chp 4 market-based valuation: price multiples. 1. introduction among the most familiar and widely...

TRANSCRIPT

CHP 4

MARKET-BASED

VALUATION: PRICE

MULTIPLES

1. INTRODUCTION

Among the most familiar and widely used valuation tools are price multiples.

Price multiples are ratios of a stock’s market price to some measure of value per share.

2. PRICE MULTIPLES IN VALUATION Price multiples are most frequently applied to

valuation using the method of comparables. This method involves using a price multiple to evaluate whether an asset is relatively undervalued, fairly valued, or overvalued in relation to a benchmark value of the multiple.

The benchmark value of the multiple may be the multiple of a similar company or the median or average value of the multiple for a peer

group of companies, an industry, an economic sector, an equity index, or

the median or average own past values of the multiple.

The economic rationale for the method of comparables is the law of one price.

Price multiples may also be applied to valuation using the method based on forecasted fundamentals. Discounted cash flow models provide the basis and rationale for this method.

Fundamentals also interest analysts who use the method of comparables, because differences between a price multiple and its benchmark value may be explained by differences in fundamentals.

3. PRICE TO EARNINGS

The key idea behind the use of P/Es is that earning power is a chief driver of investment value and EPS is probably the primary focus of security analysts’ attention. EPS, however, is frequently subject to distortion, often volatile, and sometimes negative.

The two alternative definitions of P/E are trailing P/E, based on the most recent four quarters of EPS, and leading P/E, based on next year’s expected earnings.

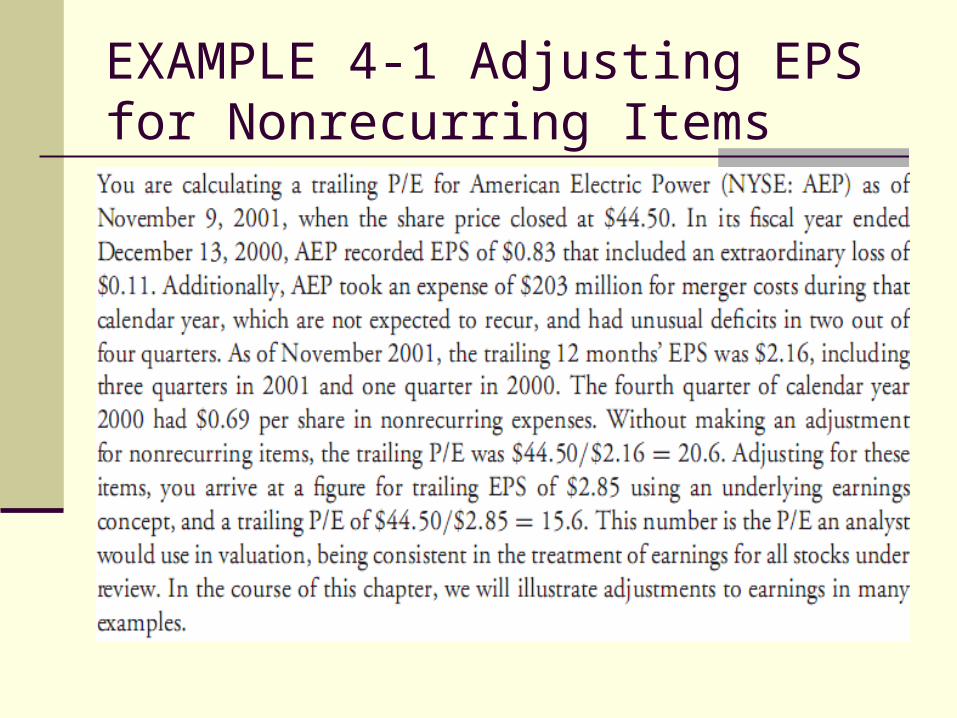

EXAMPLE 4-1 Adjusting EPS for Nonrecurring Items

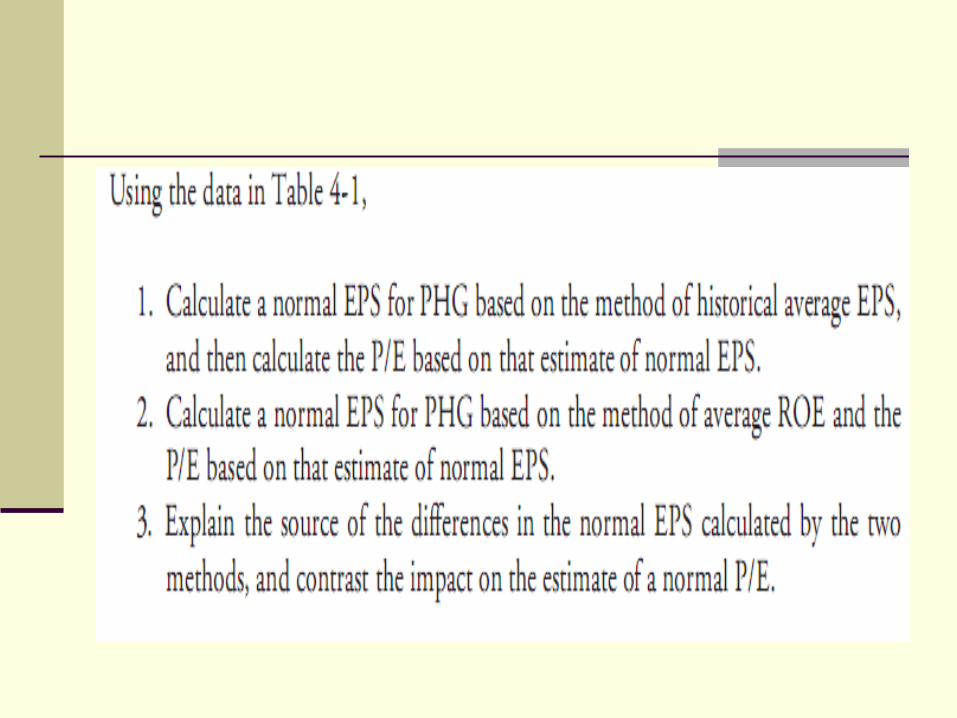

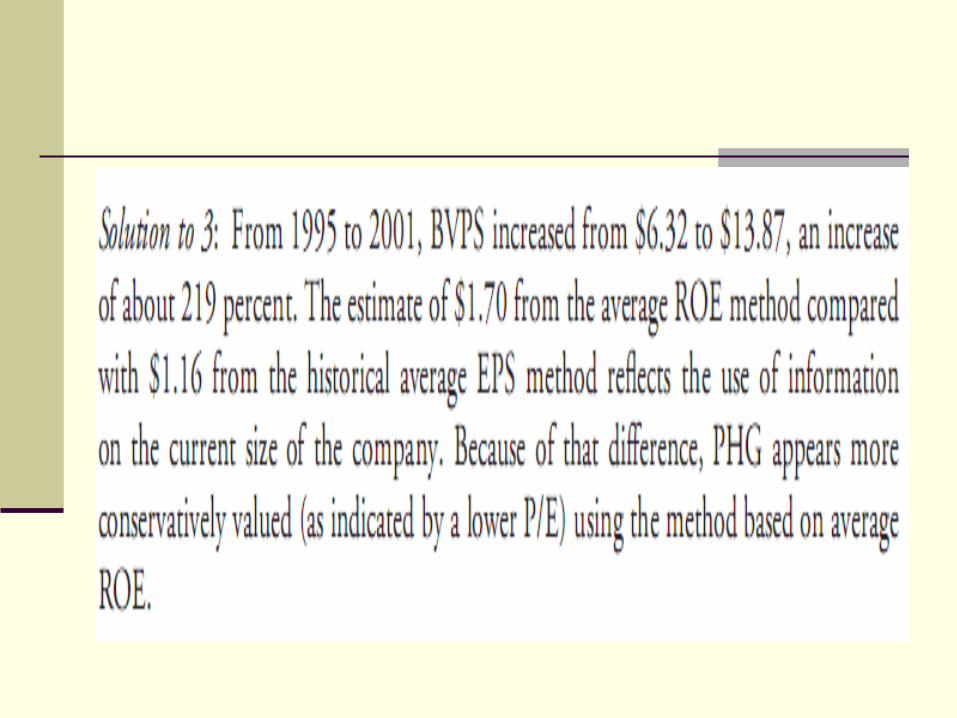

Two methods to normalize EPS:

1. Method of historical average EPS (over the most recent full cycle)

2. Method of average ROE (average ROE multiplied by current book value per share).

Earnings yield (E/P) is the reciprocal of the P/E. When stocks have negative EPS, a ranking by earnings yield is meaningful whereas a ranking by P/E is not.

EXAMPLE 4-2 Normalizing EPS for Business-Cycle Effects

EXAMPLE 4-5 Calculating a Leading P/E Ratio (1)

EXAMPLE 4-6 Calculating a Leading P/E Ratio (2)

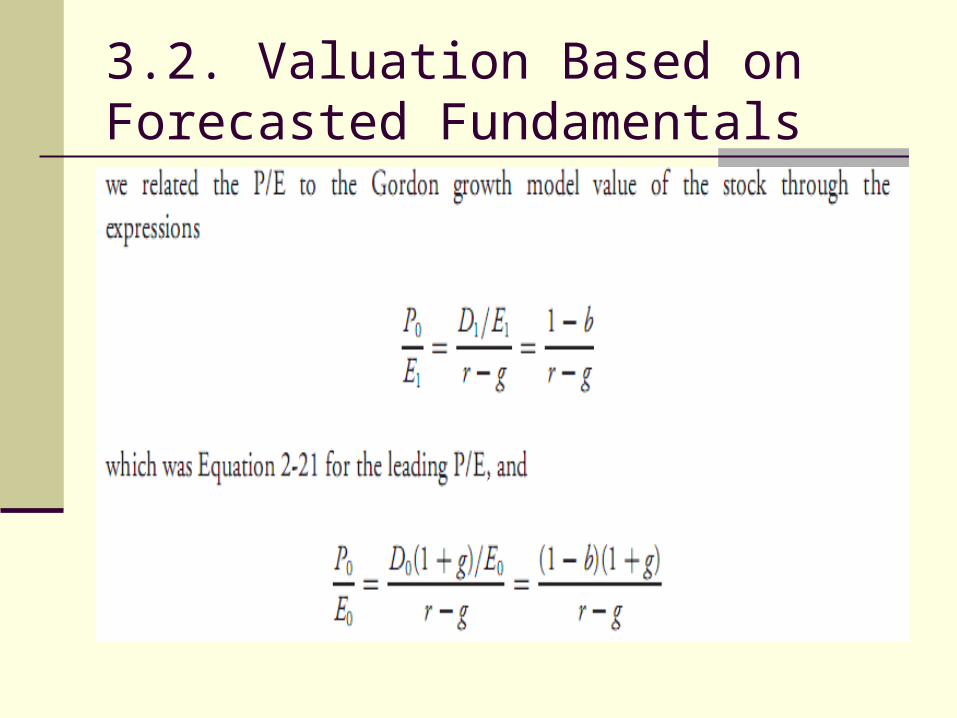

3.2. Valuation Based on Forecasted Fundamentals

EXAMPLE 4-7 Leading P/E Based onFundamental Forecasts (1)

EXAMPLE 4-8 Leading P/E Based onFundamental Forecasts (2)

3.3. Valuation Using Comparables

The most common application of the P/E approach to valuation is to compare a stock’s price multiple with a benchmark value of the multiple.

EXAMPLE 4-10 A Simple Peer Group Comparison

EXAMPLE 4-11 A Peer Group Comparison Modified by Fundamentals

EXAMPLE 4-12 Relative Industry Valuation

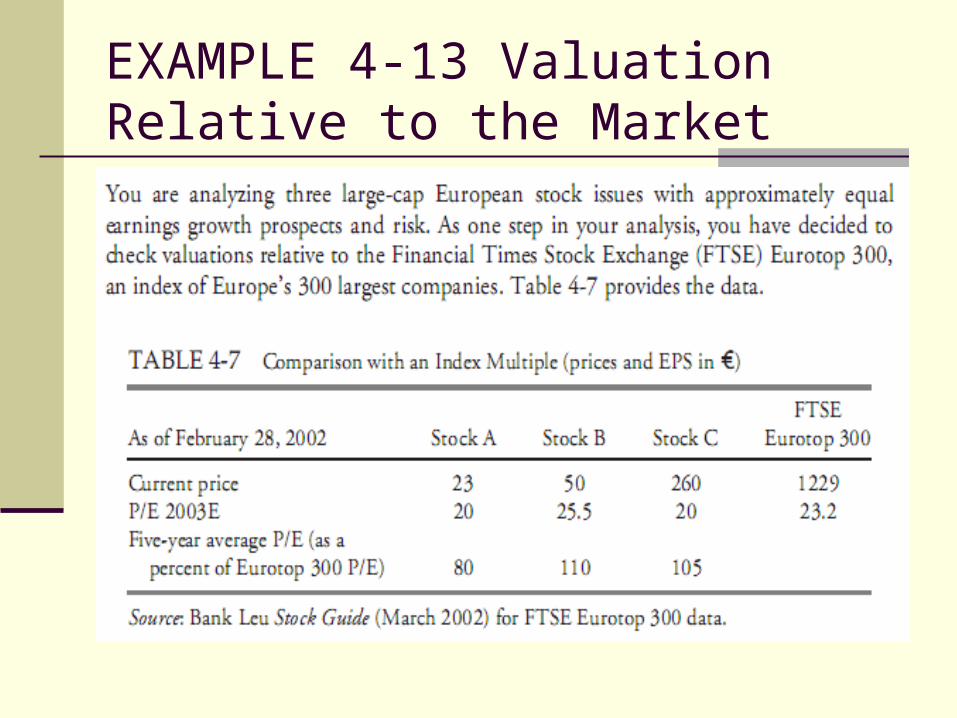

EXAMPLE 4-13 Valuation Relative to the Market

EXAMPLE 4-16 Valuation Relative to Own Historical P/Es

3.3.5. Using P/Es to Obtain Terminal Value in Multistage Dividend Discount Models

EXAMPLE 4-17 Valuing the Mature Growth Phase Using P/Es

As an energy analyst, you are valuing the stock of an oil exploration company. You have projected earnings and dividends three years out (to t = 3), and you have gathered the following data and estimates:

4. PRICE TO BOOK VALUE

Book value per share attempts to represent the investment that common shareholders have made in the company, on a per-share basis. Inflation, technological change, and accounting distortions, however, can impair book value for this purpose.

Book value is calculated as common shareholders’ equity divided by the number of shares outstanding. Analysts adjust book value to more accurately reflect the value of shareholders’ investment and to make P/B more useful for comparing different stocks.

The fundamental drivers of P/B are ROE and the required rate of return. The justified P/B based on fundamentals bears a positive relationship to the first factor and an inverse relationship to the second factor.

EXAMPLE 4-19 Computing Book Value per Share

4.2. Valuation Based on Forecasted Fundamentals

For example, if a business’s ROE is 12 percent, its required rate of return is 10 percent,and its expected growth rate is 7 percent, then its justified P/B based on fundamentals is(0.12 − 0.07)/(0.10 − 0.07) = 1.7.

5. PRICE TO SALES

An important rationale for the price-to-sales ratio (P/S) is that sales, as the top line in an income statement, are generally less subject to distortion or manipulation than other fundamentals such as EPS or book value. Sales are also more stable than earnings and never negative.

P/S fails to take into account differences in cost structure between businesses, may not properly reflect the situation of companies losing money, and can be subject to manipulation through revenue recognition practices.

The fundamental drivers of P/S are profit margin, growth rate, and the required rate of return. The justified P/S based on fundamentals bears a positive relationship to the first two factors and an inverse relationship to the third factor.

EXAMPLE 4-22 Calculating P/S

5.2. Valuation Based on Forecasted Fundamentals

EXAMPLE 4-25 Justified P/S Based on Forecasted Fundamentals

6. PRICE TO CASH FLOW

EXAMPLE 4-28 Calculating Earnings-Plus-Noncash Charges (CF)

EXAMPLE 4-30 Justified Price to Cash Flow Based on Forecasted Fundamentals

8. DIVIDEND YIELD

EXAMPLE 4-33 Calculating Dividend Yield

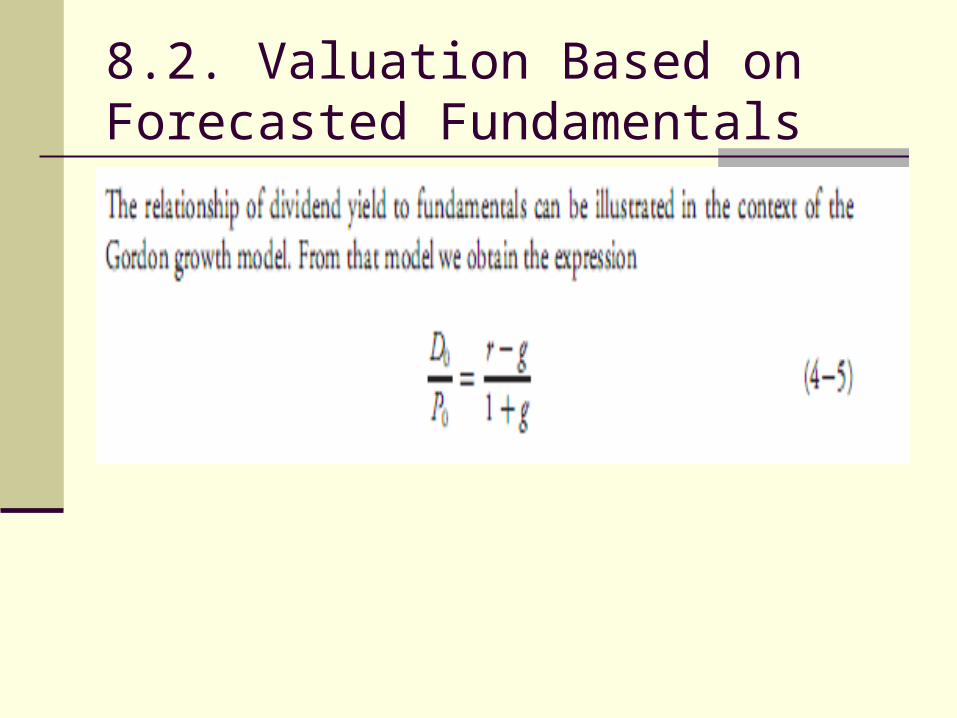

8.2. Valuation Based on Forecasted Fundamentals