china tax & investment news - ernst & youngfile/ey... · china tax & investment news 1...

TRANSCRIPT

China Tax & Investment News 1

23 approvals on tax matters are nowremoved – yet, not sure if it is good news

Issue No.CTIN201500525 May 2015

Introduction

In order to remove all of the approvals on non-administrative licensing matters (“非行政许可审批”, hereinafter referred to as “the Approvals”), on 10 May 2015, theState Council released Guofa [2015] No. 27 (hereinafter referred to as “Circular27”) to further clean-up 133 items that were subject to the Approval, among those,49 were eliminated and 84 were treated as government internal matters andshould be subject to internal approval procedures(政府内部审批)1 .

Under Circular 27, the Approval in relation to 23 tax relevant items is eliminated,i.e., the approvals are no longer required for taxpayers who involved in suchmatters. These matters include certain important applications like tax treatybenefits, special tax treatments for corporate restructuring, etc. This issue ofChina Tax and Investment News is to discuss tax matters related to Circular 27 ingreater detail.

China Tax &Investment News

Note:

1. China administrative approval system involves administrative licensing matters, internal approvaland other approvals. Circular 27 aims to clean up all approvals in relation to non-administrativelicensing matters.

China Tax & Investment News 2

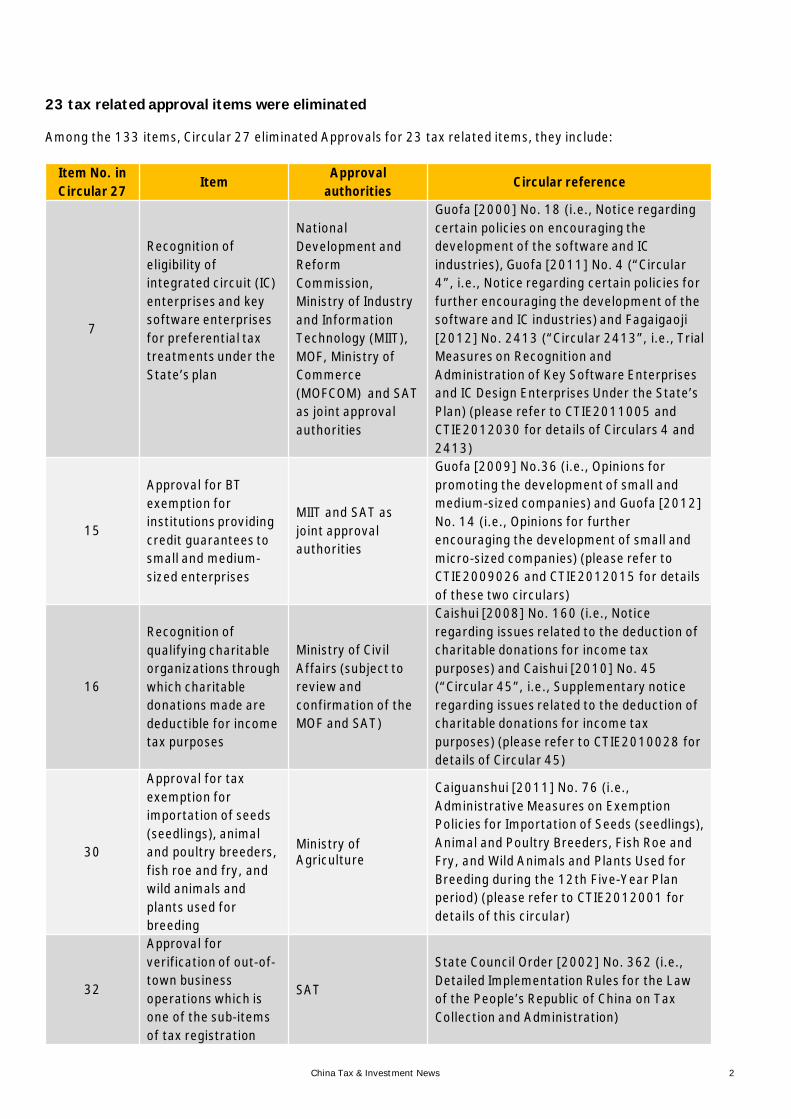

23 tax related approval items were eliminated

Among the 133 items, Circular 27 eliminated Approvals for 23 tax related items, they include:

Item No. inCircular 27

ItemApproval

authoritiesCircular reference

7

Recognition ofeligibility ofintegrated circuit (IC)enterprises and keysoftware enterprisesfor preferential taxtreatments under theState’s plan

NationalDevelopment andReformCommission,Ministry of Industryand InformationTechnology (MIIT),MOF, Ministry ofCommerce(MOFCOM) and SATas joint approvalauthorities

Guofa [2000] No. 18 (i.e., Notice regardingcertain policies on encouraging thedevelopment of the software and ICindustries), Guofa [2011] No. 4 (“Circular4”, i.e., Notice regarding certain policies forfurther encouraging the development of thesoftware and IC industries) and Fagaigaoji[2012] No. 2413 (“Circular 2413”, i.e., TrialMeasures on Recognition andAdministration of Key Software Enterprisesand IC Design Enterprises Under the State’sPlan) (please refer to CTIE2011005 andCTIE2012030 for details of Circulars 4 and2413)

15

Approval for BTexemption forinstitutions providingcredit guarantees tosmall and medium-sized enterprises

MIIT and SAT asjoint approvalauthorities

Guofa [2009] No.36 (i.e., Opinions forpromoting the development of small andmedium-sized companies) and Guofa [2012]No. 14 (i.e., Opinions for furtherencouraging the development of small andmicro-sized companies) (please refer toCTIE2009026 and CTIE2012015 for detailsof these two circulars)

16

Recognition ofqualifying charitableorganizations throughwhich charitabledonations made aredeductible for incometax purposes

Ministry of CivilAffairs (subject toreview andconfirmation of theMOF and SAT)

Caishui [2008] No. 160 (i.e., Noticeregarding issues related to the deduction ofcharitable donations for income taxpurposes) and Caishui [2010] No. 45(“Circular 45”, i.e., Supplementary noticeregarding issues related to the deduction ofcharitable donations for income taxpurposes) (please refer to CTIE2010028 fordetails of Circular 45)

30

Approval for taxexemption forimportation of seeds(seedlings), animaland poultry breeders,fish roe and fry, andwild animals andplants used forbreeding

Ministry ofAgriculture

Caiguanshui [2011] No. 76 (i.e.,Administrative Measures on ExemptionPolicies for Importation of Seeds (seedlings),Animal and Poultry Breeders, Fish Roe andFry, and Wild Animals and Plants Used forBreeding during the 12th Five-Year Planperiod) (please refer to CTIE2012001 fordetails of this circular)

32

Approval forverification of out-of-town businessoperations which isone of the sub-itemsof tax registration

SAT

State Council Order [2002] No. 362 (i.e.,Detailed Implementation Rules for the Lawof the People’s Republic of China on TaxCollection and Administration)

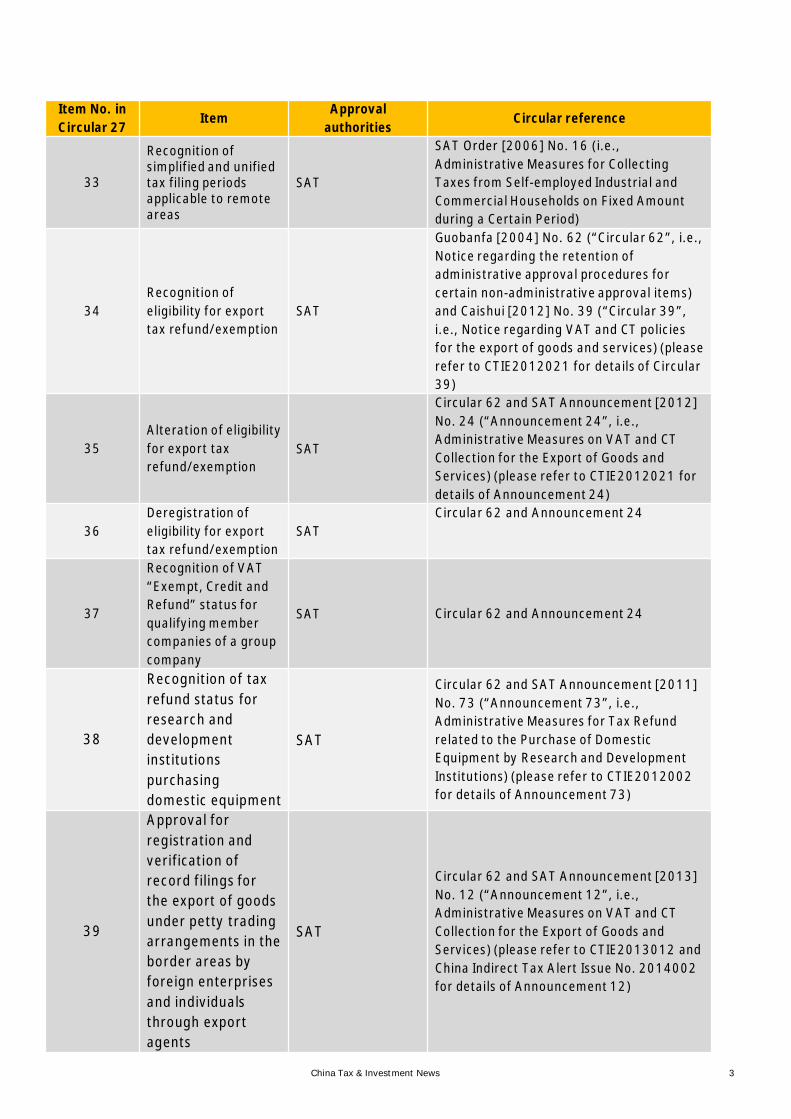

China Tax & Investment News 3

Item No. inCircular 27

ItemApproval

authoritiesCircular reference

33

Recognition ofsimplified and unifiedtax filing periodsapplicable to remoteareas

SAT

SAT Order [2006] No. 16 (i.e.,Administrative Measures for CollectingTaxes from Self-employed Industrial andCommercial Households on Fixed Amountduring a Certain Period)

34Recognition ofeligibility for exporttax refund/exemption

SAT

Guobanfa [2004] No. 62 (“Circular 62”, i.e.,Notice regarding the retention ofadministrative approval procedures forcertain non-administrative approval items)and Caishui [2012] No. 39 (“Circular 39”,i.e., Notice regarding VAT and CT policiesfor the export of goods and services) (pleaserefer to CTIE2012021 for details of Circular39)

35Alteration of eligibilityfor export taxrefund/exemption

SAT

Circular 62 and SAT Announcement [2012]No. 24 (“Announcement 24”, i.e.,Administrative Measures on VAT and CTCollection for the Export of Goods andServices) (please refer to CTIE2012021 fordetails of Announcement 24)

36Deregistration ofeligibility for exporttax refund/exemption

SATCircular 62 and Announcement 24

37

Recognition of VAT“Exempt, Credit andRefund” status forqualifying membercompanies of a groupcompany

SAT Circular 62 and Announcement 24

38

Recognition of taxrefund status forresearch anddevelopmentinstitutionspurchasingdomestic equipment

SAT

Circular 62 and SAT Announcement [2011]No. 73 (“Announcement 73”, i.e.,Administrative Measures for Tax Refundrelated to the Purchase of DomesticEquipment by Research and DevelopmentInstitutions) (please refer to CTIE2012002for details of Announcement 73)

39

Approval forregistration andverification ofrecord filings forthe export of goodsunder petty tradingarrangements in theborder areas byforeign enterprisesand individualsthrough exportagents

SAT

Circular 62 and SAT Announcement [2013]No. 12 (“Announcement 12”, i.e.,Administrative Measures on VAT and CTCollection for the Export of Goods andServices) (please refer to CTIE2013012 andChina Indirect Tax Alert Issue No. 2014002for details of Announcement 12)

China Tax & Investment News 4

Item No. inCircular 27

ItemApproval

authoritiesCircular reference

40

Approval for includingvehicles in thecatalogue whichintroduces vehicleseligible for VehiclePurchase Tax (VPT)exemption

SAT

SAT Order [2014] No. 33 (“Order 33”, i.e.,Measures for VPT Collection andAdministration) (please refer toCTIE2014050 for details of Order 33)

41

Approval for VPTexemption on non-transport vehicleswith fixed devices

SAT Order 33

42Approval for VPTexemption for busesand electric buses

SAT

Guoshuifa [2012] No. 61 (i.e., Noticeregarding several issues related to the VPTexemption for buses and electric busespurchased by urban public transportcompanies)

43

Approval forrecognition,alteration andtermination ofdesignated shops inHainan whereforeign tourists canpurchase goodseligible for taxrefunds

SAT and theCommerceAuthority of Hainanprovince as jointapproval authorities

SAT Announcement [2010] No. 28 (i.e.,Administrative Measures for the Pilot Run ofTax Refunds on Goods Purchased by ForeignTourists in Hainan)

44

Recognition of taxrefund status forenterprises engagingin the production ofethylene and aromatichydrocarbons

SAT

SAT Announcement [2012] No. 36 (i.e.,Provisional Measures for CTRefund/exemption on Naphtha and Fuel OilsUsed for the Production of Ethylene andAromatic Hydrocarbons)

45Approval for non-residents’ eligibilityfor tax treaty benefits

SAT

Circular 62 and Guoshuifa [2009] No. 124(“Circular 124”, i.e., AdministrativeMeasures for Non-residents Enjoying TreatyBenefits (Trial)) (please refer toCTIE2009023 and International Tax andTransaction Tax Bulletin Issue No. 2009002for details of Circular 124)

46

Examination andapproval for whetherthe cost allocationagreements ofenterprises are basedon the arm’s lengthprinciple

SAT

Guoshuifa [2009] No. 2 (i.e.,Implementation Measures for Special TaxAdjustments (Trial)) (please refer toTransfer Pricing Tax Alert Issue Nos.2009001, 2009002 and 2009003)

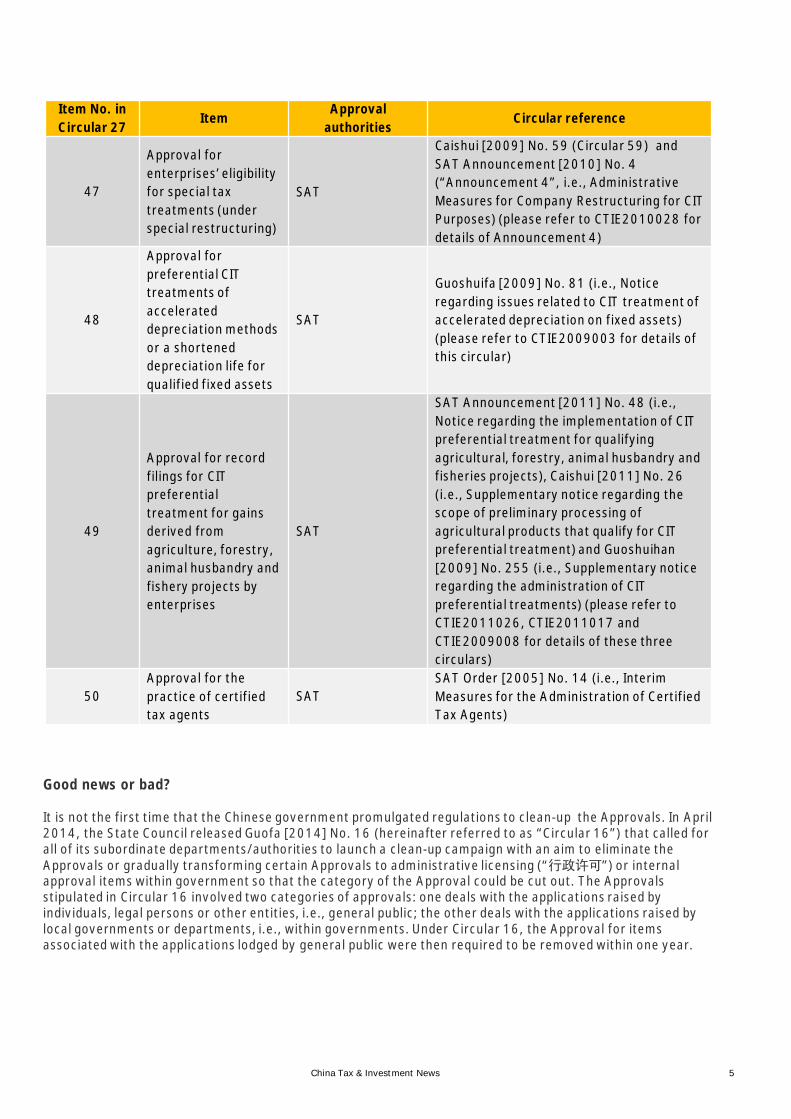

China Tax & Investment News 5

Item No. inCircular 27

ItemApproval

authoritiesCircular reference

47

Approval forenterprises’ eligibilityfor special taxtreatments (underspecial restructuring)

SAT

Caishui [2009] No. 59 (Circular 59) andSAT Announcement [2010] No. 4(“Announcement 4”, i.e., AdministrativeMeasures for Company Restructuring for CITPurposes) (please refer to CTIE2010028 fordetails of Announcement 4)

48

Approval forpreferential CITtreatments ofaccelerateddepreciation methodsor a shorteneddepreciation life forqualified fixed assets

SAT

Guoshuifa [2009] No. 81 (i.e., Noticeregarding issues related to CIT treatment ofaccelerated depreciation on fixed assets)(please refer to CTIE2009003 for details ofthis circular)

49

Approval for recordfilings for CITpreferentialtreatment for gainsderived fromagriculture, forestry,animal husbandry andfishery projects byenterprises

SAT

SAT Announcement [2011] No. 48 (i.e.,Notice regarding the implementation of CITpreferential treatment for qualifyingagricultural, forestry, animal husbandry andfisheries projects), Caishui [2011] No. 26(i.e., Supplementary notice regarding thescope of preliminary processing ofagricultural products that qualify for CITpreferential treatment) and Guoshuihan[2009] No. 255 (i.e., Supplementary noticeregarding the administration of CITpreferential treatments) (please refer toCTIE2011026, CTIE2011017 andCTIE2009008 for details of these threecirculars)

50Approval for thepractice of certifiedtax agents

SATSAT Order [2005] No. 14 (i.e., InterimMeasures for the Administration of CertifiedTax Agents)

Good news or bad?

It is not the first time that the Chinese government promulgated regulations to clean-up the Approvals. In April2014, the State Council released Guofa [2014] No. 16 (hereinafter referred to as “Circular 16”) that called forall of its subordinate departments/authorities to launch a clean-up campaign with an aim to eliminate theApprovals or gradually transforming certain Approvals to administrative licensing (“行政许可”) or internalapproval items within government so that the category of the Approval could be cut out. The Approvalsstipulated in Circular 16 involved two categories of approvals: one deals with the applications raised byindividuals, legal persons or other entities, i.e., general public; the other deals with the applications raised bylocal governments or departments, i.e., within governments. Under Circular 16, the Approval for itemsassociated with the applications lodged by general public were then required to be removed within one year.

China Tax & Investment News 6

In response to Circular 16, Circular 27 removed a list of the Approvals and changed the way how certain itemsapproved, i.e., adopting internal approval process while the applicants are governments or authoritiesthemselves. It may reflect the Chinese government’s intention to improve administrative efficiency and restrictdiscretionary power for certain government authorities. Obviously, the Chinese government has removed mostof approvals on non-administrative licensing matters already and may eventually eliminate this category ofapproval.

All tax related items under Circular 27 fall under the scope of removal. Such removals include the approval inrelation to tax treaty benefits of non-residents, qualifying special tax treatment for corporate restructuring,certain tax preferential treatments under current Corporate Income Tax (CIT) regime, etc.. Although it looks likesimplification of process, it is indeed hard to conclude that the move is good. The removal of approvals for theprescribed tax matters may not mean that the relevant tax matters no longer require verifications; furtherregulations may come into place to clarify the administration going forward. In the absence of new procedures,taxpayers could be taking risk when formal approvals or confirmations from tax authorities are not available; itwill be particularly challenging on judgmental matters like whether one qualifies for treaty benefits or whether arestructuring qualifies for special tax treatments. Before the promulgation of Circular 27, taxpayers could gaincertainty through formal filing/applications.

According to Circular 59, enterprises qualifying for and choosing special tax treatment shall perform filing-for-record (“备案”) to demonstrate their eligibility. The subsequent Announcement 4 stated that enterprises canobtain the confirmation from tax authorities if they consider necessary. Circular 27 only serves as a generalguideline; it does not clarify detailed administration process going forward, such as whether filing-for-record isrequired or any other procedures shall be followed. In this case, with the Approval being removed by Circular27, written confirmation from tax authorities to secure the special tax treatment could become remote; yet,taxpayers would need to collect sufficient evidence to prove their compliance.

Non-residents claiming tax treaty benefits in relation to dividends, interests, royalties and capital gains could beanother challenging area. Circular 124 was the circular formulating procedures for tax treaty benefitsapplications; with the enforcement of Circular 27, formal approval is no longer required. Nevertheless, it maynot be unreasonable to infer that filing-for-record may become the process for claiming treaty benefits givenanti-avoidance is still on the top of the agenda of tax authorities. This can be evidenced by the recentShuizongfa [2015] No. 60 which aims to create friendly environment supporting the national strategy of “OneBelt One Road”, a direction to shift approvals to filing-for–record process in relation to treaty benefit claims wasmentioned.

Similar examples also include the recognition of qualified software and IC enterprises, other tax preferentialtreatments under current CIT regime, etc.. Without formal verification and confirmation, taxpayers have toassume the primary responsibility to prove their eligibility, or else significant tax risk can arise.

What else is uncertain?

Similar to previous regulations announced by the State Council, Circular 27 only laid down guiding principles,leaving room for government authorities to further interpret. Circular 27 could give rise to significantuncertainties on tax positions that may better be supported by formal approvals. As a normal practice,following the promulgation of the State Council’s instruction, government authorities may publish further rulesthat are usually more detailed and specific, taxpayers should therefore watch out for any further developmentseither at the state or local levels. With that, it is not easy to predict whether more lenient or stringentadministration would be introduced or more discretion powers are left to in-charge tax authorities at local levels.

In addition, a list of items subject to approval was announced by the SAT in its announcement [2014] No. 10(Circular 10) released in February 2014. The list contained items subject to either administrative licensing orthe Approval. In view of the determination of Chinese government in regard to elimination of all the Approvals,it is rather uncertain on whether those subject to the Approvals under Circular 10 but not included in theCircular 27 list shall also be cancelled, or they will be transformed to other administrative measures; such as theapproval of overseas-registered China residents, tax preferential treatment in western areas and preferentialtreatment for technology transfer, etc.. Taxpayers should watch out on any development in these areas as well.

China Tax & Investment News 7

Conclusion

Circular 27 appears to relax the administration for 23 tax matters, which however does not mean tax authoritieswill neglect supervision over these matters. Instead, it could mean the focus of tax administration is now shiftedto post-transaction inspections; which is in line with many other countries’ practices that the proof of taxcompliance always rest with taxpayers and they have to take the consequence on non-compliance. That is to say,tax authorities will assume their administrative function on tax matters through routine administrationmeasures or more frequent and thorough tax inspections.

Enterprises are recommended to proactively communicate with the respective government authorities or taxpractitioners with regards to matters stipulated in Circular 27 to understand the changes that may now be putin place. As mentioned, subsequent rules may be further announced, taxpayers should stay tuned on anydevelopment to ensure compliance. We shall keep you posted.

China Tax & Investment News 8

Contact usFor more information, please contact your usual Ernst & Young contact or one of the following of Ernst & Young’s China taxleaders.

► Walter Tong+86 21 2228 [email protected]

► Henry Chan (Beijing)+86 10 5815 [email protected]

► Alan Lan (Tianjin)+86 10 5815 [email protected]

Office Tax Leaders

► Samuel Yan (Dalian)+86 10 5815 [email protected]

Service Line Tax Leaders

► Andrew Choy (International Tax andTransfer Pricing)+86 10 5815 [email protected]

► Becky Lai (Tax policy)+852 2629 [email protected]

► David Chan (Transaction Tax)+852 2629 [email protected]

► Paul Wen (Human Capital)+852 2629 [email protected]

► Jane Hui+852 2629 [email protected]

Author – China Tax Center

Greater China Tax Leader

► Andy Chen (Qingdao)+86 10 5815 [email protected]

► Vickie Tan (Shanghai / Wuhan)+86 21 2228 [email protected]

► Audrie Xia (Suzhou)+86 21 2228 [email protected]

► Patricia Xia (Hangzhou)+86 21 2228 [email protected]

► Chuan Shi (Chengdu)+86 21 2228 [email protected]

► Rio Chan (Guangzhou / Xiamen)+86 20 2881 [email protected]

► Lawrence Cheung (Shenzhen)+86 755 2502 [email protected]

► Clement Yuen (China South)+86 755 2502 [email protected]

China Tax & Investment News 8

► Robert Smith (Indirect Tax)+86 21 2228 [email protected]

China Tax & Investment News 9

About EYEY is a global leader in assurance, tax, transaction and advisoryservices. The insights and quality services we deliver help build trustand confidence in the capital markets and in economies the worldover. We develop outstanding leaders who team to deliver on ourpromises to all of our stakeholders. In so doing, we play a criticalrole in building a better working world for our people, for our clientsand for our communities.

EY refers to the global organization and may refer to one or more ofthe member firms of Ernst & Young Global Limited, each of which isa separate legal entity. Ernst & Young Global Limited, a UK companylimited by guarantee, does not provide services to clients. For moreinformation about our organization, please visit ey.com.

© 2015 Ernst & Young (China) Advisory LimitedAll Rights Reserved.

APAC no. 03001959ED None.

This material has been prepared for general informational purposes only andis not intended to be relied upon as accounting, tax, or other professionaladvice. Please refer to your advisors for specific advice.

ey.com/china

EY | Assurance | Tax | Transactions | Advisory