coase versus the coasians - scholar.harvard.edu · coase versus the coasians* edwardglaeser...

TRANSCRIPT

COASE VERSUS THE COASIANS

EDWARD GLAESER

SIMON JOHNSON

ANDREI SHLEIFER

Who should enforce laws or contracts judges or regulators Many Coasiansthough not Coase himself advocate judicial enforcement We show that the incen-tives facing judges and regulators crucially shape this choice We then compare theregulation of nancial markets in Poland and the Czech Republic in the 1990s InPoland strict enforcement of the securities law by a highly motivated regulator wasassociated with a rapidly developing stock market In the Czech Republic hands-offregulation was associated with a moribund stock market

I INTRODUCTION

At the heart of economistsrsquo traditional skepticism about gov-ernment regulation is the Coase theorem [Coase 1960] Thetheorem states that when property rights are well dened andldquotransaction costsrdquo are zero market participants will organizetheir transactions in ways that achieve efcient outcomes Whenthey can do so it is not necessary for the government to engage inldquocorrectiverdquo actions through taxes regulations or even legalrules Financial markets are often used to demonstrate the Coasetheoremrsquos case against regulation Advocates of the regulation ofthese markets point to a variety of potential failures such as theability of security issuers to ldquoexpropriaterdquo both potential and exist-ing investors through misrepresentation or prot diversion Inves-torsrsquo fear of such expropriation prevents rms from raising externalfunds and keeps efcient projects from being undertaken

Not so reply the Coasians They point out that most securi-ties transactions take place between sophisticated adults andthat both the buyers and the issuers of securities have availableto them a vast range of private arrangements to achieve ef-ciency including contracts such as corporate charters certica-tion by intermediaries and various forms of bonding Such con-tracts render most laws and regulations unnecessary [Stigler1964 Easterbrook and Fischel 1991]

We thank Alberto Alesina Simeon Djankov Oliver Hart Louis KaplowLawrence Katz Rafael La Porta Florencio Lopez-de-Silanes Gerry McDermottRandall Morck Raghuram Rajan Mark Ramseyer Steven Shavell Peter Teminand three anonymous referees for helpful comments and the National ScienceFoundation and the Massachusetts Institute of Technology EntrepreneurshipCenter for nancial support

copy 2001 by the President and Fellows of Harvard College and the Massachusetts Institute ofTechnologyThe Quarterly Journal of Economics August 2001

853

On the face of it the Coasiansrsquo argument is powerful Yet itcrucially relies among other assumptions on the possibility ofeffective judicial enforcement of complicated contracts Judgesmust be able and more importantly willing to read complicatedcontracts verify whether the events triggering particular clauseshave actually occurred and interpret broad and ambiguous lan-guage These requirements on the judges apply as strongly to thejudicial enforcement of laws where the interpretation and appli-cation of particular statutes requires signicant investment Inreality courts in many countries are undernanced unmoti-vated unclear as to how the law applies unfamiliar with eco-nomic issues or even corrupt Such courts cannot be expected toengage in costly verication of the facts of difcult cases orcontingencies of complicated contracts Indeed even when con-tracts are restricted by statutes the courts may not have theresources or incentives to verify whether or how particular stat-utes apply

Financial contracting illustrates these problems When is theinformation that a rmrsquos manager fails to disclose to shareholdersldquomaterialrdquo and hence has to be disclosed because of a statute ora contract When does a corporation ldquoabuserdquo minority sharehold-ers as opposed to just following the managersrsquo best ldquobusinessjudgmentrdquo When does a broker fail to engage in ldquohonest tradingrdquoin executing customer orders When does a manager trade onldquoinside informationrdquo rather than simply happen to be lucky Theinterpretation of the contracts or statutes involving such terms isexpensive and requires powerful incentives to motivate an adju-dicator to invest in understanding the case Absent such incen-tives courts often postpone decisions or simply let go the poten-tial violators of rules and contracts

An alternative strategy is the enforcement of legal rules byregulators as opposed to judges In our view the crucial distinc-tion between judges and regulators is that the latter can be moreeasily provided with incentives to punish violations of particularstatutes1 Judges in contrast are by design more independentand therefore harder to motivate The stronger incentives of theregulators have the benet of bringing about more aggressiveenforcement than can be achieved through courts Yet these

1 The classic reference on the incentive of law enforcers is Becker and Stigler[1974] to whose work we return below A recent survey of public enforcement oflaw by Polinsky and Shavell [2000] scarcely pays attention to the incentives of theenforcers

854 QUARTERLY JOURNAL OF ECONOMICS

incentives also have the potential cost of excessively aggressiveenforcement when regulators motivated to nd violations penal-ize innocent suspects There is thus a trade-off between enforce-ment by judges facing relatively weak but unbiased incentivesand enforcement by regulators facing stronger but possibly biasedincentives2

We present a theoretical model that sheds light on this trade-off and identies the circumstances under which enforcement byjudges or regulators is preferred The model shows that relativeto judges regulators may be better motivated to invest in under-standing the laws and circumstances of a case but also morelikelymdashif overmotivatedmdashto reach politically desirable decisionsat the expense of doing justice The model also shows how reduc-ing the costs of the investment in information by law enforcerscan improve enforcement efciency

We then illustrate the model by comparing the regulation ofsecurities markets through corporate and securities laws in Po-land the Czech Republic and to a lesser extent Hungary Inthese transition economies nancial regulation was designedessentially from scratch and hence we can compare both thedesigns of laws and regulations and their consequences Themodel bears in particular on the design of securities laws sincethese laws shape the incentives of market regulators as well asthe costs of information acquisition by the enforcers

We show that in its securities law Poland adopted a morestringent regulatory stance than did the Czech Republic Thisdifference was reected not just in the general philosophies ofregulation but in the statutes and the mechanisms of law en-forcement In contrast to the Czech Republic Poland adoptedlegal rules highly protective of investors mandated extensiveinformation disclosure by securities issuers and intermediariesand created an independent and highly motivated regulator toenforce the rules We nd that this approach to regulation inPoland has stimulated rapid development of securities marketsand enabled a number of rms to raise external funds Theexpropriation of investors has been relatively modest In contrastthe lax regulations in the Czech Republic enforced by an unmo-tivated ofce in the nance ministry have been associated with

2 Coase [1988 pp 117ndash118] recognized that regulation may be preferred tojudicially enforced contracts as a method of regulating some types of conductldquoThere is no reason why on occasion such governmental regulation should not bean improvement on economic efciencyrdquo

855COASE VERSUS THE COASIANS

security delistings and a notable absence of equity nancethrough a public market by either new or existing rms Expro-priation of investors has been rampant and has acquired a newCzech-specic name tunneling [Coffee 1996 1998 1999 Pistor1999 Johnson et al 2000b] Starting in 1996 the Czech govern-ment tightened its regulations Hungary adopted an intermediateregulatory stance and has shown an intermediate level of nan-cial development

II A MODEL OF ENFORCEMENT INCENTIVES

A Basic Model

We consider a situation in which the government wishes topunish particular conduct creating negative externalities such asnondisclosure of material information by a manager or ldquomarketmanipulationrdquo by a broker This task is assigned to an enforce-ment ofcial (an adjudicator) The question we address is whetherthe government wants this adjudicator to be a judge or a regula-tor In the case of a judge we focus on the inquisitorial legalsystem of civil law countries where the judge must himself un-dertake an investigation into the facts of the situation and thelaw The model we present focuses on the case where there is alegal rule or law that restricts certain conduct The question ofwho should adjudicate however equally well applies to a situa-tion in which two private parties such as an investor and a brokercontractually agree on their conduct and have a dispute onwhether this contract was followed

Our general assumption is that the society does not have fullcontrol over the incentives facing law enforcement ofcials Its abil-ity to reward them for ldquoenforcing the lawrdquo is limited because ldquodoingjusticerdquo is largely unveriable Many of the rewards that theseofcials receive for doing justice are intangible including self-es-teem and the respect of onersquos peers On the other hand the govern-ment does have the ability to politicize the enforcement of particularlegal rules by rewarding the enforcers for certain outcomes such asnding violations We are interested in the conditions under whichthe government would choose such politicization

We consider an adjudicator (who can be a judge or a regula-tor) examining a possible violation of a legal rule For a cost c gt0 this adjudicator can undertake an investigationmdashwhich forsimplicity we call searchmdashand nd out for sure whether a viola-

856 QUARTERLY JOURNAL OF ECONOMICS

tion had taken place We think of c as a personal cost to theadjudicator which includes the time he might otherwise spendworking on other matters The adjudicator has complete discre-tion as to whether to penalize the potential violator and candecide to do so without searching and incurring the cost c

The adjudicator derives a payoff of b from following the lawor doing justice which here means punishing a violator of the ruleand letting go an innocent person We can think of b as self-esteem or long-run respect of the peers which evidently mattersto judges [Posner 1995] We assume that in the short run thegovernment cannot increase b since it cannot verify whetherthe adjudicator actually searches or makes correct decisionsTraining judges and building up their prestige presumably raisesb but such policies may take decades to pay off

In addition the adjudicator derives the payoff a from eachsuspect he punishes whether or not this suspect actually violatedthe rules If a = 0 this adjudicator is only interested in justiceand is not motivated by ldquopoliticsrdquo or short-run career concerns Ifa gt 0 this adjudicator has a personal interest in nding viola-tions This can be so for a number of reasons The state may beconcerned with nding violators of particular rules to achieve itsbroader political goals such as ghting drugs or persecutingparticular ethnic minorities More narrowly only successful pun-ishments of violators may be recorded by the superiors of anenforcer and hence his future career or budget may be deter-mined by the number of penalties he metes out Still anotherimportant reason why adjudicators may wish to achieve certainoutcomes is that these improve their career opportunities follow-ing government service [Glaeser Kessler and Piehl 2000] Inprinciple law enforcement can be heavily politicized and a couldbe a lot higher than b We can also imagine the case where a lt0 which might describe regulators ldquocapturedrdquo by the industrythat they are supposed to regulate [Stigler 1971] In this case theanalysis becomes very simple the adjudicator will generally notnd any violations Note that as we have set up the model a band c capture the private rather than social payoffs and costs tothe adjudicator

To complete the model we assume that the fraction p ofsuspected violators of the legal rule are actually guilty and thefraction (1 2 p) are innocent The payoffs to the adjudicator andthe associated probabilities are shown in Table I

The adjudicator makes the ex ante decision of whether to

857COASE VERSUS THE COASIANS

search We refer to the strategy of letting everyone go regardlessof violation as ldquoleniencyrdquo and the strategy of punishing everyoneregardless of violation as ldquoabuserdquo With b gt 0 it never pays theadjudicator to sink the cost c and then ignore the information heobtains and be either lenient or abusive If he searches he alwayspunishes the violators and lets go the innocent But before searchit may pay the adjudicator to be either lenient or abusive de-pending on the magnitudes of a b c and p

To analyze the adjudicatorrsquos incentives for enforcement werst consider his payoffs to the three strategies he can pursueleniency abuse and search These payoffs are given by

(1) Leniency (1 2 p)b(2) Abuse a + pb(3) Search b + pa 2 c

These payoffs dene the optimal strategies of the enforcer assummarized in

PROPOSITION 1 Fix b and p The following strategies are followedfor respective parameter values

Leniency a (1 2 2p)b and c $ (a + b) pAbuse a $ (1 2 2p)b and c $ (b 2 a)(1 2 p)Search c (a + b) p and c (b 2 a)(1 2 p)

These conditions divide the space of parameter values into threeregions as shown in Figure I3

The interpretation of these conditions is straightforward Forlow-powered punishment incentives and high cost of search theadjudicator chooses leniency For high-powered punishment in-centives and high cost of search the adjudicator turns to abuseHe only searches for the truth as long as the cost of investigationis low enough that for low arsquos he prefers search to leniency andfor high arsquos he prefers search to abuse

Even this simple analysis in Figure I has several implica-

3 Note that if a gt b the only equilibrium outcome is abuse

TABLE I

Not Punish Punish Probability

Innocent b a 1 2 pGuilty 0 a + b p

858 QUARTERLY JOURNAL OF ECONOMICS

tions First we can think of c as a measure of the efciency of thejudicial system the cost to the adjudicator of obtaining informa-tion In principle c can be reduced through legal and regulatoryreform In the context of nancial markets for example c can bereduced by improving accounting systems and disclosure by issu-ers and intermediaries The model implies that reductions in thelevel of c always lead to increases in search For high levels of csearch may not be achievable Increasing career or nancial in-centives of the enforcers only moves the system from leniency toabusemdasha risk that a society may not wish to take if it prefers theformer to the latter Put differently a relatively efcient legalsystemmdashwhich could potentially be designed using appropriatelegal rulesmdashis necessary for achieving just outcomes without itit may be better to settle for leniency

Second for moderate and low levels of c increasing incen-tives for punishment may indeed have the effect of moving theadjudicator from leniency to search Even here however signi-cant increases in a move the adjudicator out of search and intoabuse This analysis cautions against the Becker-Stigler [1974]

FIGURE IA Simple Model of Incentives for Enforcement

The adjudicatorrsquos incentive for enforcement divides the space of parametervalues into three regions leniency abuse and search

859COASE VERSUS THE COASIANS

enthusiasm for the high-powered enforcement incentives as itshows the risk for abuse particularly in inefcient legal systems

We can use this model to provide further comparative staticsresults summarized in

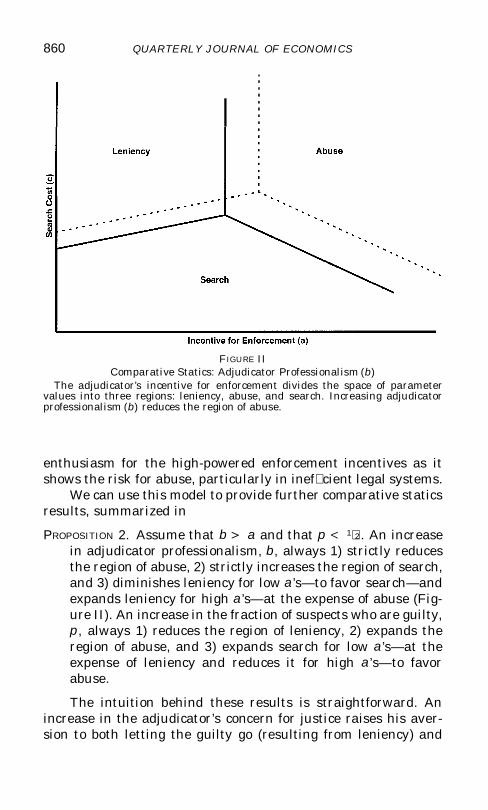

PROPOSITION 2 Assume that b gt a and that p lt 12 An increasein adjudicator professionalism b always 1) strictly reducesthe region of abuse 2) strictly increases the region of searchand 3) diminishes leniency for low arsquosmdashto favor searchmdashandexpands leniency for high arsquosmdashat the expense of abuse (Fig-ure II) An increase in the fraction of suspects who are guiltyp always 1) reduces the region of leniency 2) expands theregion of abuse and 3) expands search for low arsquosmdashat theexpense of leniency and reduces it for high arsquosmdashto favorabuse

The intuition behind these results is straightforward Anincrease in the adjudicatorrsquos concern for justice raises his aver-sion to both letting the guilty go (resulting from leniency) and

FIGURE IIComparative Statics Adjudicator Professionalism (b)

The adjudicatorrsquos incentive for enforcement divides the space of parametervalues into three regions leniency abuse and search Increasing adjudicatorprofessionalism (b) reduces the region of abuse

860 QUARTERLY JOURNAL OF ECONOMICS

punishing the innocent (resulting from abuse) As a consequencefor a broader range of parameter values he conducts a searchSince with p lt 12 most suspects are innocent a higher b makesleniency more attractive relative to abuse further shrinking thelatter region

An increase in the guilty share of the population p obviouslyexpands the range of abuse and contracts the range of search Forlow incentives the attractiveness of search rises relative to thatof leniency and hence the scope of search expands For highincentives the attractiveness of search falls relative to that ofabuse and hence the scope of search contracts

B An Extension

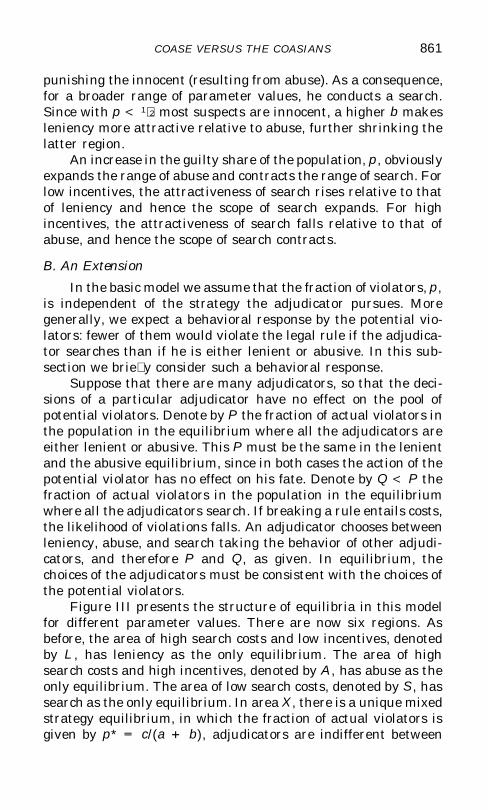

In the basic model we assume that the fraction of violators pis independent of the strategy the adjudicator pursues Moregenerally we expect a behavioral response by the potential vio-lators fewer of them would violate the legal rule if the adjudica-tor searches than if he is either lenient or abusive In this sub-section we briey consider such a behavioral response

Suppose that there are many adjudicators so that the deci-sions of a particular adjudicator have no effect on the pool ofpotential violators Denote by P the fraction of actual violators inthe population in the equilibrium where all the adjudicators areeither lenient or abusive This P must be the same in the lenientand the abusive equilibrium since in both cases the action of thepotential violator has no effect on his fate Denote by Q lt P thefraction of actual violators in the population in the equilibriumwhere all the adjudicators search If breaking a rule entails coststhe likelihood of violations falls An adjudicator chooses betweenleniency abuse and search taking the behavior of other adjudi-cators and therefore P and Q as given In equilibrium thechoices of the adjudicators must be consistent with the choices ofthe potential violators

Figure III presents the structure of equilibria in this modelfor different parameter values There are now six regions Asbefore the area of high search costs and low incentives denotedby L has leniency as the only equilibrium The area of highsearch costs and high incentives denoted by A has abuse as theonly equilibrium The area of low search costs denoted by S hassearch as the only equilibrium In area X there is a unique mixedstrategy equilibrium in which the fraction of actual violators isgiven by p = c(a + b) adjudicators are indifferent between

861COASE VERSUS THE COASIANS

search and leniency and choose them in proportions that makep be the optimal response by the potential violators In area Ythere are three equilibria including pure search pure abuse anda mixture of the two with the fraction of actual violators given byp = 1 2 c(b 2 a) The reason for multiplicity is that startingwith the mixed strategy equilibrium in this region a decision byone adjudicator to become more abusive can increase the incen-tive of the potential violators to break the rule making abuserather than search more attractive for other adjudicators Fi-nally in area Z there are also multiple equilibria including pureabuse

The addition of the behavioral response introduces the pos-sibility of multiple and mixed strategy equilibria (alternativelydifferent adjudicators do different things) Nonetheless the gen-eral thrust of the results including our principal point that pro-viding adjudicators with incentives is desirable for moderate lev-els of investigation costs is preserved

C Implications

What does this analysis imply for the choice of optimal en-forcement incentives To begin we can think of a = 0 as the case

FIGURE IIIIncentives for Enforcement with Behavioral Response by Potential ViolatorsThere are six different regions of equilibria

862 QUARTERLY JOURNAL OF ECONOMICS

of ldquotrue justicerdquo which is perhaps provided by judges truly inde-pendent of the government We can alternatively think of high arsquosas regulators or prosecutors whose careers and budgets dependnot only on doing justice but also on nding violations Onefurther difference between judges and regulators might be thegreater specialization of the latter leading to lower search cost cbut one can of course imagine specialized judges as in the casesof bankruptcy or family law The intermediate arsquos may perhapscorrespond to civil law judges who are part of the civil service andhence may be dependent on the government but who at the sametime have less of an incentive to nd violations than regulators do[Ramseyer and Rasmusen 1997] Using this interpretation thequestion becomes ldquoWho should enforce a particular legal rulerdquo

The model illustrates the costs and benets of enforcementby judges and regulators The government must choose the in-centives of an enforcer namely a (so long as career concerns arenot dominated by outside opportunities) to achieve two objec-tives The rst is to stimulate search as opposed to leniency andthereby to punish the violators (this is the problem that Coasianslargely ignore) The second objective is to achieve justice by notpunishing the innocent (this is the problem that the advocates ofgovernment regulation usually ignore) Increasing a has the bene-t of stimulating search relative to leniency and thereby makingit more likely that the violators are punished but also the costof increasing the likelihood of abusemdashthe punishment of theinnocent as well as the violators without search Put differentlyturning the enforcement of a legal rule over to an apolitical judgehas the benet that the innocent would be rarely punished but ajudgemdashespecially a judge with a low bmdashwould also tend towardleniency In contrast politicizing the system and turning theenforcement to a regulator moves it away from leniency (providedthat this regulator is not captured ie a gt 0) but risks abuse

In principle the government would wish to have judges withvery high brsquosmdasha very professional and motivated judiciary whichhas both sufcient incentives to investigate and a strong interestin justice But this may not be possible In this event the modelsuggests that the best enforcement strategymdashparticularly wheninvestigations are personally expensive (though not prohibitivelyexpensive)mdashmay be to have a regulator with a high enough a toget some search but not so high as to risk abuse How high an athe government chooses would depend on how much it caresabout punishing the violators relative to avoiding punishing the

863COASE VERSUS THE COASIANS

innocent Presumably in the cases where punishing the innocentis particularly expensive to the society such as criminal law thecosts of abuse are sufciently high that most governments wouldstill set a low and allocate adjudication to judges In civil situa-tions however the case for regulation is stronger at least whenc is moderately high The other way of looking at this is thatenforcement reforms which lower c are likely to stimulate searchand lead to more efcient outcomes regardless of whether a judgeor a regulator handles the enforcement

These predictions of the model relate to the case for securitiesmarkets regulation made by James Landis [1938] the architect ofsuch regulation in the United States and one of the rst SECcommissioners Landis was skeptical that the courts were moti-vated enough to punish dishonesty in security issuance and trad-ing in a world where the opportunities for promoters and insidersto expropriate investors were extensive He thought that an in-dependent and highly motivated SEC whose only objective wouldbe to assure the integrity of nancial markets could do thisbetter He also argued that using regulators as adjudicators is abetter strategy because they face lower costs of investigationLower costs encourage search and make abuse less likely for agiven level of incentives The model can thus account for somebasic intuitions for when regulation might be preferred to judicialenforcement

In the following sections we examine the implications of themodel for nancial regulation in Poland and the Czech Republic(and to a lesser extent Hungary) We examine the reform in twocrucial areas governing nancial markets corporate law andsecurities law Corporate law deals in particular with the rela-tionship between corporate insiders and shareholders and istypically enforced through private litigation Securities law regu-lates nancial markets As such it also deals with some aspects ofshareholder protection In addition securities law species thestatus and the powers of the securities regulator and deals withdisclosure of information by securities issuers and intermediar-ies Variation in the securities laws therefore can be interpretedas variation in a and c in the model a more motivated regulatorwould have a higher a and greater disclosure would correspondto a lower c We show that Poland and the Czech Republic haveadopted very different strategies toward shareholder protectionespecially in their securities laws and that these strategies canbe interpreted in light of the model Our evidence suggests that

864 QUARTERLY JOURNAL OF ECONOMICS

the greater success of nancial development in Poland than in theCzech Republic might be related to the more appropriate regula-tory stance in Poland in line with the predictions of the theo-retical analysis

III INITIAL CONDITIONS

In broad terms Poland and Czechoslovakia share similarhistories over the past 50 years Both countries turned commu-nist and became Soviet satellites shortly after World War II andspent the next 40 years building socialism In 1989 the twocountries spearheaded the anticommunist revolution In PolandSolidarity won overwhelming support in the June 1989 electionsand by September 1989 was able to form a government InCzechoslovakia the communists gave up their ldquoleading rolerdquo inthe country in the face of massive protests in November 1989 andthe communist President resigned in December Free elections inJune 1990 completed a sequence of events that came to be knownas ldquothe velvet revolutionrdquo

At the beginning of reforms Poland had a larger populationof 38 million people compared with 103 million in the CzechRepublic The Czech Republic in 1989 had per capita income of$5727 in constant 1995 U S dollars compared with Polandrsquos$3045 Both countries were fully industrialized with an indus-trial structure largely shaped by decades of Soviet-style centralplanning Both countries border on Western Europe and in par-ticular Germany although Warsaw is 569 miles from Frankfurtwhile Prague is only 261 miles away

Both countries initiated economic reforms immediately aftershedding communism In Poland critical legislation on liberaliza-tion was passed in the fall of 1989 and the key measures cameinto effect on January 1 1990 Small-scale privatization began inMay 1990 although large-scale privatization started with a whis-per in 1991 ran into political obstacles and spread over most ofthe 1990s In Czechoslovakia reforms were also initiated in early1990 with the devaluation of the currency budget cuts andbanking reform The formal reform package including price in-creases started on January 1 1991 The law on large-scale pri-vatization was adopted on February 1 1991 Privatizationthrough vouchers took place in two waves in 1992 (completed in

865COASE VERSUS THE COASIANS

mid-1993) and 1993 (completed in 1994) Most rules of privatiza-tion including those on Investment Privatization Funds weredeveloped in 1991 [Coffee 1996]

Moreover both countries were virtually nished withthese basic reforms by 1994 They received virtually identicalscores on every World Bank indicator of the pace of transition[de Melo Denizer and Gelb 1996] The European Bank forReconstruction and Development also ranked them veryclosely (see Table II) Although the Czech Republic moved morerapidly on large-scale privatization and so had a somewhathigher share of its GDP generated in the private sector inmatters such as small-scale privatization governance and re-structuring price and trade liberalization competition policybanking reform and nancial institutions the countries are

TABLE IICOMPARISON OF ECONOMIC REFORM POLICIES BY THE EBRD

PolandCzech

Republic PolandCzech

Republic PolandCzech

Republic

Transitionindicators 1997

Transitionindicators 1996

Transitionindicators 1995

Private sectorshare of GDP 65 75 60 75 60 70

Large-scaleprivatization 3+ 4 3 4 3 4

Small-scaleprivatization 4+ 4+ 4 4 4 4

Governance andrestructuring 3 3 3 3 3 3

Price liberalization 3 3 3 3 3 3Trade and foreign

exchange system 4+ 4+ 4 4 4 4Competition policy 3 3 3 3 3 3Banking reform

and interest rateliberalization 3 3 3 3 3 3

Securities marketand nonbanknancialinstitutions 3+ 3 3 3 3 3

Scale is from 1 (no reform) to 4+ (full reform)Source European Bank for Reconstruction and Development [1997 1996 1995]

866 QUARTERLY JOURNAL OF ECONOMICS

neck and neck and very far advanced4 In short both countrieswere rapid and thorough reformers in their emergence fromcommunism especially in comparison with other transitioneconomies

There are however two differences which we come back tobelow First the Czech large-scale voucher privatization wasfaster and more extensive than privatization in Poland whichover time utilized a variety of methods from direct sales to sharetransfers to mutual funds As a consequence the number ofpublicly held companies in the early 1990s was signicantlyhigher in the Czech Republic than in Poland Second during thisperiod Poland grew faster but also had higher ination than theCzech Republic The assessments of growth rates depend onexactly how they are calculated The level of GDP in Poland in1997 stood at 110 relative to 100 in 1989 whereas in the CzechRepublic it stood only at 90 Using constant 1995 dollars how-ever Polandrsquos advantage is smaller5 During 1992ndash1997 theCzech ination averaged 139 percent per annum while Polishination was signicantly higher at 265 percent

In legal development the two countries again appear similarIn the universe of transition economies both get perfect or nearlyperfect scores although these scores have only been kept after1995 The European Bank for Reconstruction and Developmentevaluates transition economies on the extensiveness of laws(since 1996) effectiveness of laws (since 1996) and overall legaldevelopment (since 1995) Table III Panel A presents the scoresfor Poland and the Czech Republic which again are close to eachother and as high as those of any transition economy6 The legalsystems of the two countries however lagged behind those of richmarket economies Freedom House generates an index of ldquoequal-ity of citizens under the law and access of citizens to a non-discriminatory judiciaryrdquo In 1995ndash1996 both Poland and the

4 In 1997 the EBRD gave Poland a 3+ relative to the Czech Republicrsquos 3 onsecurities markets and nancial institutions We argue below that the differenceshould have been larger

5 The World Bank reports the level of real GDP using constant 1995 pricesbut calculates growth rates using the GDP deator Given the large changes inrelative prices during reforms it is hard to know which measure is better Onevery available measure however Poland has had more growth since 1989 andgrew signicantly faster during the 1995ndash1998 period

6 Pistor [1995] assesses the extent of legal development in a number oftransition economies She gives Poland and the Czech Republic the same scorethe highest (shared with Hungary) among all the transition economies shestudies

867COASE VERSUS THE COASIANS

Czech Republic received scores of 5 out of 10 compared with 75or 10 for the rich industrial countries7 The 1997 World Competi-tiveness Yearbook [IMD 1997] in its question on the legal frame-work gave Poland 416 out of 9 and the Czech Republic 466 Thiscompares with 846 for the world leader Singapore (and overeight generally for rich industrial countries) and the low of 235for Venezuela Finally the 1996 Global Competitiveness Report[World Economic Forum 1996] in its question on condence inthe fair administration of justice gives 293 out of 6 to the CzechRepublic and 292 to Poland This compares with the high of 578for New Zealand and the low of 177 for Russia All the surveysthen treat the judicial systems of the two countries as aboutequally advanced ahead of world laggards yet far behind the richindustrial countries

These results are echoed by the concerns of knowledgeableobservers about the state of the judicial system in the two coun-tries in the early stages of reform [Gray et al 1993] With respect

7 These numbers come from Economic Freedom of the World 1997 by JamesGwartney and Robert Lawson a publication of The Fraser Institute a conserva-tive think tank in Canada

TABLE IIILEGAL ENVIRONMENT

Panel A PolandCzech

Republic PolandCzech

Republic PolandCzech

Republic PolandCzech

Republic

EBRD 1997 1996 1995

Extensivenessof laws 4 4 4 4 na na

Effectivenessof laws 4+ 4 3 4 na na

Overall 4 4 4 4 4 4

Panel B

Wall Street JournalCEER survey

December 1997ndashJanuary 1998

December 1996ndashJanuary 1997

December 1995ndashJanuary 1996

February1995

Rule of lawlegalsafeguards 9 87 9 88 91 91 na na

Legal framework 98 98

Scale for legal extensiveness and legal effectiveness is from 1 (no reform) to 5 (full reform)Scale for rule for lawlegal safeguards and legal framework is from 1 to 10 (the highestbest score)Source European Bank for Reconstruction and Development [1997 1996 1995] and Central European

Economic Review a supplement of the Wall Street Journal Europe (issues indicated in table)

868 QUARTERLY JOURNAL OF ECONOMICS

to Poland Gray et al [p 109] write ldquoMany of the newly appointedjudges lack experience Developing such expertise will taketime Lack of experience and expertise creates uncertainty in thebusiness population rdquo With respect to the Czech RepublicGray et al [p 59] note ldquoAs in other Central and East Europeancountries judicial institutions in the Czech Republic are ill pre-pared to cope with the rapidly emerging challenges of the marketeconomy Incapacity in the court system is likely to be aconstraint for some time to comerdquo

In summary the economies and the economic policies ofPoland and the Czech Republic share some remarkable similari-ties during the 1990s The two countries emerged from socialismwith a need to massively reorganize their economies and pro-ceeded to do so both rapidly and effectively In many crucialrespects they followed similar policies toward this goal andachieved similar results especially compared with other lesssuccessful transition economies

IV COMPANY LAW

Recent research shows that investor protection through com-pany laws and commercial codes is an important deterrent ofexpropriation of outside investors and as such a key determinantof the development of securities markets across countries [LaPorta et al 1997 1998 1999 2000 Johnson et al 2000a] Beforefocusing on securities regulations therefore it is important tocompare Poland and the Czech Republic along this dimension8

La Porta et al [LLSV 1998] propose six dimensions to evalu-ate how well a commercial code (or company law) protects mi-nority shareholders against expropriation by the insiders andcombine them into an index of shareholder protection Table IVPanel A presents and explains this index and its components forPoland and the Czech Republic based on their rst postreform

8 Polandrsquos law dates back to the code of 1934 which was modied repeatedlythrough the communist era and in the early 1990s The Polish commercial codehas both German and French inuences [Gray et al 1993 Pistor 1999] Althoughthe Czech Republic also had a commercial code from the 1930s its laws wereldquomore thoroughly abrogatedrdquo than those of Poland during communism and itaccordingly adopted a new commercial code on January 1 1992 [Gray et al 1993]The principal inuence on the Czech commercial code was German In this andthe following sections we examined the laws adopted in the early 1990s whichare relevant for nancial development during the 1990s Toward the end of thedecade the laws have been revised in both countries particularly in the CzechRepublic

869COASE VERSUS THE COASIANS

TABLE IVCOMPARISON OF LLSV DIMENSIONS

SHAREHOLDER RIGHTS FROM COMMERCIAL CODES

Panel A

Poland CommentLLSVscore Czech Comment

LLSVscore

Proxy-by-mail No Article 405 (proxyin person isallowed)

0 No Article 185 0

Shares blockedbefore generalmeeting ofshareholders

Yes Article 399 (oneweek ahead ofmeeting)

0 Yes (one week aheadof meeting)

0

Oppressedminoritymechanism

Yes Articles 409 and414

1 Yes Can protestdecision ofgeneralassembly

1

Shareholders havepreemptive rightto new issues

No Not mentioned inPolish law

0 No Can be excludedby Articles ofAssociation(Article204(2))

0

Percent of votesneeded to callextraordinarygeneral meeting

10 Article 394 1 10 Article 181 1

Cumulative voting Yes Article 379A combination of

shareholderswith at least20 of theshare capitalcan elect aboard member

1 No Articles 186 and200

51 of the votesis enough toappoint allthe directors13 of seats goto employeesif at least 500workers

0

ldquoAnti-DirectorRightsrdquo indexcalculated as inLLSV

3 2

870 QUARTERLY JOURNAL OF ECONOMICS

Denitions used in Panel A(from LLSV [1998])

One share-one vote Equals one if the company law or commercial code ofthe country requires that ordinary shares carryone vote per share and zero otherwiseEquivalently this variable equals one when thelaw prohibits the existence of both multiple-votingand nonvoting ordinary shares and does not allowsetting maximum number of votes per shareholderirrespective of the number rms of shares ownedand zero otherwise

Proxy by mail allowed Equals one if the company law or commercial codeallows shareholders to mail their proxy vote to therm and zero otherwise

Shares not blockedbefore meeting

Equals one if the company law or commercial codedoes not allow rms to require that shareholdersdeposit their shares prior to a generalshareholders meeting thus preventing them fromselling those shares for a number of days andzero otherwise

Cumulative voting orproportionalrepresentation

Equals one if the company law or commercial codeallows shareholders to cast all their votes for onecandidate standing for election to the board ofdirectors (cumulative voting) or if the companylaw or commercial code allows a mechanism ofproportional representation in the board by whichminority interests may name a proportionalnumber of directors to the board and zerootherwise

Oppressed minoritiesmechanism

Equals one if the company law or commercial codegrants minority shareholders either a judicialvenue to challenge the decisions of management orof the assembly or the right to step out of thecompany by requiring the company to purchasetheir shares when they object to certainfundamental changes such as mergers assetdispositions and changes in the articles ofincorporation The variable equals zero otherwiseMinority shareholders are dened as thoseshareholders who own 10 percent of share capitalor less

Preemptive rights Equals one when the company law or commercialcode grants shareholders the rst opportunity tobuy new issues of stock and this right can bewaived only by a shareholdersrsquo vote equals zerootherwise

Percentage of sharecapital to call anextraordinaryshareholdersrsquo meeting

The minimum percentage of ownership of sharecapital that entitles a shareholder to call for anextraordinary shareholdersrsquo meeting it rangesfrom 1 to 33 percent

871COASE VERSUS THE COASIANS

commercial codes Neither country allows proxy-by-mail (scorezero) each requires that shares be blocked before the annualmeeting of shareholders (score zero) and neither gives sharehold-ers a preemptive right to new share issues (score zero) They eachrequire 10 percent of the votes to call an extraordinary share-holder meeting (score 1) and each provide the minority share-holders with some opportunities to protest certain majority deci-sions (score 1) The two laws differ in one important dimensionusing this classication the Polish law allows a signicant (20percent and in some cases less) minority shareholder to elect adirector Under the Czech law 51 percent of the votes are enoughto appoint all directors Overall Poland ends up with a score of 3out of 6 on anti-director rights and the Czech Republic with ascore of 2

To put these scores in perspective the highest actual share-holder rights score in the LLSV [1998] sample of 49 countries is5 Several common law countries such as the United States theUnited Kingdom and Canada receive this score Belgium is thelowest in the sample with a score of 0 but several countriesincluding Italy Jordan and Mexico get a score of 1 The averagein the sample is 3 Thus Poland is average in the world inprotecting shareholder rights through the company law while theCzech Republic is below the average

Some additional rules in the commercial codes not studiedby LLSV [1998] are also more protective of minority shareholdersin Poland (Table IV Panel B) Poland gives important rights tosignicant minority shareholders (those with either 20 percent ofthe votes or 20 percent of share capital) In Poland but not in theCzech Republic this group can demand the appointment of anadditional board of auditors and not just a seat on the supervi-sory board This group can also check who attended the generalshareholdersrsquo meeting thus keeping the management from ma-nipulating the total number of the available votes Both countriesgenerally require supermajorities for important decisions suchas the change in the objectives of the company Poland grants ashorter term in ofce to directors (three years) than does theCzech Republic (ve years) In one interesting regard the Czechlaw is more protective of minority shareholders Article 185 of theCzech 1992 Commercial Code requires that a quorum of 30 per-cent of the total possible votes be present at a general meeting ofshareholders The Polish Commercial Code does not set any suchquorum (Article 401)

872 QUARTERLY JOURNAL OF ECONOMICS

TABLE IV(CONTINUED)

Panel B

Poland Czech Republic

Further rights ofshareholders ldquoOneshare-one voterdquo (forordinary shares) andno limits on votes pershareholder

No Art 404 canlimit votesof largeshareholders

No Can set max votesper shareholder(Article 180)

Supervisory board andmanagement boardboth elected byshareholdersrsquo meeting

Yes Articles 377and 366

Yes Articles 194 and200

Shareholdersrepresenting at leastone-fth of shares candemand an additionalboard of auditors

Yes Article377(3)

No Not mentioned inCzech law

Shareholders with 10of share capitalrepresented atgeneral meeting cancheck the list ofattendance

Yes Article 403 No Article 185

Two-thirds majority ofgeneral assembly orvotes cast needed forlarge purchases (overone-fth of sharecapital) within twoyears of registrationof company

Yes Article 389 No Not mentioned inCzech law

Two-thirds majority ofgeneral assembly orvotes cast needed tochange articles ofassociation or objectsof company

Yes Article 409each sharehas onevotewithoutpreferencesorrestrictions

Yes Article 187

Term of board ofdirectors(management board)

3 years Article 366and 381

5 years Article 194

Bearer shares allowed Yes Article 345 Yes Article 155 and156

Preference sharesallowed (possiblywithout voting rights)

Yes Article 357 Yes Article 159

Quorum of votes neededto be present

None Article 401 30 Article 185

873COASE VERSUS THE COASIANS

In summary Polandrsquos company law is somewhat more pro-tective of minority shareholders than the Czech law These dif-ferences in themselves however do not appear to be signicantenough to account for the differences in nancial developmentdocumented below

V SECURITIES LAW AND REGULATION

Despite the many crucial similarities the two countries fol-lowed different approaches to reform in terms of the governmentrsquosinterest in regulatory intervention This difference did not escapethe early observers of the two countries who viewed Czech eco-nomic policy as more laissez-faire than Polish economic policyFor example in each of the three years 1994 ndash1996 the conser-vative Heritage Foundation gave the Czech Republic a perfect(from its perspective) score of 1 and Poland a mediocre score of 3on its measure of ldquoregulationrdquomdashthe extent to which governmentrestricts economic activity Along similar lines Euromoney con-sidered Poland to be riskier for foreign investment and lendingthan the Czech Republic in part because property rights wereless secure from government intervention

These observers had every right to form such opinions basedon the pronouncements about markets and market reform comingfrom economic ofcials in the two countries Vaclav Klaus theCzech Finance Minister and later Prime Minister was both tre-mendously articulate and unabashedly antigovernment in hisvision of reforms ldquoWe knew that we had to liberalize deregulateprivatize at a very early stage of the transformation process evenif we might be confronted with rather weak and therefore notfully efcient markets Conceptually it wasmdashat least for memdashrather simple all you had to do was to apply the economic phi-losophy of the University of Chicago [Klaus 1997 from a 1995speech]rdquo Leszek Balcerowicz the champion of Polish reformswas more cautious ldquoThe capacity of the state to deal with variousproblems varies mainly because of varying informational re-quirements On this basis one can distinguish on the one handthe sphere of the statersquos natural competence (legislating andenforcing the law dealing with other states for example) and onthe other hand its sphere of natural incompetence (a massive anddetailed industrial policy for example) [1995 p 176]rdquo

These differences revealed themselves most clearly in theregulation of capital markets The Polish ldquoLaw of Public Trading

874 QUARTERLY JOURNAL OF ECONOMICS

in Securities and Trust Fundsrdquo was adopted on March 22 1991and became effective in early April 1991 The Czech ldquoSecuritiesActrdquo was adopted in 1992 and became effective on January 11993 Although this Act was passed after privatization hadstarted nancial institutions such as Investment PrivatizationFunds (IPFs) apparently did not lobby for or against it In factthe Czech rules were established before privatization started andbefore the IPFs existed and only codied later [Coffee 1996]They were a product of the governmentrsquos economic philosophynot lobbying

In our analysis of securities laws we focus especially on twoissues First we show that there were signicant differences inthe institutions of securities regulation in the two countriesparticularly with respect to the independence and the power ofsecurities regulators We interpret the greater independence andpower of the regulator as an increase in the parameter a in themodel the incentives of the adjudicator Second we show that theissuers and the intermediaries in the two countries faced radi-cally different disclosure requirements so that the regulators hadvery different access to information We interpret the greatermandatory disclosure and the use of intermediaries to enforce itas reductions in the parameter c in the model the cost of search

From this perspective on regulation an examination of secu-rities laws in Poland and the Czech Republic reveals profounddifferences To begin the two laws differed in the identity of thegovernment body supervising securities markets In Poland itwas an independent Securities Commission In the Czech Repub-lic such a commission was not established initially and marketswere supervised by the Capital Markets Supervisors Ofce of theMinistry of Finance The Ministry of Finance during this periodwas rst under Klaus and later when he became Prime Ministerremained indifferent to regulating securities markets Both su-pervisory bodies received the power to generate regulations toissue and revoke licenses and to impose nes for violations ofsecurity laws and regulations but had to refer criminal cases tothe public prosecutor The criminal channel was scarcely used ineither country The fact that the Polish Securities Commissionwas independent and charged solely with supervision of securi-ties markets is likely to have provided it with greater incentivesto nd violations than those faced by the Czech Ministry ofFinance with its much broader agenda

A key difference in the structure of securities laws in the two

875COASE VERSUS THE COASIANS

countries is in the emphasis on the regulation of intermediariesThe idea of focusing the regulation of securities markets on in-termediaries is sometimes credited to James Landis [Landis1938 McCraw 1984] who reasoned that the U S SEC couldmonitor neither the compliance with disclosure reporting andother rules by all listed rms nor the trading practices of allmarket participants Rather the SEC would regulate intermedi-aries such as brokers accounting rms investment advisorsetc placing on them the burden of assuring compliance withregulatory requirements by issuers and traders By maintainingsubstantial administrative power over the intermediaries includ-ing the power to issue and revoke licenses the Commission couldforce them to monitor market participants Moreover the inter-mediaries would be relatively few in number and more concernedwith their own reputations with the SEC compared with most ofthe issuers By privatizing part of the enforcement of disclosure tothe intermediaries the regulator could reduce the share of theenforcement costs he had to bear himselfmdasha reduction in c in ourmodel

Table V compares the two laws from the perspective of theregulation of nancial intermediaries In the regulation of indi-vidual brokers Poland instituted relatively elaborate licensingrequirements accompanied by tests Brokers were supposed toengage in ldquohonest tradingrdquo as interpreted by the Commission andcould lose their license The Czech Republic had much more proforma licensing of brokers with easy exams no warning concern-ing ldquohonest tradingrdquo and evidently no real power of the Commis-sion to revoke licenses The Polish Commission used the broadldquohonest tradingrdquo requirement and its own power to interpret itto discourage brokersrsquo practices that might not have served theinterests of clients

Brokerage rms were also licensed in both countries butfaced considerably stiffer regulations in Poland For example theregulator received the right to access and inspect the books ofbrokerage rms and these rms had to disclose their ownershipstructure stay away from trading in the securities issued by aparent or a subsidiary company and retain organizational andnancial separateness from banks which owned some of themThese regulations did not exist in the Czech Republic It is clearthat the Czech Republic adopted a very hands-off stance towardbrokers and brokerage rms in contrast to Poland

The Czech Securities law contained no regulation of invest-

876 QUARTERLY JOURNAL OF ECONOMICS

TABLE VREGULATION OF INTERMEDIARIES

Poland Czech Republic

Individual brokers

Licensed by securitiesmarket regulator

Yes Articles 182and 141

Yes Section 49

Must pass examadministered bysecurities marketregulator

Yes Article 141(4) No Section 49

Required to engage inldquohonest tradingrdquo and actin the interest of clients

Yes Article 171 No Section 49

License can be suspendedor revoked by SecuritiesCommission

Yes Article 162and 163

Yes Section 49

Brokerage enterprises

Licensed by securitiesmarket regulator

Yes Article 182 Yes Section 45

Securities market regulatorhas right of access andinspection

Yes Article 26 No Sections 45ndash48

License can be suspendedor revoked by securitiesmarket regulator

Yes Article 253 Yes Section 48(2)

Required to engage inldquohonest tradingrdquo and actin the interest of clients

Yes Article 252(3) No Sections 45ndash48

Must not conduct otherbusiness with the samename

Yes Article 186 No Sections 45ndash48

Must report who has morethan 5 percent of votingrights at general meetingof shareholders

Yes Article 232 No Sections 45ndash48

Must report any change ofvoting rights for oneperson above 2 percent

Yes Article 233 No Sections 45ndash48

Bank engaged in brokerageoperations must haveorganizational andnancial separateness ofdepartment for publictrading in securities

Yes Article 24 No Sections 45ndash48

Must not trade securitiesissued by parent orsubsidiary company

Yes Article 31 No Sections 45ndash48

877COASE VERSUS THE COASIANS

TABLE V(CONTINUED)

Poland Czech Republic

Investment advisers(rms engaged in advisory activity in the eld of public trading)

Licensed by securitiesmarket regulator

Yes Article 33 No Not mentioned inthe Czech law

Must pass exam set bysecurities marketregulator

Yes Article 333 No Not mentioned inthe Czech law

Securities market regulatorhas right of access andinspection

Yes Article 33 No Not mentioned inthe Czech law

License can be suspendedor revoked by securitiesmarket regulator

Yes Article 33 No Not mentioned inthe Czech law

Required to engage inldquohonest tradingrdquo and actin the interest of clients

Yes Article 33 No Not mentioned inthe Czech law

Must not conduct otherbusiness with the samename

Yes Article 33 No Not mentioned inthe Czech law

Must report who has morethan 5 percent of votingrights at general meetingof shareholders

Yes Article 33 No Not mentioned inthe Czech law

Must report any change ofvoting rights for oneperson above 2 percent

Yes Article 33 No Not mentioned inthe Czech law

Bank engaged ininvestment advisoryoperations must haveorganizational andnancial separateness ofdepartment for publictrading in securities

Yes Article 33 No Not mentioned inthe Czech law

Must not trade securitiesissued by parent orsubsidiary company

Yes Article 33 No Not mentioned inthe Czech law

Sources Poland Act of Trading in Securities and Trust Funds 1991 Czech Securities Act 1992

878 QUARTERLY JOURNAL OF ECONOMICS

TABLE V(CONTINUED)

Poland Czech

Stock markets

Trading must take place ona stock exchange Yes Article 541 No

Section 50 of theSecurities Law

Securities regulatorcontrols stock exchangerules Yes No

Not mentioned inCzech law

Securities exchange shouldensure a uniform market Yes Article 57(1) No

Not mentioned inCzech law

Securities exchange shouldensure dissemination ofuniform information onthe value of securities Yes Article 57(3) No

Not mentioned inCzech law

Agreements among anygroups to articiallyraise or lower the priceof securities areprohibited Yes Article 643 No

Not mentioned inCzech law

Mutual funds

Mutual funds may beadministered solely bymutual fund companies Yes Article 892 No

Not mentioned inCzech law

Mutual fund companies arelicensed by securitiesregulator Yes Article 89 Yes Section 8

Mutual fund company canbe dissolved by securitiesregulator Yes Article 98 Yes Section 37

Mutual fund companiesmust be joint stockcompanies Yes Article 901 No Section 2

Only registered shares areallowed in mutual fundcompanies (no bearershares) Yes Article 922 No

Not mentioned inCzech law

Closed-end funds areallowed No Article 104 Yes

Founder limited to 10 ofshare capital Yes Article 93(1) No

Not mentioned inCzech law

Founder not allowed to beon Management Board Yes Article 93(1) No

Not mentioned inCzech law

Publicly traded securitiesor governmentobligations Yes Article 107 No Section 17

879COASE VERSUS THE COASIANS

ment advisors the Polish law contained substantial regulationsincluding licensing The Polish law restricted trading to takeplace on a stock exchange and regulated these exchanges to

TABLE V(CONTINUED)

Poland Czech

No more than 5 of thefunds assets can be insecurities issued by oneissuer Yes Article 108 No Section 17

Custodian banks (for mutual funds)

All fund assets must beentrusted to a trusteebank Yes Article 1121 Yes Section 31

Trustee bank must makesure that sale andretirement ofparticipation units in thefund are consonant withthe law and house rulesof the fund Yes

Article1122(2) No

Not mentioned inCzech law

Trustee bank mustcompute the net worth ofthe fundrsquos assets Yes

Article1122(3) No

Not mentioned inCzech law

Trustee bank must notexecute instructions thatare in conict with thelaw or house rules of thefund Yes

Article1122(4) No

Not mentioned inCzech law

Trustee bank must makesure income of the fundis made public Yes

Article1122(6) No

Not mentioned inCzech law

Trustee bank may not be afounder of the mutualfund company or a buyerof its securities or theadministrator of thecompany Yes Article 1131 No

Not mentioned inCzech law

Mutual fund company maynot buy securities issuedby the trustee bank or arelated company Yes Article 1132 No

Not mentioned inCzech law

Source Polish Act of Trading in Securities and Trust Funds 1991 Czech Investment Companies andInvestment Funds Act April 1992 and Stock Exchange Act 1992

880 QUARTERLY JOURNAL OF ECONOMICS

ensure some transparency in trading The Czech law did notinclude such regulations The Polish law contained detailed regu-lations of mutual funds and in fact for several years the entryinto this activity was severely limited The Czech law took a muchmore lenient approach again Finally the Polish law containedstringent regulations of custodian banks which are an importantcheckpoint for changes in ownership that might facilitate tunnel-ing The Czech law again was less restrictive

Finally the Polish Securities law to a much greater extentthan the Czech law established administrative procedures en-abling the securities market regulator to discipline the interme-diaries without recourse to the judicial system The intermediariescould then appeal the decisions of the regulator to administrativecourts but then they rather than the regulator had to face thedelays and the inefciency of the judicial system Because the judi-ciary in neither country is corrupt the regulators had little fear oftheir lawful decisions being overturned

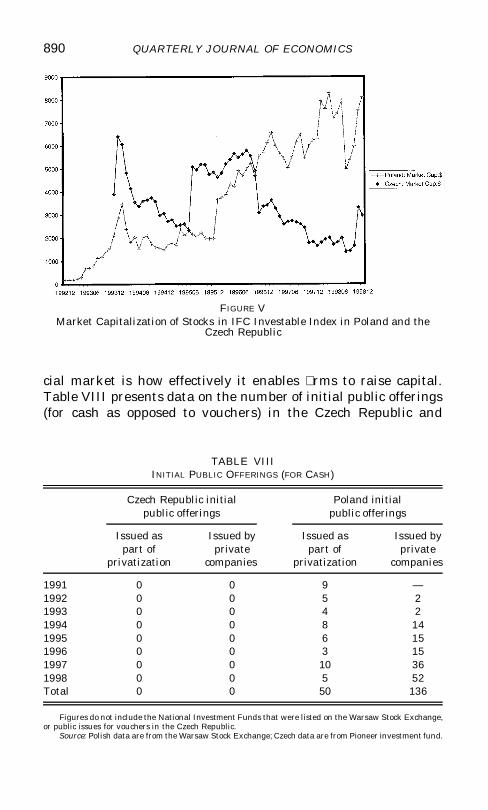

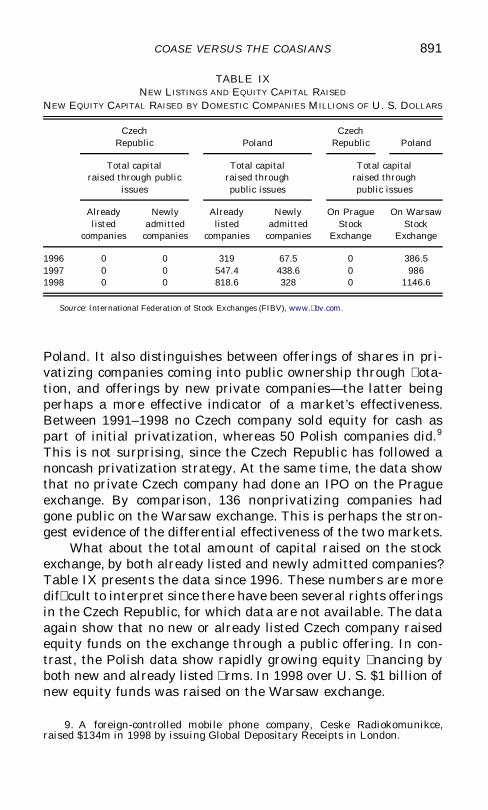

Table VI compares the two original laws from the perspectiveof the regulation of security issuers especially in the area ofdisclosure Recall that greater disclosure of nancial informationcan serve to reduce the cost of information acquisition by a regu-lator or a judge In Poland the introduction of securities to publictrading required both permission of the regulator and a prospec-tus The Czech law required neither The Polish law requiredmonthly quarterly semiannual and annual reporting of nan-cial information the Czech law only the annual results ThePolish law required disclosure of all material information theCzech law only that of signicant adverse developments

Financial results are one area where disclosure may be im-portant ownership structure is another The Polish law requireddisclosure of substantial minority shareholdings the Czech lawdid not Indeed under the original Polish law a shareholdercrossing 10 20 33 50 66 and 75 percent ownership stakes hadto publicly disclosure his ownership The lack of disclosure ofminority shareholdings has been seen as a problem in several WestEuropean countries since it enables anonymous large shareholdersto collude with management and expropriate minority shareholders[European Corporate Governance Network 1997] Finally the orig-inal Polish law also required a mandatory bid for the remainingshares when a 50 percent ownership threshold was reached theCzech law did not Such mandatory bids combined with disclosureof ownership are intended to prevent the expropriation of minority

881COASE VERSUS THE COASIANS

TA

BL

EV

IR

EG

UL

AT

ION

OF

LIS

TE

DC

OM

PA

NIE

S

Pol

and

Cze

chR

epu

blic

Reg

ula

tion

ofli

sted

com

pan

ies

Intr

odu

ctio

nof

secu

riti

esin

topu

blic

trad

ing

requ

ires

perm

issi

onof

the

secu

riti

esre

gula

tor

Yes

Art

icle

49N

oN

otm

enti

oned

inC

zech

law

Intr

odu

ctio

nof

secu

riti

esin

topu

blic

trad

ing

requ

ires

apr

ospe

ctu

sY

esA

rtic

le50

2N

oN

otm

enti

oned

inC

zech

law

Fal

sest

atem

ent

inpr

ospe

ctu

sis

forb

idde

nY

esA

rtic

le11

8Y

esS

ecti

on79

Mon

thly

repo

rtin

gof

n

anci

alin

form

atio

nY

esR

eg

ofS

ecC

omm

an

dS

tock

Exc

han

geN

oN

otm

enti

oned

inC

zech

law

Qua

rter

lyre

port

ing

of

nan

cial

info

rmat

ion

Yes

Reg

of

Sec

Com

m

and

Sto

ckE

xch

ange

No

Not

men

tion

edin

Cze

chla

w

Sem

ian

nu

alre

port

ing

of

nan

cial

info

rmat

ion

Yes

Reg

of

Sec

Com

m

and

Sto

ckE

xch

ange

No

Not

men

tion

edin

Cze

chla

w

An

nua

lre

port

ing

of

nan

cial

info

rmat

ion

Yes

Reg

of

Sec

Com

m

and

Sto

ckE

xch

ange

Yes

Sec

tion

80

Obl

igat

ion

topu

blis

hal

lm

ater

ial

info

rmat

ion

Yes

Reg

of

Sec

Com

m

and

Sto

ckE

xch

ange

No

Sec

tion

80ju

stsi

gni

can

tad

vers

ede

velo

pmen

ts

Con

stra

ints

onpu

rch

aser

spo

ten

tial

con

trol

ling

shar

ehol

ders

Tra

nsp

aren

cyof

own

ersh

ipre

quir

emen

tY

esN

oC

entr

efo

rS

ecu

riti

esca

nch

ange

own

ersh

ipw

ith

out

disc

losu

reT

hre

shol

dat

wh

ich

mus

tde

clar

est

ake

(per

cen

t)N

one

10Y

esA

rtic

le72

No

Not

men

tion

edin

Cze

chla

w20

Yes

No

Not

men

tion

edin

Cze

chla

w33

Yes

No

Not

men

tion

edin

Cze

chla

w50

Yes

No

Not

men

tion

edin

Cze

chla

w66

Yes

No

Not

men

tion

edin

Cze

chla

w75

Yes

No

Not

men

tion

edin

Cze

chla

w

882 QUARTERLY JOURNAL OF ECONOMICS

For

mof

disc

losu

rere

quir

edto

Sec

uri

ties

Com

mis

sion

Yes

No

Not

men

tion

edin

Cze

chla

wT

oA

nti-

Mon

opol

yO

fce

Yes

No

Not

men

tion

edin

Cze

chla

wT

oco

mpa

ny

Yes

No

Not

men

tion

edin

Cze

chla

wC

ompa

ny

mu

stan

nou

nce

wh

oow

ns

mor

eth

an10

Y

esIn

2n

atio

nal

Pol

ish

new

spap

ers

No

Not

men

tion

edin

Cze

chla

w

Th

resh

old

atw

hic

hm

ust

mak

ege

ner

alof

fer

Mu

stm

ake

offe

rif

inte

nd

topa

sssp

eci

edth

resh

old

for

own

ersh

ipst

ake

Yes

An

ype

rson

wh

oin

tend

sto

acqu

ire

shar

esin

one

com

pan

yon

ceor

byw

ayof

repe

ated

tran

sact

ion

sbe

com

ing

wit

hin

12m

onth

sth

eh

olde

rof

shar

esin

anam

oun

tth

atgu

aran

tees

him

reac

hin

gor

surp

assi

ng

33pe

rcen

tof

vote

sat

the

gen

eral

mee

tin

gsh

all

beob

lige

dto

doso

sole

lyby

way

ofpu

blic

invi

tati

onto

subs

crib

efo

rth

esa

leor

the

exch

ange

orsh

ares

(Art

icle

73)

No

Not

men

tion

edin

Cze

chla

w

Mu

stm

ake

offe

rif

actu

alow

ner

ship

stak

epa

sses

spec

ied

thre

shol

dY

esA

nype

rson

who

has

beco

me

aho

lder

ofsh

ares

inon

eco

mpa

nyre

pres

enti

ngov

er50

perc

ent

ofth

evo

tes

atth

ege

nera

lmee

ting

sha

llbe

oblig

edp

rior

toex

erci

sing

any

pow

ers

resu

ltin

gfr

omth

eri

ght

tovo

tet

oan

noun

cean

invi

tati

onto

subs

crib

efo

rth

esa

leor

exch

ange

ofth

ere

mai

ning

shar

esin

that

com

pany

(Art

icle

87)

No

Not

men

tion

edin

Cze

chla

w

883COASE VERSUS THE COASIANS

TA

BL

EV

I(C

ON

TIN

UE

D)

Pol

and

Cze

chR

epu

blic

Ten

der

offe

rru

les

Not

allo

wed

toh

ide

behi

nda

rela

ted

com

pany

Yes

Can

not

hide

beh

ind

ldquodep

ende

nt

subj

ectrdquo

(Art

icle

72(2

)A

rtic

le73

(2))

No

Not

men

tion

edin

Cze

chla

w

Tra

nsa

ctio

ns

insh

are

onth

est

ock

exch

ange

shou

ldbe

susp

ende

dY

esA

lltr

ansa

ctio

ns

inth

issh

are

onth

est

ock

exch

ange

shou

ldbe

susp

ende

dN

oN

otm

enti

oned

inC

zech

law

Tim

eli

mit

for

subs

crib

ing

Yes

25da

ysN

oN

otm

enti

oned

inC

zech

law

Mu

stbu

yal

lth

esh

ares

offe

red

Yes

No

Not

men

tion

edin

Cze

chla

wS

peci

ed

pric

efo

rpu

rch

ase

t

heC

omm

issi

onm

ayfo

rbid

the

anno

unc

ing

ofth

ein

vita

tion

if

the

pric

eof

fere

din

the

invi

tati

onis

low

erby

10pe

rcen

tth

anth

eav

erag

em

arke

tpr

ice

duri

ng

3m

onth

sim

med

iate

lypr

eced

ing

the

anno

unc

emen

tof

the

invi

tati

on

(Art

icle

74)

The

pric

eof

fere

d

can

not

belo

wer

than

the

hig

hes

tpr

ice

paid

ther

eby

for

the

shar

esin

the

last

12m

onth

sor

wh

ere

nosu

chpr

ice

was

paid

mdashth

eav

erag

em

arke

tpr

ice

inth

ela

st30

days

befo

reth

ean

noun

cem

ent

ofth

ein

vita

tion

Th

epr

ice

shal

lal

sobe

rega

rded

asth

eva

lue

ofth

ings

orri

ghts

inte

nded

tobe

give

nby

the

invi

ting

pers

onin

exch

ange

for

shar

esC

ondi

tion

su

nde

rw

hic

hca

nldquog

opr

ivat

erdquoS

ecu

riti

esC

omm

issi

onm

ust

appr

ove

Yes

Not

spec

ied

Sou

rces

Pol

ish

and

Cze

chS

ecur

itie

sL

aws

884 QUARTERLY JOURNAL OF ECONOMICS

shareholders in tender offers since they force an acquirer to buy outminority shareholders when he gains control

This evidence shows that Poland chose to regulate its secu-rities markets more stringently than the Czech Republic In linewith the model its law provided for extensive disclosure of nan-cial and ownership information a way to reduce c and thus tofacilitate regulation (as well as private governance) The Polishreliance on nancial intermediaries to ensure nancial disclosurecan also be seen as a reduction in c Also in line with the modelPoland relied on administrative control over markets by a moti-vated securities regulator an increase in a relative to judicialenforcement This could in principle motivate the regulators tobecome informed and reduce the likelihood of leniency We nextconsider whether this approach worked

VI OUTCOMES

A Qualitative Assessments

Stable prices rapid privatization and openness to the Westcombined to generate favorable initial assessments of the Czecheconomic reforms By 1996 however there was mounting evi-dence of systematic expropriation of minority shareholders byInvestment Privatization Funds and company insiders colludingwith them Coffee [1996] who rst presented his paper in 1994drew attention to such expropriationmdashwhich came to be knownas tunneling In a typical scheme the managers of an IPF holdinga large stake in a privatized company would agree with themanagers of this company to create a new (possibly off-shore)entity which they would jointly control The IPF might then sellits shares in the company to this entity at below market pricethereby expropriating the shareholders of the IPF The companycould also sell some of its assets or its output to the new entityagain at below fair value thereby expropriating its own minorityshareholders These arrangements between corporate managersand their large shareholders (IPFs) enriched them at the expenseof minority investors in both the rms and the IPFs (see Coffee[1996 1998] for a discussion of tunneling in the Czech Republic)

The laxity of the securities law accommodated tunnelingFirst since transactions did not need to take place on an ex-change large blocks of shares could change hands off the ex-change at less than the prevailing market price Even on an

885COASE VERSUS THE COASIANS

exchange there was no guarantee of price uniformity Moreoverbrokers and brokerage rms had no restrictions on facilitatingsuch transactions nor did the custodian banks have any regula-tory duty to stop them Second since there was no requirement ofownership disclosure the acquirers of large blocks could remainsecret Third without a mandatory bid these acquirers had noobligation to buy out the remaining minority shareholdersFourth the IPFs appear to have been under no restrictions inpursuing such transactions since their management did not oweany clearly regulated duty to their investors let alone to theminority shareholders of the companies they tunneled Fifththere was no reason to disclose any nancial transactions be-tween the new owner of shares and the company since suchtransactions were generally allowed and did not need to be dis-closed except perhaps in the annual report several months laterFinally the minority shareholders had virtually no legal recoursein stopping such expropriation except in a very few cases whenthe oppressed minority mechanism came into play and evensubstantial minority shareholders could not elect their own di-rectors to represent their interests

During the mid-1990s the heyday of tunneling in the CzechRepublic the regulators did very little to stop it Part of theproblem was the weakness of the laws But equally importantwas probably the lack of interest of securities regulators com-bined with judicial ineffectiveness

By 1996 it became widely believed that something had gonewrong with the regulation of the Czech nancial markets InMarch 1996 the Central European Economic Review a publica-tion of the Wall Street Journal surveyed assorted brokerages andfund managers on corporate governance in four transition econo-mies The survey asked respondents to comment on the disclo-sure of large shareholdings transparency of markets quality ofreporting protection of small shareholders and insider tradingThe Polish market came out as the best of the four followed bythe Hungarian market The Czech market came third ahead ofthe Russian market which received the lowest score on everydimension The Polish market outscored the Czech market onevery dimension with large spreads on the disclosure of owner-ship and transparency Consistent with this general assessmentthe International Federation of Stock Exchanges admitted theWarsaw Exchange as a full member as early as 1994 on thegrounds that the regulation of securities markets met its stan-

886 QUARTERLY JOURNAL OF ECONOMICS

dards As of this writing the Prague Stock Exchange still had notbeen admitted even as an associate member

Financial scandals in Poland were typically less egregiousthan those in the Czech Republic and often invited an aggressiveregulatory response The best known Polish scandal involves afailure of a large conglomerate Elektrim to reveal in a prospec-tus an existing agreement to sell some shares in a valuablesubsidiary to a third party at below market price (allegedly as apayment for services) When the agreement came to light Elek-trimrsquos shareholders complained and the Securities Commissionquickly referred the case to a public prosecutor The top managerof Elektrim was forced to step down The Elektrim case illus-trates the crucial interaction between the corporate and securi-ties law in the enforcement of investor rights The failure by thecompany to disclose possibly material information in a prospectuswas the source of the Commissionrsquos investigation under the se-curities law This failed disclosure also brought about an effort bythe outside shareholders to change the board of directors usingthe commercial code which ultimately brought down the topmanager This interplay between the securities law and the com-pany law appears in other countries as well the securities lawforces disclosure which in turn invites shareholder activism us-ing the provisions of company law

The Polish regulator has also been aggressive in its admin-istrative oversight of the intermediaries In 1994 Bank Slaskione of the largest Polish banks which owned the largest broker atthe time was privatized In response to the evidence that thebrokerage arm of the bank favored the insiders in allocatingshares in this privatization the regulators took away its broker-age license This was done against opposition from the Ministry ofFinance