co proposers in crowdfunding (muller et al. 2016)

TRANSCRIPT

Social Ties in Organizational Crowdfunding:Projects with Visible Members are More Successful

Michael Muller*, Mary Keough**, John Water**,

Werner Geyer*, Alberto Alvarez Saez**,

David Leip**, Cara Viktorov**

*IBM Research and **IBM

CSCW 2016 1

Outline

• Crowdfunding – quick introduction

– On the Internet

– Inside an organization: Democratizing innovation

• The myth of the solitary entrepreneur

– Teams of project proposers

• What happens if the team of proposers is highly visible?

– Project success– Project success

– Mediated by social ties

• Implications and conclusions

2

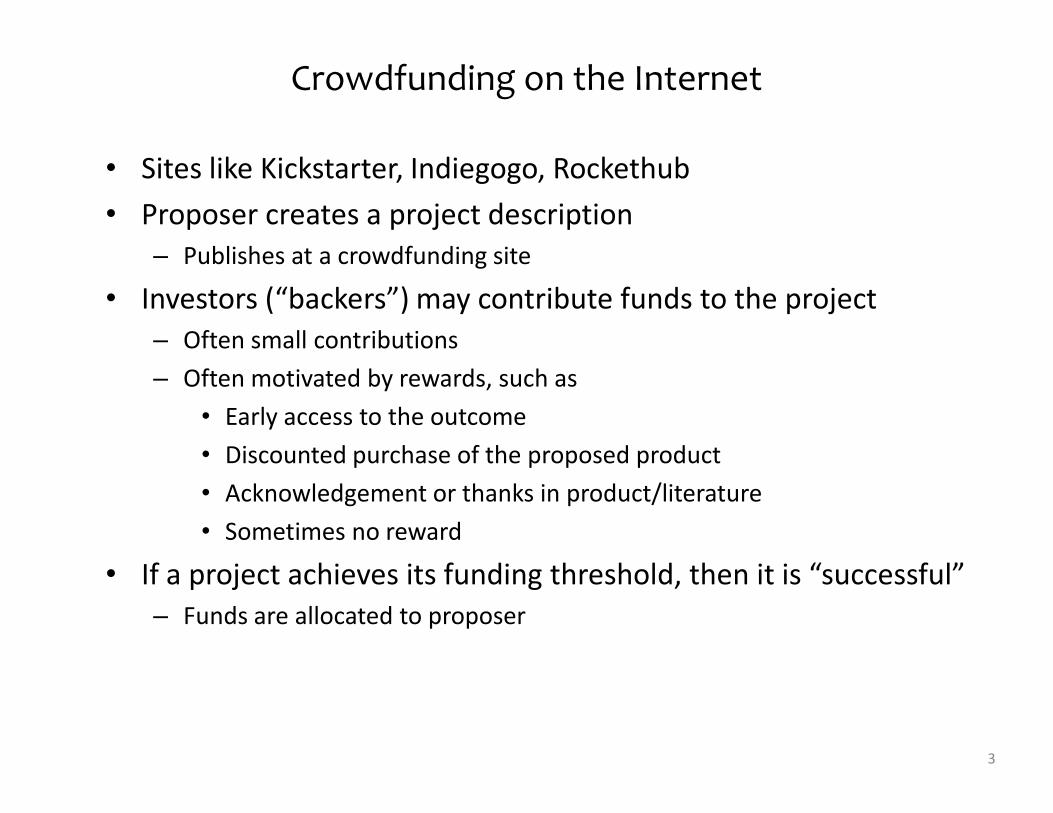

Crowdfunding on the Internet

• Sites like Kickstarter, Indiegogo, Rockethub

• Proposer creates a project description

– Publishes at a crowdfunding site

• Investors (“backers”) may contribute funds to the project

– Often small contributions

– Often motivated by rewards, such as

• Early access to the outcome• Early access to the outcome

• Discounted purchase of the proposed product

• Acknowledgement or thanks in product/literature

• Sometimes no reward

• If a project achieves its funding threshold, then it is “successful”

– Funds are allocated to proposer

3

Background

• Economic and business theorists [Belleflamme et al., 2012; Mollick, 2012;

Ordanini et al., 2011]

– “microfinance” [Mollick, 2012]

• Collaboration and competition in crowdfunding [Lin et al., 2014; Renault, 2014]

• Success factors [Belleflamme et al., 2012; Bock et al., 2014; Burtsch et al., 2013; Etter

et al., 2013; Greenberg & Gerber, 2014; Greenberg et al., 2013a, 2013b; Harburg et al., 2015;

Harms, 2007; Hui et al., 2013, 2014a; 2014b; Mollick, 2012; Muller et al., 2013, 2014;

Ordanini et al., 2011; Zvilichovsky et al., 2014]Ordanini et al., 2011; Zvilichovsky et al., 2014]

– Active promotion of ideas to strangers [Muller et al., 2013; Sakamoto and Nakajima, 2013]

– “Friends and family” [Agarwal et al., 2015; Bock et al., 2014; Burtsch et al., 2013]

– Exploit social ties [Agarwal et al., 2015; Lu et al., 2014], shown

ethnographically by Harburg et al. [2015], quantitatively by Mollick [2012]

• Social capital and social ties

– Theorized more generally by Granovetter [1973]

4

Myth of the Solitary Entrepreneur

• Attractive to individualist culture focused on leaders

– Reified in the design of crowdfunding platforms like Kickstarter

– A nearly “classic” example of concepts of Friedman (Value Sensitive

Design, e.g., [2006]) and of Winner (Do Artifacts Have Politics?)[1976]

• Hui and Gerber: Ethnographic analysis [2013, 2014a, 2014b]

– Projects often require a group of people to create a persuasive proposal [Hui et al., 2014a; Lin et al., 2014]

– Proposers help one another in an informal community of practice

• Mollick; Zvilichovsky: Quantitative analysis [Mollick, 2012; Zvilichovsky et al., 2014]

– Similar conclusions

• However, most Internet sites display only the name of a single

proposer

– Exception: RocketHub

• We also assumed that there was a unitary project proposer

– Until…

5

Organizational Crowdfunding

2012-2014

• Organization assigns

budget to each participant

• Proposer submits project

–

• Participants invest

• Funded project receive

immediate executive

support + operational

assistance

6

Organizational Crowdfunding

2012-2014

• Organization assigns

budget to each participant

• Proposer submits project

–

Mid-2015

• Organization assigns

budget to each participant

• Proposer submits project

– Proposer displays names of

co-Proposers in project

• Participants invest

• Funded project receive

immediate executive

support + operational

assistance

co-Proposers in project

description

• Peers invest

• Funded project receive

immediate executive

support + operational

assistance

7

Example of Projects with and without Members

Proposer and Co-Proposers

appear at top of page

C

Engaging

B

Project with

co-Proposers

Engaging

By Amy Blanks,Ling Shin, Bill Ranney, Sam Curmer, Nora Chen, and Rita Ferrar

Project with

no Co-Proposers

by Nora Chen

A

No

Co-Proposers

Has

Co-Proposers

Proposal

Details

8

Co-Proposers

Original

Proposer

detailed view of one proposal

Ling Shin

Bill Ranney

Sam Curmer

Nora Chen

Rita Ferrar

Amy Blanks

by Amy Blanks et al.

Research Hypotheses

9

Are projects with Co-Proposers More Successful?

• More people to do the work

– However, they have always been involved (Hui and Gerber)

• More visible people � more opportunity for their social

networks to self-engage

• Social ties in crowdfunding

– “Friends and family” (Agarwal et al.)

– Importance of activation of social ties to elicit crowdfunding support

(Hui; Moisseyev; Mollick)

• Importance of social ties for collaboration and community

– Granovetter

10

Data Sets

• Crowdfunding service, ifundIT

– Activity log of proposals, investments, comments …

� For each project:

• Proposer

• Co-Proposers

• Investors

• Investments

• Social networking service, IBM Connections Profiles

– Features from the Beehive project (Di Micco, Geyer, Millen et al.)

� For each person:

• Friend links (bi-directional)

11

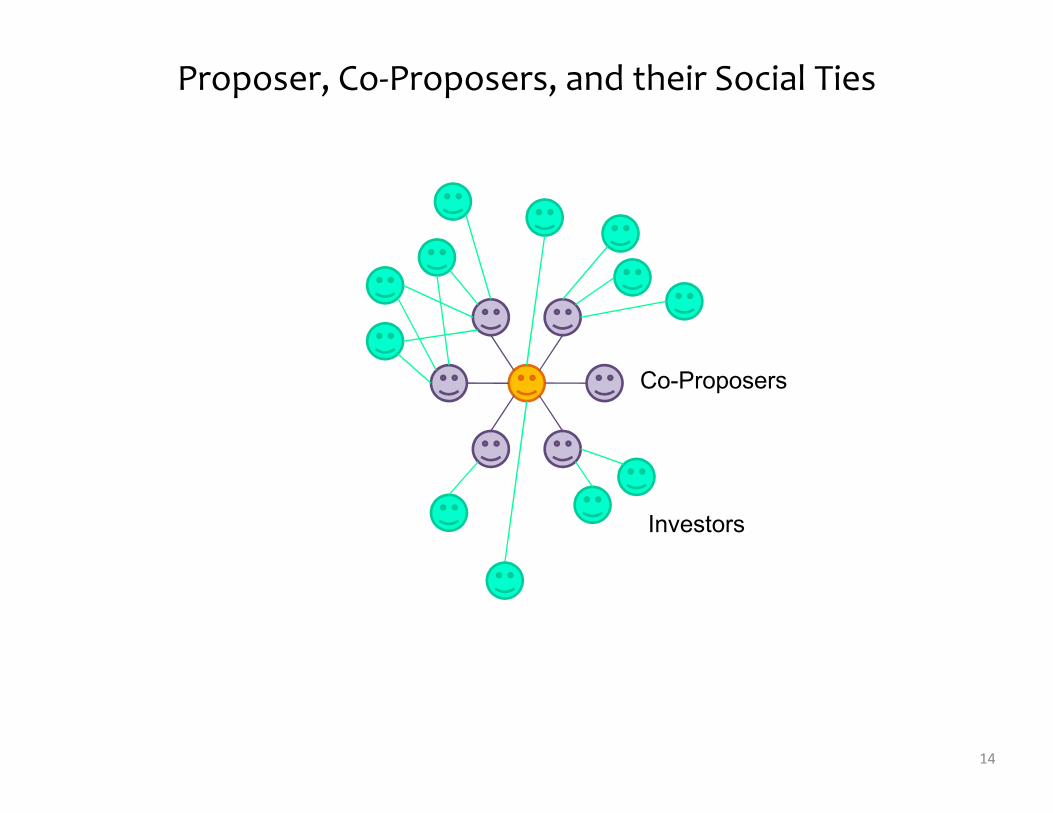

Proposer, Co-Proposers, and their Social Ties

Proposer

12

Proposer

Proposer, Co-Proposers, and their Social Ties

Co-Proposers

13

Proposer, Co-Proposers, and their Social Ties

Co-Proposers

14

Investors

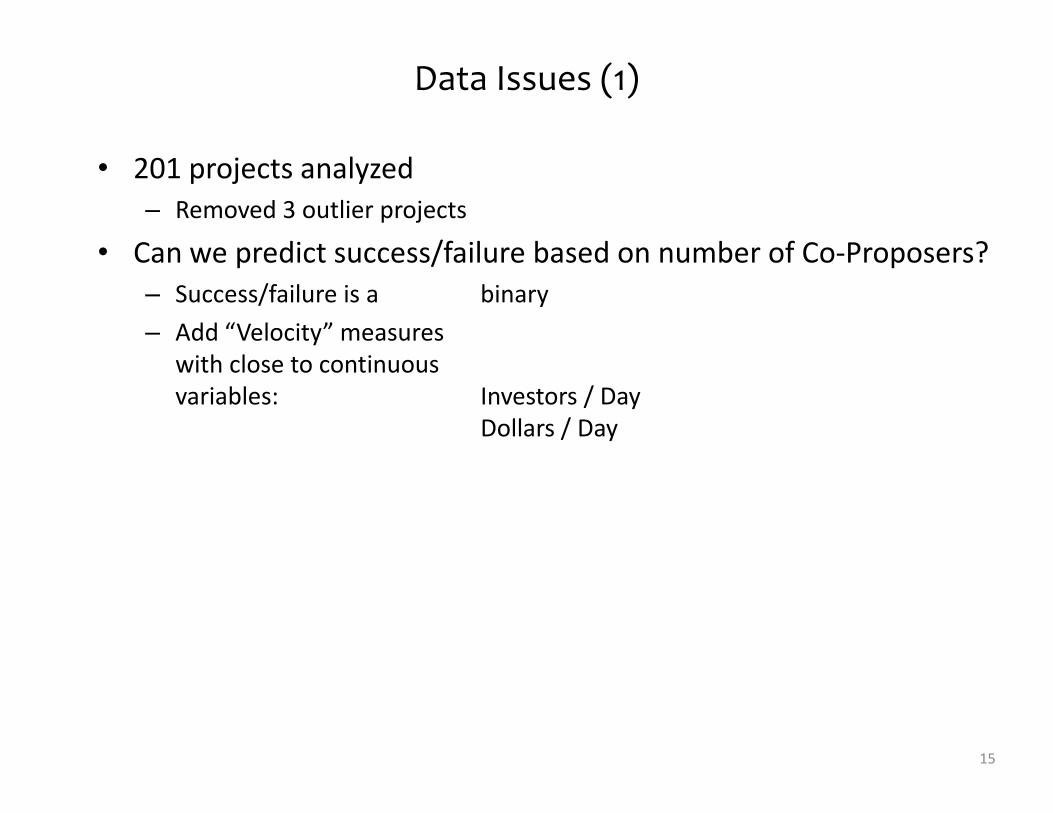

Data Issues (1)

• 201 projects analyzed

– Removed 3 outlier projects

• Can we predict success/failure based on number of Co-Proposers?

– Success/failure is a binary

– Add “Velocity” measures

with close to continuous

variables: Investors / Dayvariables: Investors / Day

Dollars / Day

15

Research Hypotheses: Focus on Co-Proposers

Core hypotheses

• RH1: Projects with more Co-Proposers will be more successful

– RH1a: … as measured by Success/Failure to raise targeted funding level

– RH1b: … as measured by Investors / Day

– RH1c: … as measured by Dollars / Day

• RH2: Projects with more Co-Proposers � more social ties

• RH3: Projects with more social ties � more socially-tied investors (people)

• RH4: Projects with more socially-tied investors � more socially-tied • RH4: Projects with more socially-tied investors � more socially-tied

investments (dollars)

Additional hypotheses

• RH5: Projects with more Co-Proposers � more socially-tied investors

(people)

• RH6: Projects with more Co-Proposers � more socially-tied investments

(dollars)

16

Results

17

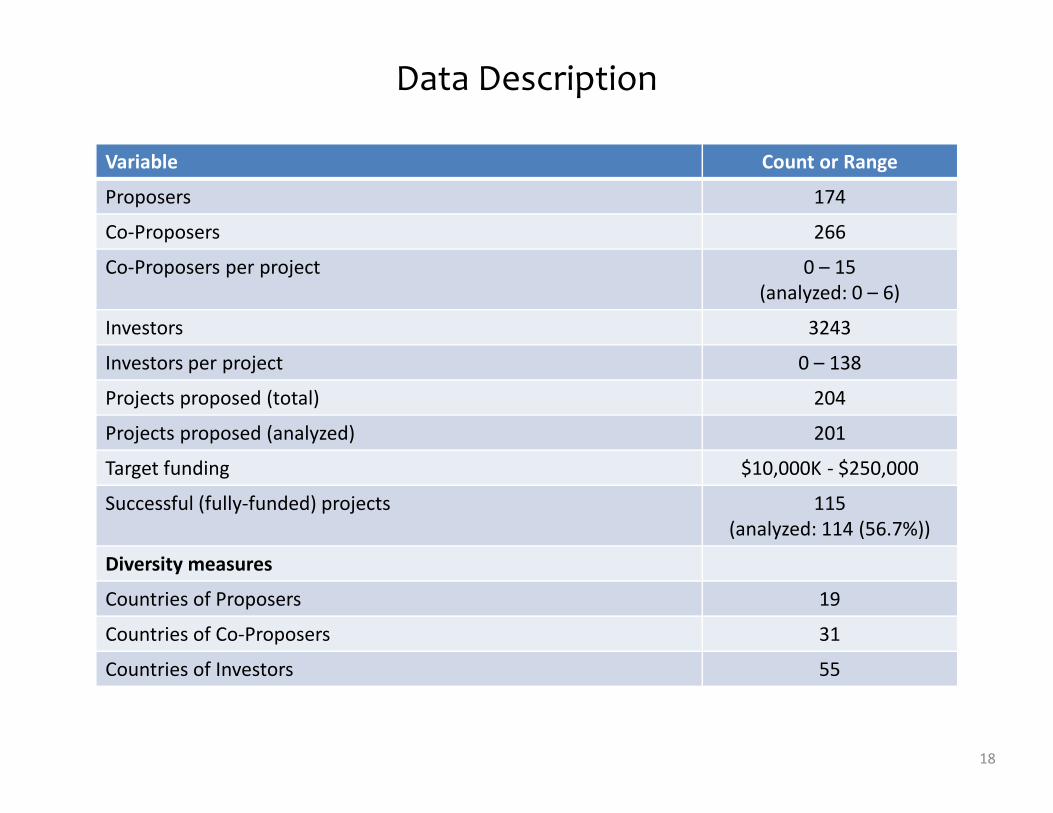

Data Description

Variable Count or Range

Proposers 174

Co-Proposers 266

Co-Proposers per project 0 – 15

(analyzed: 0 – 6)

Investors 3243

Investors per project 0 – 138

Projects proposed (total) 204Projects proposed (total) 204

Projects proposed (analyzed) 201

Target funding $10,000K - $250,000

Successful (fully-funded) projects 115

(analyzed: 114 (56.7%))

Diversity measures

Countries of Proposers 19

Countries of Co-Proposers 31

Countries of Investors 55

18

Data Description

Variable Count or Range

Proposers 174

Co-Proposers 266

Co-Proposers per project 0 – 15

(analyzed: 0 – 6)

Investors 3243

Investors per project 0 – 138

Projects proposed (total) 204Projects proposed (total) 204

Projects proposed (analyzed) 201

Target funding $10,000K - $250,000

Successful (fully-funded) projects 115

(analyzed: 114 (56.7%))

Diversity measures

Countries of Proposers 19

Countries of Co-Proposers 31

Countries of Investors 55

19

Data Issues (2)

• Non-normal distributions

of independent and

dependent data

• Nonparametric statistics

– Theil-Sen slope estimator

(evaluated throughKendall tau

0

20

40

60

80

100

120

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Nu

mb

er

of

Pro

ject

s

Number of Members per Project

(evaluated throughKendall tau

for significance testing) [Theil, 1950]

• Similar to OLS regression slope

– Jonckheere-Terpstra S statistic

(evaluated through Z transformation for significance testing)[Jonckheere, 1954]

• Similar to OLS trend analysis

• Repeated tests on same dataset

– Bonferroni adjustment for significance levels [Bonferroni 1936; Dean, 1959]

20

The Core Components of the Analysis(Figure 3)

ProposerProposer’s

Social Ties

Proposer’s

Socially-tied

Investors

Proposer’s

Socially-tied

Investments ($)Project Success

Co-Proposers’Co-Proposers’ Co-Proposers’

21

p < .001b

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

Co-Proposers

More Sensitive Outcome Measures

ProposerProposer’s

Social Ties

Proposer’s

Socially-tied

Investors

Proposer’s

Socially-tied

Investments ($)Project Success

Co-Proposers’Co-Proposers’ Co-Proposers’

22

p < .001b

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

Co-ProposersInvestors

per Day

Dollars

per Day

RH1a, RH1b, RH1c

ProposerProposer’s

Social Ties

Proposer’s

Socially-tied

Investors

Proposer’s

Socially-tied

Investments ($)Project Success

Co-Proposers’Co-Proposers’ Co-Proposers’

RH1: Projects with more

co-proposers are more

likely to be successful

23

p < .001b

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

Co-Proposers

p < .05

Investors

per Day

Dollars

per Day

p < .01

p < .01RH1b

RH1c

RH1a

RH2

ProposerProposer’s

Social Ties

Proposer’s

Socially-tied

Investors

Proposer’s

Socially-tied

Investments ($)Project Success

Co-Proposers’Co-Proposers’ Co-Proposers’

RH2: More Co-Proposers

� More social ties

24

p < .001b

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

p < .000001

Co-Proposers

p < .05

Investors

per Day

Dollars

per Day

p < .01

p < .01RH1b

RH1c

RH1a

RH2

RH3

ProposerProposer’s

Social Ties

Proposer’s

Socially-tied

Investors

Proposer’s

Socially-tied

Investments ($)Project Success

Co-Proposers’Co-Proposers’ Co-Proposers’

RH3: More social ties �

More socially-tied

investors

25

p < .001b

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

p < .000001

Co-Proposers

p < .05

Investors

per Day

Dollars

per Day

p < .01

p < .01RH1b

RH1c

RH1a

RH2

p < .000001b

RH3

RH4

ProposerProposer’s

Social Ties

Proposer’s

Socially-tied

Investors

Proposer’s

Socially-tied

Investments ($)Project Success

Co-Proposers’Co-Proposers’ Co-Proposers’

RH4: More socially-tied

investors � More socially-

tied investmehts

26

p < .001b

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

p < .000001

Co-Proposers

p < .05

Investors

per Day

Dollars

per Day

p < .01

p < .01RH1b

RH1c

RH1a

RH2

p < .000001b p < .000001b

RH3 RH4

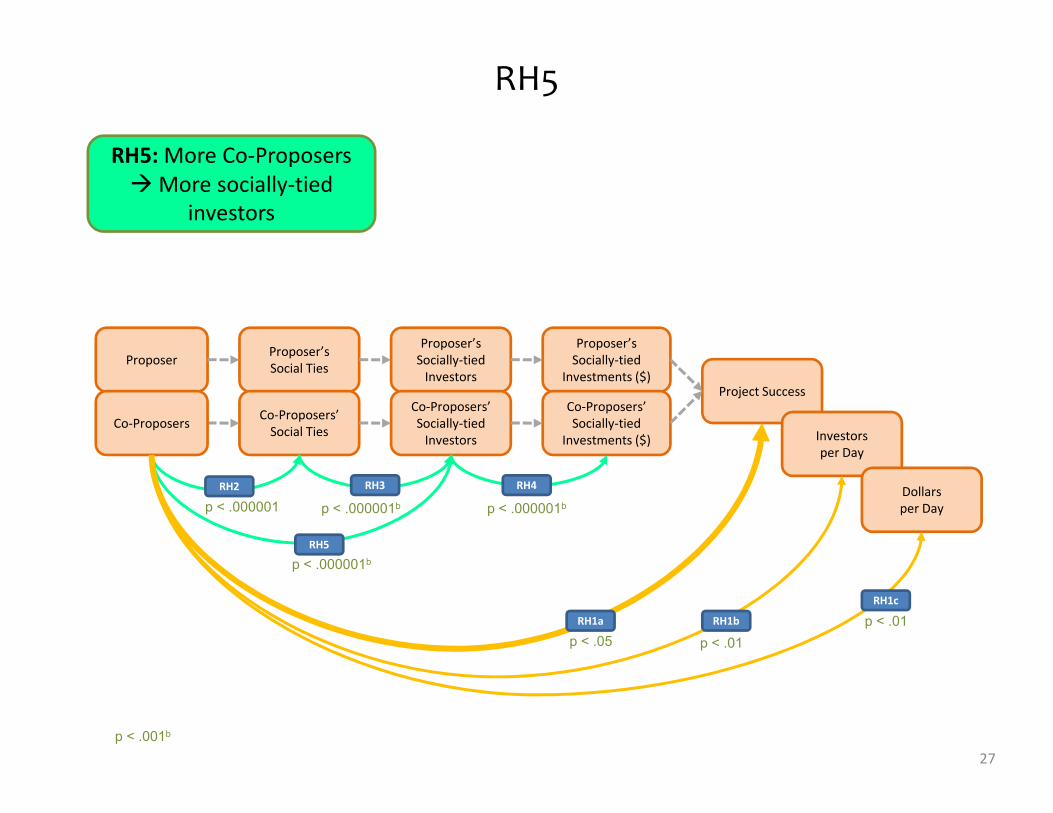

RH5

ProposerProposer’s

Social Ties

Proposer’s

Socially-tied

Investors

Proposer’s

Socially-tied

Investments ($)Project Success

Co-Proposers’Co-Proposers’ Co-Proposers’

RH5: More Co-Proposers

� More socially-tied

investors

27

p < .001b

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

p < .000001

Co-Proposers

p < .05

p < .000001b

Investors

per Day

Dollars

per Day

p < .01

p < .01

RH5

RH1b

RH1c

RH1a

RH2

p < .000001b p < .000001b

RH3 RH4

RH6

ProposerProposer’s

Social Ties

Proposer’s

Socially-tied

Investors

Proposer’s

Socially-tied

Investments ($)Project Success

Co-Proposers’Co-Proposers’ Co-Proposers’

RH6: More Co-Proposers

� More socially-tied

investments

28

p < .001b

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

p < .000001

Co-Proposers

p < .05

p < .000001b

p < .000001b

Investors

per Day

Dollars

per Day

p < .01

p < .01

RH5

RH1b

RH1cRH6

RH1a

RH2

p < .000001b p < .000001b

RH3 RH4

Similar for Proposers

ProposerProposer’s

Social Ties

Proposer’s

Socially-tied

Investors

Proposer’s

Socially-tied

Investments ($)Project Success

Co-Proposers’Co-Proposers’ Co-Proposers’

p < .000001 p < .000001b

p < .000001b

Similar outcomes for

social ties of proposers

29

p < .001b

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

p < .000001

Co-Proposers

p < .05

p < .000001b

p < .000001b

Investors

per Day

Dollars

per Day

p < .01

p < .01

RH5

RH1b

RH1cRH6

RH1a

RH2

p < .000001b p < .000001b

RH3 RH4

Research Hypotheses

Core hypotheses

� RH1: Projects with more Co-Proposers will be more successful

� RH1a: … as measured by Success/Failure to raise targeted funding level

� RH1b: … as measured by Investors / Day

� RH1c: … as measured by Dollars / Day

Social ties

� RH2: Projects with more Co-Proposers � more social ties

� RH3: Projects with more social ties � more socially-tied investors (people)

� RH4: Projects with more socially-tied investors � more socially-tied

investments (dollars)

Additional hypotheses

� RH5: Projects with more Co-Proposers � more socially-tied investors

(people)

� RH6: Projects with more Co-Proposers � more socially-tied investments

(dollars)

30

Another Way to Analyze the Data

31

Research Hypotheses: Focus on Aggregated Proposer Team

Core hypotheses

• RH7: Projects with more Aggregated Proposers will be more successful

– RH7a: … as measured by Success/Failure to raise targeted funding level

– RH7b: … as measured by Investors / Day

– RH7c: … as measured by Dollars / Day

• RH8: Projects with more Proposers � more social ties

• RH9: Projects with more social ties � more socially-tied investors (people)

• RH10: Projects with more socially-tied investors � more socially-tied • RH10: Projects with more socially-tied investors � more socially-tied

investments (dollars)

32

Combine Proposers and Co-Proposers into a Single Team(Figure 4)

Proposers’ + Co-Proposers’ Co-Proposers’ Proposer +

33

Project Success

Proposers’ +

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

Proposer +

Co-Proposers

Investors

per Day

Dollars

per Day

RH7a, RH7b, RH7c

Proposers’ + Co-Proposers’ Co-Proposers’ Proposer +

RH7: Projects with more

proposers are more likely

to be successful

34

Project Success

Proposers’ +

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

Proposer +

Co-Proposers

p < .008

p < .0002

Investors

per Day

Dollars

per Day

p < .0002

RH7b

RH7c

RH7a

RH8

Proposers’ + Co-Proposers’ Co-Proposers’ Proposer +

p < .000001

RH8

RH8: More social ties �

More socially-tied

investors

35

Project Success

Proposers’ +

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

Proposer +

Co-Proposers

p < .008

p < .0002

Investors

per Day

Dollars

per Day

p < .0002

RH7b

RH7c

RH7a

RH9

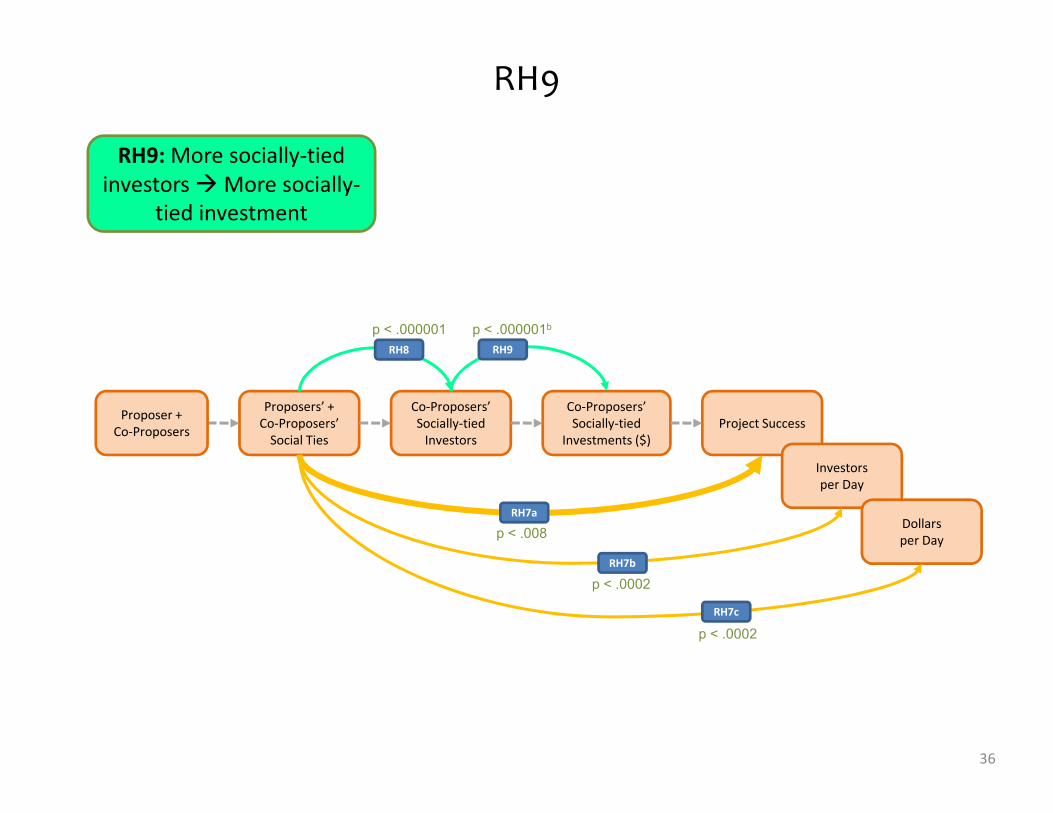

Proposers’ + Co-Proposers’ Co-Proposers’ Proposer +

p < .000001 p < .000001b

RH8 RH9

RH9: More socially-tied

investors � More socially-

tied investment

36

Project Success

Proposers’ +

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

Proposer +

Co-Proposers

p < .008

p < .0002

Investors

per Day

Dollars

per Day

p < .0002

RH7b

RH7c

RH7a

RH10

Proposers’ + Co-Proposers’ Co-Proposers’ Proposer +

p < .000001 p < .000001b

RH8

p < .000001b

RH10

RH9

RH10: More social ties �

More socially-tied

investment

37

Project Success

Proposers’ +

Co-Proposers’

Social Ties

Co-Proposers’

Socially-tied

Investors

Co-Proposers’

Socially-tied

Investments ($)

Proposer +

Co-Proposers

p < .008

p < .0002

Investors

per Day

Dollars

per Day

p < .0002

RH7b

RH7c

RH7a

Research Hypotheses: Focus on Aggregated Proposer Team

Core hypotheses

� RH7: Projects with more Proposers will be more successful

� RH7a: … as measured by Success/Failure to raise targeted funding level

� RH7b: … as measured by Investors / Day

� RH7c: … as measured by Dollars / Day

� RH8: Projects with more Proposers � more social ties

� RH9: Projects with more social ties � more socially-tied investors (people)

� RH10: Projects with more socially-tied investors � more socially-tied � RH10: Projects with more socially-tied investors � more socially-tied

investments (dollars)

38

What Kinds of Social Ties?

39

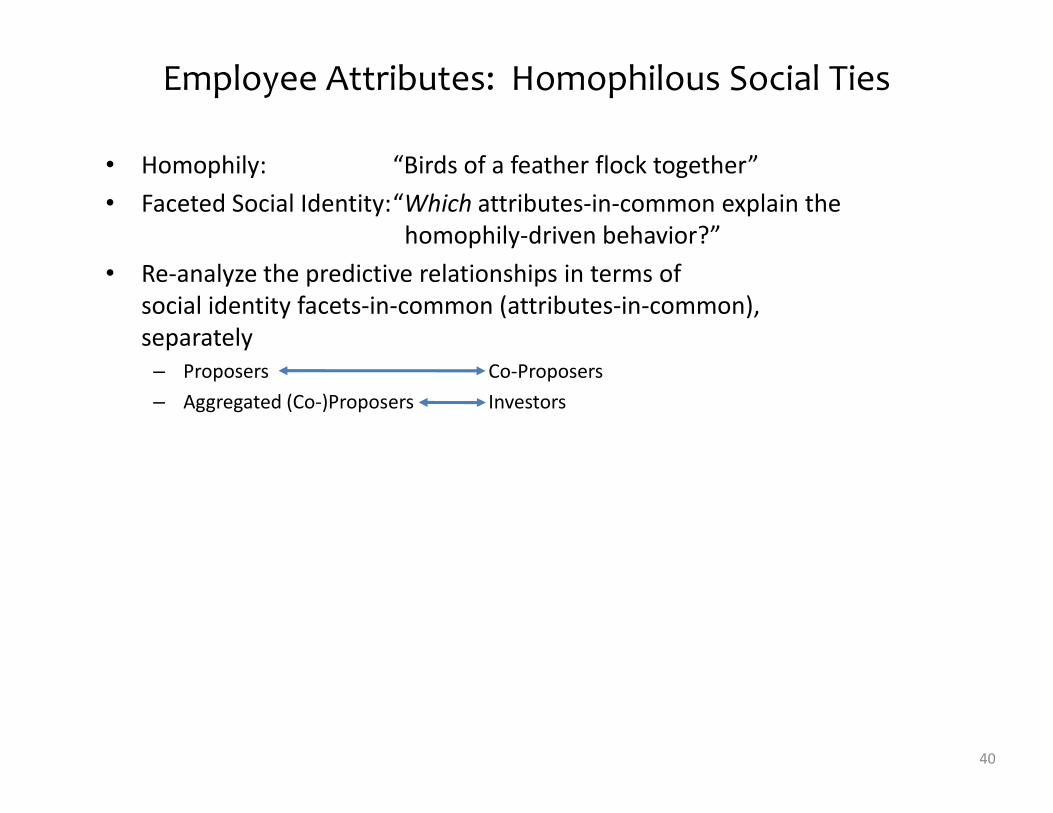

Employee Attributes: Homophilous Social Ties

• Homophily: “Birds of a feather flock together”

• Faceted Social Identity:“Which attributes-in-common explain the

homophily-driven behavior?”

• Re-analyze the predictive relationships in terms of

social identity facets-in-common (attributes-in-common),

separately

– Proposers Co-Proposers

– Aggregated (Co-)Proposers Investors– Aggregated (Co-)Proposers Investors

40

Which Social Identity Facets Matter, & to Whom?

b Significance level after Bonferroni correction

* Initially significant, but not significant after Bonferroni correction

• Why does homophily affect (Co-)Proposers-and-Investors, but not

Relationship Proposers & Co-Proposers (Co-)Proposers & Investors

Facet

(Attribute-in-Common)

Country Division Dept. Country Division Dept.

Success

Investors/Day

Dollars/Day

n.s.

n.s.

n.s.

p<.009b

n.s.*

n.s.*

n.s.

n.s.

n.s.

p<.001b

p<.001b

p<.001b

p<.001b

p<.001b

p<.001b

p<.001b

n.s.*

n.s.*

• Why does homophily affect (Co-)Proposers-and-Investors, but not

Proposers-and-Co-Proposers?

• Hui and Gerber: Proposers choose their Co-Proposers for necessary skills

• Perhaps skill-based selection is stronger than homophily for Proposers-and-

Co-Proposers relationships

41

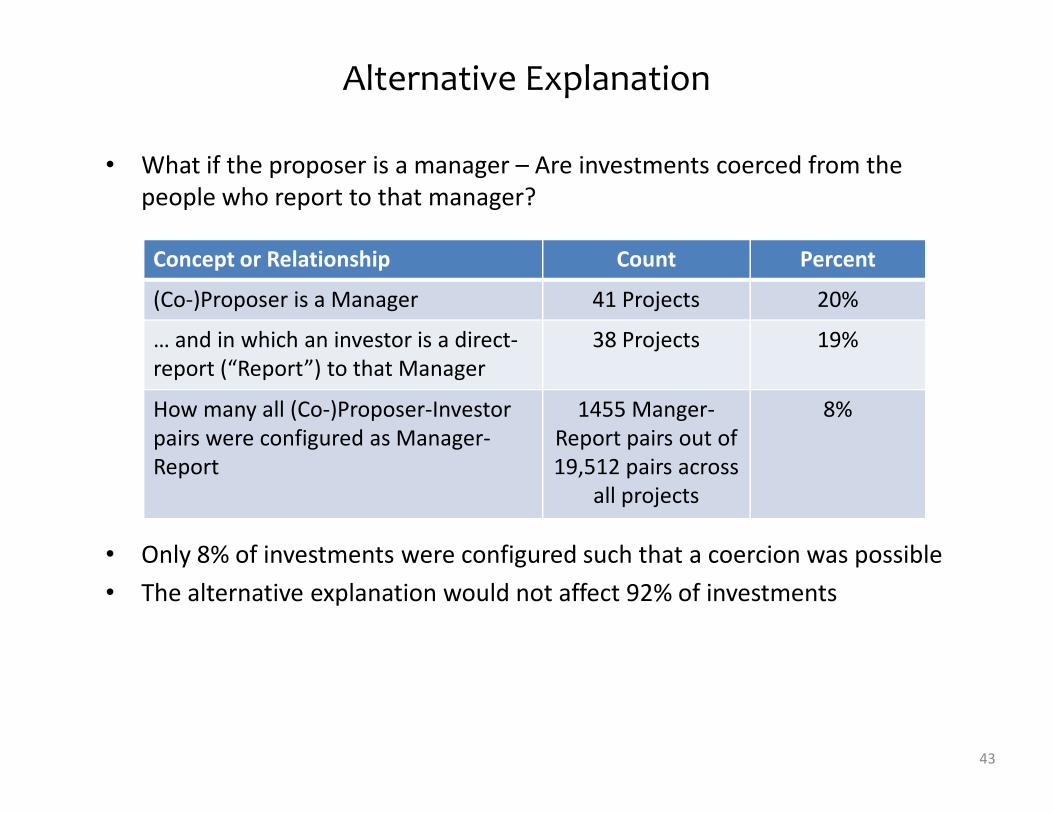

But what if there is anAlternative Explanation?

42

Alternative Explanation

• What if the proposer is a manager – Are investments coerced from the

people who report to that manager?

Concept or Relationship Count Percent

(Co-)Proposer is a Manager 41 Projects 20%

… and in which an investor is a direct-

report (“Report”) to that Manager

38 Projects 19%

How many all (Co-)Proposer-Investor 1455 Manger- 8%

• Only 8% of investments were configured such that a coercion was possible

• The alternative explanation would not affect 92% of investments

43

How many all (Co-)Proposer-Investor

pairs were configured as Manager-

Report

1455 Manger-

Report pairs out of

19,512 pairs across

all projects

8%

Summing Up

44

Conclusions (1)

• Findings

� Quantitative support for the ethnographic report of Hui and Gerber:

Collaboration matters in crowdfunding [Hui et al., 2013, 2014a, 2014b]

� Groups are more successful than individuals [Greenberg et al., 2013a, 2013b,

2014]

� Part of the effect is mediated through social ties [Hui et al., 2013, 2014a,

2014b; Mollick, 2012; Muller et al., 2014]

• Theory• Theory

� Social ties matter in (organizational) crowdfunding [Agarwal et al., 2015; Lu

et al., 2014; Mollick, 2012; Zvilichovsky, 2014]

�Ties of the proposer, Ties of the co-proposers

• Perhaps ties of the investors? (future work)

– Further study

• Is tie-strength is important, or is it only the existence of a tie?

• Some social ties are created through the crowdfunding: Do

proposers and investors increase their social networks through

participation in crowdfunding? (thanks to Tanja Aitamurto)45

Our Current Analysis

Co-Proposers

46

Investors

Expand to the Social Ties of the Investors?

Co-Proposers

47

Investors

Social ties of the Investors

Conclusions (2)

• Findings

� Quantitative support for the ethnographic report of Hui and Gerber:

Collaboration matters in crowdfunding [Hui et al., 2013, 2014a, 2014b]

� Groups are more successful than individuals [Greenberg et al., 2013a, 2013b,

2014]

� Part of the effect is mediated through social ties [Hui et al., 2013, 2014a,

2014b; Mollick, 2012; Muller et al., 2014]

• Theory• Theory

� Social ties matter in (organizational) crowdfunding [Agarwal et al., 2015; Lu

et al., 2014; Mollick, 2012; Zvilichovsky, 2014]

�Ties of the proposer, Ties of the co-proposers

• Perhaps ties of the investors? (future work)

– Further study

• Is tie-strength is important, or is it only the existence of a tie?

• Some social ties are created through crowdfunding [Muller et al., 2014]:

Do proposers and investors increase their social networks through

participation in crowdfunding? (thanks to Tanja Aitamurto)48

Conclusions (3)

• Design

– Crowdfunding sites, and proposers at those sites, may be able to

increase success rates by making collaborators more visible

– Should platforms provide support to engage the social networks of

investors who commit to a project?

• Systems

– Recommendation agents to help recruit co-proposers and investors– Recommendation agents to help recruit co-proposers and investors

• Organizations

– Innovation teams are stronger than solitary individuals

– Organizational crowdfunding is a promising approach to

• Engage the workforce

• Democratize innovation

49

Presentation available at Slideshare.nethttp://www.slideshare.net/traincroft/co-proposers-in-crowdfunding-muller-et-al-2016-58941402

or fromor from

50