coal gasification opportunities and challenges for...

TRANSCRIPT

1© 2016 Deloitte Touche Tohmatsu India LLP

Coal Gasification

Opportunities and Challenges for

India

Kalpana JainGasification India: 2016

− Need for clean coal

− Why gasification?

− Importance for India

− China story

− Opportunity areas

− Key challenges

− Economics

− Way forward

Contents

2© 2016 Deloitte Touche Tohmatsu India LLP

Need for clean coal

© 2016 Deloitte Touche Tohmatsu India LLP 3

• Coal – prime fossil fuel in India

‒ Abundant reserves

‒ Vital for Energy Security

• Mostly available in low quality, high ash

• Environmental issues

Coal Conversion

• Coal Gasification

• Coal to Liquid

Beneficiation (pre combustion)

• Practical challenges in achieving desired

levels

• Disposal issues

Clean Coal Technologies

Why gasification?

4

Source: Vision 2030” Natural Gas Infrastructure in India, Report by

Industry Group For Petroleum & Natural Gas Regulatory Board

In order to overcome uncertain natural gas

supply, unlocking domestic coal gas potential a

need

• Increasing demand for natural gas in India;

driven by growing economy – resurging

industrial production & infrastructure

development

• Current natural gas shortage estimated at 14.1

million tons; increasing dependence on imports;

price volatility

• Urea shortage estimated at around 7-8 million

tons

39%48%

61%52%

0%

20%

40%

60%

80%

100%

2013-14 2029-30

Imported LNG Domestic sources

Globally, share of unconventional

gas expected to increase

© 2016 Deloitte Touche Tohmatsu India LLP

242.66

378.06

516.97

654.55

746.03

0

100

200

300

400

500

600

700

800

2012-13 2016-17 2021-22 2026-27 2029-30

MM

SC

MD

Natrural Gas Demand in India

Power FertilizerCity Gas IndustrialPetrochem/Refineries Sponge Iron/Steel

Importance for India

5© 2016 Deloitte Touche Tohmatsu India LLP

Government Benefits

• Savings in foreign exchange

• Revenue generation – taxes, duties, royalty, etc.

• Employment generation

Syn Gas

(use as

feed/ fuel)

• Urea

• Steel

• Chemical

• Refinery

• Petrochemical

Coal

Gasification

Potential areas for utilization Recent examples

Company End Use Status

JSPL DRI Operating

GAIL, RCF,

CIL, FCIL

Urea JV formed, initial

studies underway

Adani Urea, Methanol,

SNG

MoU signed with

State Governments

Importance for India

6© 2016 Deloitte Touche Tohmatsu India LLP

Optimization of coal reserve

Reserves (as on 1 April 2014) Proved Indicated Inferred Total

0-300 m 96.3 69.5 10.5 176.3

300-600 m 13.6 58.7 16.5 88.8

0-600 m* 13.8 0.4 0.0 14.2

600 – 1200 m 2.2 13.9 6.1 22.2

Total 125.9 142.5 33.1 301.5

All quantities in billion tons

• Abundant reserves

• Ranked 3rd in non coking coal and lignite

ore deposits

• Potential to generate ~ 2500 m3 of syn gas

per ton of coal

Technical Advantages

• Low emissions

• Low ash disposal

• Low water consumption

• Improved efficiency

• No land degradation, landscape changes

• No R&R issues

• Increased safety

• Saleable by-products

* Jharia coal field

Importance for India

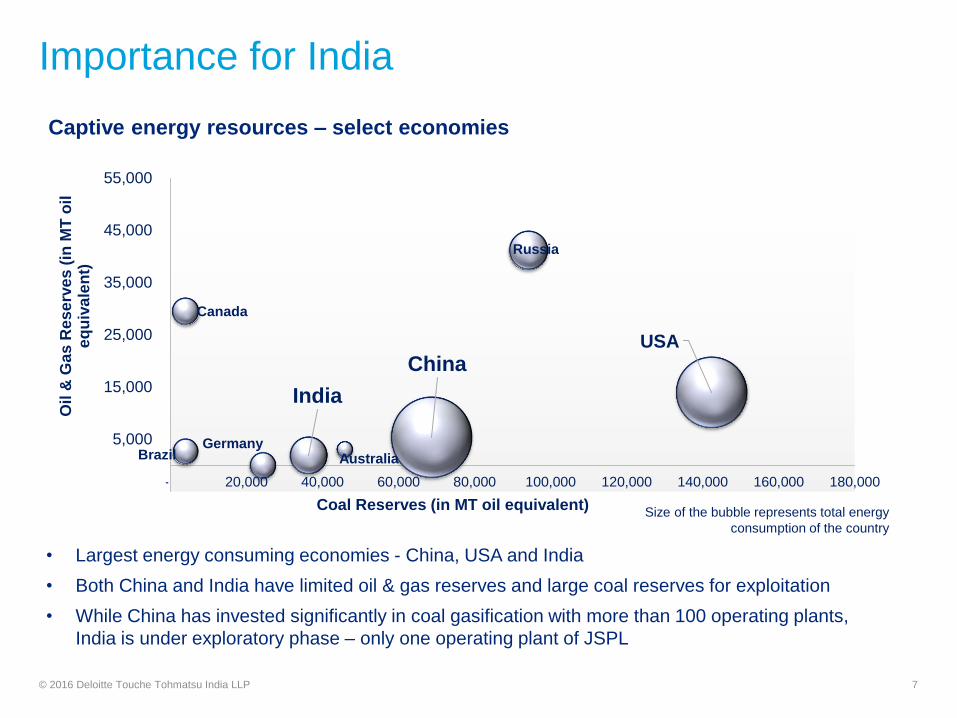

7© 2016 Deloitte Touche Tohmatsu India LLP

Captive energy resources – select economies

• Largest energy consuming economies - China, USA and India

• Both China and India have limited oil & gas reserves and large coal reserves for exploitation

• While China has invested significantly in coal gasification with more than 100 operating plants,

India is under exploratory phase – only one operating plant of JSPL

USA

Canada

BrazilGermany

Russia

China

India

Australia

(5,000)

5,000

15,000

25,000

35,000

45,000

55,000

- 20,000 40,000 60,000 80,000 100,000 120,000 140,000 160,000 180,000

Oil

& G

as

Re

se

rve

s (

in M

T o

il

eq

uiv

ale

nt)

Coal Reserves (in MT oil equivalent)Size of the bubble represents total energy

consumption of the country

China story

8© 2016 Deloitte Touche Tohmatsu India LLP

• Volume of coal gasified: ~ 250,000 tons per day

• More than 107 plants operating and about 40 plants to be commissioned between 2015-19 (coal

consumption of 600,000 tons per day)

Product 2015 2020

Methanol 96.3 66

LPG 13.6 5

DME 13.8 20

Olefin 2.2 15

Ethylene Glycol 1.7 NA

Oil products 2.4 30

Urea 60 NA

Coal gas based production

(million tons)

Product wise distribution of coal

based plants (no. of plants)

3% 2%

11%

32%

50%

2%

Hydrogen

SNH

Chemicals

Ammonia

Methanol

FT-Liquid

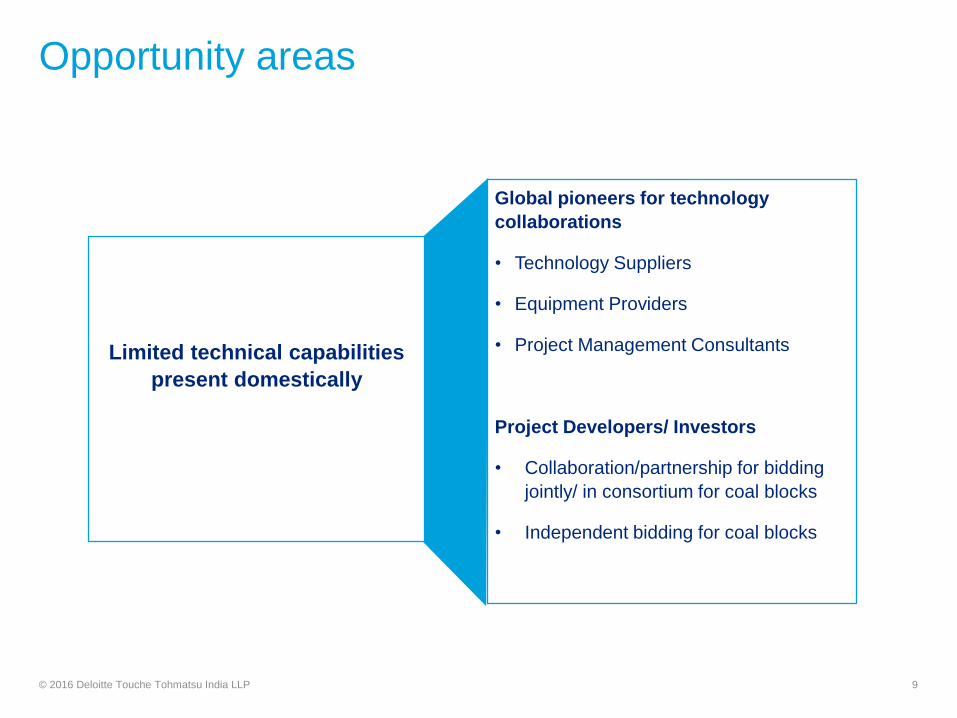

Opportunity areas

9© 2016 Deloitte Touche Tohmatsu India LLP

Global pioneers for technology

collaborations

• Technology Suppliers

• Equipment Providers

• Project Management Consultants

Project Developers/ Investors

• Collaboration/partnership for bidding

jointly/ in consortium for coal blocks

• Independent bidding for coal blocks

Limited technical capabilities

present domestically

Key challenges

10© 2016 Deloitte Touche Tohmatsu India LLP

Risk Areas Challenges Possible Mitigation

Technology • Indian coal quality – high ash

• Lack of proven expertise

• Plant configuration challenge

• By products

• CO2 emissions

• Larger requirement of water & land

• Investment in R&D

• Use of CO2 - Manufacture

products which can consume CO2

e.g. Urea. Possibility of use for

EOR of nearby O&G fields

• Sale of by products

Financing • Relatively higher capital costs as

compared to natural gas based projects

• Long gestation period and development

concerns

• Economic viability concerns

• Government support

• Ownership of block with plant

located at proximity

• Economies of scale

Regulatory • Resistance to coal use

• Coal blocks bidding not allowed for coal

gasification

• Close participation of Government

and Private sector required

• Need for a separate regulatory

framework

Though need of self reliance on energy supply is critical, price competitiveness will play a major role

11© 2016 Deloitte Touche Tohmatsu India LLP

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

US

D /

mm

btu

Indicative price gap (natural gas – coal)* (USD/ mmbtu)

US

Asia**

* Coal prices in USD/ MT converted into equivalent prices in USD/ mmbtu.

Doesn’t include conversion cost of coal gasification

Prices are illustrative

• Price gap between gas and coal is higher in Asia as compared to US

• For India, which is dependent on imported LNG, the gap may be able to cover conversion cost of

gasification

Economics – key driver for coal gas developments

** Japan reference price

In China a Coal To Gas plant

costing $630-950 million for

every BCM of gas capacity

estimated to breakeven at a

gas price of $6.5-8 per mmbtu

Economics – key driver for coal gas developments

12© 2016 Deloitte Touche Tohmatsu India LLP

US

D /

mm

btu

4

8

12

16

20

US gas price

India – current

domestic gas price

India – current

imported LNG

Note: Price estimates are indicative in nature and subject to change based on contract terms,

market and regulatory changes.

India – pooled

gas price for Urea

Economics – An illustration: Production of Urea

13© 2016 Deloitte Touche Tohmatsu India LLP

• Preliminary studies suggest cost of syn gas production from coal could be cheaper by upto 30%

compared to natural gas

• Indicative cost of production (fixed plus variable) of Urea:

Cost through coal gasification*

* Delivered washed coal cost @ ~ INR 2,000 / MT

-

50.00

100.00

150.00

200.00

250.00

300.00

350.00

6 6.5 7 7.5 8 8.5 9 9.5 10 10.5

US

D /

MT

GAS PRICE - USD/ MMBTU

UREA - COST OF PRODUCTION Indicative Capital Cost (1.3

MMTPA) Urea Plant

• Natural gas based:

USD 0.9 – 1 billion

• Coal gas based:

USD 1.2 – 1.4 billion

Way forward…

14© 2016 Deloitte Touche Tohmatsu India LLP

Given the infrastructure development needs and significant coal reserves, investment in

coal gasification needs to grow in coming years ….

Collaborative

development & R&D

Government commitment

and support – strong

governance & regulatory

framework

Technological

advancements

“In countries like India, there are vast opportunities for those wishing to invest in clean coal technology,

since our dependence will not reduce very soon.” – Narendra Modi, Hon’ble Prime Minister of India

Opportunity Potential

&

Economics

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of

which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche

Tohmatsu Limited and its member firms.

This material has been prepared by Deloitte Touche Tohmatsu India LLP (“DTTILLP”), a member of Deloitte Touche Tohmatsu Limited, on a specific request

from you and contains confidential information. The information contained in this material is intended solely for you thereby, any disclosure, copy or further

distribution of this material or the contents thereof is strictly prohibited.

©2016 Deloitte Touche Tohmatsu India LLP. Member of Deloitte Touche Tohmatsu Limited