chris de vries - venmyn deloitte - partnering for power: mining and power generation partnering to...

TRANSCRIPT

Partnering for Power

Mining and Power Generation Partnering to Deliver

Southern Africa’s Energy Needs

Chris de Vries

Venmyn Deloitte

Mozambique Coal Conference – Maputo

28 July 2015

© 2015 Deloitte Touche Tohmatsu Limited 2

Contents

• Power market disruptors

• Changing power market structures and dynamics

• The Case for Coal IPPs

• Coal IPPs in the Southern African Power Pool

• The Case for Partnership in Coal IPPs and partnership models

• Conclusion: Opportunities in the Coal IPP Sector

3

Southern African

Power Trends

© 2015 Deloitte Touche Tohmatsu Limited 4

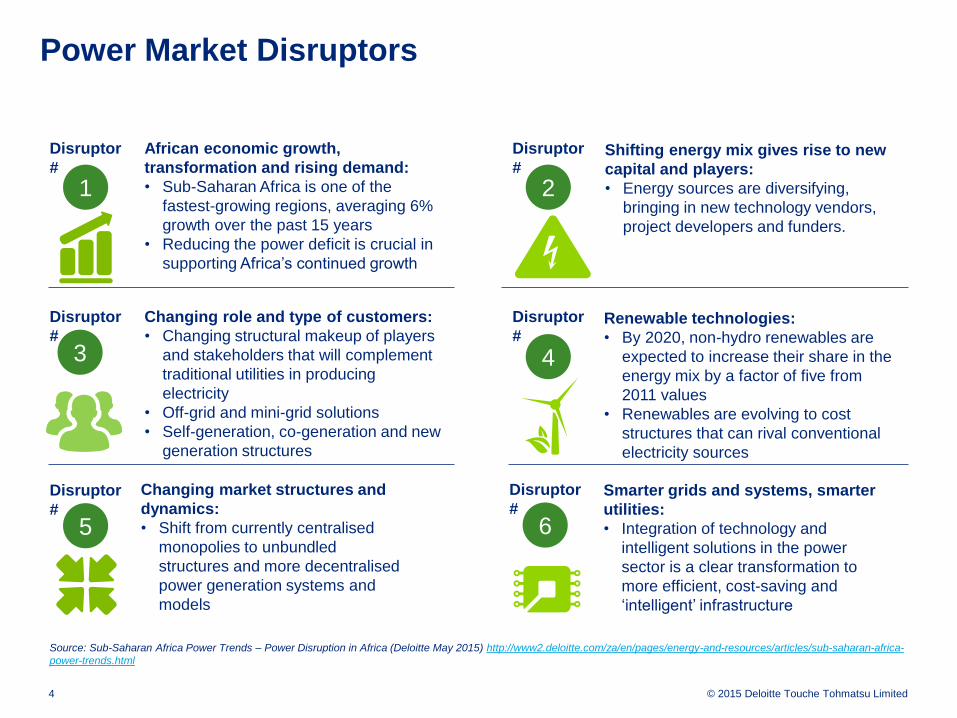

Power Market Disruptors

Source: Sub-Saharan Africa Power Trends – Power Disruption in Africa (Deloitte May 2015) http://www2.deloitte.com/za/en/pages/energy-and-resources/articles/sub-saharan-africa-

power-trends.html

1

African economic growth,

transformation and rising demand:

• Sub-Saharan Africa is one of the

fastest-growing regions, averaging 6%

growth over the past 15 years

• Reducing the power deficit is crucial in

supporting Africa’s continued growth

Disruptor

#

2

Shifting energy mix gives rise to new

capital and players:

• Energy sources are diversifying,

bringing in new technology vendors,

project developers and funders.

Disruptor

#

4

Renewable technologies:

• By 2020, non-hydro renewables are

expected to increase their share in the

energy mix by a factor of five from

2011 values

• Renewables are evolving to cost

structures that can rival conventional

electricity sources

3

Disruptor

#

Changing role and type of customers:

• Changing structural makeup of players

and stakeholders that will complement

traditional utilities in producing

electricity

• Off-grid and mini-grid solutions

• Self-generation, co-generation and new

generation structures

5

Disruptor

#

Changing market structures and

dynamics:

• Shift from currently centralised

monopolies to unbundled

structures and more decentralised

power generation systems and

models

Disruptor

#

6

Disruptor

# Smarter grids and systems, smarter

utilities:

• Integration of technology and

intelligent solutions in the power

sector is a clear transformation to

more efficient, cost-saving and

‘intelligent’ infrastructure

© 2015 Deloitte Touche Tohmatsu Limited 5

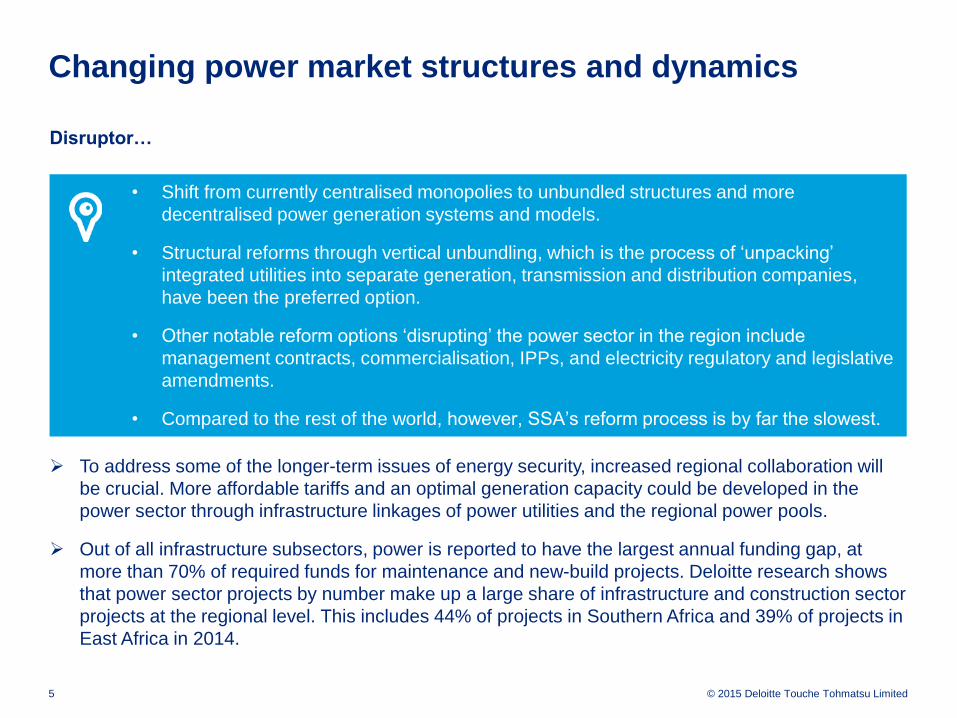

Changing power market structures and dynamics

Disruptor…

• Shift from currently centralised monopolies to unbundled structures and more

decentralised power generation systems and models.

• Structural reforms through vertical unbundling, which is the process of ‘unpacking’

integrated utilities into separate generation, transmission and distribution companies,

have been the preferred option.

• Other notable reform options ‘disrupting’ the power sector in the region include

management contracts, commercialisation, IPPs, and electricity regulatory and legislative

amendments.

• Compared to the rest of the world, however, SSA’s reform process is by far the slowest.

To address some of the longer-term issues of energy security, increased regional collaboration will

be crucial. More affordable tariffs and an optimal generation capacity could be developed in the

power sector through infrastructure linkages of power utilities and the regional power pools.

Out of all infrastructure subsectors, power is reported to have the largest annual funding gap, at

more than 70% of required funds for maintenance and new-build projects. Deloitte research shows

that power sector projects by number make up a large share of infrastructure and construction sector

projects at the regional level. This includes 44% of projects in Southern Africa and 39% of projects in

East Africa in 2014.

6

The Case for Coal

IPPs and the

Partnership Model

© 2015 Deloitte Touche Tohmatsu Limited 7

The Southern African Power

Pool is facing a net power deficit,

with only Mozambique in a

power surplus, albeit insufficient

to address the regional shortfall

Southern African Power Pool – a regional power deficit

Power deficit

Power deficit

Power deficit

Power deficit

Power deficit

Power surplus

© 2015 Deloitte Touche Tohmatsu Limited 8

The age of the IPP

Governments are increasingly looking to the private sector to support energy diversification and

security

Mozambique

• EDM looking to develop two new

hydro projects, but…

• Relying on private sector to develop

coal and gas IPPs

• Have awarded Power Purchase

Agreements (PPAs) to several IPPs

and MOUs with others

Zambia

• 2 PPAs signed with Coal IPPs, one

of which is owned 35% by ZESCO.

ZESCO also signed MOU with

Botswana Coal IPP

Botswana

• 300MW greenfields IPP RFP

• 300MW brownfields IPP RFP

South Africa

• 3725MW Renewable Energy

Independent Power Producer

Procurement Programme

• 2500MW coal baseload IPP

procurement programme

Zimbabwe

• Various greenfields and

brownfields hydro projects

• 22 Licenced IPP projects

• Government developing IPP policy

framework

© 2015 Deloitte Touche Tohmatsu Limited 9

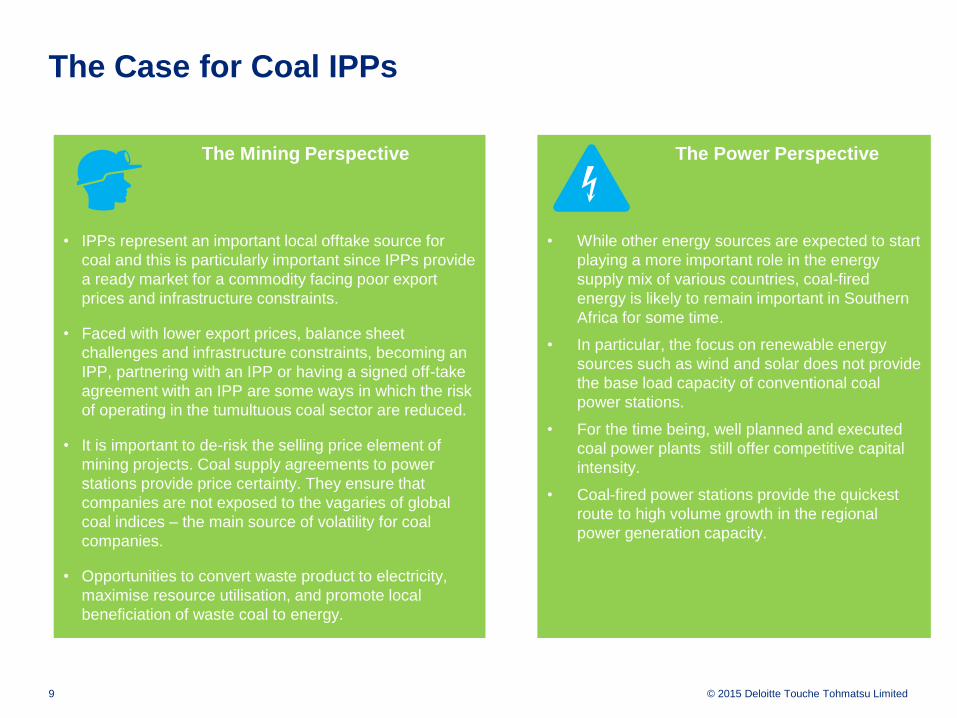

The Case for Coal IPPs

• While other energy sources are expected to start

playing a more important role in the energy

supply mix of various countries, coal-fired

energy is likely to remain important in Southern

Africa for some time.

• In particular, the focus on renewable energy

sources such as wind and solar does not provide

the base load capacity of conventional coal

power stations.

• For the time being, well planned and executed

coal power plants still offer competitive capital

intensity.

• Coal-fired power stations provide the quickest

route to high volume growth in the regional

power generation capacity.

The Power Perspective

• IPPs represent an important local offtake source for

coal and this is particularly important since IPPs provide

a ready market for a commodity facing poor export

prices and infrastructure constraints.

• Faced with lower export prices, balance sheet

challenges and infrastructure constraints, becoming an

IPP, partnering with an IPP or having a signed off-take

agreement with an IPP are some ways in which the risk

of operating in the tumultuous coal sector are reduced.

• It is important to de-risk the selling price element of

mining projects. Coal supply agreements to power

stations provide price certainty. They ensure that

companies are not exposed to the vagaries of global

coal indices – the main source of volatility for coal

companies.

• Opportunities to convert waste product to electricity,

maximise resource utilisation, and promote local

beneficiation of waste coal to energy.

The Mining Perspective

© 2015 Deloitte Touche Tohmatsu Limited 10

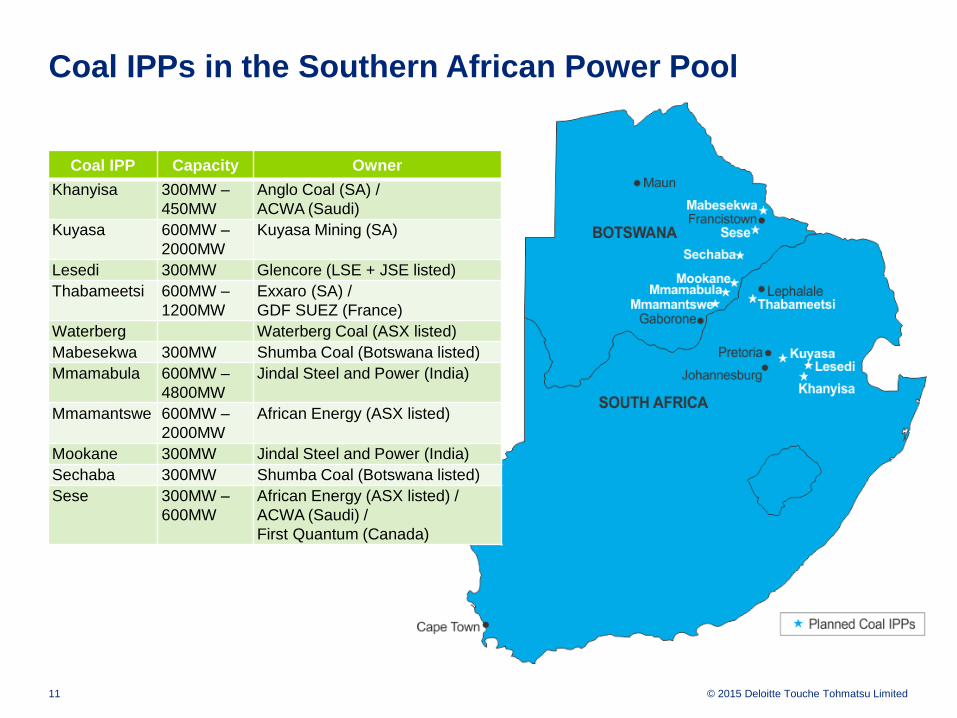

Coal IPPs in the Southern African Power Pool

Planned Coal IPPs

25 Coal IPP projects in 5 countries

© 2015 Deloitte Touche Tohmatsu Limited 11

Coal IPPs in the Southern African Power Pool

Coal IPP Capacity Owner

Khanyisa 300MW –

450MW

Anglo Coal (SA) /

ACWA (Saudi)

Kuyasa 600MW –

2000MW

Kuyasa Mining (SA)

Lesedi 300MW Glencore (LSE + JSE listed)

Thabameetsi 600MW –

1200MW

Exxaro (SA) /

GDF SUEZ (France)

Waterberg Waterberg Coal (ASX listed)

Mabesekwa 300MW Shumba Coal (Botswana listed)

Mmamabula 600MW –

4800MW

Jindal Steel and Power (India)

Mmamantswe 600MW –

2000MW

African Energy (ASX listed)

Mookane 300MW Jindal Steel and Power (India)

Sechaba 300MW Shumba Coal (Botswana listed)

Sese 300MW –

600MW

African Energy (ASX listed) /

ACWA (Saudi) /

First Quantum (Canada)

© 2015 Deloitte Touche Tohmatsu Limited 12

Coal IPPs in the Southern African Power Pool

Coal IPP Capacity Owner

Maamba 300MW –

600MW

Nava Bharat (India) / Government

of Zambia

Sinazongwe 300MW –

600MW

EMCO (India)

Lusulu 600MW –

2000MW

Pan African Sunlight (France)

Sengwa 300MW –

1400MW

RioZim (Zimbabwe)

Shangano 600MW Southern Energy

Entuba 600MW Makomo Resources (Zim) / Sino

Hydro (China)

Gwayi 600MW China Africa Sunlight (China)

Hwange 300MW –

1200MW

Shanghai Electric (China)

Hwange 600MW Essar (India)

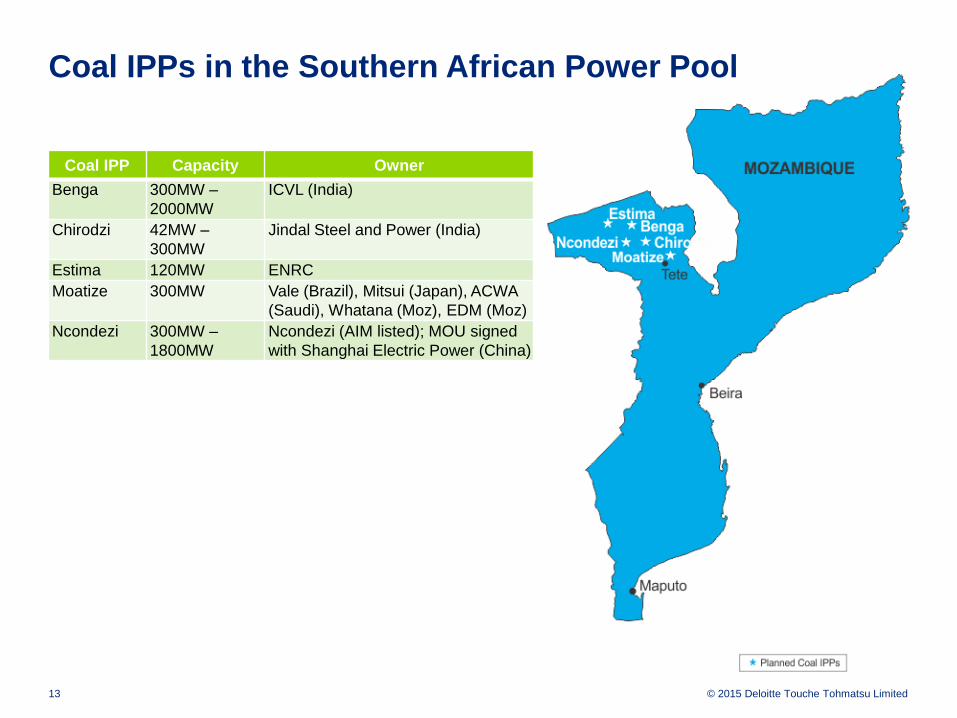

© 2015 Deloitte Touche Tohmatsu Limited 13

Coal IPPs in the Southern African Power Pool

Coal IPP Capacity Owner

Benga 300MW –

2000MW

ICVL (India)

Chirodzi 42MW –

300MW

Jindal Steel and Power (India)

Estima 120MW ENRC

Moatize 300MW Vale (Brazil), Mitsui (Japan), ACWA

(Saudi), Whatana (Moz), EDM (Moz)

Ncondezi 300MW –

1800MW

Ncondezi (AIM listed); MOU signed

with Shanghai Electric Power (China)

© 2015 Deloitte Touche Tohmatsu Limited 14

Funding partners

The Case for Partnership in Coal IPPs

Technical partners

• Mining Companies

• Power companies

• Technology vendors

• Consultants and

service providers

• Banks

• Development finance

institutions

• Private Equity

• Government

investment

• Equity and debt

capital markets

• Vendor finance

Governments

• National power

companies

• Government equity

ownership

• Government

departments

• Inter-governmental

bodies (Southern

African Power Pool)

Delivering a successful Coal IPP calls for partnerships at a technical, funding and governmental

level. Closer relationships between public and private players in terms of technical and funding

models, as well as regional projects and solutions is a key requirement.

© 2015 Deloitte Touche Tohmatsu Limited 15

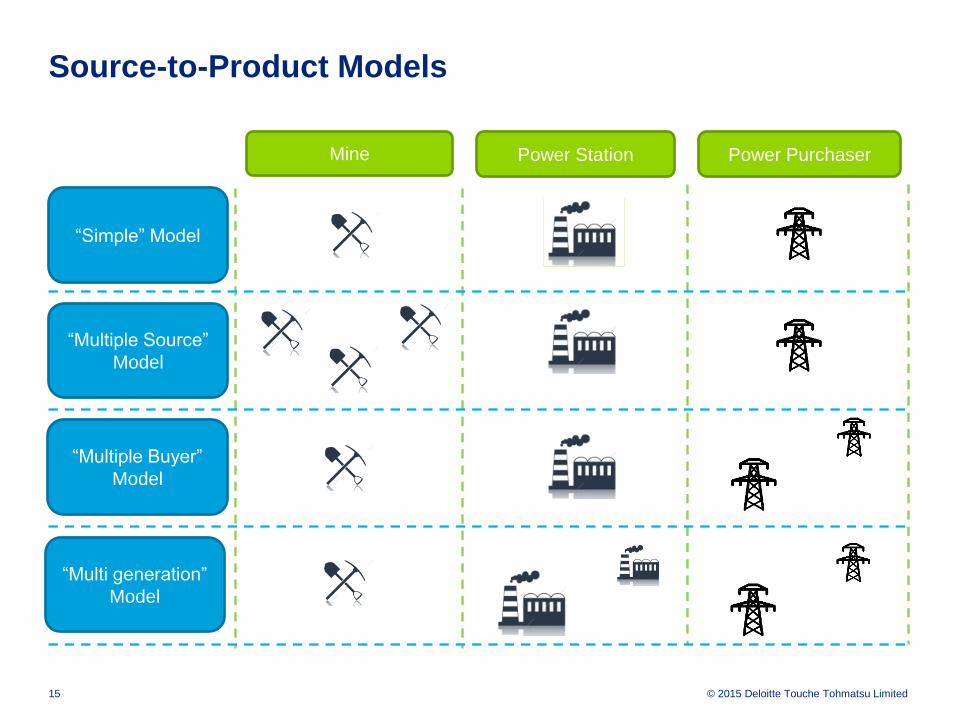

Source-to-Product Models

Mine Power Station Power Purchaser

“Simple” Model

“Multiple Source”

Model

“Multi generation”

Model

“Multiple Buyer”

Model

© 2015 Deloitte Touche Tohmatsu Limited 16

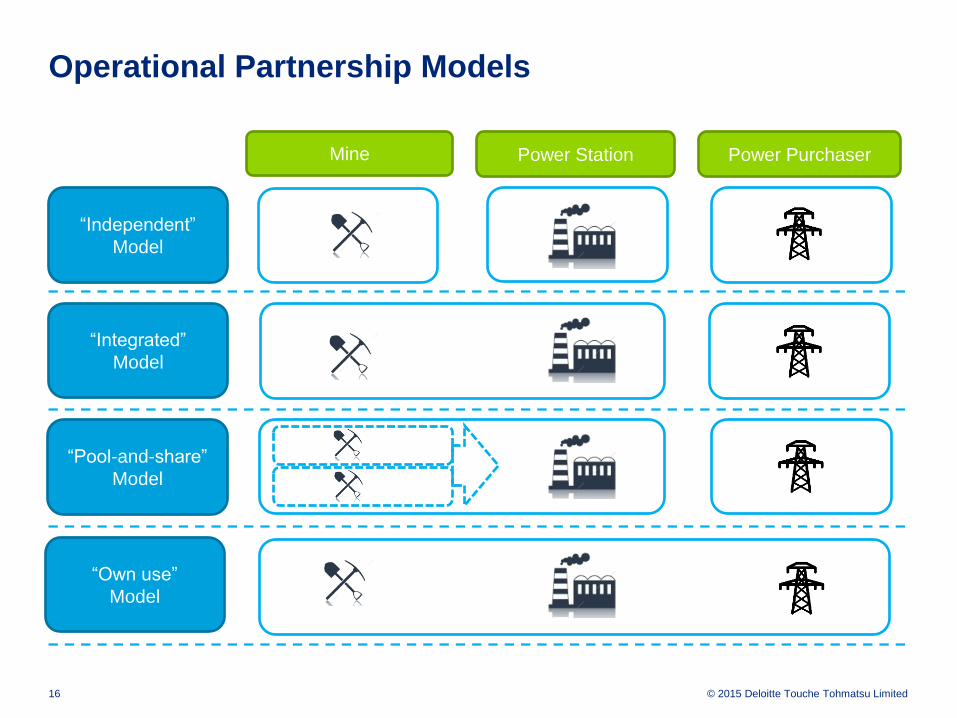

Operational Partnership Models

Mine Power Station Power Purchaser

“Independent”

Model

“Integrated”

Model

“Own use”

Model

“Pool-and-share”

Model

© 2015 Deloitte Touche Tohmatsu Limited 17

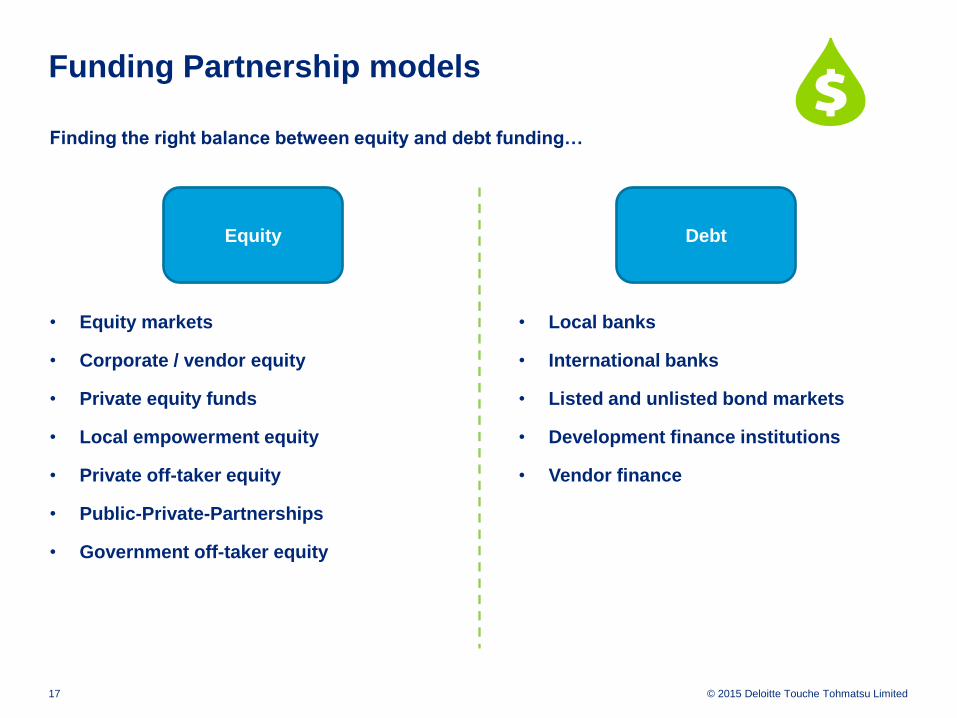

Funding Partnership models

Equity Debt

Finding the right balance between equity and debt funding…

• Equity markets

• Corporate / vendor equity

• Private equity funds

• Local empowerment equity

• Private off-taker equity

• Public-Private-Partnerships

• Government off-taker equity

• Local banks

• International banks

• Listed and unlisted bond markets

• Development finance institutions

• Vendor finance

© 2015 Deloitte Touche Tohmatsu Limited 18

Conclusion: Opportunities in the Coal IPP Sector

Restructuring Utilities Given the restructuring of utilities,

which is encouraging greater

private participation in the African

electricity market, greater

opportunities for private sector

players will emerge, with a

particular focus on sources for

project funding.

Diversified

investment attraction Opportunities also exist

increasingly for non-traditional

funding mechanisms, as

countries seek to supplement

traditional funding mechanisms

that are not meeting project

funding needs.

New-build projects There are various opportunities

within the new build and civil

construction and supply of inputs

environment for power generation

projects in traditional thermal

sectors.

Portfolio optimisation Opportunities exist to work with

national utilities in designing and

implementing optimisation

strategies for both local and

regional generation and

distribution

Southern Africa’s power sector is adapting and rapidly changing in line with global trends and local

realities. While supply to date still continues to fall short of demand requirements, reducing the

current power shortcomings will be crucial in supporting the next chapter of Africa’s growth model.

This makes the market attractive for new entrants. Solutions that are emerging in other parts of the

world will be replicated into the African power sector. A number of global utilities have seen the

continent as a growth market for their businesses, bringing into the market proven technologies that

need localisation.

© 2015 Deloitte Touche Tohmatsu Limited 20

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms,

each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of

Deloitte Touche Tohmatsu Limited and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally

connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and deep local expertise to help clients

succeed wherever they operate. Deloitte's approximately 170,000 professionals are committed to becoming the standard of excel lence.

This publication is for internal distribution and use only among personnel of Deloitte Touche Tohmatsu Limited, its member fi rms, and their related

entities (collectively, the “Deloitte Network”). None of the Deloitte Network shall be responsible for any loss whatsoever sustained by any person

who relies on this publication.