305 128 292

Totals: 32 352 42 290 125 z? 1s)9 319

“’ Audit firm size was not systematically different between the ZERO and NONZERO point groups (p ~0.58). The SIZE

variable in a one-way ANOVA model with POINTS as the dependent variable was also insignificant.

i’ Substitution of the Firm variable for SIZE in the ANOVA model results in a nonsignificant (p ~0.267) interaction term

P Group Firm). For the Nonzero point group, variations in moral atmosphere among different size firms is apparently a

more influential moderator of independence behavior than variations in the moral atmosphere at the firm level of analysis.

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 12/16

348

J. T. SWEENEY and R. W. ROBERTS

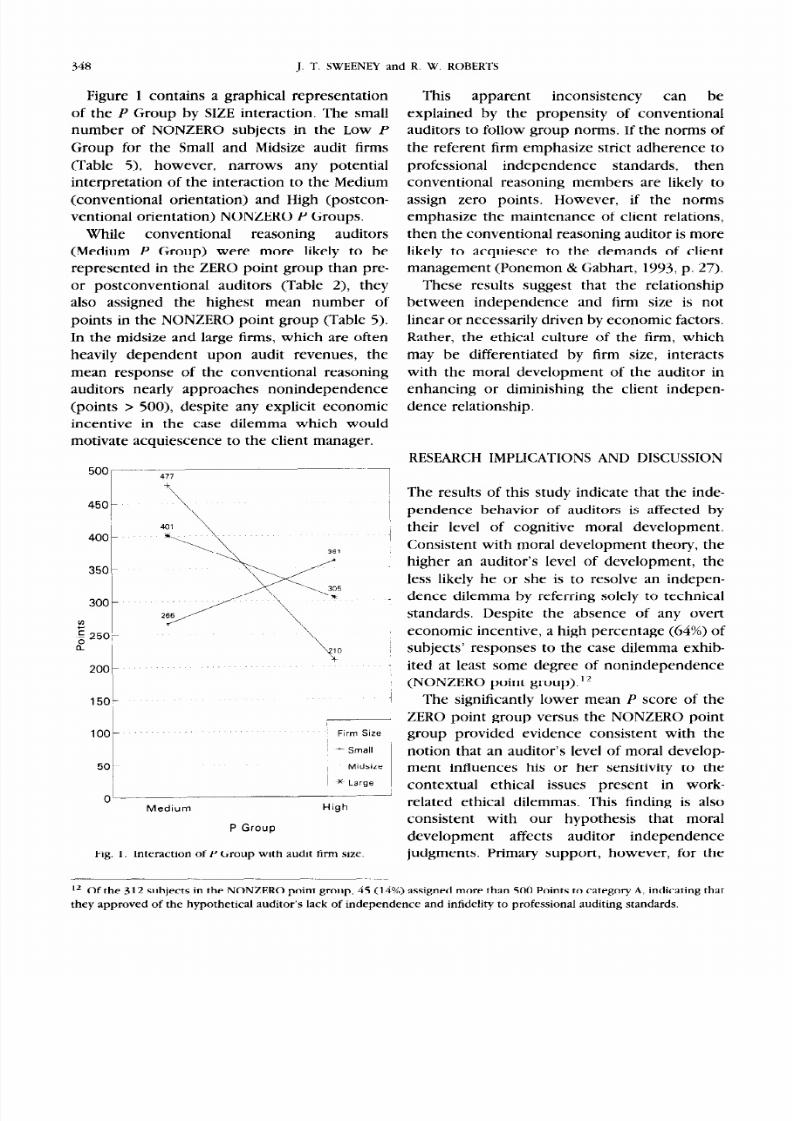

Figure 1 contains a graphical representation

of the

P

Group by SIZE interaction. The small

number of NONZERO subjects in the Low

P

Group for the Small and Midsize audit firms

(Table 5) however, narrows any potential

interpretation of the interaction to the Medium

(conventional orientation) and High (postcon-

ventional orientation) NONZERO P Groups.

While

conventional reasoning auditors

(Medium

P

Group) were more likely to be

represented in the ZERO point group than pre-

or postconventional auditors (Table 2) they

also assigned the highest mean number of

points in the NONZERO point group (Table 5).

In the midsize and large firms, which are often

heavily dependent upon audit revenues, the

mean response of the conventional reasoning

auditors nearly approaches nonindependence

(points > 500) despite any explicit economic

incentive in the case dilemma which would

motivate acquiescence to the client manager.

50,

i

Firm Size

~ -

Small

- MIdsize

Large

Medium

P GrouD

High

Fig. 1. Interaction of P Group with audit firm size.

This apparent inconsistency

can be

explained by the propensity of conventional

auditors to follow group norms. If the norms of

the referent firm emphasize strict adherence to

professional independence standards, then

conventional reasoning members are likely to

assign zero points. However, if the norms

emphasize the maintenance of client relations,

then the conventional reasoning auditor is more

likely to acquiesce to the demands of client

management (Ponemon & Gabhart, 1993, p. 27).

These results suggest that the relationship

between independence and firm size is not

linear or necessarily driven by economic factors.

Rather, the ethical culture of the firm, which

may be differentiated by firm size, interacts

with the moral development of the auditor in

enhancing or diminishing the client indepen-

dence relationship.

RESEARCH IMPLICATIONS AND DISCUSSION

The results of this study indicate that the inde-

pendence behavior of auditors is affected by

their level of cognitive moral development.

Consistent with moral development theory, the

higher an auditor’s level of development, the

less likely he or she is to resolve an indepen-

dence dilemma by referring solely to technical

standards. Despite the absence of any overt

economic incentive, a high percentage (64%) of

subjects’ responses to the case dilemma exhib-

ited at least some degree of nonindependence

(NONZERO point group).i2

The significantly lower mean

P

score of the

ZERO point group versus the NONZERO point

group provided evidence consistent with the

notion that an auditor’s level of moral develop-

ment influences his or her sensitivity to the

contextual ethical issues present in work-

related ethical dilemmas. This finding is also

consistent with our hypothesis that moral

development affects auditor independence

judgments. Primary support, however, for the

‘a Of the 312 subjects in the NONZERO point group, 45 (14%) assigned more than 500 Points to category A, indicating that

they approved of the hypothetical auditor’s lack of independence and infidelity to professional auditing standards.

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 13/16

COGNITIVE MORAL DEVELOPMENT AND AUDITOR INDEPENDENCE

349

moral development-independence relationship

was supplied by our ANOVA tests.

Audit firm size interacted with moral

development level in affecting subjects’ inde-

pendence judgment, although the direction of

the relationship is unclear. This result provides

evidence consistent with the proposition

(Ponemon, 1990, 1992a, 1994) that the moral

atmosphere of an audit firm influences an audi-

tor’s consideration of client issues.

Perhaps as a partial response to spiraling

litigation costs, audit firms have invested

increasingly greater resources in programs

designed to foster ethical auditor behavior. The

results of this study and those of other

researchers (Ponemon, 1992b, 1994; Windsor

& Ashkanasy, 1995) strongly suggest that the

moral reasoning ability of auditors and accoun-

tants affects their resolution of work-related

ethical dilemmas. Furthermore, whether conven-

tional or postconventional auditors are more

likely to comply with professional standards

may be context specific and at least partially

dependent upon the ethical values promoted

by the referent audit firm.

If the auditing profession equates ethical

behavior with strict adherence to professional

standards, then the results of this research

have important implications for audit firms in

understanding the relationship between moral

development and ethical behavior. Auditors

whose moral development was primarily

conventional in nature were more likely to

comply absolutely with professional indepen-

dence standards and were more affected by

potential penalties for noncompliance than

postconventional auditors. For those subjects

who did not comply absolutely, however, the

response of conventional auditors deviated the

most from independence standards, particularly

in midsize and large firms. These results suggest

that for conventional reasoning auditors, strong

firm norms for independence and the presence

of penalties for nonindependent behavior are

effective mechanisms for promoting behavior

consistent with professional standards.

Postconventional auditors were more likely

to consider contextual factors beyond the

scope of professional standards when forming

their independence judgments and were unaf-

fected by the presence of potential penalties

for nonindependence. These results, combined

with the finding of Windsor and Ashkanasy

(1995) that high moral reasoning auditors

are unaffected by client economic pressure,

suggest

that the independence behavior

of postconventional auditors is motivated by

concerns other than self-interest.

Given the increasing competition and declin-

ing margins in the audit industry, firms which

are heavily dependent upon audit revenues may

incorporate into their culture or value systems

an emphasis on client relations and retention.

These values may then be consciously or

unconsciously inculcated in the ethical schema

of the firm members, particularly those who

reason at a conventional level, and subsequently

influence their responses to ethical dilemmas.

Audit firms can promote ethical behavior by

emphasizing adherence to professional codes of

conduct and high ethical standards above all

other competing values.

The results of this study suggest several areas

for future research. First, research on factors

which enhance or repress the ethical sensitivity

of auditors will contribute to our understanding

of this component of ethical behavior. Secondly,

the connection between ethical sensitivity and

moral development in affecting ethical behavior

presents opportunities for future exploration.

Finally, the influence of moral atmosphere in

affecting ethical behavior is an area of research

which presents an excellent opportunity for

furthering our understanding of the socializing

influence of the audit firm.

There are some limitations to the study that

should be discussed. First, the auditors in our

sample came only from public accounting firm

offices in the Midwest and were not randomly

selected. Generalization of the results of this

study are valid only to the extent that public

accountants in the Midwest are similar to their

counterparts in other regions of the country.

The inclusion of auditors at all positional ranks

from thirteen different office locations, repre-

senting eight different public accounting firms

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 14/16

350

J. T. SWEENEY and R. W. ROBERTS

and three different firm size categories mitigates

this type of research: (1) cases may lack realism

potential biases due to nonrandom selection. and the richness found in an actual audit set-

Finally, auditor independence is a state of

ting, (2) participants may not answer truthfully,

mind and therefore unobservable. The use of and (3) the auditor’s actual independence

hypothetical cases to measure auditor indepen-

behavior may be affected by variables not

dence is subject to several criticisms inherent in represented in the case.

BIBLIOGRAPHY

American Institute of Certified Public Accountants (AICPA). (1988). The Code of Prof essional Conduct of

the American I nstitute of Certif ied Public Accountants. New York: AICPA.

Antle, R. (1984). Auditor independence. Journal of Accounting Research, Spring, l-20.

Arnold, D. F., & Ponemon, L. A. (1991). Internal auditors’ perceptions of whistle-blowing and the

influence of moral reasoning: an experiment.

Auditi ng: A Journal of Practice and Theory,

1- 15.

Bernardi, R. A. (1994). Fraud detection: the effect of client integrity and competence and auditor cognitive

style. Auditi ng: A Journal of Practice and Theory (Supplement), 68-84.

Bebeau, M. J., Rest, J. R., & Yamoor, C. M. (1985). Measuring dental students ethical sensitivity. Journal of

Dental Education, 225-235.

Colby, A., & Kohlberg, L. (1987).

The Measurement of MoralJudgment. New

York: Cambridge University

Press.

Cushing, B. E. (1990). Discussion of “Auditor Independence Judgments: A Cognitive Developmental

Model and Experimental Evidence”. Contemporary Accounting Research. 252-260.

DeAngelo, L. E. (1981a). Auditor Size and Auditor Quality. Journal of Accounting and Economics

(August), 183- 199.

DeAngelo, 1.. E. 198lb). Auditor independence, ‘low balling,’ and disclosure regulation. Journal of

Accounting and Economics, August, 113-127.

Farmer, T. A., Rittenberg L. E., & Trompeter G M. (1987). An investigation of the impact of economic and

organizational factors on auditor independence. Auditi ng: A Journal of Theory and Practice, Fall, l-14.

Fogarty, T. (1992). Organizational socialization in accounting firms: a theoretical framework and agenda

for future research. Accounti ng, Or ganizations and Society, 129- 149.

Gaa, J. C. (1992). The auditor’s role: the philosophy and psychology of independence and objectivity.

Proceedings of the 1992 Deloit te and Touche/University of Kansas Symposium on Auditi ng

Problems, pp. 7-43. IJniversity of Kansas, School of Business.

Gaa, J. C. (1994). me Ethical Foundations of Public Accounting. Research Monograph Number 22.

Vancouver, British Columbia: CGA-Canada Research Foundation.

Kohlberg, L. (1969). Stage and sequence: the cognitive developmental approach to socialization. In D. A.

Goslin (Ed.), Handbook of Socialization Theory and Research (pp. 347-480). Chicago: Rand McNally.

Iampe, J. C., & Finn, D. W. (1992). A model of auditors’ ethical decision processes. Auditing: A Journal of

Practice and Tbeoly (Supplement), 33-59.

Loeb, S. E. (1971). A survey of ethical behavior in the accounting profession. Journal of Accounting

Research, 287-306.

Magee. R. P., & Tseng, M. (1990). Audit pricing and independence. he Accounting Review, April, 315-336.

Palmrose, 2. V. (1988). An analysis of auditor litigation and audit service quality. The Accounting Review,

January, 55-73.

Ponemon, L. A. (1990). Ethical judgments in accounting: a cognitive developmental perspective. Critical

Perspectives 071Accounting, 191-215.

Ponemon, L. A. (1992a). Auditor underreporting and moral reasoning: an experimental-lab study.

Contemporary Accounti ng Research, 169-189.

Ponemon, L. A. (1992b). Ethical reasoning and selection-socialization in accounting. Accounting, Organi-

zations and Society, 239-258.

Ponemon, L. A. (1993). The influence of ethical reasoning on auditors’ perceptions of management’s

integrity and competence. Adzlances in Accounti ng, l-29.

Ponemon, L. A. (1994). Whistle-blowing as an internal control mechanism: individual and organizational

considerations.

Auditi ng: A Journal of Practice and Theory, 118-130.

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 15/16

COGNITIVE MORAL DEVELOPMENT AND AUDITOR INDEPENDENCE

351

Ponemon, L. A. (1995). The objectivity of accountants’ litigation support judgments. The Accounting

Review, July, 467-488.

Ponemon, L. A., & Gabhart, D. R. (1990). Auditor independence judgments: a cognitive developmental

model and experimental evidence. Contempom y Accounti ng Research, 227-25 1.

Ponemon, L. A., & Gabhart, D. R. (1993). Ethical reasoning in accounting and auditing. Research

Monograph Number 21. Vancouver, British Columbia: CGA-Canada Research Foundation.

Ponemon, L. A., & Gabhart, D. R. (1994). Ethical reasoning research in the accounting and auditing

professions. In J. R. Rest and D. Narvaez (Eds), Moral Development in theprofessions:psycholo~ and

upplied ethics (pp. 101-l 19). Hillsdale, New Jersey: Laurence Erlbaum Associates.

Pratt, J., & Belieau P. (1992). Organizational culture in public accounting: size, technology, rank, and

functional area. Accounti ng, Organi zations and Society, 667-684.

Public Oversight Board (POB) of the American Institute of Public Accountants (1993). In the public

interest.

Stamford, Conn: AICPA.

Public Oversight Board (POB) Advisory Panel on Auditor Independence (1994). Strengthening the

prof essionali sm of the independent auditor. Stamford, Conn: AICPA.

Randall, D. M., & Fernandes, M. F. (1991). The social desirability response in ethics research.Journul of

Business Ethics, 805-817.

Rest, J. R. (1986). Moral development: advances in research and theory. New York: Prager Press.

Rest, J. R. (1979).

Development inj udging Moral I ssues.

Minneapolis, MN: University of Minnesota Press.

Rest, J. R. (1993). Gui defor the Defi ni ng I ssues Test. Version 1.3. Minneapolis, MN: lrniversity of Minnesota

Rest, J. R. (1994). Background: theory and research. In J. R. Rest and D. Na TdeZ (Eds), Moral devefop-

ment in the prof essions: psychology and appli ed ethics (pp. I-26). Hillsdale, NJ: Laurence Erlbaum

Associates.

Rest, J. R., & Thoma, S. (1985). Relation of moral judgment development to formal education. Derjelop-

mental Psychology, 709-7 14.

Securities & Exchange Commission (SEC), Office of the Chief Accountant (1994). Stuff report on auditor

independence

Shaub. M. K. (1989). An empirical examination of the determinants of auditors’ ethical sensitivity.

Doctoral dissertation. Lincoln, NE: University of Nebraska.

Shaub M. K. (1994). An analysis of the association of traditional demographic variables with the moral

reasoning of auditing students and auditors. Journal of Accounting Education. Winter, l-26

Sweeney, J. T. (1995). The moral expertise of auditors. an exploratory analysis. Research on Accounti ng

Ethics, 213-234.

Thoma, S. J. (1986). Estimating gender differences in the comprehension and preference of moral issues.

Detrelopmental Review, 165- 180.

Trevino, L. (1986). Ethical decision making in organizations: a person-situational interactionist model.

Academy of Management Review, 601-617.

Trevino, L. (1992). Moral reasoning and business ethics: implications for research, education, and man-

agement. Jour nal of Business Ethi cs, 445-459.

Tsui, J. S. L., & GUI, F A. (1996) Auditors’ behavior in an audit conflict situation: a research note on the

role of locus of control and ethical reasoning. Accounti ng, Organ izations and Society, 4 -5 1.

Windsor, C. A., & Ashkanasy, N. M. (1995). The effect of client management bargaining power, moral

reasoning development, and belief in a just world on auditor independence. Accounting, Organizutions

and Society, 20, 701-720.

Watts, R. L., & Zimmerman, J. L. (1986). Positi ue accounti ng theory. New York: Prentice Hall, Inc.

8/11/2019 Cognitive Moral Development and Auditor Independence 1997 Accounting, Organizations and Society

http://slidepdf.com/reader/full/cognitive-moral-development-and-auditor-independence-1997-accounting-organizations 16/16

352

J. T. SWEENEY and R. W. ROBERTS

APPENDIX

Instructions:

1. Please read the case very carefully.

2. Using your judgment, please allocate 1000

points to the following two categories:

(a) You agree with the decision of the

auditor.

(b) You do not agree with the decision of

the auditor.

Unless you are in absolute agreement with

the auditor’s decision, do not allocate 1000

points to any single category. For example, if

you are about 80% in agreement with the audi-

tor’s decision, allocate 800 points to category A

and 200 points to category B.

Case

S t u d y I

Chris Gibson has been employed by the public

accounting firm of RS and T for the past

four years and is the senior in-charge of the

Greenwood Manufacturing Company audit.

Greenwood is a manufacturer of household

furniture and a division of a large, publicly traded

corporation. With annual sales of approximately

40 million, Greenwood is in good financial

health and the corporation has received unquali-

fied audit opinions in recent years.

25,000 disbursement. Mr. Johnson asked Chris

to close the door, pulled a file from his desk,

and then began the following conversation:

“I expected you might be dropping by to

discuss that withdrawal. The disbursement is

my personal responsibility, and I repaid it the

next day. You can verify the receipt by exam-

ining the bank statement. I have copies of all

supporting documents in this file.

“I withdrew those funds from the company

account after receiving a phone call that after-

noon from my son, a student at the university.

At the time, I was unaware he had developed a

severe gambling problem. He told me that he

had substantial losses which he was unable to

pay. Furthermore, he had been threatened with

bodily harm if he didn’t pay 25,000 in gam-

bling debts by that night. The only way I could

obtain that much cash in a matter of hours was

to access company funds. I repaid the amount

the following day with personal funds. My son

has since obtained counseling and treatment for

his gambling problem.

“You’re the only person I’ve confided in: you

must realize I will lose my job if this matter

becomes public.”

While visually inspecting the accounting

records of Greenwood in a search for unusual

appearing transactions, Chris discovered an

uncoded cash disbursement of 25,000. Chris

decided to discuss the situation with the

controller, Ed Johnson.

Ed Johnson first worked for Greenwood

Manufacturing when it began operations in

1970. Mr. Johnson has held the controllers’

position for eight years and is generally regar-

ded as one of the most competent and highly

respected executives at Greenwood. Mr.

Johnson has always been cooperative and

professional during the course of the audit.

Chris confirmed that the support from Mr.

Johnson’s file was consistent with his explana-

tion. As the corporate internal audit staff has yet

to complete its annual audit of the Greenwood

Manufacturing division, Chris is aware that the

disbursement may be subsequently examined.

Chris decides not to disclose the information

obtained concerning the disbursement.

A: Chris should not have disclosed the disbursement.

Points:------ (not to exceed 1000)

B: Chris should have disclosed the disbursement.

Points:------ (not to exceed 1000)

Ed Johnson was alone in his office when (Remember, the combined points assigned to

Chris Gibson entered and referred to the

category A and B must equal 1000.)